UK Travel Insurance Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

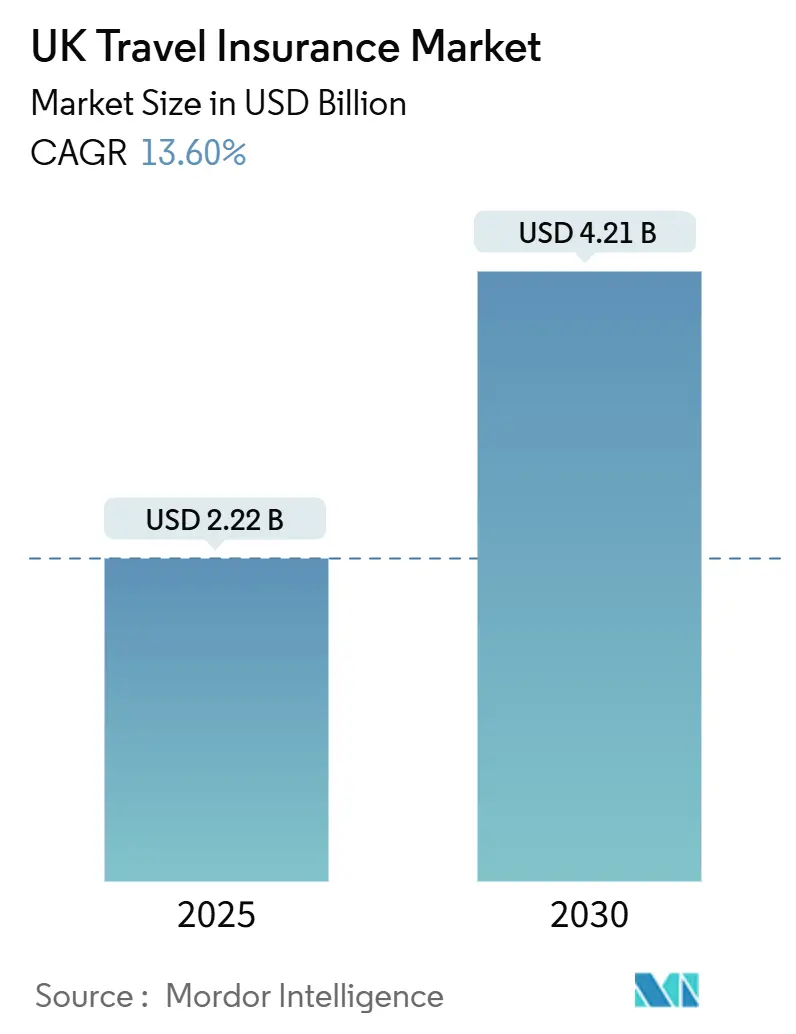

| Market Size (2025) | USD 2.22 Billion |

| Market Size (2030) | USD 4.21 Billion |

| Growth Rate (2025 - 2030) | 13.60% CAGR |

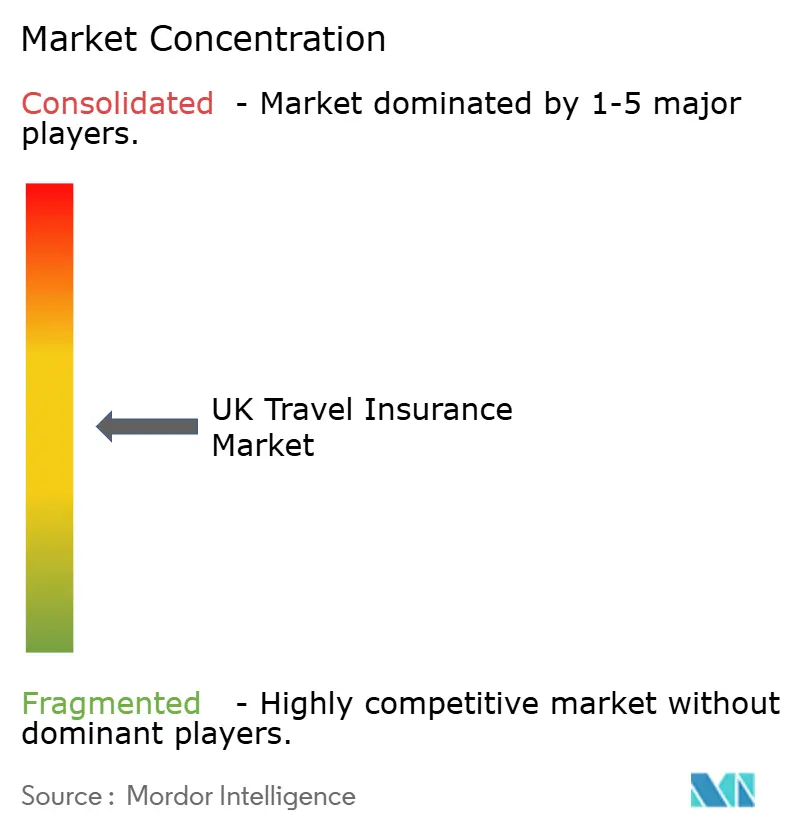

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UK Travel Insurance Market Analysis by Mordor Intelligence

The UK Travel Insurance Market size is estimated at USD 2.22 billion in 2025, and is expected to reach USD 4.21 billion by 2030, at a CAGR of 13.60% during the forecast period (2025-2030). Post-pandemic demand for leisure travel, evolving coverage needs post-Brexit, and a swift shift to digital platforms are propelling growth in the United Kingdom travel insurance market. Online travel booking platforms have seamlessly integrated single-trip policies, driving their volume growth. Meanwhile, comprehensive plans, bolstered by consumers' heightened sensitivity to travel risks, lead in revenue generation. While aggregator platforms dominate online searches and purchases, established insurers are steering customers to their websites, aiming to cut commission costs and harness data insights. While European destinations still hold sway, UK residents are increasingly venturing into the Asia-Pacific, eyeing longer-haul travel. The market is witnessing intensified competition, with global insurers, niche providers, and digital-first entrants leveraging AI for underwriting and claims automation, aiming to boost service speed and curtail costs.

Key Report Takeaways

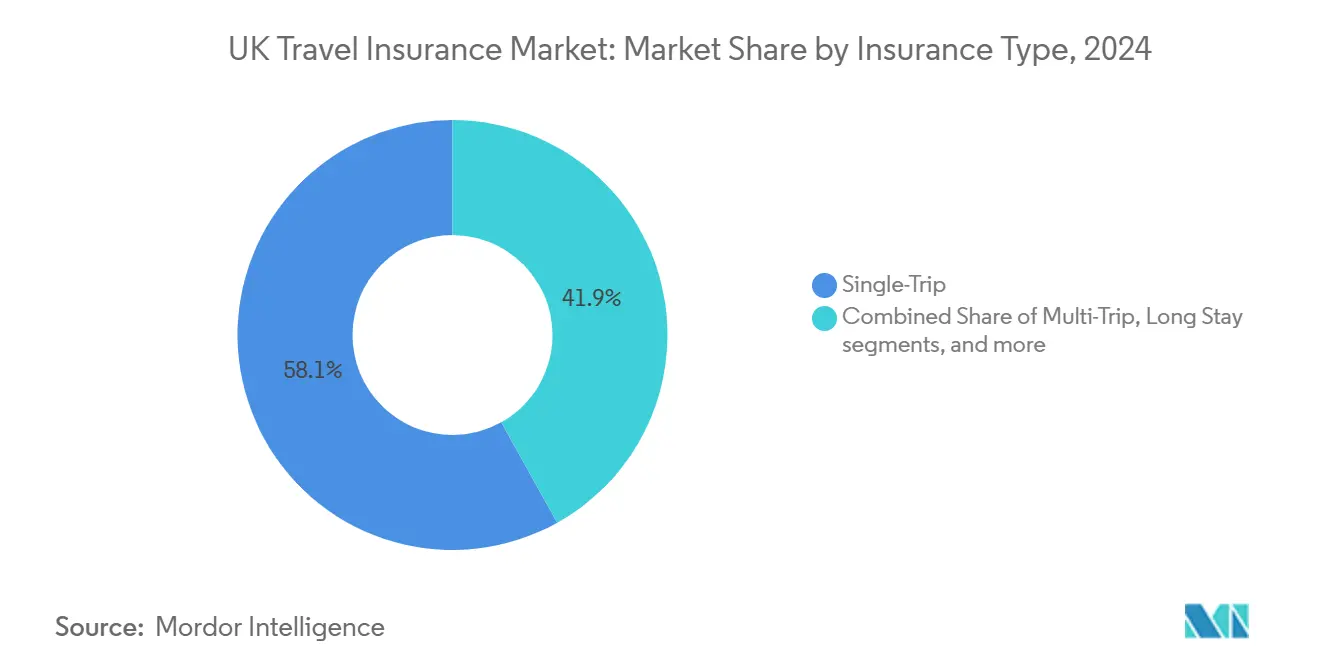

- By insurance type, single-trip policies held 58.1% of the United Kingdom travel insurance market share in 2024; annual multi-trip is forecast to compound at 6.12 % to 2030.

- By coverage, comprehensive plans captured 70.2 % of the UK travel insurance market revenue in 2024; adventure sports add-ons are projected to expand at 6.81% CAGR through 2030.

- By distribution, aggregators controlled 46.3% of sales in 2024, while direct insurer websites are rising at an 8.21% CAGR.

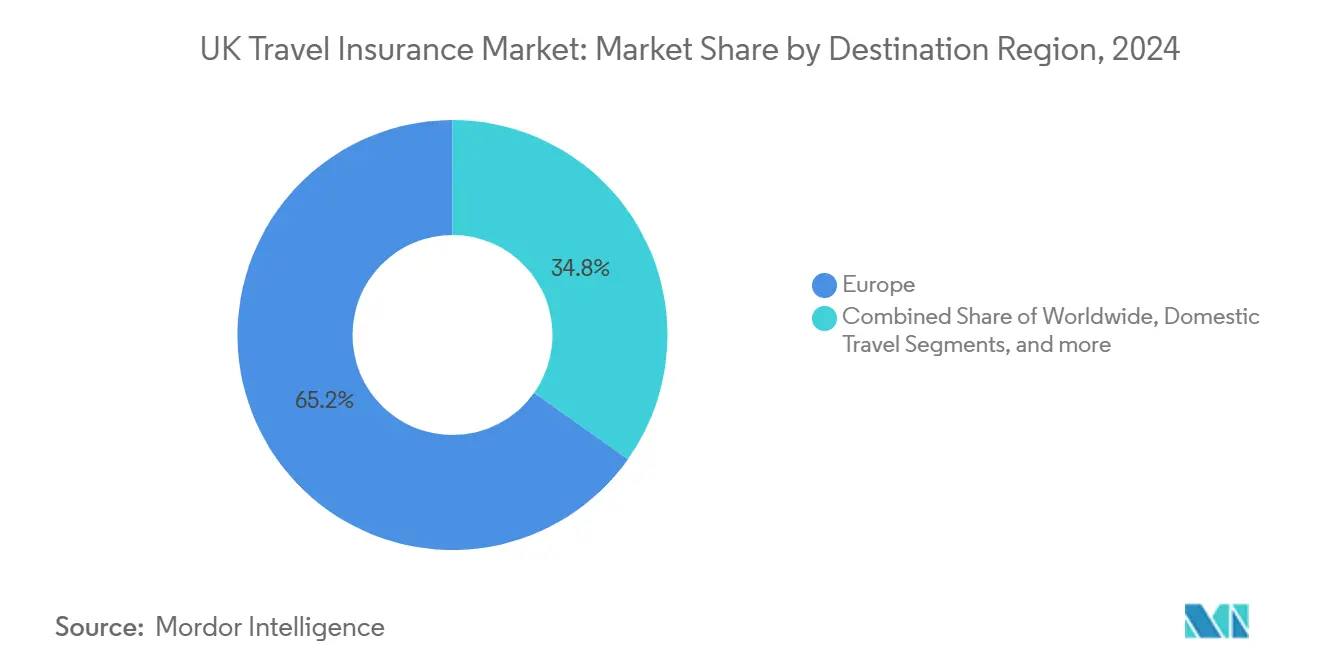

- By destination, Europe accounted for 65.2% of the United Kingdom travel insurance market size in 2024.

- By end-user, individuals represented 78.2% of premiums in 2024; the corporate/SME slice is growing at 5.81 % CAGR on stronger duty-of-care requirements.

UK Travel Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-Brexit medical-cover gaps | +3.2% | European Union | Medium term (2–4 years) |

| Increased outbound travel by UK residents | +4.1% | Global (Europe & Asia-Pacific focus) | Short term (≤ 2 years) |

| Growth in package holidays & specialised travel | +2.5% | Global | Medium term (2–4 years) |

| Digital transformation & online access | +2.8% | National (UK) | Medium term (2–4 years) |

| Heightened risk awareness post-pandemic | +1.9% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Post-Brexit medical-cover gaps driving EU policy demand

UK travellers heading to the EU now face reduced medical coverage due to the shift from the European Health Insurance Card (EHIC) to the Global Health Insurance Card (GHIC)[1]Dean Sobers, “The EHIC and GHIC Explained,” which.co.uk. This change has increased the likelihood of out-of-pocket expenses for private treatments and medical repatriation. In response, insurers are crafting bespoke post-Brexit travel insurance products that enhance GHIC benefits, often streamlining processes for those with chronic health issues. The Financial Conduct Authority (FCA), under its Consumer Duty framework, is emphasizing clearer communication about GHIC's limitations. This push is nudging more travellers towards opting for comprehensive private insurance. With growing awareness, the demand for travel policies focused on Europe is anticipated to persist in the medium term.

Increased international travel by UK residents

As UK residents increasingly venture abroad, the travel insurance market is witnessing a significant upswing. This growth is underpinned by robust household savings, a rekindled enthusiasm for vacations, and a rebound in airline capacities. Travelers are now opting for extended itineraries, especially multi-country jaunts and long-haul trips, leading to heightened average premium values. Popular destinations like Greece, Malta, and Thailand are witnessing a surge in British tourists. In response, insurers are bolstering their offerings, introducing services such as medical tele-consultations and round-the-clock assistance hotlines, ensuring comprehensive support for travelers[2]European Travel Commission, “European Tourism: Trends & Prospects (Q1/2025),” etccorporate.org. . While there's a marked uptick in demand for single-trip policies, this trend also sets the stage for a potential shift towards annual multi-trip plans for those who travel frequently.

Growth in package holidays & specialized travel

In the United Kingdom, a revival in cruises, winter sports holidays, and adventure travel is fueling a surge in demand for customized travel insurance. In response, insurers are rolling out specialized policy modules targeting risks such as cabin confinement, equipment loss, and medical evacuations from high altitudes. Leading tour operators, including TUI, are embedding these insurance covers directly into their booking processes, making it easier for customers and driving higher adoption rates[3]Post Magazine, “Aviva Expects Mid-2025 Completion on DLG Deal,” postonline.co.uk. Furthermore, the rising trend of parametric insurance—providing automatic payouts for incidents like sailing delays—is not only boosting claims satisfaction but also strengthening customer loyalty.

Digital transformation and online accessibility

Incumbent carriers and newcomers are weaving AI into underwriting, fraud screening, and claims triage, compressing cycle times from days to minutes. Fully app-based providers like Giga sure allow on-demand activation moments before boarding, appealing to digital natives who value convenience. Direct channels let insurers harvest behavioral data, create hyper-personal quotes, and retain margin otherwise lost to comparison portals. As web self-service normalizes, the United Kingdom travel insurance market is poised to tilt further toward proprietary ecosystems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Travel-cost inflation reducing discretionary spend | −1.8% | Global (long-haul bias) | Short term (≤ 2 years) |

| Public confusion over GHIC vs private cover | −1.2% | European Union | Medium term (2–4 years) |

| Regulatory compliance burden (FCA Consumer Duty) | −0.9% | United Kingdom | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Travel-cost inflation is squeezing discretionary spend.

In the United Kingdom, rising travel costs, especially soaring airfares and accommodation prices, are straining household budgets. As a result, some travelers are either scaling back their coverage levels or opting out of travel insurance entirely. In 2024, premiums for single-trip policies saw a 7% uptick, with annual multi-trip plans, particularly those targeting older travelers, experiencing even steeper hikes. While modular insurance designs offer customers the flexibility to trim non-essential benefits to curb costs, many price-sensitive segments still grapple with the perceived value of these offerings. Although wage growth might ease some of this financial strain by late 2026, short-term market expansion is likely to be stifled by these discretionary constraints.

Public confusion over GHIC vs private cover leads to under-purchase

In the UK, many travelers are mistakenly equating the Global Health Insurance Card (GHIC) with private travel insurance, leading to a notable under-purchase of travel insurance. A common misconception is that GHIC provides comprehensive medical coverage. However, travelers often overlook key exclusions, including private treatment, repatriation, and support for destinations outside the European Union. This misunderstanding is especially prevalent among those taking short city breaks, who tend to perceive their risk as minimal. Insurers are ramping up educational initiatives, like policy alerts on aggregator platforms and clearer summaries, but shifting public awareness and behavior is anticipated to take several travel cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Insurance Type: Single-trip resilience alongside multi-trip traction

Single-trip plans generated the largest slice of the United Kingdom travel insurance market in 2024, securing a 58.1% share as holidaymakers locked in cover within booking funnels. They thrive on flexibility, letting occasional travellers tailor sums assured to destination risk and season length. Premium uplifts tied to parametric delay protection and instant payout mechanics bolster revenue per policy. The United Kingdom travel insurance market size for single-trip policies is projected to widen steadily on the back of European short breaks and resurgent cruise departures.

Annual multi-trip contracts, while smaller today, are outpacing overall expansion at 6.12% CAGR. Corporates are aggregating staff journeys under blanket programs that tick duty-of-care boxes, and frequent leisure travellers value the convenience of one purchase covering unlimited trips. Mobile dashboards that store policy documents and track live claims further enhance appeal. As traveller frequency normalizes above pre-2020 levels, the segment is set to crowd more space within the UK travel insurance market.

By Coverage Type: Comprehensive dominance with adventure add-ons gaining ground

Comprehensive packages commanded 70.2% % of the UK travel insurance market in 2024 because they bundle medical, cancellation, baggage, and liability in one purchase. Tiered plan structures now allow customers to slide benefit limits up or down while keeping breadth intact, balancing price and protection. Digital elements such as telemedicine and push-notification security alerts enlarge perceived value, reinforcing stickiness.

Adventure sports riders are accelerating as Britons book ski weekends, diving safaris, and mountain-trail treks. Granular risk classification—covering everything from zip-lining to kitesurfing—lets insurers price precisely and stay profitable. Medical-only and cancellation-only options maintain niche relevance for cost-focused travelers, yet their share is unlikely to dislodge the dominance of bundled solutions across the UK travel insurance market.

By Distribution Channel: Aggregator leadership as direct sales surge

Comparison sites held 46.3% of 2024 premiums, testament to their strong SEO positioning and consumer trust in instant price grids. Enhanced filters that sort by excess level and medical-screening tolerance boost usability. However, the sites sometimes obscure nuanced exclusions, fueling FCA concern around informed decisions. Direct insurer sites, though smaller today, are growing 8% CAGR as brands invest in UX, chatbots, and loyalty integration. Owning the interface delivers richer behavioral insight, supporting personalized cross-sell into home or pet lines and lifting lifetime value. Broker and travel agent pathways persist for complex or embedded scenarios, ensuring multichannel diversity within the UK travel insurance market.

By Destination Region: Europe’s anchor with Asia-Pacific ascent

Europe’s enduring proximity delivered a 65.2% share of the UK travel insurance market size in 2024. Frequent weekend hops and budget-carrier routes keep single-trip volumes high. Yet Brexit-induced medical gaps heighten demand for robust cover that supplements GHIC limits. Asia-Pacific volumes, although smaller, are rising 7.51% CAGR as British tourists chase cultural exploration and warmer climates. Dengue flare-ups in Thailand underscore the need for region-specific medical evacuation riders. Worldwide policies that include the USA and Caribbean remain premium-priced due to elevated healthcare costs, a pattern likely to persist.

By End-User: Individual strength alongside corporate opportunity

Individuals accounted for 78.2% of written premiums in 2024, anchored in streamlined mobile purchase journeys and targeted marketing on social platforms. Solo travel is an expanding sub-trend, with 70% of World Nomads policies now bought by single voyagers. Products emphasize emergency GPS location sharing and 24/7 helplines to mitigate perceived vulnerability. Corporate and SME schemes, meanwhile, are gaining 5.81% CAGR as firms tighten duty-of-care governance. Integrated dashboards that map traveller itineraries and push security alerts are fast becoming table stakes for HR departments seeking real-time oversight.

Geography Analysis

European cover retains primacy in the UK travel insurance market as British arrival numbers to Greece, Portugal, and Malta climbed through 2024. The EHIC-to-GHIC shift leaves sizeable treatment and evacuation gaps, steering tourists toward private plans that guarantee direct billing at private clinics plus repatriation if necessary. Price sensitivity is creeping up as hotels and restaurants adjust to stronger euro exchange rates, yet comprehensive policies remain non-negotiable for many families.

Worldwide options that include the USA, Canada, and Caribbean command higher premiums because a single hospital stay in Florida can run into six-figure dollar sums. Insurers load limits accordingly and often bundle pre-trip tele-consultations to triage minor conditions before departure. Demand is steady as long-haul leisure and visiting friends and relatives traffic normalizes.

On the domestic front, staycations within the UK still attract families taking premium cottages or adventure holidays in national parks. Insurers respond with packages that wrap gear cover, cancellation, and severe weather disruption in one certificate, keeping the United Kingdom travel insurance market broadly diversified by destination.

Competitive Landscape

The United Kingdom travel insurance market sits in the middle of the concentration spectrum. Heavyweights such as Aviva Plc, AXA, and Allianz Partners leverage multi-line balance sheets to invest in AI-driven claims modules and expand embedded distribution. Aviva’s rise in UK & Ireland general-insurance GWP in 2024 provides ample capital for product refinement. Allianz Partners broadened reach by aligning with MGA Avid Insurance, keeping underwriting control while accessing niche broker networks.

Specialized brands carve defensible niches. Staysure focuses on travellers over 45 with medical histories, deploying medically screened quotation flows that mainstream insurers find tough to replicate. World Nomads courts adventure seekers and solo explorers through content-rich blogs and community engagement. Insurtech disruptors such as Urban Jungle and Gigasure win younger demographics through transparent pricing, instant activation, and pay-as-you-go modules.

Strategic M&A and alliances mark the landscape. Zurich’s purchase of AIG’s personal-travel unit plugs a North American gap and bolsters scale for its Cover-More subsidiary. Partnerships between tour operators and insurers, exemplified by TUI’s switch from AXA to Allianz Partners, highlight the commercial power of embedded sales. Across the board, digital maturity is widening performance gaps: carriers with automated fraud detection and straight-through settlement see materially lower expense ratios, enabling sharper price-competition without eroding margin.

UK Travel Insurance Industry Leaders

Aviva Plc

AXA UK & Ireland

Allianz Partners

Direct Line Group

Admiral Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Allianz Partners launched cruise-specific cover with Norwegian Cruise Line, embedding quotes at checkout.

- January 2025: Urban Jungle partnered with P J Hayman to launch modular travel policies underwritten by Canopius.

- September 2024: Zurich acquired AIG’s global personal travel insurance arm for USD 600 million to deepen Cover-More’s footprint.

- September 2024: SiriusPoint began underwriting Gigasure’s app-based custom policies featuring instant flight-delay payouts.

UK Travel Insurance Market Report Scope

| Single-Trip |

| Annual Multi-Trip |

| Long-Stay / Backpacker |

| Business Travel |

| Baggage and Personal Effects |

| Medical-Only |

| Trip Cancellation / Curtailment |

| Others (PEMCs, Winter Sports Coverage, Cruise Cover, Adventure Sports/Activities, Cancel For Any Reason (CFAR)) |

| Online Aggregators |

| Direct Insurer Websites / Apps |

| Insurance Brokers / IFAs |

| Travel Agents / Tour Operators |

| Banks & Credit-Card Providers |

| European Coverage |

| Worldwide Coverage |

| Domestic Travel |

| Individuals |

| Families / Groups |

| Corporate / SME Clients |

| By Insurance Type | Single-Trip |

| Annual Multi-Trip | |

| Long-Stay / Backpacker | |

| Business Travel | |

| By Coverage Type | Baggage and Personal Effects |

| Medical-Only | |

| Trip Cancellation / Curtailment | |

| Others (PEMCs, Winter Sports Coverage, Cruise Cover, Adventure Sports/Activities, Cancel For Any Reason (CFAR)) | |

| By Distribution Channel | Online Aggregators |

| Direct Insurer Websites / Apps | |

| Insurance Brokers / IFAs | |

| Travel Agents / Tour Operators | |

| Banks & Credit-Card Providers | |

| By Destination Region | European Coverage |

| Worldwide Coverage | |

| Domestic Travel | |

| By End-User | Individuals |

| Families / Groups | |

| Corporate / SME Clients |

Key Questions Answered in the Report

What is the current value of the UK travel insurance market?

The UK travel insurance market is worth USD 2.22 billion in 2025 and is projected to reach USD 4.21 billion by 2030, growing at 13.6% CAGR.

Why are single-trip policies more popular than annual ones?

Single-trip plans integrate seamlessly into booking sites, offer destination-specific flexibility and appeal to occasional travellers who prefer pay-per-trip simplicity.

How has Brexit affected travel insurance needs?

Brexit replaced EHIC with GHIC, which excludes private treatment and repatriation, driving demand for policies that fill these gaps, especially for European trips.

Which destination region is expanding fastest?

Asia-Pacific coverage is advancing at a 7.5% CAGR because UK travellers are exploring Southeast Asian, Japanese and Australian itineraries more frequently.

Page last updated on: