UAE Construction Consulting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

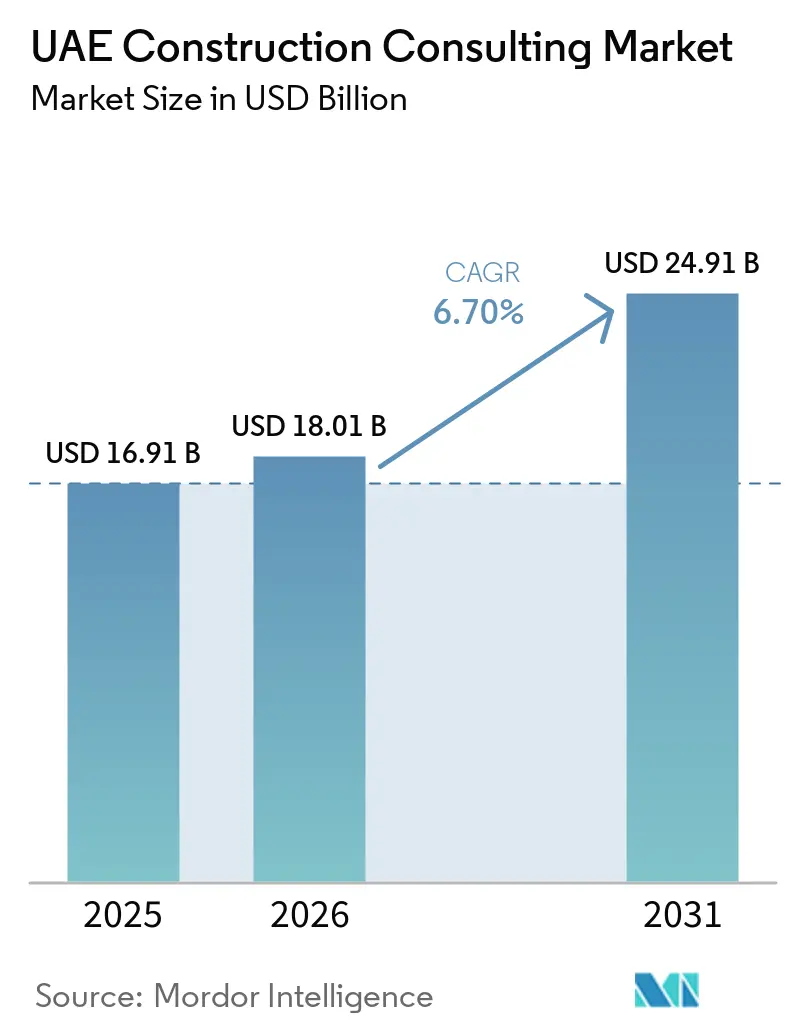

| Base Year Market Size (2025) | USD 16.91 Billion |

| Market Size (2026) | USD 18.01 Billion |

| Market Size (2031) | USD 24.91 Billion |

| Growth Rate (2026 - 2031) | 6.70% CAGR |

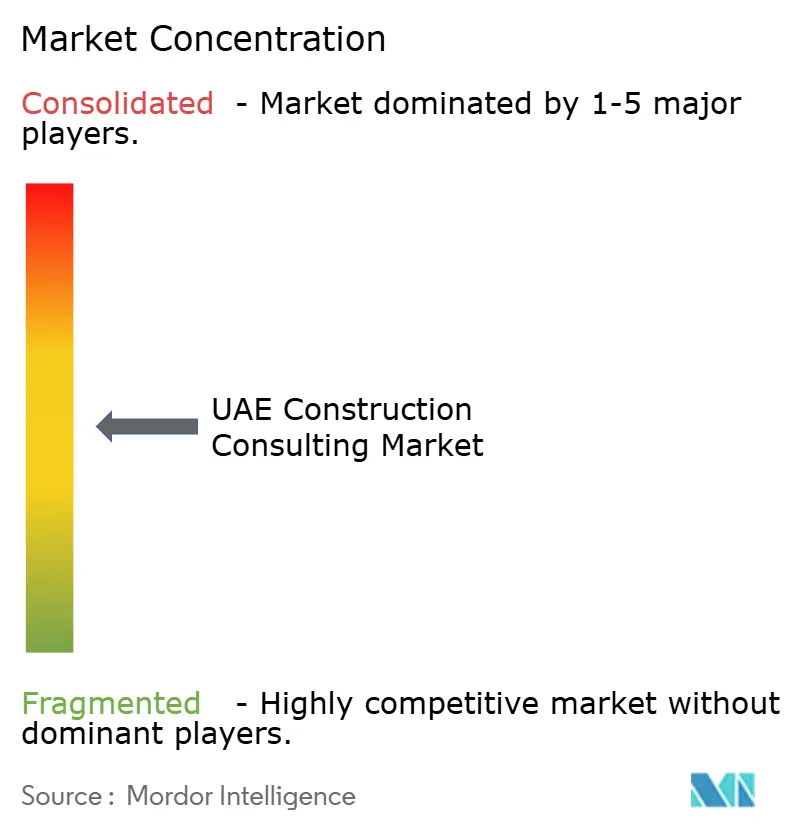

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Construction Consulting Market Analysis by Mordor Intelligence

The UAE Construction Consulting Market size was valued at USD 16.91 billion in 2025 and is estimated to grow from USD 18.01 billion in 2026 to reach USD 24.91 billion by 2031, at a CAGR of 6.70% during the forecast period (2026-2031).

Three structural forces underpin this long-run expansion. First, the federal “Projects of the 50” program and the Dubai 2040 Urban Master Plan together sustain a USD 700 billion capital pipeline that locks in multi-year demand for feasibility, master planning, and project management services. Second, Abu Dhabi’s AED 106 billion (USD 28.9 billion) Emirati housing initiative, launched in September 2025, is driving integrated design work on utilities, district cooling, and community amenities. Third, Dubai Municipality’s mandatory Building Information Modeling (BIM) regime, effective January 2024, elevates the complexity of permit submissions and triggers higher-margin digital-twin consulting engagements. Across these programs, Federal PPP (Public-Private Partnership) Law No. 12 of 2023 has created new advisory opportunities by allowing full foreign ownership of project vehicles, offering sovereign guarantees, and formalizing value-for-money assessments, all of which boost demand for transaction, legal, and technical due diligence services.

Key Report Takeaways

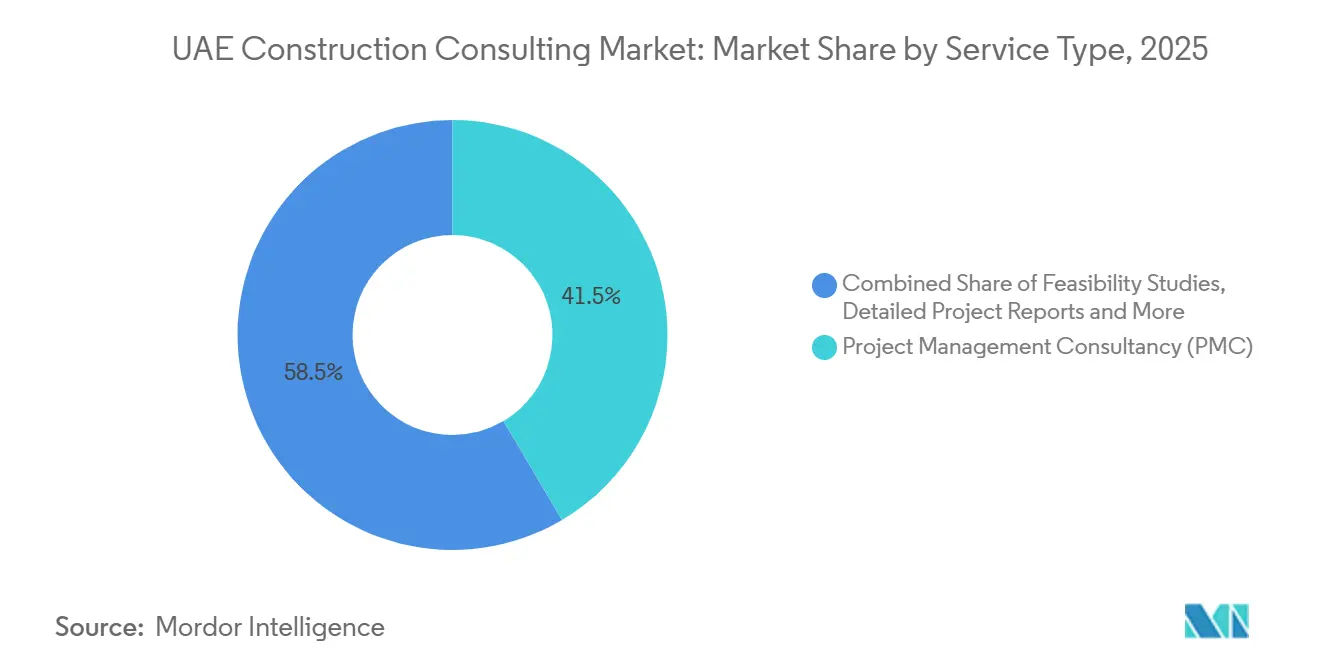

- By service type, project management consultancy captured 41.5% of the UAE construction consulting market share in 2025, while master planning and other advisory work are projected to grow at a 8.05% CAGR between 2026 and 2031.

- By sector, residential projects accounted for 40.5% of the UAE construction consulting market size in 2025, whereas commercial projects are forecast to expand at a 7.78% CAGR over 2026-2031.

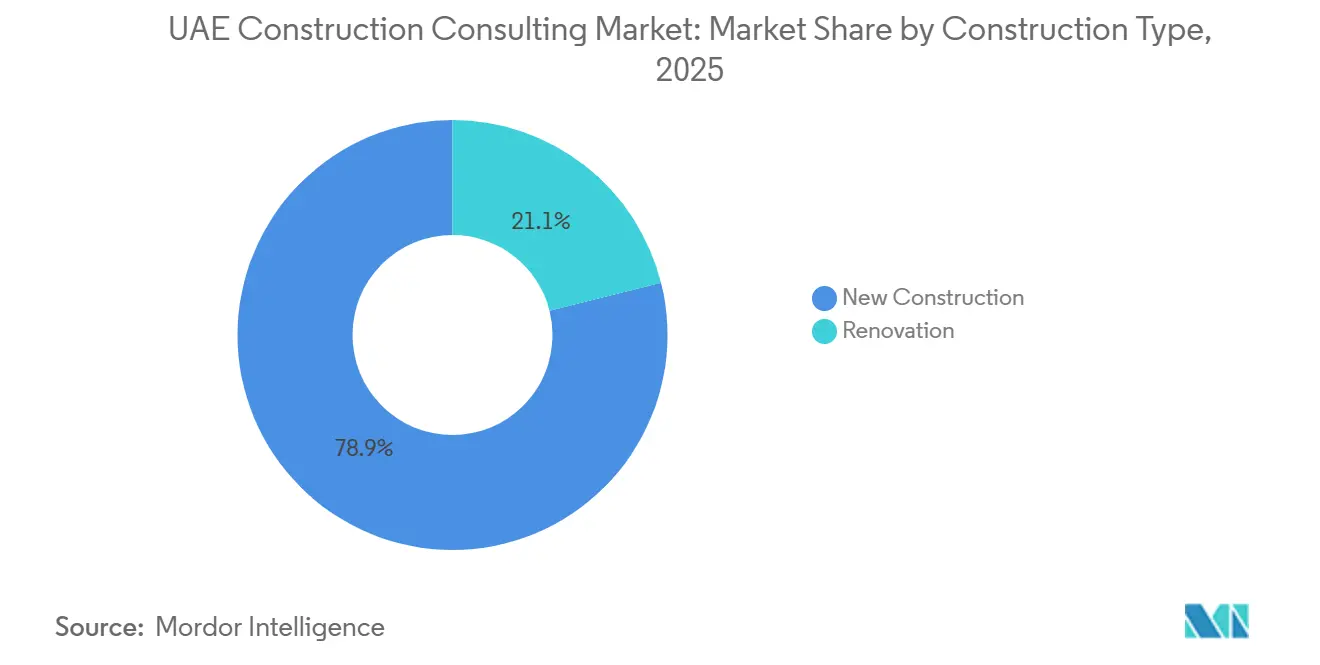

- By construction type, new construction accounted for 78.9% of the UAE construction consulting market share in 2025, and renovation consulting is expected to grow at an 8.30% CAGR through 2031.

- By investment source, private funding accounted for 70% of 2025 spending in the UAE construction consulting market, yet public-sector projects are set to increase at a 8.60% CAGR through 2031.

- By geography, Dubai generated 49.50% of 2025 revenue in the UAE construction consulting market, whereas Abu Dhabi is projected to record the fastest growth at a 7.75% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

UAE Construction Consulting Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| USD 700 billion federal and Dubai 2040 pipelines sustain consulting demand | +1.8% | Dubai & Abu Dhabi | Long term (≥ 4 years) |

| Federal PPP Law No. 12 (2023) unlocks transport and utilities advisory | +1.2% | Nationwide | Medium term (2–4 years) |

| COP28 legacy accelerates net-zero retrofits and carbon audits | +1.0% | Dubai, Abu Dhabi, Ras Al Khaimah | Medium term (2–4 years) |

| Mandatory BIM under Dubai Circular 9-1-2 drives digital-twin work | +0.9% | Dubai | Short term (≤ 2 years) |

| Abu Dhabi Industrial Strategy pushes off-site modular integration | +0.7% | Abu Dhabi | Medium term (2–4 years) |

| Free-zone hyperscale data-center boom requires commissioning expertise | +0.6% | Dubai & Abu Dhabi | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

USD 700 Billion Federal and Dubai 2040 Pipelines Sustain Consulting Demand

Federal megaprojects and Dubai’s 2040 master plan collectively anchor the UAE construction consulting market by ensuring a visible pipeline of mixed-use districts, rail lines, and open-space upgrades. Dubai alone plans to lift its resident base from 3.3 million to 5.8 million by 2040, doubling urban parkland to 42.8 km² and rolling out five transit-oriented centers. Large projects such as the 30 km Dubai Metro Blue Line, now under a five-year PMC mandate with Parsons, illustrate the breadth of integrated design, procurement, and commissioning services required[1]Roads and Transport Authority, “Dubai Metro Blue Line Project Brief,” rta.ae . Feasibility modeling, value-capture studies, and land-phasing advice are growing at double-digit rates as developers rush to lock in approvals before construction costs rise. Consultants positioned early in this cycle secure repeat downstream assignments, reinforcing fee visibility through 2031.

Federal PPP Law No. 12 (2023) Unlocks Transport and Utilities Advisory

Effective December 2023, the federal PPP statute permits two-stage tenders, sovereign guarantees, and full foreign equity participation. Ministries must engage external advisors for financial, legal, and technical appraisals before issuing a request for proposal, thereby expanding the UAE construction consulting market for transaction and risk-allocation specialists. Early pilot projects in federal highways and bulk water transmission are set for issuance in 2027, with consultants steering demand assessment, life-cycle costing, and concession drafting. Because Abu Dhabi and Dubai already run parallel PPP regimes, professionals versed in those frameworks enjoy a first-mover edge under the federal law[2]UAE Ministry of Finance, “Federal Public-Private Partnership Law No. 12 of 2023,” finance.gov.ae .

COP28 Legacy Accelerates Net-Zero Retrofits and Carbon Audits

COP28 galvanized public entities to formalize energy-reduction targets, triggering an 8.30% CAGR outlook for retrofit consulting. Dubai intends to retrofit 30,000 buildings by 2030, a USD 8 billion program projected to cut 1 million tons of CO₂ and save 1.7 TWh of electricity[3]Dubai Electricity & Water Authority, “Dubai Demand Side Management Strategy,” dewa.gov.ae . Ras Al Khaimah’s Resolution No. 18 of 2024 mandates 30% energy savings for government facilities, further enlarging the addressable pool of performance-contract projects. The Emirates Green Building Council’s new retrofit-training certification elevates technical standards, favoring consultants able to bundle energy audits, measurement and verification, and green-finance structuring.

Mandatory BIM Under Dubai Circular 9-1-2 Drives Digital-Twin Work

From January 2024, all Dubai permit submissions for buildings over 20 stories or 20,000 m² must include architectural BIM; structural BIM kicks in above 40 stories. Submissions must use BIM Open format on the Build-in-Dubai portal, compelling firms to invest in interoperable software, cybersecurity, and cloud storage. Compliance adds roughly 5-7% to pre-contract design budgets but raises consultant margins by 15-25% as clients demand integrated clash detection, parametric energy modeling, and IoT-based facility management dashboards. Smaller firms without digital capacity face consolidation or niche outsourcing roles.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expat turnover post-visa reforms inflates labor costs | -0.8% | Dubai & Abu Dhabi | Short term (≤ 2 years) |

| Import-linked cement and rebar volatility upsets cost plans | -0.6% | Dubai, Sharjah, Ajman | Medium term (2–4 years) |

| Permitting disparities outside Dubai lengthen the pre-construction | -0.4% | Northern Emirates | Medium term (2–4 years) |

| Cross-border data-residency gaps heighten BIM cyber risk | -0.3% | Major BIM projects | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expat Turnover Post-Visa Reforms Inflates Labor Costs

Long-term residency visas, introduced in 2023, gave senior engineers greater mobility and bargaining power. Attrition has spiked as professionals exit for Saudi gigaprojects that offer packages up to 30% higher. Firms now pay wage premiums or rely on costly short-term contractors to close skill gaps, squeezing margins on fixed-fee contracts. Without succession pipelines with local universities, mid-size consultancies risk profitability erosion and lost bids.

Import-Linked Cement and Rebar Volatility Upsets Cost Plans

Deformed rebar averaged AED 2,437.87/t in Q4-2025 yet swung 18% year-on-year, while ready-mix concrete hovered near AED 268.01/m³. Because materials account for almost half of total build costs, feasibility models become rapidly outdated, forcing advisers to add contingencies that can price bids out of the competition. Smaller firms without proprietary cost-tracking tools face renegotiations and reputational damage when budgets blow out.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Project-Management Consultancy Retains Primacy, Master Planning Climbs

Project management consultancy accounted for 41.5% of 2025 revenue, underscoring its centrality to multidisciplinary coordination on megaprojects. The Dubai Metro Blue Line proves the point: Parsons oversees design reviews, procurement, construction supervision, and handover phases for a 14-station network projected to serve 320,000 daily riders. Fee structures increasingly peg remuneration to milestone delivery, tightening alignment between consultant performance and client cash flow.

Master planning and other advisory services are projected to grow at a 8.05% CAGR through 2031, reflecting a strategic shift toward front-end value creation. WSP’s January 2026 appointment to reimagine the 5 million m² Jebel Ali Racecourse redevelopment demonstrates how clients now demand urban design, LEED ratings, mobility analytics, and geotechnical studies under one roof. Firms that can pivot from early-stage land-use strategy to BIM-enabled detailed design retain clients across the entire delivery continuum, thereby expanding their share of the UAE construction consulting market.

By Sector: Residential Dominates, Commercial Outpaces

Residential work accounted for 40.5% of 2025 billings, as government entities prioritized social-housing allocations. Mohammed Bin Rashid Housing Establishment earmarked AED 5.4 billion (USD 1.47 billion) for 3,004 homes across six districts, guaranteeing a steady stream of infrastructure, utilities, and community-facility tasks. Consultants adept at navigating freehold regulations, deed registration, and citizen-eligibility criteria emerge as preferred partners.

Commercial projects, spanning office, retail, logistics, and hyperscale data centers, are slated to expand at a 7.78% CAGR through 2031 on the back of Dubai’s D33 Economic Agenda and Abu Dhabi’s industrial diversification. Terralogix Logistics Park’s 3.3 million ft² footprint in Al Warsan and Microsoft’s 200 MW data-center rollout within Khazna hubs illustrate niche advisory opportunities in high-bay warehouse design, energy-efficient cooling, and Tier III+ certifications. Together, these trends steadily increase the UAE construction consulting market share for commercial assignments.

By Construction Type: New-Build Rules, Renovation Gains Traction

New projects accounted for 78.9% of 2025 consulting revenue, driven by greenfield districts such as Dubai South’s HAYAT community and Abu Dhabi’s Yas Canal villas. Consultants remain embedded for up to eight years, covering everything from concept master plans to commissioning.

Renovation assignments, however, show the fastest velocity with an 8.30% CAGR outlook. Dubai’s plan to invest USD 8 billion in retrofitting 30,000 existing buildings incentivizes energy audits, measurement and verification, and ESCO contract design. Ras Al Khaimah’s Resolution 18/2024 adds a structured accreditation regime, raising professional barriers and cementing premium rates for established engineering firms.

By Investment Source: Private Capital Leads, Public Spending Accelerates

Private developers accounted for 70% of 2025 fees as groups like Aldar Properties and Emaar pressed ahead with backlog pipelines exceeding USD 54 billion. Consultants supply brand-led placemaking, sales-center mock-ups, and phased infrastructure delivery that sync with off-plan sales.

Public-sector work is forecast to climb at an 8.60% CAGR, tied to the USD 8.16 billion Tasreef stormwater upgrade and the USD 1.63 billion Fourth Federal Corridor. PPP Law No. 12 gives ministries clear authority to hire external advisers, ensuring a broader competitive field and increasing the overall size of the UAE construction consulting market allocated to public works.

Geography Analysis

Dubai generated 49.50% of market revenue in 2025, thanks to its transparent permitting regime, mandatory BIM framework, and a USD 680 million second-phase expansion of the Tasreef drainage program. Signature projects from the 30 km Metro Blue Line to the Jebel Ali mixed-use redevelopment fill consultant order books across project management, utilities, and digital engineering. Government entities routinely package scope across design, sustainability, and asset handover, preserving fee continuity for multidisciplinary firms.

Abu Dhabi, projected to grow at a 7.75% CAGR, is in heavy build-out mode. The AED 28.9 billion housing initiative, USD 2.72 billion in industrial-strategy incentives, and the USD 1.5 billion 1.5 GW Khazna solar plant present sustained advisory opportunities. The KEZAD expansion weaves together auto, food, and light-manufacturing hubs, drawing on master planning, transport modeling, and circular-economy compliance expertise. Consultants who can secure in-country value certification help clients unlock preferential procurement ratings, making local know-how as critical as technical expertise.

The Northern Emirates collectively supply the remainder. Sharjah’s 300,000 t/yr waste-to-energy complex and the Emirates Road widening to 25 km signal an uptick in heavy-engineering advisory work. Ras Al Khaimah’s mandatory energy-saving decree funnels retrofit demand to firms with ESCO accreditation experience. At the same time, Ajman and Umm Al Quwain depend on federal corridor links that now require holistic transport and stormwater modeling. Uneven permitting regimes outside Dubai lengthen project gestation but also expand revenue for consultants skilled at multi-agency coordination.

Competitive Landscape

The UAE construction consulting market is moderately concentrated, with AECOM, Atkins-SNC Lavalin, WSP, Parsons, and Jacobs collectively accounting for 55-60% of total billings, while regional specialists share the remainder. These global firms leverage advanced digital-twin capabilities, strong financial positions, and multidisciplinary teams to comply with Dubai’s mandatory Building Information Modeling (BIM) regulations. To address rising fee pressures, they bundle project management, cost control, and sustainability analytics into single contracts. Many collaborate with local architects and quantity surveyors to meet licensing requirements while retaining design leadership. Talent retention remains a challenge, but firms that offer in-house upskilling programs better manage wage inflation.

Recent project wins highlight strategic execution by leading firms. Parsons secured a five-year project management consultancy contract for the Dubai Metro Blue Line, while AECOM leads infrastructure consulting for KEZAD’s industrial expansion. WSP is managing the master plan for the Jebel Ali Racecourse redevelopment, and Jacobs completed systems integration for the Etihad Rail Stage 2 freight line. These projects reflect a growing preference for firms capable of managing schemes from concept to handover.

Regional consultancies like Dar Al-Handasah and KEO International Consultants maintain market share through Arabic-language expertise, municipal relationships, and cost-competitive fees. Developer-backed entities, such as Aldar Projects, are reshaping competition by self-performing project management on significant backlogs. Meanwhile, energy-service diversification and technology-driven entrants offering cloud-native solutions are intensifying competition. Incumbent firms are focusing on cybersecurity, data-residency compliance, and green-finance structuring to sustain their value propositions.

UAE Construction Consulting Industry Leaders

AECOM Middle East

AtkinsRéalis (Atkins UAE)

WSP Middle East

Dar Al Handasah Consultants

KEO International Consultants

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Dubai Municipality awarded five Tasreef Phase 2 packages totaling USD 680 million to widen the stormwater network across 430 million m² serving 3 million residents.

- January 2026: Dubai South Properties issued a USD 544 million construction contract for the 10 million ft² HAYAT community, breaking ground in Q2 and supporting 2,500 residential units plus wellness amenities.

- January 2026: WSP won the detailed master plan for ARM Holding’s 5 million m² Jebel Ali Racecourse redevelopment featuring 1.5 million m² of parkland.

- November 2025: Microsoft and G42 unveiled a plan to add 200 MW of Khazna data-center capacity as part of a USD 15.2 billion UAE investment.

UAE Construction Consulting Market Report Scope

| Project Management Consultancy (PMC) |

| Feasibility Studies |

| Detailed Project Reports (DPR) |

| Design and Engineering Services |

| Master Planning and Other Services |

| Residential | |

| Commercial | Office |

| Retail | |

| Industrial and Logistics | |

| Data Center | |

| Others - Institutional, Hospitality etc. | |

| Infrastructure/Civil | Transportation Infrastructure (Roadways, Railways, Airways, others) |

| Energy & Utilities | |

| Social Infrastructure | |

| Others |

| New Construction |

| Renovation |

| Public |

| Private |

| Abu Dhabi |

| Dubai |

| Sharjah |

| Rest of UAE |

| By Service Type | Project Management Consultancy (PMC) | |

| Feasibility Studies | ||

| Detailed Project Reports (DPR) | ||

| Design and Engineering Services | ||

| Master Planning and Other Services | ||

| By Sector | Residential | |

| Commercial | Office | |

| Retail | ||

| Industrial and Logistics | ||

| Data Center | ||

| Others - Institutional, Hospitality etc. | ||

| Infrastructure/Civil | Transportation Infrastructure (Roadways, Railways, Airways, others) | |

| Energy & Utilities | ||

| Social Infrastructure | ||

| Others | ||

| By Construction Type | New Construction | |

| Renovation | ||

| By Investment Source | Public | |

| Private | ||

| By Geography | Abu Dhabi | |

| Dubai | ||

| Sharjah | ||

| Rest of UAE | ||

Key Questions Answered in the Report

How large will consulting revenue linked to the UAE federal and Dubai megaprojects be by 2031?

The UAE construction consulting market size is on track to reach USD 24.91 billion by 2031, lifted by the USD 700 billion national infrastructure pipeline.

Which service line is expanding fastest?

Master planning and related strategic advisory are forecast to post an 8.05% CAGR over 2026–2031, the quickest among all service types.

What share of 2025 revenue came from residential work?

Residential assignments accounted for 40.5% of market revenue in 2025, making housing the single-largest sector that year.

Which emirate presents the highest growth outlook?

Abu Dhabi is projected to expand at a 7.75% CAGR through 2031, driven by major housing and industrial programs.

How will mandatory BIM rules affect consultant margins?

Dubai’s BIM regime is raising design-phase fees by roughly 15–25% because clients now require integrated digital twin delivery, driving higher margins for firms with advanced modeling capabilities.

What risks could slow market growth?

Rising expatriate wage demands, volatile import prices for key materials, and uneven permitting outside Dubai could collectively shave up to 2.1 percentage points off forecast CAGR unless mitigated through talent pipelines, cost-tracking tools, and regulatory harmonization.

Page last updated on: