United Arab Emirates Customer Data Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

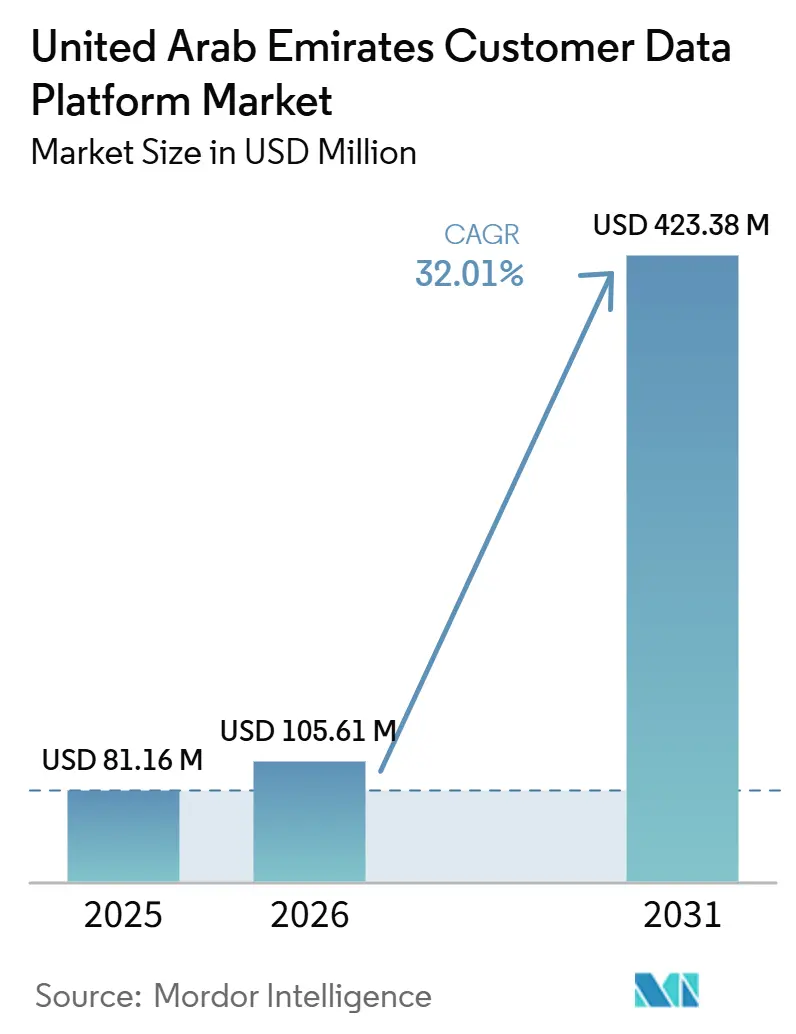

| Base Year Market Size (2025) | USD 81.16 Million |

| Market Size (2026) | USD 105.61 Million |

| Market Size (2031) | USD 423.38 Million |

| Growth Rate (2026 - 2031) | 32.01% CAGR |

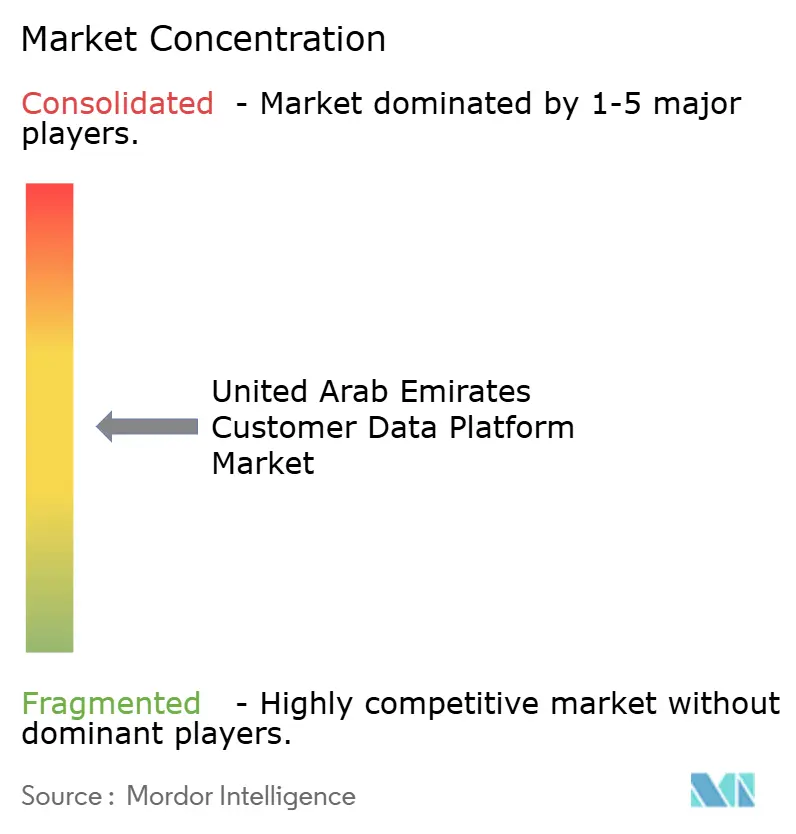

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates Customer Data Platform Market Analysis by Mordor Intelligence

The United Arab Emirates customer data platform market size was valued at USD 81.16 million in 2025 and estimated to grow from USD 105.61 million in 2026 to reach USD 423.38 million by 2031, at a CAGR of 32.01% during the forecast period (2026-2031). The United Arab Emirates customer data platform market is moving ahead on the back of stricter consent rules, stronger demand for first-party data, and wider use of AI-led customer engagement across large enterprises. The shift away from third-party tracking has made unified customer records more valuable for brands that need better targeting, stronger retention, and cleaner activation across channels. Local cloud infrastructure has also reduced a major adoption barrier because enterprises can now keep sensitive data within UAE borders while still using global platform capabilities. Competition remains active because large global vendors are expanding local ecosystems, while regional and specialist players are trying to win demand tied to bilingual deployment, loyalty data use, and sector-specific workflows. Growth still faces friction from integration complexity, higher delivery costs, and shortages in AI and data engineering talent, but the commercial direction of the United Arab Emirates customer data platform market remains favorable.

Key Report Takeaways

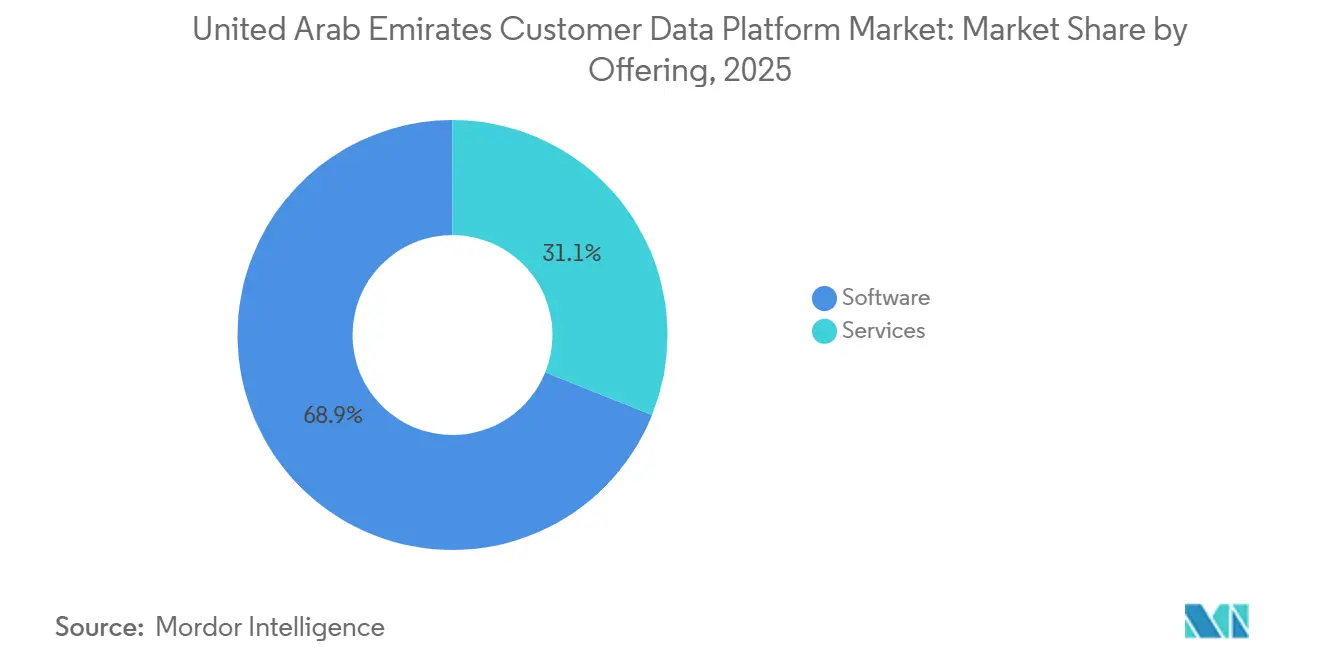

- By offering, software held 68.93% of the United Arab Emirates customer data platform market in 2025, while services are projected to expand at a 34.66% CAGR through 2031.

- By deployment mode, cloud accounted for 72.84% of the United Arab Emirates customer data platform market in 2025 and is also expected to record the fastest growth at a 33.89% CAGR through 2031.

- By organization size, large enterprises held 66.49% share in 2025, while SMEs are projected to grow at a 35.27% CAGR through 2031.

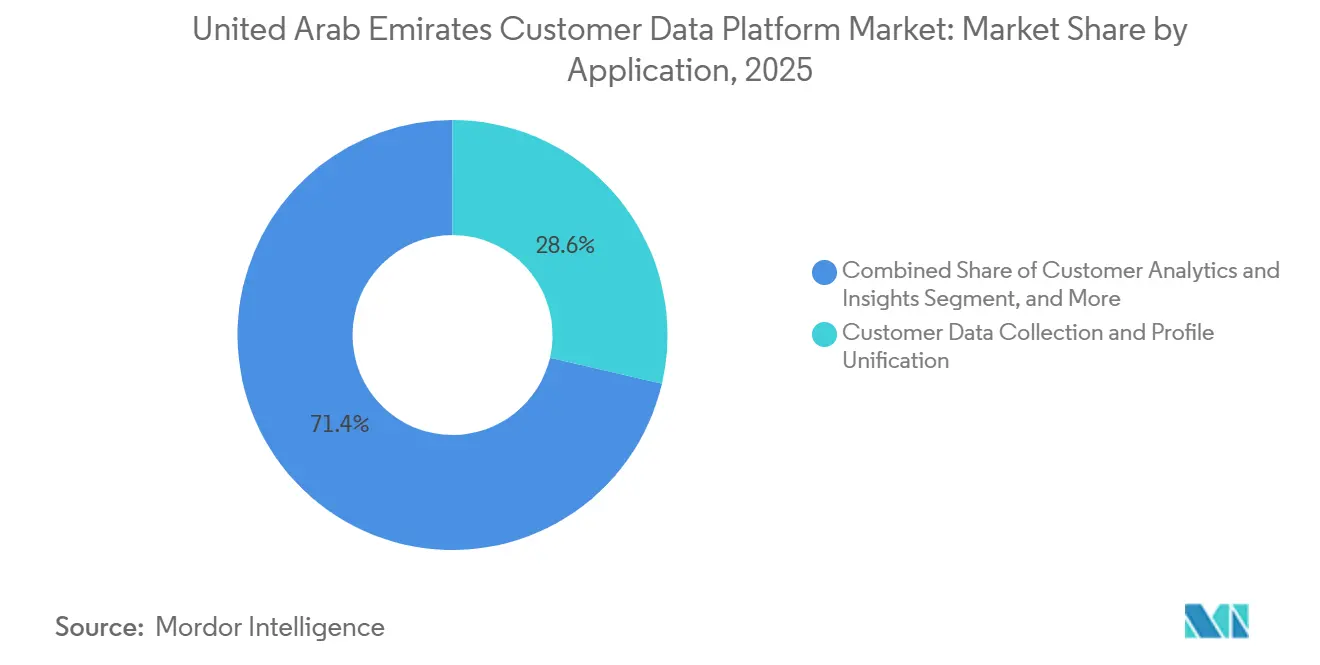

- By application, customer data collection and profile unification accounted for 28.64% of the market share in 2025, while audience segmentation and personalization are projected to expand at a 36.11% CAGR through 2031.

- By end-user industry, Retail and E-Commerce held 26.57% of the United Arab Emirates customer data platform market share in 2025, while the same segment is expected to post the fastest growth at a 34.79% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Arab Emirates Customer Data Platform Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising Demand for First-Party Data Activation | +6.5% | UAE-wide, with concentrated impact in Dubai and Abu Dhabi digital commerce hubs | Short term (≤ 2 years) |

| Retail and E-Commerce Personalization Requirements | +5.8% | UAE-wide, particularly Dubai retail corridors and cross-border e-commerce | Short term (≤ 2 years) |

| Cloud-Native Enterprise Architecture Adoption | +5.2% | UAE-wide, early adoption concentrated in free zones and regulated sectors | Medium term (2-4 years) |

| AI-Powered Customer Journey Orchestration | +4.9% | UAE-wide, with strongest uptake in BFSI, retail, and telecom | Medium term (2-4 years) |

| Expansion of Omnichannel Loyalty Programs | +3.6% | UAE-wide, with cross-sector spillover to hospitality and fuel retail | Medium term (2-4 years) |

| Privacy-By-Design Customer Identity Management | +3.2% | UAE-wide, amplified in ADGM and DIFC jurisdictions with distinct data frameworks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for First-Party Data Activation

The removal of third-party tracking support has pushed brands in the United Arab Emirates customer data platform market toward owned customer data as the main source of targeting precision and audience control. This shift matters more in the UAE because brands often serve customers across many nationalities, languages, and purchase patterns, which makes generic audience pools less useful than unified first-party profiles. The PDPL has also made consent-aware data collection a formal operating requirement rather than a discretionary marketing choice, which raises the value of platforms that can unify identity data with permission controls built into the data model.[1]UAE Government, “Personal Data Protection Law - Federal Decree-Law No. 45 of 2021,” UAE AI Office, ai.gov.ae The result is that vendors in the United Arab Emirates customer data platform market are being measured against real deployment outcomes, not only against feature lists or campaign promises. This is also why clean-room collaboration, retailer data use, and direct profile ownership are becoming central to brand data strategy in the country.

Retail and E-Commerce Personalization Requirements

Retail demand continues to shape the commercial center of the United Arab Emirates customer data platform market because personalization is closely tied to conversion, repeat purchase, and loyalty economics. Research published in 2026 confirmed a positive statistical relationship between AI-powered personalization and consumer engagement in the UAE e-commerce sector, which gives retailers stronger justification for data unification and real-time segmentation investment.[2]Emad Masoud et al., “The Impact Of AI-Powered Personalization On Consumer Engagement: Evidence From The UAE E-Commerce Sector,” Strategic Business Research, doi.org The operating challenge is not limited to basic recommendation engines because UAE retailers often need to recalibrate campaigns quickly around peak shopping periods and bilingual audience behavior. That makes centralized customer records, event-level signals, and fast audience recomposition more useful than disconnected point tools. The United Arab Emirates customer data platform market is therefore benefiting from a retail environment where measurable engagement gains are pushing data architecture decisions closer to revenue priorities.

Cloud-Native Enterprise Architecture Adoption

Cloud deployment already dominates the United Arab Emirates customer data platform market, and that position has strengthened because local infrastructure now supports data residency needs that once delayed adoption. Salesforce activated Hyperforce infrastructure in the UAE, which made local hosting of Customer 360 and Data Cloud capabilities more workable for organizations that must align with domestic privacy obligations. This matters because regulated sectors and large enterprises want faster activation without exposing sensitive customer records to cross-border transfer concerns. At the same time, many enterprises still depend on legacy Oracle and SAP environments, so the strongest demand is going to vendors that can connect modern cloud systems with older operational stacks. That hybrid need keeps the United Arab Emirates customer data platform market open to providers that can handle both speed and integration depth.

AI-Powered Customer Journey Orchestration

AI use is advancing quickly, but the United Arab Emirates customer data platform market is growing because customer-facing AI still depends on well-structured data beneath it. SAP Emarsys reported in September 2025 that 82% of UAE marketers viewed AI as central to personalization, yet only 31% of consumers felt brands were actually personalizing content to their needs. The same release showed that many marketers still struggle to turn available data into usable activation, which keeps identity resolution and audience readiness at the center of platform selection. This gap is why journey orchestration is moving beyond campaign automation toward real-time decisioning across service, media, and commerce environments. Vendors with stronger profile stitching, consent visibility, and activation connectors are therefore better placed to capture the next phase of the United Arab Emirates customer data platform market.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Fragmented Legacy Data Architectures in Large Enterprises | -3.8% | UAE-wide, most acute in government-linked entities and diversified conglomerates | Medium term (2-4 years) |

| High Implementation and Integration Cost Burden | -3.2% | UAE-wide, disproportionately constrains SMEs and mid-market firms | Short term (≤ 2 years) |

| Data Residency and Consent Management Complexity | -2.5% | UAE-wide, amplified in ADGM and DIFC with jurisdiction-specific frameworks | Long term (≥ 4 years) |

| Shortage of Reverse ETL and CDP-Specific Talent | -2.1% | UAE-wide, hiring pressure highest in Dubai and Abu Dhabi tech corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Legacy Data Architectures in Large Enterprises

Large enterprises remain important buyers in the United Arab Emirates customer data platform (CDP) market. However, many continue to rely on legacy ERP, CRM, and transactional systems that were not designed to support real-time customer profile unification. This creates slow and complex integration processes, as data often remains dispersed across multiple operational layers, with inconsistent identifiers and incompatible schemas. Such fragmentation can extend implementation timelines, create ambiguity around internal ownership, and make it difficult for enterprises to justify the expected ROI during budget approvals. Although the United Arab Emirates CDP market continues to show strong growth potential, vendors that underestimate the level of pre-deployment data architecture work required may experience slower expansion and limited traction within enterprise accounts.

High Implementation and Integration Cost Burden

Cost remains a practical brake on the United Arab Emirates customer data platform market because platform fees are only one part of the total deployment burden. Implementation often requires data engineers, middleware work, consent mapping, and integration support that adds recurring expense beyond the initial software contract. CDP.com estimated that operating a composable CDP can require 3 to 5 dedicated data engineers, translating into annual staffing costs of USD 450,000 to USD 1 million before licensing. In the UAE, where AI, cloud, and machine learning talent remains tight, these delivery costs can rise further and weigh more heavily on mid-market firms. The result is a two-speed market where large enterprises move ahead with full deployments while smaller firms often delay adoption or rely on narrower point solutions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Gain Momentum as Delivery Complexity Increases

Software remained the leading offering in 2025 with a 68.93% share, which showed that most buyers still preferred packaged capabilities over internal builds. This concentration reflected enterprise demand for ready-made profile unification, segmentation, and activation functions that can be deployed faster than fully custom systems. Large UAE organizations also favored vendor-backed platforms because they reduce internal product development risk and create clearer procurement paths. That made software the revenue anchor of the United Arab Emirates customer data platform market in 2025.

Services, however, are projected to grow faster at a 34.66% CAGR through 2031, which shows that delivery complexity is rising across the United Arab Emirates customer data platform market. Enterprises now need more help with ERP integration, bilingual data normalization, consent configuration, and ongoing managed operations. Outcome-based service models are also becoming more relevant because buyers want execution accountability tied to activation milestones rather than only billable hours. As platform features narrow across top vendors, service quality is becoming a stronger differentiator for the United Arab Emirates customer data platform industry.

By Deployment Mode: Cloud Leads on Scale and Growth

Cloud accounted for 72.84% of the United Arab Emirates customer data platform market size in 2025, and it is also projected to record the fastest growth at a 33.89% CAGR through 2031. This dual position is unusual and points to a market where compliance and scalability are increasingly being addressed in the same deployment model. On-premises systems continue to matter in some government-linked and regulated environments, while hybrid models remain relevant for organizations that still depend on older operational stacks. Even so, the cloud has become the default direction of the United Arab Emirates customer data platform market.

The main reason is that sovereign and locally hosted cloud infrastructure has reduced the risk attached to cross-border data exposure. Salesforce Hyperforce in the UAE and local hyperscale infrastructure have made it easier for enterprises to use global CDP functionality while keeping deployment aligned with domestic privacy expectations.[3]Salesforce, “Salesforce Hyperforce: Public Cloud Infrastructure In UAE,” Salesforce, salesforce.com The UAE Central Bank’s sovereign financial cloud initiative with Core42 also showed that even regulated financial environments are moving toward cloud-based analytics and data services. For vendors, the opportunity is not only in pure cloud contracts but also in architectures that can bridge local compliance, older enterprise systems, and real-time activation needs. That keeps cloud at the center of the United Arab Emirates customer data platform market while preserving room for hybrid deployment specialists.

By Organization Size: Large Enterprises Hold Revenue While SMEs Expand Faster

Large enterprises held 66.49% of the market in 2025, which kept revenue concentrated among organizations with larger budgets, longer buying cycles, and broader customer data estates. Airlines, banks, telecom operators, and large retail groups continue to set the tone because their data complexity makes unified identity and orchestration more commercially valuable. flydubai’s January 2026 selection of Amperity to unify passenger data across check-in, in-flight recognition, service, and marketing systems showed the scale at which enterprise deployments are now being pursued. This enterprise concentration remains a defining feature of the United Arab Emirates customer data platform market.

SMEs are projected to expand faster at a 35.27% CAGR through 2031, which points to widening demand beyond the top corporate tier. Lower SaaS entry points, national digitalization support, and stronger proof of return from loyalty-linked personalization are helping smaller firms enter the market. GCC data showing that 67% of SMBs now use at least one SaaS application, up from 41% in 2022, supports the view that software adoption barriers are easing across the region. Still, smaller firms need quicker onboarding, simpler data preparation, and lighter integration requirements than enterprise buyers. Vendors that address those needs well are likely to widen their reach across the United Arab Emirates customer data platform market over the forecast period.

By Application: Profile Unification Anchors Spending While Personalization Accelerates

Customer data collection and profile unification accounted for 28.64% of the United Arab Emirates customer data platform market size in 2025, which confirms that most deployments still begin with foundational data assembly and identity work. This layer remains essential because downstream analytics, segmentation, and journey activation all depend on a stable customer record. Marketing campaign orchestration, customer analytics, consent management, and related applications continue to build on top of that base. As a result, profile unification remains the first commercial step for many buyers in the United Arab Emirates customer data platform market.

Audience segmentation and personalization are projected to grow at a 36.11% CAGR through 2031, which makes it the fastest-moving application area in the forecast period. Checkout.com reported in 2026 that 54% of UAE shoppers were comfortable allowing AI assistants to shop on their behalf, which suggests that personalization is expanding into new forms of assisted and autonomous commerce. That change increases the need for real-time segmentation, low-latency activation, and consent-aware audience logic across channels. Consent and preference management is also becoming more strategically important as PDPL enforcement expectations mature and brands need auditable permission records inside the customer model. This is pushing the United Arab Emirates customer data platform industry toward faster architecture upgrades and stronger event-driven activation capability.

By End-User Industry: Retail and E-Commerce Leads on Both Share and Growth

Retail and E-Commerce held 26.57% of the United Arab Emirates customer data platform market share in 2025, and it is also projected to expand at a 34.79% CAGR through 2031. This combined leadership reflects a sector where personalization directly affects basket value, loyalty performance, and repeat purchase behavior. The UAE retail environment includes large franchise networks, hypermarkets, loyalty ecosystems, and digital-first commerce brands, all of which create rich customer data flows. That keeps Retail and E-Commerce at the forefront of the United Arab Emirates customer data platform market.

The practical use case set is also widening quickly. Max Fashion’s June 2026 launch of Google Cloud’s Virtual Try-On API in the UAE showed how AI-led experience layers are being brought into day-to-day retail engagement. BFSI remains the second-largest end-user segment as financial institutions look for better customer intelligence across cross-sell, fraud, and KYC modernization. The UAE Central Bank’s move to develop a unified digital e-KYC platform also supports demand for centralized identity and customer data architecture in financial services. Healthcare, telecom, media, manufacturing, and government also add demand, especially where unified records support service coordination and compliant data use. The Ministry of Health and Prevention’s Enterprise Data Warehouse and Bayan disease registry program reflects a similar institutional preference for unified data environments.[4]Ministry Of Health And Prevention UAE, “Emirates Health Platform Continues Participation At World Health Expo 2026 - MoHAP Showcases Enterprise Data Warehouse And National Disease Registry System ‘Bayan,’” Ministry Of Health And Prevention UAE, mohap.gov.ae

Geography Analysis

The UAE held the leading position in the Middle East customer data platform landscape, which keeps the United Arab Emirates customer data platform market at the center of regional adoption. This position is supported by strong digital infrastructure, broad internet and smartphone use, and a national policy environment that links AI adoption with economic modernization. The UAE National AI Strategy 2031 has reinforced the need for data systems that can support automation, profiling, and customer-facing intelligence across sectors. The country’s loyalty ecosystem also gives the United Arab Emirates customer data platform market unusually strong first-party data depth, especially in retail and fuel-linked consumer programs.

Dubai and Abu Dhabi remain the main commercial hubs for deployment, but they show different demand patterns inside the United Arab Emirates customer data platform market. Dubai supports high activity across retail, travel, hospitality, e-commerce, and fintech, which favors platforms built for rapid segmentation and omnichannel activation. Abu Dhabi shows a stronger pull from government-linked entities, regulated finance, and large institutions that need tighter auditability and formal consent controls. The ADGM data protection update in September 2025 added more jurisdiction-specific precision to how organizations operating in that perimeter manage consent and data use. This split means vendors need both growth-oriented activation capability and more formal governance support to scale across the country.

Across the emirates, SMEs are becoming a larger addressable base as cloud software becomes easier to adopt and national digitalization programs widen technology use. UAE demand is also supported by vendor localization efforts that combine local data handling with direct enterprise engagement. Tealium’s collaboration with AWS, formalized at GITEX Global 2025 in Dubai, illustrated how vendors are using UAE-based infrastructure commitments to strengthen trust, latency performance, and compliance readiness. This approach should help the United Arab Emirates customer data platform market keep expanding across both enterprise and emerging mid-market accounts.

Competitive Landscape

The United Arab Emirates customer data platform market is moderately concentrated at the top, but it remains fragmented beyond the first tier. Adobe, Salesforce, and Oracle continue to compete for large enterprise mandates, while specialist and regional vendors pursue SME demand, narrower use cases, and localized delivery models. This keeps pricing pressure active and shortens the life of simple feature-led differentiation. It also means the United Arab Emirates customer data platform market is being shaped as much by ecosystem depth and deployment capability as by core platform functionality.

Large vendors are increasingly using partnerships and infrastructure commitments to deepen their position. Adobe expanded its agentic partner ecosystem in April 2026 and linked that effort with system integrators that can package Adobe Experience Platform capabilities into sector-ready implementations.[5]Adobe Inc., “Adobe Unveils CX Enterprise Coworker To Build Agentic-Enabled Workflows For Customer Experience Orchestration,” Adobe Newsroom, adobe.com Salesforce also extended its regional positioning through Headless 360 and its UAE Hyperforce footprint, which pushed its role closer to API-led customer data infrastructure rather than only front-end CRM delivery. Tealium’s localized AWS alignment shows how mid-tier vendors are using trusted infrastructure partnerships to compete for enterprises that want regional data handling and faster activation. These moves are raising the execution bar across the United Arab Emirates customer data platform market.

Competitive white space still exists, especially around bilingual configuration, Arabic-language consent experiences, and identity logic tuned to local customer behavior. Composable architectures are also appealing to engineering-led organizations that already run modern cloud data stacks and want activation without full traditional suite licensing. BlueConic’s June 2026 acquisition of Blueshift showed the opposite path, with one vendor trying to combine behavioral context, AI decisioning, and multi-channel execution in a single environment. That leaves the United Arab Emirates customer data platform market open to both consolidation and specialization over the next few years.

United Arab Emirates Customer Data Platform Industry Leaders

Adobe Inc.

Salesforce, Inc.

Oracle Corporation

SAP SE

Tealium, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: BlueConic acquired Blueshift, an AI-powered cross-channel marketing platform, creating a closed-loop solution that combines first-party behavioral data capture, AI decisioning, and owned-channel execution (email, SMS, push, in-app, web) within a single CDP architecture. The acquisition directly addresses the "data-to-action" gap that constrains personalization at scale for B2C brands in the UAE retail and travel sectors.

- June 2026: Rokt mParticle launched its Performance Engine, led by an Audience Agent that converts first-party data into measurable revenue lift for global enterprises. The product targets the UA CDP use case of translating unified profiles into high-performing paid media audiences, a capability gap that UAE retail and e-commerce operators have highlighted as a critical unmet need.

- June 2026: Adobe released CX Enterprise Coworker as a generally available product, an agentic AI solution that automates customer experience orchestration workflows across Adobe Experience Platform, Real-Time Customer Data Platform, Customer Journey Analytics, and Journey Optimizer. Built on open standards including Model Context Protocol (MCP) and Agent2Agent (A2A), the product is designed to interoperate with AI infrastructure from AWS, Google Cloud, Microsoft, and Anthropic.

- April 2026: Salesforce launched Headless 360 in the Middle East, exposing the full depth of Salesforce capabilities, including Data Cloud, as APIs, MCP tools, and CLI commands for AI agent consumption. The launch marks a strategic repositioning of Salesforce's UAE platform from CRM interface to agentic data infrastructure, enabling autonomous AI workflows without human UI navigation.

- February 2026: The UAE Central Bank and Abu Dhabi-based AI company Core42 announced the development of a sovereign financial cloud infrastructure, designed to support AI-powered real-time analytics, multi-cloud management, and data protection for licensed financial institutions. The initiative is accompanied by new CBUAE guidelines for responsible AI and machine learning use by financial institutions.

United Arab Emirates Customer Data Platform Market Report Scope

The United Arab Emirates customer data platform market refers to platforms and services that help organizations consolidate customer data from multiple sources into unified, centralized profiles. These solutions support identity resolution, real-time data integration, segmentation, personalization, and analytics, enabling enterprises to deliver consistent omnichannel customer experiences. The market is driven by rapid digital transformation across retail, banking, telecom, and government services, along with the growing adoption of AI-powered personalization and increasing compliance requirements related to data privacy regulations. As a result, CDPs are becoming a critical component of the UAE’s smart economy initiatives.

The United Arab Emirates Customer Data Platform Market Report is Segmented by Offering (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid) Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Customer Data Collection and Profile Unification, Audience Segmentation and Personalization, Marketing Campaign and Customer Journey Orchestration, Customer Analytics and Insights, Consent and Preference Management, and Other Applications), and End-User Industry (Retail and E-Commerce, Banking, Financial Services, and Insurance (BFSI), Healthcare and Life Sciences, IT and Telecom, Media and Entertainment, Industrial Manufacturing, Government and Public Administrationm and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization |

| Marketing Campaign and Customer Journey Orchestration |

| Customer Analytics and Insights |

| Consent and Preference Management |

| Other Applications |

| Retail and E-Commerce |

| Banking, Financial Services, and Insurance (BFSI) |

| Healthcare and Life Sciences |

| IT and Telecom |

| Media and Entertainment |

| Industrial Manufacturing |

| Government and Public Administration |

| Other End-User Industries |

| By Offering | Software |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization | |

| Marketing Campaign and Customer Journey Orchestration | |

| Customer Analytics and Insights | |

| Consent and Preference Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| Banking, Financial Services, and Insurance (BFSI) | |

| Healthcare and Life Sciences | |

| IT and Telecom | |

| Media and Entertainment | |

| Industrial Manufacturing | |

| Government and Public Administration | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the size outlook for the United Arab Emirates Customer Data Platform market?

The United Arab Emirates Customer Data Platform market size was USD 81.16 million in 2025, reached USD 105.61 million in 2026, and is forecast to hit USD 423.38 million by 2031 at a 32.01% CAGR.

Which deployment model leads customer data platform adoption in the UAE?

Cloud leads adoption, with 72.84% share in 2025, and it is also the fastest-growing deployment mode with a 33.89% CAGR through 2031.

Which end-user sector is driving the strongest demand in the UAE?

Retail and E-Commerce leads both on scale and momentum, with 26.57% share in 2025 and a projected 34.79% CAGR through 2031.

Why are UAE companies investing more in customer data platforms?

Demand is rising because brands need first-party data, better consent management, stronger personalization, and cleaner AI-ready customer profiles across channels.

What application area is expanding the fastest in the UAE customer data platform space?

Audience segmentation and personalization is the fastest-growing application, with a projected 36.11% CAGR from 2026 to 2031.

What is the main challenge slowing wider deployment across the UAE?

The main barriers are legacy system integration, high implementation cost, and tight availability of specialized AI and data engineering talent.

Page last updated on: