Turkey Data Center Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | 316.70 megawatt |

| Market Volume (2026) | 471.39 megawatt |

| Market Volume (2031) | 525.99 megawatt |

| Growth Rate (2026 - 2031) | 2.23% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Turkey Data Center Market Analysis by Mordor Intelligence

The Turkey data center market size reached 66 MW of installed IT load in 2025 and is forecast to expand to 140 MW by 2030, translating into a 16.23% CAGR across the period. This rapid scale-up reflects Turkey’s role as a digital interconnection bridge between Europe, the Middle East and Asia, combined with forceful regulatory triggers such as the Personal Data Protection Law (KVKK) and a USD 46.2 billion public digital-infrastructure budget earmarked for 2025. Global hyperscalers are committing fresh capital, regional telecom groups are modernizing backbone networks, and tax incentives inside technology-free zones are compressing payback periods for new builds. The surge in OTT video, competitive mobile-gaming leagues and private 5G deployments has pulled utilization to 71%, while energy-efficiency retrofits keep average power-usage-effectiveness below 1.3 despite a 25% grid-tariff hike in April 2025. Competitive rivalry is being reshaped by foreign entries Equinix’s June 2024 USD 93 million Istanbul acquisition is the sharpest example yet indigenous carriers such as Turkcell still control the majority of carrier-neutral fiber pairs into the largest facilities.

Key Report Takeaways

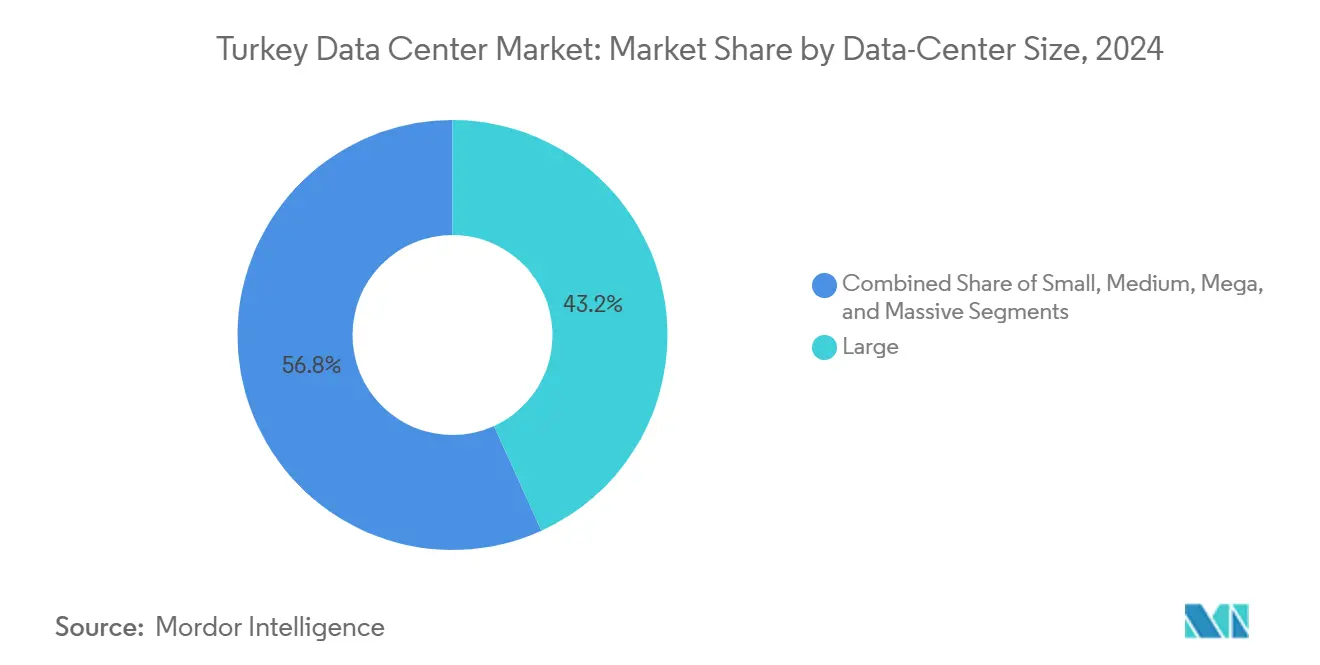

- By data center size, large data centers held 43.2% of Turkey data center market share in 2024, while the Mega-facility segment is projected to post the highest growth at 17.5% CAGR through 2030.

- By tier standard, tier III infrastructure accounted for 57% of the Turkey data center market size in 2024; Tier IV leads future growth with an 18.2% CAGR as operators harden sites against seismic risk.

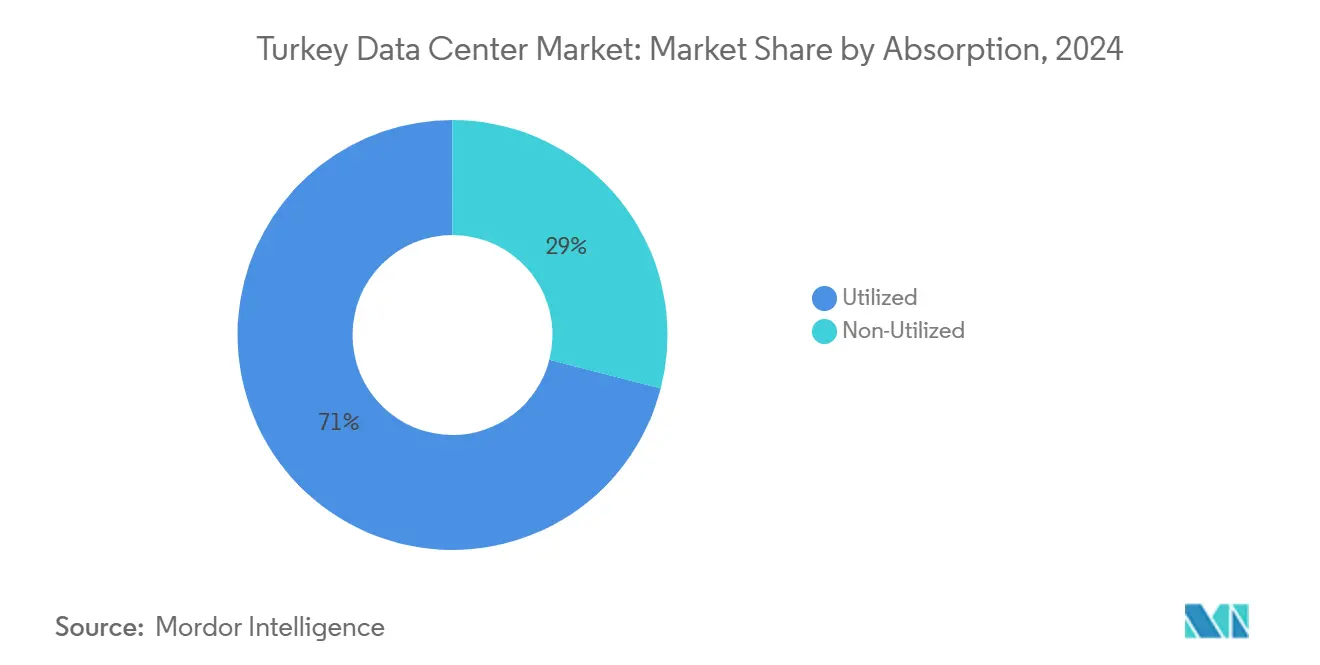

- By absorption, the utilized capacity represented 71% of the current supply in 2024, and this absorption level is expected to expand at a 13.8% CAGR, indicating sustained underlying demand momentum.

- By hotspot, İstanbul captured 78% of the Turkey data center market in 2024, whereas İzmir is advancing at a 16.9% CAGR and is on track to be the fastest-growing hotspot by 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Turkey Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in OTT streaming, gaming and mobile-data consumption | +3.20% | National, focused on İstanbul and İzmir | Short term (≤ 2 years) |

| Government “Digital Türkiye 2024-2028” program | +2.80% | Country-wide with priority regions | Medium term (2-4 years) |

| Entry and expansion of hyperscale cloud platforms | +4.10% | İstanbul, İzmir, select secondary cities | Medium term (2-4 years) |

| KVKK localization mandates | +2.50% | National | Long term (≥ 4 years) |

| Trans-continental submarine-cable corridors | +1.90% | İstanbul and Çanakkale | Long term (≥ 4 years) |

| Tax incentives in tech-free zones | +1.80% | Nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in OTT Streaming, Gaming and Mobile-Data Consumption

Connected-device volumes reached 18.8 billion in 2024, up 13% year-on-year, creating bandwidth peaks that can only be met through proximate compute capacity.[1]Timur Sırt, “Increase in Connected IoT Devices Drives Economic Growth,” Daily Sabah, dailysabah.com Edge-node clusters are therefore being embedded inside multi-tenant data centers in İstanbul and İzmir to trim content-delivery latency below 20 milliseconds for real-time game play. The national 5G rollout, accelerated by ULAK-TURKSAT’s private-network agreement in March 2025, is saturating radio backhaul links and pushing traffic bursts into local caches. Cloud providers have reacted by pre-leasing entire halls months before energization, ensuring reserved power for AI-based recommendation engines. The consumption boom is also driving investment in immersion cooling and modular UPS systems to contain rising power densities. These technology upgrades reinforce the Turkey data center market as a strategic edge-media hub serving three continents.

Government “Digital Türkiye 2024-2028” Digital-Transformation Agenda

An outlay of USD 16.3 billion within the 2025 public-investment program targets communications infrastructure, with specific milestones for fiber-to-the-home coverage and sovereign cloud adoption. [2]Republic of Turkey, “Türkiye Allocates USD 46.2 Billion to Public Investments in 2025,” invest.gov.tr The National AI Strategy intends to lift AI’s GDP contribution to 5% by 2025 and to spawn 50,000 skilled jobs. Procurement guidelines already stipulate preference for domestically hosted workloads, driving municipal and central-government agencies to migrate archives from offshore data pools into Tier III and Tier IV sites. The 2025 Cybersecurity Law No. 7545 raises minimum compliance to ISO 27001 plus independent SOC monitoring, nudging banks and utilities to sign multi-year colocation deals in Turkish facilities. Meanwhile, smart-city pilots in Bursa, Konya and Gaziantep require regional micro-data centers to shorten sensor-to-AI feedback loops, thereby dispersing fresh capacity into secondary provinces. Collectively, these measures convert policy blueprints into visible rack demand.

Entry and Expansion of Hyperscale Cloud Platforms

Microsoft, Google and G42’s Khazna Data Centers have each placed Turkey on their near-term site roadmaps, citing its cross-border latency advantage to the Caucasus, Levant and Southern Europe. Equinix’s IS2 campus will scale to 22 MW, linking directly into MedNautilus and BlueMed cable systems to furnish sub-50-millisecond round trips into Frankfurt, Tel-Aviv and Dubai. Hyperscale design templates are lifting the baseline fit-out standard in the Turkey data center market, including hot-aisle containment, backbone lithium-ion battery UPS strings and 100 Gbit cross-connect fabrics. Domestic operators are responding by upgrading roof-height clearance for high-density racks and negotiating renewable PPAs that hedge against tariff escalation. Enterprise customers benefit from multicloud on-ramps housed under a single roof, compressing migration timetables and minimizing data-egress charges. As a result, hyperscale activity now influences wholesale land prices along the Marmara coastline and in İzmir’s industrial districts.

KVKK Localization Mandates

Amendments adopted in late 2024 tightened cross-border data-transfer exemptions, obliging platforms with more than 1 million daily Turkish users to process and store personal information domestically. Financial-services, health-care and critical-infrastructure operators now confront hard residency clauses that can only be satisfied through certified Turkish facilities. The Data Protection Authority’s 2025 guidelines favor Binding Corporate Rules but still demand local primary processing, prompting multinationals to lease contiguous racks in Tier IV builds outside earthquake zones. Compliance audits consider not just logical segregation but also physical location, accelerating take-up of domestically anchored disaster-recovery footprints. The permanence of localization rules establishes a non-cyclical demand floor, insulating the Turkish data center market from external macroeconomic swings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising electricity tariffs and Lira volatility | –2.1% | Nationwide; greatest impact on energy-intensive operations | Short term (≤ 2 years) |

| Earthquake-zone engineering and insurance premiums | –1.4% | İstanbul and other high-seismic regions | Medium term (2-4 years) |

| Scarcity of Tier IV certified facilities outside İstanbul | -1.20% | Central and Eastern Turkey | Medium term (2-4 years) |

| TEİAŞ grid-interconnection auction backlog delays | -1.00% | Nationwide; particularly affect new hyperscale developments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Electricity Tariffs and Lira Volatility

The April 2025 25% grid-tariff jump threatens EBITDA margins because energy outlays regularly top 35% of operating costs for high-utilization campuses. Operators billing in Turkish lira but sourcing equipment in USD or EUR face widened FX mismatches during fit-out cycles. PPAs tied to wind and solar farms now serve as currency and price hedges, yet only large incumbents can shoulder the multiyear commitment volumes required. Smaller entrants struggle to pass cost spikes onto customers locked into three-year fixed colocation contracts, heightening consolidation pressure within the Turkey data center industry.

Earthquake-Zone Engineering and Insurance Premiums

Istanbul’s probabilistic hazard model pegs a 7.33-magnitude scenario as plausible within the next decade, forcing financiers to add higher debt-service-coverage cushions and insurers to lift deductibles on Tier III buildings.[3]Business Standard, “Istanbul Worries Next Earthquake Will Be a Big One,” business-standard.com Tier IV concrete-core designs incorporating base isolators inflate capex by 15-25% compared with green-field Tier III shells. Some corporate tenants are now stipulating off-fault-line locations such as İzmir or Tekirdağ for primary deployments, eroding İstanbul’s automatic site-selection advantage. As insurance carriers tighten limits on critical-infrastructure coverage within the seismic red zone, projects that proceed must lock in longer gestation periods and higher contingency budgets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data-Center Size: Hyperscale Momentum Reshapes Capacity Mix

The Turkey data center market size for the Large category stood at 28 MW in 2024, accounting for 43.2% of the total installed load, underscoring corporate demand for cost-optimized colocation suites. The Turkey data center market share held by mega facilities is still modest, but their 17.5% CAGR to 2030 will shift the country toward a dual-campus model that prioritizes 10 MW blocs equipped with liquid-cooling manifolds.

Mega builds are typically situated on 10-hectare plots along the Marmara shoreline, allowing phased capacity additions while benefiting from proximity to the Eurasia Tunnel fiber ring. Hyperscale anchors increasingly pre-commit 70-80% of such sites, leaving limited white space for enterprise “cloud-adjacent” cages. Massive campuses exceeding 40 MW remain aspirational but have workable economic potential once the İzmir cable-station cluster is commissioned in 2027. Meanwhile, Small and Medium facilities show resilience by specializing in edge analytics workloads for retail, manufacturing, and telecom base-station aggregation nodes.

By Tier Standard: Resilience Becomes a Market Differentiator

Tier III retained a 57% share of Turkey data center market size in 2024, but its growth is plateauing as regulated industries push toward Tier IV redundancies. Tier IV’s 18.2% CAGR implies that, by 2030, at least one-third of new white space will incorporate concurrently maintainable power paths, autonomous fire-suppression segments and structural base-isolation.

Earthquake-resistant criteria drive this premiumization. Financial institutions are mandated to host hot-standby cores in buildings that commit to 99.995% availability, a threshold only Tier IV meets. The 2025 Cybersecurity Law further obliges operators of essential services to maintain real-time replication across separate grid feeds sourced from distinct substations, another hallmark of Tier IV topologies. Tier I and Tier II footprints persist for edge use cases where cost trumps uptime, but their aggregated load share is sliding as hyperscale footprints dominate procurement pipelines.

By Absorption: Utilization Signals Balanced Supply–Demand

Utilized capacity reached 71% of available power in 2024, encompassing 47 MW of live equipment across 36 commercial facilities. That percentage is slated to climb as high as 79% by 2030 because existing campuses reserve expansion bays that fill rapidly once fiber cross-connects go live. Non-utilized capacity remains indispensable as it grants hyperscalers the runway to plug modules inside pre-built shell-and-core blocks.

Within the utilized bucket, wholesale leases represent over half of the incremental take-up, as cloud providers typically request contiguous 1 MW suites. Retail colocation still commands price premiums due to cross-carrier meet-me rooms inside İstanbul’s carrier hotels. Sectorally, BFSI clients backhaul encrypted traffic to Ankara for regulatory reasons, while media and gaming companies push cache appliances toward İzmir to exploit submarine exit points. This segmentation balance offers a stabilizing influence on the Turkey data center market, insulating facility operators from cyclical shocks within any single vertical.

By Hotspot: Geographical Diversification Gains Traction

İstanbul contributed 78% of aggregate MVA transformer capacity in 2024, essentially cementing its role as the nation’s interconnection metropolis. Yet power-grid congestion in the European-side districts and earthquake premiums are catalyzing a structural shift toward İzmir. The Turkey data center market size tied to İzmir is anticipated to increase from 5 MW in 2024 to 17 MW by 2030, driven by the commissioning of Vodafone-DAMAC’s 6 MW modular campus in 2025.

EXA Infrastructure’s 1,850 km terrestrial fiber route overlays İzmir with 400G backhaul into Sofia and Athens, enhancing route diversity. Secondary cities, such as Ankara, Bursa, and Gaziantep, collectively host less than 10 MW today, but are conducting feasibility studies aimed at placing micro-data centers close to industrial clusters. Their cost advantages, lower land prices, and cooler ambient temperatures could translate into 40–60 basis-point OPEX savings per delivered kW. Over the long term, the Turkish data center market is expected to evolve from a single-city cluster to a hub-and-spoke topology, paralleling the country’s ongoing motorway and high-speed rail expansion.

Geography Analysis

İstanbul’s dominance is rooted in its triple-landing submarine-cable hotspots (Yeniköy, Tuzla and Pendik) that supply direct optic reach into Marseille, Bari and Alexandria. The city’s dense banking and OTT clusters fuel 15 kW-per-rack average densities inside the legacy carrier hotels of Ümraniye and Esenyurt. Municipal planning now allocates new industrial-zoned plots along the Anatolian shoreline with double 154 kV grid feeds to accommodate growth, although seismic retrofits remain a high-cost prerequisite.

İzmir’s 16.9% CAGR is anchored by its lower seismic risk profile, 5–10% lower land costs and adjacency to the BlueMed, Medusa and Arianna cable systems due to be active by 2027. The city’s port logistics simplify inbound shipment of containerized prefabricated modules, shaving weeks off staging schedules. Tax authorities have additionally approved accelerated depreciation for energy-saving chillers deployed within İzmir’s designated free-zone parcels, dropping effective corporate-tax rates by up to 6 percentage points for qualifying builds.

Rest-of-Turkey nodes are spreading along new fiber rights-of-way mapped onto state motorway projects. Ankara commands regulatory data hosting for ministries and defense contractors, while Kocaeli’s petrochemical belt is moving IoT telemetry storage onshore to comply with KVKK. Bursa’s automotive OEMs need low-latency digital-twin platforms, which encourages containerized data centers situated inside industrial-organized zones. Cumulatively, these provincial deployments could lift non-İstanbul load share from 22% to near 35% by 2030, affording the national grid additional resilience and dispersing macro-economic benefits.

Competitive Landscape

The Turkey data center market currently comprises approximately 20 commercial facilities, totaling 66 MW of installed IT load. No single operator exceeds a 30% revenue share, leaving room for new entrants yet signaling early-stage consolidation potential. Foreign investors, such as Equinix, Telehouse, and Khazna, import global design and operational expertise, thereby raising customer expectations for carrier neutrality and SLA transparency. Domestic telcos Turkcell, Türk Telekom, and Vodafone Türkiye counterbalance foreign peers through nationwide fiber control and last-mile access across 32 million homes.

Strategic playbooks are increasingly centered on energy efficiency and resilience. Radore, Teknotel, and Comnet have installed adiabatic cooling, reducing the site PUE to 1.15 during the winter months. Meanwhile, Turkcell and Türk Telekom are trialing lithium-ion UPS banks paired with rooftop solar arrays to offset grid-tariff shocks. On the services front, KoçSistem and Medianova bundle SOC-as-a-service with colocation cages to satisfy compliance with Law No. 7545, whereas Hosthink and Netdirekt differentiate themselves through bare-metal automation aimed at DevOps teams.

At least three midsized facilities (2–4 MW each) are known to be canvassing advisers for buy-side approaches, and private-equity funds view the Turkey data center market as under-priced relative to Western European benchmarks. Cross-border alliances for example the July 2025 Sparkle-Turkcell cable MoU are incorporating capacity swaps that guarantee anchor tenancy commitments for upcoming campuses. Competition is therefore migrating beyond rack price toward ecosystem breadth, latency proximity and sovereign-cloud attestation.

Turkey Data Center Industry Leaders

Türk Telekom

Vodafone Türkiye

Equinix İstanbul

Telehouse İstanbul (İsnet)

Radore Data Center

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Sparkle and Turkcell signed an MoU for a new submarine cable linking Turkey and Europe, delivering 25 Tbps of capacity and integrating into the BlueMed network.

- June 2025: Equinix acquired an Istanbul data center from Zenium for USD 93 million, with expansion potential to 22 MW.

- April 2025: G42’s Khazna Data Centers announced Turkish expansion to back national AI ambitions.

- March 2025: ULAK and TURKSAT inked a 5G private-network contract, reinforcing mobile backhaul for edge clouds.

- February 2024: Vodafone and DAMAC committed USD 100 million to a 6 MW İzmir campus coming online Q1 2025.

Turkey Data Center Market Report Scope

Turkey Data Center Market is Segmented by Data-Center Size (Small, Medium, Large, Mega, Massive), Tier Standard (Tier I and II, Tier III, Tier IV), Absorption (Non-Utilized, Utilized (Colocation Type (Hyperscale, Retail, Wholesale), End-User (BFSI, Cloud Service Providers, E-Commerce, Government, Manufacturing, Media and Entertainment, Telecom, and Other End-Users)), and Hotspot(Istanbul, Izmir, Rest of Turkey). The Market Forecasts are Provided in Terms of Volume (MW).

| Small |

| Medium |

| Large |

| Mega |

| Massive |

| Tier I and II |

| Tier III |

| Tier IV |

| Non-Utilized | ||

| Utilized | By Colocation Type | Hyperscale |

| Retail | ||

| Wholesale | ||

| By End-User | BFSI | |

| Cloud Service Providers | ||

| E-Commerce | ||

| Government | ||

| Manufacturing | ||

| Media and Entertainment | ||

| Telecom | ||

| Other End-Users | ||

| Istanbul |

| izmir |

| Rest of Turkey |

| By Data-Center Size | Small | ||

| Medium | |||

| Large | |||

| Mega | |||

| Massive | |||

| By Tier Standard | Tier I and II | ||

| Tier III | |||

| Tier IV | |||

| By Absorption | Non-Utilized | ||

| Utilized | By Colocation Type | Hyperscale | |

| Retail | |||

| Wholesale | |||

| By End-User | BFSI | ||

| Cloud Service Providers | |||

| E-Commerce | |||

| Government | |||

| Manufacturing | |||

| Media and Entertainment | |||

| Telecom | |||

| Other End-Users | |||

| By Hotspot | Istanbul | ||

| izmir | |||

| Rest of Turkey | |||

Key Questions Answered in the Report

What is the forecasted installed IT load in Turkey by 2030?

The Turkey data center market is projected to reach 140 MW of installed IT load by 2030, up from 66 MW in 2025.

Which Turkish city is expected to grow fastest as a data-center hotspot?

İzmir is forecast to expand at a 16.9% CAGR through 2030, benefiting from submarine-cable proximity and lower seismic risk.

How will KVKK localization rules influence facility demand?

KVKK mandates domestic processing for key data classes, compelling multinational and local firms to lease compliant Turkish colocation space, thus lifting long-term demand.

What segment shows the highest future CAGR?

Mega-facility builds are expected to grow at 17.5% CAGR, driven by hyperscale cloud deployments and AI workloads.

How are operators managing energy-price volatility?

Many are signing renewable PPAs, investing in high-efficiency cooling and deploying lithium-ion UPS systems to cut OPEX and hedge tariff risk.

What is the impact of earthquake risk on site selection?

Elevated insurance premiums and structural-engineering costs are redirecting some new capacity to lower-risk regions like İzmir and Ankara, while İstanbul campuses add Tier IV seismic resilience.

Page last updated on: