UAE Frontline Worker Technology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

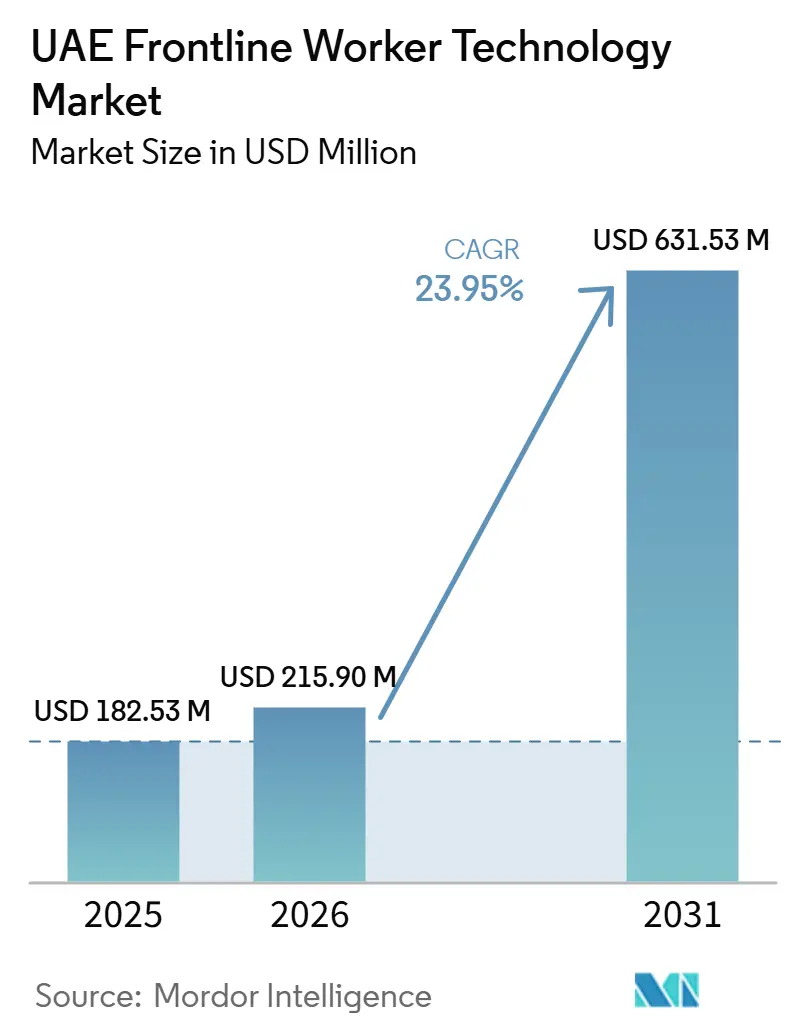

| Base Year Market Size (2025) | USD 182.53 Million |

| Market Size (2026) | USD 215.90 Million |

| Market Size (2031) | USD 631.53 Million |

| Growth Rate (2026 - 2031) | 23.95% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Frontline Worker Technology Market Analysis by Mordor Intelligence

The UAE frontline worker technology market size was valued at USD 182.53 million in 2025 and estimated to grow from USD 215.90 million in 2026 to reach USD 631.53 million by 2031, at a CAGR of 23.95% during the forecast period (2026-2031). The UAE frontline worker technology market is expanding as employers move frontline operations into formal digital systems that support compliance, communication, task visibility, and field execution. Adoption is no longer limited to a narrow set of advanced users, because construction, retail, healthcare, logistics, and public services now face similar pressure to document work, reduce delays, and improve staff coordination. Abu Dhabi remains central to current spending because national energy, industrial, and government entities are deploying connected worker systems at scale, while Dubai supports high software transaction volumes through its dense service, retail, logistics, and municipal operating base. Cloud deployment, platform localization, and AI-enabled workflow tools are widening the addressable opportunity across both large organizations and mid-sized employers. Competitive activity is also shifting from standalone applications to broader platforms that combine mobile workflows, analytics, safety reporting, and workforce oversight, thereby strengthening the recurring revenue potential for vendors active in the UAE frontline worker technology market.

Key Report Takeaways

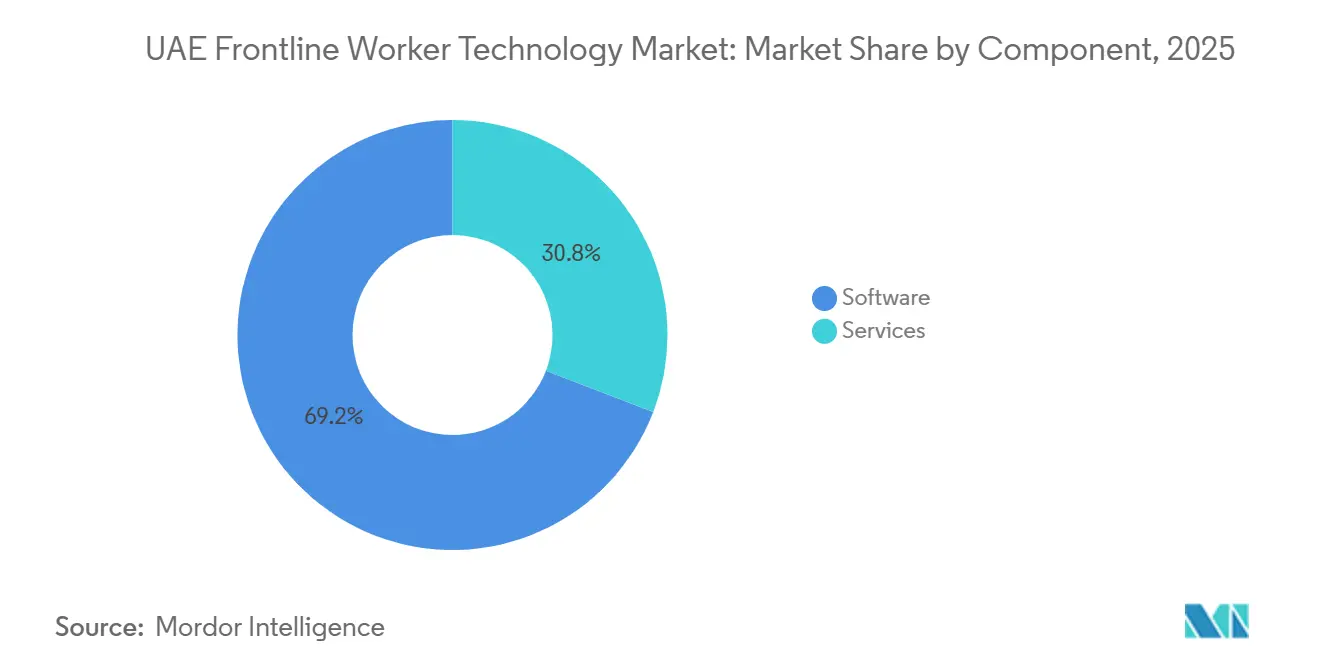

- By component, software held 69.18% of revenue in 2025, while services are projected to expand at a 26.14% CAGR through 2031.

- By deployment, cloud-based deployments accounted for 65.84% of revenue in 2025 and are projected to record the fastest growth at 27.08% through 2031 in the UAE frontline worker technology market.

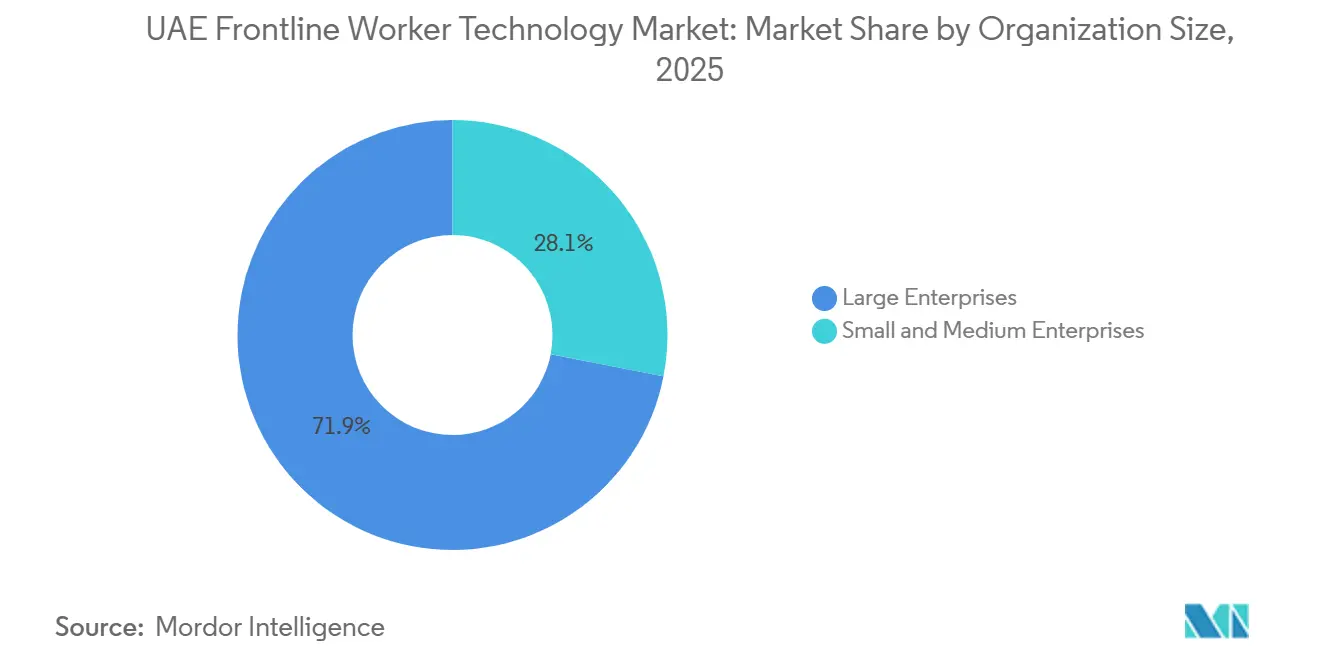

- By organization size, large enterprises accounted for 71.93% of revenue in 2025, while SMEs are expected to expand at a 26.63% CAGR through 2031.

- By application, employee communication and engagement led with a 24.92% share in 2025, while workforce analytics and performance management are projected to advance at a 28.41% CAGR through 2031.

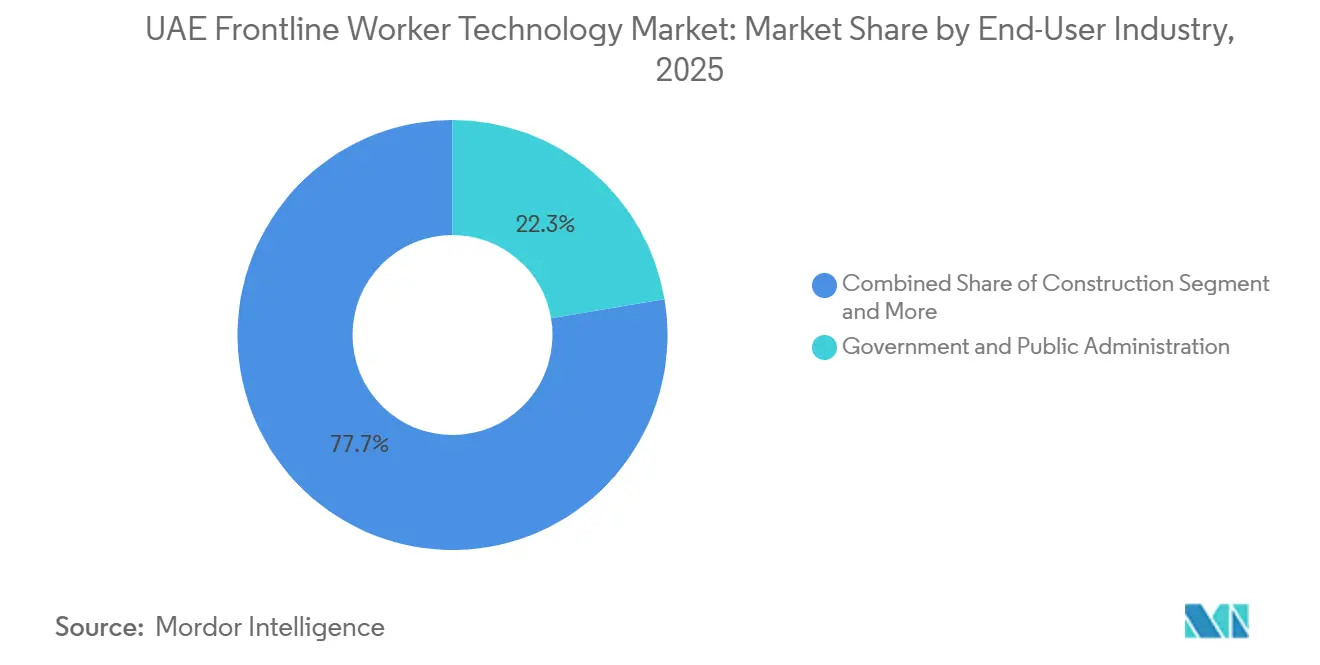

- By end-user industry, government and public administration held 22.34% of revenue in 2025, while healthcare and life sciences are expected to expand at a 27.86% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

UAE Frontline Worker Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Mandates for Digitized Worker Safety Compliance | +4.5% | UAE-wide, concentrated in Abu Dhabi and Dubai free zones | Short term (≤ 2 years) |

| Integration of AI-Guided Workflows With Field Operations | +4.0% | Abu Dhabi, Dubai, UAE government entities | Medium term (2-4 years) |

| Rapid Adoption of Connected Wearables in Hazardous Operations | +3.5% | Abu Dhabi, Sharjah, Ras Al Khaimah, Dubai construction sites | Short term (≤ 2 years) |

| Expansion of Smart City and Industrial Digitalization Programs | +3.0% | Dubai, Abu Dhabi, UAE industrial zones | Medium term (2-4 years) |

| Workforce Productivity Pressure in High-Churn Frontline Roles | +2.5% | UAE-wide, especially retail, hospitality, and construction | Long term (≥ 4 years) |

| Localization of Safety and Workforce Platforms for UAE Enterprises | +2.0% | UAE and broader GCC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Mandates for Digitized Worker Safety Compliance

The UAE frontline worker technology market is benefiting from a compliance environment that now favors continuous digital monitoring over occasional manual audits. Employers are facing stronger expectations for workplace safety documentation, corrective action tracking, and structured reporting, which underscores the value of software that captures field data in real time. The Ministry of Human Resources and Emiratisation launched the AI-powered Smart Safety Tracker at GITEX Global 2025, leveraging generative AI and computer vision to identify violations, generate inspection reports, and recommend corrective actions without extensive manual review.[1]Ministry Of Human Resources And Emiratisation coverage, “MoHRE Launches AI-Powered Smart Safety Tracker for Workers at GITEX Global 2025,” Gulf News, gulfnews.com Gulf News also reported in 2026 that the UAE set 5 mandatory health and safety standards for employers, which reinforced the operational need for auditable worker safety processes across worksites and service locations. As a result, the UAE frontline worker technology market is seeing greater recurring software demand from employers seeking budget-protected compliance systems rather than optional productivity tools.

Integration Of AI-Guided Workflows With Field Operations

The UAE frontline worker technology market is also moving forward as AI-guided workflows shift from pilot programs into scaled operational use. ADNOC expanded its partnership with Microsoft in November 2025 to co-develop and deploy AI agents across operations, following training for more than 40,000 employees and achieving over 70,000 hours of monthly productivity gains from earlier deployments. In May 2026, the UAE launched its first batch of Agentic AI services across government functions and approved a national program to train 80,000 federal workers across 5 capability categories. Oracle announced in February 2026 that e& UAE deployed Oracle Fusion Cloud HCM with embedded AI and generative AI in a sovereign OCI Dedicated Region, demonstrating how workforce systems are tied to national data governance requirements and enterprise-scale automation.[2]Oracle, “e& Drives AI Transformation for Global Workforce With Oracle,” Oracle News, oracle.com This pattern matters because the UAE frontline worker technology market is increasingly being shaped by platforms that connect workforce data, guide actions, and enable policy controls within a single operating layer.

Rapid Adoption Of Connected Wearables In Hazardous Operations

The UAE frontline worker technology market is gaining momentum from industrial wearable deployments that are growing in scale, becoming more structured, and increasingly integrated with enterprise software. In August 2025, Blackline Safety began its rollout with ADNOC under a multi-year agreement covering up to 28,000 connected safety devices and services, including G6 wearable gas detectors and location beacons. Emirates Global Aluminum stated in June 2025 that it was trialing new wearable technology for heat-stress monitoring across Jebel Ali and Al Taweelah, adding real-time health telemetry and location services to its worker safety programs.[3]Emirates Global Aluminium, “EGA Trialling New Wearable Technology as Part of Annual Beat the Heat Safety Programme,” EGA Media Centre, media.ega.ae A 2024 SPE paper on Mubadala Energy described the integration of Edge AI, smartwatch-based wearables, and real-time HSSE monitoring into a unified operational data platform, including automated alerts and fatigue analytics. These deployments show that wearables are no longer isolated safety devices, because they now feed broader analytics, supervision, and workflow systems that enlarge the opportunity for the UAE frontline worker technology market. The same shift also favors vendors that can integrate sensor data, worker communication, and compliance reporting without forcing employers to use separate system stacks.

Expansion Of Smart City And Industrial Digitalization Programs

The UAE frontline worker technology market is drawing support from wider digitalization programs that extend beyond traditional workforce software budgets. Smart city projects, industrial modernization plans, and AI-led operating models are creating follow-on demand for worker-facing interfaces, mobile task execution, and real-time coordination tools. In June 2026, Hydrocarbon Processing reported Honeywell’s live proof-of-concept for Experion Cognition at Borouge International’s Ruwais facility, where the platform predicted alarm incidents 5-10 minutes before they occurred. Oracle’s February 2026 announcement on e& UAE also showed that sovereign cloud infrastructure is being used to support workforce data consolidation and AI-assisted employee workflows at scale. This matters because once infrastructure operators invest in AI, cloud, and operational visibility, the next requirement often becomes worker-level execution software, which lifts software attachment rates across the UAE frontline worker technology market. The effect is especially strong in public-sector, utility, industrial, and logistics settings, where digital control systems must connect with people as well as assets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost Of Rugged Devices And Platform Rollouts | -2.5% | UAE-wide, most acute for SMEs in the Northern Emirates | Short term (≤ 2 years) |

| Data Privacy And Worker Surveillance Concerns | -1.8% | UAE-wide, especially government-adjacent deployments in Abu Dhabi | Medium term (2-4 years) |

| Integration Complexity Across Legacy OT And IT Environments | -1.5% | Abu Dhabi, Sharjah, and Ajman industrial environments | Medium term (2-4 years) |

| Limited ROI Visibility For Smaller And Mid-Sized Employers | -1.2% | UAE-wide, highest exposure in hospitality and retail SMEs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost Of Rugged Devices And Platform Rollouts

The UAE frontline worker technology market still faces a clear affordability barrier, especially outside large enterprise accounts. Rugged handhelds, hazardous-area wearables, smart glasses, and industrial mobile computers require meaningful device spending before employers even begin software, integration, and support costs. Smaller firms in retail, hospitality, construction, and field services often struggle to justify multi-year licensing and deployment commitments when staff turnover is high and workforce tenure is short. This issue is visible in the October 2025 agreement between e& UAE and Honeywell, which introduced a device-as-a-service model for SMB digital transformation that bundled devices, connectivity, and analytics into a lower-entry commercial structure. Even with such models, the UAE frontline worker technology market remains sensitive to total ownership cost because employers still need localization, onboarding, system integration, and ongoing support before full value can be realized.

Data Privacy And Worker Surveillance Concerns

The UAE frontline worker technology market also faces a restraint linked to location tracking, biometric monitoring, and AI-based observation of worker behavior. Platforms that log worker movement, check PPE use via vision systems, or capture health telemetry raise governance concerns that can slow procurement decisions and lengthen internal review cycles. Gulf News reported in 2026 that the UAE set 5 mandatory health and safety standards for employers, keeping worker protection central while also raising expectations for responsible implementation. Oracle’s February 2026 update on the sovereign OCI Dedicated Region deployment for e& UAE also underlined how data residency requirements are shaping enterprise technology choices in sensitive environments. The result is not a collapse in adoption, but a more selective market where vendors must demonstrate governance readiness, alignment with local hosting, and transparent communication with workers before contracts move forward.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Platforms Drive Adoption Economics

Software accounted for 69.18% of the UAE frontline worker technology market share in 2025, which made it the clear revenue leader within the component structure. This leadership reflects the UAE employers' preference for configurable platforms that support communication, compliance, workflow management, and reporting without requiring repeated hardware replacement. The UAE frontline worker technology market has therefore leaned toward software-led procurement in government, oil and gas, logistics, and large healthcare environments where users want faster rollout and easier updates across multiple sites. Oracle stated in February 2026 that e& UAE deployed Oracle Fusion Cloud HCM with embedded AI on a sovereign OCI Dedicated Region, demonstrating how enterprise buyers are placing workforce data, AI functions, and governance needs within scalable cloud software layers. That operating model strengthens recurring licensing and makes software the commercial anchor of many large contracts in the UAE frontline worker technology market.

Services are projected to expand at a 26.14% CAGR through 2031, making it the fastest-growing component of the category mix. This rise shows that deployment complexity is increasing as customers ask for Arabic-language workflow localization, change management, training, and system integration with ERP, HCM, and safety systems. The same trend was evident in e& UAE’s 2026 Oracle workforce transformation, where the platform rollout required coordination across global operations and strict data-sovereignty requirements. For vendors, this means product strength alone is no longer enough, because buyers in the UAE frontline worker technology industry increasingly expect implementation depth and post-deployment support. It also means that service capability is becoming part of competitive differentiation rather than a secondary attach item.

By Deployment: Cloud Architecture Anchors The Platform Strategy

Cloud-based deployment accounted for 65.84% of revenue in 2025 and is the fastest-growing deployment model, with a 27.08% CAGR through 2031. That share shows how strongly the UAE frontline worker technology market favors centralized architectures that can manage distributed workers, devices, and reporting tasks across locations. Employers benefit from over-the-air updates, real-time analytics dashboards, and shared access across field teams, supervisors, and headquarters users. Oracle’s February 2026 sovereign cloud deployment for e& UAE demonstrates that cloud adoption is advancing even in sensitive workforce environments when local data governance can be addressed. The UAE frontline worker technology market is therefore not moving away from the cloud, but toward more controlled and compliant cloud architectures.

Hybrid deployment still matters in regulated and industrial settings where latency, security, or operational continuity limit a full move to public cloud environments. Some petrochemical, government, and classified operating contexts continue to retain local control layers while connecting reporting or analytics to broader digital platforms. This is consistent with the competitive reality of the UAE frontline worker technology market, where vendors must often support mixed estates rather than a simple cloud-only migration path. The legacy system issue is especially relevant in older industrial facilities, because modern APIs and frontline applications do not always connect cleanly with long-established operational systems. That friction slows some projects, but it also creates long-term demand for deployment expertise, middleware capability, and more flexible platform design across the UAE frontline worker technology market.

By Organization Size: Large Enterprises Anchor Demand While SMEs Accelerate

Large enterprises accounted for 71.93% of revenue in 2025, indicating that the UAE frontline worker technology market remains anchored in buyers with scale, compliance exposure, and IT capacity. National energy companies, major healthcare groups, public entities, and logistics operators have the budgets and organizational needs to support end-to-end workforce digitization. ADNOC’s multi-year wearable agreement with Blackline Safety, Burjeel Holdings’ large Oracle Health EMR deployment, and enterprise-scale workforce transformation programs at e& UAE all reflect that pattern.[4]Blackline Safety, “Blackline Safety Begins Rollout With ADNOC Under Multi-Year Purchase Agreement,” Business Wire, businesswire.com These buyers also tend to purchase broader platforms rather than isolated applications, which increases contract value and supports multi-module expansion over time. As a result, large accounts continue to shape product expectations across the UAE frontline worker technology market.

SMEs are projected to expand at a 26.63% CAGR through 2031, making them the fastest-growing segment by organization size in the market. This growth matters because SMEs account for a large share of UAE business activity and employ a substantial portion of the national workforce, even though many still operate with limited internal IT support. The October 2025 device-as-a-service agreement between e& UAE and Honeywell addressed this gap by packaging mobile devices, connectivity, and analytics into a more accessible commercial model for SMBs. The UAE frontline worker technology market will likely see faster penetration in this segment when tools become simpler to deploy, easier to localize, and less dependent on internal technical teams. That creates room for channel-led sales, managed services, and lighter implementation models that differ from the large enterprise approach.

By Application: Analytics Gains Ground On Established Communication Tools

Employee communication and engagement accounted for 24.92% of the UAE frontline worker technology market in 2025, making it the largest application area. This position reflects the fact that many employers begin frontline digitization with multilingual messaging, mobile alerts, shift coordination, and workforce connectivity across dispersed teams. In construction, hospitality, retail, and logistics, communication tools often deliver clear operational value early by reducing missed instructions, improving response times, and creating a direct channel between supervisors and field staff. That early utility has helped communication remain the entry point for many deployments in the UAE frontline worker technology market. It also creates a base layer that can later support analytics, compliance workflows, and task execution modules.

Workforce analytics and performance management are projected to expand at a 28.41% CAGR through 2031, which is the highest growth rate across all application categories. The June 2026 Zebra launch of Nucleus, Workcloud BI, and Workcloud IO showed how vendors are embedding AI-powered dashboards and workflow orchestration more directly into frontline environments. Employers are moving beyond simple communication and now want visibility into execution quality, labor productivity, incident response, and field-level accountability. The UAE frontline worker technology market is therefore shifting toward applications that convert day-to-day worker activity into measurable operational intelligence. Safety and compliance management also remain important because the same data streams can support digital audits, inspection reports, and corrective action tracking when paired with wearable or vision inputs.

By End-User Industry: Government Leads, Healthcare Accelerates

Government and public administration accounted for 22.34% of revenue in 2025, making this segment the largest end-user segment in the UAE frontline worker technology market. This leadership reflects the scale of public service operations across utilities, ports, municipal services, emergency response, and administrative field functions, as well as the UAE’s willingness to adopt digital operating tools at the policy level. The National reported in May 2026 that the UAE launched its first batch of Agentic AI services and approved training for 80,000 federal workers, which signals direct state support for broader workforce digitization. Government demand in the UAE frontline worker technology market also tends to influence private-sector expectations, as public procurement often sets standards for compliance, reporting, and service delivery speed. That gives the segment both direct revenue weight and indirect market-shaping power.

Healthcare and life sciences are projected to expand at a 27.86% CAGR through 2031, which makes it the fastest-growing vertical. Burjeel Holdings launched one of the region’s largest Oracle Health EMR platforms in February 2026 and provided intensive training to more than 3,700 clinical employees, showing how frontline clinical workflows are being digitized at scale. Medcare became the first healthcare provider in the region to adopt an AI-first electronic health record platform in June 2026, which further underlined the move toward AI-enabled clinical workflow support. The UAE frontline worker technology market is benefiting because hospitals and care networks need stronger coordination, faster documentation, and better workforce efficiency in labor-intensive settings. Similar digital needs are also present in logistics, industrial manufacturing, retail, hospitality, and construction, but healthcare is advancing faster because workflow pressure and documentation intensity are both high.

Geography Analysis

Abu Dhabi is the primary demand anchor within the UAE frontline worker technology market, supported by its concentration of oil and gas operators, industrial assets, and government-linked organizations. Large-scale industrial deployment activity gives the emirate a decisive advantage in high-value contracts and complex connected worker programs. In August 2025, ADNOC’s agreement with Blackline Safety covered up to 28,000 connected safety devices and services, setting a clear benchmark for frontline safety infrastructure in the region. The National reported in November 2025 that ADNOC also expanded its AI partnership with Microsoft after more than 40,000 employees had completed AI training and earlier deployments had generated over 70,000 hours of monthly productivity gains. A 2024 SPE paper on Mubadala Energy further showed that Abu Dhabi’s industrial base is integrating Edge AI, wearable monitoring, and unified HSSE data platforms in live operating settings.

Dubai generates a distinct form of strength for the UAE's frontline worker technology market, as it drives high transaction intensity across logistics, retail, hospitality, construction, and service-heavy operations. Demand in the emirate is shaped less by a single dominant industrial cluster and more by a large number of worker-coordination, scheduling, communication, and municipal-compliance use cases. Logistics Gulf reported in June 2025 that Mashreq became the first bank in the GCC to deploy all 3 core SAP Fieldglass modules, which showed that even sectors outside heavy industry are adopting structured workforce management tools. Ghassan Aboud Holding also deployed end-to-end SAP cloud solutions across Grandiose Supermarkets and related businesses in June 2026, linking retail and food operations on a unified platform. These patterns reinforce Dubai’s role as a broad-based software consumption center for the UAE frontline worker technology market.

The Northern Emirates, especially Sharjah, Ajman, Fujairah, and Ras Al Khaimah, form the market’s underpenetrated growth band. Their current revenue base is smaller, but they host meaningful manufacturing and operational labor pools where connected worker tools can improve safety, task visibility, and site coordination. This is where affordability, deployment simplicity, and channel support matter most, because SME concentration is higher and enterprise-style procurement is less common. The e& UAE and Honeywell device-as-a-service model launched in October 2025 is structurally well-suited to this context because it lowers the entry barrier for smaller employers that still need modern workforce tools. As those models become more practical, the UAE frontline worker technology market is likely to widen geographically beyond the large contract centers of Abu Dhabi and Dubai.

Competitive Landscape

The UAE frontline worker technology market is fragmented, with no single vendor controlling demand across all applications, user groups, or end-user industries. Competition includes connected worker specialists, enterprise software providers, industrial automation firms, and device manufacturers that are adding analytics and workflow functions to their installed base. This structure keeps the market open, but it also raises buyer expectations because vendors must demonstrate product depth, deployment capability, and local fit simultaneously. In June 2026, Zebra Technologies launched the Nucleus device management platform along with Workcloud BI and Workcloud IO, expanding its role from hardware support into AI-enabled frontline software and workflow orchestration. That move reflects a wider shift in the UAE frontline worker technology market, where hardware vendors are trying to secure more software and analytics revenue per deployment.

Another visible strategy is deep process integration into industrial and regulated operating environments. Honeywell’s live proof-of-concept for Experion Cognition at Borouge International’s Ruwais facility showed how industrial automation suppliers are moving closer to frontline decision support, with alarm prediction and autonomous control room intelligence tied to operating workflows. Oracle’s February 2026 sovereign cloud workforce deployment for e& UAE also highlighted a second strategy: major enterprise software vendors combining AI capabilities with strong data residency alignment. These moves matter because the UAE frontline worker technology market increasingly rewards vendors that can satisfy workflow needs, compliance controls, and local hosting requirements in a single offering. In practical terms, product breadth and infrastructure readiness are becoming as important as interface quality or feature count.

A third strategy is expansion through more accessible delivery models aimed at the mid-market. The October 2025 agreement between e& UAE and Honeywell bundled devices, 4G and 5G connectivity, managed services, and AI-driven analytics into a format aimed at SMB digital transformation. That model addresses a real gap in the UAE frontline worker technology market, because many smaller employers need practical deployment support more than advanced standalone features. Arabic-language workflow localization and easier onboarding also remain important areas where regional partners can influence vendor success. The field is therefore competitive, but not uniform, because strong positions are being built through vertical expertise, cloud compliance, and go-to-market adaptation rather than scale alone.

UAE Frontline Worker Technology Industry Leaders

Zebra Technologies Corporation

Honeywell International Inc.

Microsoft Corporation

RealWear, Inc.

PTC Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: ADNEC Group received the SAP Adoption Excellence Award, recognizing its enterprise-wide deployment of SAP HCM solutions across multiple operational clusters with distinct workflows and reporting hierarchies. The deployment drove measurable improvements in workforce operations, embedded AI-assisted human capital management, and demonstrated scalability across a complex, diversified organization.

- June 2026: Honeywell demonstrated a live proof-of-concept of Experion Cognition, an AI-enabled autonomous control room platform, at Borouge International's Ruwais facility in Abu Dhabi. The system predicted alarm incidents an average of 5-10 minutes in advance and is set for commercial availability in Q3 2026, marking a significant pivot toward AI-guided workflow intelligence for industrial frontline operators.

- June 2026: Zebra Technologies launched the Zebra Nucleus device management platform alongside Workcloud BI, AI-powered role-based mobile dashboards, and Workcloud IO, workflow orchestration. The launch represents a major expansion of Zebra's frontline software portfolio, enabling real-time operational intelligence directly on frontline devices and standardizing deployment across Zebra's full hardware portfolio.

- June 2026: EMSTEEL Group adopted RISE with SAP, deploying SAP S/4HANA Cloud Private Edition on Microsoft Azure as its core ERP platform. The implementation unified finance, procurement, supply chain, and operational reporting for one of the UAE's largest publicly traded industrial manufacturers, extending standardized digital workflows to frontline production staff.

UAE Frontline Worker Technology Market Report Scope

The UAE Frontline Worker Technology Market Report is Segmented by Component (Software, and Services), Deployment (Cloud-Based, Hybrid, and On-Premises), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Employee Communication and Engagement, and More), and End-User Industry (Retail and E-Commerce, Industrial Manufacturing, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| Hybrid |

| On-Premises |

| Large Enterprises |

| Small and Medium Enterprises |

| Employee Communication and Engagement |

| Workforce Execution and Task Management |

| Workforce Scheduling and Coordination |

| Learning and Knowledge Enablement |

| Workforce Analytics and Performance Management |

| Safety and Compliance Management |

| Other Applications |

| Retail and E-Commerce |

| Industrial Manufacturing |

| Healthcare and Life Sciences |

| Transportation and Logistics |

| Hospitality |

| Construction |

| Government and Public Administration |

| Other Industries |

| By Component | Software |

| Services | |

| By Deployment | Cloud-Based |

| Hybrid | |

| On-Premises | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Employee Communication and Engagement |

| Workforce Execution and Task Management | |

| Workforce Scheduling and Coordination | |

| Learning and Knowledge Enablement | |

| Workforce Analytics and Performance Management | |

| Safety and Compliance Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| Industrial Manufacturing | |

| Healthcare and Life Sciences | |

| Transportation and Logistics | |

| Hospitality | |

| Construction | |

| Government and Public Administration | |

| Other Industries |

Key Questions Answered in the Report

What is the current and forecast size of the UAE frontline worker technology market?

The UAE frontline worker technology market was valued at USD 182.53 million in 2025, stands at USD 215.90 million in 2026, and is forecast to reach USD 631.53 million by 2031 at a 23.95% CAGR.

Which segment leads by component in the UAE frontline worker technology space?

Software led the component mix with 69.18% of revenue in 2025, reflecting employer preference for scalable and configurable digital platforms.

Which deployment model is expanding the fastest in the UAE?

Cloud-based deployment led with 65.84% of revenue in 2025 and is also projected to grow the fastest at a 27.08% CAGR through 2031.

Why are large enterprises still the main buyers of frontline worker platforms in the UAE?

Large enterprises held 71.93% of revenue in 2025 because they face stronger compliance needs, have larger IT budgets, and often deploy multi-module systems across many sites.

Which application area is growing the fastest across frontline worker solutions?

Workforce analytics and performance management is projected to grow at a 28.41% CAGR through 2031 as employers seek better visibility into execution quality and worker productivity.

Which end-user group is creating the strongest growth opportunity through 2031?

Healthcare and life sciences is expected to expand at a 27.86% CAGR through 2031 as hospitals and care networks invest in AI-enabled clinical workflow and workforce coordination tools.

Page last updated on: