Triptorelin Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.91 Billion |

| Market Size (2031) | USD 2.47 Billion |

| Growth Rate (2026 - 2031) | 5.25% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

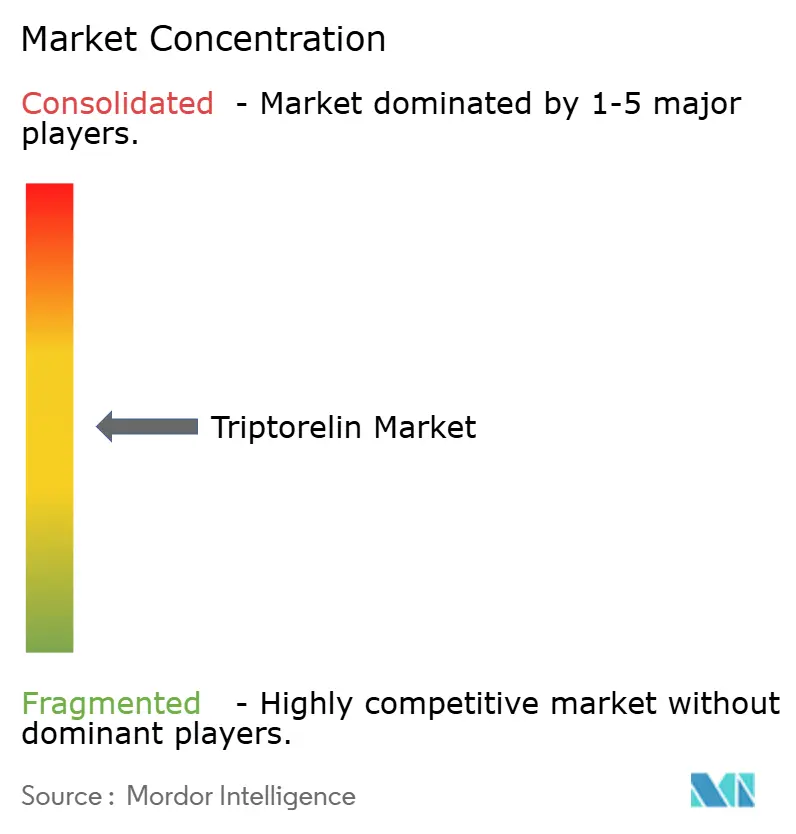

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Triptorelin Market Analysis by Mordor Intelligence

The Triptorelin Market size is projected to be USD 1.83 billion in 2025, USD 1.91 billion in 2026, and reach USD 2.47 billion by 2031, growing at a CAGR of 5.25% from 2026 to 2031.

The triptorelin market serves several treatment pathways at the same time, including prostate cancer, endometriosis, central precocious puberty, fertility preservation, and selected endocrine care settings, which gives demand a broader base than many other specialty injectable products[1]American Urological Association, “Advanced Prostate Cancer: AUA/SUO Guideline (2026),” American Urological Association, auanet.org. The triptorelin market also benefits from long-acting depot formats because fewer injections can improve treatment continuity and make the product more practical for hospital-based care and long-duration therapy. Demand in the triptorelin market remains closely tied to the burden of hormone-sensitive disease, especially prostate cancer in aging populations and endometriosis in women of reproductive age, while pediatric use in central precocious puberty is adding a second layer of growth. The main structural pressure on the triptorelin market comes from oral GnRH antagonists in prostate cancer, especially where cardiovascular risk is a major prescribing concern, but the molecule still holds a durable role because it has established use across multiple clinical settings rather than a single demand pool.

Key Report Takeaways

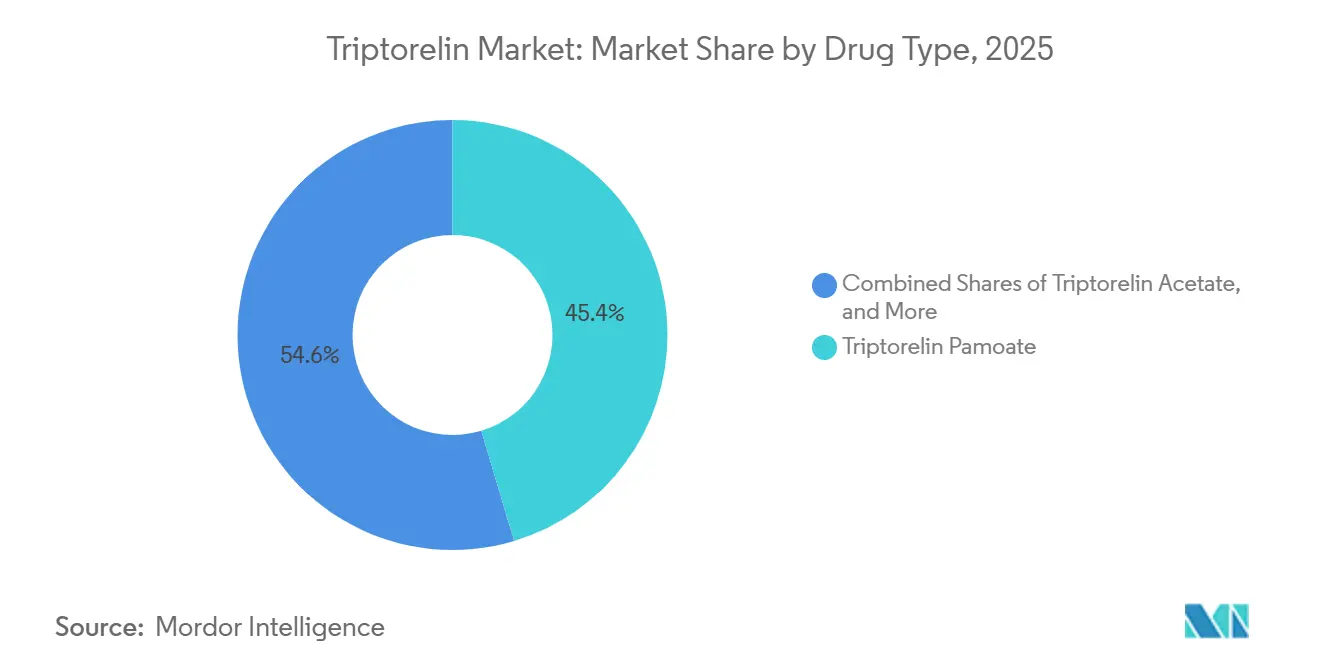

- By drug type, triptorelin pamoate held 45.35% of the triptorelin market share in 2025, while triptorelin embonate is expected to record the highest CAGR at 6.34% through 2031.

- By route of administration, intramuscular delivery accounted for 82.23% of revenue in 2025, while subcutaneous delivery is forecast to grow fastest at a 5.68% CAGR through 2031.

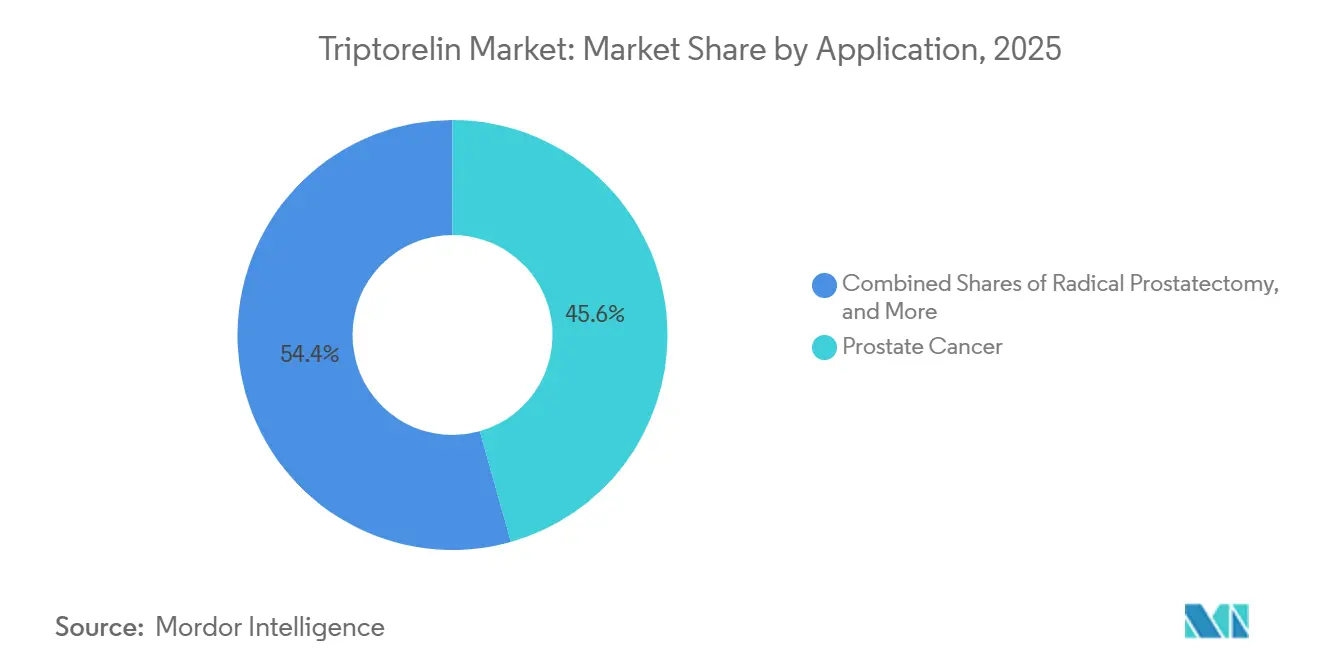

- By application, prostate cancer held 45.62% share of the triptorelin market size in 2025, while endometriosis is projected to expand at a 6.23% CAGR through 2031.

- By distribution channel, hospital pharmacies accounted for 55.47% of revenue in 2025, while online pharmacies are expected to advance at a 6.55% CAGR through 2031.

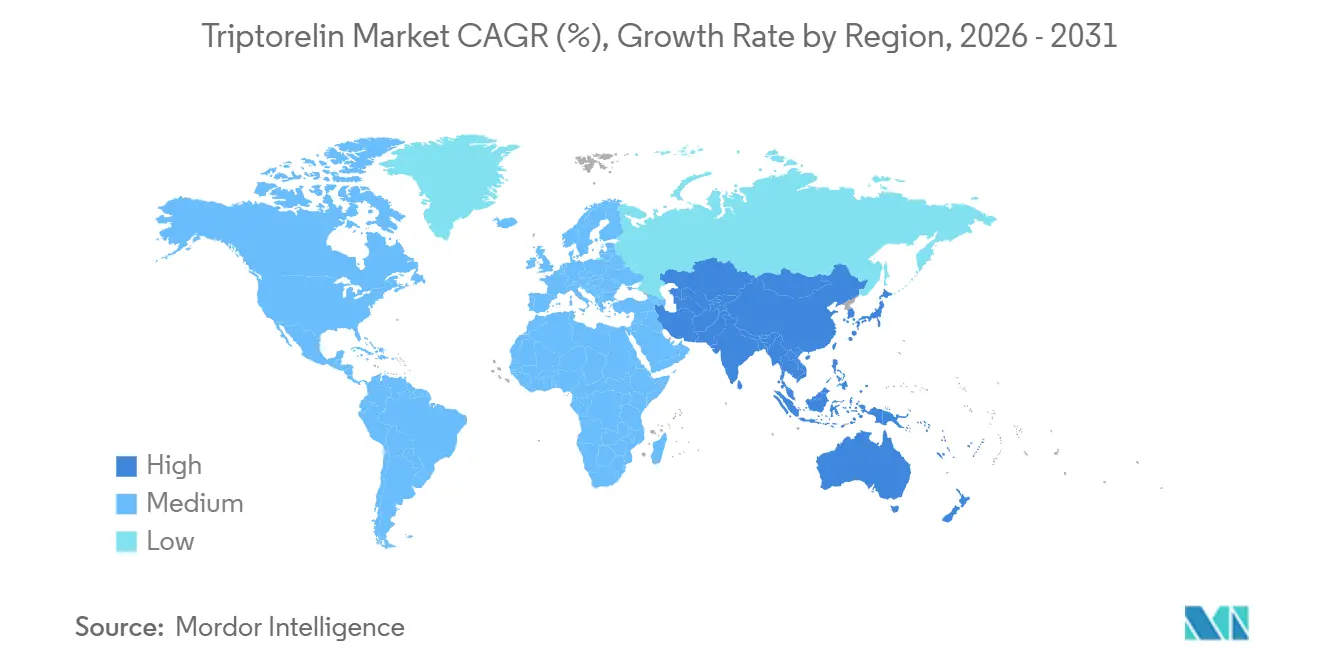

- By geography, North America held 40.36% of global revenue in 2025, while Asia-Pacific is set to grow fastest at a 6.39% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Triptorelin Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Burden of Prostate Cancer and Endometriosis | +1.2% | Global, demand concentrated in North America, Europe, and East Asia | Long term (≥ 4 years) |

| Growing Use in Central Precocious Puberty Management | +0.8% | Asia-Pacific core, North America, and Europe | Medium term (2-4 years) |

| Shift Toward Long-Acting Depot Formulations | +0.7% | Global, with early institutional gains in Western Europe and Japan | Medium term (2-4 years) |

| Expansion of Fertility and Gender-Affirming Use Cases | +0.5% | North America and Europe | Short term (≤ 2 years) |

| Emerging Clinical Trial Activity in New Indications | +0.4% | Global, with early gains in China and Europe | Long term (≥ 4 years) |

| Hospital Procurement Preference for High-Compliance Injectable Therapies | +0.6% | North America, Europe, and Asia-Pacific core | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Burden Of Prostate Cancer And Endometriosis

Global prostate cancer incidence reached 1.32 million cases in 2021, and the same body of disease burden work projects cases to reach 2.4 million by 2040, which keeps a large and growing treatment base in view for the triptorelin market. The United States alone is expected to record 333,830 new prostate cancer diagnoses and 36,320 deaths in 2026, and current treatment guidance continues to support LHRH agonists as first-line castration options in metastatic hormone-sensitive disease. Endometriosis adds a second major demand pool because the World Health Organization[2]World Health Organization, “Endometriosis,” World Health Organization, who.int estimates that 190 million women of reproductive age are affected globally, and a 2026 review confirmed GnRH agonists as one of the strongest hormonal options for pain control across a long span of randomized evidence. The triptorelin market therefore, carries durable demand because both diseases have large active patient populations, and the endometriosis treatment pool still appears underpenetrated due to persistent diagnostic delay.

Growing Use In Central Precocious Puberty Management

A Phase 3 study published in October 2024 across 12 Chinese sites showed 100% luteinizing hormone suppression at month 6 after a single 22.5 mg triptorelin pamoate depot dose in children with central precocious puberty[3]Zhe Sun et al., “A Phase 3, Open-Label, Single-Arm Trial of the Efficacy and Safety of Triptorelin 6-Month Formulation in Chinese Children with Central Precocious Puberty,” Advances in Therapy, domain springer.com. The same study also reported pubertal regression or stabilization in 98.5% of participants and no grade 3 or higher adverse events, which gives the triptorelin market a strong pediatric efficacy and safety reference in a large future demand center. A second development came in April 2026 when population pharmacokinetics work for GenSci006 advanced the pediatric extrapolation framework for triptorelin acetate microspheres, which matters for new formulation approvals in the Asia-Pacific. These findings support a broader move from short-interval pediatric use toward longer-interval options, which can improve continuity during treatment courses that often last several years.

Shift Toward Long-Acting Depot Formulations

A 2025 real-world study in advanced prostate cancer showed that 98.3% of patients receiving 6-month long-acting triptorelin achieved testosterone suppression below 1.7 nmol/L, which supports confidence in extended interval disease control. The same study found that 92% stayed on the formulation through 12 months, while 85.2% of patients who switched from shorter intervals named reduced injection frequency as the main reason, showing that convenience now carries direct commercial weight in the triptorelin market. In Switzerland, Debiopharm[4]Debiopharm, “Debiopharm's Pamorelin Receives Swiss Approval for Subcutaneous Administration, Enhancing Treatment Flexibility for Prostate Cancer Patients,” Debiopharm, debiopharm.com received approval for subcutaneous administration of Pamorelin LA 3.75 mg and 11.25 mg in 2025, and the company stated that testosterone suppression remained equivalent while pain and hematoma risk were lower for relevant patients.

Expansion Of Fertility And Gender-Affirming Use Cases

An ASRM committee opinion issued in 2026 recognized triptorelin-based ovarian suppression as a validated fertility preservation option during cytotoxic chemotherapy for hormone-sensitive breast cancer. This matters for the triptorelin market because it formalizes a use case that links oncology and reproductive medicine and broadens the clinical base beyond prostate cancer and gynecologic pain treatment. Data presented in 2025 on triptorelin with estradiol therapy in transgender girls showed progressive inhibin B suppression over 2.5 years, which supports ongoing use as a puberty blocker in gender affirming care. A 2025 review in Nature Reviews Endocrinology also confirmed that GnRH analogs, including triptorelin, remain central to gender affirming hormone therapy initiation protocols in youth globally.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Peptide Synthesis and Sterile Injectable Manufacturing | -0.7% | Global, felt most strongly in emerging markets | Long term (≥ 4 years) |

| Regulatory and Label Expansion Complexity Across Major Markets | -0.5% | North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Formulation Switching Risk From Generic and Regional Competition | -0.6% | North America and Europe | Medium term (2-4 years) |

| Adherence Friction From Injection-Based Administration and Cold-Chain Handling | -0.4% | Global, with higher relevance in Asia-Pacific, Middle East, and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost Of Peptide Synthesis And Sterile Injectable Manufacturing

Triptorelin is a decapeptide analog, and its production depends on expensive protected amino acids, high-grade purification, sterile fill finish capacity, and cold chain handling, which keeps costs elevated across the triptorelin market. These requirements create entry barriers for smaller players, but they also limit margin expansion for companies trying to compete with lower-priced generic or regional products in a technically demanding injectable category. Supply chain fragility is also visible because NHS Scotland issued a medicine supply alert in March 2025 for Gonapeptyl Depot 3.75 mg, with disruption continuing through January 2026. A supply issue in one sterile depot product can affect several therapeutic areas at once because the same molecule serves prostate cancer, endometriosis, and central precocious puberty. The triptorelin market, therefore faces a basic cost restraint that is not only about manufacturing expense, but also about maintaining a reliable supply across multiple clinical uses at the same time.

Regulatory And Label Expansion Complexity Across Major Markets

Regulatory expansion remains difficult because authorities do not always accept foreign efficacy data as sufficient for local label growth. In India, the Central Drug Standard Control Organization required Dr. Reddy's Laboratories to run a dedicated Phase III study for the endometriosis indication in triptorelin 3.75 mg, which delayed expansion for a large generic participant in a high-growth therapy area. The same regulator also required Indian population-specific data before pediatric expansion for triptorelin 22.5 mg, which adds time and cost to the approval path for new indications in the triptorelin market. Divergent requirements across the FDA, EMA, NMPA, and CDSCO make multi-region launches harder because each extended interval or new salt form can face a different data expectation. This slows commercialization and favors companies with stronger regulatory resources, which means the triptorelin market does not reward formulation development on speed alone.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Type: Embonate Formulations Gain Regulatory Momentum

Triptorelin pamoate held 45.35% share in 2025, while triptorelin embonate is projected to grow at a 6.34% CAGR through 2031, which sets the current shape of competition across salt forms in the triptorelin market. Pamoate remains the largest format because it already has broad clinical familiarity and support across branded product lines used in prostate cancer, central precocious puberty, and other hormone suppression settings. That installed base matters because prescribers and procurement teams often stay with a depot format once it is established in hospital protocols. Embonate has gained fresh attention after the 2025 Swiss approval for subcutaneous Pamorelin LA and the completed European decentralized procedure for the 6 month Decapeptyl embonate formulation in advanced or metastatic prostate cancer.

By Route of Administration: IM Dominance Persists As SC Route Builds Institutional Footing

Intramuscular administration accounted for 82.23% of revenue in 2025, which shows how firmly the triptorelin market still rests on established depot injection practice in oncology and endocrine care. The intramuscular route built this lead over many years because deeper depot delivery supports formulation volume and predictable release in an elderly prostate cancer population that is commonly treated in specialist settings. Subcutaneous delivery is the fastest-growing route, and the triptorelin market size for this route is projected to advance at 5.68% CAGR through 2031. Swiss approval for subcutaneous Pamorelin LA in 2025 gave this route a major institutional reference point because Debiopharm reported equivalent testosterone suppression with lower pain and reduced hematoma risk.

By Application: Prostate Cancer Anchors Revenue While Endometriosis Delivers Stronger Growth

Prostate cancer accounted for 45.62% share of the triptorelin market size in 2025, which made it the largest application by a wide margin. The segment stays dominant because androgen deprivation remains a core treatment pillar, and the 2026 AUA and SUO guideline still supports LHRH agonists as standard castration options in metastatic hormone sensitive disease. Disease burden also supports this position because global incidence is still rising and long range projections point to 2.4 million prostate cancer cases by 2040. Endometriosis is the fastest growing application at a 6.23% CAGR through 2031, supported by a very large untreated or late treated population and strong evidence for GnRH agonist pain control. The coexistence of a large oncology base and a growing gynecology base gives the triptorelin market better demand balance than a single use product would have.

By Distribution Channel: Hospital Pharmacies Remain The Core Supply Point

Hospital pharmacies accounted for 55.47% of revenue in 2025, which reflects how strongly the triptorelin market is tied to controlled cold chain handling, specialist reconstitution, and supervised injectable administration. This channel remains dominant because oncology and pediatric endocrine treatment often starts within hospital-linked systems where drug handling standards and documentation are already in place. Institutional procurement also favors suppliers with a consistent supply record because a disruption in one triptorelin depot can affect several patient groups at once. The hospital channel, therefore, captures value not only through dispensing volume but also through formulary trust and workflow familiarity. Online pharmacies are the fastest-growing channel at a 6.55% CAGR through 2031, which shows that the triptorelin market is beginning to absorb more digitally coordinated specialty distribution.

Geography Analysis

North America held 40.36% of global revenue in 2025, which made it the largest regional contributor in the triptorelin market. The region stays ahead because the United States continues to carry a high prostate cancer burden, with 333,830 new diagnoses expected in 2026 under current guideline references. The triptorelin market in North America also benefits from established reimbursement structures and specialist oncology networks that can absorb long-acting depot therapy on a routine basis. The United States remains the main branded base through products such as Trelstar and Triptodur, while the mature prescribing environment also makes it one of the most active settings for generic substitution pressure. Europe remains a clinically important region because it houses entrenched branded depot use and a highly regulated approval and procurement environment.

Asia-Pacific is the fastest-growing geography, and the triptorelin market size in the region is projected to rise at 6.39% CAGR through 2031. China stands out because the 2024 Phase 3 central precocious puberty study supported 100% luteinizing hormone suppression with the 6-month pamoate formulation in Chinese children, which strengthens the case for broader pediatric use. Japan, India, Australia, and South Korea also contribute to the regional growth profile because specialist endocrine and oncology treatment capacity is expanding across several of the largest healthcare systems. The triptorelin market therefore has its strongest forward regional momentum in Asia-Pacific, where pediatric and oncology drivers are working together rather than independently.

Competitive Landscape

The triptorelin market shows moderate consolidation rather than a tightly closed structure. Ipsen and Debiopharm remain central to the branded side of the category, while Ferring, Verity, and Azurity also hold visible positions through established depot products and prescribing franchises. At the same time, the presence of generic manufacturers in established markets prevents the competitive field from becoming highly concentrated. This matters because the triptorelin market is not shaped by discovery science alone, but by formulation performance, supply reliability, and the ability to stay embedded in hospital treatment pathways. Companies that can preserve all 3 of those strengths are in the best position to defend their share even when price competition rises.

Long-term pressure still exists because oral GnRH antagonists are becoming more relevant in prostate cancer. Real-world cardiovascular findings presented at ASCO GU 2026 showed numerically lower major adverse cardiac event rates with antagonists in men receiving androgen deprivation therapy, which could influence prescribing for higher-risk patients.

Triptorelin Industry Leaders

Ipsen S.A.

Debiopharm Group

Ferring Pharmaceuticals

Arbor Pharmaceuticals, LLC

Teva Pharmaceutical Industries Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: GeneScience Pharmaceuticals Co., Ltd. (GenSci)’s population pharmacokinetics study for GenSci006, a 3.75 mg triptorelin acetate microsphere formulation targeting CPP treatment, was published in Clinical Pharmacokinetics, advancing the pediatric extrapolation methodology for new triptorelin formulations seeking regulatory approval in Asia-Pacific markets.

- September 2025: Debiopharm announced that Swissmedic approved the subcutaneous administration of Pamorelin LA 3.75 mg and 11.25 mg (triptorelin embonate) for prostate cancer in Switzerland, the first regulatory authorization of the SC route for these formulations.

Global Triptorelin Market Report Scope

As per the scope of the market, triptorelin is a gonadotropin-releasing hormone (GnRH) agonist used to regulate hormone production in the body. It is widely prescribed for the treatment of hormone-dependent conditions such as prostate cancer, endometriosis, uterine fibroids, central precocious puberty, and in assisted reproductive technologies. Triptorelin is administered under medical supervision through intramuscular (IM) or subcutaneous (SC) injection, depending on the formulation and therapeutic indication.

The Triptorelin Market Report segments the market by drug type, including Triptorelin Pamoate, Triptorelin Acetate, and Triptorelin Embonate. Based on route of administration, the market is categorized into Intramuscular (IM) and Subcutaneous (SC) formulations. By application, the market covers Prostate Cancer, Radical Prostatectomy, Endometriosis, Salivary Gland Cancer, Central Precocious Puberty, Uterine Fibroids, Fertility Suppression and Assisted Reproduction Protocols, and Others (including Hormone-Sensitive Breast Cancer and additional hormone-dependent disorders). Furthermore, the market is segmented by distribution channel into Hospital Pharmacies, Retail Pharmacies, Online Pharmacies, and Others, including Specialty Pharmacies and Government Procurement Channels. Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Triptorelin Pamoate |

| Triptorelin Acetate |

| Triptorelin Embonate |

| Intramuscular (IM) |

| Subcutaneous (SC) |

| Prostate Cancer |

| Radical Prostatectomy |

| Endometriosis |

| Salivary Gland Cancer |

| Central Precocious Puberty |

| Uterine Fibroids |

| Fertility Suppression and Assisted Reproduction Protocols |

| Others (Salivary Gland Cancer, Hormone-Sensitive Breast Cancer) |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| Others (Specialty Pharmacies, Government Procurement Channels) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Type | Triptorelin Pamoate | |

| Triptorelin Acetate | ||

| Triptorelin Embonate | ||

| By Route of Administration | Intramuscular (IM) | |

| Subcutaneous (SC) | ||

| By Application | Prostate Cancer | |

| Radical Prostatectomy | ||

| Endometriosis | ||

| Salivary Gland Cancer | ||

| Central Precocious Puberty | ||

| Uterine Fibroids | ||

| Fertility Suppression and Assisted Reproduction Protocols | ||

| Others (Salivary Gland Cancer, Hormone-Sensitive Breast Cancer) | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| Others (Specialty Pharmacies, Government Procurement Channels) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2031 outlook for triptorelin?

The triptorelin market is projected to reach USD 2.47 billion by 2031 from USD 1.91 billion in 2026, expanding at a 5.25% CAGR over 2026-2031.

Which therapeutic area contributes the most revenue to triptorelin sales?

Prostate cancer remains the largest application, with 45.62% of revenue in 2025, supported by continued reliance on androgen deprivation therapy in clinical guidelines.

What is driving faster growth in endometriosis use?

Endometriosis is expected to grow at a 6.23% CAGR through 2031 because the diagnosed and treated population still trails the full affected population, and GnRH agonists remain well supported for pain control.

Why are long acting triptorelin formulations gaining attention?

Real world data showed strong testosterone suppression and high persistence with 6 month treatment, while fewer injections improve convenience for patients and providers.

Which region offers the strongest growth potential for triptorelin through 2031?

Asia-Pacific is the fastest growing region with a 6.39% CAGR through 2031, supported by rising prostate cancer incidence and stronger pediatric opportunity in central precocious puberty.

How concentrated is competition among triptorelin suppliers?

Competition is moderate because branded leaders remain important, but generics and multiple regional suppliers prevent the category from becoming tightly controlled by a small group.

Page last updated on: