United Kingdom Enterprise Content Management (ECM) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

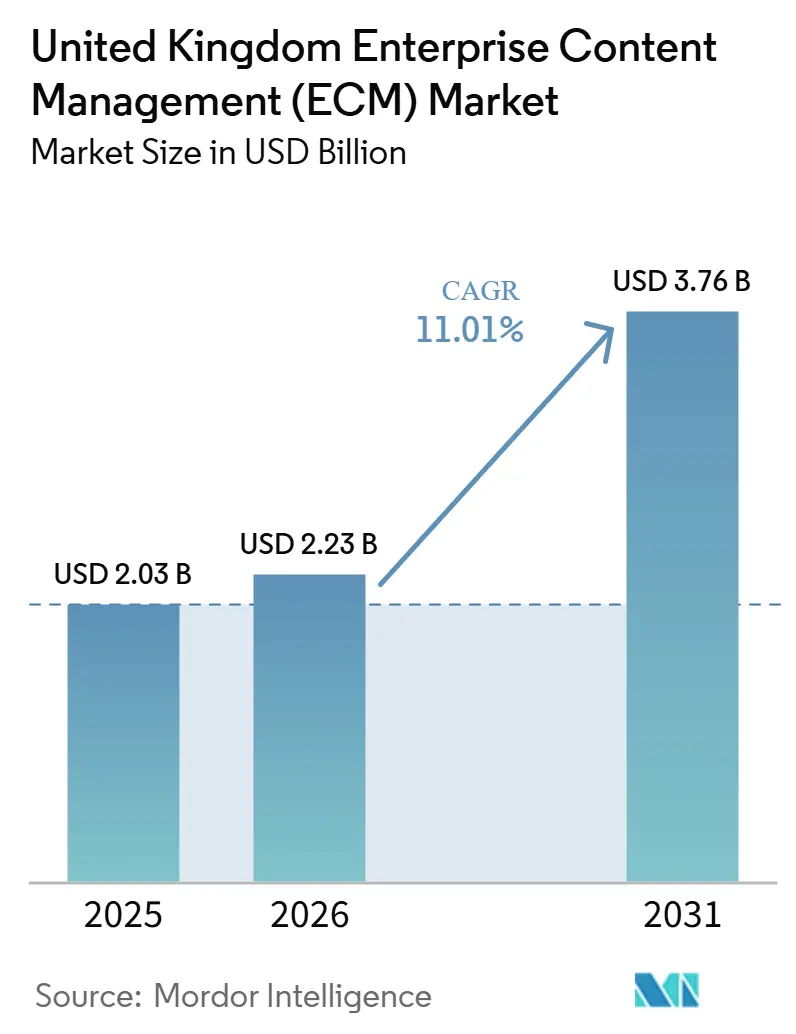

| Base Year Market Size (2025) | USD 2.03 Billion |

| Market Size (2026) | USD 2.23 Billion |

| Market Size (2031) | USD 3.76 Billion |

| Growth Rate (2026 - 2031) | 11.01% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Enterprise Content Management (ECM) Market Analysis by Mordor Intelligence

The United Kingdom enterprise content management (ECM) market size was valued at USD 2.03 billion in 2025 and USD 2.23 billion in 2026, and is forecast to reach USD 3.76 billion by 2031, growing at an 11.01% CAGR during 2026-2031. The United Kingdom enterprise content management (ECM) market is expanding because enterprises now treat content governance as a core operating need rather than a back-office software decision. Demand is rising as firms seek to consolidate documents, records, approvals, and archived files into a single, controlled environment across cloud, hybrid, and legacy systems. Tighter expectations around audit trails, retention, privacy, and internal accountability are also pushing boards and operating teams to formalize how business content is stored and retrieved. The United Kingdom enterprise content management (ECM) market is also benefiting from AI-led workflow changes, as automated classification, search, and document handling shorten processing time and strengthen the value proposition for new deployments. Competitive conditions remain active because large platform vendors still lead enterprise accounts, while narrower specialists are gaining traction where buyers want quicker implementation, stronger vertical fit, or better sovereign deployment options.

Key Report Takeaways

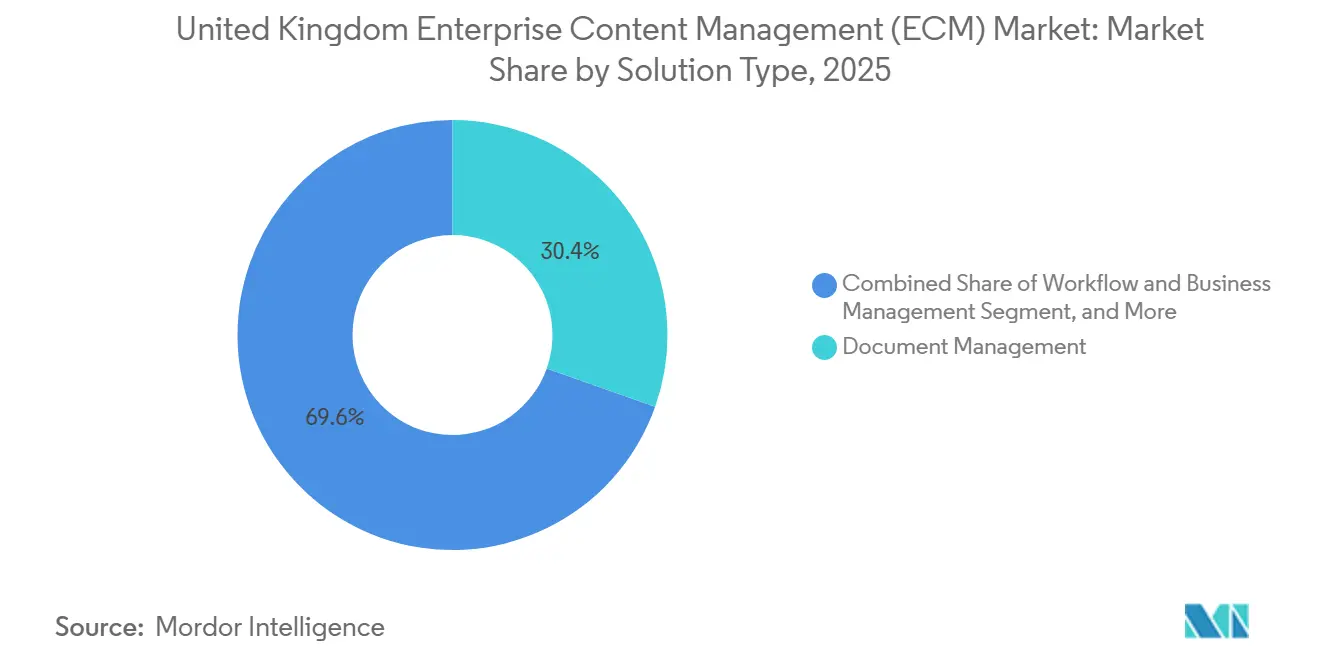

- By solution type, Document Management led with 30.42% revenue share in the United Kingdom enterprise content management (ECM) market in 2025, while Workflow and Business Process Management is forecast to expand at a 13.61% CAGR through 2031.

- By deployment mode, Cloud held 77.18% of the United Kingdom enterprise content management (ECM) market in 2025, while the cloud segment is also projected to record the highest CAGR of 14.03% through 2031.

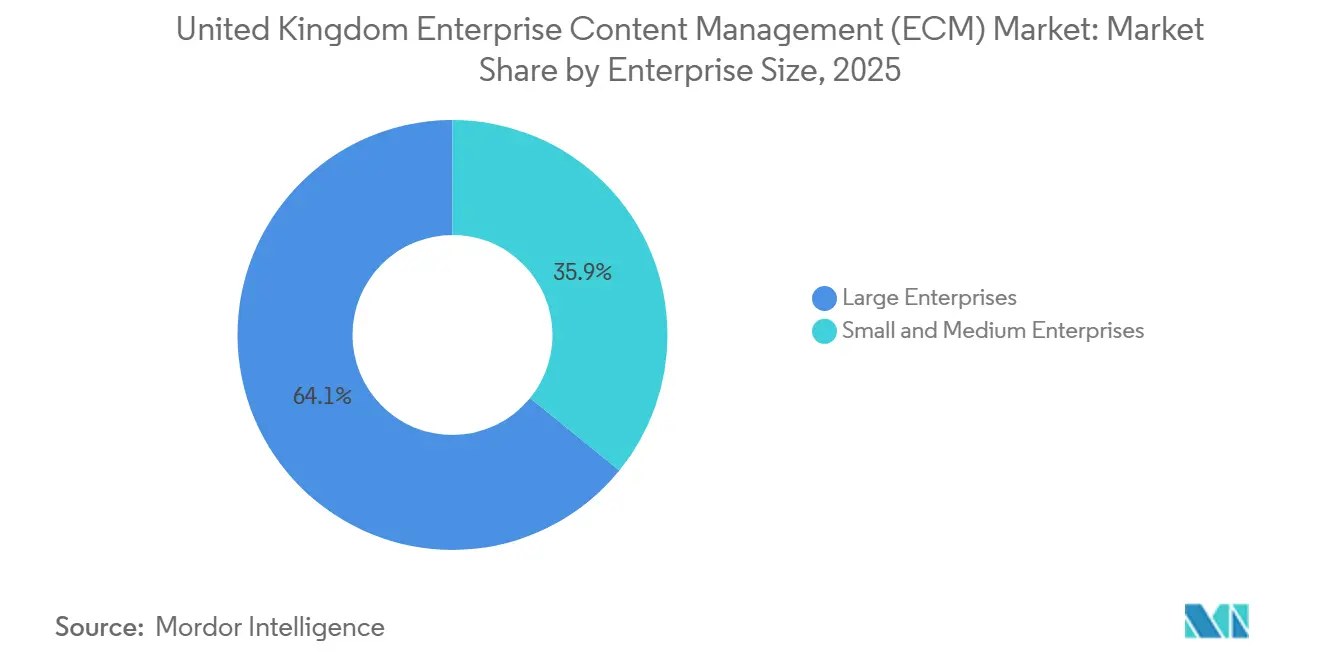

- By enterprise size, Large Enterprises held 64.14% of the market in 2025, while SMEs are projected to grow at a 13.28% CAGR through 2031.

- By end-user industry, BFSI accounted for 24.86% of revenue in 2025, while Healthcare is projected to grow at a 13.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Enterprise Content Management (ECM) Market Trends and Insights

Drivers Impact Analysis*

| river | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Digital Transformation Across UK Enterprises | +2.5% | National, concentrated demand in London, South East, and Edinburgh | Short term (≤ 2 years) |

| Compliance-Driven Content Governance and Auditability | +2.2% | National, with strong relevance in regulated sectors and public institutions | Short term (≤ 2 years) |

| AI-Based Content Classification and Search Accuracy Gains | +1.9% | National, led by financial services, legal, and professional services hubs | Medium term (2-4 years) |

| Cloud Migration of Legacy Document Repositories | +1.6% | National, with adoption gaps in Northern England, Wales, and the public sector | Medium term (2-4 years) |

| Hybrid Workforces Requiring Secure Content Access | +1.1% | National, strongest in knowledge-intensive sectors | Short term (≤ 2 years) |

| Sector-Specific Modernization in BFSI, Healthcare, and Government | +0.8% | National, concentrated in London, Manchester, and Edinburgh | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Digital Transformation Across UK Enterprises

The United Kingdom enterprise content management (ECM) market is gaining from a wider shift in business digitization, but many organizations still operate with uneven content practices across departments. A large share of firms already use cloud tools, yet enterprise-wide standardization of content flows, approval chains, and record handling remains incomplete, leaving room for deeper platform adoption. This gap matters because storing files in digital systems is not the same as governing them through searchable, policy-based repositories and connected workflows. The United Kingdom enterprise content management (ECM) market therefore benefits as transformation programs move from basic software rollout to process redesign, information control, and automation. Public sector modernization efforts are also reinforcing this direction by keeping document infrastructure, digital records, and service delivery systems on national procurement agendas.[1]UK Government, “UK Business Data Survey 2026,” GOV.UK, gov.uk

Compliance-Driven Content Governance and Auditability

Regulatory pressure is making controlled document handling a day-to-day operating requirement across the United Kingdom enterprise content management (ECM) market. Financial services firms, government bodies, healthcare providers, and other regulated organizations all need stronger retention logic, clearer version control, and better proof of who accessed or changed a file. This is shifting purchase priorities toward platforms that support audit trails, record retention policies, defensible deletion, and secure retrieval without extensive customization. Buyers are also putting more weight on systems that can support AI use without weakening documentation standards or internal governance. In the United Kingdom enterprise content management (ECM) market, this keeps compliance-linked demand resilient even when broader technology budgets face scrutiny.

AI-Based Content Classification and Search Accuracy Gains

AI features are changing how buyers assess the United Kingdom enterprise content management (ECM) market, as content systems are now expected to do more than just store files. Enterprises increasingly want tools that can classify documents, enrich metadata, improve search quality, and reduce the time employees spend locating the right information. These gains are especially relevant in document-heavy environments such as legal work, claims administration, compliance review, and case handling. Early adopters also build cleaner metadata structures, which lowers future effort for workflow automation and later AI deployment. Microsoft's workarounds for SharePoint Embedded and Copilot-linked content experiences show how established platforms are pushing document environments toward AI-ready infrastructure.[2]UK Government, “Better Patient Care as NHS Set to Introduce Single Patient Record,” GOV.UK, gov.uk

Cloud Migration of Legacy Document Repositories

The United Kingdom enterprise content management (ECM) market continues to benefit from the slow replacement of older file servers, departmental archives, and basic document stores. Many organizations still keep important content in systems that were not built for modern search, retention control, or integration with workflow tools. Migration is creating work for vendors that can map metadata, preserve permissions, and move records into cloud or hybrid repositories without disrupting operations. This is especially relevant in mid-sized organizations and public bodies that adopted basic document tools years ago and now need stronger governance and better flexibility. Government survey data still shows a mixed infrastructure base, with public cloud, private cloud, and on-premises systems all in active use, which confirms that the migration cycle remains open.[3]Microsoft, “SharePoint Showcase: Using SharePoint Embedded to Create AI-Ready Infrastructure,” Microsoft Community Hub, techcommunity.microsoft.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration Complexity with Legacy Line-of-Business Systems | -1.5% | National, most acute in public sector and legacy BFSI institutions | Short term (≤ 2 years) |

| Data Residency and Sovereignty Constraints for Sensitive Content | -1.2% | National, especially in sovereign, defense, and public sector environments | Medium term (2-4 years) |

| High Cost of Migration, Metadata Cleanup, and Change Management | -0.9% | National, most acute for SMEs and public bodies | Medium term (2-4 years) |

| Skills Shortage in ECM, Information Governance, and Automation | -0.7% | National, with wider gaps outside the main digital hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Integration Complexity with Legacy Line-of-Business Systems

Integration remains one of the clearest limits on how quickly the United Kingdom enterprise content management (ECM) market can scale across older enterprise estates. Large banks, insurers, and public institutions often run policy, claims, benefits, finance, or case systems that were built before current API standards became common. That makes document connectivity slower, more service-intensive, and more expensive than software buyers first expect. Even where vendors offer prebuilt connectors, teams still need to align fields, reconcile inconsistent metadata, and test access rules across multiple repositories. This means many large deployments in the United Kingdom enterprise content management (ECM) market still behave like multi-stage transformation programs rather than simple software implementations.

Data Residency and Sovereignty Constraints for Sensitive Content

Data location rules are another brake on the United Kingdom enterprise content management (ECM) market, especially for public sector, defense, healthcare, and sensitive financial use cases. Organizations handling citizen, patient, or high-value internal records often cannot move content freely into standard shared cloud environments. This pushes buyers toward hybrid models, sovereign cloud options, or private infrastructure that takes longer to approve and costs more to operate. The Government's Technology Adoption Review 2025 also identified data sovereignty as a structural barrier that can raise the cost of cloud adoption in sensitive settings. OpenText's sovereign cloud partnership with S3NS shows that vendors are responding, but these architectures still add friction compared with standard cloud rollouts.[4]UK Government, “Technology Adoption Review 2025,” Department for Science, Innovation and Technology, gov.uk

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Document Management Leads as Workflow Automation Accelerates

Document Management held 30.42% of the United Kingdom enterprise content management (ECM) market share in 2025, making it the largest solution category in the portfolio. This lead reflects the steady need to digitize, index, store, and retrieve business-critical records in regulated environments. Banks, legal firms, public institutions, and healthcare providers all manage high volumes of contracts, forms, case files, and controlled records that still require strong document discipline. Records Management and Case Management also remain important because many organizations need formal retention schedules, complete case histories, and evidence trails that support audits and reviews.

The United Kingdom enterprise content management (ECM) market is now moving beyond simple storage toward more active process execution. Workflow and Business Process Management is projected to grow at a 13.61% CAGR through 2031, which makes it the fastest-growing solution segment in the mix. Demand is shifting toward systems that can route approvals, escalate exceptions, link documents to ERP and CRM steps, and reduce manual handoffs between teams. Microsoft's Copilot-related SharePoint development also points to a stronger buyer expectation for action-oriented content workflows rather than passive repositories.

By Deployment Mode: Cloud Architecture Commands the UK Market

Cloud captured 77.18% of the United Kingdom enterprise content management (ECM) market in 2025, confirming that SaaS delivery has become the default choice for most new deployments. Buyers prefer cloud models because they reduce infrastructure maintenance, shorten upgrade cycles, and make it easier to scale storage and workflow capacity. This model also aligns well with subscription pricing, which lowers entry barriers for organizations that do not want large upfront license commitments. At the same time, on-premises deployments remain relevant in defense, high-security public workloads, and some tightly controlled financial environments.

Cloud is also the fastest-growing deployment model, with a projected 14.03% CAGR through 2031. The United Kingdom enterprise content management (ECM) market still leaves a clear role for hybrid architecture because many large enterprises need both controlled local repositories and cloud-based automation. Hybrid adoption is strongest when firms want to preserve sensitive content on internal infrastructure while using cloud tools for collaboration, AI, or broader workflow reach. Hyland's Azure-focused partnership highlights how vendors are positioning around regional deployment flexibility, data residency, and multi-region support for enterprise buyers.

By Enterprise Size: Large Enterprises Lead as SMEs Accelerate

Large Enterprises accounted for 64.14% of market revenue in 2025, reflecting the greater governance burden and integration needs in large organizations. High document volumes, stricter audit expectations, and complex process chains make formal content management platforms harder to avoid at this scale. This is especially true in banking, insurance, pharmaceuticals, and government, where unmanaged content can create regulatory, operational, and service risks. Large accounts also support renewal streams and professional services work, which keeps them central to vendor strategy in the United Kingdom enterprise content management (ECM) market.

SMEs are projected to grow at a 13.28% CAGR through 2031, making them the fastest-growing segment of enterprises. That change reflects a better fit between cloud-native pricing and the budget realities of smaller firms. Vendors are also reducing adoption friction with preconfigured templates, managed services, and bundled workflow features that require less internal expertise. OECD work on UK SME technology adoption supports this direction, showing that cloud and AI adoption have widened enough to create a stronger base for broader content platform uptake.

By End-User Industry: BFSI Holds the Largest Share as Healthcare Accelerates

BFSI accounted for 24.86% of the market in 2025, making it the largest end-user segment in the United Kingdom enterprise content management (ECM) market. The sector's position comes from its need to manage high-value records, customer documentation, compliance evidence, policy files, and claims information in a controlled way. Banks and insurers also operate under record-keeping expectations that make searchability, retention control, and audit readiness essential rather than optional. Government and public sector organizations form another important demand block because digital service delivery depends on stable records handling, secure retrieval, and trusted case documentation.

Healthcare is projected to grow at a 13.74% CAGR through 2031, which makes it the fastest-growing end-user vertical. This reflects the push to modernize patient information flows, reduce fragmentation, and support more connected clinical records across providers. The single patient record agenda in England reinforces the need for platforms that can manage sensitive content with stronger accessibility and governance controls. Manufacturing, energy, media, retail, education, and telecom also create targeted opportunities where firms need to organize engineering files, multichannel content assets, supplier records, and regulated operational documents.

Geography Analysis

The United Kingdom enterprise content management (ECM) market operates as one national market, but spending intensity still clusters around a few stronger regional demand centers. London and the South East represent the largest concentration of activity because they bring together financial institutions, legal firms, major headquarters, and professional service providers. These organizations often face heavier record-keeping requirements and more complex approval chains than firms in less-dense regional markets. Large businesses are also more likely to use public cloud or third-party software than sole traders, which reinforces the adoption premium tied to major enterprise hubs. This concentration keeps London central to high-value deployments, system integrator activity, and larger multi-year transformation programs.

Scotland, the English Midlands, and Northern England form the next major layer of demand in the United Kingdom enterprise content management (ECM) market. Edinburgh benefits from its fintech base, where firms need stronger audit trails, records control, and secure digital workflows similar to those seen in London. The Midlands and North West also benefit from healthcare modernization and industrial use cases that require structured control of engineering records, quality documents, and supplier information. Wales and Northern Ireland remain smaller in value terms, but they continue to build demand through public sector digitization and regional service modernization.

Regional expansion depends less on basic software awareness and more on whether organizations have the skills, funding, and deployment support needed to execute complex projects. The Technology Adoption Review 2025 highlighted persistent digital adoption gaps outside the strongest hubs, signaling a wider runway for vendors that can simplify rollout and offer managed implementation. This matters because many organizations outside London recognize the value of content modernization, but they often lack the internal capacity to manage migration, governance design, and change management in-house. The United Kingdom enterprise content management (ECM) market, therefore, has room to deepen across regions as vendors build better partner coverage, lighter deployment models, and stronger local support structures.

Competitive Landscape

The United Kingdom enterprise content management (ECM) market is fragmented at the top end, with Microsoft, OpenText, IBM, SAP, and Box holding meaningful positions through large enterprise relationships and broad product ecosystems. These vendors benefit from established procurement access, strong integration coverage, and familiarity within large IT and compliance teams. Even so, their presence does not shut out challengers because buyers still replace incumbents when implementation feels too slow or product fit becomes too broad. AI-native specialists and context-focused vendors are therefore finding openings where customers want faster deployment, simpler workflow design, or more vertical alignment. This keeps the United Kingdom enterprise content management (ECM) market competitive, even as the top tier remains visible and well-resourced.

A major pattern in 2026 is portfolio sharpening among established vendors. OpenText completed the divestiture of eDOCS to NetDocuments for USD 163 million in January 2026, and the Vertica divestiture to Rocket Software for USD 150 million in February 2026, demonstrating a clear focus on narrowing its focus to core AI-led content priorities. OpenText also moved into sovereign infrastructure through its S3NS partnership, which aligns with buyers' demand for solutions that cannot rely on standard multi-tenant cloud environments. These moves show that scale alone is no longer enough, because platform relevance now depends on AI readiness, deployment flexibility, and clearer portfolio focus.

Challengers are competing by building on top of existing enterprise ecosystems rather than forcing a full replacement. M-Files strengthened its Microsoft collaboration in 2026, which supports its position with organizations seeking better document control within familiar Microsoft environments. Hyland also expanded its AI platform layer with Enterprise Context Engine, Enterprise Agent Mesh, Agent Lifecycle Management, and Control Tower, demonstrating how leading vendors are seeking to convert content repositories into broader automation environments. As a result, the United Kingdom enterprise content management (ECM) market is being shaped by a mix of large incumbent breadth and focused innovation from vendors that can move faster around AI, governance, and deployment design.

United Kingdom Enterprise Content Management (ECM) Industry Leaders

OpenText Corporation

Microsoft Corporation

IBM Corporation

Oracle Corporation

Hyland Software, Inc.

- *Disclaimer: Major Players sorted in no particular order

United Kingdom Enterprise Content Management (ECM) Market Report Scope

The United Kingdom enterprise content management (ECM) market is the ecosystem of software solutions and services that systematically capture, manage, store, preserve, and deliver an organization's unstructured and structured content and documents within the country. This includes technologies such as document management, records management, workflow, business process management, case management, digital asset management, and web content management. Deployed on-premises, in the cloud, or in hybrid models, these solutions cater to organizations of all sizes across diverse industries in the UK, including BFSI, government, healthcare, IT, and manufacturing. Driven by the country's aggressive digital transformation strategies, the widespread adoption of remote and hybrid work models, and the critical need to comply with stringent data privacy regulations (such as the UK GDPR and the Data Protection Act 2018), ECM solutions enable UK businesses to streamline complex administrative workflows, enhance enterprise-wide collaboration, ensure robust information governance, and transition from legacy paper-based systems to highly efficient, digitized operations.

The United Kingdom Enterprise Content Management (ECM) Market Report is Segmented by Solution Type (Document Management, Records Management, Workflow and Business Process Management, Case Management, Digital Asset Management, Web Content Management, and Other Solutions), Deployment Mode (On-Premises, Cloud, and Hybrid), Enterprise Size (Small and Medium Enterprises, and Large Enterprises), and End-User Industry (BFSI, Government and Public Sector, Healthcare, IT and Telecommunications, Manufacturing, Retail, Media and Entertainment, Education, Energy and Utilities, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Document Management |

| Records Management |

| Workflow and Business Process Management |

| Case Management |

| Digital Asset Management |

| Web Content Management |

| Other Solutions |

| On-Premises |

| Cloud |

| Hybrid |

| Small and Medium Enterprises |

| Large Enterprises |

| BFSI |

| Government and Public Sector |

| Healthcare |

| IT and Telecommunications |

| Manufacturing |

| Retail |

| Media and Entertainment |

| Education |

| Energy and Utilities |

| Other End-User Industries |

| By Solution Type | Document Management |

| Records Management | |

| Workflow and Business Process Management | |

| Case Management | |

| Digital Asset Management | |

| Web Content Management | |

| Other Solutions | |

| By Deployment Mode | On-Premises |

| Cloud | |

| Hybrid | |

| By Enterprise Size | Small and Medium Enterprises |

| Large Enterprises | |

| By End-User Industry | BFSI |

| Government and Public Sector | |

| Healthcare | |

| IT and Telecommunications | |

| Manufacturing | |

| Retail | |

| Media and Entertainment | |

| Education | |

| Energy and Utilities | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the size outlook for enterprise content management in the United Kingdom?

The United Kingdom enterprise content management (ECM) market size was valued at USD 2.03 billion in 2025 and USD 2.23 billion in 2026, and is forecast to reach USD 3.76 billion by 2031, growing at an 11.01% CAGR during 2026-2031.

Which solution category leads current demand in the UK?

Document Management is the largest solution segment, with 30.42% revenue share in 2025, because regulated sectors still need strong control over storage, indexing, retrieval, and records access.

Which deployment model is expanding the fastest?

Cloud is both the largest deployment mode and the fastest-growing one, with 77.18% share in 2025 and a projected 14.03% CAGR through 2031.

Why are UK enterprises investing more in content platforms now?

The main triggers are stronger governance needs, wider digital process standardization, AI-based workflow gains, and ongoing migration away from older content repositories.

Which customer group offers the strongest growth potential?

SMEs offer strong growth potential, with a projected 13.28% CAGR through 2031, as subscription pricing and preconfigured deployments reduce adoption barriers.

Which end-user segment is accelerating the most?

Healthcare is the fastest-growing end-user vertical, with a projected 13.74% CAGR through 2031, supported by patient record modernization and wider clinical content integration needs.

Page last updated on: