Turning Centers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 21.90 Billion |

| Market Size (2031) | USD 28.40 Billion |

| Growth Rate (2026 - 2031) | 5.34% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

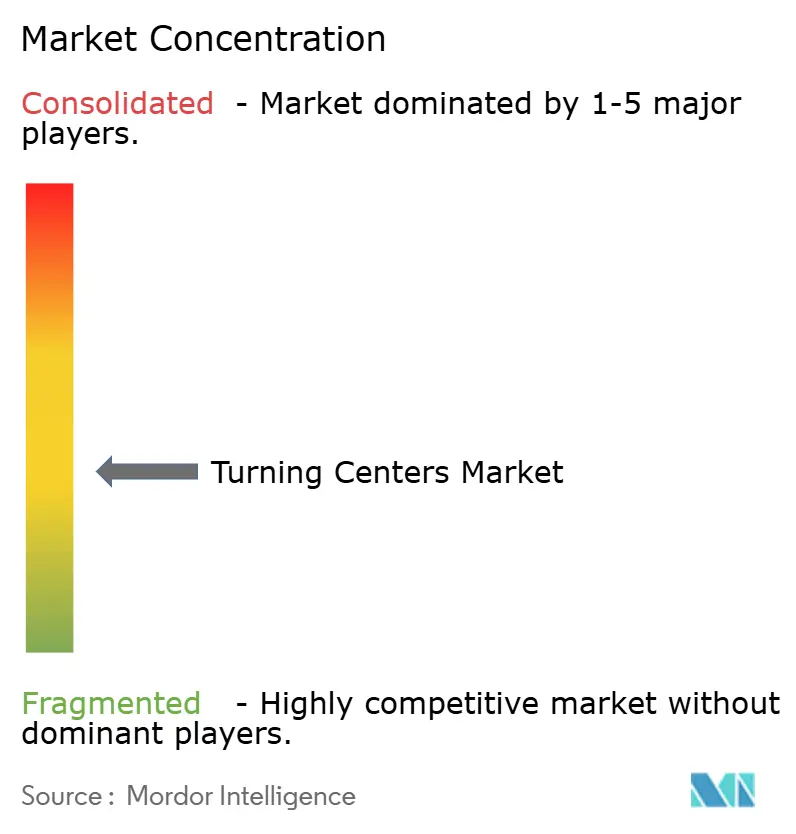

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Turning Centers Market Analysis by Mordor Intelligence

The Turning Centers Market size is projected to be USD 20.80 billion in 2025, USD 21.90 billion in 2026, and reach USD 28.40 billion by 2031, growing at a CAGR of 5.34% from 2026 to 2031.

The turning centers market is expanding as manufacturers replace older 2- and 3-axis machines with multi-axis platforms that complete more work in a single setup. Investment activity is also being supported by stronger capital spending on precision machining infrastructure, especially in the United States, where metalworking machinery orders rose sharply in 2025 and continued to increase in early 2026. Demand is also being shaped by reshoring programs, electric vehicle powertrain requirements, and aerospace production methods that favor single-clamp machining and tighter process control. Asia-Pacific remains the largest base for the turning centers market because of the scale of manufacturing in China, Japan, South Korea, and India, while North America is gaining from new regional production capacity, and Europe continues to hold its place through high-precision machine builders. Competition is more concentrated among premium machine builders than in entry-level systems, with Japanese and German builders leading advanced turn-mill platforms.

Key Report Takeaways

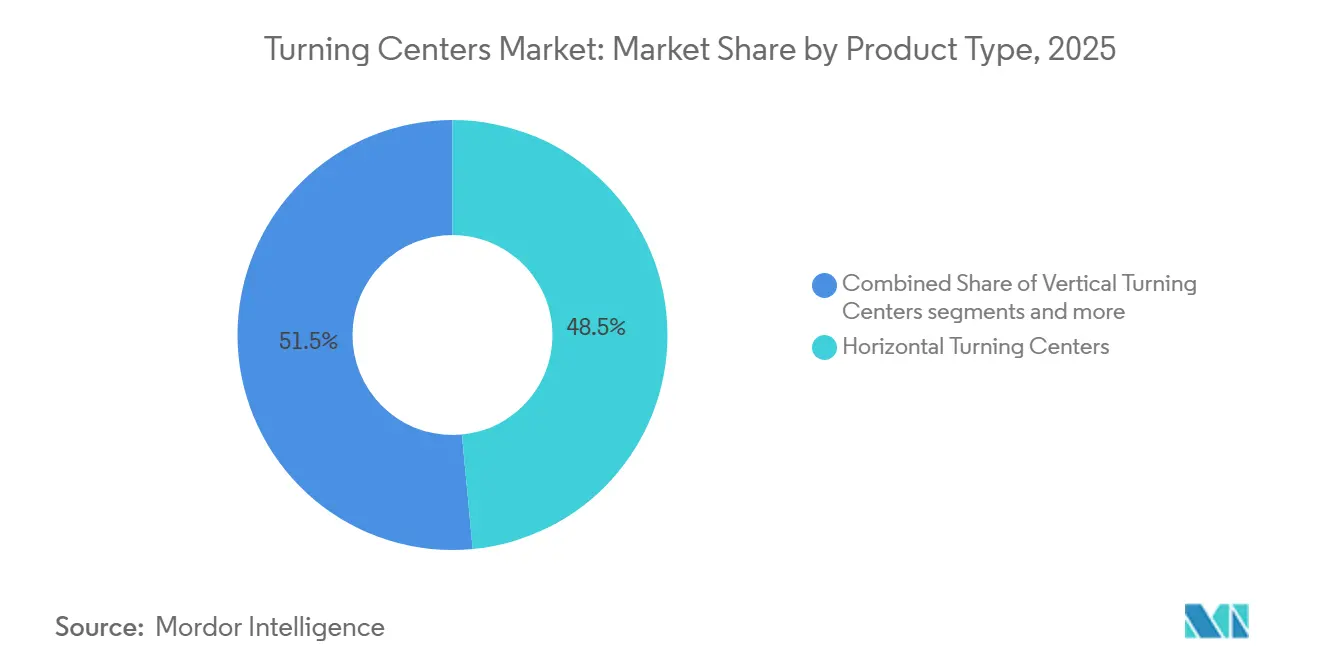

- By product type, horizontal turning centers held 48.5% of the turning centers market share in 2025, while multi-tasking turning centers are forecast to expand at a 7.2% CAGR through 2031.

- By axis configuration, 3-axis turning centers accounted for 52% of the market in 2025, while the 5-axis and above segment is expected to record the highest projected CAGR at 8.1% through 2031.

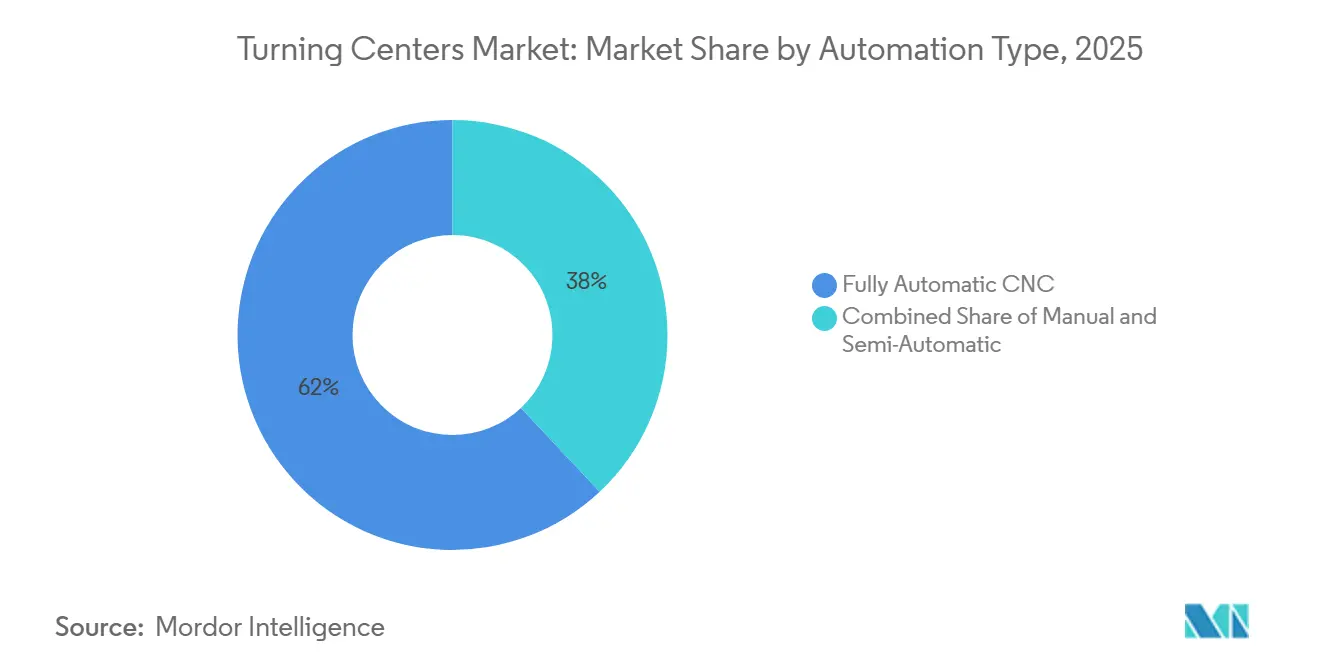

- By automation type, fully automatic CNC turning centers accounted for 62% of the turning centers market size in 2025, and this segment is projected to expand at a 6.8% CAGR through 2031.

- By end-user industry, automotive and commercial vehicles held 38.5% of the market in 2025, while aerospace and defense are forecast to grow at a 7.5% CAGR through 2031.

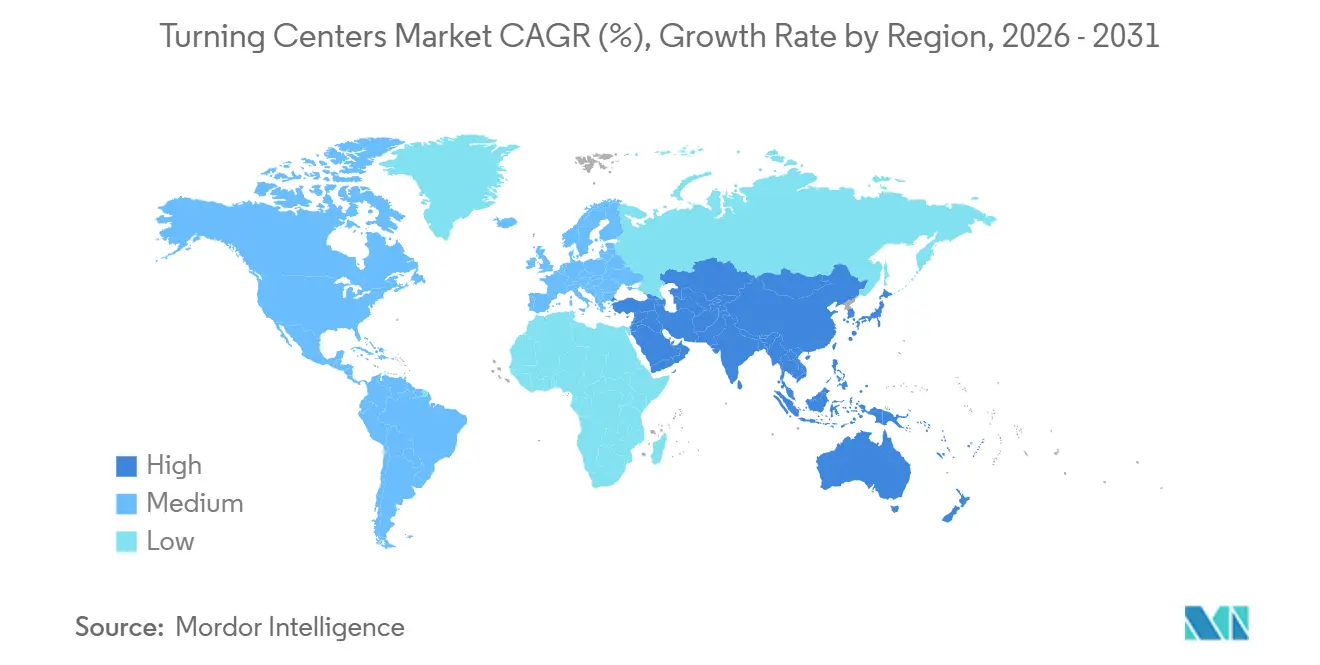

- By geography, Asia-Pacific accounted for 58.2% of the turning centers market size in 2025 and is projected to expand at a 5.9% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Turning Centers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift to Multi-Tasking Turning Centers: Reduced Setup Times and Floor Space | +1.0% | Global | Medium term (2-4 years) |

| Reshoring And Friendshoring Investments in the United States, Mexico, And India | +0.9% | North America, South Asia | Medium term (2-4 years) |

| EV Powertrain Complexity Raising Demand for Y-Axis And B-Axis Turning Centers | +0.8% | Asia-Pacific, Europe | Short term (≤ 2 years) |

| Aerospace Single-Piece-Flow Requirements Supporting 5-Axis Turn-Mill Adoption | +0.7% | North America, Europe | Medium term (2-4 years) |

| Growing Complexity of Oil and Gas Valve and Wellhead Components Requiring Multi-Axis Turning Centers | +0.6% | Middle East, North America | Medium term (2-4 years) |

| Labor Cost Pressure Supporting Lights-Out Turning Cell Investment | +0.5% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shift to Multi-Tasking Turning Centers: Reduced Setup Times and Floor Space

The turning centers market benefits from the shift toward machines that eliminate multiple setup steps within a single production flow. Manufacturers are increasingly adopting multitasking turning centers to combine turning, milling, drilling, boring, and other machining operations on a single platform, thereby improving process continuity and reducing manual intervention. Conventional processing still causes time losses due to re-clamping, re-indicating, and part transfers between separate machines, while also increasing the risk of dimensional variation and alignment errors. WFL reported that aerospace deployments reduced the number of sequential setups from more than 10 to 3-5 on average, while productivity for the same part families improved by 200%-300%. This improvement is particularly relevant for complex, high-value components that require tight tolerances and repeatable machining quality. This shift also reduces work-in-process inventory, as fewer machines are involved in the route and fewer batches wait between steps, allowing plants to shorten lead times and improve floor-level efficiency. Nidec Takisawa also introduced a compact multitasking model with a 30% smaller footprint than conventional alternatives, supporting the turning centers market in space-constrained plants where manufacturers need higher output without expanding production space.

Reshoring and Friendshoring Trends Driving Investments in the United States, Mexico, and India

The turning centers market is also being supported by production programs that move precision machining closer to end-use demand. The Reshoring Initiative reported 244,000 United States manufacturing jobs announced in 2024 through reshoring and foreign direct investment, showing that production location decisions are feeding new equipment demand.[1]Reshoring Initiative, “2024 Annual Report Including 1Q2025 Insights,” Reshoring Initiative, reshorenow.org This matters because new domestic plants and supplier expansions need machining capacity that can be installed quickly and run with fewer setups. In India, the Production Linked Incentive scheme had attracted INR 2.4 lakh crore (USD 26.7 billion) in cumulative investment across 14 sectors by March 2026, and the automobile and auto-components program alone drew INR 44,326 crore (USD 4.9 billion), which directly supports demand for precision-machining equipment.[2]Press Information Bureau, “Production Linked Incentive Scheme Performance Update,” Government of India, pib.gov.in AMT also found in its 2025 survey that workforce availability remained central to further reshoring, which strengthens the case for more automated cells in the turning centers market.

EV Powertrain Complexity Driving Y-Axis and B-Axis Turning Center Adoption for Motor Shaft and Housing Families

The turning centers market is benefiting from electric vehicle parts that demand tighter geometric control than many combustion drivetrain components. Motor shafts in EV drive units are now operating at speeds above 18,000 RPM, and the cited balancing requirement of ISO 1940 G1.0 underscores the need for highly stable, precise processing. That requirement makes simple 2-axis machining less suitable for full-process shaft production when bearing-seat accuracy must stay at or below 0.01 mm across the shaft length. Y-axis and B-axis machine layouts help combine turning, milling, and related operations into a single clamping cycle, reducing cumulative error across the part. As EV output rises, contract manufacturers that previously used simpler platforms are moving toward higher-capability machines, which lifts the technical mix of the turning centers market.

Aerospace Single-Piece-Flow Requirements Driving 5-Axis Turn-Mill Adoption

The turning centers market is also being driven by aerospace production methods that prioritize one-piece flow and minimal part handling. A single re-clamping event can shift the datum on a high-value titanium or nickel-alloy part and place the full blank outside tolerance. HAINBUCH documented a GE Aerospace application in Wilmington in which turbine components were fully machined in a single setup, completed after a 180-degree flip on a DMG MORI NT-series mill-turn platform. WFL also reported that Schaeffler Aerospace achieved turning tolerances of 20 µm and milling tolerances of 10 µm during complete machining with a B-axis-enabled MILLTURN system. AMT data further showed that aerospace customers increased machinery orders by 45.1% in 2025 versus 2024, reinforcing the demand outlook for advanced machines in the turning centers market.[3] Association For Manufacturing Technology, “Reshoring Survey Reveals 4 Priorities for US Reindustrialization,” AMT, amtonline.org

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Unit Price and Long ROI Horizon Limiting SME Adoption | -0.6% | Global, intensified in Southeast Asia and South America | Long term (≥ 4 years) |

| Export Controls Restricting Access to Advanced 5-Axis Turning Center Technology | -0.5% | Middle East, Eastern Europe, parts of Asia-Pacific | Short term (≤ 2 years) |

| Programming Complexity in Multi-Axis Turning Centers | -0.4% | Global | Medium term (2-4 years) |

| Toolholder and Fixturing Ecosystem Fragmentation (BMT, VDI, Capto) | -0.3% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Unit Price and Long ROI Horizon Limiting SME Adoption

The turning centers market still faces a structural limit: smaller contract shops cannot absorb the large upfront equipment costs. A fully configured multi-axis machine can cost USD 250,000 to USD 800,000 at the machine level. At the same time, a fully equipped production cell with automation, tooling, workholding, and software can cost more than USD 1 million. Under standard single-shift assumptions, the payback period is often 3 to 5 years, which is longer than the capital planning horizon used by many small and medium-sized manufacturers. This slows replacement demand in the turning centers market because the largest productivity gains are concentrated in companies that already have stronger order visibility, better utilization, and in-house programming depth. The gap is wider in Southeast Asia and South America, where financing costs remain higher, and incentive support is less developed.

Export Controls Restricting Access to Advanced 5-Axis Turning Center Technology

The turning centers market is also constrained by export control rules that affect advanced multi-axis platforms and related software. The United States Bureau of Industry and Security classifies certain 5-axis machine tools and associated capabilities under controlled categories, and the August 2024 rule expanded restrictions on the operation of CNC machine tool software for Russia and Belarus. These controls do not stop domestic use inside the main producing economies, but they slow international delivery and limit addressable demand for some high-specification systems. DMG MORI stated that longer export license processing times and related shipment delays contributed to a 6% decline in 2025 sales revenue, even as order intake increased by 4%. This creates a split in the turning centers market, where, particularly in markets affected by recent export controls, machines face greater trade friction than standard machines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Multi-Tasking Models Gain Share Beyond Horizontal Dominance

Horizontal turning centers held 48.5% of the market in 2025, making them the largest product category in the turning centers market. Their strong position stems from long-standing use in automotive, general industrial, and contract-machining lines that process large volumes of rotational parts. Workholding remains simple, chip flow is well understood, and maintenance practices are familiar to a wide installed base. Those factors keep horizontal systems as the default choice when throughput, standardization, and unit cost matter more than process consolidation.

Vertical turning centers serve a different part profile in the turning centers market because they are better suited to large-diameter, heavy, and disc-shaped workpieces. That fit has supported use in energy, wind power, and large industrial machinery applications where gravity-assisted loading is an operational advantage. Multi-tasking turning centers, however, are the fastest-growing product type and are projected to rise at a 7.2% CAGR through 2031. WFL showed that setup reduction and process consolidation can produce major productivity gains, which explains why multi-tasking platforms are taking share in the turning centers market.

By Axis Configuration: 5-Axis Adoption Accelerates in High-Value Applications

3-axis turning centers accounted for 52% of the market in 2025, underscoring that the turning centers market still relies heavily on conventional turning, facing, and boring work. This installed base remains important across general industrial output and in large volumes of automotive parts, where part geometry remains relatively straightforward. The 4-axis machines broaden capability through live tooling or C-axis functionality, reducing the need for a second setup on parts with off-center features. That makes them a practical bridge between basic lathes and more advanced mill-turn platforms.

The fastest expansion in the turning centers market is occurring in 5-axis and above systems, which are forecast to grow at a 8.1% CAGR through 2031. These machines are gaining popularity because aerospace, EV, and oil and gas parts often require B-axis motion, contouring flexibility, and synchronized operations that simpler layouts cannot match. A peer-reviewed MDPI study on monolithic blisk machining found that 5-axis simultaneous contouring reduced stack-up errors by 72% compared with 3-axis multi-setup methods. As qualification requirements become stricter in high-value programs, buyers in the turning centers market have less room to compromise on machine capability.

By Automation Type: Fully Automatic CNC Commands the Core, Lights-Out Expands Its Frontier

Fully automatic CNC turning centers held 62% of the market in 2025, which made this the largest automation category in the turning centers market. The same segment is also projected to grow at a 6.8% CAGR through 2031, indicating that installed-base dominance and forward growth are moving in tandem. Semi-automatic systems still retain a role in toolrooms, prototype work, and smaller shops where operators remain part of the process loop. Manual turning centers continue to serve training, repair, and maintenance applications, but their share is narrowing over time.

The market is increasingly shifting beyond CNC control toward autonomous manufacturing cells and toward autonomous cell behavior around the machine. Robotic handling, automated tool changes, and in-process gauging reduce labor dependence and support longer unattended runs. This is especially relevant in regions where manufacturers are under pressure to add output without adding full shifts of skilled operators. As a result, the turning centers market is moving toward cells that combine machine performance with process continuity rather than stand-alone machine capability.

By End-User Industry: Aerospace & Defense Outpaces Automotive in Growth Rate

Automotive and commercial vehicles accounted for 38.5% of the market in 2025, maintaining their position as the largest end-user base in the turning centers market. That position reflects the scale of crankshaft, camshaft, rotor, hub, shaft, and brake component production across global vehicle supply chains. Turning remains well aligned with these part families because they are cylindrical, repetitive, and often produced in high volume. Even as powertrain mix changes, the broad need for rotational precision components keeps automotive demand relevant.

Aerospace and defense is the fastest-growing end-user group in the turning centers market, with a projected CAGR of 7.5% through 2031. The segment is benefiting from single-piece flow manufacturing, difficult-to-machine materials, and documentation standards that favor premium turn-mill platforms. HAINBUCH documented that complete machining on a DMG MORI NT-series machine eliminated the need for a secondary milling setup in a GE Aerospace application, thereby supporting traceability and process stability for safety-critical parts. Medical devices, oil and gas, electrical and electronics, and general industrial machinery all remain meaningful demand pools in the turning centers market because each one requires a distinct balance of precision, rigidity, and part-handling capability.

Geography Analysis

Asia-Pacific held 58.2% of the turning centers market share in 2025 and is also the fastest-growing regional segment with a projected 5.9% CAGR through 2031. China remains the largest contributor within the regional base due to its scale in automotive, electronics, and general industrial production. Japan also remains central to the turning centers market through its depth in machine tool manufacturing and export strength. JMTBA reported total Japanese machine tool orders of JPY 1,604.32 billion (USD 10.3 billion) in 2025, with foreign orders increasing by 11.5%. India is also becoming a stronger source of incremental demand as manufacturing incentives translate into new precision machining capacity.

North America is the clearest growth engine outside Asia-Pacific in the turning centers market. United States metalworking machinery orders reached USD 5.74 billion in 2025, and Q1 2026 orders stood at USD 1.61 billion, indicating continued acceleration in capital equipment spending. Aerospace buyers in the region also lifted machinery spending by 45.1% in 2025 versus 2024, which aligns with expanding demand for advanced 5-axis and turn-mill systems. Mexico continues to benefit as suppliers place turning capacity near vehicle assembly and in cross-border production programs.

Europe remains important to the turning centers market because Germany, Italy, and Switzerland hold a dense base of precision machine tool capability. DMG MORI reported 2025 order intake of EUR 2,340.2 million (USD 2,752.8 million), with international orders up 10%, which shows that premium equipment demand remained resilient despite delivery friction. The Middle East & Africa remains a relatively small demand base, but oil and gas services, defense manufacturing, and downstream processing are creating new installed-base opportunities. South America remains anchored by Brazil and mining-related maintenance activity, although financing limits continue to slow broader adoption in the turning centers market.

Competitive Landscape

The turning centers market is moderately fragmented in premium multi-axis systems and far more fragmented in mid-range and entry-level equipment. Japanese builders such as DMG MORI, Mazak, and Okuma hold strong positions in 5-axis, turn-mill, and higher-value configurations where machine accuracy, software integration, and service support matter most. Korean suppliers remain active in horizontal and vertical systems through price discipline and close ties with automotive manufacturing programs. European specialists also keep defensible positions in selected applications because their engineering depth is difficult to replace with lower-cost alternatives. Chinese domestic manufacturers are narrowing the gap in 3-axis and entry-level 4-axis machines, but the turning centers market still shows a clear divide between standard capacity and premium capability.

A major competitive shift in the turning centers market is the move from machine supply to full-cell delivery. Customers increasingly value an integrated turnkey manufacturing cell that combines the machine, loading system, in-process measurement, and digital monitoring rather than sourcing each part separately. DMG MORI Federal Services announced a USD 40.5 million investment in a new 90,000-square-foot advanced manufacturing and R&D facility in the Chicago area in February 2026, which strengthens its regional position in defense, aerospace, and advanced industrial applications. That type of investment shows that local engineering support is becoming just as important as machine specification in the turning centers market.

Technology-led product launches are also shaping the competitive balance in the turning centers market. Nidec Takisawa launched the TEX-2500S multitasking turning center with a 30% smaller footprint and the capacity to hold up to 60 tools, directly targeting customers who want compact yet capable systems. DMG MORI also reported EUR 88.4 million (USD 95.5 million) in research and development spending in 2025, demonstrating continued focus on advanced capabilities and software-linked retention. The companies that can combine precision, automation integration, service density, and application engineering are expected to remain competitive based on current industry trends and hold the strongest positions as replacement cycles continue.

Turning Centers Industry Leaders

DMG MORI

Mazak Corporation

Okuma Corporation

DN Solutions

Haas Automation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: DMG MORI Federal Services, Inc. announced a USD 40.5 million investment to establish a new 90,000-square-foot advanced manufacturing and R&D facility in the Chicago, Illinois metropolitan area, creating 74 jobs. The facility targets North American defense, aerospace, and advanced industrial machining customers and is supported by the Illinois EDGE program.

- January 2026: DMG MORI expanded the deployment of the CELOS X digital manufacturing platform across turning centers, enabling AI-assisted process optimization, predictive maintenance, and cloud connectivity.

Global Turning Centers Market Report Scope

The Turning Centers Market is Segmented by Product Type (Horizontal Turning Centers, Vertical Turning Centers, and More), by Axis Configuration (3-Axis, 4-Axis, and More), by Automation Type (Manual, Semi-Automatic, and More), by End-User Industry (Automotive and Commercial Vehicles, and More), and by Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

| Horizontal Turning Centers |

| Vertical Turning Centers |

| Multi-Tasking Turning Centers |

| Others |

| 3-Axis |

| 4-Axis |

| 5-Axis and Above |

| Manual |

| Semi-Automatic |

| Fully Automatic CNC |

| Automotive and Commercial Vehicles |

| Aerospace & Defense |

| Medical Devices and Surgical Instruments |

| Oil, Gas, and Energy |

| Electrical, Electronics and Semiconductor Equipment |

| General Industrial Machinery |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Benelux (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Southeast Asia (Indonesia, Vietnam, Thailand, Malaysia, Philippines) | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Product Type | Horizontal Turning Centers | |

| Vertical Turning Centers | ||

| Multi-Tasking Turning Centers | ||

| Others | ||

| By Axis Configuration | 3-Axis | |

| 4-Axis | ||

| 5-Axis and Above | ||

| By Automation Type | Manual | |

| Semi-Automatic | ||

| Fully Automatic CNC | ||

| By End-User Industry | Automotive and Commercial Vehicles | |

| Aerospace & Defense | ||

| Medical Devices and Surgical Instruments | ||

| Oil, Gas, and Energy | ||

| Electrical, Electronics and Semiconductor Equipment | ||

| General Industrial Machinery | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Benelux (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Southeast Asia (Indonesia, Vietnam, Thailand, Malaysia, Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the expected value of the turning centers market by 2031?

Turning center market is projected to reach USD 28.4 billion by 2031, rising from USD 21.9 billion in 2026 at a 5.34% CAGR.

Which product category leads equipment demand?

Horizontal turning centers led in 2025 with a 48.5% share because they remain the standard choice for high-volume rotational part production.

Which machine configuration is growing the fastest?

5-axis and above is the fastest-growing axis configuration, with an 8.1% CAGR through 2031, driven by demand for aerospace, EVs, and complex components.

Why is Asia-Pacific the largest regional base?

Asia-Pacific accounted for 58.2% in 2025, driven by China's large-scale production, Japan's anchor role in machine tool capability, and India's new manufacturing capacity.

What is the biggest hurdle for smaller manufacturers?

High upfront costs remain the main hurdle, as advanced multi-axis cells can exceed USD 1 million and often require a 3- to 5-year payback period.

What strategies are shaping competition in 2026?

Local expansion, automation integration, and compact multi-tasking product launches are shaping competition, as shown by DMG MORI’s Illinois investment and Nidec Takisawa’s launch of the TEX-2500S.

Page last updated on: