UHT Cream In Foodservice Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 4.18 Billion |

| Market Size (2031) | USD 5.54 Billion |

| Growth Rate (2026 - 2031) | 5.81% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

UHT Cream In Foodservice Market Analysis by Mordor Intelligence

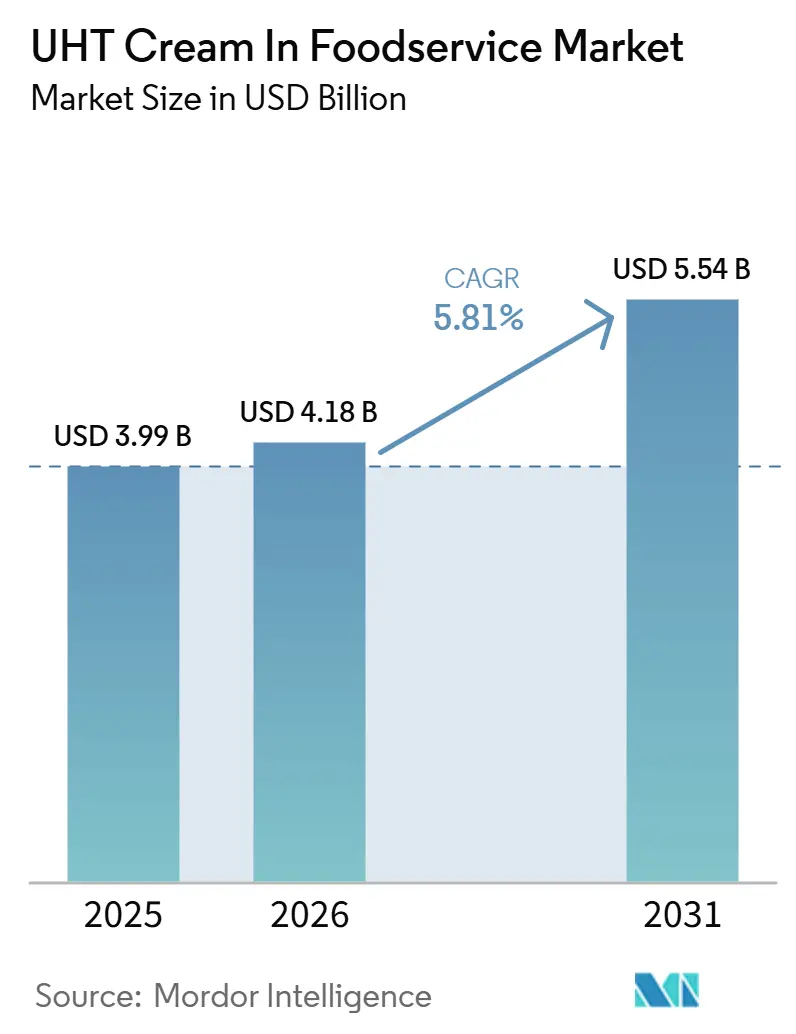

The global UHT cream in foodservice market was valued at USD 3.99 billion in 2025, estimated to reach USD 4.18 billion in 2026, and anticipated to grow to USD 5.54 billion by 2031, at a CAGR of 5.81% during the forecast period. Market growth is driven by increasing demand for shelf-stable dairy ingredients that enhance operational efficiency, reduce food waste, and simplify inventory management across professional foodservice operations. Growing preference for ready-to-use dairy ingredients that support standardized preparation, consistent product quality, and faster kitchen workflows is further accelerating market adoption. Additionally, advancements in UHT processing and aseptic packaging technologies are improving product quality, shelf stability, and functional performance, making UHT cream a more reliable ingredient for commercial foodservice.

Key Report Takeaways

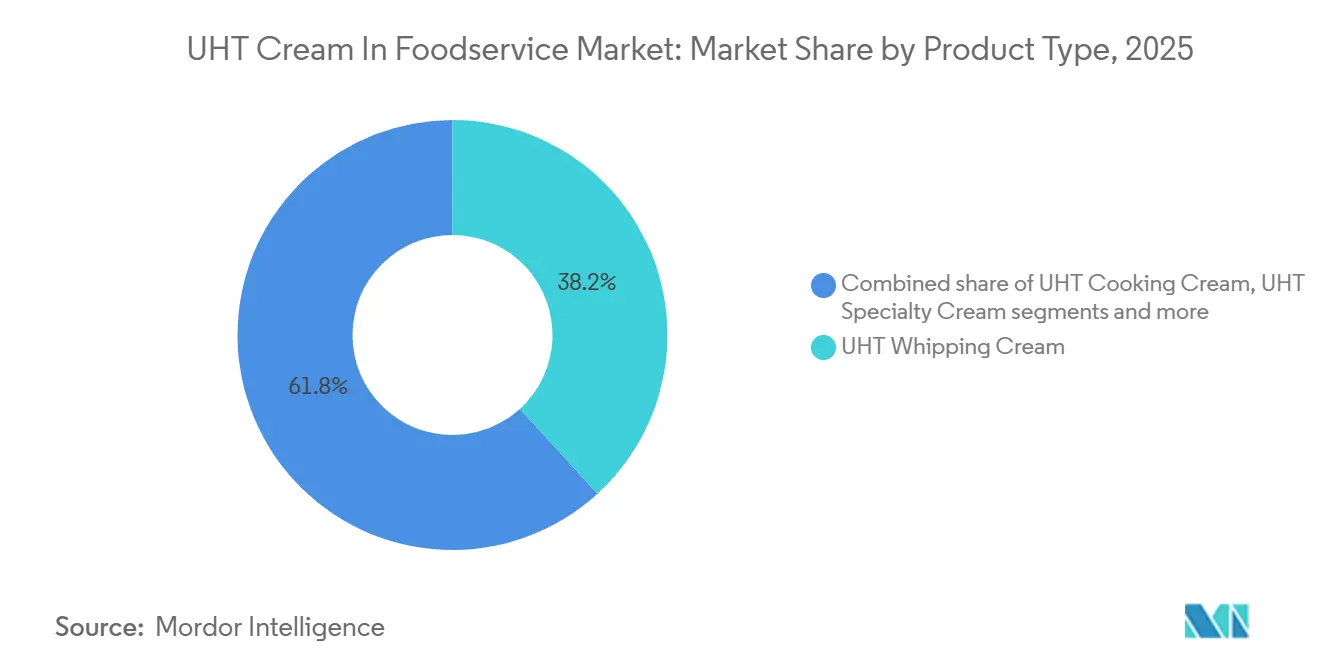

- By product type, UHT whipping cream held a 38.23% revenue share of the global UHT cream in foodservice market in 2025; UHT specialty cream is forecast to expand at a 6.45% CAGR through 2031.

- By packaging format, cartons accounted for a 46.91% revenue share in 2025; plastic tubs are projected to advance at a 6.81% CAGR through 2031.

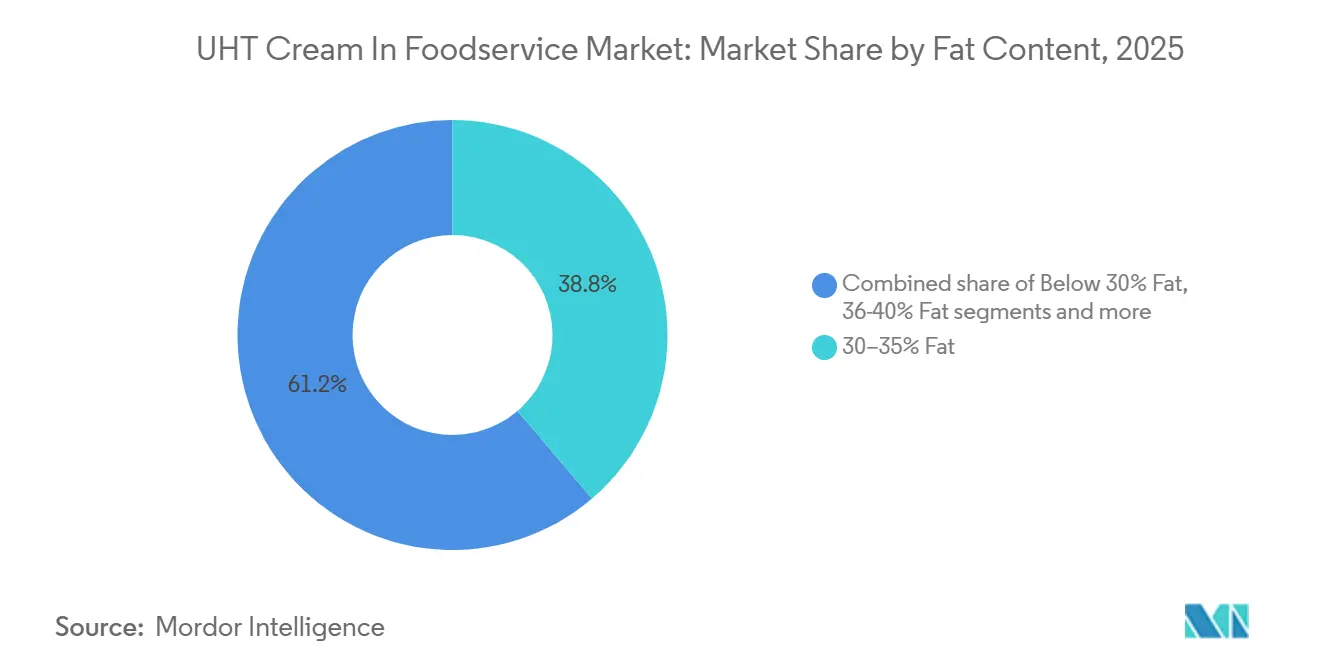

- By fat content, 30–35% fat products represented a 38.76% share in 2025; below 30% fat formulations are expected to grow at a 6.73% CAGR through 2031.

- By foodservice establishment, cafés and bars captured a 34.56% share in 2025; cloud kitchens are anticipated to register the fastest growth at a 6.36% CAGR through 2031.

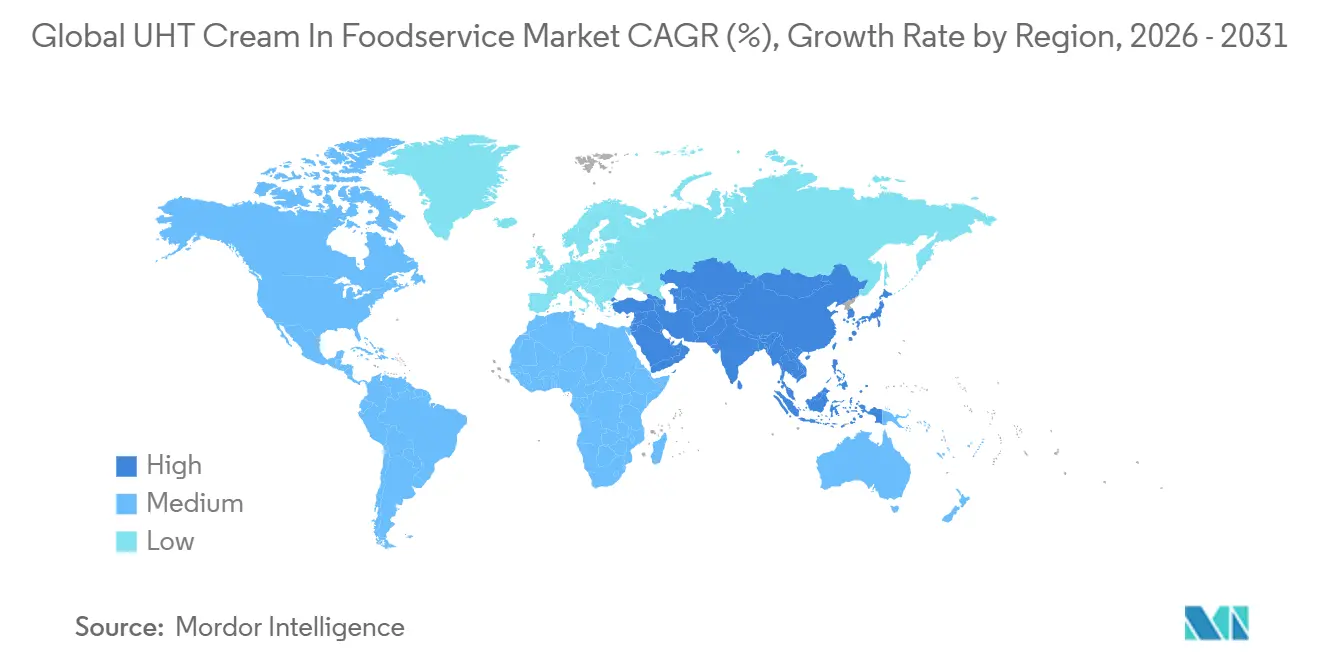

- By geography, North America commanded a 33.21% share of the global UHT cream in foodservice market in 2025; Asia-Pacific is expected to post a 7.34% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global UHT Cream In Foodservice Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for shelf-stable dairy products | +1.5% | Global | Medium term (2–4 years) |

| Increasing focus on food waste reduction | +0.6% | North America and Europe | Medium term (2–4 years) |

| Adoption of ready-to-use culinary ingredients | +0.9% | Global | Short term (≤ 2 years) |

| Rising demand for premium foodservice offerings | +0.8% | Asia-Pacific and North America | Medium term (2–4 years) |

| Innovation in specialty UHT cream products | +0.7% | Global | Short term (≤ 2 years) |

| Growth of organized foodservice supply chains | +0.8% | Asia-Pacific core, spill-over to Middle-East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing demand for shelf-stable dairy products

Growing demand for shelf-stable dairy products is a key driver of the global UHT cream in foodservice market. Foodservice operators increasingly prioritize ingredients that offer longer shelf life, consistent quality, and greater operational flexibility. Unlike conventional refrigerated cream, UHT cream can be stored at ambient temperatures for several months before opening, significantly reducing dependence on cold chain infrastructure during transportation and storage. This extended shelf life helps restaurants, cafés, hotels, catering companies, and institutional kitchens optimize inventory management, lower the risk of spoilage, and reduce product wastage, particularly in operations with fluctuating demand. The ability to maintain product quality over extended storage periods also enables bulk procurement, improves supply reliability, and minimizes delivery frequency, resulting in more efficient kitchen operations.

Increasing focus on food waste reduction

Increasing focus on food waste reduction is driving the market, as commercial kitchens seek ingredients that minimize spoilage and improve inventory efficiency. UHT cream's extended ambient shelf life allows foodservice operators to store products for prolonged periods before opening, reducing expiry-related losses and enabling more accurate inventory planning. This is particularly valuable in restaurants, cafés, hotels, catering services, and institutional kitchens where demand fluctuates considerably. According to the United States Food Waste Pact 2025 Impact Report, the foodservice sector accounts for nearly 13 million tons of food waste annually, highlighting the need for ingredients that help reduce wastage throughout food preparation and storage [1]Source: United States Food Waste Pact, "United States Food Waste Pact 2025 Impact Report, foodwastepact.refed.org. By extending usable storage time and allowing operators to purchase products in larger quantities without compromising quality, UHT cream supports waste reduction initiatives while improving operational efficiency and inventory management across professional foodservice establishments.

Adoption of ready-to-use culinary ingredients

The adoption of ready-to-use culinary ingredients is driving the global UHT cream market in foodservice, as commercial kitchens increasingly prioritize products that simplify food preparation and improve operational efficiency. UHT cream is supplied in a ready-to-use format that eliminates additional processing before use, enabling chefs and kitchen staff to streamline workflows and maintain consistent preparation standards. Its stable composition and reliable performance reduce preparation time, support standardized recipes, and improve productivity during peak service hours. As foodservice establishments continue to address labor shortages, faster order turnaround, and the need for consistent product quality, demand for convenient dairy ingredients that reduce kitchen complexity is increasing.

Rising demand for premium foodservice offerings

Rising demand for premium foodservice offerings is driving the global UHT cream in foodservice market. Consumers increasingly seek high-quality dining and beverage experiences, encouraging foodservice operators to use premium dairy ingredients that deliver consistent taste, texture, and product quality. Premium restaurants, cafés, hotels, and specialty beverage outlets are placing greater emphasis on ingredient quality to differentiate their offerings and improve customer satisfaction. According to the United States Bureau of Labor Statistics, the average food-away-from-home expenditure of United States households reached approximately USD 3,945 in 2024, reflecting sustained consumer spending on dining and foodservice experiences [2]Source: United States Bureau of Labor Statistics, "Average annual food away from home expenditures of United States households", bls.gov. This trend is encouraging operators to adopt premium UHT cream that offers reliable quality, extended shelf life, and operational convenience while supporting consistent menu standards. As foodservice establishments continue to elevate their offerings through premium ingredients and standardized preparation, demand for high-quality UHT cream is expected to grow steadily.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent dairy regulatory compliance | -0.5% | Europe and North America | Long term (≥ 4 years) |

| Fluctuating raw milk availability | -0.6% | Global | Short term (≤ 2 years) |

| Aseptic packaging supply constraints | -0.4% | Global | Medium term (2–4 years) |

| Limited use in premium culinary applications | -0.3% | Western Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent dairy regulatory compliance

Stringent dairy regulatory compliance acts as a restraint on the global UHT cream in foodservice market, as manufacturers must adhere to rigorous food safety, quality, labeling, and traceability requirements across multiple countries and regions. UHT cream producers must comply with strict regulations governing raw milk quality, thermal processing, microbiological safety, packaging integrity, allergen labeling, and product traceability, which increases operational complexity and compliance costs. Differences in regulatory frameworks between markets often require additional product testing, certification, documentation, and packaging modifications before products can be commercialized. Maintaining compliance also requires continuous investment in quality assurance systems, production monitoring, and regulatory audits, creating challenges particularly for smaller manufacturers seeking international expansion.

Fluctuating raw milk availability

Fluctuating raw milk availability restrains the global UHT cream in foodservice market by creating uncertainty in the supply of the primary raw material required for production. Seasonal variations in milk production, adverse weather conditions, livestock diseases, feed quality issues, and changing farming conditions can affect both the volume and quality of raw milk available to dairy processors. These fluctuations may disrupt production schedules, reduce manufacturing efficiency, and lead to inconsistent cream yields, making it difficult for manufacturers to ensure a stable supply to foodservice customers. Additionally, variability in raw milk availability can increase procurement complexity and limit production planning, posing challenges for companies that must consistently meet the requirements of large-scale foodservice operators and long-term supply agreements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Whipping Cream Anchors Volume, Specialty Formats Drive Value Growth

UHT Whipping Cream held the largest product segment share at 38.23% in 2025. This is attributed to its functional performance, long ambient shelf life, and ability to maintain consistent quality throughout storage and handling. Its stability under varying storage conditions reduces spoilage risks and minimizes inventory losses, making it a reliable dairy ingredient for professional foodservice operations. The product delivers consistent whipping volume, stable texture, and uniform aeration, enabling standardized preparation and reducing variability during food production. Its compatibility with automated preparation processes and ease of handling improve operational efficiency while lowering preparation time and labor requirements.

UHT Specialty Cream is the fastest-growing product segment, projected to expand at a 6.45% CAGR from 2026 to 2031. Growth is driven by the increasing demand for differentiated dairy ingredients that address evolving foodservice preparation requirements. As menus become more diverse and technically demanding, foodservice operators require cream products with specific functional characteristics such as improved heat stability, enhanced whipping consistency, better emulsion stability, and controlled texture. This has increased demand for specialized formulations tailored to different preparation methods and performance requirements. In addition, the growing emphasis on product consistency across multiple outlets, reduced preparation errors, and simplified kitchen operations is encouraging the adoption of specialty UHT cream.

By Packaging Format: Cartons Dominate; Plastic Tubs Gain in Delivery-Oriented Channels

Cartons accounted for 46.91% of the packaging market in 2025, driven by their ability to preserve product quality through aseptic packaging while providing extended ambient shelf life and efficient storage. Their lightweight design, ease of transportation, and compatibility with automated filling and dispensing systems make them well suited for high-volume foodservice operations. Cartons also optimize warehouse space, simplify inventory management, and reduce product handling, supporting efficient back-of-house operations. Additionally, their widespread availability and compatibility with existing UHT processing infrastructure have reinforced their position as the preferred packaging format in the foodservice sector.

Plastic tubs are projected to grow at a CAGR of 6.81% from 2026 to 2031, driven by increasing demand for resealable and easy-to-handle packaging that improves operational convenience in professional kitchens. Their wide opening allows easy scooping, portion control, and repeated access during food preparation, helping reduce handling time and product spillage. Plastic tubs also offer greater durability during transportation and storage, making them suitable for high-frequency kitchen use. Furthermore, evolving packaging innovations and regulatory initiatives, such as the European Packaging and Packaging Waste Regulation (PPWR), which introduces recyclability requirements for packaging formats from August 2026, are encouraging the development and adoption of more recyclable plastic packaging solutions, supporting the segment's future growth.

By Fat Content: Mid-Range Fat Leads; Low-Fat Formats Capture Health-Conscious Foodservice

The 30–35% fat content segment accounted for 38.76% of the market in 2025. This fat range offers reliable consistency during processing while maintaining a smooth texture and desirable mouthfeel, making it a preferred specification for professional foodservice operations. It also provides greater formulation flexibility, allowing manufacturers to deliver standardized product quality and dependable performance across a wide range of food preparation conditions. Its ability to balance functionality with efficient ingredient utilization has reinforced its position as the leading fat content category.

The below 30% fat content segment is projected to grow at a CAGR of 6.73% from 2026 to 2031, driven by increasing demand for lighter dairy ingredients that align with evolving menu development trends. Foodservice operators are expanding offerings that emphasize lighter formulations while maintaining desirable texture and consistency, encouraging greater adoption of lower-fat UHT cream. Manufacturers are also investing in formulation technologies that improve the stability, mouthfeel, and performance of lower-fat cream products, making them increasingly suitable for professional food preparation. These advancements, combined with a growing focus on diversified menu options, are supporting the rapid growth of this segment.

By Foodservice Establishment: Cafes and Bars Set the Volume Floor; Cloud Kitchens Establish the Growth Ceiling

Cafés and bars accounted for 34.56% of the market in 2025, driven by increasing emphasis on premium beverage quality, menu innovation, and operational efficiency. These establishments require dairy ingredients that deliver consistent texture, stability, and reliable performance while simplifying storage and inventory management. The long shelf life of UHT cream helps minimize product spoilage and supports uninterrupted operations, particularly in outlets with high-frequency beverage preparation. The continuous introduction of new beverage offerings and growing demand for standardized product quality across café formats have further reinforced the dominance of this segment.

Cloud kitchens are projected to grow at a CAGR of 6.36% from 2026 to 2031, driven by the rapid digitalization of foodservice and increasing demand for delivery-focused meal preparation. These establishments prioritize ingredients that offer extended shelf life, consistent quality, and efficient inventory management to support high-volume production with minimal waste. UHT cream aligns with these operational requirements by reducing storage complexity and ensuring standardized preparation across multiple orders. The continued expansion of online food delivery platforms and delivery-only kitchen models is further accelerating the adoption of UHT cream within this establishment type.

Geography Analysis

North America held 33.21% of the global UHT cream in foodservice market in 2025, supported by its mature and highly organized foodservice industry, widespread adoption of value-added dairy ingredients, and strong preference for standardized food preparation. The region benefits from extensive use of UHT dairy products across commercial kitchens due to their long shelf life, consistent quality, and operational convenience [3]Source: United States Department of Agriculture (USDA), "Food Prices and Spending", usda.gov. According to the United States Department of Agriculture (USDA), food sales at full-service establishments reached approximately USD 488.4 billion in 2025, reflecting the significant scale of professional foodservice demand that continues to support UHT cream consumption. Well-established distribution networks, advanced cold chain infrastructure after product opening, and the growing focus on reducing food waste further strengthen the region's market position.

Asia-Pacific is projected to be the fastest-growing regional market, expanding at a CAGR of 7.34% from 2026 to 2031. Growth is driven by the rapid expansion of café culture, increasing penetration of international and domestic foodservice chains, and the proliferation of cloud kitchens and online food delivery platforms. The region is also witnessing rising adoption of premium dairy ingredients as foodservice operators diversify menus and emphasize product consistency. Continuous investment in modern foodservice infrastructure, increasing availability of UHT dairy products, and expanding organized foodservice networks are expected to further accelerate regional market growth.

Europe represents a mature and well-established market, supported by its strong dairy processing industry, widespread acceptance of UHT dairy products, and extensive presence of professional foodservice operators. South America is experiencing steady market growth, supported by the modernization of the foodservice sector and increasing adoption of shelf-stable dairy ingredients. The Middle East and Africa market is gaining momentum owing to the continued expansion of hospitality and tourism. Increasing investments in hotels, restaurants, cafés, and catering services are driving demand for long shelf-life dairy ingredients that support efficient food preparation and minimize wastage.

Competitive Landscape

The global UHT cream in foodservice market is consolidated, with a mix of multinational dairy processors and regional dairy cooperatives competing on product quality, manufacturing capabilities, and established foodservice relationships. Fonterra Co-operative Group Limited, Arla Foods amba, and Lactalis Group hold prominent positions in the premium UHT cream segment for professional foodservice channels, supported by extensive dairy processing expertise, global production networks, and broad foodservice portfolios.

Competition is increasingly focused on product innovation tailored to the needs of professional foodservice operators. Manufacturers are expanding portfolios with lactose-free UHT cream, high-performance specialty formulations, and multi-functional cook-and-whip creams designed to offer greater versatility across commercial kitchen operations. Companies are also introducing bulk ambient packaging solutions that improve storage efficiency and reduce waste in high-volume institutional foodservice environments, while developing application-specific formulations that provide enhanced stability, consistent texture, and reliable performance under demanding preparation conditions. These innovations are allowing suppliers to differentiate themselves beyond price-based competition.

Technology is becoming a key competitive differentiator as manufacturers invest in advanced UHT processing, aseptic filling systems, and packaging innovations that extend shelf life while preserving product quality and functionality. Companies are improving production automation, quality control systems, and traceability capabilities to ensure consistent product performance and compliance with increasingly stringent food safety requirements. Investments in sustainable packaging materials, recyclable aseptic formats, energy-efficient manufacturing technologies, and digital supply chain management are further strengthening competitive positioning by improving operational efficiency, supporting sustainability objectives, and addressing the procurement requirements of global foodservice customers.

UHT Cream In Foodservice Industry Leaders

-

Arla Foods amba

-

Lactalis Group

-

Nestlé S.A.

-

Danone S.A.

-

Royal FrieslandCampina N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Friesland Campina Ingredients completed the strategic expansion of its Borculo facility in the Netherlands, doubling production capacity to strengthen its global dairy ingredient supply chain and support high-value nutrition markets.

- October 2025: SPX FLOW, through its APV brand, and Arla Foods launched a USD 30 million UHT Center of Excellence at the Lockerbie Creamery in Scotland, focused on scaling production of extended-shelf-life dairy products.

- January 2025: Fonterra has begun construction on a USD 150 million ultra-high-temperature (UHT) cream plant at its Edendale site in Southland, New Zealand, to meet global demand for premium dairy products.

Global UHT Cream In Foodservice Market Report Scope

UHT Cream refers to dairy or plant-based cream sterilized using Ultra-High Temperature (UHT) processing. This makes the product shelf-stable for months without refrigeration until opened. The global UHT cream in foodservice market is segmented by product type, packaging format, fat content, foodservice establishment, and geography. Based on product type, the market is segmented into UHT whipping cream, UHT cooking cream, UHT thickened cream/heavy cream, UHT specialty cream, and other UHT cream types. Based on packaging format, the market is segmented into cartons, plastic tubs, glass jars, and others. Based on fat content, the market is segmented into below 30% fat, 30–35% fat, 36–40% fat, and above 40% fat. Based on foodservice establishment, the market is segmented into cafes and bars, cloud kitchens, full-service restaurants, and quick service restaurants. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. For each segment, the market sizing and forecast have been done based on the value (in USD million).

| UHT Whipping Cream |

| UHT Cooking Cream |

| UHT Thickened Cream/Heavy Cream |

| UHT Specialty Cream |

| Other UHT Cream Types |

| Cartons |

| Plastic Tubs |

| Glass Jars |

| Others |

| Below 30% Fat |

| 30-35% Fat |

| 36-40% Fat |

| Above 40% Fat |

| Cafes and Bars? |

| Cloud Kitchen? |

| Fulll-Service Restaurants? |

| Quick Service Restaurants? |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | UHT Whipping Cream | |

| UHT Cooking Cream | ||

| UHT Thickened Cream/Heavy Cream | ||

| UHT Specialty Cream | ||

| Other UHT Cream Types | ||

| By Packaging Format | Cartons | |

| Plastic Tubs | ||

| Glass Jars | ||

| Others | ||

| By Fat Content | Below 30% Fat | |

| 30-35% Fat | ||

| 36-40% Fat | ||

| Above 40% Fat | ||

| By Foodservice Establishment | Cafes and Bars? | |

| Cloud Kitchen? | ||

| Fulll-Service Restaurants? | ||

| Quick Service Restaurants? | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is driving growth in UHT cream use across foodservice channels?

Growth is being supported by ambient shelf stability, lower waste risk, easier inventory control, and wider use across bakeries, cafés, cloud kitchens, and institutional kitchens. The category is forecast to rise from USD 4.18 billion in 2026 to USD 5.54 billion by 2031 at 5.8% CAGR.

Which region is leading global demand for UHT cream in foodservice?

North America led with 33.21% share in 2025 because of its mature organized foodservice system, broad distributor reach, and strong chain procurement practices.

Which region is expanding the fastest through 2031?

Asia-Pacific is projected to grow at 7.34% CAGR through 2031, supported by café culture growth, cloud kitchen expansion, and large-scale beverage and dessert demand.

Which product segment is growing the fastest?

UHT specialty cream is projected to grow at 6.45% CAGR through 2031 as operators look for barista, low-fat, lactose-free, and multi-function formats with stronger application performance.

Page last updated on: