United Arab Emirates Solar Photovoltaic (PV) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

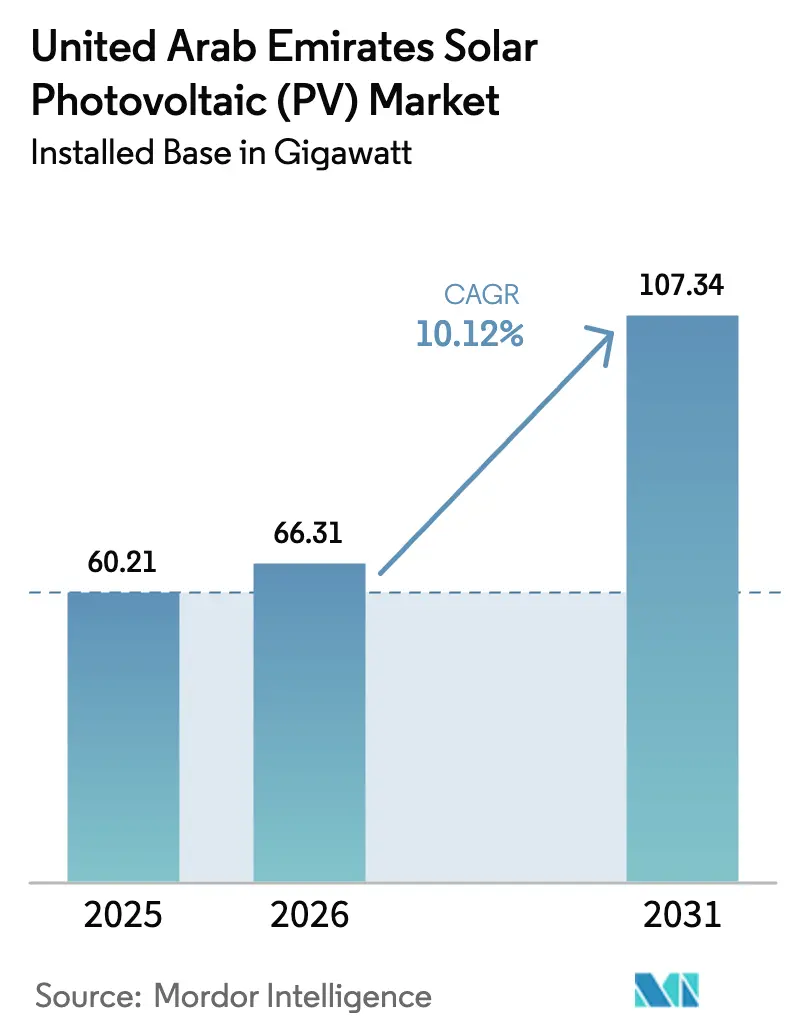

| Base Year Market Size (2025) | 60.21 gigawatt |

| Market Volume (2026) | 66.31 gigawatt |

| Market Volume (2031) | 107.34 gigawatt |

| Growth Rate (2026 - 2031) | 10.12% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United Arab Emirates Solar Photovoltaic (PV) Market Analysis by Mordor Intelligence

United Arab Emirates Solar Photovoltaic (PV) market size in 2026 is estimated at 66.31 gigawatt, growing from 2025 value of 60.21 gigawatt with 2031 projections showing 107.34 gigawatt, growing at 10.12% CAGR over 2026-2031.

Favorable economics, spearheaded by record-low tariffs of 1.413 cents per kWh at Al Ajban, position utility-scale solar as the least-cost power source in the country. Robust federal targets requiring 44% clean energy and 14.2 GW of renewables by 2030 supply long-term visibility for investors, while rapid uptake of n-type TOPCon bifacial modules supports higher yields under desert heat. Grid-forming inverters and large-format battery systems are maturing, mitigating the risk of intermittency and maintaining project bankability. Simultaneously, off-grid microgrids serving islands, desalination hubs, and telecom towers offer premium margins and hedge against curtailment.

Key Report Takeaways

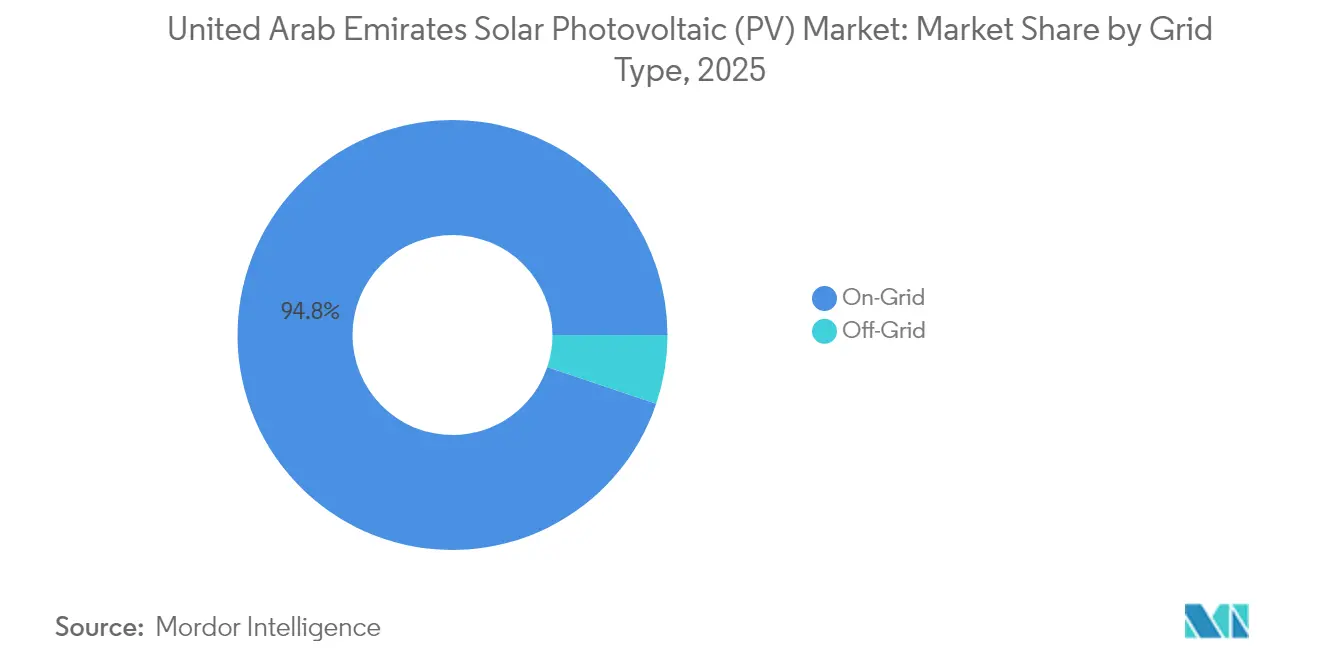

- By grid type, on-grid installations held 94.82% of the UAE solar photovoltaic (PV) market share in 2025, while off-grid installations are projected to grow at a 18.45% CAGR through 2031.

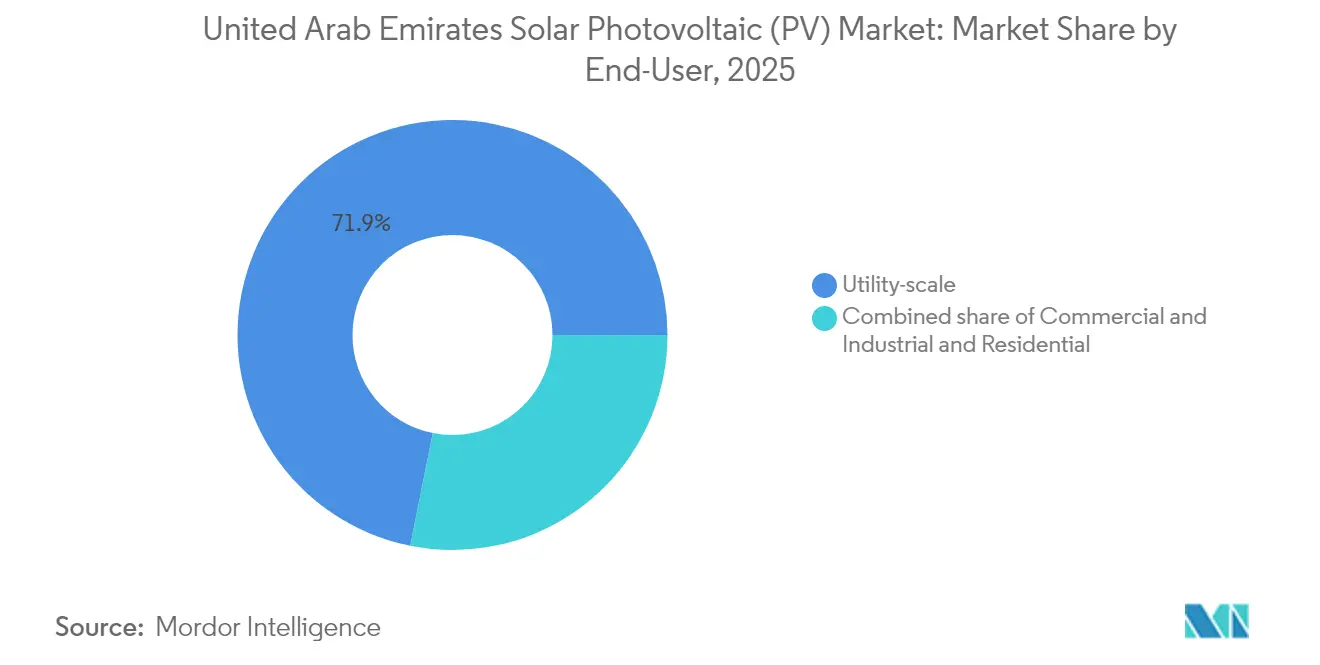

- By end-user, utility-scale projects accounted for 71.85% of capacity in 2025; residential rooftops are projected to expand at a 15.35% CAGR between 2026-2031.

- By component, n-type TOPCon bifacial modules captured 1,845 MW at MBR Solar Park Phase VI in 2025 and are forecast to command the fastest adoption rate at a double-digit CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Arab Emirates Solar Photovoltaic (PV) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Falling solar PV tariffs | +2.80% | Abu Dhabi, Dubai | Medium term (2-4 years) |

| Rising government policies & targets | +3.10% | National | Long term (≥ 4 years) |

| Megawatt-scale utility PV projects | +2.50% | Abu Dhabi, Dubai | Short term (≤ 2 years) |

| Local granular-silicon manufacturing push | +0.90% | Abu Dhabi, Jebel Ali | Long term (≥ 4 years) |

| Offshore/floating PV for desalination & islands | +0.60% | Coastal emirates | Medium term (2-4 years) |

| Hybrid solar+storage for 24/7 supply | +2.20% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Falling Solar PV Tariffs

Record-setting bids at Al Ajban reduced the benchmark price to 1.413 cents per kWh in 2024, eclipsing the previous global low at Al Dhafra. Module overcapacity in China has forced polysilicon prices below USD 7/kg, a level that has trimmed utility-scale capital costs by 15% compared to 2022. The result is a levelized cost below that of combined-cycle gas units, spurring the early retirement of aging turbines. Developers now routinely specify bifacial TOPCon modules with 23.3% efficiency, pairing them with trackers to unlock an extra 10%-15% yield.[1]Astronergy, "ASTRO N5 Module Data sheet," astronergy.com With inverter and balance-of-system prices falling 8%-12% annually, tariffs below 1.4 cents are expected to hold through 2026.

Rising Government Policies & Targets

The UAE Energy Strategy 2050 obliges 44% clean energy and 14.2 GW of renewables by 2030, underpinning a multibillion-dirham procurement pipeline. Dubai’s Clean Energy Strategy 2030 aims for 75% clean energy by 2050, accelerating MBR Solar Park toward its 5 GW goal. Abu Dhabi’s Department of Energy mandates Emirates Water and Electricity Company (EWEC) to source 1.4 GW of renewables annually from 2027, anchoring bankable offtake contracts. Net-metering at 0.28 AED/kWh sustains rooftop economics, though the recent cap reduction to 1 MW introduces caution among large commercial users.

Megawatt-Scale Utility PV Projects

Flagship parks concentrate capital and technology. MBR Solar Park surpassed 2,860 MW in 2024 and aims to reach 5,000 MW, incorporating 1,000 MW of integrated storage by 2029. Al Dhafra’s 2 GW plant supplies 160,000 households and validated bifacial performance in harsh desert winds. The AED 22 billion 5.2 GW solar-plus-19 GWh storage project, led by Masdar, G42, and ADQ, will deliver 1 GW of dispatchable output for 19 hours daily from 2027. Streamlined tenders now move from RFP to financial close in under 12 months, reducing developer overheads.

Hybrid Solar+Storage for 24/7 Supply

Battery costs plunged from USD 300/kWh in 2020 to around USD 120/kWh in 2024. DC-coupled designs share inverters, trimming balance-of-system expense by up to 15% and lifting round-trip efficiency to 92%. Masdar’s Sir Bani Yas microgrid reduced diesel use by 1.5 million liters per year and demonstrated island resilience. DEWA’s D33 policy now offers industrial users a 25% connection-charge discount when storage is paired with solar, reducing the payback period to roughly five years.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid integration & curtailment risk | -1.40% | National | Short term (≤ 2 years) |

| Nuclear generation crowd-out | -0.80% | Abu Dhabi | Medium term (2-4 years) |

| Rooftop net-metering policy uncertainty | -0.50% | Dubai, Sharjah, Ajman | Short term (≤ 2 years) |

| Dust/soiling-water scarcity O&M burden | -1.10% | Inland desert sites | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Grid Integration & Curtailment Risk

Barakah’s 5.6 GW baseload occupies about 40% of Abu Dhabi demand, leaving limited room for daytime solar.[2]World Nuclear Association, "Barakal Unit 4 Connected to Grid," worldnuclear.org Curtailment reached an estimated 3%-5% in 2024, trimming developer revenue despite take-or-pay contracts. Grid-forming inverters, such as Huawei’s FusionSolar, introduce synthetic inertia within milliseconds, easing frequency swings when the solar share spikes. EWEC’s AED 1.5 billion HVDC link between Abu Dhabi and Dubai will boost transfer capacity; however, until its completion, curtailment threatens margins.

Dust/Soiling-Water Scarcity O&M Burden

Sharjah Sustainable City data indicate a 0.21% daily output loss due to dust, equivalent to 24% annually without regular cleaning.[3]M. Al-harthy et al., "Quantifying Soiling Losses in Sharjah," ieeexplore.ieee.org Manual washing consumes up to 0.5 liters per square meter per cycle, which is expensive in a desalination-dependent country. Robotic dry-brush systems at Al Dhafra reduce water use by 80% but incur approximately USD 20/kW in capital expenditures. Anti-soiling nano-coatings from Trina Solar reduce deposition by roughly one-third, extending wash intervals to three weeks. A 200 MW site study found that robotic cleaning increased the net present value by USD 12 million over 25 years, validating the business case.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grid Type: On-Grid Scale Continues, Off-Grid Accelerates

On-grid systems accounted for 94.82% of the UAE's solar photovoltaic (PV) market capacity in 2025, primarily driven by long-term power purchase agreements with DEWA and EWEC. Utility parks, such as MBR Solar Park and the upcoming 5.2 GW solar-plus-storage project, will account for approximately 40.8 GW of the 47.13 GW net increase forecasted to 2031. The UAE solar photovoltaic (PV) market size for on-grid additions is thus on track to more than double by the end of the decade. Standardized tender templates and favorable land concessions minimize development risk, while grid upgrades align with increasing capacity. However, rising curtailment during low-demand months pushes operators to integrate storage and invest in grid-forming inverters.

Off-grid installations, although starting from a small base, are set to post a 18.45% CAGR through 2031, outpacing every other segment. Remote islands, desalination facilities, and telecom towers are now favoring solar-plus-storage over diesel, with Sir Bani Yas Island's 4.5 MW array and 3 MW/6 MWh battery system eliminating 1.5 million liters of diesel annually. [4]Masdar, "Sir Bani Yas Solar-Battery Project Factsheet," masdar.ae The UAE solar photovoltaic (PV) market benefits from microgrid economics where grid extension costs exceed USD 500,000/km. Projects in the Northern Emirates, backed by ADNOC Distribution's Phase 2 station solarization, illustrate the emerging commercial logic. Floating solar for desalination at Hassyan will broaden the addressable off-grid pool once commissioned in 2027.

By End-User: Residential Momentum Challenges Utility Dominance

Utility-scale plants represented 71.85% of capacity in 2025, underpinned by multi-year PPAs and debt leverage ratios of nearly 80%. Tariffs below 1.5 cents per kWh keep these assets competitive against gas peakers. The UAE solar photovoltaic (PV) market, dominated by utility-scale, is projected to maintain absolute leadership; however, its CAGR lags behind smaller formats. Developers are responding to curtailment and nuclear crowd-out by co-locating 4-hour storage, which boosts capacity factors and protects revenue.

Residential rooftops are forecast to grow at 15.35% CAGR, triple the utility-scale rate. Shams Dubai surpassed 10,000 participants and 280 MW of distributed capacity in 2024. Turnkey system costs now range from USD 0.90 to 1.10/W, making paybacks of six years achievable even after the net-metering cap was reduced to 1 MW. Solar-as-a-service firms, such as Yellow Door Energy and SirajPower, finance zero-upfront installations, thereby broadening access. The UAE solar photovoltaic (PV) market share held by residential systems could reach the low-double digits by 2031, provided other emirates replicate Dubai’s incentives. Commercial and industrial rooftops bridge the two ends, with CleanMax’s AED 99 million financing to roll out 69 MWp across 92 sites, signaling lender confidence.

Geography Analysis

Abu Dhabi and Dubai host more than 84% of the national solar photovoltaic (PV) capacity, cementing their primacy in the UAE solar PV market. Abu Dhabi leads in absolute volume, with the 2 GW Al Dhafra plant, the 1.5 GW Al Ajban project, and the 5.2 GW solar-plus-19 GWh storage megaproject slated for 2027. EWEC’s commitment to procure 1.4 GW annually from 2027 maintains a predictable pipeline and supports supply-chain localization. Robust transmission corridors and the presence of Barakah’s baseload inform an integrated planning approach that reduces curtailment. [5]EWEC, "Future Capacity Procurement Outlook," ewec.ae

Dubai has adopted a single-site strategy at the MBR Solar Park, which reached 2,860 MW in 2024 and aims to reach 5 GW by 2029. Complementing the flagship park, the Shams Dubai rooftop scheme embeds distributed generation across commercial and residential districts, slightly altering load curves and providing ancillary capacity during peak afternoons. Grid investments, including phase-shifting transformers and STATCOM installations, safeguard voltage stability as the share of solar energy rises.

Sharjah, Ajman, Ras Al Khaimah, Fujairah, and Umm Al Quwain collectively account for less than 9% of current capacity, yet they offer niche growth opportunities. Sharjah Sustainable City functions as a testbed for bifacial and anti-soiling studies, circulating O&M best practices nationwide. ADNOC Distribution’s rollout of off-grid arrays at over 100 service stations in the Northern Emirates illustrates commercial appetite even in smaller load centers. Coastal Fujairah is poised for solar-powered desalination, while Ajman is exploring green hydrogen pilots. Cumulatively, the lesser-populated emirates may secure 5%-7% of incremental capacity by 2031, primarily through distributed systems that mitigate curtailment risk and capitalize on high irradiation.

Competitive Landscape

State-linked developers command the upstream value chain. Masdar alone has stakes exceeding 8 GW in domestic solar projects and leverages sovereign backing for competitive financing. DEWA doubles as regulator and developer, reinforcing its influence via MBR Solar Park expansions and distributed-generation rules. TAQA co-owns Al Dhafra and Al Ajban, guaranteeing offtake certainty for lenders.

Chinese OEMs dominate equipment supply: JinkoSolar shipped half of all Middle East modules during H1 2024, while Trina Solar localizes wafers and modules at Khalifa Economic Zone to satisfy 40% local-content rules. The UAE solar photovoltaic (PV) market welcomes this shift as it reduces logistics lead time and hedges against tariff volatility. European EPC firms continue to win balance-of-plant lots, though rising Emirati fabrication capacity in mounting structures and cabling is eroding their margin.

Commercial and industrial solar-as-a-service providers disrupt the mid-downstream. Yellow Door Energy, SirajPower, and CleanMax MEA bundle zero-capex PPAs with operations and maintenance, capturing clients seeking ESG compliance without upfront spend. CleanMax's AED 99 million loan from HSBC in January 2025 underpins a 69 MWp rollout across 92 sites, displaying maturing lender confidence. Emerge, the Masdar-EDF joint venture, leverages its parent's balance sheets to bid aggressively for industrial microgrids that incorporate storage. As curtailment and tariff compression squeeze returns, developers are experimenting with vertical integration, linking manufacturing, EPC, and O&M, to preserve consolidated margins.

United Arab Emirates Solar Photovoltaic (PV) Industry Leaders

-

Masdar

-

ACWA Power

-

TAQA + EDF Renewables JV

-

JinkoPower

-

CleanMax MEA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: CleanMax MEA secured AED 99 million (USD 27 million) in financing from HSBC to scale its distributed solar portfolio to 69 MWp across 92 industrial facilities, malls, schools, and universities in the UAE, marking the largest single financing round for a behind-the-meter solar provider in the region and signaling growing institutional appetite for commercial and industrial solar assets.

- November 2024: Emirates Water and Electricity Company awarded the 1.5 GW Al Ajban Solar Project to a consortium led by EDF Renewables (20%), Masdar (60%), and Korea Western Power (20%) at a tariff of 1.413 cents per kWh, setting a new global benchmark for utility-scale solar and commencing construction for Q3 2026 commissioning.

- October 2024: Masdar, G42, and ADQ announced an AED 22 billion investment to develop a 5.2 GW solar photovoltaic plant paired with 19 GWh of battery energy storage in Abu Dhabi, designed to deliver 1 GW of baseload renewable power around the clock and scheduled for commissioning in 2027, representing the world's largest single-site solar-plus-storage project.

- October 2024: Dubai Electricity and Water Authority announced that the Shams Dubai net-metering program has surpassed 10,000 participants and installed 280 MW of rooftop solar capacity, demonstrating the scalability of distributed generation in urban environments and contributing to Dubai's goal of achieving 25% clean energy by 2030.

United Arab Emirates Solar Photovoltaic (PV) Market Report Scope

Solar photovoltaic energy (PV) converts sunlight directly into electricity through a technology based on the photovoltaic effect. Solar radiation that strikes one face of a photoelectric cell (many of which are installed on a solar panel) produces a voltage differential between the two faces, allowing electrons to flow from one face to the other, generating an electric current.

The United Arab Emirates solar photovoltaic (PV) market is segmented by grid type and end-user. By grid type, the market is segmented into on-grid and off-grid. By end-user, the market is segmented into utility-scale, commercial, industrial, and residential.

The report also covers the market size and forecasts for the United Arab Emirates. For each segment, market sizing and forecasts have been conducted based on installed capacity (GW).

| On-Grid |

| Off-Grid |

| Utility-scale |

| Commercial and Industrial (C&I) |

| Residential |

| Solar Modules/Panels |

| Inverters (String, Central, Micro) |

| Mounting and Tracking Systems |

| Balance-of-System and Electricals |

| Energy Storage and Hybrid Integration |

| By Grid Type | On-Grid |

| Off-Grid | |

| By End-User | Utility-scale |

| Commercial and Industrial (C&I) | |

| Residential | |

| By Component (Qualitative Analysis) | Solar Modules/Panels |

| Inverters (String, Central, Micro) | |

| Mounting and Tracking Systems | |

| Balance-of-System and Electricals | |

| Energy Storage and Hybrid Integration |

Key Questions Answered in the Report

How large is the UAE solar photovoltaic (PV) market today?

Installed capacity reached 66.31 GW in 2026 and is projected to grow to 107.34 GW by 2031 under a 10.12% CAGR.

What drives investment in Emirati utility-scale solar?

Record-low tariffs, strong sovereign offtake guarantees, and clear capacity targets under the UAE Energy Strategy 2050 draw capital toward gigawatt-scale parks.

Are residential rooftops financially attractive after the net-metering cap cut?

Yes, turnkey costs of USD 0.90-1.10/W and a 0.28 AED/kWh export rate still deliver six-year paybacks for typical Dubai households.

How is curtailment risk being addressed?

Grid-forming string inverters, large batteries, and new HVDC links between Abu Dhabi and Dubai provide flexibility to absorb high midday solar output.

Which technology is displacing PERC modules?

N-type TOPCon bifacial panels with efficiencies above 23% now dominate new procurements because they outperform under high temperatures and leverage albedo gains.

What share of new capacity will come from off-grid projects?

Off-grid microgrids are set to grow at 18.45% CAGR and could account for 5%-7% of incremental capacity by 2031, especially in islands and desalination applications.

Page last updated on: