Typhoid Fever Vaccines Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

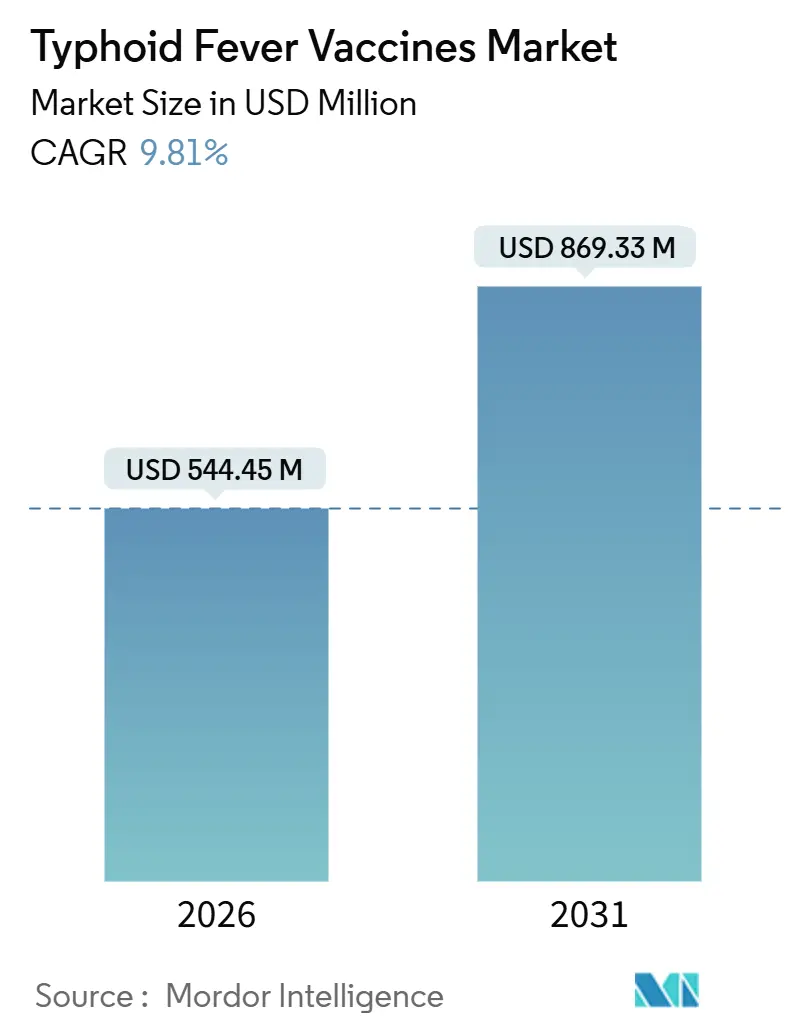

| Market Size (2026) | USD 544.45 Million |

| Market Size (2031) | USD 869.33 Million |

| Growth Rate (2026 - 2031) | 9.81% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

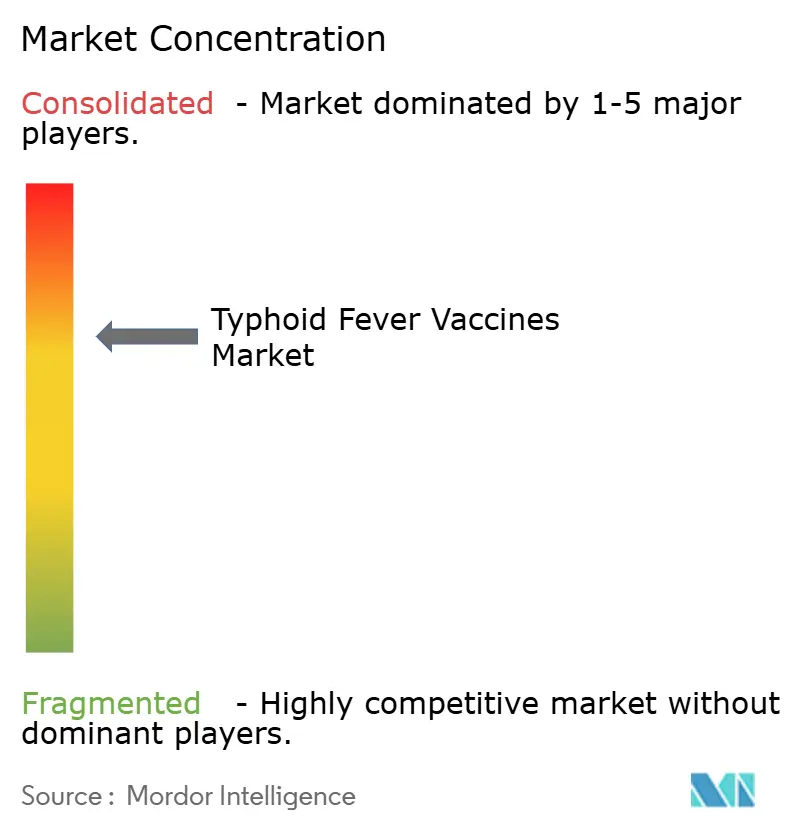

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Typhoid Fever Vaccines Market Analysis by Mordor Intelligence

The Typhoid Fever Vaccines Market size is estimated at USD 544.45 million in 2026, and is expected to reach USD 869.33 million by 2031, at a CAGR of 9.81% during the forecast period (2026-2031).

The current market size reflects donor-funded conjugate introductions, rising antimicrobial resistance, and wider national program adoption rather than a simple rise in dose volume. Gavi shipped more than 91 million typhoid conjugate vaccine (TCV) doses between 2021 and 2024, completing routine introductions and outbreak campaigns in six countries.[1]Christophe Fournier, “Gavi Progress Report 2024,” Gavi, gavi.org Conjugate formulations therefore capture incremental growth while Vi polysaccharide (Vi-PS) vaccines still finance existing procurement channels. Regional fill-finish build-outs in South Asia and Africa shorten lead times and shift price negotiations. The revival of travel medicine after COVID-19 further broadens private-sector demand and supports oral Ty21a volumes.

Key Report Takeaways

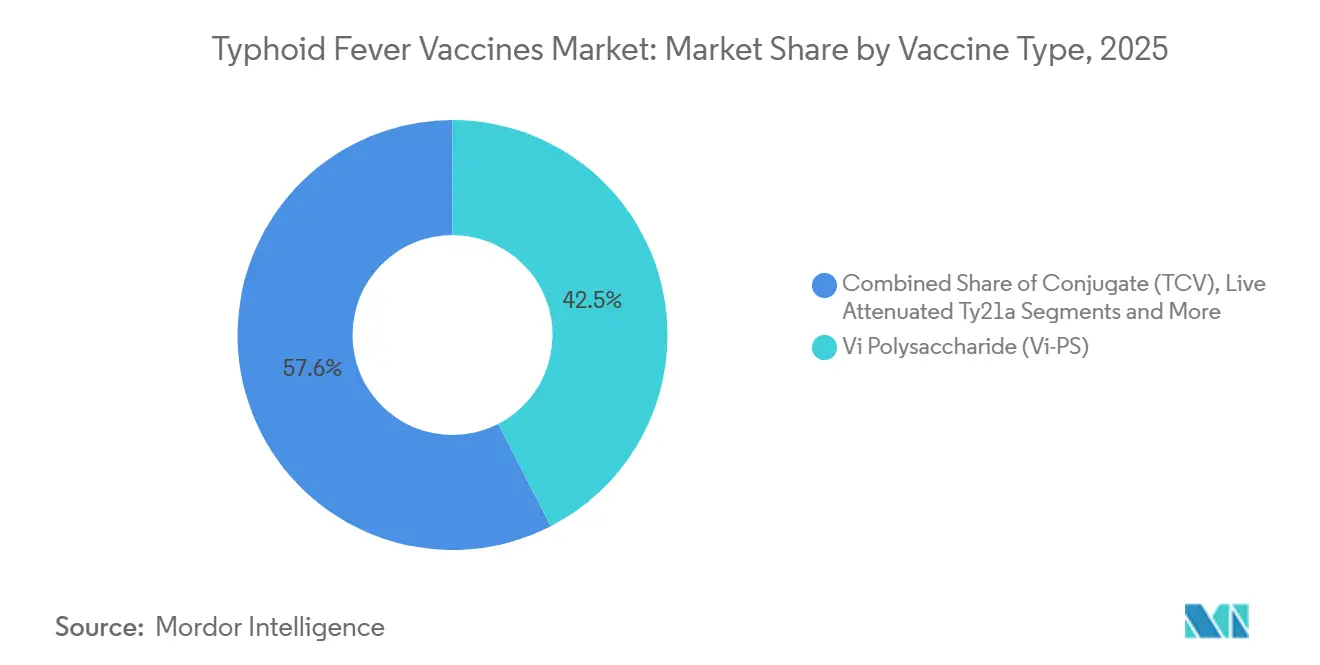

- By vaccine type, Vi-PS retained 42.45% of typhoid fever vaccines market share in 2025, while conjugates are expanding at 13.63% CAGR to 2031.

- By route, injectables held 63.62% of the typhoid fever vaccines market size in 2025; oral formulations are tracking an 11.06% CAGR through 2031.

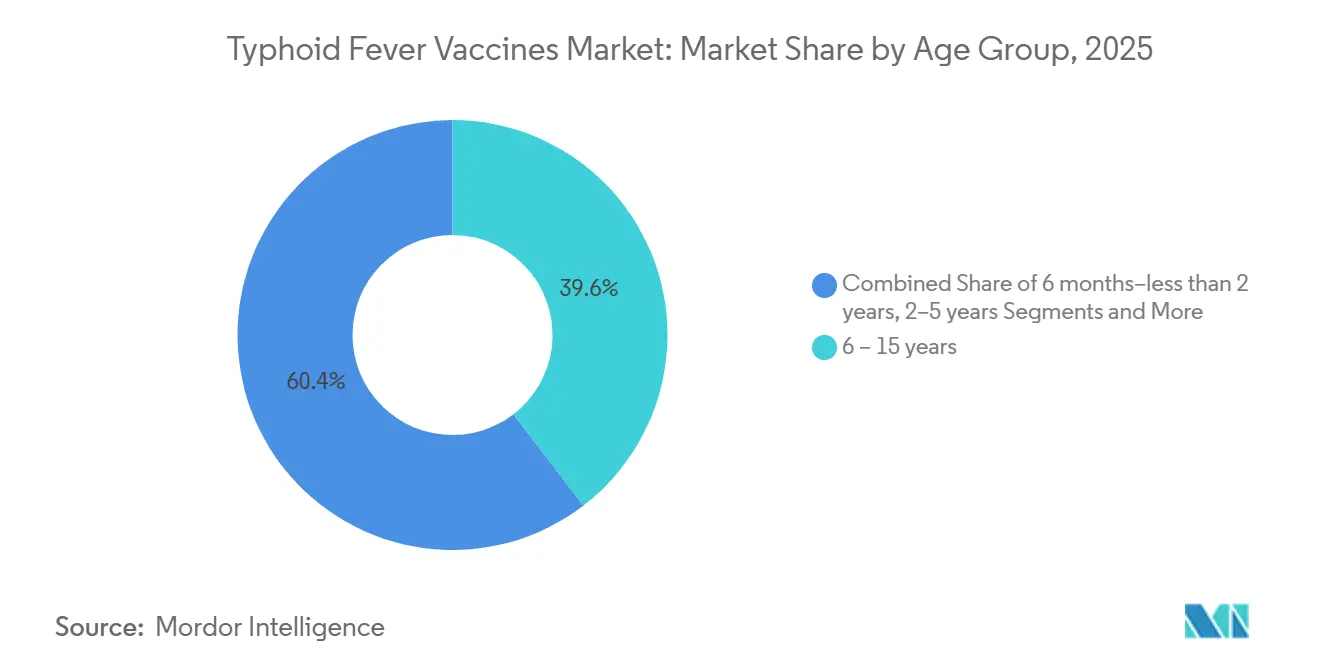

- By age group, infants 6 months to <2 years represent the fastest-growing cohort at 12.78% CAGR, while the 6–15-years segment led with 39.57% market share in 2025.

- By end user, public programs covered 51.44% of 2025 demand; travel and retail clinics are growing at 11.88% CAGR on recovering international mobility.

- By geography, Asia-Pacific generated 44.25% of 2025 revenue; the Middle East and Africa region is forecast to advance at an 11.44% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Typhoid Fever Vaccines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| WHO and Gavi-backed TCV routine roll-out | +2.8% | Asia-Pacific, Middle East, Africa | Medium term (2–4 years) |

| Escalating antimicrobial-resistant S. Typhi | +2.1% | South Asia, Middle East, Africa, spillover globally | Short term (≤2 years) |

| Endemic burden and catch-up campaigns | +1.6% | Asia-Pacific and Africa endemic zones | Medium term (2–4 years) |

| Regional fill-finish capacity expansion | +1.3% | India, Bangladesh, Senegal, Kenya, South Africa | Long term (≥4 years) |

| Rebound in international travel | +0.9% | North America, Europe serving travelers to endemic regions | Short term (≤2 years) |

| Typhoid vaccine in climate disaster response | +0.5% | South Asia, Africa disaster-prone areas | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

WHO And Gavi-Backed TCV Routine Roll-Out

Gavi support has transformed TCVs from optional travel interventions into scheduled infant doses. Seven countries introduced TCVs by late 2024, vaccinating over 64 million children and stabilizing multi-year procurement. WHO prequalification of four conjugates widened supplier diversity and pushed prices below USD 2 per dose.[2]Kate O’Brien, “2025 WHO Global Vaccine Market Report,” World Health Organization, who.int The alliance’s 2026–2030 plan rings-fences USD 1.2 billion for the African Vaccine Manufacturing Accelerator, signaling long-term demand security that de-risks factory investment.

Escalating Antimicrobial-Resistant S. Typhi Strains

Extensively drug-resistant typhoid, first documented in Sindh in 2016, is now entrenched across South Asia. Pakistan’s campaign vaccinated 8.2 million residents, and ceftriaxone resistance surfaced in Bangladesh in 2024. Carbapenem-resistant isolates appeared in India during 2025, narrowing therapy options. The CDC and Coalition Against Typhoid both note that vaccination delivers the most practical block against resistance-driven morbidity.

Endemic Burden And Catch-Up Campaigns In Asia And Africa

Typhoid still causes 7 million cases and more than 93,000 annual deaths, 90% in Asia-Africa children under 15 years. Catch-up drives in Pakistan, Liberia, Zimbabwe, Samoa, Nepal, Malawi, and Tuvalu compressed time to herd immunity. WHO guidance urges campaigns when surveillance undercounts true incidence, making mass action a faster path to control.

Regional Fill-Finish Capacity Expansion

The African Vaccine Manufacturing Accelerator underwrites projects such as the 300 million-dose MADIBA facility in Senegal, Biovac’s new Cape Town lab, and Kenya’s Biovax Institute. Biological E scaled TyphiBEV with a USD 36 million plant in India. Domestic capacity cuts freight delays and invites local bids in Gavi tenders.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sparse surveillance data delaying adoption | -1.4% | Endemic Asia-Pacific and Africa with weak lab networks | Medium term (2–4 years) |

| Post-COVID fiscal pressure on budgets | -1.1% | Gavi-eligible countries and traditional donors | Short term (≤2 years) |

| Vi-PS bulk supply bottlenecks | -0.7% | North America, Europe, global legacy markets | Short term (≤2 years) |

| Rural African cold-chain energy deficits | -0.9% | Sub-Saharan Africa rural districts | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Sparse Surveillance Data Delaying National Adoption

Passive systems miss most typhoid cases, hindering policy decisions. WHO’s 2025 surveillance standards admit many endemic nations rely on clinical diagnosis alone. Bayesian models applied in Tanzania showed hospital data captured only a fraction of community incidence. Health ministries therefore struggle to justify TCV financing without stronger evidence.

Post-COVID Fiscal Pressure On Donor And Government Budgets

Gavi seeks USD 9 billion for 2026–2030, yet high-income donors face strained fiscal space. Middle-income nations graduating from Gavi must now self-fund, often while repaying pandemic debt.[3]Amanda Glassman, “Financing the 2026-30 Gavi Strategy,” Center for Global Development, cgdev.orgShortfalls could slow introductions or shrink catch-up scope.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vaccine Type: Conjugates Displace Legacy Polysaccharides

Conjugate vaccines gained momentum once WHO recommended them for infants in 2017, and they are expanding at 13.63% CAGR through 2031, while Vi-PS still accounted for 42.45% of 2025 revenue. Typbar-TCV showed 79–85% efficacy and at least 4-year durability, which supports its role in the typhoid fever vaccines market size growth. Live attenuated Ty21a is rising at 11.06% on travel demand following Bavarian Nordic’s purchase. Pipeline bivalent and trivalent projects from Serum Institute, GSK, and the University of Maryland hint at broader antigen coverage that could shift future typhoid fever vaccines market share.

Conjugates address polysaccharide hyporesponsiveness and permit infant dosing, ensuring better memory responses. Vi-PS remains relevant for travelers needing a quick single injection. Oral Ty21a adds convenience for older children and adults. Investigational combination vaccines may streamline procurement if they secure WHO prequalification.

By Route of Administration: Injectables Dominate, Orals Gain Niche Traction

Injectables accounted for 63.62% of 2025 value because national programs use intramuscular delivery. Conjugates and Vi-PS formats both rely on the cold chain, yet offer a single-dose schedule that aligns with EPI visits. Oral Ty21a, though room-temperature stable, serves only those older than 6 years and follows a 4-capsule course. Still, needle-free appeal and traveler adoption keep the oral segment advancing above the overall typhoid fever vaccines market CAGR.

The injectable segment benefits from routine procurement volumes negotiated below USD 2 per dose, while oral formats command higher retail margins in private-sector channels. Strategic focus on thermostable conjugate presentations could eventually narrow the advantage that oral capsules hold in fragile cold-chain regions.

By Age Group: Infant Cohorts Accelerate As National Programs Mature

Infants aged 6 months to <2 years now represent the fastest-growing slice of the typhoid fever vaccines market, increasing at 12.78% CAGR as Gavi introductions embed a single TCV dose into routine schedules. School-aged children (6–15 years) retained 39.57% of 2025 revenue due to recent catch-up campaigns. Toddlers and adults grow nearer to the overall rate as legacy traveler and occupational indications level off.

Manufacturers must balance episodic bulk orders for campaigns with steady recurrent shipments for birth cohorts. Upcoming dose-finding studies aim to validate infant administration for newer combination candidates, securing long-term pipeline relevance.

By End User: Public Programs Lead, Travel Clinics Surge

Public and government programs generated 51.44% of 2025 demand, yet travel and retail clinics are tracking 11.88% CAGR into 2031 as international movement normalizes. Hospitals and private facilities in middle-income countries bridge the gap when Gavi eligibility ends. Dual pricing strategies are therefore required to satisfy both high-volume, low-margin public buyers and high-margin, lower-volume private channels.

TCVs at UNICEF tender prices below USD 2 contrast with U.S. travel-clinic fees that can exceed USD 50 per dose. Manufacturers that segment production lines accordingly will manage capacity constraints and prevent stock-out spillovers.

Geography Analysis

Asia-Pacific held 44.25% of 2025 revenue, buoyed by multiple CDSCO approvals in India and CNBG’s long-standing Vi-PS license in China. Pakistan’s campaign against XDR typhoid shows how resistance can trigger rapid uptake. Indian firms are now piloting bivalent and OMV-based candidates with Gates Foundation support, ensuring continued leadership.

The Middle East and Africa region is forecast to post an 11.44% CAGR through 2031 on the back of Gavi’s USD 1.2 billion manufacturing accelerator and Senegal’s 300 million-dose MADIBA site. WHO emergency frameworks further anchor demand by making typhoid vaccination part of humanitarian kits. Gulf travel hubs add episodic orders during Hajj and expatriate rotations.

North America and Europe show mature traveler markets where Vi-PS and Ty21a dominate. FDA and EMA label updates keep these products current, and the CDC Yellow Book now gives typhoid heightened visibility for South Asia itineraries. South America remains a niche region, although historical Ty21a field data from Chile support ongoing use among travelers.

Competitive Landscape

The market is moderately concentrated: four WHO-prequalified conjugate suppliers—Bharat Biotech, Biological E, SK Bioscience, and Zydus—anchor public-sector tenders, while Sanofi and GSK lead the polysaccharide space. Serum Institute’s Phase II/III bivalent trial and GSK’s dual candidates illustrate a pivot toward multi-antigen protection. The University of Maryland’s trivalent project confirms academic-industry partnerships as emerging disruptors.

Thermostability and combination profiles are the next competitive battlegrounds. Oral vector platforms, though still pre-commercial for typhoid, could erode injectable share if they clear regulatory hurdles. WHO prequalification remains the entry gate; companies lacking it must partner or finance the lengthy process themselves.

Typhoid Fever Vaccines Industry Leaders

-

PT Bio Farma

-

Sanofi

-

Bharat Biotech

-

Biological E

-

GlaxoSmithKline

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: A TCV campaign covered 33 Rohingya camps in Cox’s Bazar to protect children aged 9 months to 15 years

- March 2025: Bangladesh launched a nationwide TCV drive supported by the United Nations, targeting children 9 months to 15 years

- January 2025: Serum Institute of India received clearance to begin Phase II/III testing of its bivalent Typhi-Paratyphi A conjugate vaccine.

Global Typhoid Fever Vaccines Market Report Scope

Typhoid fever vaccines are immunizations that protect against Salmonella Typhi bacteria, which cause typhoid, a serious waterborne disease. They stimulate antibody production, with conjugate vaccines (TCVs) being the preferred option for all ages, including children under 2, offering long-term protection with a single dose.

The Typhoid Fever Vaccines Market Report is segmented by Vaccine Type, Route of Administration, Age Group, End User, and Geography. By Vaccine Type, the market is segmented into Conjugate, Vi Polysaccharide, Live Attenuated Ty21a, and Others. By Route of Administration, the market is segmented into Injectable and Oral. By Age Group, the market is segmented into 6 months–<2 years, 2–5 years, 6–15 years, and >15 years. By End User, the market is segmented into Public Health & Government Programs, Hospitals & Clinics, and Travel & Retail Clinics/Pharmacies. By Geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| Conjugate (TCV) |

| Vi Polysaccharide (Vi-PS) |

| Live Attenuated Ty21a |

| Others |

| Injectable |

| Oral |

| 6 months – less than 2 years |

| 2 – 5 years |

| 6 – 15 years |

| More than 15 years |

| Public Health and Government Programs |

| Hospitals & Clinics |

| Travel & Retail Clinics and Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Vaccine Type | Conjugate (TCV) | |

| Vi Polysaccharide (Vi-PS) | ||

| Live Attenuated Ty21a | ||

| Others | ||

| By Route of Administration | Injectable | |

| Oral | ||

| By Age Group | 6 months – less than 2 years | |

| 2 – 5 years | ||

| 6 – 15 years | ||

| More than 15 years | ||

| By End User | Public Health and Government Programs | |

| Hospitals & Clinics | ||

| Travel & Retail Clinics and Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the typhoid fever vaccines market by 2031?

The market is expected to reach USD 869.33 million by 2031, expanding at a 9.81% CAGR.

Which vaccine type is growing fastest within the typhoid fever vaccines market?

Conjugate vaccines, supported by WHO prequalification and Gavi funding, are rising at 13.63% CAGR.

Why are infants the focus of new typhoid immunization schedules?

WHO recommends a single TCV dose from 6 months, making infants the fastest-growing cohort at 12.78% CAGR.

How is travel medicine influencing demand?

Post-pandemic travel recovery drives an 11.88% CAGR in travel and retail clinics, boosting booster dose sales.

Which region shows the highest future growth?

The Middle East and Africa region is forecast to grow at 11.44% CAGR through 2031, backed by new manufacturing capacity.

Page last updated on: