United Arab Emirates Corrugated Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

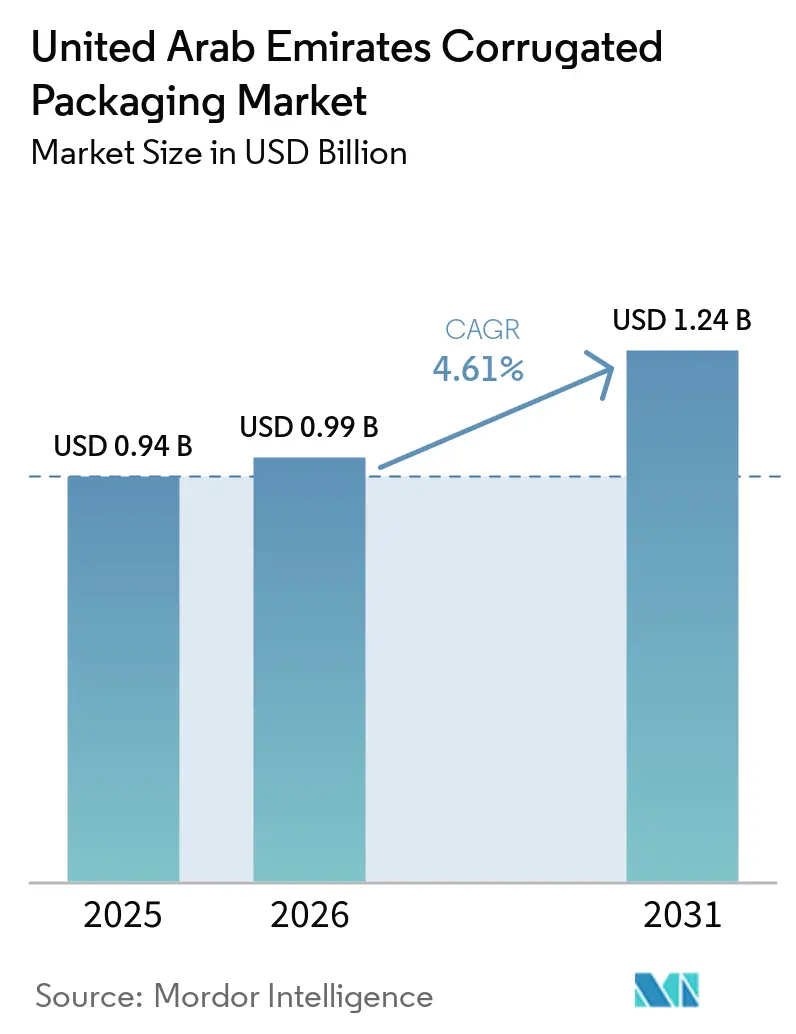

| Base Year Market Size (2025) | USD 0.94 Billion |

| Market Size (2026) | USD 0.99 Billion |

| Market Size (2031) | USD 1.24 Billion |

| Growth Rate (2026 - 2031) | 4.61% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates Corrugated Packaging Market Analysis by Mordor Intelligence

The United Arab Emirates corrugated packaging market size was valued at USD 0.94 billion in 2025 and estimated to grow from USD 0.99 billion in 2026 to reach USD 1.24 billion by 2031, at a CAGR of 4.61% during the forecast period (2026-2031). The measured growth reflects the country’s evolution from an oil-linked trading post into a diversified logistics and light-manufacturing hub where corrugated packaging supports food re-exports, electronics nearshoring, and omnichannel retail. Capacity additions in recycled containerboard mills, government subsidies for bio-barrier coatings, and the 2026 ban on single-use plastics collectively redirect demand toward fiber-based formats. Shifts in linerboard mix show a bifurcation: premium exporters insist on virgin kraft while domestic fast-moving goods absorb recycled grades. Competitive intensity is rising as global players enter through acquisitions that bundle heavy-duty expertise with sustainability credentials.

Key Report Takeaways

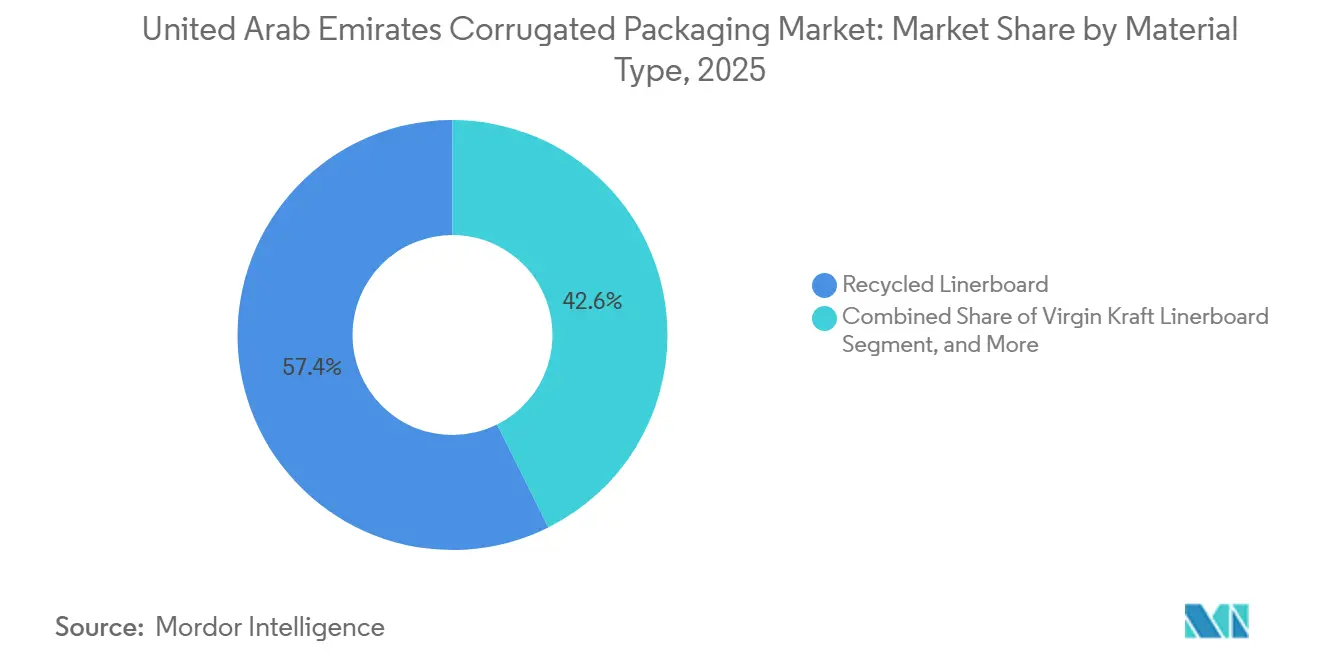

- By material type, the recycled linerboard segment captured 57.36% of the United Arab Emirates corrugated packaging market share in 2025.

- By flute type, the United Arab Emirates corrugated packaging market size for f flute is projected to grow at an 6.14% CAGR through 2031.

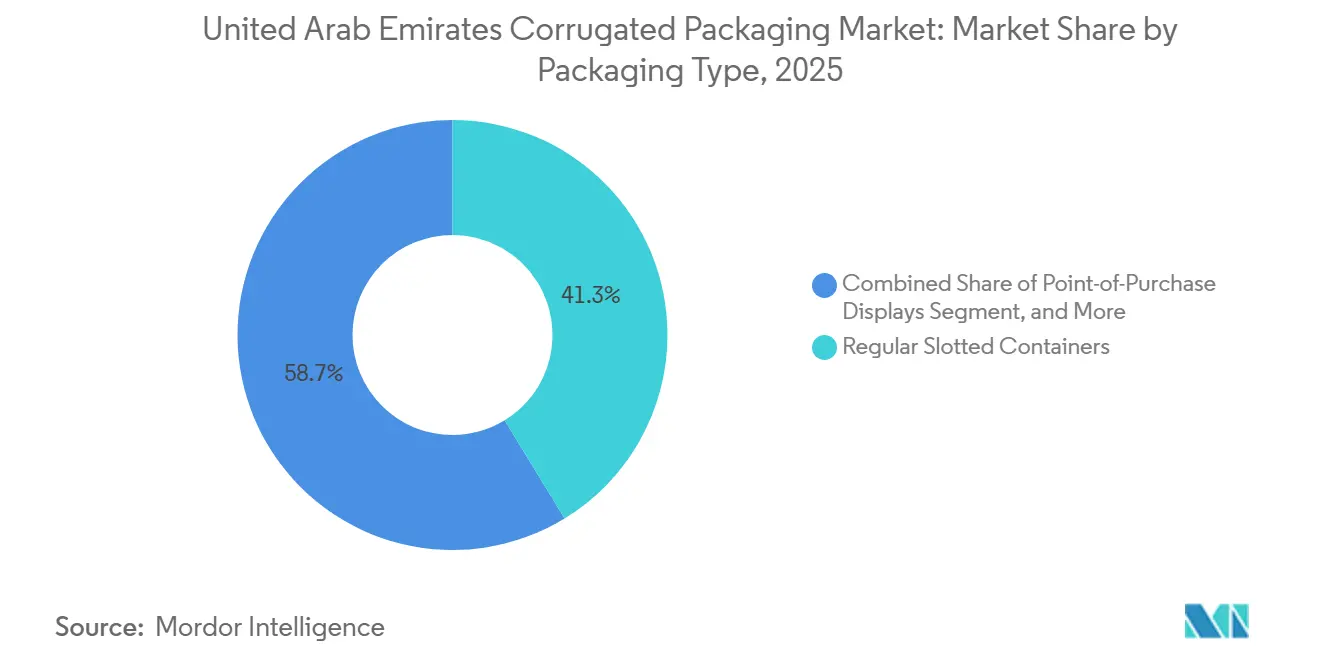

- By packaging type, the regular slotted containers segment captured 41.27% of the United Arab Emirates corrugated packaging market share in 2025.

- By wall type, the United Arab Emirates corrugated packaging market size for double-wall is projected to grow at an 5.15% CAGR through 2031.

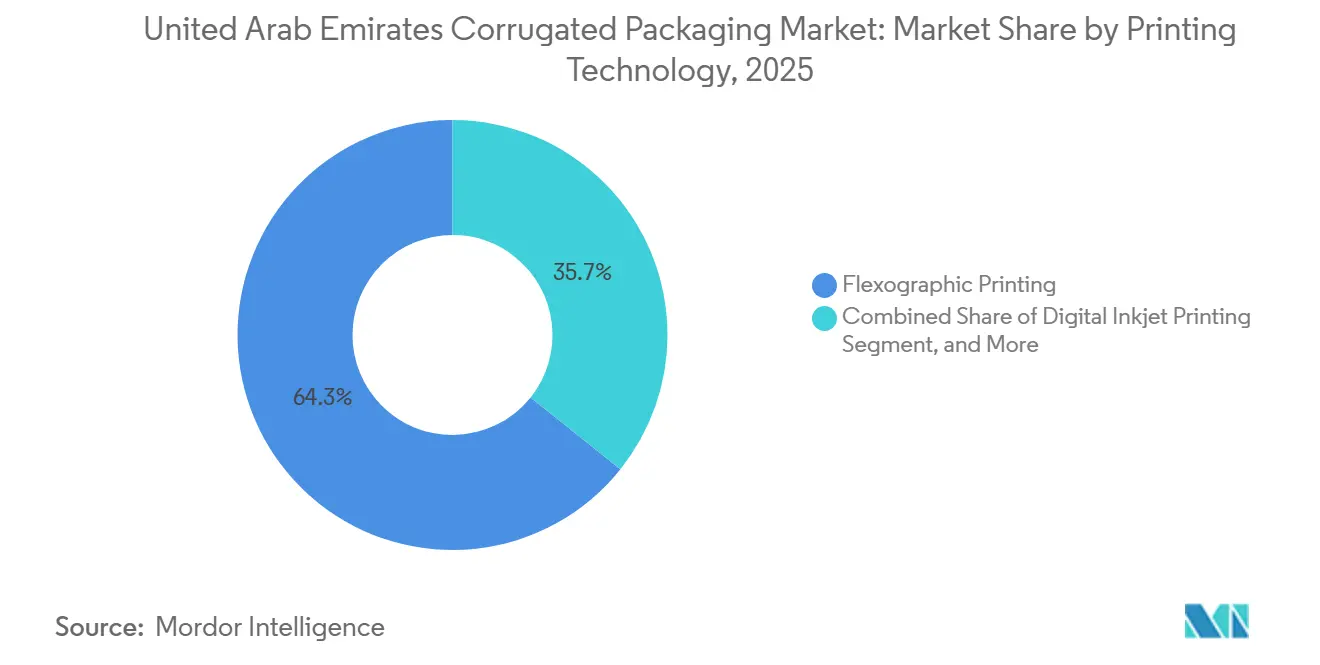

- By printing technology, the flexographic printing segment captured 64.27% of the United Arab Emirates corrugated packaging market share in 2025.

- By end-user industry, the United Arab Emirates corrugated packaging market size for e-commerce fulfillment centers is projected to grow at an 5.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Arab Emirates Corrugated Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising E-commerce Logistics Acceleration | +1.8% | Global focus, early gains in Dubai, Abu Dhabi, Sharjah | Medium term (2-4 years) |

| Growth in Processed Food and Beverage Exports | +1.2% | National, KEZAD and Jebel Ali Free Zone | Medium term (2-4 years) |

| Regulatory Shift Toward Recyclable Packaging | +1.0% | National, aligned with UAE Net Zero 2050 | Long term (≥4 years) |

| Nearshoring-Led Electronics Output | +0.7% | APAC spill-over into UAE free zones | Medium term (2-4 years) |

| Craft-Brewery Demand for Custom Boxes | +0.3% | National, limited to licensed venues | Short term (≤2 years) |

| Government Subsidies for Bio-Based Coatings | +0.5% | National pilot zones | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising E-Commerce Logistics Acceleration

Dubai’s Logistics Corridor reduces sea-to-air transfer times by 40%, enabling cross-border merchants to promise same-day delivery to Gulf buyers. Smaller, more fragmented parcel sizes lift unit-level packaging intensity, while brand owners migrate to digitally printed mailers that double as marketing canvases. Fulfillment centers consumed 180 million m² of corrugated board in 2025, and volume is rising at 5.24% annually as Dubai and Abu Dhabi cement their last-mile leadership. ISO 12647-2 print compliance has become an entry ticket for converters serving multinational platforms, favoring plants with inline inkjet lines over legacy flexo assets.

Growth in Processed Food and Beverage Exports

Free-zone processors aggregate raw ingredients, retort or chill-fill them, and then ship finished SKUs to shelves in the Middle East and North Africa. Corrugated shippers must survive humid Red Sea legs while flaunting recycled logos to satisfy European retailers. Union Paper Mills’ carton-to-linerboard line recycles 10,000 tons annually, providing local circular fiber for food packaging. Labeling laws mandating tamper-evidence and traceability codes are driving demand for litho-laminated graphics that integrate QR codes.

Regulatory Shift Toward Recyclable Packaging

The plastic bag and EPS ban, effective January 2026, redirects take-out meals, produce trays, and quick-service drink carriers into fiber substrates. Brands chasing early compliance are locking in packaging lines with Forest Stewardship Council or Program for the Endorsement of Forest Certification chain-of-custody audits, raising supplier barriers. Hotpack Global’s portfolio reached 97% of its items are recyclable or compostable, helping it clinch retailer contracts as the single-use cut-off approaches. Municipal targets of 75% landfill diversion by 2030 incentivize segregation of used corrugated, creating a steadier domestic bale stream for mills.

Nearshoring-Led Electronics Output

VVDN Technologies expanded its Dubai plant in 2025 to produce routers and IoT devices for Western brands, tightening local demand for triple-wall anti-static packaging.[1]VVDN Technologies, “VVDN Expands Dubai Facility for Electronics Manufacturing,” vvdntech.com Free-zone assemblers cut end-to-end lead times by up to 12 days compared with direct China-to-Europe lanes, and they pay premium rates for moisture-barrier liners to defend against warranty claims. International Electrotechnical Commission electrostatic discharge norms are now embedded in bid specs, so converters with conductive inserts or ionization-treated liners enjoy a price premium.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recycled Paper Price Volatility | -0.9% | Global, acute in the UAE | Short term (≤2 years) |

| Competition of Returnable Plastic Crates | -0.6% | National fresh produce channels | Medium term (2-4 years) |

| Water-Scarcity Constraints on Mills | -0.4% | National, all mills | Long term (≥4 years) |

| Dependence on Imported Virgin Fiber | -0.3% | Global supply chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Recycled Paper Price Volatility

Recovered paper imports swing with freight costs and exporter policy shifts, and mixed-grade containerboard ranged USD 110-145 tons (-35/ +32%) in 2024-2025. Short-term spikes force converters into tense quarterly renegotiations, while limited hedging tools in the region transfer risk downstream. Star Paper Mill’s new 135,000-ton plant hopes to source 80% from domestic waste, yet local recovery sits at 35-40%, leaving mills exposed to imported bales

Competition from Returnable Plastic Crates

Large grocers run closed-loop produce circuits using reusable high-density polyethylene crates, lowering per-trip costs by up to 50% over 80 rotations. Because the plastic ban exempts multi-use formats, fiber shippers lose on durability in chilled chains. Corrugators answer with waxed or water-based barrier boxes that last three to five trips and partner with 3PLs for take-back and recycling, but economics still favor crates in high-rotation produce aisles

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Recycled Linerboard Dominates, Virgin Kraft Accelerates

Recycled linerboard accounted for 57.36% of the United Arab Emirates corrugated packaging market share in 2025, a level supported by import-heavy waste fiber flows and brand sustainability pledges. Virgin Kraft, although smaller, is projected to grow 5.57% annually through 2031 on the strength of export-class food and pharma packs seeking pristine surfaces. The United Arab Emirates corrugated packaging market size is attached to virgin grades, therefore grows faster than the all-material average, widening the price spread between commodity and premium stock. Domestic mills such as Star Paper Mill aim to lock in bale availability, softening volatility for recycled converters.

Premium exporters in regulated categories often split runs, specifying recycled outer liners for local transit cartons while shifting to food-contact virgin for European shipments that demand chain-of-custody proof. Semi-chemical mediums and white-top liners sit in a middle lane, winning where cushioning or high-graphic retail faces are non-negotiable. The bifurcation signals that future investment will twin de-inked recycled lines with bleached kraft imports, rather than betting on a single grade.

By Flute Type: B Flute Leads, F Flute Gains in High-Graphic Retail

B Flute retained 44.31% volume in 2025 thanks to its balanced stacking strength and broad machine compatibility. F Flute, however, is expected to post a 6.14% CAGR through 2031 as cosmetic and pharma display cartons migrate to ultra-thin profiles that present sharper shelf edges. United Arab Emirates corrugated packaging market size growth for F Flute mirrors the country’s pivot to value-added re-exports, and its lighter profile also reduces airfreight cube for last-minute promotional launches.

Converters investing in dual-wall corrugators capable of switching from B to micro-flutes on the fly can hedge demand swings while compressing setup time. Queenex Corrugated Carton Factory’s installation of a five-color die-cut line illustrates the technical upgrades required to work with thin flutes without washboarding.[2]Queenex Corrugated Carton Factory, “About Us,” qucarton.ae As F Flute picks up share in personal-care sachet boxes and gift sets, demand for tight-tolerance cutting dies, and high-opacity inks rises too.

By Packaging Type: RSC Prevails, Custom Die-Cut Accelerates

Regular slotted containers (RSCs) accounted for 41.27% of 2025 shipments, as they feed highly automated lines in logistics parks. Yet custom die-cut formats are growing 5.91% annually, capturing direct-to-consumer and subscription services where unboxing equals marketing spend. The elevated graphics possible in a die-cut blank allow e-tailers to preview brand personality before the product is even opened, giving custom blanks an outsized brand return on investment.

Supply-chain digitization lets fulfillment software define exact dimensions for each SKU, trimming void fill and freight costs. That transition pulls volume from generic RSC to right-sized, variable-print runs produced on hybrid digital-flexo lines. United Arab Emirates corrugated packaging market share for branded die-cuts will thus keep inching up, especially as 2026 carbon reporting rules reward cube-optimized packaging.

By Wall Type: Single-Wall Dominates, Triple-Wall Ramps Up

Single-wall maintained 64.12% share in 2025 because inland truck routes rarely exceed 300 km, and most food SKUs max out below 20 kg. Triple-wall, forecast to grow 5.15% through 2031, supports electronics exports, heavy machinery spares, and dangerous-goods commodity chemicals routed to Europe and North America. The higher material factor is offset by lower damage claims and warranty returns. Rengo’s Tri-Wall acquisition brought heavy-duty know-how to Jebel Ali, enabling assemblers to bundle on-site packout services for fragile modules.

As Etihad Rail links free zones to ports, multimodal transit will increase, further boosting triple-wall adoption in the United Arab Emirates corrugated packaging market. Arabian Packaging, with 140,000 metric tonnes of annual capacity and a fully automated plant, supplies triple-wall and double-wall configurations to industrial clients and leverages its partnership with Etihad Rail to reduce freight costs and carbon emissions.

By Printing Technology: Flexo Leads, Digital Inkjet Rises

Flexographic presses still produced 64.27% of 2025 output, anchored by long-run food and beverage shippers. Digital inkjet, however, expands at 5.36% annually because short-run cosmetics, craft confectionery, and promotional campaigns demand on-the-fly artwork. The United Arab Emirates corrugated packaging market, addressed by digital lines, therefore scales faster than flexo, even though the absolute volume remains lower. Inkjet eliminates plate costs, enabling lot-coded or influencer-co-branded graphics.

Brand owners value the carbon savings from zero plates and lower setup wastage. Converters adding roll-to-roll inkjet coupled with inline die-cut infeed achieve next-day turns that keep pace with social-media-driven product drops. Emirates Printing Press, certified to ISO 12647-2 for process-standard offset printing, offers litho-laminated corrugated boxes that combine the structural benefits of corrugated with the visual impact of offset lithography, a hybrid solution that commands premium pricing in luxury and pharmaceutical segments.

By End-User Industry: Processed Food Leads, E-Commerce Surges

Processed food accounted for 26.31% of demand in 2025, affirming the UAE’s role as a re-exporter of pantry staples to Africa and the wider Middle East. E-commerce fulfillment centers now post the highest 5.24% CAGR, reflecting same-day import-reexport models staked on regional air hubs. The United Arab Emirates corrugated packaging market size allocation to e-commerce therefore rises fastest among all verticals, forcing converters to optimize box-on-demand modules at hub warehouses.

Electronics, beverages, and fresh produce fill the mid-ranks, each with differentiated liner specs. Phased single-use plastic prohibitions push fresh produce into fiber trays with ventilation and moisture coatings, nudging incremental corrugated tonnage even as returnable crates nip share at the top grocers. ISO 22000 and Hazard Analysis and Critical Control Points certifications are becoming table stakes for converters serving food and pharmaceutical clients, raising barriers to entry and favoring established players with robust quality-management systems.

Geography Analysis

Corrugated packaging demand is concentrated in Dubai, Abu Dhabi, and Sharjah, which together accounted for more than three-quarters of 2025 consumption. Dubai’s Jebel Ali Free Zone and National Industries Park host the lion’s share of corrugators, lured by proximity to sea-air multimodal nodes. Abu Dhabi’s KEZAD clusters virgin-fiber-intensive mills and bio-barrier pilot lines that align with the emirate’s industrial strategy. Sharjah, with lower land costs, accommodates second-tier converters supplying retail in the northern emirates.

Etihad Rail’s spine network will connect Abu Dhabi to Dubai and onto Ras Al Khaimah by 2027, trimming corridor freight costs by up to 20% and tilting plant location decisions toward rail-adjacent plots.[3]Arabian Packaging, “Company Overview and Etihad Rail Partnership,” arabianpackaging.com Northern emirates hosting material recovery facilities supply baled recovered fiber to new recycled containerboard mills, creating a domestic loop that cushions volatility in imported bales. The geographic compactness of 83,600 km² also underpins just-in-time deliveries, letting converters operate with lean finished-goods inventories.

Customs-bonded status in free zones supports hub-and-spoke packouts, where corrugated arrives flat, is assembled on demand, and is loaded with goods for re-export. Dubai’s 5% import duty waiver on raw paper entering free-zones lowers corrugator cost base, while Sharjah’s community recycling programs backfill bale gaps during shipping surges. Overall, location advantages blend hard infrastructure with regulatory incentives, keeping the United Arab Emirates corrugated packaging market resilient to regional disruptions.

Competitive Landscape

Market structure is moderately fragmented, with the top five players holding 45-50% of capacity, but none alone exceeds 20%. Hotpack Global leverages 13 UAE plants and a 2.2 MW rooftop solar array to pitch low-carbon credentials to multinationals chasing Scope 3 cuts. Arabian Packaging’s Etihad Rail deal offers carbon-efficient inland transport, while Union Paper Mills secures domestic recycled fiber with a carton-to-linerboard line, insulating against imported bale gaps.

Rengo’s 2025 acquisition of Pronk Multiservice ME FZE injected Japanese heavy-duty expertise, enabling triple-wall and honeycomb offerings aligned with electronics and machinery exporters.[4]Rengo, “Tri-Wall Acquires Manufacturer of Heavy Duty Packaging Materials,” rengo.co.jp Mondi’s Western European mega-box assets, folded into its global network, enable it to cross-sell integrated kraft bags and corrugated packaging to GCC customers requiring multi-format packaging.

Investment focus tilts toward end-of-line automation, color management certifications, and circular-economy fiber sourcing. Emerging disruptor Star Paper Mill opened a USD 54 million recycled board mill in April 2026, capturing linerboard margin and promising bale security for captive converting start-ups. Hybrid digital-flexo presses, bio-based coatings, and rail-integrated logistics define new bases of competition, replacing sheer tonnage as the sole differentiator.

United Arab Emirates Corrugated Packaging Industry Leaders

Rengo Co. Ltd.

Hotpack Packaging Industries LLC

Falcon Pack Industries LLC

Union Paper Mills LLC

Queenex Corrugated Carton Factory LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Star Paper Mill commissioned a USD 54 million recycled containerboard plant in KEZAD, adding 135,000 tons of annual capacity and sourcing 80% domestic waste.

- March 2026: Rengo subsidiary Tri-Wall began operating Shandong’s first heavy-duty corrugated plant, reinforcing its UAE-plus-China heavy-duty strategy.

- February 2026: Hotpack Global adopted HPE GreenLake cloud infrastructure with Emtech to optimize IT spend and lower carbon footprint.

- January 2026: Hotpack Global won Sustainable Business of the Year 2025-FMCG at Dubai’s Sustainability 2040 Awards, reflecting a 97% recyclable portfolio.

United Arab Emirates Corrugated Packaging Market Report Scope

The United Arab Emirates corrugated packaging market report encompasses a comprehensive analysis of the industry's transition toward high-performance, sustainable solutions driven by national economic diversification and a stringent regulatory push against single-use plastics. It evaluates the impact of the UAE’s strategic transshipment role, centered on the Jebel Ali logistics corridor, and the specialized requirements of expanding domestic sectors such as aerospace, food processing, and luxury electronics.

The United Arab Emirates Corrugated Packaging Market Report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, Corrugating Medium, Semi-Chemical Fluting, and Other Materials), Flute Type (A Flute, B Flute, C Flute, E Flute, and F Flute), Packaging Type (Regular Slotted Containers, Die-Cut Custom Boxes, Folding Cartons, Point-of-Purchase Displays, Pallet Boxes, and Other Packaging Types), Wall Type (Single-Wall, Double-Wall, Triple-Wall, and Single Face), Printing Technology (Flexographic Printing, Digital Inkjet Printing, Litho-Lamination, Screen Printing, and Other Printing Technologies), End-User Industry (Processed Foods, Fresh Food and Produce, Beverages, Electrical Products, Personal Care and Cosmetics, E-commerce Fulfillment Centers, Pharmaceuticals, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Kraft Linerboard |

| Recycled Linerboard |

| Corrugating Medium |

| Semi-Chemical Fluting |

| Other Materials |

| A Flute |

| B Flute |

| C Flute |

| E Flute |

| F Flute |

| Regular Slotted Containers |

| Die-Cut Custom Boxes |

| Folding Cartons |

| Point-of-Purchase Displays |

| Pallet Boxes |

| Other Packaging Types |

| Single-Wall |

| Double-Wall |

| Triple-Wall |

| Single Face |

| Flexographic Printing |

| Digital Inkjet Printing |

| Litho-Lamination |

| Screen Printing |

| Other Printing Technologies |

| Processed Foods |

| Fresh Food and Produce |

| Beverages |

| Electrical Products |

| Personal Care and Cosmetics |

| E-commerce Fulfillment Centers |

| Pharmaceuticals |

| Other End-User Industries |

| By Material | Virgin Kraft Linerboard |

| Recycled Linerboard | |

| Corrugating Medium | |

| Semi-Chemical Fluting | |

| Other Materials | |

| By Flute Type | A Flute |

| B Flute | |

| C Flute | |

| E Flute | |

| F Flute | |

| By Packaging Type | Regular Slotted Containers |

| Die-Cut Custom Boxes | |

| Folding Cartons | |

| Point-of-Purchase Displays | |

| Pallet Boxes | |

| Other Packaging Types | |

| By Wall Type | Single-Wall |

| Double-Wall | |

| Triple-Wall | |

| Single Face | |

| By Printing Technology | Flexographic Printing |

| Digital Inkjet Printing | |

| Litho-Lamination | |

| Screen Printing | |

| Other Printing Technologies | |

| By End-User Industry | Processed Foods |

| Fresh Food and Produce | |

| Beverages | |

| Electrical Products | |

| Personal Care and Cosmetics | |

| E-commerce Fulfillment Centers | |

| Pharmaceuticals | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the 2026 value of the United Arab Emirates corrugated packaging market?

The market is estimated at USD 0.99 billion in 2026 and is projected to reach USD 1.24 billion by 2031.

Which material grade is growing fastest through 2031?

Virgin kraft linerboard, driven by premium export packs, is forecast to expand at a 5.57% CAGR.

How will the 2026 single-use plastic ban affect demand?

The ban redirects many food-service and retail applications from plastic to fiber, lifting corrugated volumes and accelerating investment in recyclable coatings.

Why are e-commerce fulfillment centers important for corrugated demand?

Same-day Gulf deliveries and brand-driven unboxing experiences increase box customization and raise per-unit packaging intensity.

What role does Etihad Rail play in the packaging supply chain?

Rail links between free zones and ports cut freight costs up to 20%, encouraging converters to co-locate near railheads and optimize inventory flow.

How are UAE mills exposed to recovered paper price swings?

Approximately 80% of recycled fiber is imported, so mills face significant price volatility unless domestic recovery rates rise or integrated capacity grows.

Page last updated on: