United Arab Emirates AI Copilot Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

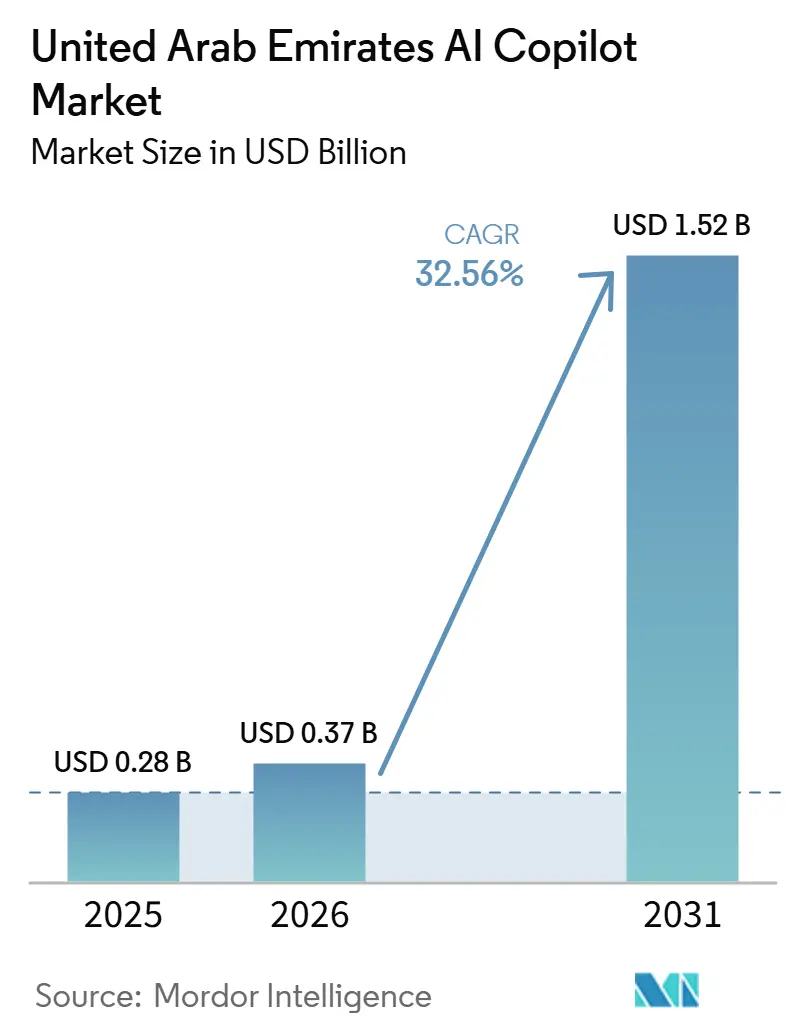

| Base Year Market Size (2025) | USD 0.28 Billion |

| Market Size (2026) | USD 0.37 Billion |

| Market Size (2031) | USD 1.52 Billion |

| Growth Rate (2026 - 2031) | 32.56% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates AI Copilot Market Analysis by Mordor Intelligence

The United Arab Emirates AI copilot market size was valued at USD 0.28 billion in 2025 and is estimated to grow from USD 0.37 billion in 2026 to reach USD 1.52 billion by 2031, at a CAGR of 32.56% during the forecast period 2026-2031. The United Arab Emirates AI copilot market is expanding quickly because large public entities and major enterprises are moving from pilots to production rollouts within a short period, thereby reducing the delays that usually affect enterprise software adoption. The country also benefits from very high AI usage at the population level, with Microsoft’s AI Economy Institute reporting that 64.0% of the working-age population used AI tools by the end of 2025 and 70.1% did so in Q1 2026, which creates a receptive environment for workplace copilots and lowers adoption friction inside organizations. Sovereign infrastructure requirements are also shaping the United Arab Emirates AI copilot market, since vendors with in-country processing, regulated deployment options, and Arabic-capable models hold a stronger position than providers that depend on generic offshore delivery. Federal programs are reinforcing this momentum through public-sector adoption targets, workforce training, and a more centralized policy structure that supports wider enterprise deployment in regulated settings. As a result, the United Arab Emirates AI copilot market is moving beyond broad productivity use and opening up broader opportunities in regulated workflows, bilingual enterprise operations, and sector-specific use cases.

Key Report Takeaways

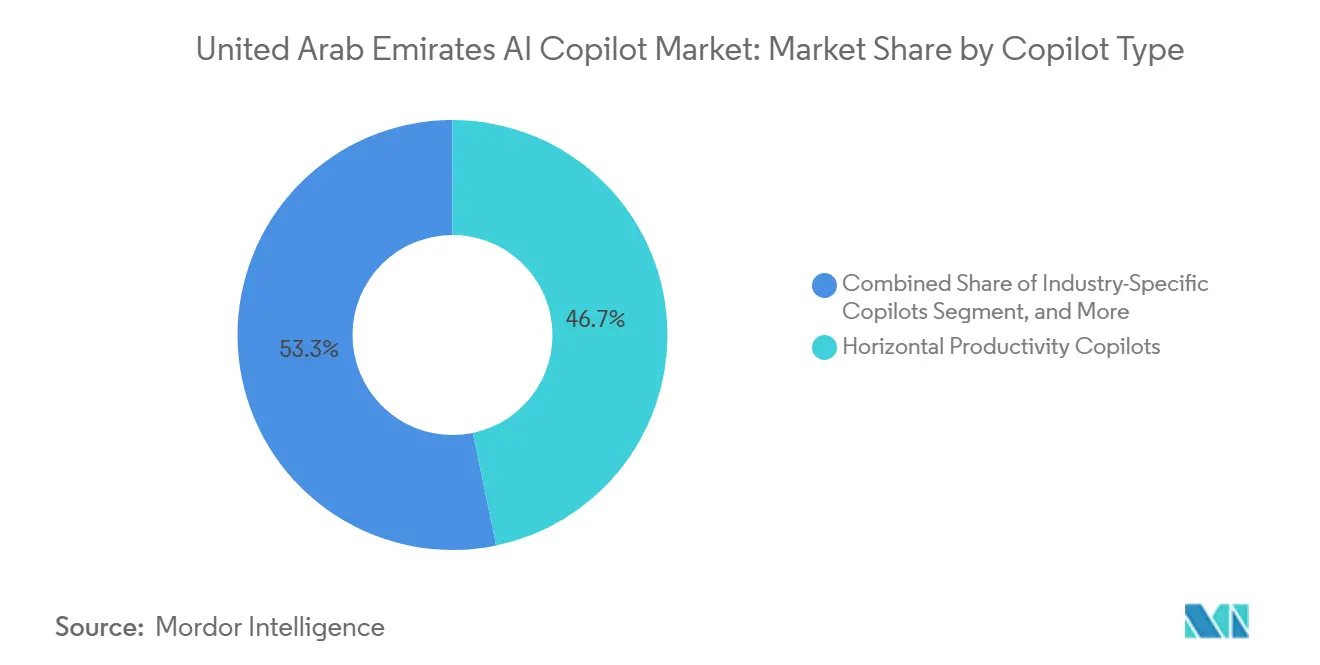

- By copilot type, Horizontal Productivity Copilots held 46.74% revenue share of the United Arab Emirates AI copilot market in 2025, while Industry-Specific Copilots are projected to expand at 34.92% CAGR through 2031.

- By deployment mode, Cloud-Based deployments accounted for 78.41% of revenue in the United Arab Emirates AI copilot market in 2025, while Hybrid deployments are forecast to grow at a 34.61% CAGR through 2031.

- By organization size, Large Enterprises accounted for 72.38% of revenue share in 2025, while Small and Medium Enterprises are projected to record the highest CAGR of 35.14% through 2031.

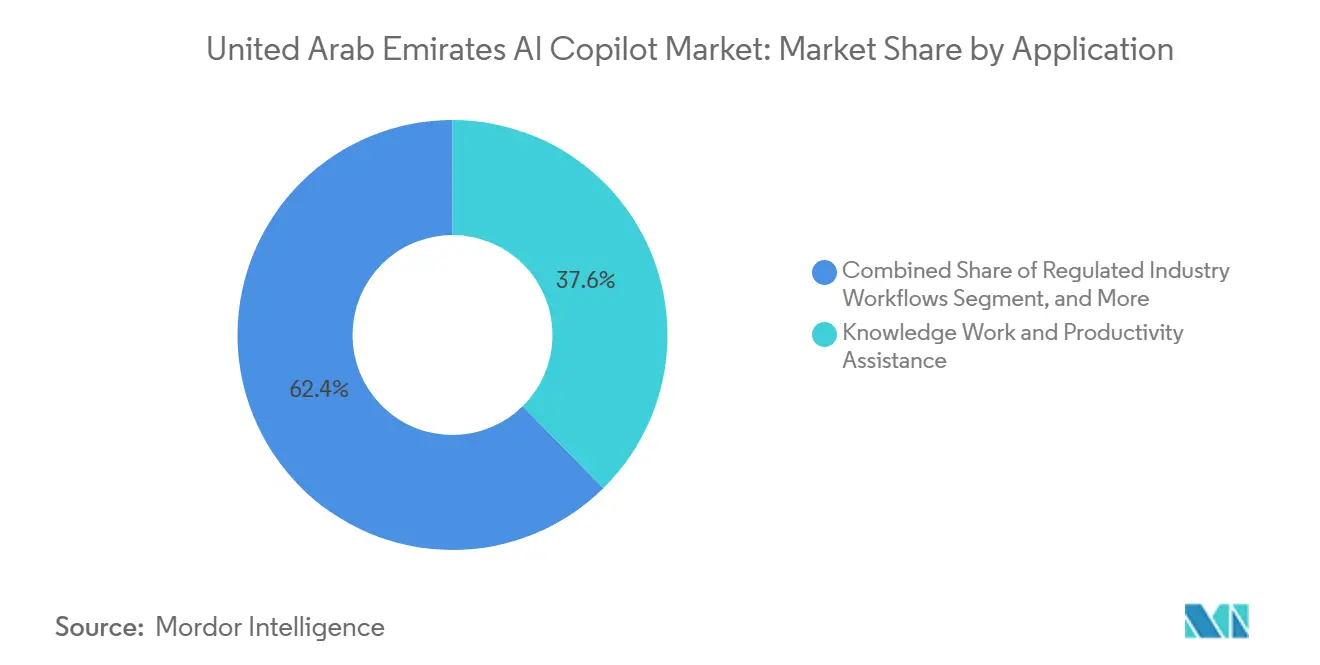

- By application, Knowledge Work and Productivity Assistance accounted for 37.62% of revenue in 2025, while Regulated Industry Workflows are projected to grow at a 34.48% CAGR through 2031.

- By end-user industry, BFSI held 27.13% revenue share in the United Arab Emirates AI copilot market in 2025, while Government and administration is forecast to expand at a 35.82% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Arab Emirates AI Copilot Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Enterprise Copilot Pilots Across Public and Private Sectors | +8.5% | UAE-wide, with the strongest concentration in Abu Dhabi and Dubai | Short term (≤ 2 years) |

| Strong UAE Cloud and Digital Government Readiness | +6.2% | Abu Dhabi and Dubai, with spillover to other emirates through federal programs | Short term (≤ 2 years) |

| Rising Demand for Arabic-First and Bilingual Workflows | +4.8% | UAE-wide and relevant for wider GCC-facing enterprise operations | Medium term (2-4 years) |

| Vendor Bundling Inside Productivity and CRM Stacks | +4.1% | Strongest in Dubai enterprise clusters and free-zone business networks | Short term (≤ 2 years) |

| Data Residency and Sovereign AI Demand in Regulated Industries | +3.6% | UAE-wide, especially in BFSI, healthcare, energy, and government | Medium term (2-4 years) |

| Government-Led AI Adoption in Priority Sectors | +3.2% | Federal level, with early gains in Abu Dhabi and Dubai ministries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding Enterprise Copilot Pilots Across Public and Private Sectors

Large pilot programs are transitioning to production deployments at a visible pace in the United Arab Emirates AI copilot market, shortening evaluation cycles across both public and private organizations. Abu Dhabi Government launched the Frontier Employee Program with Microsoft in 2026 and deployed Microsoft 365 Copilot to 35,000 civil servants across 27 entities, making it one of the region’s largest public-sector AI productivity rollouts.[1]Abu Dhabi Government and Microsoft, “Abu Dhabi Government Partners with Microsoft for Frontier Employee Programme, in One of Public Sector’s Largest AI Productivity Rollouts,” Zawya, zawya.com Dubai Holding also integrated OpenAI and Anthropic models across real estate, hospitality, retail, and entertainment operations in a unified enterprise environment, providing the United Arab Emirates AI copilot market with a high-profile, multi-sector reference case. ADNOC reported by November 2025 that more than 40,000 employees had completed AI training, utilization exceeded 90%, and the program had generated more than 70,000 monthly productivity hours, demonstrating that large-scale adoption can shift from training to measurable operational value. Once these deployments became visible, nearby enterprises had less reason to treat copilots as experimental tools, so the United Arab Emirates AI copilot market began to benefit from local peer effects rather than only top-down policy direction.

Strong UAE Cloud and Digital Government Readiness

Cloud readiness is a core enabler for the United Arab Emirates AI copilot market because large-scale copilots depend on stable digital infrastructure, identity controls, and high-volume processing capacity. Abu Dhabi’s Government Digital Strategy 2025-2027 committed AED 13 billion (USD 3.5 billion) and set a target of 100% sovereign cloud adoption and more than 200 AI use cases across government by 2027, creating a direct demand path for cloud-native, sovereign-ready solutions. In March 2025, the Abu Dhabi Department of Government Enablement signed agreements with Microsoft and Core42 for a sovereign cloud environment capable of processing more than 11 million daily digital interactions, thereby strengthening the infrastructure base needed for broader copilot deployment. Microsoft’s in-country processing for Microsoft 365 Copilot from its Dubai and Abu Dhabi data centers, and the UAE Sovereign Launchpad from e& and AWS, widened the options available to buyers who need local hosting and compliance alignment. This level of infrastructure maturity means the United Arab Emirates AI copilot market is growing with fewer technical bottlenecks than many other national markets that are still building basic cloud and sovereign compute foundations.[2]e&, “UAE Sovereign Launchpad Offered by e and Powered by AWS Is Now Live and Commercially Available Across UAE,” PR Newswire, prnewswire.com

Rising Demand for Arabic-First and Bilingual Workflows

Arabic capability is becoming a practical buying requirement in the United Arab Emirates AI copilot market, as a large share of enterprise communication, customer engagement, and compliance activities is conducted in Arabic and English. e& UAE deployed an Arabic-first AI Telco Copilot and presented it at GITEX Global 2025, which showed that local operators are building domain-specific copilots rather than waiting for generic global releases to catch up. du also launched an Arabic Telecom Large Language Model with Microsoft, Nokia, Khalifa University’s 6G Research Center, and the International Telecommunication Union for internal telecom operations in the UAE, reinforcing the country’s move toward sector-specific bilingual systems.[3]du, “du Partners with Microsoft, Nokia, Khalifa University, and ITU to Launch Region’s First Arabic Telecom LLM for Operational Excellence,” Zawya, zawya.com This matters because Arabic support in the United Arab Emirates AI copilot market is tied not only to user comfort, but also to recordkeeping, customer disclosures, internal approvals, and regulated workflow accuracy. As more institutions require bilingual outputs that work inside existing operating controls, language depth is becoming one of the clearest points of differentiation between broad platform providers and localized enterprise AI vendors.

Vendor Bundling Inside Productivity and CRM Stacks

Bundled software offerings are accelerating seat expansion in the United Arab Emirates AI copilot market by reducing procurement friction that often slows enterprise AI adoption. Microsoft’s Copilot integration in Microsoft 365, combined with in-country data processing from early 2026, lets organizations extend an existing software relationship rather than start a separate vendor evaluation and security review.[4]Microsoft, “Microsoft Announces In-Country Data Processing for Microsoft 365 Copilot in the UAE to Accelerate AI Adoption,” Microsoft News Source EMEA, news.microsoft.com e& UAE and Microsoft also launched a localized SMB bundle in Dubai that combined Dynamics 365, Azure, and Copilot, which widened access for smaller firms that wanted enterprise-grade tools without enterprise-grade deployment complexity. This model supports faster user activation in the United Arab Emirates AI copilot market by enabling access through familiar workplace software and billing structures. It also raises the competitive bar for smaller vendors, since they now have to win through deeper domain expertise, better workflow execution, or more relevant Arabic functionality rather than broad productivity features alone.

Restraints Impact Analysis*

| estraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Enterprise Data and Legacy Workflow Integration | -3.8% | UAE-wide, strongest in older enterprise estates and federal bodies with legacy systems | Medium term (2-4 years) |

| Governance Concerns Around Hallucinations and Auditability | -3.1% | UAE-wide, especially in BFSI, healthcare, and government | Medium term (2-4 years) |

| Skilled AI Operations and Prompt Engineering Talent Shortage | -2.4% | UAE-wide, with greater pressure outside major talent hubs | Medium term (2-4 years) |

| High Cost of Enterprise-Grade Licenses and Secure Deployments | -2.0% | UAE-wide, especially for SMEs and sovereign-compliant deployments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Enterprise Data and Legacy Workflow Integration

The United Arab Emirates AI copilot market still faces a serious limitation due to fragmented data estates and older workflow systems that do not integrate cleanly with modern AI tools. McKinsey’s GCC AI survey found that only 37% of non-value-creating organizations had a well-established technology foundation and strong data fundamentals, while 53% identified output inaccuracies due to poor data quality as a barrier to AI adoption. MIT Sloan Management Review Middle East also reported that 67% of organizations cited integration complexity and 56% pointed to outdated infrastructure as common obstacles to scaling AI, while only 33% said that more than 30% of their data was accessible for AI use. In the United Arab Emirates AI copilot market, this issue is more damaging than it is for basic analytics because copilots depend on timely access to files, applications, records, and process context to produce grounded outputs. Where cloud applications and legacy ERP systems still operate in parallel, organizations face a higher risk of incomplete or misleading responses, which slows production decisions even when buyer interest remains strong.

Governance Concerns Around Hallucinations and Auditability

Governance risk remains a meaningful restraint because many of the fastest adopters in the United Arab Emirates AI copilot market also operate under strict audit, disclosure, and control requirements. The draft points to the Central Bank's AI framework for financial services and to Mashreq’s Arabic AI trade finance deployment, which moved into production with conditions on model audit, data residency, and human oversight. Endava’s late 2025 research across UAE and Saudi business leaders found that data privacy, AI decision transparency, and cybersecurity concerns remained among the biggest barriers to moving from basic AI tools to more autonomous, agentic systems. GitLab’s June 2026 release of AI auditing, governance, and compliance controls also showed that vendors now see traceability and approval chains as central product requirements for enterprise adoption. The result is that the United Arab Emirates AI copilot market is growing quickly, but regulated buyers still move more carefully when workflows involve sensitive records, customer outcomes, or direct operational decisions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Copilot Type: Bundled Productivity Tools Lead, Vertical AI Closes In

Horizontal Productivity Copilots accounted for 46.74% of the United Arab Emirates AI copilot market share in 2025, which reflects the early advantage of tools embedded in office suites and enterprise productivity platforms. This segment expanded first because government entities and large corporations could add Copilot to existing Microsoft 365 environments without changing their core workplace software stack or vendor relationships. The United Arab Emirates AI copilot market, therefore, entered its first major growth phase through summarization, drafting, email support, meeting follow-up, and internal search rather than through highly specialized autonomous workflows. This pattern also favored vendors with large installed user bases, because deployment speed depended heavily on how easily copilots could be activated within software that employees already used every day.

Industry-Specific Copilots are projected to grow at 34.92% CAGR from 2026 to 2031, and that faster pace reflects demand for tools tuned to sector regulations, Arabic documentation, and domain-specific processes. Banks, energy companies, healthcare providers, and government bodies need copilots that can work with local terminology, regulated workflows, and narrower knowledge environments rather than only general text assistance. The Kore.ai partnership with G42’s Inception supports this shift by combining an enterprise conversational AI platform with UAE-focused product development across investment management, energy, and workflow automation. The technical direction of the United Arab Emirates AI copilot industry also supports this movement, as Arabic telecom models and sector-built copilots demonstrate that localized depth can be developed in operational settings. Over time, the United Arab Emirates AI copilot market is likely to keep broad productivity tools in the lead by scale, while shifting a larger share of new spend toward vertical copilots that can handle regulated and domain-rich work with greater precision.

By Deployment Mode: Cloud Still Dominant, Hybrid Captures Regulated-Sector Growth

Cloud-based deployments held 78.41% of the United Arab Emirates AI copilot market share in 2025, making cloud the primary delivery model for early-stage expansion across public and private organizations. This position reflects the country’s strong hyperscaler presence, the availability of local data center capacity, and the convenience of scaling copilots across large user groups without first building heavy internal infrastructure. In the United Arab Emirates AI copilot market, cloud also gained ground, as many first-wave use cases centered on productivity, communication, and document workflows that fit naturally into software-as-a-service environments. The presence of local processing and sovereign-ready cloud options reduced some of the trust barriers that usually slow adoption in government-linked and regulated sectors.

Hybrid deployments are projected to grow at a 34.61% CAGR from 2026 to 2031, driven by customer demand for cloud performance while keeping selected data, approvals, or system layers under tighter local control. The sovereign cloud agreement between Abu Dhabi’s Department of Government Enablement, Microsoft, and Core42 helped establish hybrid architecture as a practical operating model for public-sector AI rather than a temporary compromise. The United Arab Emirates AI copilot market size linked to hybrid environments is being supported by both large regulated institutions and smaller firms that are starting with cloud-based productivity and then adding more controlled handling for client and operational data. On-premises deployment remains relevant, but it is mostly limited to highly restricted environments where full isolation is required, and broad seat expansion is less important. That means the United Arab Emirates AI copilot market is not moving away from cloud, but it is becoming more selective about which workloads remain in shared environments and which move into sovereign or hybrid structures.

By Organization Size: Large Enterprises Lead, SMEs Accelerate Fastest

Large Enterprises captured 72.38% of the United Arab Emirates AI copilot market share in 2025, indicating that the first large revenue pools still sit with organizations with stronger budgets, larger digital estates, and dedicated change-management capacity. These organizations can adopt multi-seat licensing, build security controls, implement structured employee training, and connect copilots to broader workflow redesign. ADNOC’s scale illustrates this pattern, with more than 40,000 employees trained, utilization above 90%, and more than 70,000 monthly productivity hours reported by November 2025 under its expanded Microsoft engagement. Large entities also became early reference buyers in the United Arab Emirates AI copilot market, and their public examples made it easier for other organizations to justify internal deployment decisions. This explains why large enterprises remain central to current revenue, even as adoption is spreading more widely across smaller businesses.

Small and Medium Enterprises are projected to grow at a 35.14% CAGR from 2026 to 2031, making them the fastest-expanding organization-size segment in the United Arab Emirates AI copilot market. The Presight and Abu Dhabi Chamber agreement, which targets more than 102,000 registered SMEs, provides this shift with a direct route into the business base rather than leaving adoption dependent solely on vendor-led sales outreach. The draft also notes that SMEs accounted for 59% of UAE AI software spend by business count in 2026, suggesting the user base is already broadening, even if large enterprises still dominate value. Lower setup friction, prebuilt connectors, localized bundles, and easier access to cloud tools are all reducing the entry barrier for smaller firms looking to automate customer support, back-office tasks, and internal coordination. As that pattern continues, the United Arab Emirates AI copilot market is likely to become less concentrated by buyer type, even though large enterprises will still account for the biggest individual deals.

By Application: Knowledge Work Anchors Revenue, Regulated Workflows Drive Growth

Knowledge Work and Productivity Assistance accounted for 37.62% of revenue in 2025, making it the largest application area in the United Arab Emirates AI copilot market. This first wave focused on email drafting, meeting notes, internal search, document preparation, and everyday workplace assistance because those tasks were easier to scale across large employee bases and easier to supervise. DEWA’s adoption of Microsoft 365 Copilot Cowork in May 2026 showed that, even within productivity use cases, the market is already shifting from simple retrieval to supervised multi-step execution within everyday work tools. The size of this segment reflects how the United Arab Emirates AI copilot market first expanded through broad seat activation before moving deeper into more specialized workflows. It also shows that buyers initially preferred use cases where the value was visible, the training burden was manageable, and the governance risk was relatively lower.

Regulated Industry Workflows are projected to grow at a 34.48% CAGR from 2026 to 2031, which is one of the most important shifts in the United Arab Emirates AI copilot market because it moves AI closer to high-value operational work. In financial services, compliance-related process automation is gaining momentum under the Central Bank’s open finance framework and wider regulatory pressure around auditable digital operations. Mashreq’s NeoLC Arabic AI trade finance system illustrates the direction of travel, as it pairs bilingual model outputs with data residency discipline and human review rather than treating AI automation as fully hands-off. The United Arab Emirates AI copilot market size tied to regulated workflow automation is likely to increase as buyers become more comfortable with review layers, audit trails, and bounded deployment models. This means productivity assistance will remain important, but the most strategic expansion in the United Arab Emirates AI copilot market is likely to come from workflows where AI can reduce cycle time, improve compliance handling, and support controlled decision-making in real business operations.

By End-User Industry: BFSI Dominates Revenue, Government Sector Grows Fastest

BFSI accounted for 27.13% of the United Arab Emirates AI copilot market share in 2025, which made it the largest end-user segment by revenue. This position stems from the sector’s stronger digital systems, larger technology budgets, and the direct need to automate documentation-heavy, compliance-intensive work. The 2026 Evident AI Index for Banks placed Emirates NBD, First Abu Dhabi Bank, and Mashreq among the top 10 most AI-mature banks in the Middle East and Africa, while First Abu Dhabi Bank was noted for more than 30 agentic AI use cases in production. In the United Arab Emirates AI copilot market, BFSI also benefits from clearer workflow economics than many sectors because trade finance, customer service, internal review, and document handling all produce visible outcomes when AI support is deployed effectively. That combination of readiness and regulatory need explains why BFSI remains the biggest current revenue contributor.

Government and administration is projected to grow at a 35.82% CAGR from 2026 to 2031, making it the fastest-growing end-user category in the United Arab Emirates AI copilot market. The UAE Government 4.0 program, the plan to transition 50% of federal services to agentic AI within 2 years, and the training program for 80,000 federal employees are all directly increasing demand for structured public-sector deployments. IT and telecommunications are another important adopter group, supported by large-scale deployments and telecom-specific Arabic AI development, while healthcare and life sciences are progressing along a more policy-led, controlled adoption path. Energy and utilities, education, manufacturing, retail, and media also contribute significant demand, but the strongest expansion in the United Arab Emirates AI copilot market is still centered on areas where policy backing, digital maturity, and operational value are already aligned.

Geography Analysis

Abu Dhabi and Dubai account for the largest share of the United Arab Emirates AI copilot market, with Abu Dhabi acting as the sovereign AI and public-sector center and Dubai acting as the main commercial and enterprise deployment hub. Abu Dhabi’s Government Digital Strategy 2025-2027 allocated AED 13 billion (USD 3.5 billion) and targeted 100% sovereign cloud adoption and more than 200 AI use cases across government by 2027, which created the strongest public-sector demand pipeline in the country. The Frontier Employee Program deployed Microsoft 365 Copilot across 35,000 civil servants across 27 entities in 2026, giving Abu Dhabi one of the most visible public-sector rollouts in the regional United Arab Emirates AI copilot market. Abu Dhabi also widened the market base through the Presight and Abu Dhabi Chamber initiative, which supports adoption beyond ministries and very large enterprises, reaching more than 102,000 SMEs. The emirate’s sovereign cloud work with Microsoft and Core42 adds the infrastructure depth needed for regulated and government-led deployments in the United Arab Emirates AI copilot market.

Dubai is the second major demand cluster in the United Arab Emirates AI copilot market and plays a different role from Abu Dhabi, as it is more strongly shaped by enterprise headquarters activity, free-zone flexibility, and commercial go-to-market execution. Dubai Holding’s deployment with Microsoft, OpenAI, and Anthropic created a multi-model enterprise environment across real estate, hospitality, retail, and entertainment, serving as a flagship private-sector reference point in the country. Microsoft’s local processing presence in Dubai also supports cloud-based enterprise adoption by reducing data-handling concerns for large businesses. GITEX Global continues to strengthen Dubai’s position in the United Arab Emirates AI copilot market because country-specific product launches, Arabic AI demonstrations, and vendor partnerships are often announced there before moving into broader deployment.

The northern and eastern emirates still represent a smaller share of the United Arab Emirates AI copilot market, but they are becoming more addressable as bundled pricing, federal training programs, and cloud access reduce the entry barrier for smaller organizations. The federal agentic AI training program for 80,000 government workers spreads capability across institutions in all emirates rather than concentrating workforce preparation in only Abu Dhabi and Dubai. Sharjah’s education and manufacturing profile aligns well with research, learning, and industrial workflow use cases, while firms in Ajman, Ras Al Khaimah, Fujairah, and Umm Al Quwain are more likely to adopt packaged solutions than large, custom enterprise builds. This means the United Arab Emirates AI copilot market is expanding nationwide, even if the largest revenue pools and most visible deployments remain concentrated in the two primary emirates.

Competitive Landscape

The United Arab Emirates AI copilot market shows moderate concentration at the platform layer and broader fragmentation at the application layer. Microsoft holds the strongest enterprise position because it combines a large installed software base with local processing, sovereign deployment relevance, and high-visibility customer references across government and major companies. OpenAI also strengthened its position by launching UAE data residency for business users in November 2025, which improved its appeal in a market where local data handling is becoming a basic buying condition. This gives hyperscaler-linked platforms an advantage in the United Arab Emirates AI copilot market, as many customers prefer a combination of scale, ecosystem familiarity, and compliance readiness over a narrow feature set alone.

A second tier of competition in the United Arab Emirates AI copilot market comes from enterprise AI specialists and regional players that focus on deeper workflow execution, Arabic capability, or more flexible deployment models. Kore.ai’s partnership with G42’s Inception is a strong example because it linked an established enterprise AI platform with local product R&D and sector knowledge that can be applied across regulated and domain-heavy workflows. Presight is also building a meaningful position through its SME-focused partnership with Abu Dhabi Chamber, which gives it access to a large business base that global enterprise platforms may not serve directly. GitLab’s June 2026 governance release and its deeper Claude integration show how specialist vendors are trying to win through secure development workflows, tighter oversight, and better enterprise control rather than general productivity features.

Arabic language depth and sovereign deployment architecture are emerging as the clearest areas of differentiation in the United Arab Emirates AI copilot market. du’s Arabic Telecom Large Language Model and e& UAE’s Arabic-first Telco Copilot show that local language performance is being built into operational systems and internal workflows rather than added later as a surface feature. The largest whitespace appears to be in SME-facing vertical copilots, because smaller organizations need lighter, Arabic-capable, pre-integrated tools at lower cost and lower implementation complexity than many large enterprise platforms are built to provide. That is likely to keep the United Arab Emirates AI copilot market open to new entrants that can balance localization, workflow relevance, and practical deployment simplicity without competing head-on with broad hyperscaler ecosystems.

United Arab Emirates AI Copilot Industry Leaders

Microsoft Corporation

ServiceNow, Inc.

Google LLC

Salesforce, Inc.

OpenAI, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Abu Dhabi Government launched the Frontier Employee Programme in partnership with Microsoft, deploying Microsoft 365 Copilot to 35,000 civil servants across 27 government entities, building on 9,000 existing licenses, as part of Abu Dhabi's commitment to becoming the world's first AI-native government by 2027. The initiative standardizes a single AI productivity platform across the Abu Dhabi public sector and is underpinned by a March 2025 sovereign cloud agreement with Microsoft and Core42 for processing over 11 million daily digital interactions.

- June 2026: The UAE established a federal Artificial Intelligence and Data Authority reporting directly to the Cabinet, unifying the former Office of Artificial Intelligence, the Digital Government Sector, and the UAE Data Office under a single body chaired by the Minister of State for Artificial Intelligence, Omar Al Olama. The authority is mandated to guide national AI and data strategy, operate AI-powered national data platforms, set compliance standards, and strengthen international AI partnerships, providing the unified regulatory interface that enterprise copilot vendors have sought for large-scale federal procurement.

- May 2026: Presight (a G42 company) and the Abu Dhabi Chamber of Commerce and Industry signed a strategic cooperation agreement to deploy agentic AI capabilities across Abu Dhabi Chamber's network of over 102,000 registered small and medium enterprises, in one of the largest SME AI deployment initiatives announced in the GCC. The partnership is structured with an initial pilot cohort and a roadmap to scale across the full SME base, directly supporting the national program to accelerate industrial capability and empower SMEs.

- May 2026: Dubai Electricity and Water Authority became the first UAE government entity to adopt Microsoft 365 Copilot Cowork, marking a shift from information-retrieval copilot use to multi-step task execution across Microsoft 365 applications. The deployment enables DEWA employees to delegate complex, multi-step operations to AI, representing an operational evolution from copilot-as-assistant to copilot-as-agent across government workflows.

United Arab Emirates AI Copilot Market Report Scope

The United Arab Emirates AI copilot market refers to the ecosystem of artificial intelligence-driven intelligent assistants integrated into enterprise and consumer software applications to enhance human capabilities and automate complex tasks within the UAE. These copilots leverage advanced foundation models, including large language models (LLMs) and generative AI, to provide real-time contextual suggestions, generate content, analyze data, and execute workflows seamlessly within existing digital tools. The market encompasses various copilot types ranging from general horizontal productivity tools to specialized functional, technical, and industry-specific solutions. Deployed across cloud, hybrid, and on-premises environments, these AI systems serve organizations of all sizes nationwide. They are used across diverse applications, including knowledge work assistance, software development, customer service, and sales enablement, in industries such as IT, BFSI, healthcare, and government. Driven by the UAE's aggressive digital government initiatives, its ambition to become a global AI leader as outlined in the UAE Strategy for Artificial Intelligence 2031, and the rapid adoption of advanced technologies by both public and private sectors, AI copilots help organizations in the UAE drive operational efficiency, reduce manual cognitive load, and accelerate innovation.

The United Arab Emirates AI Copilot Market Report is Segmented by Copilot Type (Horizontal Productivity Copilots, Functional Workflow Copilots, Technical and Engineering Copilots, and Industry-Specific Copilots), Deployment (Cloud-Based, Hybrid, and On-Premises), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Knowledge Work and Productivity Assistance, Software Engineering and Technical Operations, Customer and Employee Service Operations, Sales, Marketing and Revenue Enablement, Business Process and Enterprise Operations, and Regulated Industry Workflows), and End-User Industry (IT and Telecommunication, BFSI, Healthcare and Life Sciences, Retail and E-Commerce, Industrial Manufacturing, Education and Research Institutions, Media and Entertainment, Government and Administration, Energy and Utilities, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Horizontal Productivity Copilots |

| Functional Workflow Copilots |

| Technical and Engineering Copilots |

| Industry-Specific Copilots |

| Cloud-Based |

| Hybrid |

| On-Premises |

| Large Enterprises |

| Small and Medium Enterprises |

| Knowledge Work and Productivity Assistance |

| Software Engineering and Technical Operations |

| Customer and Employee Service Operations |

| Sales, Marketing and Revenue Enablement |

| Business Process and Enterprise Operations |

| Regulated Industry Workflows |

| IT and Telecommunication |

| BFSI |

| Healthcare and Life Sciences |

| Retail and E-Commerce |

| Industrial Manufacturing |

| Education and Research Institutions |

| Media and Entertainment |

| Government and administration |

| Energy and Utilities |

| Other End-User Industries |

| By Copilot Type | Horizontal Productivity Copilots |

| Functional Workflow Copilots | |

| Technical and Engineering Copilots | |

| Industry-Specific Copilots | |

| By Deployment | Cloud-Based |

| Hybrid | |

| On-Premises | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Knowledge Work and Productivity Assistance |

| Software Engineering and Technical Operations | |

| Customer and Employee Service Operations | |

| Sales, Marketing and Revenue Enablement | |

| Business Process and Enterprise Operations | |

| Regulated Industry Workflows | |

| By End-User Industry | IT and Telecommunication |

| BFSI | |

| Healthcare and Life Sciences | |

| Retail and E-Commerce | |

| Industrial Manufacturing | |

| Education and Research Institutions | |

| Media and Entertainment | |

| Government and administration | |

| Energy and Utilities | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the size of the United Arab Emirates AI copilot market in 2026?

The United Arab Emirates AI copilot market size is USD 0.37 billion in 2026 and is projected to reach USD 1.52 billion by 2031 at a 32.56% CAGR.

Which copilot type leads revenue in the United Arab Emirates?

Horizontal Productivity Copilots led the market in 2025 with 46.74% share because the earliest deployments were tied to existing enterprise productivity suites and broad workplace use cases.

Which deployment model is growing fastest in the United Arab Emirates AI copilot market?

Hybrid is the fastest-growing deployment mode with a 34.61% CAGR from 2026 to 2031 because regulated buyers want cloud performance with tighter local control over sensitive data and workflows.

Why is BFSI the largest end-user segment for AI copilots in the UAE?

BFSI accounted for 27.13% of 2025 revenue because banks already had strong digital foundations, larger AI budgets, and a direct need to automate compliance-heavy and document-rich workflows.

Why are SMEs becoming important buyers of AI copilots in the UAE?

SMEs are the fastest-growing organization-size segment at 35.14% CAGR, supported by lower setup friction, bundled software offers, and initiatives such as the Presight and Abu Dhabi Chamber partnership for over 102,000 SMEs.

What are the main barriers to wider adoption in the United Arab Emirates AI copilot market?

The main barriers are fragmented enterprise data, legacy integration complexity, and governance concerns around hallucinations, auditability, privacy, and human oversight in regulated use cases.

Page last updated on: