United Arab Emirates AI-Powered Energy Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

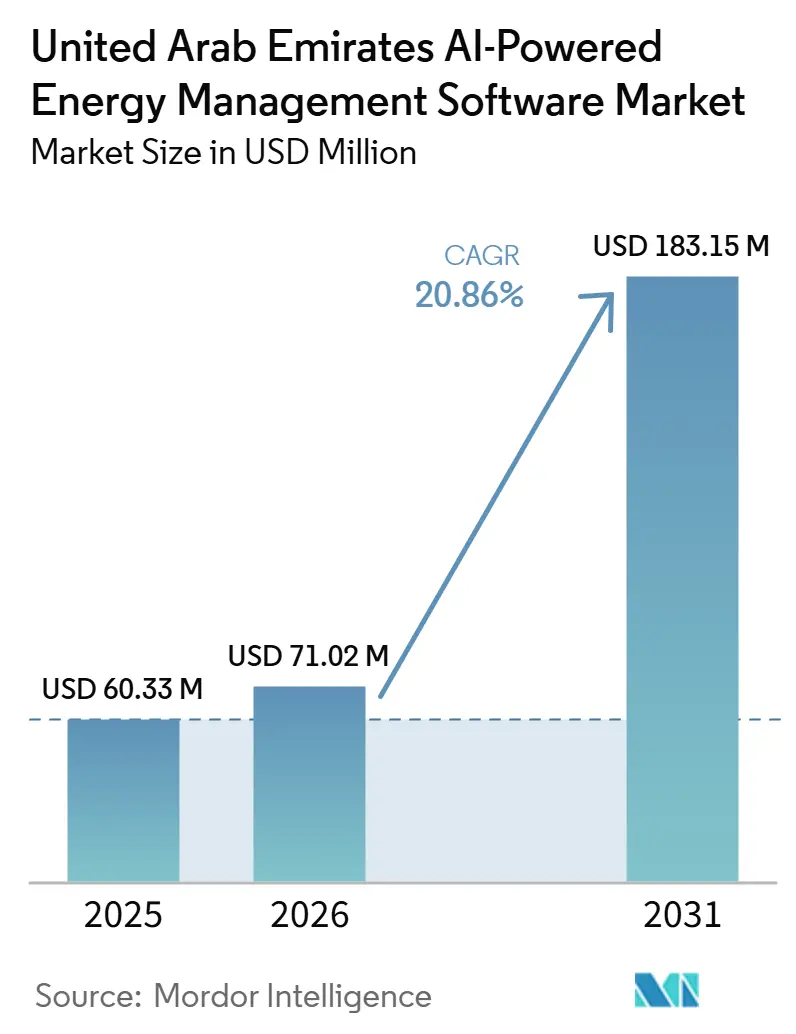

| Base Year Market Size (2025) | USD 60.33 Million |

| Market Size (2026) | USD 71.02 Million |

| Market Size (2031) | USD 183.15 Million |

| Growth Rate (2026 - 2031) | 20.86% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates AI-Powered Energy Management Software Market Analysis by Mordor Intelligence

The United Arab Emirates AI-powered energy management software market size was valued at USD 60.33 million in 2025 and estimated to grow from USD 71.02 million in 2026 to reach USD 183.15 million by 2031, at a CAGR of 20.86% during the forecast period (2026-2031). The United Arab Emirates AI-powered energy management software market is being shaped by a national efficiency agenda that makes energy optimization a long-duration operating priority rather than a short-cycle spending decision. Demand is centered in Dubai and Abu Dhabi, where large commercial portfolios, utility digitization, and public retrofit programs are creating a sustained need for software that can monitor, predict, and optimize energy use at scale. Cloud delivery is gaining traction because it shortens deployment timelines, reduces upfront system burden, and lets operators update models and dashboards continuously across multiple sites. The value of these systems tends to deepen after deployment because metered savings, anomaly records, and operating history create localized data that improves model accuracy over time. Growth remains exposed to legacy building integration issues, cybersecurity reviews, and gaps in localized training data, but those constraints are being outweighed by policy-driven demand and expanding AI adoption across the energy system.

Key Report Takeaways

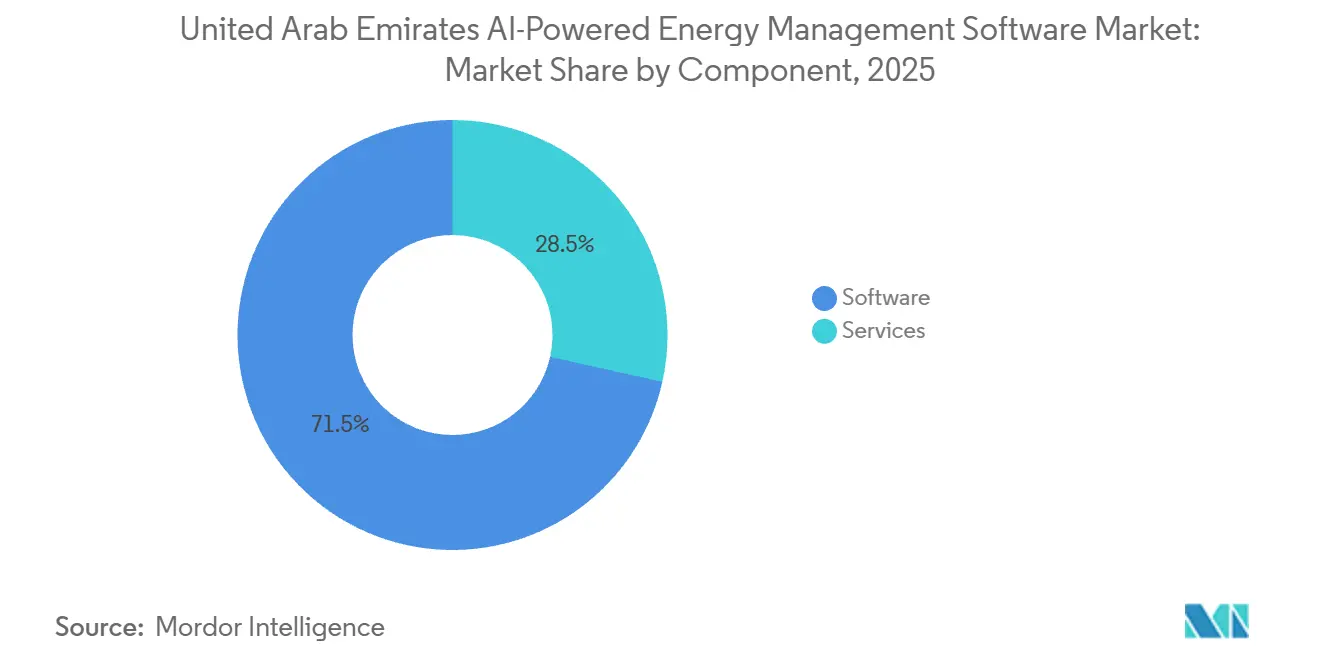

- By component, software held 71.50% share in 2025, while services are projected to expand at a 23.40% CAGR through 2031 in the United Arab Emirates AI-powered energy management software market.

- By deployment mode, cloud-based solutions held 61.00% share in 2025 and are projected to record the fastest growth at a 24.10% CAGR through 2031.

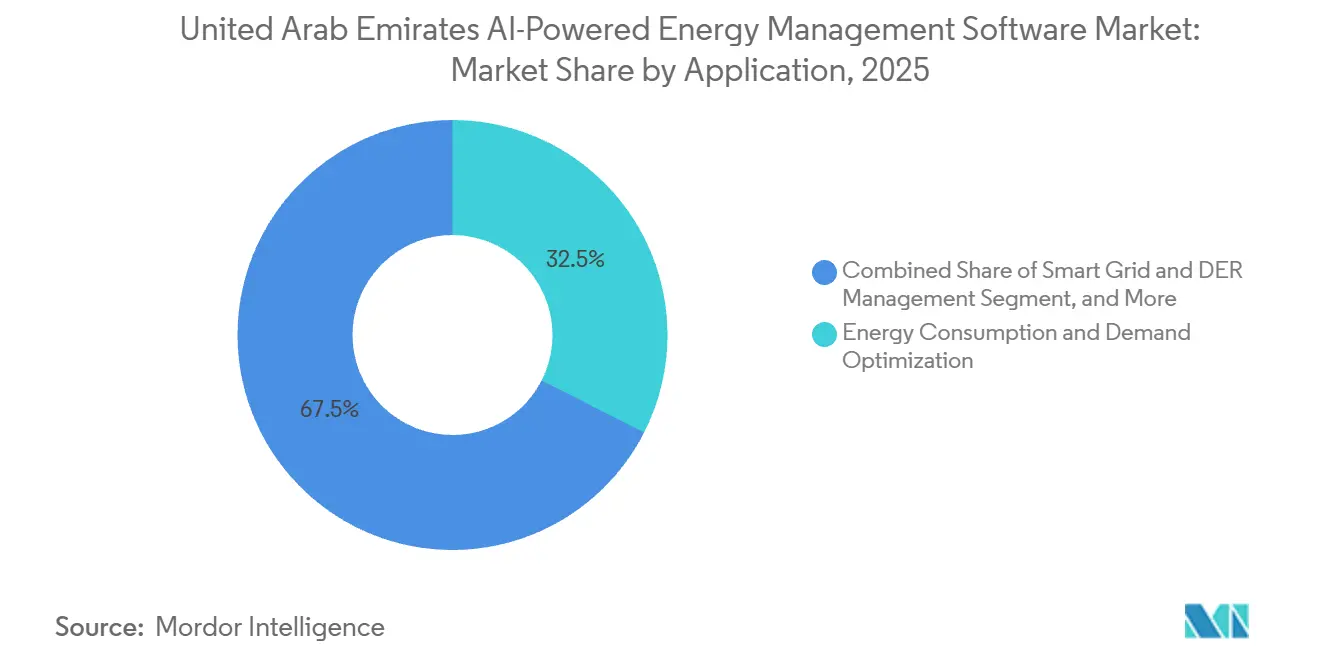

- By application, energy consumption and demand optimization accounted for a 32.50% share in 2025, while renewable energy forecasting and integration is projected to expand at a 25.60% CAGR through 2031.

- By end user, commercial buildings held 34.00% share in 2025, while utilities are projected to advance at a 24.80% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Arab Emirates AI-Powered Energy Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Smart Building Retrofit Programs | +4.5% | Dubai, Abu Dhabi | Short term (≤ 2 years) |

| Rising Grid Interoperability Needs Across Distributed Energy Assets | +3.8% | UAE-wide, strongest in Dubai and Abu Dhabi | Medium term (2-4 years) |

| Expansion of Cloud-Based Energy Analytics and SaaS Procurement | +3.2% | UAE-wide | Short term (≤ 2 years) |

| Accelerating Compliance with National Net Zero and Energy Efficiency Targets | +2.8% | UAE-wide | Medium term (2-4 years) |

| Emirate-Level Demand for AI-Based Peak Load Orchestration in Mixed-Use Portfolios | +2.1% | Dubai, Abu Dhabi | Medium term (2-4 years) |

| Rising Need for Utility-Hosted, UAE-Hosted Data Residency Architectures | +1.7% | UAE-wide, concentrated in regulated sectors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Smart Building Retrofit Programs

The United Arab Emirates AI-powered energy management software market is seeing strong pull from retrofit activity because older buildings cannot deliver verified savings with manual controls alone. Abu Dhabi reinforced this direction in November 2025 when TAQA Energy Services and Sdeira Group launched a large residential retrofit project at Aryam ICAD Residential City, where upgraded HVAC systems and advanced monitoring and control technologies were deployed across 8 building clusters.[1]Abu Dhabi News, “TAQA Energy Services, Sdeira Group Launch Building Retrofit Project at Aryam ICAD Residential City,” Abu Dhabi News, abudhabinews.net Dubai added a visible reference point in May 2026 when DEWA inaugurated Al Shera'a, a net-positive government building that integrated more than 110,000 smart sensors and generated more than 1.9 million automated control commands each day across nearly 100 systems. These projects matter because they move procurement away from pilot dashboards and toward platforms that can document savings, support audits, and keep optimization active after the retrofit is complete. Once savings are measured at the site level, the same operating data becomes training material for model tuning, which raises switching costs and strengthens vendor positions over time.

Rising Grid Interoperability Needs Across Distributed Energy Assets

The United Arab Emirates AI-powered energy management software market is also benefiting from the move toward a more distributed energy system, where buildings, storage assets, solar generation, and charging infrastructure need a common intelligence layer. DEWA completed the region's first virtual power plant in July 2024, bringing together rooftop solar, battery storage, EV chargers, and flexible commercial loads within one grid management framework. The coordination burden rises as more assets sit at the edge of the grid, because operators need software that can read conditions across sites and respond without creating local inefficiencies elsewhere. In April 2026, the Ministry of Energy and Infrastructure launched a smart microgrid project that allows buildings to generate and manage electricity more autonomously, with wider public and private sector expansion planned under a national standardization pathway. This shift gives AI platforms a larger role than simple building control, because the same tools are increasingly expected to support orchestration across distributed energy resources, local demand, and grid-facing operating decisions.

Expansion of Cloud-Based Energy Analytics and SaaS Procurement

The United Arab Emirates AI-powered energy management software market is moving toward cloud delivery, as many buyers seek faster deployment and reduced on-site infrastructure management. Microsoft announced in October 2025 that enterprise AI workloads for Microsoft 365 Copilot would be processed in-country in the UAE, which directly addressed data residency concerns that had slowed adoption in regulated environments. Browser-based analytics also reduce the training burden for energy managers, since dashboards and alerts can be used without deep building management system specialization. Subscription models fit the local procurement environment because they move spending into operating budgets and reduce the need for a large upfront capital cycle. That matters for the broader United Arab Emirates AI-powered energy management software market because mid-sized property operators can adopt optimization tools sooner when they are buying a service instead of redesigning their entire control stack.

Accelerating Compliance with National Net Zero and Energy Efficiency Targets

The United Arab Emirates AI-powered energy management software market is being supported by a federal energy policy that makes demand reduction and clean energy management part of long-term infrastructure planning. The UAE Energy Strategy 2050 targets a 42-45% improvement in per-capita energy consumption efficiency against 2019 levels, which gives software vendors a durable policy backdrop for monitoring and optimization solutions.[2]UAE Ministry of Energy and Infrastructure, “Energy Strategies to Achieve Net Zero,” UAE Ministry of Energy and Infrastructure, moei.gov.ae This matters because compliance-oriented programs are less likely to pause when property cycles soften, especially when energy use has to be tracked and documented across multiple assets. DEWA reinforced the same logic at the World Governments Summit in February 2026 by linking AI adoption directly to energy sector transformation and sustainability accountability in the UAE. As a result, software selection is increasingly tied to reporting, verification, and operating transparency rather than only to short-term cost savings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration Friction with Legacy Building Management Systems | -2.3% | UAE-wide, concentrated in Sharjah and Northern Emirates | Medium term (2-4 years) |

| Cybersecurity and Operational Technology Risk Concerns | -1.9% | UAE-wide, concentrated in utilities and industrial facilities | Long term (≥ 4 years) |

| High Change-Management Burden Across Multi-Site Commercial Portfolios | -1.4% | Dubai, Abu Dhabi | Short term (≤ 2 years) |

| Limited Availability of Emirate-Specific Performance Data for Model Training | -0.9% | UAE-wide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Integration Friction with Legacy Building Management Systems

The United Arab Emirates AI-powered energy management software market still faces a practical barrier in buildings that run on older management systems with limited openness. Many mid-tier offices, hospitality assets, and industrial sites were built around proprietary controls that do not connect easily to modern AI overlays. In those cases, value cannot be unlocked until data from meters, HVAC equipment, and controls can be normalized and made accessible to the software layer. The issue is not only technical, because some building owners are also tied to maintenance agreements that make third-party integration slower and more expensive. This friction is most visible outside the newest premium assets, where integration work can delay rollout even when the business case for optimization is already clear.

Cybersecurity and Operational Technology Risk Concerns

The United Arab Emirates AI-powered energy management software market also has to work through cybersecurity scrutiny because these platforms often connect directly to operating equipment rather than only to reporting tools. The risk is concrete, not theoretical, as ABB disclosed in February 2025 that its ASPECT Energy Management System had hard-coded credential vulnerabilities. Utilities, industrial operators, and government building managers, therefore, tend to require more evidence before they allow new software to interact with live control environments. Security assessments, penetration testing records, and compliance documentation can all lengthen sales cycles and raise the cost of approval. That slows deployment speed even in cases where the efficiency upside is already well understood.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Platform Leadership, Services Gain Ground Quickly

Software accounted for 71.50% of the United Arab Emirates AI-powered energy management software market size in 2025, which showed that buyers were first prioritizing the core intelligence layer for monitoring, anomaly detection, forecasting, and automated control. This lead reflected the operating structure of the market, where large property groups and public asset owners manage broad portfolios and need a centralized view of energy performance across sites. Real-time dashboards, demand response logic, and set-point optimization tools fit that need because they reduce the lag between detection and corrective action. The United Arab Emirates AI-powered energy management software market, therefore, leaned toward platforms that could turn fragmented building data into repeatable operating routines.

The services segment is projected to expand at a 23.40% CAGR from 2026 to 2031, which shows that deployment support is becoming more important as systems grow more complex. The reason is straightforward, because software value often depends on integration, calibration, model retraining, and ongoing operational tuning after the initial installation. DEWA's ambition to become the world's first AI-native utility supports this trend, since the wider use of AI across energy infrastructure raises demand for specialist implementation and managed support skills. ABB's 2025 addition of generative AI capabilities to the ABB Ability Energy Management System also showed how software and services are starting to blend, because operators increasingly need help translating system outputs into daily action.[3]ABB Ltd., “ABB Adds Generative AI Capabilities to ABB Ability Energy Management System to Accelerate Operational Insights,” ABB, abb.com

By Deployment Mode: Cloud Adoption Sets the Pace

Cloud-based solutions held 61.00% of the market in 2025, and that lead showed how strongly buyers preferred faster rollout and lower infrastructure overhead. Cloud architecture lets operators benchmark multiple sites at once, update models continuously, and pull in outside data such as weather and occupancy trends without rebuilding each local system. That creates a practical advantage in the United Arab Emirates AI-powered energy management software market, where many customers oversee mixed portfolios rather than single buildings. The same model also supports quicker pilot launches, which helps vendors prove savings before a wider rollout decision is made.

Cloud-based deployment is projected to grow at a 24.10% CAGR from 2026 to 2031, which confirms that the delivery model is still gaining ground rather than only holding an early lead. Microsoft's in-country data processing announcement in 2025 reduced one of the main objections in regulated sectors by aligning cloud adoption more closely with local data handling expectations. On-premises systems still matter in utilities, industrial facilities, and other sensitive sites where operators want tighter control over external access. Hybrid deployment remains relevant as well, because many large owners are managing both legacy properties that need local autonomy and newer sites that are better suited to centralized analytics. This balance means cloud will likely remain the growth engine, while hybrid and on-premises architectures continue to anchor the most security-sensitive use cases.

By Application: Demand Optimization Leads, Renewable Use Cases Expand Fast

Energy consumption and demand optimization captured 32.50% of the United Arab Emirates AI-powered energy management software market size in 2025, which made it the largest application area. That result reflected the basic operating reality of the country, where cooling loads are unusually high, and savings from HVAC optimization can be material for building owners. A 2025 ScienceDirect study noted that cooling can account for 60-70% of total commercial building energy use in the UAE, which helps explain why demand-side applications moved first. Johnson Controls also showed the practical value of this use case at Dubai Silicon Oasis, where its AI-driven cooling optimization delivered 30% annual energy savings, 4.2 million kWh in annual savings, and a 1,848-tonne annual carbon footprint reduction.

Renewable energy forecasting and integration is projected to expand at a 25.60% CAGR from 2026 to 2031, which marks it as the fastest-growing application segment. As solar generation, storage, and flexible loads expand, operators need stronger forecasting and dispatch intelligence to balance variable supply with real-time demand. That makes the software role broader than building control, because the platform increasingly has to support coordination between generation assets, storage behavior, and site-level consumption. DEWA and Siemens Energy highlighted this direction in October 2025 when they launched Phase 2 of the AI Plant Intelligent Controller at Jebel Ali's M-Station after Phase 1 had already improved generation efficiency by 2.2% and reduced carbon emissions by 35,000 tonnes annually per power block. Asset performance, predictive maintenance, DER management, and energy trading functions are still smaller revenue pools today, but their role should keep rising as the system becomes more digital and more distributed.

By End User: Commercial Buildings Hold the Largest Base, Utilities Grow Fastest

Commercial buildings held 34.00% of the United Arab Emirates AI-powered energy management software market share in 2025, which gave them the largest current end-user position. This reflected the heavy concentration of offices, retail centers, hospitality properties, and mixed-use assets in Dubai and Abu Dhabi, where occupancy patterns and cooling demand create a constant need for operating efficiency. These properties also lend themselves to portfolio-level benchmarking, which makes software deployment more scalable than in single-site environments. The United Arab Emirates AI-powered energy management software market has therefore drawn steady demand from property owners that want continuous HVAC tuning, lighting optimization, and verified savings reporting across many assets.

Utilities are projected to expand at a 24.80% CAGR from 2026 to 2031, which makes them the fastest-growing end-user group. DEWA's public positioning around AI-native utility operations supports that outlook, because it signals a wider shift from isolated pilots to embedded AI in generation, distribution, and facility management. Industrial facilities are also becoming more relevant, as Honeywell's Experion Cognition completed a live proof of concept at Borouge International's Ruwais facility in June 2026 for autonomous control room operations that target energy use, production, and safety together. Residential buildings remain the smallest share today, but smart metering, district cooling interfaces, and in-home digital touchpoints should gradually widen the addressable base over time.

Geography Analysis

Dubai accounted for the largest share of demand in the United Arab Emirates AI-powered energy management software market in 2025, supported by its dense commercial real estate base and active public energy programs. DEWA reported in 2026 that it managed more than 2.1 million smart electricity and water meters and that clean energy already contributed more than 21% of Dubai's energy mix. That operating environment gives software vendors a large installed base where continuous monitoring and optimization are commercially relevant. Dubai also set a visible standard in May 2026 through Al Shera'a, where smart sensors, solar generation, and automated control commands were integrated into one building-level operating model.[4]Government of Dubai Media Office, “Mohammed Bin Rashid Inaugurates ‘Al Shera’a,’ the World’s Tallest, Largest and Smartest Net-Positive Government Building,” Government of Dubai Media Office, mediaoffice.ae The emirate's role is therefore not only about size, but also about creating reference deployments that other building owners can observe and replicate.

Abu Dhabi is shaped more by utility-scale, residential retrofit, and industrial energy use than by the broad commercial density seen in Dubai. TAQA Energy Services and Sdeira Group's November 2025 retrofit launch at Aryam ICAD Residential City showed how large-scale building upgrades are feeding software demand in the emirate. Ruwais adds a different layer of demand because industrial sites there are testing autonomous control and AI-led optimization in live operating environments. Abu Dhabi also sits close to the center of the UAE's long-range infrastructure spending, which supports the buildout of software-intensive energy systems over time.

The Northern Emirates remain earlier in adoption, but they are becoming more relevant as federal programs move beyond the two main demand centers. The Ministry of Energy and Infrastructure first piloted its smart microgrid project at its Sharjah headquarters in 2025 and formally launched the broader initiative in April 2026. This matters because it extends energy intelligence infrastructure into facilities that have historically adopted new software more slowly. Operators in Sharjah, Ras Al Khaimah, Fujairah, Ajman, and Umm Al Quwain are generally more cost sensitive, so managed SaaS and bundled integration support are likely to matter more there than large performance-based contracts. That pattern should help the United Arab Emirates AI-powered energy management software market broaden geographically, even if adoption outside Dubai and Abu Dhabi remains more gradual.

Competitive Landscape

The United Arab Emirates AI-powered energy management software market remains moderately consolidated at the top end, where large automation and controls vendors benefit from installed hardware, long procurement relationships, and direct access to utility and government accounts. Those advantages matter because software performance is easier to prove when a vendor already has data continuity, facility access, and service teams on the ground. The leading strategic pattern is to extend existing control platforms with stronger AI functionality rather than replace the whole installed base at once. Johnson Controls followed that path in April 2026 when it launched Balanced Cooling in the UAE for buildings connected to district cooling networks, targeting lower Delta T surcharges and lower pumping energy use. ABB moved in a similar direction in 2025 by adding generative AI capabilities to the ABB Ability Energy Management System so operators could access insights more easily without deep programming expertise.

Partnership-led execution is also shaping the field because utility and public-sector deployments tend to require local coordination, long implementation windows, and trust in operational settings. DEWA and Siemens Energy expanded that model in October 2025 through Phase 2 of the AI Plant Intelligent Controller at Jebel Ali's M-Station. Mid-tier and AI-native challengers are trying to win where incumbents are slower, especially with faster deployment, lower upfront commitment, and UAE-aligned hosted architectures. That was visible in February 2026 when the Ministry of Energy and Infrastructure, Khazna Data Centers, and Agility announced a pilot to implement Phaidra AI for energy efficiency in data centers and district cooling environments.

Competition is therefore shifting from pure hardware heritage to a broader test that includes integration speed, model quality, service depth, and cybersecurity readiness. Security has become a real differentiator because operators are more cautious when software touches control loops, live industrial equipment, or utility assets. ABB's February 2025 advisory on hard-coded credentials in its ASPECT Energy Management System showed how closely these products are now examined at the OT layer. As a result, the United Arab Emirates AI-powered energy management software market is likely to remain competitive, but the viable field should stay limited to vendors that can satisfy both efficiency expectations and operational risk standards.

United Arab Emirates AI-Powered Energy Management Software Industry Leaders

Verdigris Technologies Inc.

CopperTree Analytics Inc.

75F, Inc.

Switch Automation Pty Ltd

GridPoint, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Honeywell introduced Experion Cognition, an AI-enabled autonomous control system platform, completing a live proof of concept at Borouge International's Ruwais facility in Abu Dhabi. The platform is designed to optimize production, reduce energy use, and enhance safety through AI-driven recommendations and automated decision-making. Honeywell has confirmed commercial availability in Q3, 2026, representing the first industrial-grade AI autonomous control deployment of this scale in the UAE's petrochemical sector.

- May 2026: DEWA inaugurated Al Shera'a, its new headquarters in Al Jaddaf and the world's tallest, largest, and smartest net-positive government building. The building integrates over 110,000 smart sensors, generates over 1.9 million automated daily control commands, and draws on 5 MW of on-site solar capacity, with nearly 100 building systems unified through a single AI-powered smart app, establishing a new reference architecture for AI-integrated facilities management in the UAE.

- April 2026: Johnson Controls launched Balanced Cooling in the UAE, a purpose-built AI diagnostic and smart valve solution for buildings connected to centralized district cooling networks. Initial deployments demonstrated potential to eliminate low Delta T surcharges by up to 100% and reduce pumping energy by up to 40%, directly supporting DEWA's district cooling penetration target of 40% in Dubai by 2030.

- April 2026: The UAE Ministry of Energy and Infrastructure formally launched a smart microgrid project, initially piloted at the Ministry's Sharjah headquarters in 2025, integrating clean energy generation, storage, and advanced digital energy management to enable autonomous building-level power operation. National expansion with public and private sector partners was announced alongside a forthcoming regulatory framework for microgrid standardization.

United Arab Emirates AI-Powered Energy Management Software Market Report Scope

The United Arab Emirates AI-powered energy management software market comprises AI-driven software solutions and related services that optimize energy production, distribution, storage, and consumption through intelligent analytics, automation, and predictive modeling. These platforms leverage machine learning, artificial intelligence, digital twins, advanced forecasting, and real-time monitoring technologies to improve energy efficiency, enhance asset utilization, facilitate renewable energy integration, and support Canada's decarbonization and net-zero objectives.

The United Arab Emirates AI-Powered Energy Management Software Report is Segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Application (Energy Consumption and Demand Optimization, Asset Performance and Predictive Maintenance, Smart Grid and Distributed Energy Resource (DER) Management, Renewable Energy Forecasting and Integration, and Energy Trading, Pricing and Market Intelligence), and End User (Utilities, Commercial Buildings, Industrial Facilities, and Residential Buildings). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance |

| Smart Grid and Distributed Energy Resource (DER) Management |

| Renewable Energy Forecasting and Integration |

| Energy Trading, Pricing and Market Intelligence |

| Utilities |

| Commercial Buildings |

| Industrial Facilities |

| Residential Buildings |

| By Component | Software |

| Services | |

| By Deployment Mode | Cloud-Based |

| On-Premises | |

| Hybrid | |

| By Application | Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance | |

| Smart Grid and Distributed Energy Resource (DER) Management | |

| Renewable Energy Forecasting and Integration | |

| Energy Trading, Pricing and Market Intelligence | |

| By End User | Utilities |

| Commercial Buildings | |

| Industrial Facilities | |

| Residential Buildings |

Key Questions Answered in the Report

What is the size of the United Arab Emirates AI-powered energy management software market?

The market was valued at USD 60.33 million in 2025, reached USD 71.02 million in 2026, and is forecast to reach USD 183.15 million by 2031 at a 20.86% CAGR.

What is driving demand for AI-powered energy management software in the UAE?

Growth is being supported by national energy efficiency targets, public and private retrofit programs, cloud adoption, and the need to optimize cooling-heavy building and utility operations.

Which component leads revenue generation in the UAE?

Software led with 71.50% share in 2025 because buyers prioritized real-time monitoring, anomaly detection, forecasting, and automated control across multi-site portfolios.

Which deployment model is expanding the fastest?

Cloud-based deployment is both the largest and fastest-growing mode, with a 61.00% share in 2025 and a projected 24.10% CAGR through 2031.

Which application area is seeing the highest growth?

Renewable energy forecasting and integration is projected to grow at a 25.60% CAGR through 2031, while energy consumption and demand optimization held the largest share at 32.50% in 2025.

Which end-user group offers the strongest near-term opportunity?

Utilities are expected to grow the fastest at a 24.80% CAGR through 2031, while commercial buildings remain the largest current user group with a 34.00% share in 2025.

Page last updated on: