Type 2 Diabetes Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

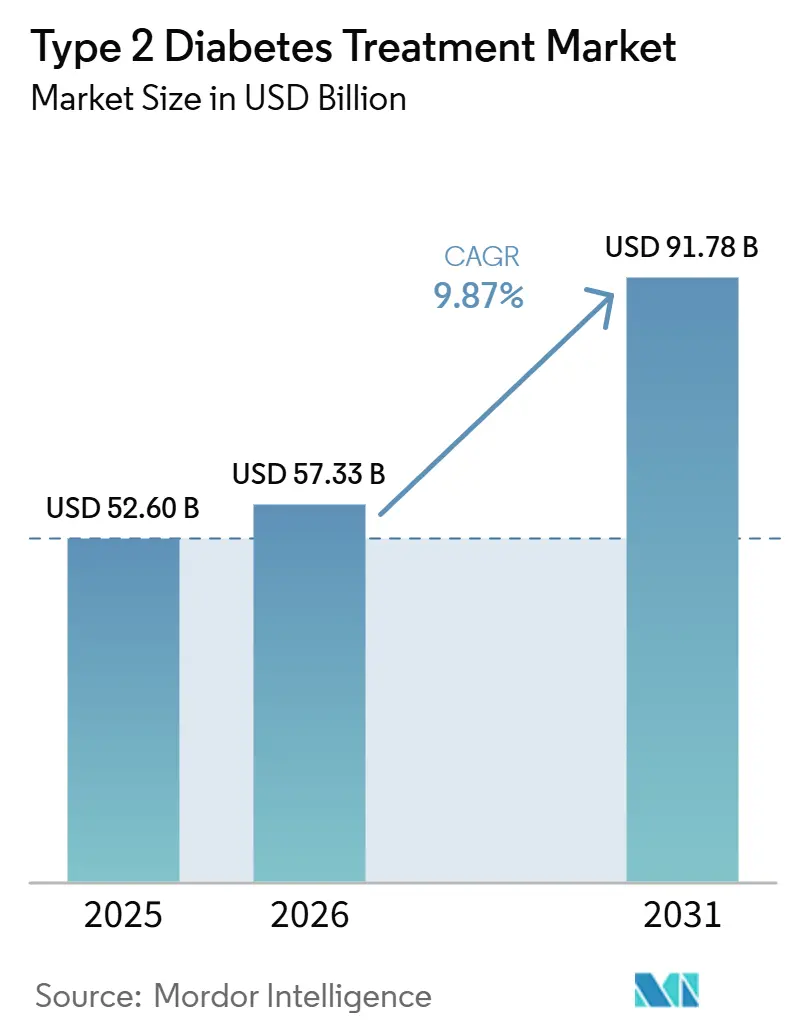

| Market Size (2026) | USD 57.33 Billion |

| Market Size (2031) | USD 91.78 Billion |

| Growth Rate (2026 - 2031) | 9.87% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Type 2 Diabetes Treatment Market Analysis by Mordor Intelligence

The Type 2 Diabetes Treatment Market size is expected to grow from USD 52.60 billion in 2025 to USD 57.33 billion in 2026 and is forecast to reach USD 91.78 billion by 2031 at 9.87% CAGR over 2026-2031.

The type 2 diabetes treatment market is expanding on the back of a rising global diabetes burden, with 589 million adults living with diabetes in 2024 and healthcare spending on the disease reaching USD 1.015 trillion that year. High BMI continues to deepen the patient pool, with 55% of preventable premature deaths from type 2 diabetes linked to obesity, which keeps treatment demand tied to a wider metabolic health problem rather than to glycemic control alone. The type 2 diabetes treatment market is also being lifted by therapy innovation, as oral GLP-1 launches, broader cardiorenal positioning, and expanding digital care tools improve treatment reach and persistence. Access remains uneven because reimbursement barriers still limit use of cardioprotective medicines in many plans, while injectable device supply and compliance demands keep some pressure on rollout speed. Even with those limits, the type 2 diabetes treatment market is supported by a durable prescription base, a growing role for premium therapies, and stronger links between drug therapy, monitoring, and care delivery.

Key Report Takeaways

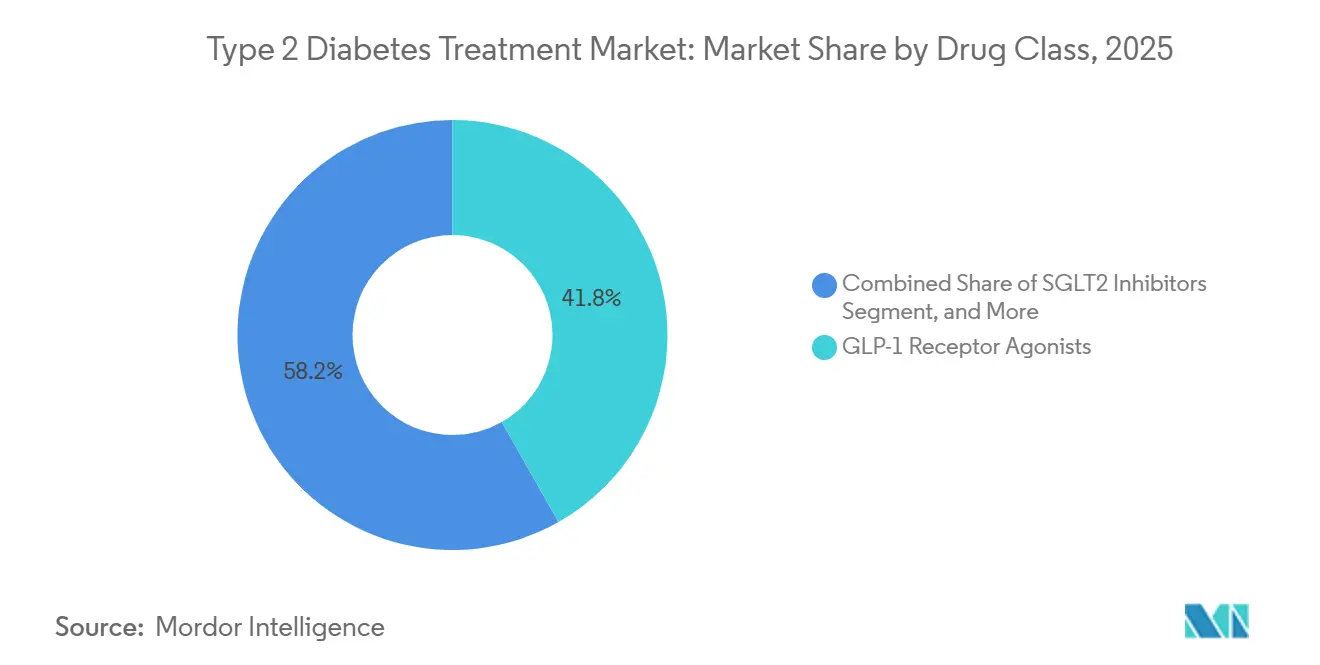

- By drug class, GLP-1 receptor agonists held 41.83% share in 2025, while SGLT2 inhibitors are projected to grow at 10.09% CAGR through 2031.

- By route of administration, oral formulations held 64.12% share in 2025, while injectable therapies are projected to grow at 11.17% CAGR through 2031.

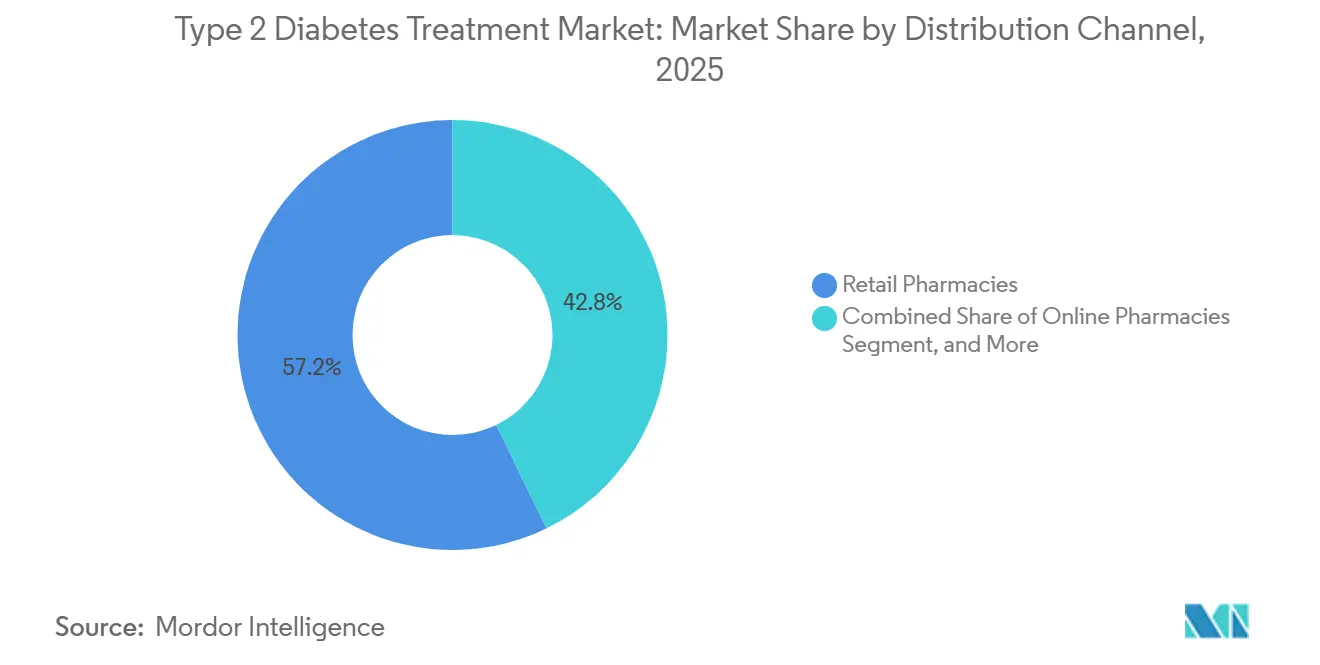

- By distribution channel, retail pharmacies held 57.16% share in 2025, while online pharmacies are projected to grow at 12.43% CAGR through 2031.

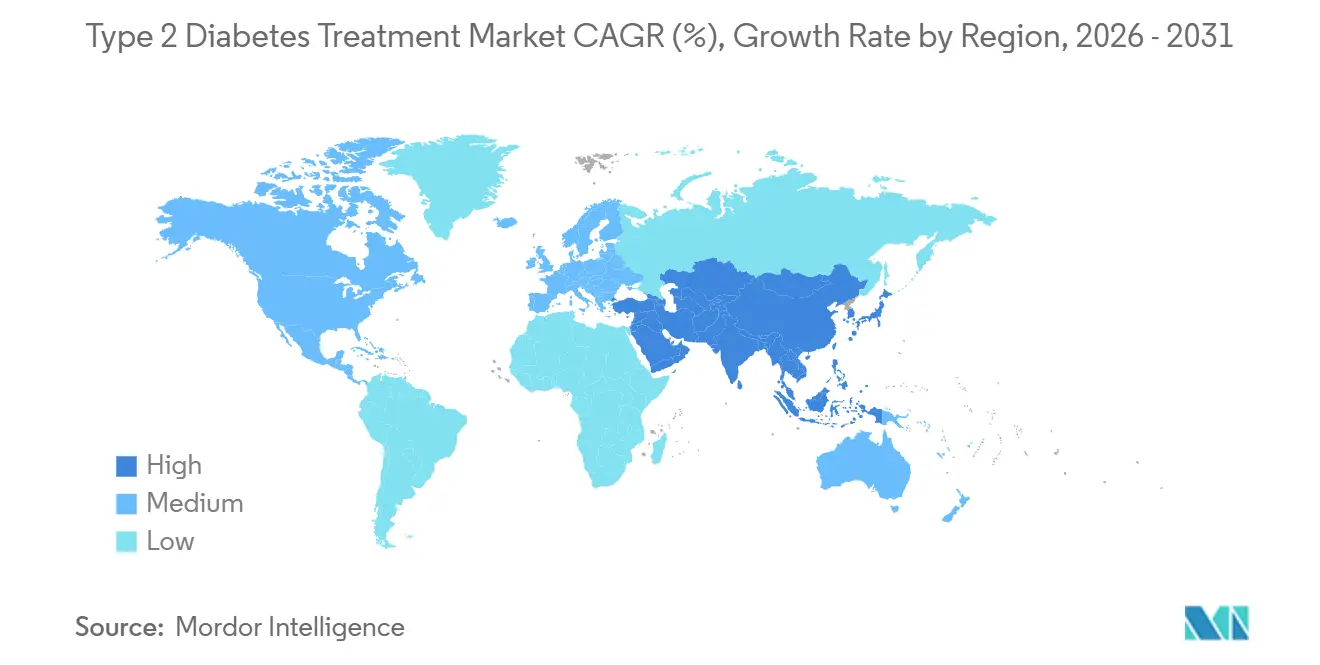

- By geography, North America held 39.91% share in 2025, while Asia-Pacific is projected to grow at 13.34% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Type 2 Diabetes Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Obesity-Linked Insulin Resistance | +2.5% | Global, with highest burden in South and Southeast Asia and North America | Long term (≥ 4 years) |

| Rapid Uptake of GLP-1 Receptor Agonists | +3.0% | North America, Europe, China, India | Medium term (2-4 years) |

| Expansion of Continuous Glucose Monitoring Reimbursement | +0.9% | North America primarily, with spillover to Europe and Australia New Zealand | Short term (≤ 2 years) |

| Pharma-Tech Partnerships for Connected Care | +0.6% | North America, Germany, Japan | Medium term (2-4 years) |

| Closed-Loop Insulin Delivery in Consumer Wearables | +0.5% | North America, Western Europe | Medium term (2-4 years) |

| Cardiometabolic Label Expansion for Existing Therapies | +1.2% | Global, concentrated in markets with strong cardiovascular risk populations | Short term (≤ 2 years) and Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Obesity-Linked Insulin Resistance

Obesity-linked insulin resistance is a core demand driver for the type 2 diabetes treatment market, because the condition is driving new diagnoses across both mature and emerging healthcare systems. A 2025 analysis in Frontiers in Public Health found that deaths from type 2 diabetes attributable to high BMI rose 203.9% between 1990 and 2021, while disability-adjusted life years increased at an annual rate of 8.9%.[1]Lijun Zhao et al., “Global, Regional, and National Burden of Type 2 Diabetes Mellitus Caused by High BMI from 1990 to 2021, and Forecasts to 2045,” Frontiers in Public Health, frontiersin.org The International Diabetes Federation also projects that the global diabetes population will reach 853 million by 2050, which points to a long runway for treatment demand in the type 2 diabetes treatment market. The burden is rising fastest in middle-income countries, where underdiagnosis, undertreatment, and rising medicine costs increasingly interact with one another. A younger adult cohort is also becoming more important, because earlier onset of the disease extends lifetime exposure to therapy and broadens the need for long-term cardiometabolic management.

Rapid Uptake of GLP-1 Receptor Agonists

Rapid adoption of GLP-1 receptor agonists is changing the revenue mix of the type 2 diabetes treatment market, because these drugs are now valued for weight, cardiovascular, and glycemic outcomes together. In October 2025, the FDA approved oral semaglutide for cardiovascular risk reduction in high-risk adults with type 2 diabetes, making it the first oral GLP-1 receptor agonist with proven cardiovascular benefit. In May 2026, Novo Nordisk made Ozempic tablets available in the United States, and in April 2026 the FDA approved Eli Lilly's Foundayo, the first non-peptide oral GLP-1 therapy. These launches are widening the addressable patient base in the type 2 diabetes treatment market by reducing the hesitation linked to self-injection. They are also raising the strategic value of oral delivery, because premium incretin therapy is now moving deeper into a segment once led mainly by mature generic products.

Cardiometabolic Label Expansion for Existing Therapies

Cardiometabolic label expansion is broadening the type 2 diabetes treatment market beyond classic diabetes management, because drug classes are now used across heart failure and kidney disease settings. The 2026 ADA and ESC positioning gave SGLT2 inhibitors a Class I, Level A recommendation for heart failure across the ejection fraction spectrum, based on outcome evidence built over several years. The same evidence base showed risk reductions of 13% to 27% across major cardiovascular phenotypes, which supports stronger use outside endocrinology-led pathways. The SURPASS-CVOT findings also reinforced the role of dual agonism in high-risk patient groups by showing an all-cause mortality advantage for tirzepatide over dulaglutide. As a result, the type 2 diabetes treatment market is drawing more activity from cardiologists and nephrologists, which expands prescribing channels and supports broader uptake across comorbid populations.

Expansion of Continuous Glucose Monitoring Reimbursement

Continuous glucose monitoring reimbursement is supporting the type 2 diabetes treatment market by making monitoring more routine for a wider group of patients. CMS revised its implantable CGM coverage policy in late 2025, while Blue Cross Blue Shield plans and Michigan Meridian Medicaid expanded access in 2026.[2]Blue Cross Blue Shield Michigan, “Continuous Blood Glucose Monitors, Medicare Plus Blue,” Blue Cross Blue Shield Michigan, bcbsm.com Wider reimbursement improves real-time visibility into patient glucose patterns and helps physicians adjust therapy sooner. That change supports better adherence and more consistent refill behavior across oral and injectable drug classes. It also strengthens the commercial logic of the type 2 diabetes treatment market, because device-enabled data can reinforce prescription persistence rather than acting as a separate revenue stream.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Novel GLP-1 and Smart Delivery Therapies | -1.6% | North America, Western Europe, high-income Asia-Pacific | Medium term (2-4 years) |

| Reimbursement Friction in Step-Therapy and Prior Authorization | -1.2% | North America, especially Medicaid and Medicare, and payer-controlled European markets | Short term (≤ 2 years) and Medium term (2-4 years) |

| Supply Constraints for Injectable Formats and Pen Components | -0.6% | Global, with stronger effects in Asia-Pacific and emerging markets | Short term (≤ 2 years) |

| Connectivity, Cybersecurity, and Data Privacy Burden on Connected Devices | -0.3% | North America and the European Union | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Novel GLP-1 and Smart Delivery Therapies

High prices for advanced GLP-1 products and smart insulin delivery systems continue to restrain the type 2 diabetes treatment market, even as clinical demand remains strong. The November 2025 U.S. pricing agreements lowered starter prices for some patients, but affordability gaps still remain for uninsured and underinsured groups. Closed-loop delivery systems add device spending on top of medicine costs, which limits adoption beyond higher-income patient groups in many countries. Payers also use step edits, therapy sequencing, and biosimilar pressure to contain spending, which can slow the use of premium treatments even when clinical need is clear. In practical terms, the type 2 diabetes treatment market is seeing strong innovation, but the premium end of the therapy stack still faces a meaningful affordability ceiling.

Reimbursement Friction in Step-Therapy and Prior Authorization

Reimbursement friction remains a material barrier for the type 2 diabetes treatment market, especially where coverage rules delay access to cardioprotective drug classes. An analysis reported from Annals of Internal Medicine found that only 47.3% of Medicaid managed care organizations covered both GLP-1 receptor agonists and SGLT2 inhibitors, while prior authorization was required in close to 60% of plans. These rules often require patients to move through older therapies first, even when newer medicines better match current cardiovascular or renal risk profiles. The delay matters most in underserved settings, where the patients with the greatest benefit potential are often the least likely to receive first-line access. That dynamic limits how quickly the type 2 diabetes treatment market can convert clinical guideline changes into realized prescription growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: GLP-1 Dominance Narrows SGLT2's Ascent

GLP-1 receptor agonists held 41.83% of the type 2 diabetes treatment market share in 2025, which kept them in the leading position across drug classes. Their lead was supported by long-running cardiovascular data and by newer label expansions that moved them closer to first-line use in high-risk patient groups. The 2025 and 2026 regulatory cycle also reduced the oral delivery gap, with oral semaglutide gaining a wider cardiovascular role and Foundayo entering the market as the first non-peptide oral GLP-1 therapy. In the type 2 diabetes industry, this shifts the class from a specialist premium option toward a broader mainstream therapy set. Biguanides, led by metformin generics, still keep a large clinical footprint because they remain cheap, familiar, and widely tolerated in first-line treatment pathways.

SGLT2 inhibitors are projected to grow at 10.09% CAGR from 2026 to 2031, which makes them the fastest-growing drug class in the type 2 diabetes treatment market. Their growth is tied to rising use in heart failure and kidney disease, not just blood sugar control, and a 2026 meta-analysis confirmed lower all-cause mortality and heart failure hospitalization across trial data. China also added momentum in January 2026, when Olorigliflozin Capsules received NMPA approval, pointing to stronger domestic competition in the class. DPP-4 inhibitors still retain relevance in cost-sensitive settings such as Japan and India, although they face slower long-term positioning than SGLT2 and GLP-1 therapies. Sulfonylureas and thiazolidinediones continue to lose relative appeal, while insulin remains necessary in advanced cases but faces volume pressure in higher-income markets where newer options are moving earlier in the care pathway.

By Route of Administration: Injectable Momentum Driven by New Delivery Systems

Oral formulations captured 64.12% of the type 2 diabetes treatment market in 2025, which reflected the huge installed base of metformin and other established oral therapies. The oral segment is now changing in mix as well as in scale, because it includes more premium incretin products rather than only lower-cost legacy medicines. That shift should lift the average selling value of oral therapy in the type 2 diabetes treatment market through the forecast period. Oral delivery also remains more accessible for broad patient populations, which supports large prescription volumes even as newer injectables gain attention. Intravenous administration continues to serve a small institutional niche tied mainly to acute glycemic crises and perioperative care.

Injectable therapies are projected to expand at 11.17% CAGR, and that pace reflects more than ongoing GLP-1 pen adoption. The type 2 diabetes treatment market size for injectable care is now being supported by automated insulin delivery systems designed specifically for adults with insulin-requiring type 2 diabetes. FDA-cleared systems such as MiniMed Flex are moving the segment toward app-controlled and lower-friction use models, which can widen uptake outside specialist settings. Device-linked treatment is also raising the regulatory and quality threshold, because cybersecurity and privacy requirements are becoming more important for connected products. In the type 2 diabetes industry, this favors companies that can combine drug, device, data, and compliance capabilities rather than relying on product strength alone.

By Distribution Channel: Online Pharmacies Reshape Access Economics

Retail pharmacies held 57.16% share in 2025, which kept them as the leading distribution channel in the type 2 diabetes treatment market. Their strength came from broad neighborhood access, familiarity among chronic care patients, and the ability to dispense both branded and generic antidiabetic products at scale. Hospital pharmacies continued to serve a smaller but important role in inpatient insulin use and initiation of more complex injectable regimens. The retail channel also benefits from stable refill patterns in long-term diabetes care, which protects volume even when new digital channels gain traction. At the same time, channel competition is increasing because patient convenience and prescription visibility now matter more in therapy management.

Online pharmacies are projected to grow at 12.43% CAGR from 2026 to 2031, making them the fastest-growing channel in the type 2 diabetes treatment market. Amazon Pharmacy is already expanding same-day delivery and kiosk pickup for oral semaglutide in the United States, which gives the channel stronger relevance for newer diabetes therapies. This is not only a logistics shift, because online channels can automate refills and improve continuity across drug and monitoring programs. That makes the channel strategically valuable in the type 2 diabetes treatment market, where adherence has a direct effect on long-term prescription value. Over time, online pharmacies are likely to become more embedded in connected care pathways rather than acting only as lower-friction dispensing outlets.

Geography Analysis

North America accounted for 39.91% of type 2 diabetes treatment market share in 2025, which made it the largest regional contributor. The region benefits from high treatment intensity, broad familiarity with premium therapies, and faster uptake of GLP-1 receptor agonists and SGLT2 inhibitors than most other markets. Reimbursement for continuous glucose monitoring is also widening, with public and private coverage changes improving access and data visibility across care pathways. Faster review pathways also support the region, as the FDA approved Foundayo under the National Priority Voucher program in 50 days during April 2026. Canada and Mexico add meaningful demand, although tighter formulary controls in both countries can slow premium therapy penetration relative to the United States.

Europe holds a substantial position in the type 2 diabetes treatment market because major countries maintain structured reimbursement systems and established chronic care pathways. Germany, the United Kingdom, France, Italy, and Spain continue to anchor demand for cardioprotective therapies and premium branded products. In September 2025, oral semaglutide gained an expanded cardiovascular label in Europe, which strengthened the role of oral GLP-1 treatment across the region. Europe is also relevant for connected care models, as companies continue to use digital support programs to strengthen treatment engagement and persistence. Lower-income parts of the region benefit from wider access to insulin and related therapies as biosimilar availability improves.

Asia-Pacific is projected to grow at 13.34% CAGR through 2031, which makes it the fastest-growing regional block in the type 2 diabetes treatment market. The region combines large patient pools with accelerating regulatory activity, especially in China and India . China approved differentiated therapies such as ecnoglutide in January 2026 and Olorigliflozin in the same month, which shows a stronger domestic innovation cycle across both GLP-1 and SGLT2 pathways. India remains important because of its scale, rising metabolic burden, and increasing adoption of newer therapies in urban care settings. Japan, South Korea, and Australia support premium-price volumes, while the Middle East and Africa and South America remain smaller contributors but continue to gain from improving access and rising chronic disease treatment needs.

Competitive Landscape

The type 2 diabetes treatment market remains concentrated around a small group of multinational leaders, with Novo Nordisk and Eli Lilly holding especially strong positions in high-value incretin therapies. AstraZeneca, Boehringer Ingelheim, Johnson and Johnson, Merck and Co., and Sanofi also remain important because they cover major positions in SGLT2 inhibitors, DPP-4 inhibitors, and insulin-based treatment pathways. Competitive pressure is increasing, but it is no longer limited to rivalry among long-established originators. In China, domestic developers are moving faster into advanced therapy classes, as shown by the 2026 approvals for ecnoglutide and Olorigliflozin. This means the type 2 diabetes treatment market is becoming more crowded in innovation, even though revenue concentration remains strongest at the top end of branded therapy.

Strategic portfolio moves are becoming more important than line extensions in the type 2 diabetes treatment market. Novo Nordisk confirmed the closure of the Akero Therapeutics acquisition in its 2025 reporting and related SEC filing, which gave it a stronger presence in MASH, a condition with clear overlap with metabolic disease and type 2 diabetes. Eli Lilly strengthened the oral GLP-1 category through the FDA approval of Foundayo, which gives it a differentiated position in a rapidly expanding treatment format. Medtronic and MiniMed are also widening their role through automated insulin delivery systems for insulin-requiring adults with type 2 diabetes. These moves show that product leadership in the type 2 diabetes treatment market increasingly depends on therapy breadth and platform reach, not only on a single molecule.

Drug and device convergence is shaping the next layer of competition in the type 2 diabetes treatment market. Companies such as Medtronic, Dexcom, Tandem Diabetes Care, Insulet, and Ypsomed are pushing deeper into type 2 care by linking insulin delivery and monitoring more closely. Senseonics and Welldoc advanced that model in June 2026 through a partnership around an AI-powered app for the Eversense 365 implantable CGM. MiniMed and Abbott also expanded work on dual glucose-ketone sensors for smart dosing systems, which points to broader platform integration around prevention and safety. As payer models place more weight on adherence and outcomes, integrated care ecosystems are likely to compete more effectively than stand-alone product offerings.

Type 2 Diabetes Treatment Industry Leaders

Boehringer Ingelheim International GmbH

AstraZeneca plc

Eli Lilly and Company

Novartis AG

Novo Nordisk A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: MiniMed and Abbott expanded their partnership to commercialise dual glucose-ketone sensors designed for exclusive integration with MiniMed's smart dosing systems, enabling real-time detection of rising ketones to prevent diabetic ketoacidosis, building on their existing Instinct sensor collaboration.

- June 2026: MiniMed Flex commercially launched in the US as the first screenless, app-controlled insulin pump, it is FDA-cleared for adults with insulin-requiring type 2 diabetes and targets lifestyle-friendly management with the SmartGuard algorithm.

- June 2026: Senseonics and Welldoc entered a strategic partnership to develop a next-generation AI-powered app for the Eversense 365 implantable CGM, the app is planned to include CGM-informed bolus calculation and metabolic tracking for US launch in H2 2026.

- May 2026: Amazon Pharmacy expanded access to oral Ozempic via same-day delivery and in-office kiosk pickup, creating a new digital distribution path for the only FDA-approved oral peptide GLP-1 medication for type 2 diabetes.

Global Type 2 Diabetes Treatment Market Report Scope

The Type 2 Diabetes Treatment Market encompasses the global development, production, distribution, and commercialization of pharmaceutical therapies used to manage type 2 diabetes mellitus (T2DM), a chronic metabolic disorder characterized by insulin resistance and impaired insulin secretion, resulting in elevated blood glucose levels. The market includes a broad range of therapeutic drug classes, such as biguanides, sulfonylureas, thiazolidinediones, DPP-4 inhibitors, GLP-1 receptor agonists, SGLT2 inhibitors, insulin, and other antidiabetic medications, available in oral, injectable, and intravenous formulations.

The Type 2 Diabetes Treatment Market is segmented by drug class, route of administration, distribution channel, and geography. Based on drug class, the market is categorized into biguanides, sulfonylureas, thiazolidinediones, DPP-4 inhibitors, GLP-1 receptor agonists, SGLT2 inhibitors, insulin, and other drug classes. By route of administration, the market is segmented into oral, injectable, and intravenous treatments. Based on distribution channel, the market comprises hospital pharmacies, retail pharmacies, and online pharmacies. Geographically, the market is analyzed across North America (the United States, Canada, and Mexico), Europe (Germany, the United Kingdom, France, Italy, Spain, and the Rest of Europe), Asia-Pacific (China, Japan, India, Australia, South Korea, and the Rest of Asia-Pacific), the Middle East & Africa (GCC, South Africa, and the Rest of the Middle East & Africa), and South America (Brazil, Argentina, and the Rest of South America).

| Biguanides |

| Sulfonylureas |

| Thiazolidinediones |

| DPP-4 Inhibitors |

| GLP-1 Receptor Agonists |

| SGLT2 Inhibitors |

| Insulin |

| Others by Drug Class |

| Oral |

| Injectable |

| Intravenous |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Biguanides | |

| Sulfonylureas | ||

| Thiazolidinediones | ||

| DPP-4 Inhibitors | ||

| GLP-1 Receptor Agonists | ||

| SGLT2 Inhibitors | ||

| Insulin | ||

| Others by Drug Class | ||

| By Route of Administration | Oral | |

| Injectable | ||

| Intravenous | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving growth in type 2 diabetes treatment through 2031?

Growth is being supported by a rising patient base, obesity-linked insulin resistance, wider use of GLP-1 and SGLT2 therapies, and better reimbursement for continuous glucose monitoring. The market is expected to reach USD 91.78 billion by 2031 at a 9.87% CAGR.

Which drug class leads revenue and which grows the fastest?

GLP-1 receptor agonists led with 41.83% share in 2025, while SGLT2 inhibitors are projected to expand at 10.09% CAGR through 2031.

Why are oral therapies still important despite strong injectable innovation?

Oral therapies held 64.12% share in 2025 because they include large metformin volumes and broad patient acceptance. New oral GLP-1 launches are also improving the value mix of this category.

Which sales channel is changing access the most?

Online pharmacies are changing access the most, with a projected 12.43% CAGR through 2031. Same-day delivery, refill automation, and digital integration are making them more relevant for chronic therapy management.

Which region offers the strongest expansion outlook?

Asia-Pacific is expected to post the fastest regional growth at 13.34% CAGR through 2031. Large patient populations, faster approvals, and stronger local innovation are supporting that pace.

Page last updated on: