United Kingdom CRM Marketing Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

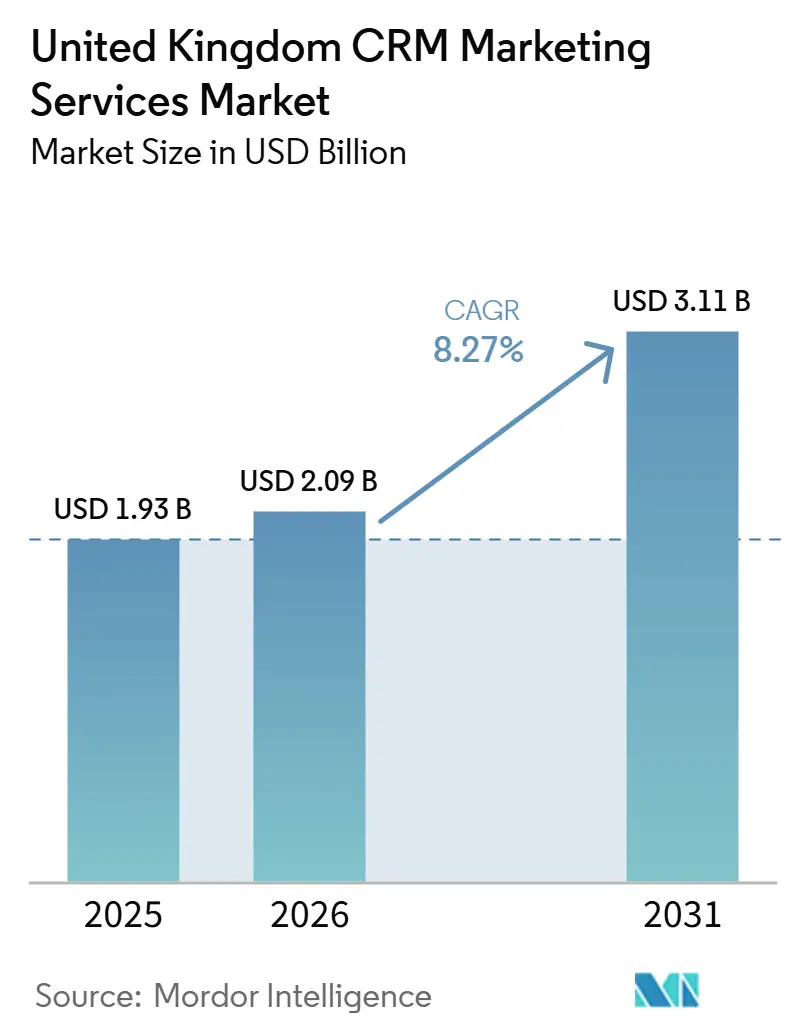

| Base Year Market Size (2025) | USD 1.93 Billion |

| Market Size (2026) | USD 2.09 Billion |

| Market Size (2031) | USD 3.11 Billion |

| Growth Rate (2026 - 2031) | 8.27% CAGR |

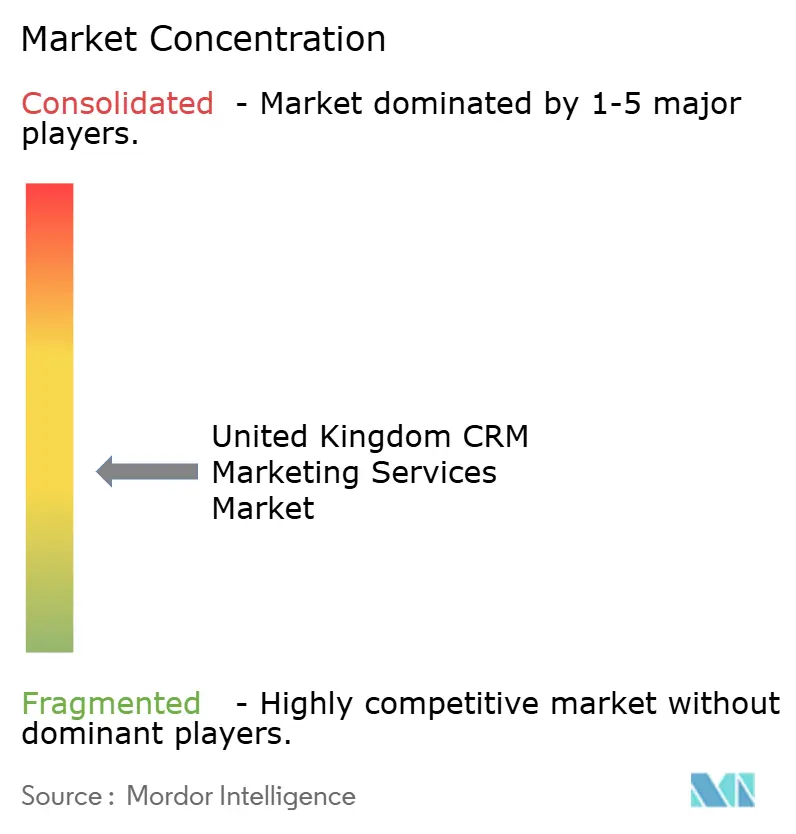

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom CRM Marketing Services Market Analysis by Mordor Intelligence

The United Kingdom CRM marketing services market size was valued at USD 1.93 billion in 2025 and estimated to grow from USD 2.09 billion in 2026 to reach USD 3.11 billion by 2031, at a CAGR of 8.27% during the forecast period (2026-2031). Demand is rising as the loss of third-party tracking methods, the broader use of AI in campaign management, and a larger shift by SMEs toward outsourced CRM support are all happening at the same time. These changes are creating overlapping buying decisions because brands that rebuild first-party data systems often need implementation, integration, and ongoing managed support together instead of in separate stages. This is changing revenue patterns in the United Kingdom CRM marketing services market because recurring managed work is becoming more important than one-time rollout projects. Competitive strategies are moving toward AI-enabled managed services, compliance-safe activation, and stronger measurement support because clients want operating help as much as they want software setup. Salesforce’s long-term UK investment also points to a deeper local ecosystem for implementation partners, managed service providers, and AI-focused CRM specialists over the forecast period.

Key Report Takeaways

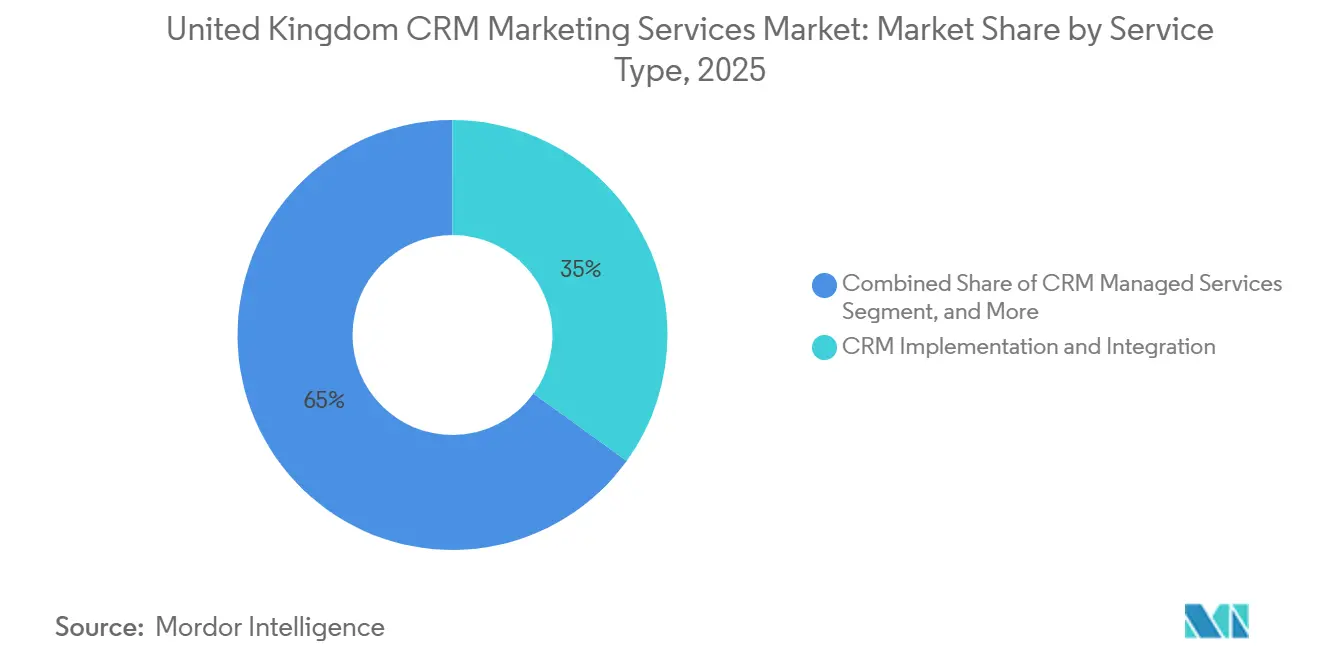

- By service type, CRM implementation and integration led with a 34.96% share in 2025, while CRM managed services are projected to expand at a 13.48% CAGR through 2031 in the United Kingdom CRM marketing services market.

- By enterprise size, large enterprises held a 69.81% share in 2025, while SMEs are projected to record the highest CAGR at 13.64% through 2031.

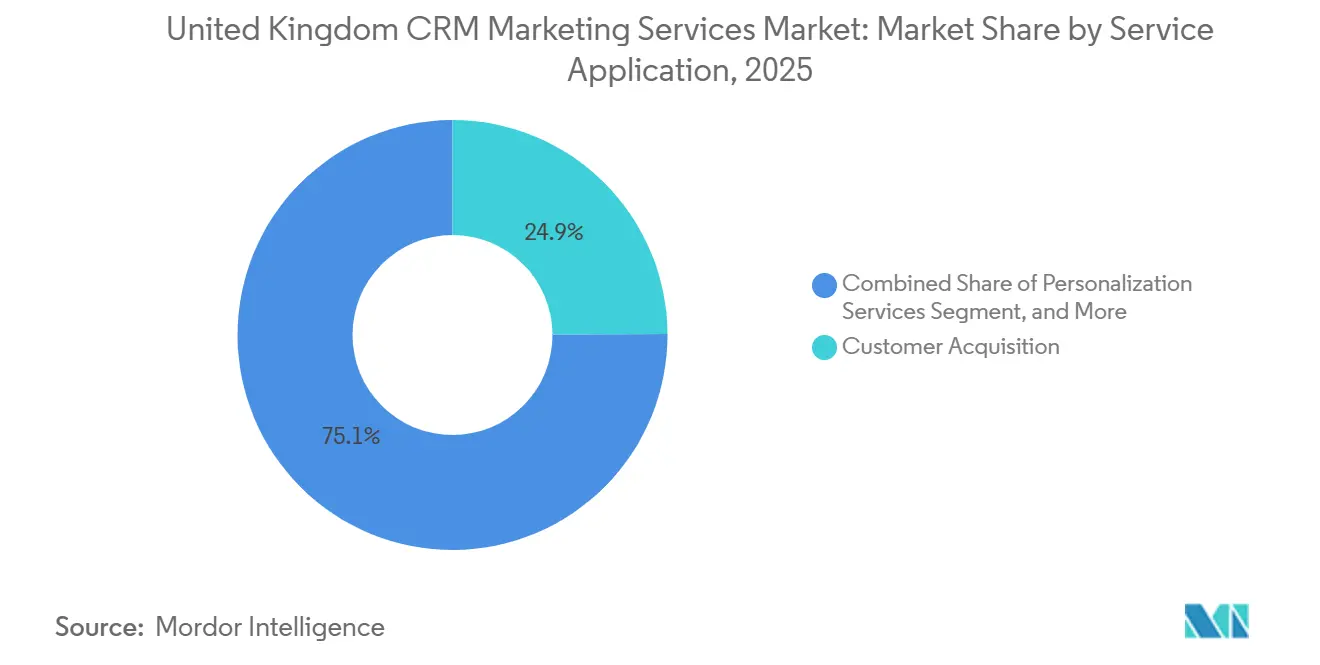

- By service application, customer acquisition accounted for a 24.93% share in 2025, while marketing automation services are projected to expand at a 15.23% CAGR through 2031.

- By end-user industry, banking, financial services, and insurance (BFSI) held a 23.86% share in 2025, while healthcare and life sciences are projected to grow at a 14.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom CRM Marketing Services Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| AI-Assisted Campaign Orchestration Adoption | +2.2% | UK-wide, strongest in London-headquartered enterprise BFSI and retail | Short term (≤ 2 years) |

| Rising Demand for First-Party Data Activation | +1.9% | UK-wide, early gains concentrated in e-commerce and direct-to-consumer brands | Short term (≤ 2 years) |

| Compliance-Led Demand for Consent-Safe Automation | +1.3% | UK-wide under ICO jurisdiction, most acute in BFSI, healthcare, and retail | Medium term (2-4 years) |

| Shift Toward Always-On Lifecycle Marketing | +1.0% | UK-wide, strongest in subscription-based business models and loyalty-driven retail | Medium term (2-4 years) |

| SME Migration to Outsourced CRM Operations | +0.8% | UK-wide, concentrated in professional services, e-commerce, and hospitality | Medium term (2-4 years) |

| Revenue Leakage Reduction Through Faster Lead Response | +0.5% | UK-wide, most acute in B2B sectors with complex sales cycles | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

AI-Assisted Campaign Orchestration Adoption

AI-assisted orchestration is changing how work is defined in the United Kingdom CRM marketing services market because providers are being asked to govern, optimize, and supervise automated campaign systems instead of only executing manual campaign tasks. Platform-led adoption is giving buyers clearer proof points because Salesforce’s May 2026 deployment for NHS Shared Business Services reduced average query handling times by 20% and routed 84% of staff queries through AI-assisted channels in its first phase.[1]Salesforce, “NHS Shared Business Services and Salesforce Deploy AI-powered Platform to Transform Corporate Services Across the NHS,” Salesforce, salesforce.com That kind of operating result is raising client expectations for CRM partners that support AI-enabled service environments. The shift does not remove the need for specialist providers because model governance, prompt design, validation, and workflow control still require hands-on expertise inside regulated and high-volume customer environments. As more campaign work moves into AI-supported execution, service providers that can combine implementation with daily operating oversight are gaining a stronger position in the United Kingdom CRM marketing services market.

Rising Demand For First-Party Data Activation

First-party data activation is becoming a core requirement in the United Kingdom CRM marketing services market as brands adjust to weaker third-party tracking and greater pressure to work from consented customer data. This is expanding demand for customer data platform work, server-side tracking support, identity resolution, and CRM integration services because many brands still have gaps between their data assets and their activation tools. DMA reported that customer data-driven campaigns using integrated, multi-channel first-party data generated 38% higher response effects for performance campaigns in 2025.[2]Data and Marketing Association, “The Value of Customer Data Report 2025,” Data and Marketing Association, dma.org.uk That performance gap is shortening internal approval cycles because first-party architecture is now tied more directly to measurable commercial outcomes. Providers that already built strong client data foundations are also harder to displace because data quality, consent design, and activation workflows create practical switching costs once they are embedded.

Compliance-Led Demand for Consent-Safe Automation

Compliance-safe automation is gaining weight in the United Kingdom CRM marketing services market because businesses are being pushed to prove that CRM activity is aligned with valid consent, channel permissions, and defensible records. Many businesses that adopted standard marketing automation before 2024 still lack the operating controls needed for stronger consent tracking, opt-in history management, and retention governance. This is concentrating opportunities among providers that can design consent-led workflows from the start instead of adding controls later. The result is a visible gap between general digital agencies and specialists that can combine marketing automation with data protection discipline. In practical terms, buyers are increasingly treating compliant-by-design CRM delivery as an operating requirement rather than an optional feature when they choose service partners in the United Kingdom CRM marketing services market.

Shift Toward Always-On Lifecycle Marketing

Always-on lifecycle programs are taking a larger role in the United Kingdom CRM marketing services market because clients are moving away from isolated campaign bursts and toward behavior-triggered communication across the full customer journey. This model improves retention logic because interactions can be tied to browsing behavior, purchase timing, service events, and renewal windows instead of fixed campaign calendars. DMA’s 2025 automation report supported the case for this shift by linking automation-enabled lifecycle marketing with stronger retention outcomes than batch-led execution models. The commercial value also compounds over time because each automated touchpoint adds more signal to the customer record and improves future personalization. That is why lifecycle design and automation architecture are becoming some of the stickiest service lines for providers operating in the United Kingdom CRM marketing services market.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Fragmented MarTech Stacks and Integration Debt | -1.5% | UK-wide, most acute in mid-market enterprises with layered legacy stacks | Medium term (2-4 years) |

| GDPR and Consent Management Complexity | -0.9% | UK-wide under ICO jurisdiction, cross-sector, with financial services and healthcare most affected | Long term (≥ 4 years) |

| Talent Shortage in CRM Operations and Marketing Automation | -0.5% | UK-wide, most severe in London, worsened by post-Brexit hiring restrictions | Long term (≥ 4 years) |

| Attribution Uncertainty Across Cookieless Journeys | -0.4% | UK-wide, most acute in digital-first consumer brands running multi-channel paid and owned media | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented MarTech Stacks and Integration Debt

Fragmented CRM, automation, analytics, and content systems remain the largest operating drag on the United Kingdom CRM marketing services market because disconnected tools slow execution and weaken data confidence. When buyers run layered legacy stacks, providers often spend too much time reconciling data and fixing workflows before they can improve campaign performance. Stack consolidation can create new implementation work, but the transition period still delays launch timelines and slows value capture for both buyers and service partners. Poor integration also hurts contract stability because providers that inherit broken environments may be judged on results before they receive a mandate to redesign the stack. This keeps integration debt as a real brake on service quality, even while it creates future project opportunities.

GDPR and Consent Management Complexity

Consent management remains a long-term restraint on the United Kingdom CRM marketing services market because the most valuable CRM use cases often depend on lawful, traceable, and well-documented data processing. The challenge is not only legal interpretation, it is also the cost and effort of maintaining channel-level consent records, evidence trails, and data governance routines over time. Mid-market organizations are especially exposed because they often want advanced personalization but delay the supporting investment needed to run it safely. This can lead buyers to narrow program scope so they stay within their compliance comfort zone, which limits the pace of CRM expansion. At the same time, the complexity strengthens the case for managed providers that can package compliant delivery as an operating outcome instead of leaving the burden with in-house teams.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Managed Services Gain Ground Alongside Core Implementation Work

CRM Implementation and Integration held 34.96% of the United Kingdom CRM marketing services market share in 2025. That leadership reflected sustained demand for platform deployment, stack consolidation, and ERP-to-CRM integration across enterprise and upper mid-market accounts. The category remained large because platform architecture changes and AI-linked feature upgrades kept even existing CRM users in need of new implementation work. Strategy, migration, modernization, and training services also remained active because businesses continued replacing legacy environments and outdated marketing systems.

CRM Managed Services is projected to expand at a 13.48% CAGR through 2031. Growth is being supported by SME demand for subscription-based CRM support, enterprise demand to externalize AI oversight, and the high cost of building capable internal operations teams. These contracts are becoming structurally stickier than project work because providers remain inside the daily operating stack and gain cumulative knowledge from live performance data. Salesforce’s plan to invest USD 6 billion in the UK through 2030 should deepen the local partner base and strengthen managed service capacity over time.

By Enterprise Size: SME Adoption Broadens the Demand Base

Large Enterprises held 69.81% of the United Kingdom CRM marketing services market share in 2025. Their spending stayed concentrated in complex multi-system environments that include ERP links, multi-brand data structures, and omnichannel engagement infrastructure. Large accounts also carry more coordination overhead because platform vendors, implementation specialists, managed service partners, and analytics providers often work on the same program. That complexity favors providers that can cover more of the delivery chain inside one operating relationship.

SMEs are projected to expand at a 13.64% CAGR through 2031. Subscription-based outsourced CRM models are lowering the historical cost barrier that once kept advanced activation, analytics, and automation out of reach for many smaller businesses. ActiveCampaign’s June 2025 MCP Server launch showed how mid-market platforms are making AI-assisted data access and automation support easier to use across plan tiers.[3]ActiveCampaign, “Introducing the ActiveCampaign MCP Server,” ActiveCampaign Community, community.activecampaign.com This helps explain why the United Kingdom CRM marketing services market is seeing its fastest incremental growth outside the largest accounts even though enterprise demand still anchors revenue.

By Service Application: Automation Expands Beyond Acquisition-Led Programs

Customer Acquisition accounted for 24.93% of the United Kingdom CRM marketing services market size in 2025. It remained the largest application because many UK businesses still prioritize filling CRM-managed funnels with new contacts and sales opportunities. Strong acquisition spending also creates follow-on demand in segmentation, analytics, database management, and ongoing optimization work. DMA found that integrated multi-channel customer data campaigns generated 23% more effects than single-channel execution, which is encouraging buyers to connect acquisition more closely with retention and reactivation programs.

Marketing Automation Services is projected to expand at a 15.23% CAGR through 2031. Behavior-triggered lifecycle programs and AI-assisted execution are moving automation from a support function to a central service line. Once a provider manages the automation layer, it often has a direct path into analytics, personalization, and omnichannel engagement services. This is making automation one of the clearest expansion routes for agencies and managed operators in the United Kingdom CRM marketing services industry.

By End-User Industry: Healthcare and Life Sciences Emerges as the Fastest-Growing Vertical

BFSI held a 23.86% share in 2025. Its lead came from high customer lifetime values, broad product portfolios, and long-standing dependence on lifecycle communications across banking, insurance, and wealth management. Existing use of major CRM platforms also supports steady services demand because these organizations continue to refine cross-sell logic, service messaging, and personalized engagement journeys. Retail and e-commerce also showed visible momentum as brands shifted more of their customer activity toward owned channels, automation, and personalization.

Healthcare and Life Sciences are projected to expand at a 14.78% CAGR through 2031. Haleon selected Salesforce Agentforce Life Sciences Cloud for Customer Engagement, Data Cloud, and Agentforce in October 2025 to support its 4,500-strong global sales force, showing how healthcare-facing organizations are moving toward AI-enabled engagement models. AstraZeneca also selected Salesforce Agentforce Life Sciences for Customer Engagement in December 2025, extending the move toward integrated HCP insight and medical-commercial coordination. Capgemini UK linked Veeva-to-Salesforce migration work to a wider redesign of HCP engagement, which supports a durable pipeline for specialist providers.[4]Capgemini UK, “Healthcare Professional Engagement, Transitioning from Legacy CRM in Life Sciences,” Capgemini, capgemini.com

Geography Analysis

The United Kingdom represented the full geographic scope of the United Kingdom CRM marketing services market size in 2025, while demand remained concentrated in London and expanded across Manchester, Bristol, Birmingham, and Edinburgh. London remained the main center for high-value CRM services because it combines financial services buyers, technology vendors, and specialist agencies in one location. DMA reported in 2025 that UK marketing professionals were ahead of European peers in customer data activation maturity, with integrated multi-channel CRM programs delivering stronger campaign outcomes. That maturity supports continued demand for implementation, analytics, and managed activation work across the country. BFSI, retail and e-commerce, and healthcare and life sciences continued to drive the largest volumes of CRM service procurement in the United Kingdom CRM marketing services market.

The public sector is also becoming more visible in demand creation. Salesforce’s May 2026 NHS Shared Business Services deployment showed that AI-enabled CRM operating models are now being applied at a national scale in service environments, not only in commercial customer programs. The UK regulatory environment also acts in 2 directions because it creates more need for consent-safe automation while raising the delivery standards expected from service providers. This favors providers that can combine activation capability with embedded data governance and operating discipline.

Talent pressure is not evenly distributed across the country. London remains the most expensive hiring market for senior CRM consultants and architects, which makes long engagements harder to sustain for mid-market buyers and many SMEs. That has encouraged smaller clients to work with regional providers or nearshore delivery structures instead of relying only on London-based specialists. Post-Brexit hiring constraints have further tightened the available talent pool for specialist CRM roles, which raises delivery pressure as buyer mandates widen. This uneven labor picture helps explain why regional delivery models and subscription-based managed services are becoming more important across the United Kingdom CRM marketing services market.

Competitive Landscape

The United Kingdom CRM marketing services market remains moderately fragmented, with no single provider holding a dominant share across service types. Competition spans 4 broad layers, global platform vendors, large consulting firms, specialist CRM agencies, and AI-native managed service providers. Platform companies such as Salesforce, Microsoft, SAP, Oracle, Adobe, and HubSpot shape demand through software ecosystems and partner networks, while specialist agencies compete on certification depth, domain knowledge, and operating support. Competitive pressure is strongest in the mid-market where switching costs are lower and multiple provider types pursue the same accounts. This structure keeps the United Kingdom CRM marketing services market active and competitive rather than concentrated around a small group of dominant firms.

Large consulting firms are moving deeper into specialist CRM territory through acquisition and service expansion. Accenture’s April 2024 acquisition of Unlimited added nearly 600 employees and brought CRM activation, behavioral science, and customer engagement capability into Accenture Song’s UK marketing practice. Merkle’s March 2026 appointment by Samsung Electronics Europe to lead CRM strategy transformation across 16 European markets showed how large service groups are competing for multi-country managed CRM mandates tied to AI and operating scale. Salesforce also reinforced its ecosystem position by opening its AI Centre in London in 2026 and deepening its UK investment commitment through 2030, which supports more partner-led delivery capacity around its platform. These moves show that major players are trying to own more of the operating layer, not only the software layer.

The clearest white space remains in compliance-native managed CRM services for regulated buyers and in AI governance support for enterprises that are scaling automated campaign environments. Smaller UK agencies with strong Salesforce Marketing Cloud or HubSpot execution depth can still win because they serve these needs more directly and often at lower cost than global firms. Twilio’s 2026 recognition as a leader in communications engagement platforms also highlights the growing role of infrastructure players that sit underneath omnichannel CRM programs and create additional integration work for service partners. As AI-enabled orchestration becomes more common, the market is likely to separate more clearly between providers that only configure tools and providers that can run, govern, and improve those environments on an ongoing basis.

United Kingdom CRM Marketing Services Industry Leaders

Salesforce, Inc.

HubSpot, Inc.

Adobe Inc.

Microsoft Corporation

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Salesforce opened its AI Centre in London, delivering on the USD 6 billion UK investment commitment, and simultaneously deployed an AI-powered Agentforce platform for NHS Shared Business Services that handles 84% of staff queries and reduced average handling times by 20%. The NHS SBS deployment marks one of the largest public sector CRM AI implementations in the UK and establishes a performance benchmark for AI-managed service interactions at national scale.

- March 2026: Samsung Electronics Europe appointed Merkle to lead CRM strategy transformation across 16 European markets in a 3-year partnership that leverages advanced AI to automate and optimize CRM activation, driving scalability and efficiency across Samsung's marketing operations. The contract is one of the largest CRM managed services mandates signed in the European market in 2026.

- December 2025: AstraZeneca selected Salesforce Agentforce Life Sciences for Customer Engagement to transform HCP engagement globally, incorporating medical-commercial coordination and AI-driven 360-degree HCP insights into its commercial operations transformation. The engagement extends Salesforce's remit with AstraZeneca to an end-to-end global customer engagement platform.

- October 2025: Haleon plc (London-listed) selected Salesforce Agentforce Life Sciences Cloud for Customer Engagement, Data Cloud, and Agentforce to support its 4,500-strong global sales force, prioritizing AI-enabled engagement with pharmacists and healthcare professionals worldwide. The deal represents one of the largest CRM platform deployments in the UK-headquartered consumer healthcare sector.

United Kingdom CRM Marketing Services Market Report Scope

The United Kingdom CRM marketing services market refers to the industry that provides platforms and services for managing customer relationships and improving marketing operations across UK businesses. It includes customer data management, campaign automation, analytics, personalization, and omnichannel engagement. These solutions help businesses strengthen customer loyalty and increase revenue while complying with national regulations, including the UK GDPR, the Data Protection Act, and PECR consent rules. The market is influenced by the United Kingdom’s strong focus on data privacy, cookie consent management, and the adoption of AI-driven personalization and automation technologies.

The United Kingdom CRM Marketing Services Market Report is Segmented by Service Type (CRM Strategy and Consulting, CRM Implementation and Integration, CRM Migration and Modernization, CRM Managed Services, and CRM Training and Support), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Service Application (Customer Acquisition, Customer Retention and Loyalty, Campaign Management Services, Marketing Automation Services, Customer Analytics and Insights, Omnichannel Customer Engagement, and Personalization Services), and End-user Industry (Banking, Financial Services, and Insurance (BFSI), Healthcare and Life Sciences, Information Technology and Telecom, Retail and E-commerce, Industrial Manufacturing, Government and Public Administration, and Other End-user Industries). The Market Forecasts are Provided in Terms of Value (USD).

| CRM Strategy and Consulting |

| CRM Implementation and Integration |

| CRM Migration and Modernization |

| CRM Managed Services |

| CRM Training and Support |

| Large Enterprises |

| Small and Medium Enterprises |

| Customer Acquisition |

| Customer Retention and Loyalty |

| Campaign Management Services |

| Marketing Automation Services |

| Customer Analytics and Insights |

| Omnichannel Customer Engagement |

| Personalization Services |

| Banking, Financial Services, and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Information Technology and Telecom |

| Retail and E-commerce |

| Industrial Manufacturing |

| Government and Public Administration |

| Other End-user Industries |

| By Service Type | CRM Strategy and Consulting |

| CRM Implementation and Integration | |

| CRM Migration and Modernization | |

| CRM Managed Services | |

| CRM Training and Support | |

| By Enterprise Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Service Application | Customer Acquisition |

| Customer Retention and Loyalty | |

| Campaign Management Services | |

| Marketing Automation Services | |

| Customer Analytics and Insights | |

| Omnichannel Customer Engagement | |

| Personalization Services | |

| By End-user Industry | Banking, Financial Services, and Insurance (BFSI) |

| Healthcare and Life Sciences | |

| Information Technology and Telecom | |

| Retail and E-commerce | |

| Industrial Manufacturing | |

| Government and Public Administration | |

| Other End-user Industries |

Key Questions Answered in the Report

What is the size outlook for the United Kingdom CRM marketing services space?

The United Kingdom CRM marketing services market size was USD 1.93 billion in 2025, is estimated at USD 2.09 billion in 2026, and is forecast to reach USD 3.11 billion by 2031 at an 8.27% CAGR.

Which service type currently leads demand in the UK?

CRM Implementation and Integration led the service mix with a 34.96% share in 2025 because platform rollout, consolidation, and integration work remained high across enterprise and upper mid-market accounts.

Which application area is growing the fastest through 2031?

Marketing Automation Services is projected to post the fastest growth at a 15.23% CAGR through 2031 as buyers shift toward behavior-triggered programs and AI-assisted execution.

Which customer group is creating the fastest incremental growth?

SMEs are expected to grow faster than large enterprises, with a 13.64% CAGR through 2031, because subscription-based managed CRM models are lowering cost and talent barriers.

Which end-user vertical offers the strongest growth opportunity?

Healthcare and Life Sciences is projected to expand at a 14.78% CAGR through 2031 as pharmaceutical and healthcare organizations replace legacy engagement models with AI-enabled CRM systems.

What is the main competitive theme shaping provider strategy in 2026?

Providers are moving beyond setup work toward managed operations, AI governance, and compliance-safe activation, while larger firms are also expanding through acquisitions and multi-market transformation mandates.

Page last updated on: