United Kingdom Automotive Reed Sensors Switches Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 10.67 Million |

| Market Size (2026) | USD 11.33 Million |

| Market Size (2031) | USD 15.32 Million |

| Growth Rate (2026 - 2031) | 6.21% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United Kingdom Automotive Reed Sensors Switches Market Analysis by Mordor Intelligence

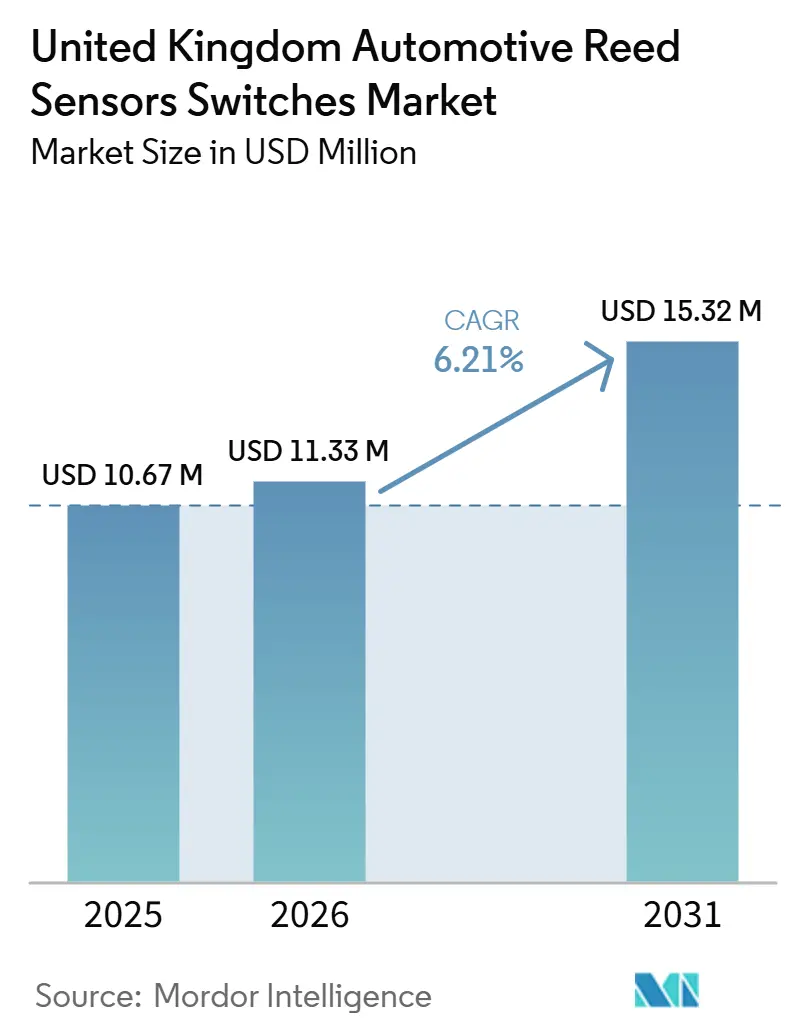

The United Kingdom automotive reed sensors switches market size was USD 10.67 million in 2025 and is estimated to grow from USD 11.33 million in 2026 to reach USD 15.32 million by 2031, at a CAGR of 6.21% during the forecast period (2026-2031). The UK automotive reed sensors market draws steady demand from a large registered vehicle parc, supporting new-fitment and replacement demand across body electronics, safety systems, and electrified drivetrain functions. Reed switches retain a broad installed base in closure, latch, and comfort functions, while integrated reed sensors support simpler module assembly through pre-aligned magnetic actuation. The ZEV mandate requires a growing share of new car sales to be zero-emission in the near term, rising to a substantial majority by the end of the decade, thereby increasing the number of battery, interlock, and charging-detection functions on electrified vehicles. This shift gives the UK automotive reed sensors market additional exposure to high-voltage isolation and low-standby-current applications. Solid-state alternatives remain a design risk, but hermetic sealing and passive operation continue to support reed-based components in demanding electrical environments.

Key Report Takeaways

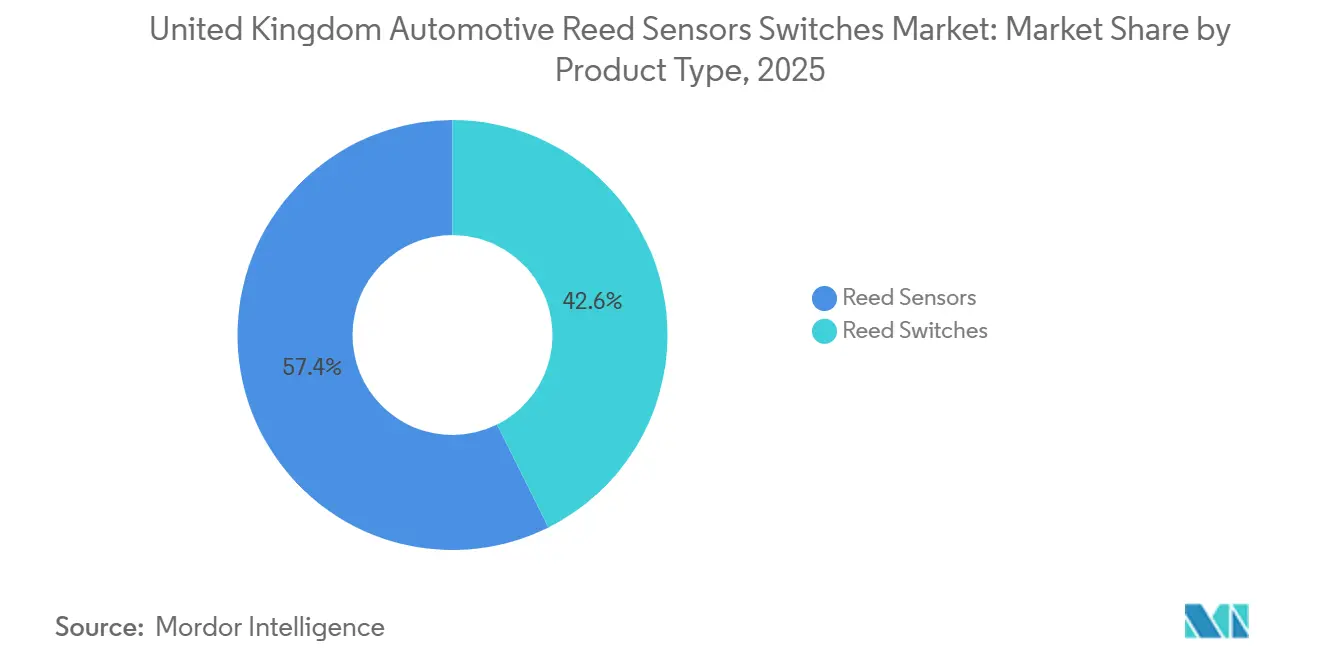

- By product type, reed switches held 57.36% revenue share in 2025, while reed sensors are forecast to grow at a 7.37% CAGR through 2031.

- By application, body electronics accounted for 30.08% revenue share in 2025, while battery and charging systems are forecast to grow at a 10.87% CAGR through 2031.

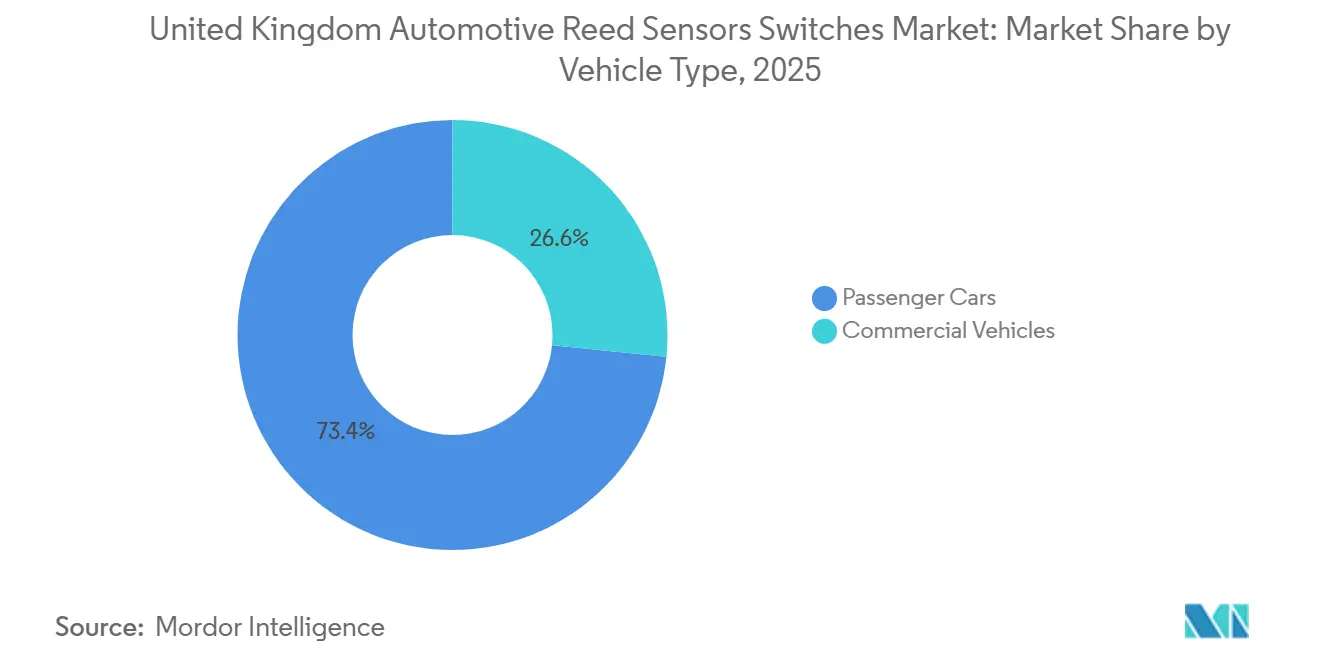

- By vehicle type, passenger cars accounted for 73.38% of revenue in 2025 and are forecast to grow at a 6.27% CAGR through 2031.

- By sales channel, OEM supply accounted for 79.01% revenue share in 2025, while the aftermarket is forecast to grow at a 6.57% CAGR through 2031.

- By propulsion type, ICE vehicles held 51.73% revenue share in 2025, while BEVs are forecast to grow at a 12.57% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Automotive Reed Sensors Switches Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ZEV-Linked EV Mix Ramp | +1.3% | National | Medium term (2-4 years) |

| Public Charging Network Growth | +1.1% | Metro Areas + Motorways | Short term (≤ 2 years) |

| Battery/Charging Sensing Nodes | +0.9% | National | Medium term (2-4 years) |

| Body Electronics Replacement Cycle | +0.8% | National | Medium term (2-4 years) |

| Aftermarket Electronics Servicing | +0.6% | National | Medium term (2-4 years) |

| Compact Module Integration Trend | +0.4% | OEM/Tier Programs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Policy-Led Electrification Increases EV Subsystem Sensing Content

Each battery-electric or plug-in hybrid vehicle sold in the United Kingdom requires more reed switches and sensors than a comparable ICE vehicle. As electrification expands, the UK automotive reed sensors market benefits from higher sensing content per vehicle. The ZEV mandate defines a phased set of registration targets, providing component planners with a clear planning framework [1]“Electric Vehicle Public Charging Infrastructure Statistics, January 2026,” GOV.UK, gov.uk.

Manufacturers exceeded the first-year target, using CO₂ conversion flexibilities to account for a portion of ZEV registrations [2]"Zero Emission Vehicle (ZEV) mandate becomes law," UK Government, gov.uk.. The mandate's banking and borrowing rules also encourage earlier standardization of high-voltage vehicle architectures, which can lead to earlier specification of reed-based isolation and interlock components.

Charging Infrastructure Expansion Supports EV Adoption and Charging-Related Electronics Demand

The UK’s public charging network continues to expand, improving charging availability and supporting broader EV adoption. Increased charging access improves EV usability and supports higher utilization rates across the installed BEV parc. As charging usage rises, both vehicle-side and charging-side interfaces require reliable detection and safety mechanisms.

This dynamic supports demand for sensing components used in charging-port status detection, connector engagement monitoring, access-door sensing, and safety interlock mechanisms. As a result, battery and charging systems remain the fastest-growing application segment, supported by infrastructure expansion and the associated growth in charging-related module deployments.

A Growing ZEV Parc Increases Serviceable Base and Accelerates Feature Penetration

The UK has a very large installed vehicle base, and the population of licensed zero-emission vehicles is increasing rapidly. A growing electrified parc expands the serviceable base for EV-associated modules and electronics components over time. This installed-base effect supports ongoing replacement demand, independent of new vehicle production cycles.

In parallel, a larger parc increases the volume of vehicles entering service and replacement cycles for body-electronics components. As electronics penetration increases across the fleet, the number of serviceable sensing points rises, supporting recurring demand for reed sensors and switches in both conventional and electrified vehicle applications.

Body Electronics Remains a High-Volume Anchor Application in the UK Parc

Body electronics support demand across ICE, HEV, PHEV, and BEV vehicles because closures, latches, and seat systems require position sensing regardless of propulsion type. The UK automotive reed sensors market benefits from a large base of registered passenger cars and an aging vehicle fleet [3]“Motorparc Registered Vehicles in Use,” SMMT, smmt.co.uk. Door-lock sensing, seat-belt buckle detection, HVAC actuator feedback, and hood or trunk position monitoring all support replacement activity.

Standex documented numerous reed switch and sensor applications in a single commercial vehicle, demonstrating the breadth of these functions at the platform level. Slow vehicle turnover helps preserve demand from older vehicles. This installed base partly offsets lower new-production volumes for legacy ICE functions.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Solid-State Sensor Substitution | -1.0% | National | Medium term (2-4 years) |

| EV Tax And Policy Shifts | -0.8% | National | Short term (≤ 2 years) |

| OEM Cost Pressure And Squeezes | -0.6% | UK/Europe Platforms | Medium term (2-4 years) |

| Platform Consolidation Reducing Variants | -0.4% | UK/Europe Platforms | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from Solid-State Sensor Technologies

In several automotive applications, OEMs may substitute reed-based solutions with solid-state sensing technologies such as Hall-effect or magnetoresistive sensors. These alternatives can be preferred where platforms require continuous measurement, tighter ECU integration, or enhanced diagnostic capability. As vehicle architectures evolve toward higher levels of electronic integration, solid-state solutions can gain share in selected sensing nodes.

This substitution pressure can limit reed penetration in specific modules, even when overall sensing demand increases. Competitive intensity is higher in applications where packaging constraints, diagnostics requirements, and cost-optimized designs favor semiconductor-based sensing approaches.

Demand Sensitivity Driven by Ownership-Cost Policy Changes for EVs

While the ZEV mandate supports long-term electrification, near-term EV demand can be influenced by changes in taxation and ownership-cost policies. Adjustments to vehicle taxation and incentive structures can affect private buyer purchase decisions and shift short-term registration volumes. This demand sensitivity can influence OEM production planning and near-term sourcing volumes for EV-associated modules.

Changes affecting total cost of ownership are particularly relevant in price-sensitive segments where purchase decisions respond quickly to policy signals. As a result, EV adoption rates can vary over short periods, creating variability in the pace of growth for battery and charging-related sensing demand tied to BEV platform volumes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Reed Switches Lead; Reed Sensors Expand Faster

Reed switches accounted for 57.36% of revenue in 2025. This position reflects decades of use in closures, latches, and position-detection applications, where a glass-encapsulated element remains practical and cost-effective. Reed sensors are forecast to grow at a 7.37% CAGR through 2031. OEM and Tier 1 managers favor preassembled and alignment-ready units because they reduce assembly variation and require less production-line space.

This preference is most evident in EV battery applications within the UK automotive reed sensors market. Standex's MHV reed relay was selected by a premium European EV manufacturer because its smaller format eliminated the need for a printed circuit board redesign. This case illustrates how miniaturization can influence design-program decisions. IATF 16949:2016 requirements also favor pre-validated module assemblies over field-assembled parts. Revenue is expected to shift gradually toward integrated sensor formats, although reed switches will continue to see substantial replacement demand from the installed base.

By Application: Body Electronics Anchor Demand; Battery and Charging Systems Drive Growth

Body electronics represented 30.08% of the UK automotive reed sensors market share in 2025. Its leading position rests on broad use across closures, seat belts, HVAC systems, and passive-entry functions. Every vehicle type in the UK parc carries these functions, making body electronics a recurring revenue base. Battery and charging systems are forecast to grow at 10.87% CAGR through 2031 as BEV and PHEV volumes increase.

Reed components support high-voltage interlocks, thermal-runaway trigger circuits, and charge-connector latch sensing. The UK has seen significant growth in public charging devices in recent years, increasing demand for charge-point sensing beyond the vehicle itself. Engine and powertrain, safety and security, infotainment and comfort, and transmission and braking functions continue to generate replacement revenue. These applications face lower volumes as ICE production declines. Other applications include fluid-level sensing in windshield washer, coolant, and brake-fluid reservoirs, which support frequent distributor-channel replacement activity.

By Vehicle Type: Passenger Cars Dominate and Lead Growth

Passenger cars accounted for 73.38% of the UK automotive reed sensors market in 2025 and are forecast to grow at a 6.27% CAGR through 2031. The segment combines a large ICE-replacement base with an expanding BEV fleet that needs battery- and charging-interlock sensing. This combination explains why passenger cars hold the largest share and the highest forecast growth rate. Their scale supports recurring demand in both new vehicles and vehicle servicing.

Commercial vehicles account for the remaining share of revenue. Fleet operators prioritize sensing reliability in harsh duty cycles, where hermetic sealing offers a durability advantage. Growth in this segment is slower because electrification has progressed more gradually in heavier vehicle classes, and replacement cycles are longer. The zero-emission bus mandate and the Bus Services Act are beginning to introduce additional sensing requirements for the light commercial and minibus categories. IATF compliance remains relevant for suppliers serving both vehicle segments.

By Sales Channel: OEMs Lead; Aftermarket Expands Faster

OEM supply accounted for 79.01% of the UK automotive reed sensor market in 2025. This share reflects direct supply programs for new vehicle production and UK-facing Tier 1 assemblers. The aftermarket accounted for a smaller share but is forecast to grow at a 6.57% CAGR through 2031. An aging vehicle parc and a growing number of vehicles beyond warranty support that faster growth.

The UK automotive reed sensor market also faces a growing segment of first-generation BEVs that will enter out-of-warranty service in the coming years. Battery-system interlocks in these vehicles can command higher selling prices than conventional body-electronics replacements and require specialized handling. Littelfuse reported substantial global Transportation segment revenue in its most recent fiscal year. Independent garage servicing of EVs remains limited by technician training requirements. Volume is expected to rise as training programs expand over the latter part of this decade.

By Propulsion Type: ICE Anchors Current Volumes; BEVs Drive Incremental Growth

ICE vehicles accounted for 51.73% of the UK automotive reed sensor market share in 2025. Petrol and diesel vehicles still accounted for 90.3% of registered passenger cars by count, sustaining demand for body-electronics replacement and servicing. BEVs are forecast to grow at 12.57% CAGR through 2031. Each BEV adds sensing functions for battery state, high-voltage safety interlocks, and charging-connector latches.

HEVs and PHEVs introduce additional sensing requirements for batteries and high-voltage systems. After BEVs, they represent the largest electrified-vehicle categories in the current UK fleet. FCEVs remain a small category, though hydrogen pilot fleets entering service in the near future carry engineering relevance. The United Kingdom has seen significant growth in BEVs on the road, according to SMMT. This growing vehicle base is expected to support aftermarket battery-system sensing demand in the coming years.

Geography Analysis

Demand for automotive reed sensors and switches in the United Kingdom is concentrated in areas with the largest vehicle parc, highest workshop density, and the strongest service and repair activity. England, particularly large metropolitan regions, accounts for a significant share of the in-use fleet and generates recurring replacement demand for body-electronics sensing points such as closures, latch modules, access systems, and comfort-related mechanisms. This concentration supports steady aftermarket consumption, aligned with the serviceable nature of many body-electronics applications over the vehicle lifecycle.

Electrification-led demand growth is more pronounced in regions with higher EV penetration and denser public charging deployment. Urban centers and key travel corridors typically see faster scaling of charging infrastructure, which supports higher EV utilization and expands the installed base of EV-associated subsystems requiring sensing and safety-state monitoring. While body-electronics demand remains broadly distributed across the country owing to the size of the overall parc, incremental growth is increasingly concentrated in EV adoption hotspots where battery and charging-related sensing requirements expand more rapidly.

Competitive Landscape

England accounts for the largest share of demand, driven by high vehicle registration density alongside automotive manufacturing and Tier 1 supply activity. The South East, West Midlands, and North West support OEM demand through Jaguar Land Rover, Stellantis at Ellesmere Port, and related supply networks. These regions also have large licensed car populations that support replacement demand. London had the largest absolute number of regional chargers, while London and the South East accounted for a significant share of public chargers. The South East and Midlands urban areas are ahead of the national ZEV penetration level, while rural Wales and Northern Ireland have lower charger density.

Scotland recorded the highest rate of rapid chargers per 100,000 people in the United Kingdom. Transport Scotland's Electric Vehicle Infrastructure Fund supported this position, alongside the central belt's battery-system and charge-connector servicing demand. Wales is at an earlier stage of its charging buildout through the ULEV Programme, and its commercial vehicle fleet presents an opportunity as logistics routes electrify. Northern Ireland had the lowest charger density among the regions. It has lower ZEV-led demand but an out-of-warranty ICE vehicle base that supports body-electronics aftermarket sales.

The UK automotive reed sensors market is affected by cross-border sourcing within the European automotive electronics supply chain. UK Tier 1 assemblers depend in part on European reed component supply and are exposed to related sourcing conditions. This dependence raises sourcing-resilience considerations for procurement teams. Demand is expected to remain uneven in the near term, as high-EV-adoption urban areas lead battery and charging applications before national ZEV targets broaden demand across the country.

United Kingdom Automotive Reed Sensors Switches Industry Leaders

-

Standex Electronics

-

Littelfuse Inc.

-

Coto Technology

-

TE Connectivity

-

PIC GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Pickering Electronics published an application guide, Reed Relays for Electric Vehicle and Charge Point Testing, detailing protocols for high-voltage measurement and insulation testing for EVs and charge points. The guide highlights reed relays' high isolation and low leakage as critical for safe high-voltage DC/AC switching in EV systems, signaling Pickering's strategic intent to expand in the UK EV testing and infrastructure segment.

- October 2025: Standex Electronics unveiled a restructured brand identity, separating into Standex Detect (reed switches, sensors, and relays), Standex Edge (power magnetics), and Standex Grid (grid solutions). The reorganization consolidates automotive reed sensing under a single focused brand, enhancing go-to-market clarity in OEM qualification programs and signaling investment in sensing-specific product roadmaps.

United Kingdom Automotive Reed Sensors Switches Market Report Scope

Automotive reed sensors/switches are magnetically actuated switching components used to detect position/state changes (open/close, proximity/position, safety-state) across vehicle systems. They are commonly deployed in body electronics (doors, trunk/hood sensing, seat and window mechanisms), safety-state interlocks, and selected electrified-vehicle/charging-adjacent modules where compact, sealed switching is preferred.

The scope includes segmentation by Product Type (Reed Switches and Reed Sensors), Application (Body Electronics, Battery and Charging Systems, and more), Vehicle Type (Passenger Cars and Commercial Vehicles), Sales Channel (OEMs and Aftermarket), Propulsion Type (Internal Combustion Engine Vehicles, Battery Electric Vehicles, and More). The market forecasts are provided in terms of value (USD).

| Reed Sensors |

| Reed Switches |

| Engine and Powertrain Systems |

| Body Electronics |

| Safety and Security Systems |

| Infotainment and Comfort Systems |

| Transmission and Braking Systems |

| Battery and Charging Systems |

| Other Applications |

| Passenger Cars |

| Commercial Vehicles |

| OEMs |

| Aftermarket |

| Internal Combustion Engine (ICE) Vehicles |

| Hybrid Electric Vehicles (HEV) |

| Plug-in Hybrid Electric Vehicle (PHEV) |

| Battery Electric Vehicles (BEV) |

| Fuel Cell Electric Vehicles (FCEV) |

| Segmentation by Product Type (Value, USD) | Reed Sensors |

| Reed Switches | |

| Segmentation by Application (Value, USD) | Engine and Powertrain Systems |

| Body Electronics | |

| Safety and Security Systems | |

| Infotainment and Comfort Systems | |

| Transmission and Braking Systems | |

| Battery and Charging Systems | |

| Other Applications | |

| Segmentation by Vehicle Type (Value, USD) | Passenger Cars |

| Commercial Vehicles | |

| Segmentation by Sales Channel (Value, USD) | OEMs |

| Aftermarket | |

| Segmentation by Propulsion Type (Value, USD) | Internal Combustion Engine (ICE) Vehicles |

| Hybrid Electric Vehicles (HEV) | |

| Plug-in Hybrid Electric Vehicle (PHEV) | |

| Battery Electric Vehicles (BEV) | |

| Fuel Cell Electric Vehicles (FCEV) |

Key Questions Answered in the Report

What is the projected value of UK automotive reed sensors switches by 2031?

The UK automotive reed sensors market is projected to reach USD 15.32 million by 2031, expanding at a 6.21% CAGR from 2026. Within the UK automotive reed sensors market, the outlook reflects demand from installed vehicle electronics, new electric vehicle systems, and replacement applications in the aging national vehicle fleet.

Which product type is growing fastest in UK automotive reed sensing?

Reed sensors are the fastest-growing product type, with a forecast CAGR of 7.37% through 2031. Preassembled and pre-aligned units can reduce assembly variation, which supports adoption in battery modules and other integrated vehicle systems.

Why are battery and charging systems important for reed components?

Battery and charging systems are expected to grow at 10.87% CAGR because BEVs and PHEVs require high-voltage interlock, thermal, and connector-latch sensing. Public charger growth also adds component demand within charging equipment, beyond component fitment in vehicles.

Is the aftermarket relevant for automotive reed sensors?

Yes. The aftermarket is forecast to grow at 6.57% CAGR as the vehicle parc ages and more BEVs move beyond manufacturer warranties. Distributor coverage, catalog breadth, and technician capability are important as independent garages take on more electronics servicing.

Why are battery and charging systems important for reed components?

Battery and charging systems are expected to grow at 10.87% CAGR because BEVs and PHEVs require high-voltage interlock, thermal, and connector-latch sensing.

Page last updated on: