United Kingdom Customer Data Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

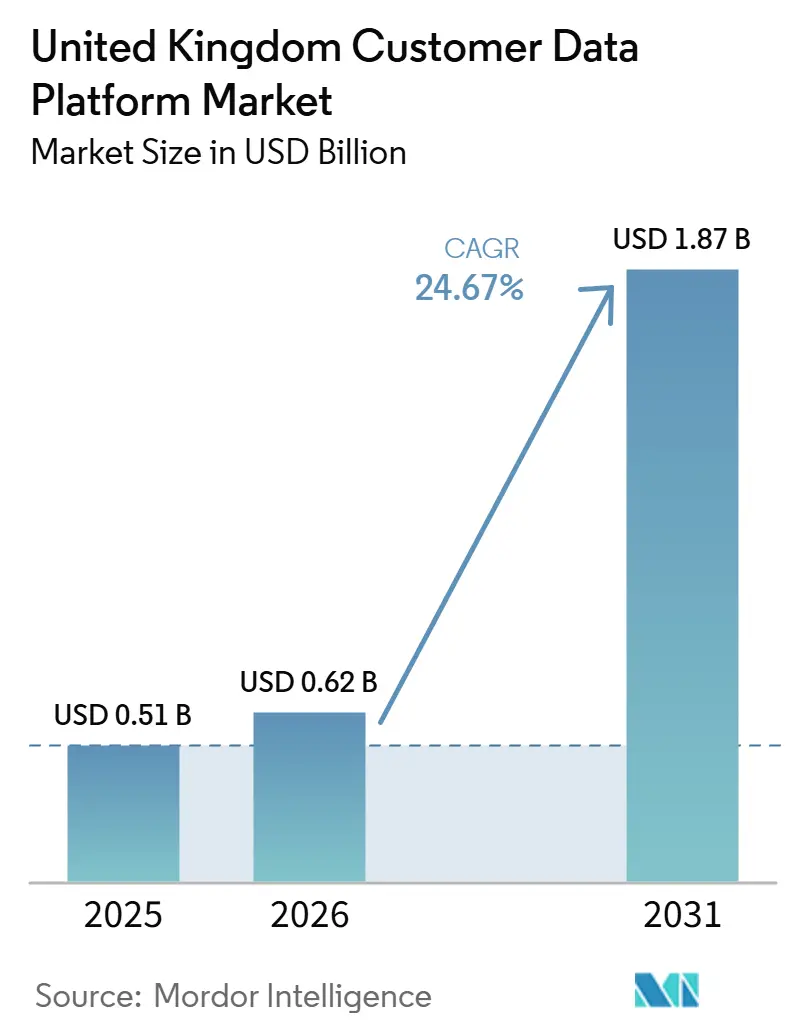

| Base Year Market Size (2025) | USD 0.51 Billion |

| Market Size (2026) | USD 0.62 Billion |

| Market Size (2031) | USD 1.87 Billion |

| Growth Rate (2026 - 2031) | 24.67% CAGR |

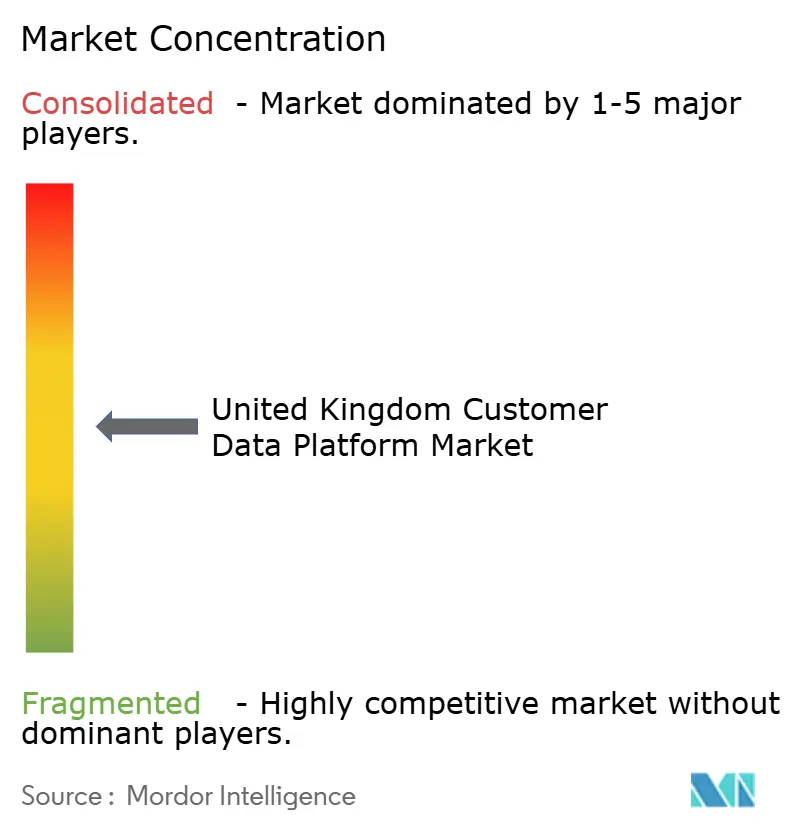

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Customer Data Platform Market Analysis by Mordor Intelligence

The United Kingdom customer data platform market size was valued at USD 0.51 billion in 2025 and estimated to grow from USD 0.62 billion in 2026 to reach USD 1.87 billion by 2031, at a CAGR of 24.67% during the forecast period 2026-2031. The United Kingdom customer data platform market is expanding because enterprises now treat first-party data control as a core operating requirement rather than a campaign tool. The withdrawal of third-party identifiers, tighter UK privacy enforcement, and the staged rollout of the Data Use and Access Act 2025 are pushing brands to unify customer data across CRM, commerce, loyalty, and service systems inside their own environments. The commercial case remains strong because unified customer data improves response quality, return on investment, and the ability to act on customer behavior across channels. The United Kingdom customer data platform market is also moving into a more execution-focused phase, where deployment quality, consent orchestration, and real-time activation matter as much as software ownership. Growth remains high through 2031, even though integration debt, skills gaps, and budget consolidation continue to slow the shift from pilot programs to scaled production use.

Key Report Takeaways

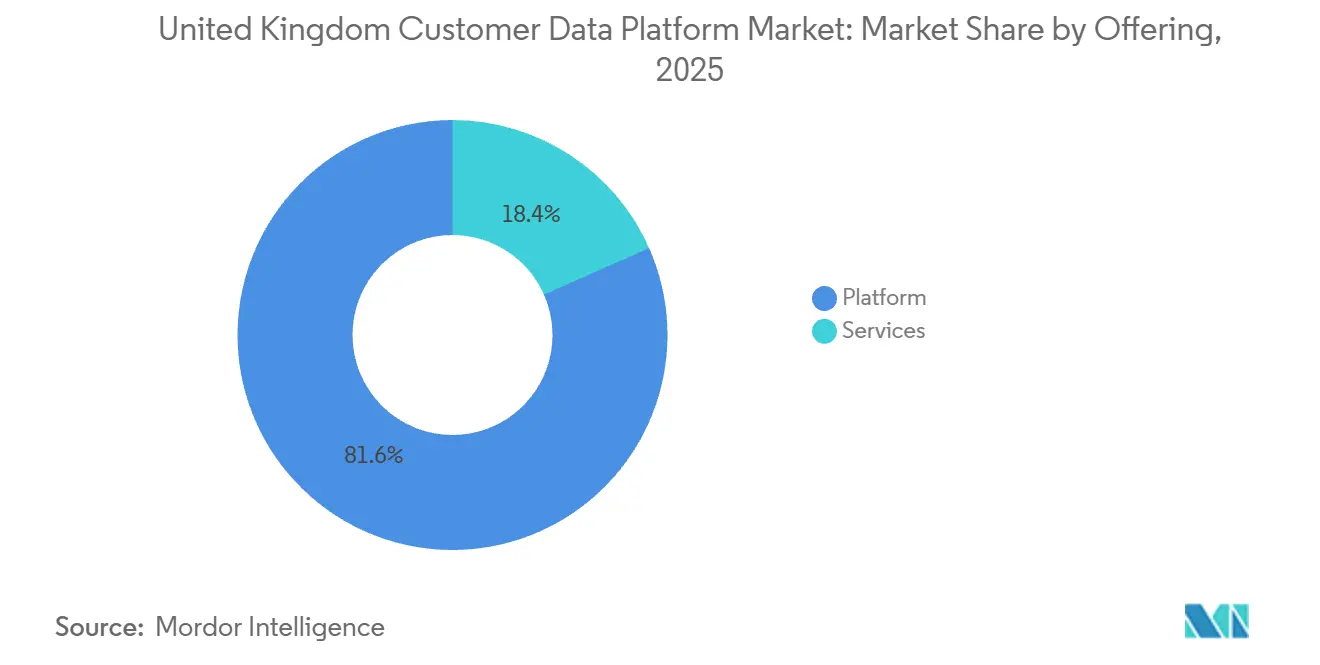

- By offering, platform held 81.62% share of the United Kingdom customer data platform market size in 2025, while services is projected to expand at a 27.92% CAGR through 2031.

- By deployment mode, cloud held 68.81% of the United Kingdom customer data platform market share in 2025, while hybrid is projected to advance at a 28.74% CAGR through 2031.

- By organization size, large enterprises accounted for 68.25% share in 2025, while SMEs are projected to record the highest CAGR at 27.45% through 2031.

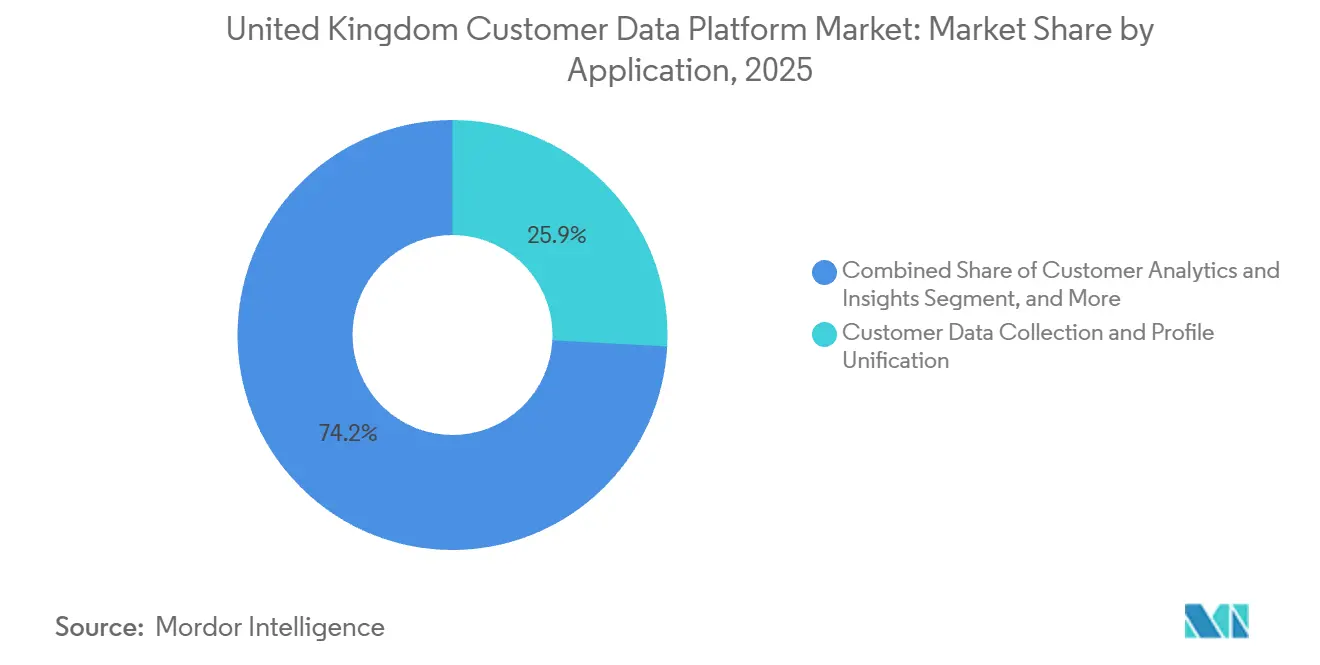

- By application, data collection and profile unification accounted for 25.85% share of the United Kingdom customer data platform market size in 2025, while customer analytics and insights is projected to grow at a 29.36% CAGR through 2031.

- By end-user industry, retail and e-commerce held 26.56% share in 2025, while healthcare and life sciences is projected to expand at a 29.84% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Customer Data Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Need for Unified First-Party Customer Profiles | +5.5% | National, with highest intensity in London, Manchester, and Birmingham commercial hubs | Medium term (2-4 years) |

| Privacy-First Marketing and Consent Management Requirements | +4.0% | National, with regulatory spill-over for UK firms with EU data flows | Short term (≤ 2 years) |

| Shift Toward Real-Time Personalization and Journey Orchestration | +3.5% | National, strongest among retail, BFSI, and media sectors | Medium term (2-4 years) |

| Cloud-Native Data Activation Across MarTech and AdTech Stacks | +3.0% | National, concentrated in cloud-mature enterprise and scale-up clusters | Long term (≥ 4 years) |

| Faster CDP Adoption in Mid-Market and Digital-First Retail Brands | +2.5% | National, with early gains in digital-first direct-to-consumer retailers | Medium term (2-4 years) |

| AI-Driven Segmentation and Predictive Churn Models | +2.5% | National, strongest in BFSI, telecom, and subscription retail | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Need for Unified First-Party Customer Profiles

The United Kingdom customer data platform market is benefiting from the shift away from third-party cookies and from tighter control by closed media ecosystems, which has made first-party data the main source of usable customer intelligence. UK brands that once depended on outside audience signals now face a direct visibility gap when customer identities sit across separate systems. That has made profile unification a practical need for campaign targeting, retention work, and cross-channel measurement. New Look showed the scale of the issue in 2025 when its deployment with Amperity and Databricks resolved 3.4 million fragmented customer profiles and found that 31% of top customers used multiple email addresses, which had weakened targeting accuracy before the rollout. The DMA also reported that performance campaigns generated 38% higher response effects when customer data was integrated across multiple channels, which supports the strong demand pull for profile unification in the United Kingdom customer data platform market.[1]Data and Marketing Association, “The Value of Customer Data Report 2025,” DMA UK, dma.org.uk Once profiles are stitched together, brands can see cross-channel revenue patterns that were previously hidden, which strengthens the business case for wider deployment across the United Kingdom customer data platform market.

Privacy-First Marketing and Consent Management Requirements

Privacy compliance has become a direct purchase driver in the United Kingdom customer data platform market because firms now need systems that can capture, govern, and pass consent signals across multiple destinations. The Data Use and Access Act 2025 received Royal Assent on June 19, 2025, and changed parts of the UK GDPR and PECR framework, including rules around automated decision-making, low-risk cookies, and recognized legitimate interest grounds. PECR penalty caps were aligned with UK GDPR levels in August 2025, which raised the possible fine ceiling for privacy breaches, increasing the cost of weak consent controls across the United Kingdom customer data platform market. The ICO also expanded compliance checks to the top 1,000 UK websites in January 2025, which signaled that consent handling and downstream data use would face much closer scrutiny. As a result, enterprises now need CDPs that can push valid permissions across channels in near real time, which supports faster adoption in the United Kingdom customer data platform market.

Shift Toward Real-Time Personalization and Journey Orchestration

The United Kingdom customer data platform market is also being pushed forward by the move from batch marketing toward live customer decisioning across paid, owned, and service channels. Salesforce announced Marketing Cloud Next in June 2025 and made agentic AI functions for campaign creation, personalization decisioning, lead management, and paid media optimization generally available on Data Cloud, which showed how major vendors are linking unified profiles to immediate action.[2]Salesforce, “Salesforce Announces Marketing Cloud Next,” Salesforce UK, salesforce.com Adobe expanded in the same direction in April 2026 with CX Enterprise, which combined AI agents, Model Context Protocol endpoints, and a governance layer to coordinate work across marketing, analytics, and content teams. When so much spending sits in digital channels, firms need customer data systems that can react quickly to behavior, and that raises the value of streaming CDP designs across the United Kingdom customer data platform market. The next step is already visible because journey orchestration is starting to shift from manual campaign design toward systems that can trigger and adjust actions automatically when customer context changes.

Cloud-Native Data Activation Across MarTech and AdTech Stacks

Cloud-native design is becoming more important in the United Kingdom customer data platform market because earlier data stacks often failed when they had to copy, move, and reconcile large customer datasets across too many tools. Warehouse-native and composable approaches answer that problem by working from governed data environments that companies already use, which is especially relevant for financial services and technology buyers with established cloud investments. The CDP Institute reported in January 2026 that composable and warehouse-native CDP vendors posted 7.8% organic employment growth, compared with the wider industry average of 1.3%, which points to stronger procurement momentum in this part of the market. Databricks introduced CustomerLake in 2026 as an agentic CDP built into the Databricks Lakehouse, bringing identity resolution, segmentation, customer 360, and activation closer to governed enterprise data. Tealium added AI at the Edge and AI Decisioning capabilities in May 2026, which supported on-device transformation and real-time decisioning on live event streams, reducing the need for slower release cycles in activation programs. These shifts matter because the United Kingdom customer data platform market increasingly rewards architectures that can keep data control, activation speed, and regional compliance requirements in the same operating model.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Governance Complexity Across Multiple Source Systems | -3.5% | National, most acute enterprises with multi-brand or legacy-estate architectures | Medium term (2-4 years) |

| High Integration Effort with Legacy CRM and Data Warehouses | -3.0% | National, concentrated in BFSI and large retail enterprises with multi-decade CRM investments | Medium term (2-4 years) |

| Budget Pressure from Platform Overlap and Tool Consolidation | -2.0% | National, most pronounced during annual IT rationalization cycles | Short term (≤ 2 years) |

| Skills Gap in Identity Resolution and Customer Data Activation | -1.5% | National, with an acute shortage in London and major UK tech hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data Governance Complexity Across Multiple Source Systems

The biggest day-to-day barrier in the United Kingdom customer data platform market is often the source environment rather than the CDP itself. Large enterprises in retail, BFSI, and telecom still carry customer data across many systems that were built or acquired at different times and for different functions. That leaves teams with inconsistent schemas, unclear ownership, uneven data quality, and incomplete consent histories before profile unification even begins. The Data Use and Access Act 2025 adds pressure because companies need clearer data lineage and stronger evidence of lawful processing from collection through activation, which is harder to maintain when the source estate is fragmented. New Look’s 2025 rollout showed how severe fragmentation can be, with 3.4 million customer profiles split across multiple records and higher-value customers hidden behind multiple identifiers. The United Kingdom customer data platform market, therefore, faces a practical speed limit, because governance repair and data model cleanup often take longer than platform procurement.

High Integration Effort with Legacy CRM and Data Warehouses

Integration effort remains another core brake on the United Kingdom customer data platform market because many incumbent CRM systems were not built for low-latency, bidirectional data exchange. UK enterprises often need to combine old CRM environments, warehouse exports, live event streams, and activation tools in one operating flow, which raises project complexity and cost. Custom APIs and middleware can solve part of the problem, but they also create ongoing maintenance work whenever source schemas change. Twilio addressed this challenge in July 2025 by making event-triggered journeys generally available in Engage, which helped combine warehouse context with live event signals and reduced reliance on slow CRM handoffs. Even with these improvements, many organizations still underestimate the ongoing work needed to keep connectors aligned with source-system updates. That recurring burden slows deployments in the United Kingdom customer data platform market, especially for teams with limited engineering depth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Platform Dominance Masks a Structural Services Shift

Platform accounted for 81.62% of the offering mix in 2025, which shows that software ownership still anchors most buying decisions in the United Kingdom customer data platform market. Large enterprises continue to view the platform layer as core infrastructure because it houses identity, segmentation, orchestration, and governance capabilities in one operating environment. This pattern also reflects the fact that many initial CDP projects start with software procurement before the operating model is fully defined. The platform-first approach remains especially visible among larger organizations that need standardized control across multiple brands, channels, and data sources. As a result, platform revenue still formed the largest revenue base in the United Kingdom customer data platform industry during 2025.

Services is projected to grow at a 27.92% CAGR through 2031, which makes it the faster-moving part of the offering structure in the United Kingdom customer data platform market. That shift points to a clear market change because enterprises now need help with implementation, identity resolution tuning, consent architecture, and ongoing optimization after the initial purchase. UK compliance requirements add to that demand because firms must connect privacy controls and activation logic in ways that internal teams often cannot manage alone. Composable architectures increase the same need, since warehouse-native deployments require stronger data engineering support than simpler packaged tools. In practice, the market is moving from a software-only purchase to a software-plus-operation model, where long-term value depends on how well the platform is activated. This is why services growth is outpacing platform growth, even though the platform base remains larger across the United Kingdom customer data platform market.

By Deployment Mode: Hybrid Architecture Emerges as the Enterprise Default

Cloud held 68.81% of the United Kingdom customer data platform market size in 2025, which confirms that SaaS deployment still offers the fastest route to live production for most buyers. Organizations continue to favor cloud because onboarding is quicker, integration with modern MarTech tools is easier, and scaling does not require capital-heavy infrastructure plans. This model fits especially well with enterprises that already run customer engagement systems in cloud environments and want fewer operational delays. Cloud also remains attractive for teams that need rapid testing across campaign workflows, audience models, and channel activation. These practical advantages kept cloud as the largest deployment mode in the United Kingdom customer data platform market during 2025.

Hybrid is projected to expand at a 28.74% CAGR through 2031, which shows that the fastest growth is coming from buyers who need more control over where and how data is processed. This is a direct response to the UK’s post-Brexit regulatory setting, where firms with EU-facing operations must manage separate rules around consent, transfers, and data handling. A hybrid design allows them to split storage or processing by jurisdiction while still keeping a unified customer decisioning framework. Tealium’s model remains relevant here because it supports composable and real-time activation needs in multi-brand environments where centralized cloud-only design is not always practical. On-premises deployment, therefore, retains a durable place in regulated settings, but the real momentum now sits with hybrid architecture across the United Kingdom customer data platform market. The United Kingdom customer data platform market is likely to keep rewarding vendors that can combine cloud flexibility with local control rather than pushing buyers into one operating model.

By Organization Size: SME Acceleration Signals a Democratization of CDP Access

Large enterprises represented 68.25% of organization-based demand in 2025, which shows how strongly the United Kingdom customer data platform market was shaped by buyers with larger budgets and deeper technical teams. These firms had the scale to justify unified identity work, broader activation programs, and enterprise-grade privacy controls earlier than smaller peers. They also faced the highest pressure to connect data across many business units and customer touchpoints, which made CDP adoption easier to defend internally. Large enterprise leadership was therefore tied to both purchasing power and operational complexity. This kept the upper end of the market in front during 2025, even as vendor models started to change.

SMEs are projected to grow at a 27.45% CAGR through 2031, which points to a wider opening of access across the United Kingdom customer data platform market. Usage-based pricing and composable design have reduced some of the entry barriers that once kept mid-market firms out of the category. Smaller digital-first retailers and subscription businesses can now begin with event collection and warehouse sync, then add activation use cases as their data maturity rises. The rise of lower-cost and more modular platforms has made that path more realistic for firms that do not want large annual software commitments. This broadens the buyer base for the United Kingdom customer data platform industry and reduces its dependence on only the largest enterprise accounts. The pattern also suggests that future growth will come not only from more enterprise rollouts, but also from a larger number of mid-sized deployments across retail, commerce, and service sectors.

By Application: Analytics And Insights Displaces Collection as the Next Value Layer

Customer Data collection and profile unification held a 25.85% share of the United Kingdom customer data platform market in 2025, confirming that basic data consolidation still served as the primary starting point for many deployments. Most organizations first adopted CDPs to solve identity stitching, audience visibility, and fragmented source data across channels. That foundation remains necessary because no higher-value use case works reliably without a persistent and trusted customer record. As a result, collection and unification retained the largest application position in 2025. It stayed central to the United Kingdom customer data platform market because it underpins segmentation, orchestration, analytics, and consent management.

Customer analytics and insights is projected to expand at a 29.36% CAGR through 2031, which shows that the market is shifting from data assembly toward predictive action. Once unified profiles are in place, companies are placing more value on churn modeling, lifetime value scoring, and next-best-action logic than on data ingestion alone. Adobe’s Customer AI capability reflects this move because it embeds churn and conversion propensity scoring directly within unified profiles, which reduces the need for separate analytics infrastructure.[3]Adobe, “Customer AI Overview,” Adobe Experience League, adobe.com This matters because propensity scores and segment outputs are no longer used only by marketing teams. Sales, service, and product functions are now drawing from the same profile layer, which increases executive support and broadens spend across the United Kingdom customer data platform market. The United Kingdom customer data platform market is therefore moving into a stage where insight delivery and business action define the next round of differentiation.

By End-User Industry: Healthcare’s Acceleration Redefines CDP Use Cases Beyond Retail

Retail and e-commerce held 26.56% of the United Kingdom customer data platform market share in 2025, keeping the sector in the lead, as it faces the clearest need for cross-channel personalization and audience activation. Retailers deal with high-frequency consumer signals across commerce, loyalty, email, mobile, and store activity, which makes unified customer identity immediately valuable. The category also has a long history of experimentation with digital targeting, search, onsite personalization, and retention programs. These conditions helped retail and e-commerce maintain the broadest deployment base in the United Kingdom customer data platform market. The segment still sets the pace for practical activation use cases because customer-level revenue impact is easier to measure there than in many other verticals.

Healthcare and life sciences is projected to grow at a 29.84% CAGR through 2031, which makes it the fastest-expanding end-user group in the United Kingdom customer data platform market. The driver is not only patient communication, but also the wider effort to unify patient-facing data for personalized care pathways, service coordination, and regulated engagement models. Bupa’s June 2026 rollout of DNA-driven personalized prevention pathways for UK insurance customers showed how health data integration is moving toward more tailored engagement supported by AI. The NHS Federated Data Platform is also building data connectivity across previously disconnected operational systems, which should improve infrastructure readiness and data literacy across healthcare organizations. BFSI remains a high-value part of the United Kingdom customer data platform market because regulated financial institutions are now more willing to implement enterprise customer data programs across channels. This means the market is widening beyond its retail roots and is being shaped by sectors where trust, governance, and real-time engagement must work together.

Geography Analysis

The United Kingdom customer data platform market is shaped by the country’s unusual mix of commercial digital scale and standalone privacy regulation. The growing digital ad spending base is important because organizations buying digital reach at that scale need reliable profile unification, stronger attribution, and faster audience refresh across channels. The market also carries a higher specification burden than many peers because firms serving both UK and EU customers must manage separate consent and transfer requirements under different regulatory settings.

London remains the main adoption hub within the United Kingdom customer data platform market because it combines FTSE 100 headquarters, large financial services buyers, and one of the deepest MarTech partner networks in Europe. This concentration gives vendors easier access to enterprise procurement teams, data engineering talent, and implementation partners that can support complex rollouts. London-based fintech and digital commerce firms also tend to be more open to warehouse-native and composable architectures because they already operate modern cloud data stacks. That makes the capital the center of higher-complexity deployments, especially where governance, personalization, and cross-channel execution need to be connected in one operating layer.

Manchester, Birmingham, and the South East also matter because they host major retail and omnichannel brand clusters that support mid-market uptake in the United Kingdom customer data platform market. These regional demand centers are tied less to highly customized enterprise builds and more to practical use cases such as loyalty activation, customer lifecycle management, and digital commerce retention. The spread of adoption outside London suggests that demand is broadening from top-tier enterprise accounts to a wider base of regional operators. It also supports service and partner growth because implementation work increasingly needs local retail and data integration expertise. The United Kingdom customer data platform market, therefore, acts as both a demanding domestic arena and a testing ground where vendors refine privacy-aware, real-time, and multi-system capabilities before extending them more widely.

Competitive Landscape

The United Kingdom customer data platform market is moderately concentrated, with global enterprise vendors competing against a rising group of composable and specialist providers rather than one company controlling the field. Salesforce, Adobe, and Oracle remain central in large enterprise and FTSE 100 buying cycles because they can connect customer data to broader sales, service, commerce, and marketing stacks. This gives them an advantage in buyers who want fewer vendors and tighter governance across business functions. At the same time, the market remains contestable because many organizations now prefer more open and modular data architectures.

Salesforce strengthened its position by linking Data Cloud to agentic marketing execution through Marketing Cloud Next, which moved the platform further from passive data storage toward live decisioning and campaign action. Oracle pushed in the same direction in April 2026 by introducing Fusion Agentic Applications for Customer Experience, which embedded coordinated AI agents across marketing, sales, and service workflows.[4]Oracle, “Oracle Introduces Fusion Agentic Applications for Customer Experience,” Oracle UK, oracle.com Adobe expanded its orchestration offer with CX Enterprise in April 2026, which added AI agents and governance features for enterprise-scale workflow coordination. These moves show that the United Kingdom customer data platform market is no longer competing only on profile unification, but also on how quickly platforms can convert customer context into governed action. Vendors that can tie identity, analytics, orchestration, and AI control together are better placed in complex enterprise deals.

A second group of competitors is gaining ground by reducing data duplication and working more closely with customer data warehouses. Hightouch reached USD 100 million in ARR in April 2026 and later raised USD 150 million in Series D financing, which reflected strong investor and buyer confidence in warehouse-native design. Databricks entered more directly with CustomerLake in 2026, giving existing lakehouse customers an embedded agentic CDP path that avoids another data store. Tealium also advanced its position in May 2026 with AI at the Edge and AI Decisioning, which supported real-time activation and on-device transformation for live event streams. The result is a market where large suite vendors still matter, but specialists can win when buyers want stronger data-plane control, lower duplication, or sharper vertical execution in the United Kingdom customer data platform market.

United Kingdom Customer Data Platform Industry Leaders

Twilio Inc.

Salesforce, Inc.

Adobe Inc.

Oracle Corporation

Tealium, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Hightouch raised USD 150 million in Series D financing led by Goldman Sachs Alternatives and Bain Capital Ventures at a USD 2.75 billion valuation, and simultaneously launched Lifecycle Studio, an agentic lifecycle marketing platform that automates campaign creation through interconnected AI agents. The round underscores market confidence in warehouse-native, composable CDP architectures as the next dominant delivery model for enterprise customer data activation.

- June 2026: Adobe accelerated its agentic AI adoption strategy, expanding partnerships with Amazon Web Services, Anthropic, Google Cloud, IBM, Microsoft, NVIDIA, and OpenAI to extend the reach of its CDP and CX orchestration capabilities. The move positions Adobe Experience Platform as a multi-model AI governance layer, allowing UK enterprises to run external AI services against governed customer profile data without duplicating or moving sensitive records.

- May 2026: Tealium unveiled AI at the Edge capabilities, an AI Decisioning engine supporting real-time churn scoring and product affinity inference on live event streams, an MCP-powered Configuration Agent for natural-language CDP management, and AI Recommended Audiences for one-click high-value segment activation, announced at its Digital Velocity conferences in New York City and London.

- April 2026: Adobe launched CX Enterprise, an AI orchestration platform combining AI agents, agent skills, Model Context Protocol endpoints, and a governance layer for auditable multi-agent workflows. The platform expands Adobe's Real-Time CDP use cases to enterprise-scale AI coordination across marketing, analytics, and content teams.

United Kingdom Customer Data Platform Market Report Scope

The United Kingdom Customer Data Platform (CDP) market comprises software platforms and associated services that collect, unify, manage, and activate customer data from multiple online and offline sources to create persistent, unified customer profiles. These platforms enable organizations to deliver personalized, privacy-compliant, and omnichannel customer experiences through capabilities such as identity resolution, audience segmentation, real-time data activation, customer journey orchestration, analytics, and consent management.

The United Kingdom Customer Data Platform Market Report is Segmented by Offering (Platform, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and SMEs), Application (Customer Data Collection and Profile Unification, Audience Segmentation and Personalization, Marketing Campaign and Customer Journey Orchestration, Customer Analytics and Insights, Consent and Preference Management, and Other Applications), End-User Industry (Retail and E-Commerce, BFSI, Healthcare and Life Sciences, IT and Telecom, Media and Entertainment, Industrial Manufacturing, Government and Public Administration, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Platform |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| SMEs |

| Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization |

| Marketing Campaign and Customer Journey Orchestration |

| Customer Analytics and Insights |

| Consent and Preference Management |

| Other Applications |

| Retail and E-Commerce |

| BFSI |

| Healthcare and Life Sciences |

| IT and Telecom |

| Media and Entertainment |

| Industrial Manufacturing |

| Government and Public Administration |

| Other End-User Industries |

| By Offering | Platform |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| SMEs | |

| By Application | Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization | |

| Marketing Campaign and Customer Journey Orchestration | |

| Customer Analytics and Insights | |

| Consent and Preference Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| BFSI | |

| Healthcare and Life Sciences | |

| IT and Telecom | |

| Media and Entertainment | |

| Industrial Manufacturing | |

| Government and Public Administration | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the size of the United Kingdom customer data platform market?

The United Kingdom customer data platform market was valued at USD 0.51 billion in 2025, stands at USD 0.62 billion in 2026, and is forecast to reach USD 1.87 billion by 2031 at a 24.67% CAGR.

What is driving demand for customer data platforms in the United Kingdom?

The main drivers are the need for unified first-party profiles, tighter privacy and consent requirements, and stronger demand for real-time personalization across digital channels.

Which deployment model is growing fastest in the United Kingdom?

Hybrid deployment is growing fastest, with a 28.74% CAGR through 2031, as firms balance cloud flexibility with data control and regulatory requirements.

Which application area is expanding the fastest?

Customer analytics and insights is the fastest-growing application, with a 29.36% CAGR through 2031, as enterprises move from basic data collection toward predictive action.

Which end-user group leads current demand and which one is growing fastest?

Retail and e-commerce led with 26.56% share in 2025, while healthcare and life sciences is projected to grow fastest at a 29.84% CAGR through 2031.

Why are SMEs becoming more important in this space?

SMEs are projected to grow at a 27.45% CAGR because modular, composable, and usage-based CDP models are lowering entry barriers for mid-market buyers.

Page last updated on: