United Arab Emirates Global Capability Centers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

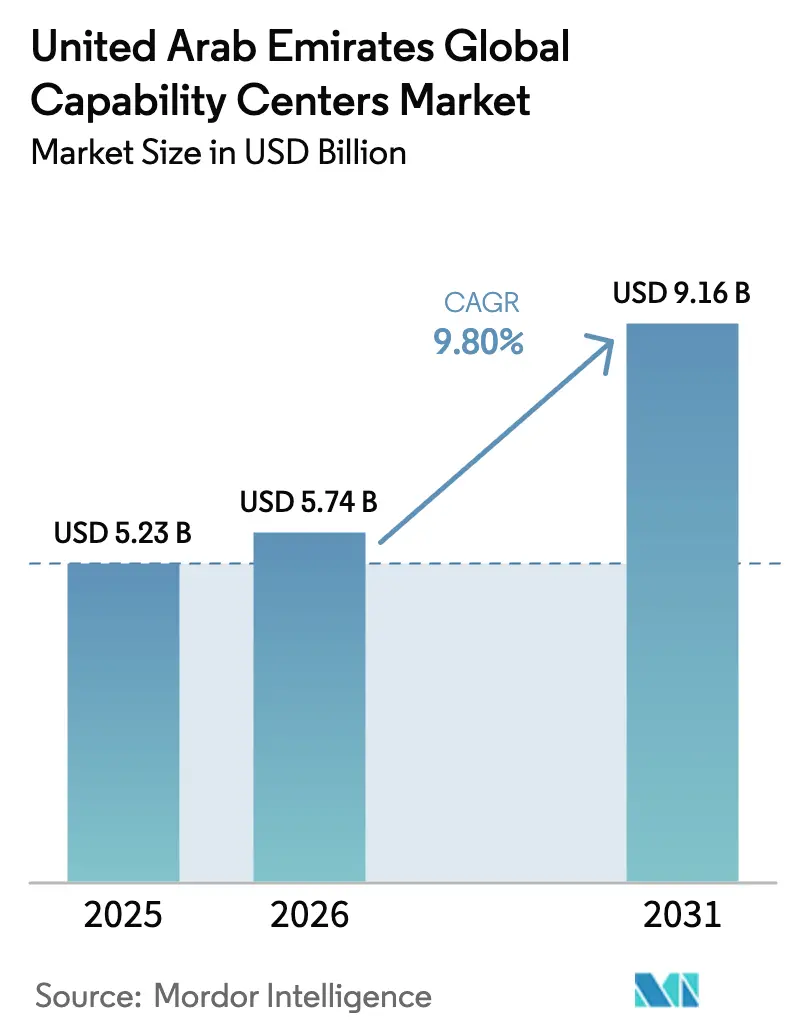

| Base Year Market Size (2025) | USD 5.23 Billion |

| Market Size (2026) | USD 5.74 Billion |

| Market Size (2031) | USD 9.16 Billion |

| Growth Rate (2026 - 2031) | 9.80% CAGR |

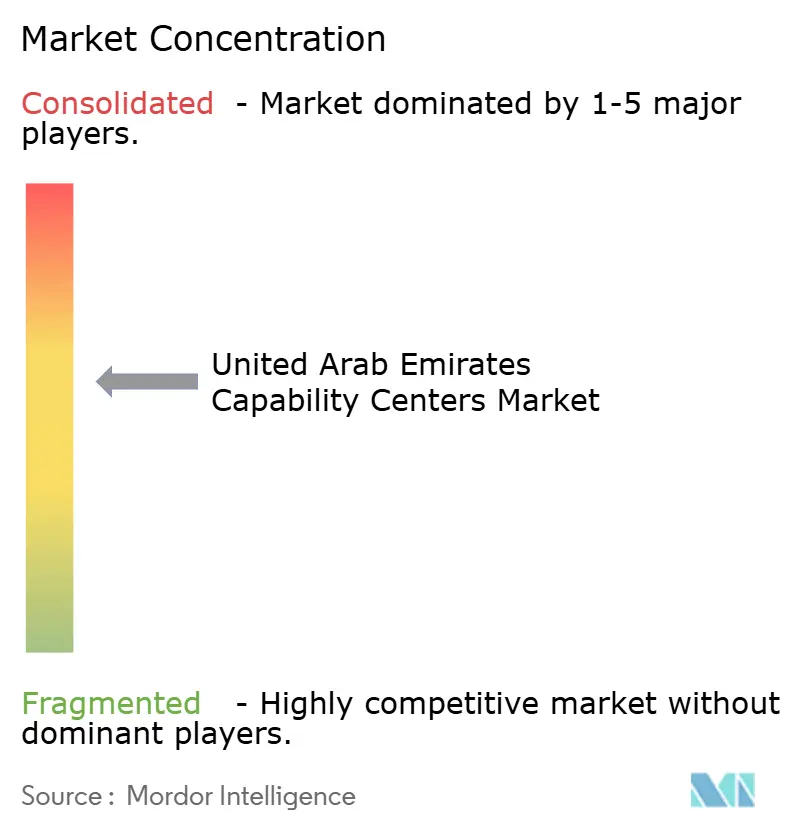

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates Global Capability Centers Market Analysis by Mordor Intelligence

The United Arab Emirates Global Capability Centers market size is expected to grow from USD 5.23 billion in 2025 to USD 5.74 billion in 2026 and is forecast to reach USD 9.16 billion by 2031 at 9.8% CAGR over 2026-2031. The market size expansion reflects sustained inflows of nearshoring mandates from multinational corporations, attracted by zero-tax free zones, advanced 5 G connectivity, and a multilingual talent pool. Intensifying European interest in politically stable hubs outside Eastern Europe, coupled with Operation 300bn manufacturing initiatives, is widening the addressable opportunity set. Within the broader context of national digital priorities, capability centers now provide critical support for AI deployments, cloud migrations, and cybersecurity modernization across industries. Competitive intensity is rising as hyperscalers and fintech start-ups bid for the same AI and cloud professionals, placing upward pressure on compensation packages.[1]Mohamad Majid, “Technology,” KPMG Lower Gulf, kpmg.com

Key Report Takeaways

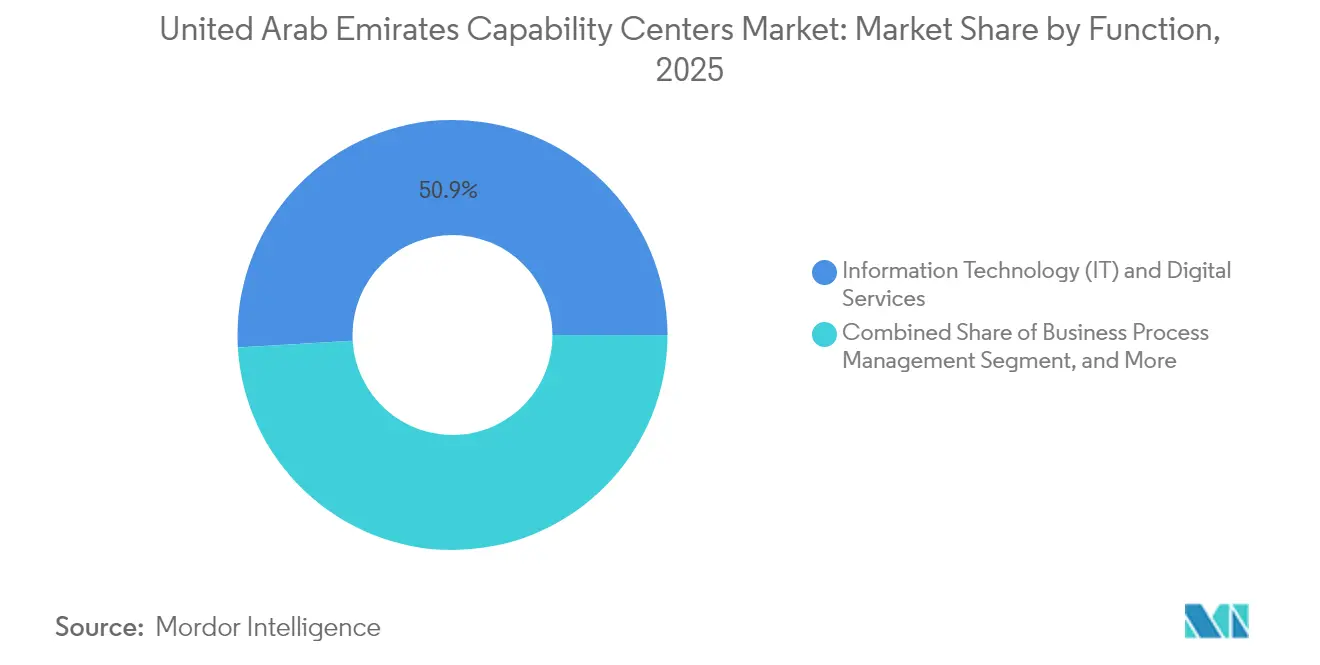

- By function, Information Technology and Digital Services led with a 50.92% revenue share in 2025; Knowledge Process Outsourcing is projected to log the fastest growth at a 10.22% CAGR through 2031.

- By engagement model, the captive format accounted for 58.85% of the 2025 United Arab Emirates Global Capability Centers market share, while hybrid build-operate-transfer structures are forecast to expand at a 10.05% CAGR to 2031.

- By organization size, large enterprises held 86.98% of the United Arab Emirates' Global Capability Centers market size in 2025; the SME segment is expected to advance at an 11.49% CAGR through 2031.

- By industry vertical, Banking, Financial Services, and Insurance commanded a 34.12% share in 2025; the Healthcare and Life Sciences sector is projected to grow at a 10.71% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Arab Emirates Global Capability Centers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government digital transformation programs are accelerating GCC demand | +2.1% | UAE national, concentrated in Dubai and Abu Dhabi | Medium term (2-4 years) |

| Zero corporate tax for free-zone GCC entities until 2029 | +1.8% | UAE free zones, spillover to the broader GCC region | Short term (≤ 2 years) |

| Multilingual talent pool fueled by high expatriate inflow | +1.4% | UAE national, with the Dubai International Financial Centre and Abu Dhabi Global Market leading | Long term (≥ 4 years) |

| European nearshoring interest amid geopolitical tensions | +1.2% | UAE national, extending to the broader Middle East and Africa | Medium term (2-4 years) |

| 5.5G private network testbeds catalyzing engineering R&D GCCs | +0.9% | UAE national, early deployment in Abu Dhabi and Dubai | Long term (≥ 4 years) |

| Emiratization-linked graduate upskilling subsidies | +0.7% | UAE national, government-backed initiatives | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Digital Transformation Programs Accelerating GCC Demand

Sweeping national initiatives to double the digital economy’s GDP share from 9.7% to 19.4% by 2035 underpin strong pipeline visibility for capability centers specializing in AI, cloud, and cybersecurity. The 100,000 sq ft Dubai AI Campus, along with strategic alliances with technology majors, demonstrates the state’s commitment to nurturing an innovation corridor that demands on-the-ground engineering, DevOps, and regulatory compliance talent.[2]Dubai AI Campus, “Dubai AI Campus names Kearney a strategic partner for AI advisory services,” consultancy-me.com Central Bank infrastructure projects, such as Aani instant payments, introduce fintech-specific workloads that require dedicated centers of excellence. These expansions sustain multi-year demand visibility while reinforcing the United Arab Emirates Global Capability Centers market as a cornerstone of the national digital strategy.

Zero Corporate Tax for Free-Zone GCC Entities Until 2029

Zero corporate tax in free zones delivers an immediate 15%-25% cost advantage versus legacy offshore sites. Multinationals are fast-tracking AED-scale commitments, illustrated by Broaden Energy’s AED 1 billion hydrogen equipment complex within Khalifa Industrial Zone.[3]Department of Economic Development, “Broaden Energy invests AED 1 billion to establish hydrogen equipment manufacturing complex in Abu Dhabi,” added.gov.ae Time-bound benefits spark urgent decision loops, inflating near-term facility absorption rates across Dubai Internet City and Abu Dhabi Global Market. Nevertheless, firms must cultivate longer-horizon differentiators, such as IP creation, talent depth, and sector-specific expertise, to remain viable once the tax holiday sunsets.

Multilingual Talent Pool Fueled by High Expatriate Inflow

Expatriates comprise more than 80% of the national workforce, enabling capability centers to service global markets in over 20 languages without incurring significant localization overhead. Programs such as the National Program for Coders, which offers Golden Visas to top software engineers, enhance AI and full-stack pipelines.[4]United Arab Emirates, “The National Program for Coders,” u.ae However, hyperscaler expansion threatens wage rationality as cloud majors recruit aggressively for the same certified professionals. Retention strategies now focus on international career mobility, advanced training modules, and equity participation, rather than solely on monetary incentives.

European Nearshoring Interest Amid Geopolitical Tensions

Conflict redirects European outsourcing roadmaps toward politically stable and time-zone-friendly destinations. TECOM Group’s USD 544 million allocation for Grade-A offices reflects the rising demand from European corporates relocating their R&D and shared-service operations. The United Arab Emirates Global Capability Centers market thus evolves from a cost arbitrage proposition to one driven by resilience, proximity to Europe, minus its geopolitical volatility. The trend remains in its early innings, yet fast-tracked arbitration frameworks and bilateral trade agreements are accelerating proof-of-concept deployments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising commercial real estate costs in Dubai's prime locations | -1.3% | Dubai's prime business districts spill over to Abu Dhabi | Short term (≤ 2 years) |

| Intense competition for digital talent from hyperscalers and fintech start-ups | -0.9% | UAE national, concentrated in technology hubs | Medium term (2-4 years) |

| Visa reform uncertainties affecting specialized expatriates | -0.6% | UAE national, affecting all emirates | Short term (≤ 2 years) |

| Limited shared-services maturity beyond Dubai and Abu Dhabi | -0.4% | Northern Emirates and emerging business districts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Commercial Real Estate Costs in Dubai Prime Locations

Grade-A rents in Dubai International Financial Centre and Dubai Internet City have climbed sharply, compressing the cost advantage traditionally associated with offshore models. TECOM’s USD 114 million outlay on fully leased towers underlines persistent demand but also signals escalating entry barriers for SMEs. Hybrid real-estate strategies, combining satellite offices in lower-rent districts with remote work models, are emerging to safeguard margins while maintaining client-facing prestige addresses.

Intense Competition for Digital Talent from Hyperscalers and Fintech Start-Ups

AWS, Microsoft, and Google have scaled headcount in the UAE, driving double-digit salary inflation for AI engineers and cloud architects. KPMG reports that 96% of local tech leaders plan to raise AI budgets within 12 months, further compounding demand. Capability centers now invest in university alliances, internal academies, and rotational programs to forge durable pipelines and contain attrition.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Function / Capability: IT Services Anchor Expansion

Information Technology and Digital Services generated USD 2.66 billion in 2025, accounting for 50.92% of the United Arab Emirates' Global Capability Centers market size. The segment’s primacy stems from cloud migration backlogs, ERP modernization cycles, and cyber-resilience mandates across government and private enterprises. Knowledge Process Outsourcing, although smaller, is projected to post a 10.22% CAGR, reflecting demand for real-time analytics, market research, and regulatory advisory services that support the country’s knowledge economy pivot. Engineering and ER&D lines are also rising as Operation 300bn directs factory automation, additive manufacturing, and digital-twin pilot work to local centers.

Advanced connectivity accelerates this functional shift. ADNOC’s USD 250 million AI-driven well digitalization program directs bespoke edge analytics work to engineering pods. Similar industrial IoT engagements create sustained use cases for private 5G labs, autonomous control algorithms, and predictive maintenance suites. As a result, the functional stack is moving up the value chain from transaction processing to high-impact design and build mandates, reinforcing the United Arab Emirates Global Capability Centers market as an engine of innovation rather than a cost-optimized back office.

By Engagement Model: Captives Retain Strategic Control

Captive facilities accounted for 58.85% of the 2025 United Arab Emirates Global Capability Centers market share, underscoring multinationals’ preference for direct oversight of strategic IP and regulated data sets. Free-zone statutes, most notably those allowing 100% foreign ownership and full profit repatriation, remove legacy barriers that once necessitated joint-venture workarounds. Large captives now handle core software platforms, risk-model calibration, and confidential R&D workflows that require strict governance.

Hybrid build-operate-transfer structures are the fastest-growing option, with a 10.05% CAGR, providing first-time entrants a graduated path to scale while mitigating start-up risk. Once staff levels and quality metrics stabilize, ownership reverts to the parent, locking in the long-term cost advantage. Pure BOT models still serve as beachheads for smaller firms that need proof-of-concept traction, yet the regulatory clarity around captives continues to steer the majority of new mandates toward direct-investment routes.

By Organization Size: SMEs Begin to Scale

Large enterprises dominated 2025 spending with 86.98% market share, a legacy of Fortune 500 offshoring paradigms that require deep benches and global process standards. Even so, the small and medium enterprise cohort is expanding at an 11.49% CAGR, signaling democratized access to offshore capability thanks to cloud-native toolsets and modular service catalogs. Government financing windows, including the AED 30 billion Emirates Development Bank program, cut capital hurdles and fund onboarding for mid-cap innovators.

SMEs leverage flexible seat arrangements in hubs such as Dubai Industrial City and Ras Al Khaimah Economic Zone to avoid premium downtown rents. Many start with ten- to twenty-person pods focused on DevOps or data science, then scale their headcount in step with global order books. This diffusion of demand widens the client base of the United Arab Emirates Global Capability Centers market, spreads talent risk, and encourages providers to launch tiered pricing models tailored to mid-market budgets.

By Industry Vertical: Healthcare Spearheads Growth

Banking, Financial Services, and Insurance accounted for 34.12% of 2025 revenue, driven by the rollout of real-time payments, the launch of digital banking, and stringent compliance updates from the Central Bank. Healthcare and Life Sciences, in contrast, is forecast to register a 10.71% CAGR, the fastest among tracked sectors, as the HELM cluster and USD 800 million of pharmaceutical capital expenditure demand data-rich pharmacovigilance, clinical-coding, and supply-chain analytics services. Manufacturing, Automotive, and industrial use cases gain further momentum from the AED 27.2 billion automotive roadmap, which commits to 7,000 skilled roles through 2030.

Vertical diversification reduces revenue cyclicality and positions the United Arab Emirates Global Capability Centers market for multi-sector resilience. Telco workloads tied to 5.5 G private networks feed OSS and BSS engineering queues, while retail platforms require last-mile analytics for cross-border e-commerce fulfillment. New economy lines, such as space technology, renewable energy, and circular polymers, round out the opportunity set and reinforce the nation’s shift toward a knowledge-based growth model.

Geography Analysis

Dubai remains the nucleus for premium finance and technology mandates. Firms gravitate to the Dubai International Financial Centre and the Dubai Internet City for direct access to financial regulators, venture investors, and connectivity that supports latency-sensitive workloads. Rising rents in these districts, however, prompt companies to deploy hub-and-spoke footprints, keeping client-facing teams in Grade-A towers while relocating back-office and engineering pods to lower-cost clusters, such as Dubai Silicon Oasis and Dubai South.

Abu Dhabi has emerged as the preferred base for engineering, ER&D, and advanced manufacturing centers. The emirate’s USD 2.7 billion industrial stimulus, paired with a goal of creating 13,600 skilled jobs by 2031, offers sizable grants, utility discounts, and streamlined licensing processes. Companies in the aerospace, hydrogen, and autonomous systems sectors have established design studios and prototyping labs within the Khalifa Industrial Zone, benefiting from proximity to port infrastructure and Masdar’s renewable energy testbeds.

The Northern Emirates, including Sharjah, Ajman, and Ras Al Khaimah, offer cost advantages and targeted industrial land, but still lack the mature vendor ecosystems found in the two largest cities. Shared-services maturity remains limited, constraining deployments that need complex legal, audit, and fintech service layers. Even so, state-backed transport upgrades and talent-mobility incentives are narrowing the readiness gap, positioning selected free zones to capture overflow demand as Dubai and Abu Dhabi approach saturation.

Competitive Landscape

Legacy Indian providers, including Tata Consultancy Services, Infosys, and Wipro, maintain strong footholds by leveraging standardized global delivery, automation assets, and cost-efficient talent pools. Their service catalogs, which were once focused on application maintenance, now include AI model governance, platform refactoring, and domain-specific accelerators that address Central Bank compliance and healthcare data privacy. Aggressive graduate intake pipelines enable these firms to scale quickly when new mandates are closed.

Global consultancies, such as Accenture, IBM, and Deloitte, lead complex digital transformation deals, leveraging proprietary frameworks and multicloud orchestration toolkits. Positioning shifts from pure advisory to managed services, so these players often establish hybrid centers that blend strategic blueprints with ongoing run-and-operate contracts. Their willingness to co-invest in industry sandboxes, especially in fintech and industrial IoT, lifts entry barriers for smaller competitors.

Hyperscalers, including AWS, Microsoft, Google, and Oracle, add a new competitive dimension by hiring thousands of AI engineers, solution architects, and DevOps specialists. Their localized cloud regions become both the substrate for client workloads and a magnet for top talent, tightening the labor market and inflating wage baselines. Niche players counter by specializing in high-barrier domains, such as synthetic-aperture radar design, green hydrogen process control, or circular-polymer analytics, areas where brand equity and domain expertise outweigh scale.

United Arab Emirates Global Capability Centers Industry Leaders

Tata Consultancy Services Limited

Accenture Plc

IBM Corporation

Cognizant Technology Solutions Corporation

Capgemini SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: The Abu Dhabi Investment Office introduced an automotive ecosystem program aimed at contributing AED 100 billion to the GDP by 2045 and creating 7,000 skilled jobs.

- January 2025: ADNOC issued a USD 250 million contract to digitize 2,000 wells via private 5 G networks and autonomous control systems.

- December 2024: Emirates Biotech unveiled a USD 218 million polylactic acid facility to achieve an annual output of 160,000 tonnes.

- December 2024: Space42 and ICEYE formed a joint venture to produce synthetic aperture radar satellites in the UAE.

United Arab Emirates Global Capability Centers Market Report Scope

The scope of the global capability center study for the market segmentation by the Function/Capability for (i) Information Technology (IT) and Digital Services segment is limited to Software Development, Cloud and Infrastructure Management, Cybersecurity, Data Analytics and AI/ML; (ii) Engineering / ER&D segment is limited to Product Design and Testing, Embedded Systems, Digital Twin / Simulation; (iii) Business Process Management (BPM) segment is limited to Finance and Accounting, HR, Payroll and Talent Management, Procurement, Customer Service; and (iv)Knowledge Process Outsourcing (KPO) segment is limited to Market Research and Insights, Risk and Compliance, Legal and Regulatory Support, Strategy and Consulting Support. Similarly, for segmentation by the Engagement Model, scope for (i) Hybrid Build-Operate-Transfer (BOT) is limited to Joint Venture / Strategic Partnership and Virtual Captive Model. The rest of the segment scope is as specified for the listed segment.

| Information Technology (IT) and Digital Services |

| Engineering / ER&D |

| Business Process Management (BPM) |

| Knowledge Process Outsourcing (KPO) |

| Captive (Self-Build)/ In-house |

| Build-Operate-Transfer (BOT) |

| Hybrid Build-Operate-Transfer (BOT) |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Banking, Financial Services, and Insurance (BFSI) |

| Telecom and IT |

| Healthcare and Life Sciences |

| Manufacturing, Automotive and Industrial |

| Retail and Consumer Goods |

| Other Industry Verticals |

| By Function / Capability | Information Technology (IT) and Digital Services |

| Engineering / ER&D | |

| Business Process Management (BPM) | |

| Knowledge Process Outsourcing (KPO) | |

| By Engagement Model | Captive (Self-Build)/ In-house |

| Build-Operate-Transfer (BOT) | |

| Hybrid Build-Operate-Transfer (BOT) | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises (SMEs) | |

| By Industry Vertical | Banking, Financial Services, and Insurance (BFSI) |

| Telecom and IT | |

| Healthcare and Life Sciences | |

| Manufacturing, Automotive and Industrial | |

| Retail and Consumer Goods | |

| Other Industry Verticals |

Key Questions Answered in the Report

How big was the United Arab Emirates Global Capability Centers market in 2026?

It reached USD 5.74 billion, underpinned by zero-tax incentives and advanced digital infrastructure.

What CAGR is forecast for UAE capability centers through 2031?

The market is projected to grow at a 9.8% CAGR, taking value to USD 9.16 billion by 2031.

Which function currently holds the largest revenue share?

Information Technology and Digital Services accounts for 50.92% of 2025 revenue, reflecting significant adoption of cloud and AI technologies.

Why are captives preferred over outsourced models in the UAE?

Free-zone rules grant 100% foreign ownership, allowing multinationals to safeguard IP and regulatory compliance while enjoying tax relief.

Which vertical is expected to expand fastest?

The Healthcare and Life Sciences sector is projected to post a 10.71% CAGR, fueled by the HELM cluster and pharmaceutical investments exceeding USD 800 million.

How are rising Dubai rents affecting capability center strategies?

Firms are adopting hub-and-spoke footprints, placing high-visibility units in premium districts and back-office roles in lower-cost zones to maintain competitiveness.

Page last updated on: