Triclabendazole Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

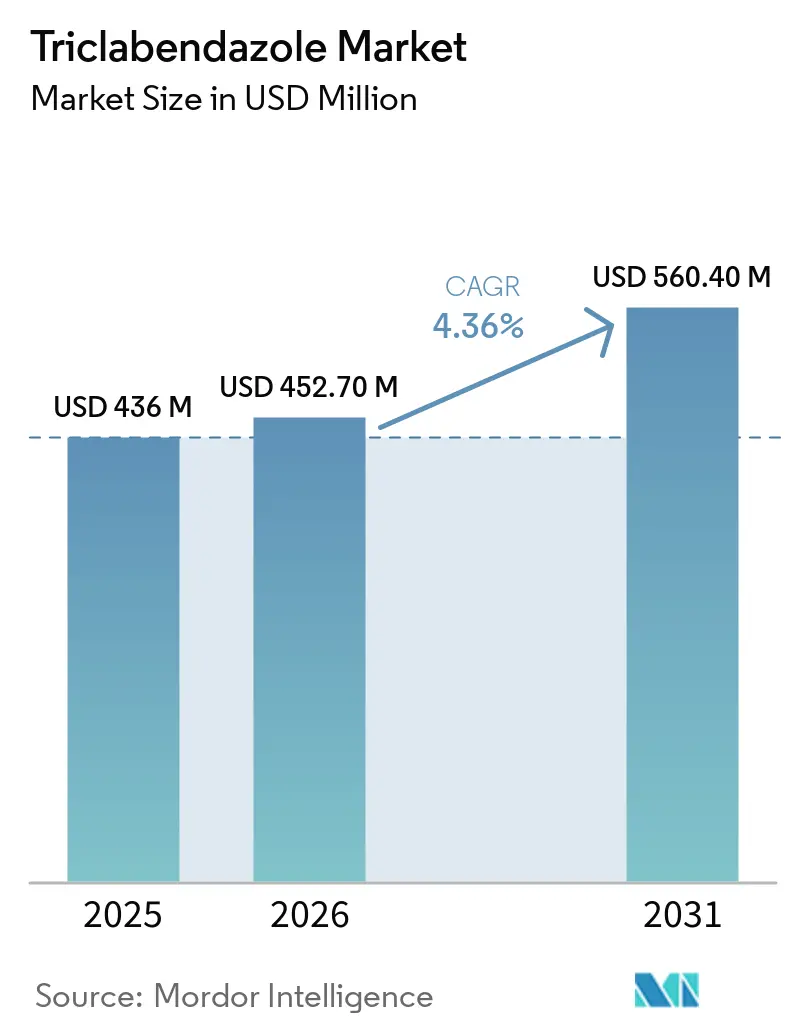

| Market Size (2026) | USD 452.70 Million |

| Market Size (2031) | USD 560.40 Million |

| Growth Rate (2026 - 2031) | 4.36% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Triclabendazole Market Analysis by Mordor Intelligence

The Triclabendazole Market size is projected to be USD 436 million in 2025, USD 452.70 million in 2026, and reach USD 560.40 million by 2031, growing at a CAGR of 4.36% from 2026 to 2031.

The growth outlook reflects climate shifts that expand fluke transmission zones, the spread of resistance that forces protocol redesign, and targeted diagnostics that alter dosing frequency in managed herds. Competitive moves cluster around combination products, diagnostics bundling, and regional scale-up by cost-competitive API suppliers, shaping both price and access dynamics in the triclabendazole market. Distribution remains concentrated in veterinary hospitals that integrate coproantigen ELISA and fecal egg count services into prescription workflows. At the same time, pharmacies gain share in deregulating markets where over-the-counter access expands the triclabendazole market. Regional performance diverges as North America holds the largest base, while Asia Pacific sets the fastest trajectory due to climate-amplified risk and intensifying ruminant production.

Key Report Takeaways

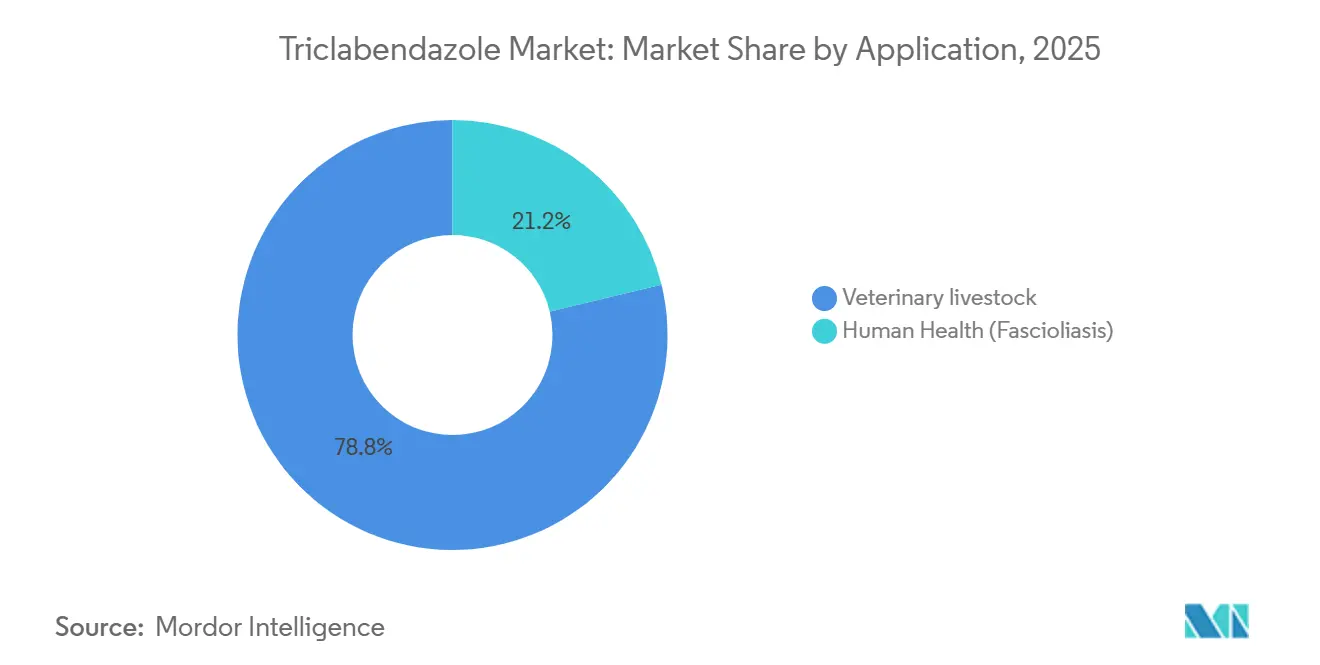

By application, veterinary livestock led with 78.77% revenue share in 2025. Veterinary livestock is forecast to expand at a 5.34% CAGR through 2031.

By product type, generics held 89.38% share in 2025. Generics are projected to grow at a 5.68% CAGR through 2031.

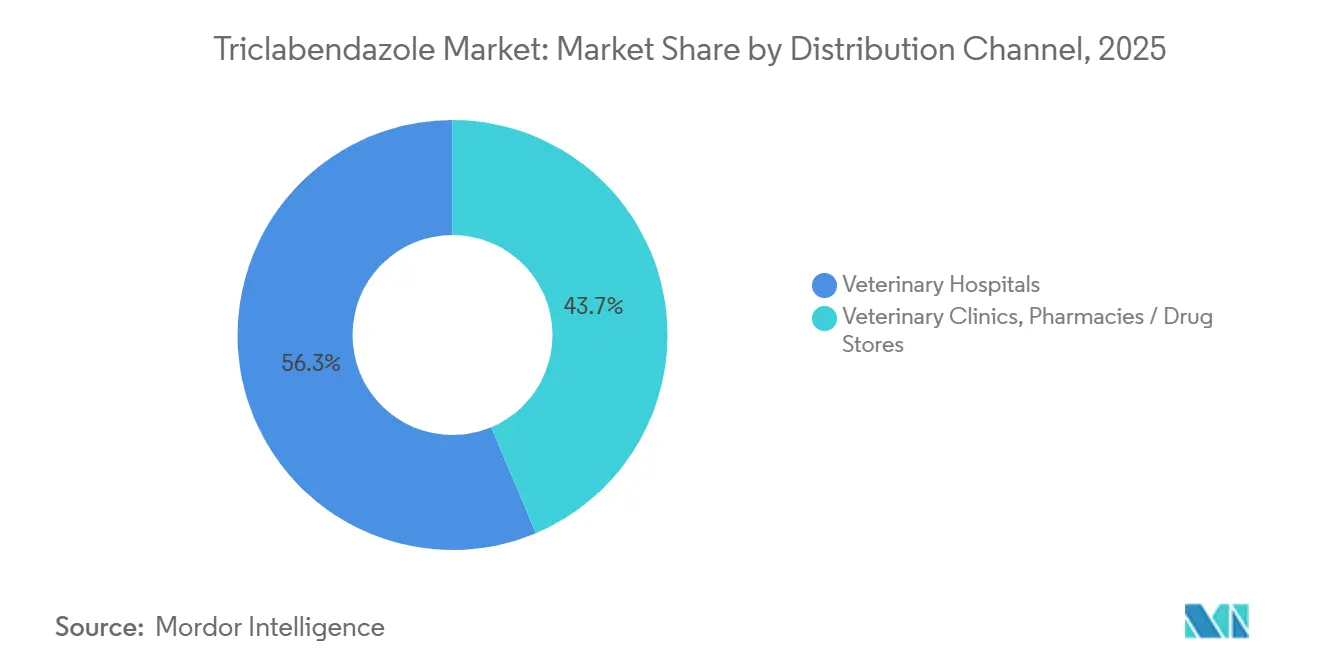

By distribution channel, veterinary hospitals held 56.34% share in 2025. Veterinary hospitals are expected to grow at a 4.87% CAGR through 2031.

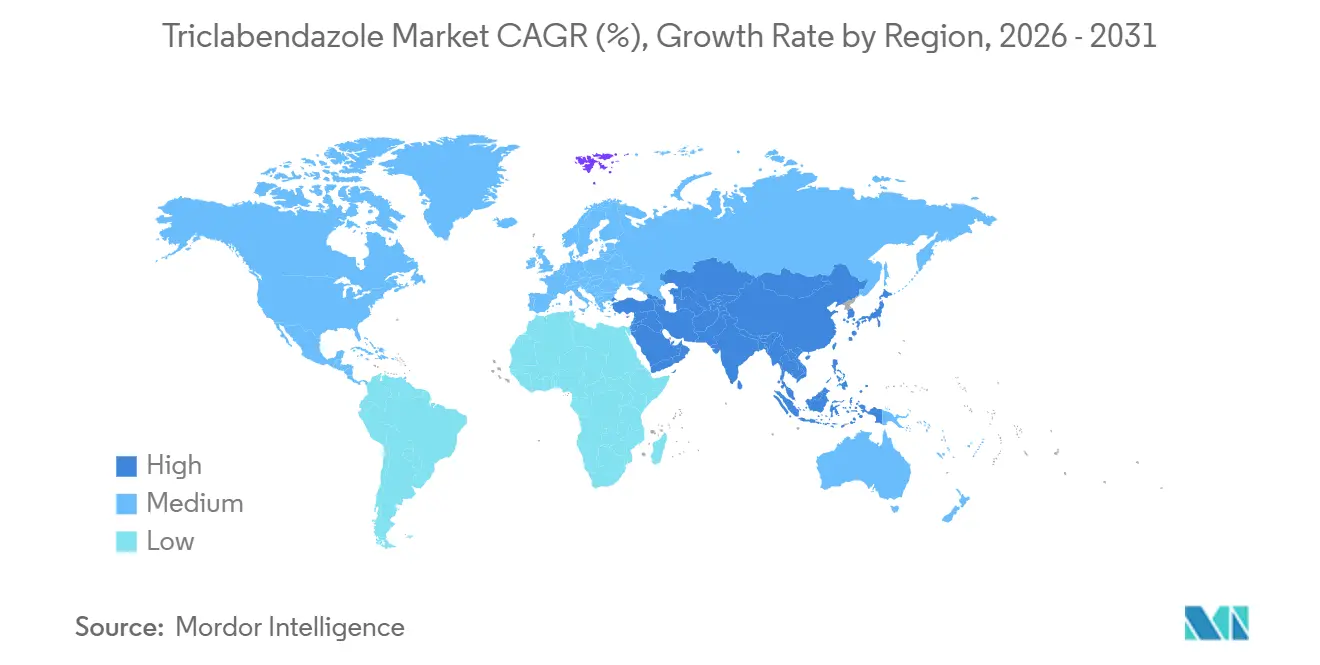

By geography, North America led with 41.34% share in 2025. Asia Pacific is projected to post the highest regional CAGR at 8.32% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Triclabendazole Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High fascioliasis burden, only flukicide across all stages | +1.2% | Global, temperate and subtropical livestock zones | Medium term (2-4 years) |

| WHO endorsement and FDA approval improve availability | +0.7% | North America, Europe, WHO-program regions | Short term (≤ 2 years) |

| Multi-stage efficacy sustains protocol standard | +0.9% | Global | Long term (≥ 4 years) |

| Climate change expands risk zones and seasonality | +1.3% | Asia Pacific, Europe northern extension, Middle East and Africa | Long term (≥ 4 years) |

| Adoption of fixed-dose combinations | +0.8% | Australia, New Zealand, Latin America, East Africa | Medium term (2-4 years) |

| Better diagnostics enable targeted treatment | +0.6% | North America, Europe, Australia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Multi-Stage Efficacy Anchors Triclabendazole as Protocol Standard Despite Resistance Emergence

Triclabendazole is the only widely used flukicide that targets both immature and adult Fasciola species in standard treatment protocols when migrating juveniles drive acute hepatic pathology. It is established that the United States labeling for human fascioliasis and pharmacological characterization reinforces this multi-stage efficacy profile, which underpins continued veterinary reliance despite documented resistance signals. Results published in Frontiers in Veterinary Science[1]Gedefaw, Tameru, Atsede Solomon Mebratu, Shimels Dagnachew, and Melkie Dagnaw Fenta. "Comparative analysis of anthelmintic treatments: impact on liver biomarkers and clinical recovery in sheep with fasciolosis." showed high efficacy along with corresponding biochemical recovery patterns, supporting durability in targeted use frameworks. Australian producer-led programs[2]"Optimising liver fluke management in cattle." Meat & Livestock Australia. Accessed April 28, 2026confirmed resistance across monitored dairy properties. Yet, producers maintained triclabendazole in seasonal strategies due to its unique immature fluke activity relative to alternatives, with reported gains in weaner growth when timing aligned to pre-winter juvenile peaks.

WHO Endorsement and FDA Validation Expand Commercial and Programmatic Access Channels

Egaten, the human triclabendazole product, is FDA approved for fascioliasis, which helped reduce ambiguity on safety and use in regulated settings and indirectly supported veterinary acceptance, where stewardship and pharmacovigilance data are valued. WHO-aligned donation programs for human fascioliasis cemented a global public health role that, in turn, lowered barriers for generics in veterinary markets as dossiers referenced safety and exposure insights from the human use experience. The downstream effect includes faster regulatory pathways in emerging markets where zoonotic disease control narratives influence ruminant drug policies, helping the triclabendazole market reach new prescriber bases through aligned public and private channels. In several jurisdictions across East Africa and Southeast Asia, validation from human programs catalyzed veterinary approvals and distribution infrastructure, improving product continuity and reducing stockouts that had hampered seasonal treatment planning. These access enablers complement evidence-based veterinary protocols and encourage formulary adoption that balances resistance stewardship with disease control goals.

Climate Change Extends Transmission Seasons and Expands Snail Habitats into Previously Marginal Zones

Warming patterns and altered rainfall are increasing environmental suitability for intermediate host snails and extending exposure windows, which raises infection risk and elevates the baseline need for flukicide intervention. Modeling across the Qinghai-Tibet Plateau[3]Luyao Xu et al., “Projected Distribution and Dispersal Patterns of Fasciola hepatica and Radix spp. in Qinghai-Tibet Plateau" projected higher-altitude suitability for Fasciola hepatica and its key snail vectors under plateau climate conditions, identifying about 85,800 km² as high-risk and 159,800 km² as medium-risk, which overlap with yak and sheep range lands and have triggered expanded surveillance programs. On-farm experience in the United Kingdom points to wetter summers and milder winters that compress traditional safe grazing periods and advance autumn dosing windows, changes that prompt rotational shifts and earlier diagnostic testing in the triclabendazole market. These climate amplitudes, coupled with waterlogged pasture in monsoonal and floodplain settings, translate to more herds and flocks entering intervention schedules and to more frequent annual treatments, strengthening the growth base of subregions.

Adoption of Fixed-Dose Combinations Enhances Compliance and Addresses Co-Infection Burdens

Field protocols increasingly use triclabendazole with macrocyclic lactones or levamisole to clear concurrent nematode burdens that can suppress recovery and performance if left untreated alongside liver fluke. Comparative trials in small ruminants documented that triclabendazole-levamisole regimens delivered near-total fecal egg count reductions with supportive clinical recovery patterns, outcomes that align with practitioner reports of improved herd-level responses when dual-pathogen coverage is required. Manufacturers in China commercialize oral suspensions with co-formulated strengths designed for weight-based dosing that field teams report as achieving high nematode reductions while retaining fluke clearance, a practical match for pastoral systems using single-visit handling to manage labor and stress. Combination formats can help distribute selection pressure across mechanisms, which is valued by veterinarians seeking to slow resistance emergence while maintaining efficacy against immature fluke stages in the triclabendazole market. Uptake is strongest where veterinary service fees are higher and where coproantigen testing is common, since single-dose convenience reduces animal handling and aligns with test-confirmed treatment episodes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Triclabendazole Resistance in Fasciola spp. | -0.90% | Australia, Ireland, United Kingdom; scattered global reports | Short term (≤2 years) |

| Milk and Meat Residue Withdrawals and Lactation Restrictions | -0.50% | Global dairy regions; highest in Europe and North America | Medium term (2–4 years) |

| Stewardship and Rotation Protocols Reducing Prophylactic Dosing Frequency | -0.40% | Developed veterinary markets (Europe, United Kingdom, Australia, New Zealand) | Medium term (2–5 years) |

| Human Market Monetization Constrained by Donation‑Based Supply | -0.30% | Endemic human fascioliasis regions (Latin America, Southeast Asia, Africa) | Long term (≥5 years) |

| Source: Mordor Intelligence | |||

Documented Triclabendazole Resistance Erodes First-Line Efficacy and Compels Protocol Adjustments

Resistance has been confirmed in multiple regions by 2026, shifting veterinary practice toward diagnostics-led dosing and more frequent rotation with alternate classes where immature efficacy tradeoffs are manageable. In Australia, structured producer programs recorded resistance across all monitored dairy farms in recent trials. However, the programs did not observe measurable production loss, a result that practitioners attribute to partial efficacy that still reduces acute disease risk relative to alternatives. Research in human fascioliasis indicated that host microbiome features were associated with treatment outcomes, showing that non-responders present distinct microbial signatures compared to responders, which complicates the attribution of all failures to parasite genetics alone. As per the data published by Farm Advisory Service[4]Farm Advisory Service, “Treatment and Control of Liver Fluke in Sheep and Cattle,” in October 2024, resistance risk is elevated, veterinarians emphasize test-and-treat, coproantigen monitoring, and scheduled rotations that preserve efficacy for high-burden windows in the triclabendazole market. Sponsors fund resistance genotyping and coproantigen testing partnerships, but stewardship programs raise costs for smaller generic suppliers, tightening the economics for low-price entrants in competitive channels.

Stringent Residue Withdrawal Periods Restrict Treatment Timing and Limit Dairy Market Penetration

Withdrawal requirements around meat and milk residues limit dosing windows in dairy and finishing operations and push treatment to dry periods that may not align with peak transmission risk. Jurisdictional labels often include explicit lactation restrictions for animals producing milk for human consumption, and they direct producers to defer dosing until dry-off, which can allow burdens to build through the season and complicate timing in years with extended pasture wetness. Meat withdrawal intervals deter finishing operations from mid-course dosing near marketing dates, steering managers toward alternatives with shorter withdrawals despite weaker control of immature stages. Analytical methods show persistent residues in fat and liver matrices at sensitive thresholds, which underpins conservative regulatory settings and associated national residue monitoring programs. Post-2000 residue harmonization has driven investment in validated HPLC and LC-MS/MS methods to monitor milk and tissue compliance, and those systems remain a baseline requirement where dairy export standards and veterinary controls are stringent. Stewardship frameworks that build test-and-treat protocols around coproantigen assays reduce unnecessary dosing and improve timing fit, but these same practices cap per-farm volume growth for flukicides in the triclabendazole market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Veterinary Livestock Maintains Dominance Through Climate-Extended Transmission Zones

Veterinary livestock accounted for 78.77% of the triclabendazole market share in 2025 and is projected to grow at a 5.34% CAGR through 2031, reflecting both climate-amplified exposure and stewardship-driven repeat interventions on confirmed cases. Demand concentrates in temperate and subtropical belts where poorly drained pastures, floodplains, and irrigated forage favor intermediate host snails that sustain transmission windows. North American cattle operations in wet bottomlands and Gulf Coast pastures maintain repeated seasonal treatments, while British Isles and northwest European herds respond to wetter summers and milder winters by compressing safe grazing intervals and advancing autumn treatments. Livestock segment durability rests on three reinforcing shifts in the triclabendazole market. Climate trends stretch exposure windows, which raises the number of herds entering seasonal treatment plans. Coproantigen ELISA and molecular diagnostics enable targeted interventions that substitute precision for blanket dosing, which improves clinical outcomes and drug stewardship at the cost of lower per-farm volumes. Together, these factors underpin the higher-than-market growth of the veterinary livestock segment in the triclabendazole market through 2031.

By Product Type: Generics Command Through API Cost Leadership and Mature Bioequivalence Pathways

Generics held 89.38% share in 2025, supported by vertically integrated manufacturers in India and China that scale API output and price finished doses below branded competitors while meeting bioequivalence standards. Integration across API synthesis, formulation, and regionally distributed fill-finish allows cost control and supply security that help generics capture a rising portion of procurement in cost-sensitive markets. Investments in regional production, including cleanroom capacity in East Africa, reinforce compliance credentials and shorten supply lines into veterinary channels[5]Norbrook, “Norbrook Opens New State-of-the-Art Cleanrooms at Nairobi Manufacturing Facility,”. Competitive positioning in the generics segment increasingly blends low price with solution selling in the triclabendazole industry. Several suppliers couple anthelmintics with veterinary service programs or diagnostics partnerships to move beyond a commodity profile and to fit stewardship standards that are more common in advanced dairy and beef regions. Portfolio breadth around fixed-dose combinations, supported by co-formulated macrocyclic lactones or levamisole, helps generics match practitioner preference for one-pass handling in large pastoral operations. Where formulary decisions emphasize value-for-money, this mix of price and convenience keeps the generics segment on a faster path than the broader triclabendazole market.

By Distribution Channel: Veterinary Hospitals Lead Through Diagnostic Integration, While Pharmacies Gain OTC Share

Veterinary hospitals held 56.34% share in 2025 and continue to gain as they integrate coproantigen ELISA and fecal testing into clinical care, which anchors prescriptions to confirmed burdens and strengthens stewardship compliance. The diagnostic-therapeutic bundle deepens relationships with producers and supports higher value per case. This dynamic also underpins recent investments by leading manufacturers to own or partner with laboratory capacity. In regulated markets, prescription requirements keep the category rooted in clinical settings. In contrast, in emerging markets, the shift to more accessible retail points increases pharmacy share for oral suspensions and pour-ons. Online veterinary pharmacies extend reach where telemedicine frameworks permit remote prescription, although fragmentation of state and cross-border rules caps scale.

Channel dynamics vary by formulation and by service model in the triclabendazole market. Injectable formats remain anchored to clinical settings due to administration and cold-chain needs, while pour-ons migrate toward retail, where self-administration is common in large herds. Over-the-counter availability expands reach in deregulating markets but intensifies stewardship responsibilities for manufacturers and distributors. Hospital-centric models gain strategic depth when laboratories support surveillance, resistance genotyping, and risk scoring that feed treatment decision support. These features bind therapeutic sales to measurable outcomes and sustain a leading role for hospital channels in the triclabendazole industry.

Geography Analysis

North America accounted for 41.34% of the triclabendazole market share in 2025, reflecting advanced veterinary infrastructure, widespread diagnostic adoption, and regulated distribution that favors clinically integrated prescribing. The United States leads regional volumes due to persistent fluke burdens in wet bottomlands and Gulf Coast pastures, which keeps biannual coverage common in risk-prone locales. Surveillance-led protocols deepen market resilience, with diagnostic-based confirmation guiding timing and rotation to manage resistance concerns in the triclabendazole market. Canada’s growth aligns with integrated dairy health programs and cross-border regulatory alignment that eases product flow. In Mexico, rural access and price-sensitive segments favor generics, yet variable veterinary access slows uptake relative to the United States and Canada.

Asia Pacific is projected to register the fastest pace at an 8.32% CAGR, underpinned by climate-driven expansion of snail habitats and intensifying ruminant systems across diverse agro-ecologies. On the Qinghai-Tibet Plateau, modeling under plateau climatic conditions indicates expanded geographical suitability for fluke transmission into higher altitudes, which is already prompting proactive surveillance and response plans in yak and sheep ranges.

The market in Europe is driven by growth factors, while stewardship frameworks are constraining prophylactic dosing in dairy regions. Southern Europe’s warming winters and variable rainfall patterns bring new pockets into regular treatment schedules, while Eastern European producers accelerate generic uptake from Indian and Chinese suppliers.

Competitive Landscape

The triclabendazole market is moderately fragmented and consolidating, with multinational leaders pursuing diagnostics-therapeutics integration while cost-competitive generics scale across emerging markets. Strategic activity in the triclabendazole market consistently centers on three themes. First, leading players are integrating diagnostics with therapeutics to differentiate on treatment stewardship and clinical outcomes. This is evident in initiatives such as Zoetis’ investments in laboratory and diagnostic services, which strengthen evidence-based prescribing and reinforce value beyond the product itself.

Second, companies are sharpening portfolio focus through targeted acquisitions that enhance margins and expand route-to-market capabilities. Examples include Virbac’s acquisition of Thyronorm and selective regional assets that strengthen presence across European and Asia–Pacific markets. These moves improve commercial reach while leveraging established local channels.

Firms are investing in adjacent therapeutic areas, digital process optimization, and supply-chain modernization to accelerate time to market and improve regulatory compliance. Together, these initiatives support competitive differentiation that extends beyond price competition. Overall, market share shifts in triclabendazole are increasingly driven by outcome-linked stewardship models and efficient access economics across regions and channels.

Triclabendazole Industry Leaders

-

Elanco Animal Health

-

MSD Animal Health

-

Novartis AG

-

Virbac

-

Zoetis

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2024: Norbrook Laboratories has inaugurated advanced, GMP-compliant cleanrooms at its Nairobi manufacturing facility following a GBP 2.3 million investment, strengthening its leadership in East Africa’s veterinary pharmaceuticals market. The upgrade enhances local manufacturing capacity for livestock health products, particularly oral drenches, supporting the production and regional supply of Triclabendazole-based flukicides used in beef and dairy cattle, as well as small ruminants. This expansion reinforces Norbrook’s ability to meet growing demand for liver fluke control across Kenya and the wider East African region while maintaining high quality and regulatory standards.

Global Triclabendazole Market Report Scope

As per the scope of the report, Triclabendazole is an anthelmintic medication (a deworming agent) specifically used to treat fascioliasis (liver fluke infection) in humans and livestock. It is a benzimidazole derivative, which means it works by killing parasitic flatworms, such as Fasciola hepatica, at all stages of development, including immature and adult worms.

The Triclabendazole market is segmented by application, product, distribution channel, and geography. Based on application, the market is segmented into veterinary and human health. The veterinary segment is further bifurcated into cattle, sheep, and goats. By product, the market is segmented into branded and generic. By distribution channel, the market is segmented into veterinary hospitals, veterinary clinics, and pharmacies/drug stores. Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Veterinary Livestock | Cattle |

| Sheep | |

| Goats | |

| Human Health |

| Brand |

| Generic |

| Veterinary Hospitals |

| Veterinary Clinics |

| Pharmacies / Drug Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Application | Veterinary Livestock | Cattle |

| Sheep | ||

| Goats | ||

| Human Health | ||

| By Product Type | Brand | |

| Generic | ||

| By Distribution Channel | Veterinary Hospitals | |

| Veterinary Clinics | ||

| Pharmacies / Drug Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the triclabendazole market outlook through 2031?

The triclabendazole market is projected to rise from USD 436 million in 2026 to USD 560.4 million by 2031 at a 4.36% CAGR, with livestock applications and Asia Pacific growth shaping the trajectory.

Which application contributes the most to demand?

Veterinary livestock accounts for 78.77% of demand and is projected to grow at a 5.34% CAGR, driven by climate-extended transmission and diagnostics-led dosing.

Which product type leads in the triclabendazole market?

Generics held 89.38% share in 2025 and are set to grow at a 5.68% CAGR, supported by API cost leadership and mature bioequivalence pathways.

Which region offers the fastest growth?

Asia Pacific is projected to grow at 8.32% CAGR due to climate-amplified risk and intensifying ruminant production across diverse systems.

Page last updated on: