Ultra-High Voltage SiC Power Device Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 7.14 Billion |

| Market Size (2030) | USD 16.66 Billion |

| Growth Rate (2025 - 2030) | 18.46% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

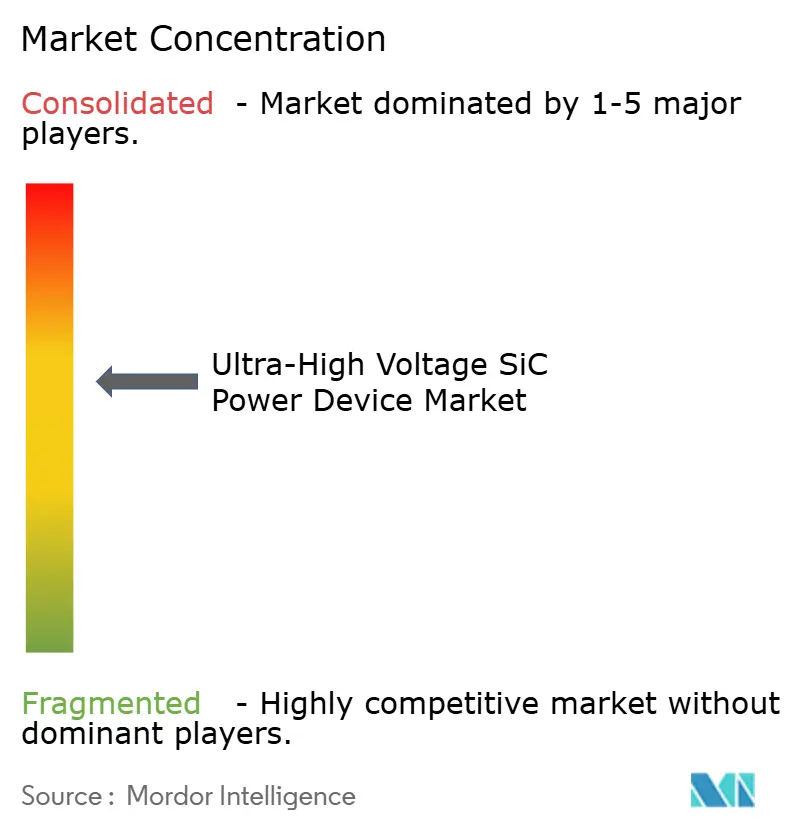

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ultra-High Voltage SiC Power Device Market Analysis by Mordor Intelligence

The ultra-high voltage SiC power device market size is estimated at USD 7.14 billion in 2025 and is projected to reach USD 16.66 billion by 2030, growing at an 18.46% CAGR during the forecast period. Robust grid modernization programs, rising renewable energy penetration, and mounting demand for compact, high-efficiency converters are reshaping procurement priorities across utilities, railways, and aerospace segments. Utilities are replacing silicon-insulated-gate bipolar transistor stacks with wide-bandgap alternatives to reduce conduction losses at voltage levels above 3.3 kV. Rail operators are electrifying mainline routes to meet emissions mandates, while aerospace OEMs are adopting SiC to minimize drivetrain weight. Suppliers able to guarantee 8-inch substrate availability, deliver 6.5 kV-plus module reliability, and provide reference designs for multi-megawatt converters are best placed to capture the next investment wave. Capital intensity remains a hurdle for new entrants, yet vertically integrated incumbents are committing billions of dollars to secure substrate supply and fab capacity, signaling confidence that demand momentum will persist through 2030.

Key Report Takeaways

- By device type, SiC MOSFET modules led with 43.21% revenue share in 2024; SiC MOSFET modules are also forecast to expand at a 19.33% CAGR through 2030.

- By voltage rating, the 3.3-5 kV segment accounted for 39.67% of revenue in 2024, while devices with a voltage rating above 10 kV are projected to register the fastest growth, with a 19.19% CAGR from 2024 to 2030.

- By application, HVDC transmission captured a 37.58% share in 2024; solid-state transformers are expected to advance at a 19.63% CAGR through 2030.

- By end-user industry, electric utilities held 34.93% of the spend in 2024, whereas the aerospace and defense sector is forecast to log the highest 19.52% CAGR to 2030.

- By geography, Asia-Pacific commanded 42.78% of 2024 revenue, and the Middle East is primed for the quickest 19.37% CAGR over the outlook window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ultra-High Voltage SiC Power Device Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in HVDC and FACTS Installations | +4.2% | Global, with concentration in China, Europe, and Middle East | Medium term (2-4 years) |

| Intensifying Global Rail Electrification Projects | +3.1% | Europe, India, China, with emerging activity in North America | Medium term (2-4 years) |

| Renewable-Heavy Utility Procurement Mandates | +3.8% | Global, led by California, EU member states, and India | Long term (≥ 4 years) |

| Accelerated Adoption of Solid-State Transformers | +2.9% | North America and Europe, pilot deployments in Asia-Pacific | Long term (≥ 4 years) |

| Government-Backed Ultra-Fast EV Charging Corridors | +2.6% | United States (NEVI program), EU (AFIR regulation), China | Short term (≤ 2 years) |

| Breakthroughs in 10 kV+ SiC Wafer Yields | +3.4% | Global, with R&D concentrated in United States, Japan, and Germany | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in HVDC and FACTS Installations

Utilities are laying new long-haul links to channel renewable electricity from remote generation clusters to load centers. China’s ±800 kV Gansu-Zhejiang project, commissioned in 2024, exemplifies the multi-gigawatt corridors now under construction. Cross-border initiatives in Europe are expected to add a further 15 GW of transfer capability by 2030. In this setting, ultra-high-voltage SiC modules, rated at 6.5 kV or higher, offer lower switching losses, reduced filter size, and faster converter response times compared to legacy thyristor stacks. The procurement pipeline for flexible AC transmission systems follows a similar trajectory, with India’s Power Grid commissioning static synchronous compensators that utilize SiC valves for millisecond-scale voltage control.[1]Power Grid Corporation of India, “STATCOM Installations and Grid Modernization,” POWERGRIDINDIA.COM Collectively, these grid-expansion and stabilization investments underpin multiyear demand visibility for devices that can withstand harsh thermal cycles, partial discharge, and high dv/dt stress.

Intensifying Global Rail Electrification Projects

Passenger and freight railways are switching from diesel traction to electric propulsion to meet stringent carbon reduction targets. The United Kingdom has earmarked GBP 2 billion (USD 2.5 billion) for 1,000 route miles of new overhead catenary by 2030. In California, Caltrain’s 2024 switch from diesel locomotives to electric multiple units with SiC-based traction converters cut per-mile energy use by 30%. High-efficiency 3.3 kV-6.5 kV modules are pivotal because they reduce cooling hardware, enhance regenerative braking recovery, and increase fleet availability. Japanese Shinkansen trainsets equipped with Mitsubishi Electric’s 3.3 kV full-SiC modules demonstrate the 40% weight savings achievable in power-converter sections, underscoring railways’ willingness to pay a premium for proven reliability over a 30-year service life.

Renewable-Heavy Utility Procurement Mandates

Policy targets embedded in California’s 10.6 GW clean-energy order, the European Union’s 42.5% renewable-electricity goal, and India’s 500 GW solar-and-wind roadmap compel utilities to build large-scale photovoltaic and wind parks.[2]California Public Utilities Commission, “Clean Energy Procurement Mandates,” CPUC.CA.GOV Inverters serving these assets must boost low-voltage, variable output to 3.3 kV or higher while riding through grid faults. SiC switches permit 3-4× higher switching frequency than silicon insulated-gate bipolar transistors, letting integrators shrink inductors and capacitors, cut enclosure footprint, and raise uptime in sandy deserts or offshore turbines. Fuji Electric’s utility-scale solar inverters, which achieve 99% peak efficiency at ambient temperatures above 50 °C, underscore why project developers are increasingly specifying SiC in their technical specifications.

Accelerated Adoption of Solid-State Transformers

Compact, multifunctional solid-state transformers integrate voltage conversion, bidirectional power flow, and harmonic filtering into a single enclosure. ABB’s 1 MVA pilot in Switzerland in 2024 reduced the substation footprint by 30% and delivered real-time voltage regulation, a proof point that is now influencing distribution grid procurement criteria. Siemens Energy’s modular platform achieves 10 kV input using cascaded SiC MOSFET modules, thereby eliminating the need for oil-filled tanks and bulky switchgear.[3]Siemens Energy, “Modular SST Platform and Grid Solutions,” SIEMENS-ENERGY.COM IEEE’s P2004 working group adds interoperability guidelines that reduce perceived technology risk. As utilities pilot more feeders, purchase orders for 6.5 kV-plus SiC modules are set to rise sharply between 2026 and 2030.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited 8-inch SiC Substrate Supply | -2.8% | Global, with bottlenecks in United States, Japan, and Europe | Short term (≤ 2 years) |

| High CapEx for >6.5 kV Fabrication Lines | -2.1% | Global, affecting new entrants and smaller players | Medium term (2-4 years) |

| Reliability Concerns in Harsh-Environment Modules | -1.6% | Middle East, Africa, and offshore applications globally | Medium term (2-4 years) |

| Talent Shortage in Wide-Bandgap Process Engineering | -1.3% | United States, Europe, and Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited 8-inch SiC Substrate Supply

Market momentum continues to outpace crystal growth capacity. Coherent Corporation’s 2024 filing showed that 8-inch wafers still represent less than 15% of total shipments. Wolfspeed’s Mohawk Valley ramp was pushed back two quarters by yield challenges, while ROHM’s Apollo line prioritizes automotive-grade material, leaving industrial and utility customers in allocation queues. Until new furnaces and polishing lines come online after 2026, device vendors must ration high-voltage modules, which forces project developers to stagger their construction schedules.

High CapEx for >6.5 kV Fabrication Lines

Building a cleanroom capable of thick-epitaxial processing, specialized ion implantation, and 2,000 °C annealing routines demands more than USD 500 million. STMicroelectronics’ EUR 730 million (USD 790 million) Catania upgrade and Infineon’s EUR 2 billion (USD 2.16 billion) Kulim expansion illustrate the capital curve. Smaller design houses must rely on foundry partners that accommodate ultra-high voltage runs behind larger automotive programs, thereby delaying the time to market for niche devices. Limited access to scale economics widens the cost gap between incumbents and challengers, slowing competitive churn.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Modules Consolidate Leadership Amid Integration Priorities

SiC MOSFET modules commanded 43.21% of 2024 revenue and are forecast to post a 19.33% CAGR to 2030. This dominance reflects integrators’ drive to standardize thermal interfaces, gate-driver layouts, and insulation distances inside multilevel converters. The ultra-high voltage SiC power device market rewards module vendors who can guarantee isolation performance in accordance with IEC 62109, pass 1,000-cycle thermal-shock tests, and deliver drop-in compatibility with existing racks. Infineon’s CoolSiC 2,000 V module showcases the move toward embedded diodes and digital gate drivers that cut loop inductance and raise system efficiency. In contrast, discretes retain relevance in aerospace power units where weight limits demand bespoke heat spreaders. Schottky diodes and PIN devices complement hybrid half-bridges that retrofit existing substations, enhancing their performance.

Adoption velocity accelerates as 8-inch wafers reach higher yields, enabling suppliers to price modules within 10% of silicon-insulated-gate bipolar transistor equivalents at voltage ratings of up to 6.5 kV. Littelfuse’s AEC-Q101 qualification demonstrates cross-segment readiness, opening automotive traction inverters and light-rail stock to the same module families. ON Semiconductor’s 1,700 V discrete launch serves cost-sensitive solar developers, signaling that the ultra-high-voltage SiC power device industry still values flexible form factors, yet the center of gravity continues to shift toward fully packaged assemblies.

By Voltage Rating: Above-10 kV Devices Move Toward Commercial Readiness

The 3.3-5 kV class held a 39.67% market share in 2024, as railways and industrial drives dominated shipment volumes. However, wafer-defect reduction advances at North Carolina State University have shrunk basal-plane dislocations by 60%, pointing to the potential for reliable 10 kV epi layers by 2027. The ultra-high voltage SiC power device market size for parts above 10 kV is projected to grow at the fastest rate, with a 19.19% CAGR, driven by offshore wind, long-distance HVDC, and aircraft auxiliary power units.

GeneSiC’s 15 kV MOSFET releases prove that edge-termination structures can now manage electric-field grading without catastrophic leakage. Meanwhile, 6.5 kV modules remain the workhorse for present HVDC converter stations, balancing arc-fault resilience with mature packaging know-how. Standards such as IEC 60747-8 add 6-12 months to the design cycle for ultra-high voltage nodes, yet field-failure data from pilot programs is closing the confidence gap.

By Application: Solid-State Transformers Register Breakout Momentum

HVDC transmission remained the largest revenue contributor, accounting for 37.58% in 2024; however, solid-state transformers are expected to post the highest CAGR of 19.63%. The ultra-high voltage SiC power device market share for solid-state transformers is poised to expand rapidly as utilities retrofit urban substations to free up space and enable bidirectional flow. Siemens Energy’s German deployment cut footprint by 40%, a tangible value driver.

Rail traction continues to scale as electrification targets spread to secondary lines in Europe, India, and North America, leveraging SiC to achieve 98.5% efficiency in regenerative braking. Renewable energy power conversion maintains its volume leadership thanks to megawatt-scale solar parks and gigawatt-class offshore wind arrays that integrate SiC inverters for grid-forming capability. EV fast-charging corridors anchor early demand for 1,200 V stages but will migrate to 1,700 V topologies as megawatt chargers surface.

By End-User Industry: Aerospace and Defense Accelerate Electrification

Electric utilities accounted for 34.93% of 2024 shipments, channeling modules into HVDC valves, FACTS banks, and feeder automation systems. The ultra-high voltage SiC power device market is anticipated to experience the steepest 19.52% CAGR from aerospace and defense customers as electric propulsion enters serial production.

Rolls-Royce’s Spirit of Innovation speed record at 555.9 km/h validated the power density gains achievable with SiC in nanosecond-scale switching windows. Rail operators come next, driven by diesel-phase-out mandates, while renewable developers deploy centralized inverters to hit grid-code requirements. EV charging network operators are opening a fluid but fast-growing market as AFIR regulations in Europe and the NEVI program in the United States trigger nationwide charger rollouts.

Geography Analysis

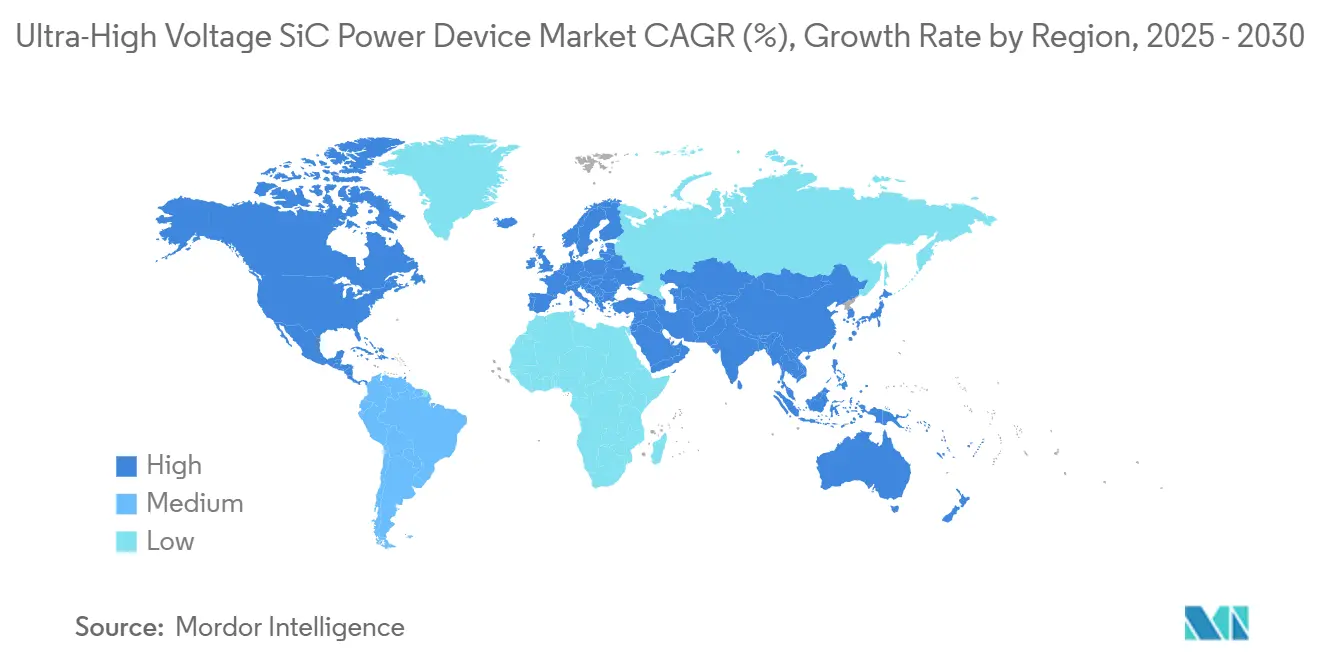

Asia-Pacific remained the revenue anchor at 42.78% in 2024 on the back of China’s 150 GW HVDC fleet and high-speed rail expansion. Japan’s Green Transformation fund funnels JPY 20 trillion (USD 150 billion) into decarbonization projects, including SiC-based railway inverters and offshore wind connections. India converted 10,000 route kilometers to electric traction in 2024 and aims for 100% network electrification by 2030, ensuring sustained module uptake. South Korea’s 20% renewable energy target drives distribution-level upgrades that incorporate SiC solid-state transformers.

The Middle East is expected to deliver the sharpest growth, with a 19.37% CAGR, as energy-exporting economies diversify. Saudi Arabia’s USD 500 billion Vision 2030 program supports HVDC links to connect solar- and wind-powered energy from desert megaprojects to coastal grids. The United Arab Emirates aims to achieve 50% clean electricity by mid-decade, installing SiC-based FACTS devices to stabilize rapidly fluctuating solar output.

Europe invests heavily in 11 cross-border interconnectors under its Projects of Common Interest roster, creating a pan-regional pull for 6.5 kV-plus modules, while North America channels USD 65 billion from the Infrastructure Investment and Jobs Act into grid modernization, seeding demand for both HVDC and solid-state transformers. South America and Africa establish micro-grid pilots that favor modular SiC inverters, offering long-tail incremental volume.

Competitive Landscape

Wolfspeed, ROHM, Infineon, Mitsubishi Electric, and STMicroelectronics collectively controlled approximately 60% of the 2024 revenue. Vertically integrated models prevail as substrate scarcity becomes the decisive constraint on shipment allocation. Wolfspeed’s Mohawk Valley fab, launched in 2024, will triple its wafer output by 2026, reinforcing the firm’s supply advantage.

ROHM’s Apollo facility in Chikugo has an 8-inch capacity but allocates priority lots to automotive traction inverters, leaving industrial users subject to lead-time fluctuations. Infineon’s acquisition of GaN Systems signals an intent to dominate wide-bandgap across the voltage spectrum, while Mitsubishi Electric leans on proven reliability data from Shinkansen trainsets to win rail bids. STMicroelectronics places a EUR 730 million bet on thick-epi lines, eyeing 10 kV devices for European offshore wind converters.

White-space prospects cluster above 10 kV, where GeneSiC’s 15 kV MOSFET introduction and Qorvo’s cascode topologies unlock simplified driver circuitry. Littelfuse’s automotive qualifications extend module reach into both industrial and transportation segments. Intellectual-property filings focus on edge termination and sintered-silver die attach to combat partial-discharge degradation at high altitude. Compliance with IEC 62109 and IEC 60747-8 imposes test-lab investments that favor incumbents with in-house reliability benches; yet, startups continue to exploit foundry capacity to prototype niche solutions, such as ultra-fast EV chargers and aerospace auxiliary power units.

Ultra-High Voltage SiC Power Device Industry Leaders

Wolfspeed, Inc.

ROHM Co., Ltd.

Infineon Technologies AG

Mitsubishi Electric Corporation

Fuji Electric Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Wolfspeed reported fiscal Q3 2025 results covering the January-March 2025 period, with the Mohawk Valley facility reaching 50% of its target production capacity for 200 mm SiC wafers. The company announced that automotive and industrial customer qualifications were progressing ahead of schedule, with volume shipments expected to begin in the second half of 2025 Wolfspeed Investor Relations.

- February 2025: The European Union's Alternative Fuels Infrastructure Regulation mandate took effect, requiring member states to install 150 kW ultra-fast EV chargers every 60 km along Trans-European Transport Network corridors. This regulatory milestone accelerated procurement of SiC-based power-factor-correction stages from suppliers including Infineon, STMicroelectronics, and ON Semiconductor European Commission.

- January 2025: India's Ministry of Railways announced the completion of electrification for an additional 2,500 route-kilometers in 2024, bringing the total electrified network to 96% of broad-gauge routes. The ministry confirmed procurement orders for SiC-based traction converters from Mitsubishi Electric and BHEL to support the remaining 4% electrification target by 2030 Ministry of Railways, India.

- January 2025: China's State Grid Corporation announced that its ±800 kV Baihetan-Jiangsu HVDC transmission line, commissioned in late 2024, successfully completed 3 months of continuous operation with SiC-based voltage-source converters demonstrating 99.2% efficiency. The utility confirmed plans to deploy similar VSC technology in 4 additional ultra-high voltage projects scheduled for 2025-2027 construction State Grid Corporation of China.

Global Ultra-High Voltage SiC Power Device Market Report Scope

The Ultra-High Voltage SiC Power Device Market Report is Segmented by Device Type (SiC MOSFET Modules, SiC MOSFET Discretes, SiC Schottky Diodes, SiC PIN Diodes, SiC Thyristors), Voltage Rating (3.3-5 kV, 6.5 kV, 10 kV, Above 10 kV), Application (HVDC Transmission, Flexible AC Transmission Systems (FACTS), Rail Traction Power, Renewable Energy Power Conversion, Solid-State Transformers, Electric Aircraft Propulsion Systems, Ultra-Fast EV Charging Infrastructure), End-User Industry (Electric Utilities, Rail Operators, Renewable Energy Developers, Industrial OEMs, Aerospace and Defense, EV Charging Network Operators), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| SiC MOSFET Modules |

| SiC MOSFET Discretes |

| SiC Schottky Diodes |

| SiC PIN Diodes |

| SiC Thyristors |

| 3.3–5 kV |

| 6.5 kV |

| 10 kV |

| Above 10 kV |

| HVDC Transmission |

| Flexible AC Transmission Systems (FACTS) |

| Rail Traction Power |

| Renewable Energy Power Conversion |

| Solid-State Transformers |

| Electric Aircraft Propulsion Systems |

| Ultra-Fast EV Charging Infrastructure |

| Electric Utilities |

| Rail Operators |

| Renewable Energy Developers |

| Industrial OEMs |

| Aerospace and Defense |

| EV Charging Network Operators |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Device Type | SiC MOSFET Modules | ||

| SiC MOSFET Discretes | |||

| SiC Schottky Diodes | |||

| SiC PIN Diodes | |||

| SiC Thyristors | |||

| By Voltage Rating | 3.3–5 kV | ||

| 6.5 kV | |||

| 10 kV | |||

| Above 10 kV | |||

| By Application | HVDC Transmission | ||

| Flexible AC Transmission Systems (FACTS) | |||

| Rail Traction Power | |||

| Renewable Energy Power Conversion | |||

| Solid-State Transformers | |||

| Electric Aircraft Propulsion Systems | |||

| Ultra-Fast EV Charging Infrastructure | |||

| By End-User Industry | Electric Utilities | ||

| Rail Operators | |||

| Renewable Energy Developers | |||

| Industrial OEMs | |||

| Aerospace and Defense | |||

| EV Charging Network Operators | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current value of the ultra-high voltage SiC power device market?

The market stands at USD 7.14 billion in 2025 and is projected to reach USD 16.66 billion by 2030.

Which device type leads revenue today?

SiC MOSFET modules hold the largest 43.21% share thanks to their plug-and-play integration benefits.

Why are utilities shifting to SiC for HVDC converters?

SiC devices cut switching losses, shrink filter components, and raise efficiency at voltage levels beyond 3.3 kV.

Which region is expected to grow fastest through 2030?

The Middle East is forecast to advance at a 19.37% CAGR as Saudi Arabia and the United Arab Emirates invest in renewables and HVDC links.

What capacity barriers limit new entrants?

Establishing a >6.5 kV production line requires over USD 500 million in capital outlay and access to scarce 8-inch substrates.

How quickly will above-10 kV devices commercialize?

Yield breakthroughs point to broad market availability by 2027, with a 19.19% CAGR forecast through 2030.

Page last updated on: