Turning Machine and Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

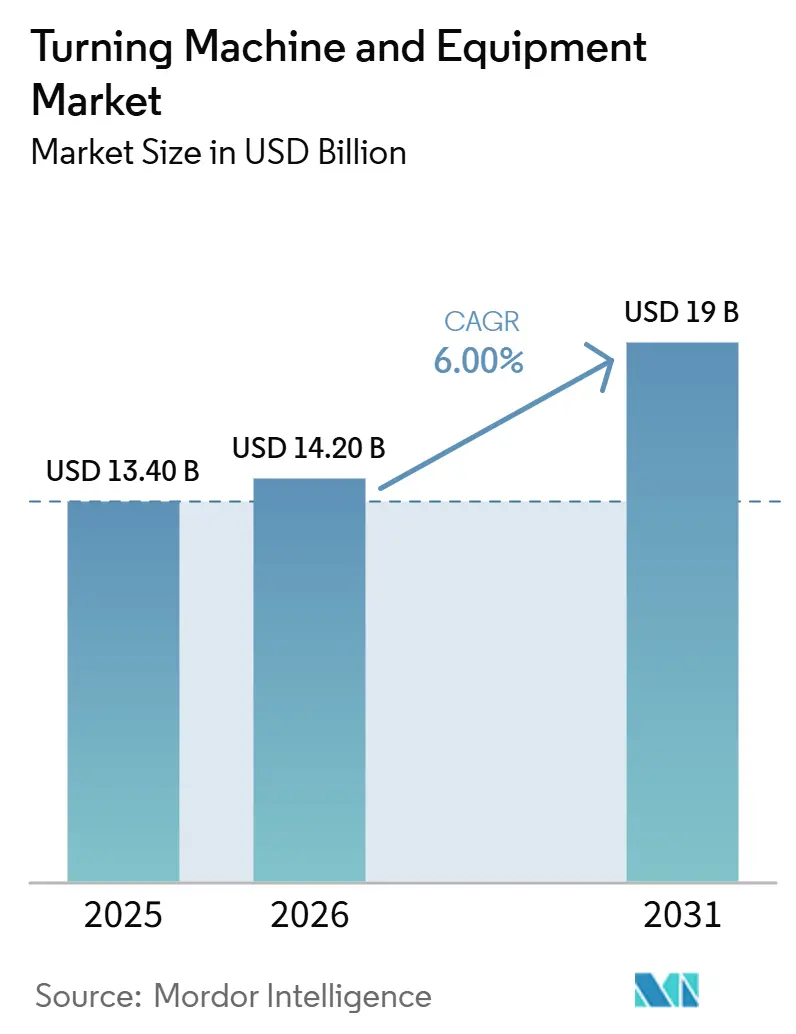

| Market Size (2026) | USD 14.20 Billion |

| Market Size (2031) | USD 19 Billion |

| Growth Rate (2026 - 2031) | 6.00% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Turning Machine and Equipment Market Analysis by Mordor Intelligence

The Turning Machine And Equipment Market size is projected to be USD 13.40 billion in 2025, USD 14.20 billion in 2026, and reach USD 19 billion by 2031, growing at a CAGR of 6% from 2026 to 2031.

Demand in the turning machine and equipment market is rising because automotive, aerospace, and medical device manufacturers continue to require tighter tolerances, repeatable output, and dependable process control. Capacity additions across Asia-Pacific, South Asia, and the Middle East are expanding the installed base of turning machines and equipment and bringing machining capacity closer to emerging manufacturing clusters. Wider adoption of multi-tasking machines is shortening cycle times, reducing handling steps, and improving capital utilization, supporting demand for higher-value CNC platforms. CNC automation is also making complex work easier to standardize, helping the turning machine and equipment market reach users who need traceability, fewer setup errors, and stronger process consistency. Competition remains moderate at the top, while the strongest growth opportunities in the turning machine and equipment market are concentrated in automation-rich systems, EV component manufacturing, and emerging industrial regions.

Key Report Takeaways

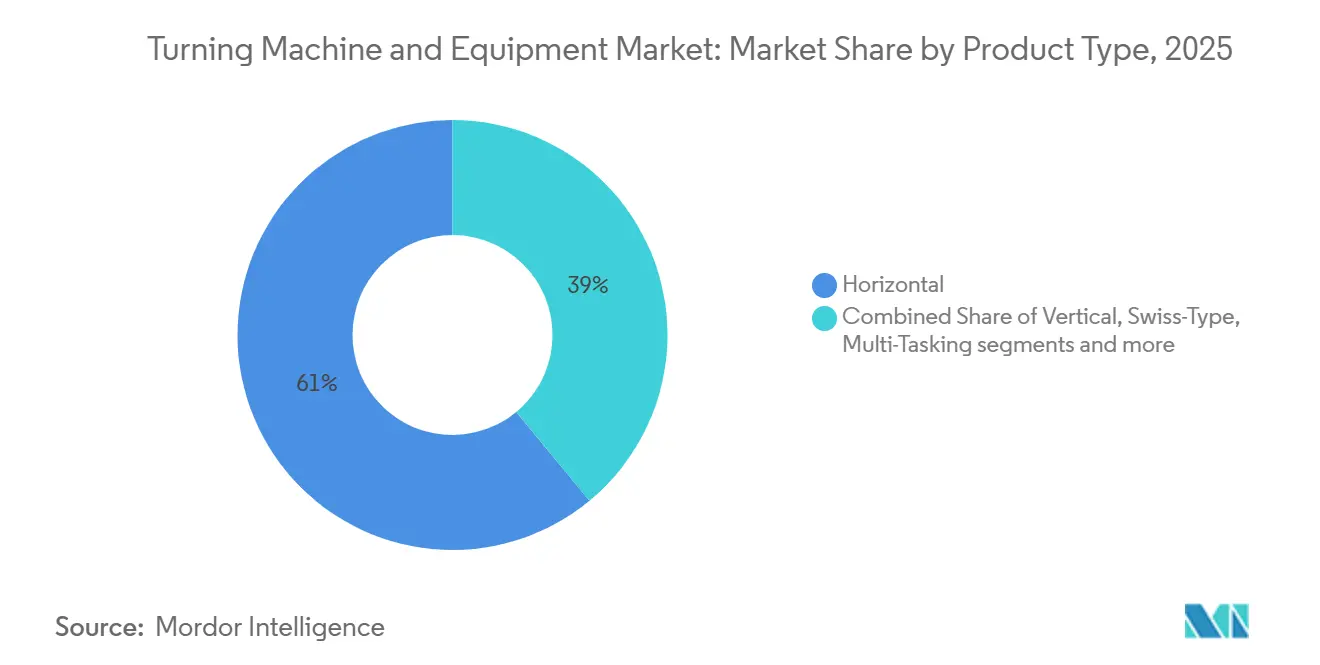

- By product type, the horizontal segment led with a 61% of the turning machine and equipment market size in 2025, while the multi-tasking segment is forecast to expand at a 7.8% CAGR through 2031.

- By automation type, fully automatic CNC held 72% of the turning machine and equipment market share in 2025, and this segment also recorded the highest projected CAGR at 7.2% through 2031.

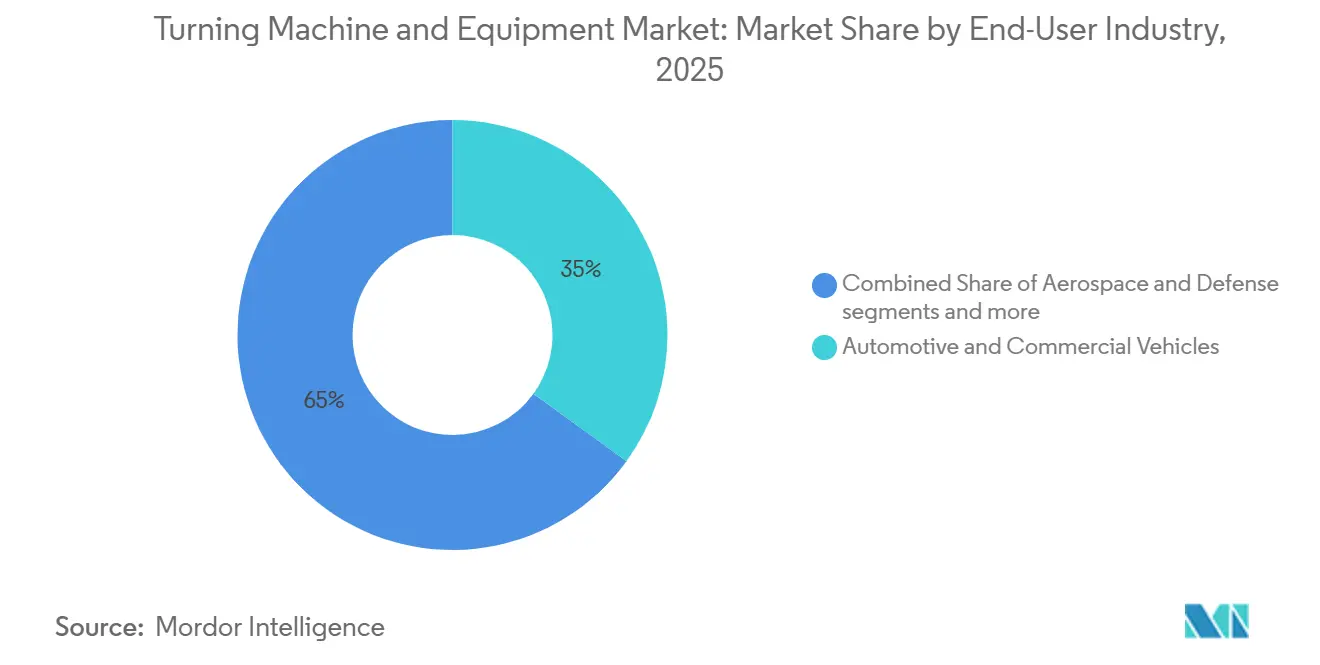

- By end-user industry, automotive and commercial vehicles accounted for a 35% share in 2025, while aerospace and defense are advancing at a 7.5% CAGR through 2031.

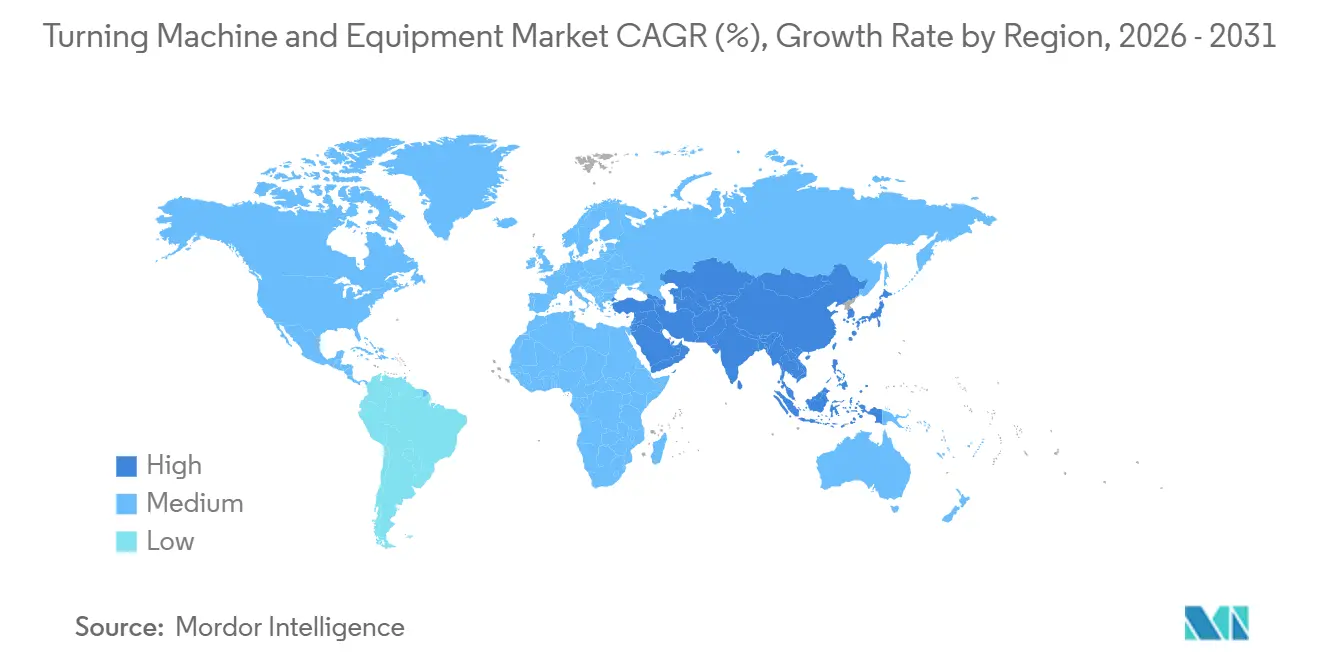

- By geography, Asia-Pacific held 48.91% share in 2025 and is projected to grow at an 8.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Turning Machine and Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Precision-Machined Components in Automotive and Aerospace | +1.5% | Global, with concentration in North America, Europe, and Japan | Short term (≤ 2 years) |

| Surge in EV and E-mobility Manufacturing Driving Demand for Shafts, Rotors, and Housings | +1.3% | Global, with concentration in China, Europe, and North America | Medium term (2-4 years) |

| Proliferation of Multi-Tasking and Turn-Mill Centers is Reducing Cycle Times | +1.1% | Global, with early adoption in North America and the Asia-Pacific core | Short term (≤ 2 years) |

| Expansion of Manufacturing Capacity in Emerging Economies | +0.9% | Asia-Pacific, South Asia, the Middle East, and Africa, with spillover to South America | Long term (≥ 4 years) |

| Growing Need for High-Mix, Low-Volume Production | +0.7% | North America and Europe | Short term (≤ 2 years) |

| Medical Device Miniaturization is riving the Adoption of Swiss-Type CNC Lathes | +0.5% | North America, Europe, and Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Precision-Machined Components in Automotive and Aerospace

Commercial aerospace continues to sustain demand for precision-machined components in the turning machine and equipment market, as fleet renewal and the addition of long-range aircraft require a steady flow of such parts. The FAA forecasts that the United States commercial aircraft fleet will grow from 7,387 aircraft in 2024 to 10,607 by 2045, supporting a long production runway for aerospace components that depend on advanced turning processes. Global general aviation billings rose 14.3% to USD 26.7 billion in 2024, while the United States manufactured general aviation aircraft deliveries reached 2,169 units, 22.5% above 2019 levels.[1]Federal Aviation Administration, “FAA Aerospace Forecasts Fiscal Years 2025-2045,” FAA, faa.gov Aerospace and defense buyers are also concentrating work with a smaller group of certified precision suppliers, which supports longer contracts and steadier machine utilization across the turning machine and equipment market. Alongside aerospace expansion, automotive manufacturers increased investment in manufacturing technology by 22.2% in 2025, adding a second strong source of demand for crankshafts, transmission housings, suspension parts, and EV-related components that rely on turning operations.[2]Association for Manufacturing Technology, “Manufacturing Technology Orders Set Record in December 2025,” AMT, amtonline.org

Surge in EV and E-mobility Manufacturing Driving Demand for Shafts, Rotors, and Housings

The EV production ramp is changing the demand profile of the turning machine and equipment market, as electric drivetrains require parts with different geometries, tighter tolerances, and more complex machining paths than many internal combustion components. The IEA reported that nearly 22 million electric cars were produced globally in 2025, up by more than 25% from the prior year.[3]Association for Manufacturing Technology, “Manufacturing Technology Orders Set Record in December 2025,” AMT, amtonline.org The IEA projects global EV sales are on track to reach 23 million in 2026, or close to 30% of all cars sold worldwide, which keeps upstream demand for rotor shafts, motor housings, and axle components firm. Machine builders are already positioning products to address this need, and INDEX-Werke explicitly markets its G and MS Series machines for the single-cycle production of electric vehicle drive components. Chinese vehicle manufacturers have announced overseas production capacity expansions exceeding 4.3 million vehicles annually by 2026, extending EV-linked demand in the turning machine and equipment market well beyond China into Southeast Asia, Europe, and Latin America.

Proliferation of Multi-Tasking and Turn-Mill Centers Is Reducing Cycle Times

Multi-tasking turning centers are changing the operating economics of the turning machine and equipment market by combining turning, milling, and, at times, grinding within a single machine cycle. AMT data shows that higher-value machinery purchases pushed the United States machinery order value growth ahead of unit growth through 2025, suggesting a clear shift toward more advanced, capital-intensive platforms. A study published in PMC found that reactive power compensation in CNC lathes reduced power consumption by 23% to 30% for screw-drive systems and by 36% to 47% for linear-drive systems, strengthening the cost case for replacing older equipment with newer multi-axis systems. Okuma’s April 2026 launch of the MULTUS U1000 and U2000, both with 5-axis simultaneous machining, an 80-tool standard magazine, and an 8.2 m² footprint, shows how machine builders are packaging full machining capability into smaller production footprints. This combination of floor-space savings, higher spindle utilization, and reduced setup time is driving the turning machine and equipment market toward platforms that deliver more finished work from each installation.

Expansion of Manufacturing Capacity in Emerging Economies

Manufacturing expansion in emerging economies is expanding the addressable base of the turning machine and equipment market, as more localized production requires new precision-machining capacity. The United States International Trade Administration reported that India’s manufacturing sector attracted USD 165.1 billion in investment in 2024, supported by a USD 24 billion commitment under the Production-Linked Incentive scheme across 14 priority sectors. The United States International Trade Administration indicates that manufacturing’s share of India’s gross value added is expected to rise from 14% in 2025 to 21% by 2032, suggesting a sustained need for industrial capital equipment as domestic production scales up. India also ranked seventh globally in annual industrial robotics installations as of 2024, indicating a broader industrial upgrading cycle that includes the adoption of CNC turning. Vietnam, Thailand, Indonesia, and Malaysia are also adding precision metalworking capacity as supply chains diversify, which supports a longer runway for the turning machine and equipment market across Southeast Asia.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Investment and Long Payback Periods Limiting SME Adoption | -0.9% | Global, with the highest drag in SME-concentrated Asia-Pacific and South America | Short term (≤ 2 years) |

| Skilled Operator Shortage Across Key Manufacturing Geographies | -0.7% | North America, Europe, and Japan | Long term (≥ 4 years) |

| Extended Machine Life Cycles and Availability of Refurbished Equipment Limiting Replacement Demand | -0.5% | Global | Medium term (2-4 years) |

| Cyclical Nature of Industrial Capital Expenditure Affecting Machine Tool Purchases | -0.4% | Global, with the sharpest cyclicality in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Investment and Long Payback Periods Limiting SME Adoption

The high upfront cost remains a clear brake on the turning machine and equipment market, as advanced CNC, multi-tasking, and swiss-type systems often sit beyond the reach of smaller manufacturers without financing or subsidies. VDW reported that domestic machine tool orders in Germany fell 16% in 2025, with the greatest caution among small- and mid-sized industrial buyers, especially in the automotive supplier base. VDW statistics also showed that the German machinery sector maintained its investment ratio at 5.2% of revenue for the sixth straight year. In contrast, per-employee investment stood at EUR 8,881 (USD 10,446.8), 50% below pre-2019 levels. Capacity utilization in German machine tools was 75.6% in 2025, down 6.1 percentage points from the prior year, making the payback case for new equipment difficult even among technically capable buyers. However, the turning machine and equipment market still faces a wide affordability gap for smaller operators who are cautious about investment timing and returns.

Skilled Operator Shortage Across Key Manufacturing Geographies

Labor availability remains a structural constraint on the turning machine and equipment market because advanced machines still require trained operators, programmers, and setup personnel. The United States Bureau of Labor Statistics projects that employment of lathe and turning machine tool setters, operators, and tenders will decline from 18,900 in 2024 to 16,400 by 2034. Yet annual openings remain meaningful because retirements and workforce exits continue. The Manufacturing Skills Institute reported that 449,000 manufacturing jobs in the United States were unfilled as of March 2025, including many CNC machinist and machine operator roles. This creates a practical tension in the turning machine and equipment market because automation reduces manual work while raising the skill level required for programming, setup, and process oversight. Buyers often delay new purchases when they cannot secure qualified labor to run more capable platforms, which slows order conversion even when financing and demand conditions are supportive.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Horizontal Dominance Meets Multi-Tasking Disruption

The horizontal segment held 61% of the turning machine and equipment market share in 2025, reflecting its broad fit across automotive drivetrain parts, aerospace structures, and general industrial turned components. The installed base remains sticky because horizontal systems benefit from broad tooling compatibility, familiar operating practices, and mature programming support across the turning machine and equipment industry. Their role in high-volume production also keeps them central, where repeatability and throughput matter more than highly specialized machine architecture. Vertical turning machines remain important in heavy-duty applications such as wind turbine hubs, large flanges, and heavy vehicle axles, where large-diameter workpieces and efficient use of floor space matter.

The multi-tasking segment is projected to grow at a 7.8% CAGR from 2026 to 2031, making it the fastest-growing product group in the turning machine and equipment market. Manufacturers are choosing these systems because they reduce work-in-process inventory, lower inter-machine handling, and cut setup changes in high-mix production. The swiss-type segment is also expanding as medical device miniaturization and semiconductor equipment demand push more bar-fed precision work into tighter tolerance ranges. NIST case studies show that United States job shops are investing in 5-axis and multi-axis capabilities to serve aerospace and medical customers seeking consolidated processes and certified production environments. This creates a balanced market landscape between stable demand for general-purpose turning systems and faster growth in highly automated platforms that can complete more machining operations with fewer setups.

By Automation Type: CNC Automation Commands, But Integration Deepens the Divide

Fully automatic CNC held 72% of the turning machine and equipment market share in 2025, confirming that buyers across major end-user sectors favored programmable, repeatable machine tools. This position is reinforced by the fact that fully automatic systems deliver stronger process data, easier connection to shop-floor software, and tighter part consistency across the turning machine and equipment industry. The same segment is forecast to grow at a 7.2% CAGR through 2031, indicating that new investment is increasingly concentrated in the highest automation tier. Semi-automatic systems remain a viable option, especially in South and Southeast Asia, where some manufacturers are not yet ready to move to fully automated loading and unloading workflows. Manual turning machine and equipment is declining in developed markets, although it still serves toolrooms, training centers, and repair shops in settings where batch sizes remain small or part geometry changes often.

The turning machine and equipment market is increasingly influenced by software integration, digital connectivity, and process traceability, as automation value now depends not only on spindle performance but also on broader manufacturing system integration. NIST documented cases in which automation integration, including collaborative robot tending, improved spindle utilization and supported return on investment within 8 months. ISO 9001 and sector-specific quality systems also raise the value of machines that can capture process data and maintain repeatable output over time. This continues to accelerate the adoption of advanced automation technologies, including robotic tending, digital monitoring, and integrated manufacturing systems, rather than maintaining equal growth across manual, semi-automatic, and fully automatic equipment categories.

By End-User Industry: Automotive Anchors, Aerospace Accelerates

Automotive and commercial vehicles accounted for 35% of the turning machine and equipment market in 2025, keeping the segment in first place because they consume large volumes of crankshafts, camshafts, transmission housings, and EV motor shafts. The segment’s scale reflects a broad installed base and a steady demand for precise, repeatable output across both legacy powertrain and newer electric platforms. AMT reported that automotive manufacturers increased investment in manufacturing technology by 22.2% in 2025, indicating that retooling demand remained active across the turning machine and equipment market. Oil, gas, and energy remained an important secondary demand pool, especially for valve bodies, downhole tools, and large-diameter components that fit vertical turning centers and heavy-duty CNC lathes. Medical devices, electronics, semiconductor equipment, and general industrial machinery also offer meaningful positions, with semiconductor demand supported by fab expansion and related tooling needs.

Aerospace and defense is forecast to grow at a 7.5% CAGR from 2026 to 2031, the fastest pace among end users in the turning machine and equipment market. AMT stated that United States aerospace manufacturers posted their highest monthly manufacturing technology order value on record in March 2025, and aerospace capacity utilization moved above pre-strike levels in February 2025. FAA fleet forecasts also support a long runway for demand, as the United States commercial fleet is expected to expand to 10,607 aircraft by 2045, up from 7,387 in 2024. AS9100D certification requirements create barriers to entry that protect established suppliers, while smaller categories such as defense ordnance and consumer goods add incremental demand inside the turning machine and equipment industry.

Geography Analysis

Asia-Pacific held 48.91% of the turning machine and equipment market share in 2025 and is projected to expand at an 8.12% CAGR through 2031. This keeps the region as both the largest and fastest-growing geography in the turning machine and equipment market. China remains the core anchor because it is the world’s largest machine tool producer and consumer, and VDW reported that China accounted for 32% of global machine tool consumption in 2025. China’s treatment of machine tools as critical core technology under its current planning framework supports continued domestic production, import substitution, and export growth. Japan also plays a leading role in the turning machine and equipment market, as companies such as Mazak, Okuma, Citizen, Tsugami, and Star Micronics continue to advance swiss-type and multitasking capabilities.

India has the fastest-growing demand momentum in Asia-Pacific, as new industrial investment is broadening the local customer base for advanced metalworking systems. The United States International Trade Administration stated that India attracted USD 165.1 billion in manufacturing investment in 2024 and expects manufacturing’s share of gross value added to rise from 14% in 2025 to 21% by 2032. The trend supports a longer purchase cycle for CNC lathes, automation systems, and related tooling across the turning machine and equipment market. Southeast Asian hubs such as Vietnam, Thailand, Indonesia, and Malaysia are also adding precision metalworking capacity as companies spread their supply chains across multiple production bases. This shift keeps regional demand broad rather than concentrated in a single national market.

Europe presents a mixed picture in the turning machine and equipment market, combining deep technical capability with cautious short-term investment behavior. Germany, Italy, and Spain remain major consumers of machine tools. At the same time, German production reached EUR 13.6 billion (USD 16.0 billion) in 2025, and turning machines and turning centers accounted for EUR 1.1 billion (USD 1.3 billion), equal to 7.5% of that total. German domestic orders fell 16% in 2025, though fourth-quarter orders recovered 4% from the prior year, suggesting the downturn had started to stabilize. The Middle East and Africa, along with South America, add smaller but steady gains to the turning machine and equipment market as Saudi Arabia, the UAE, South Africa, Brazil, and Mexico build capacity tied to oil and gas, defense, and automotive supply chains.

Competitive Landscape

The turning machine and equipment market is moderately concentrated, with strong global OEMs alongside numerous regional and emerging Chinese manufacturers. These companies compete less on headline price and more on accuracy, reliability, integration with automation, and lifetime operating value, which helps protect margins in the premium segment. Chinese manufacturers are expanding aggressively in the mid-market and export markets, and VDW reported that China’s machine tool exports reached EUR 8.6 billion (USD 10.1 billion) in 2025, up 13% from the prior year. This leaves the turning machine and equipment market with a clear split between technology-heavy premium systems and more price-competitive alternatives that are gaining ground in standard applications.

Strategic investment remains active among leading suppliers in the turning machine and equipment market. DMG MORI is committed to investing at least USD 40.5 million in a new 90,000 sq ft advanced manufacturing and R&D facility in Chicago under the Illinois EDGE program, which shows a clear push to deepen North American production and engineering capacity. In 2025, DMG MORI also invested EUR 65 million (USD 76.5 million) in property, plant, and equipment and spent EUR 88.4 million (USD 104.0 million) on R&D, indicating continued emphasis on product development and factory capabilities. Okuma expanded its product line in April 2026 with the MULTUS U1000 and U2000, both designed for full 5-axis capability and a compact footprint. Mazak also reinforced its United States manufacturing base in 2025 by completing the 40,000th machine at its Florence, Kentucky, facility and preparing for its 21st expansion.

The turning machine and equipment market presents opportunities for modular automation solutions, particularly among smaller manufacturers seeking productivity improvements with lower capital investment. Current top-tier automation ecosystems are strongest for large customers, while smaller manufacturers still need lower-cost turnkey systems that can improve labor use without requiring a full plant redesign. Patent and systems development in adaptive control, digital twin tools, and intelligent machining continue to favor Japanese and German OEMs, which supports their edge in high-precision applications. Tooling companies also matter in this competitive landscape, and Kennametal’s metal-cutting business shows how machine builders and tooling suppliers are aligning more closely around application outcomes rather than selling equipment as isolated assets.

Turning Machine and Equipment Industry Leaders

DMG MORI

Mazak Corporation

Okuma Corporation

DN Solutions

Haas Automation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Okuma launched the MULTUS U1000 and MULTUS U2000 multi-tasking turning machines at its Krefeld, Germany office. Both models feature 5-axis simultaneous machining, a standard 80-tool magazine, and the most compact footprint in the MULTUS U series at 8.2 m², targeting complex workpieces in the medical, EV component, and precision equipment sectors.

- April 2026: DMG MORI AG, through the Illinois EDGE incentive program, committed to investing at least USD 40.5 million in a new 90,000 sq-ft advanced manufacturing and R&D facility in Chicago, with at least 74 new full-time jobs, underscoring its strategic emphasis on North American CNC manufacturing and engineering capability.

- March 2026: United States metalworking machinery orders reached USD 681.3 million in March 2026, up 31.5% over March 2025, bringing the Q1 2026 total to USD 1.61 billion, a 27.8% year-over-year increase, according to AMT. This signals accelerating investment by machine shops, aerospace manufacturers, and defense manufacturers as they entered 2026.

- February 2026: PMGC Holdings Inc. completed the acquisition of SVM Machining, Inc., its third California-based CNC machine shop acquisition, expanding its precision turning, milling, and machining platform serving aerospace, defense, medical, and industrial sectors.

Global Turning Machine and Equipment Market Report Scope

The Turning Machine and Equipment Market is Segmented by Product Type (Horizontal, Vertical, Swiss-Type, Conventional, and More), by Automation Type (Manual, Semi-Automatic, and Fully Automatic CNC), by End-User Industry (Automotive & Commercial Vehicles, Aerospace & Defense, and More), and by Geography (North America, Asia-Pacific, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

| Horizontal |

| Vertical |

| Swiss-Type |

| Multi-Tasking |

| Conventional |

| Manual |

| Semi-Automatic |

| Fully Automatic CNC |

| Automotive & Commercial Vehicles |

| Aerospace & Defense |

| Medical Devices & Surgical Instruments |

| Oil, Gas, & Energy |

| Electrical, Electronics & Semiconductor Equipment |

| General Industrial Machinery |

| Others (Consumer Goods, Defense Ordnance) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Benelux (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Southeast Asia (Indonesia, Vietnam, Thailand, Malaysia, Philippines) | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Product Type | Horizontal | |

| Vertical | ||

| Swiss-Type | ||

| Multi-Tasking | ||

| Conventional | ||

| By Automation Type | Manual | |

| Semi-Automatic | ||

| Fully Automatic CNC | ||

| By End-User Industry | Automotive & Commercial Vehicles | |

| Aerospace & Defense | ||

| Medical Devices & Surgical Instruments | ||

| Oil, Gas, & Energy | ||

| Electrical, Electronics & Semiconductor Equipment | ||

| General Industrial Machinery | ||

| Others (Consumer Goods, Defense Ordnance) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Benelux (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Southeast Asia (Indonesia, Vietnam, Thailand, Malaysia, Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the market size of the turning machine and equipment market in 2026, and how is it expected to grow by 2031?

The turning machine and equipment market size stood at USD 13.4 billion in 2025, reached USD 14.2 billion in 2026, and is projected to hit USD 19 billion by 2031 at a 6% CAGR.

Which product type leads sales in the turning machine and equipment market?

Horizontal systems led with a 61% share in 2025 because they remain widely used across automotive, aerospace, and general industrial applications.

Which product category is growing the fastest through 2031?

The multi-tasking segment is forecast to grow the fastest, at a 7.8% CAGR, as buyers seek fewer setups, shorter handling times, and better machine utilization.

Why is EV production important for turning machine and equipment demand?

EV production is driving demand for rotor shafts, motor housings, and axle parts that require tighter tolerances and more advanced CNC turning capabilities.

Which end-user segment is the largest buyer of turning machine and equipment?

Automotive and commercial vehicles accounted for 35% of the market in 2025, making them the largest end-user segment for turned precision components.

Which region is strongest for turning machine and equipment demand?

Asia-Pacific remains the largest regional base, supported by China’s 32% share of global machine tool consumption in 2025 and by rising investment across India and Southeast Asia.

Page last updated on: