Treatment Planning Systems And Advanced Image Processing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.06 Billion |

| Market Size (2031) | USD 4.73 Billion |

| Growth Rate (2026 - 2031) | 9.15% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Treatment Planning Systems And Advanced Image Processing Market Analysis by Mordor Intelligence

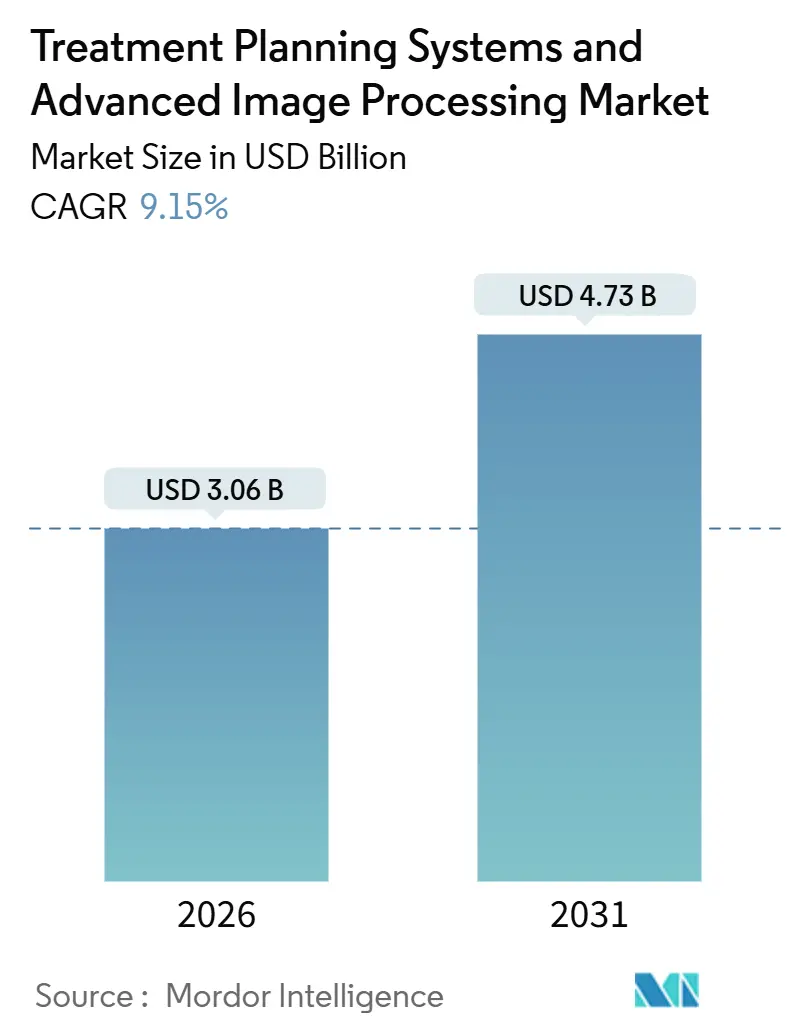

The Treatment Planning Systems And Advanced Image Processing Market size is estimated at USD 3.06 billion in 2026, and is expected to reach USD 4.73 billion by 2031, at a CAGR of 9.15% during the forecast period (2026-2031).

This expansion reflects a steady re-allocation of oncology capital toward cloud-native, GPU-accelerated software that compresses plan-generation times and supports adaptive workflows. Vendors are integrating artificial intelligence into dose-calculation loops, while broader proton-therapy reimbursement and strict interoperability mandates are reshaping purchase criteria across mature and emerging economies. Hospitals and cancer centers are shifting from monolithic suites to modular platforms that interoperate with any linear accelerator, eroding traditional hardware-software bundle margins. Competitive intensity is rising as pure-play software firms leverage subscription pricing and transformer-based auto-planning algorithms to win greenfield projects in Asia-Pacific and North America.

Key Report Takeaways

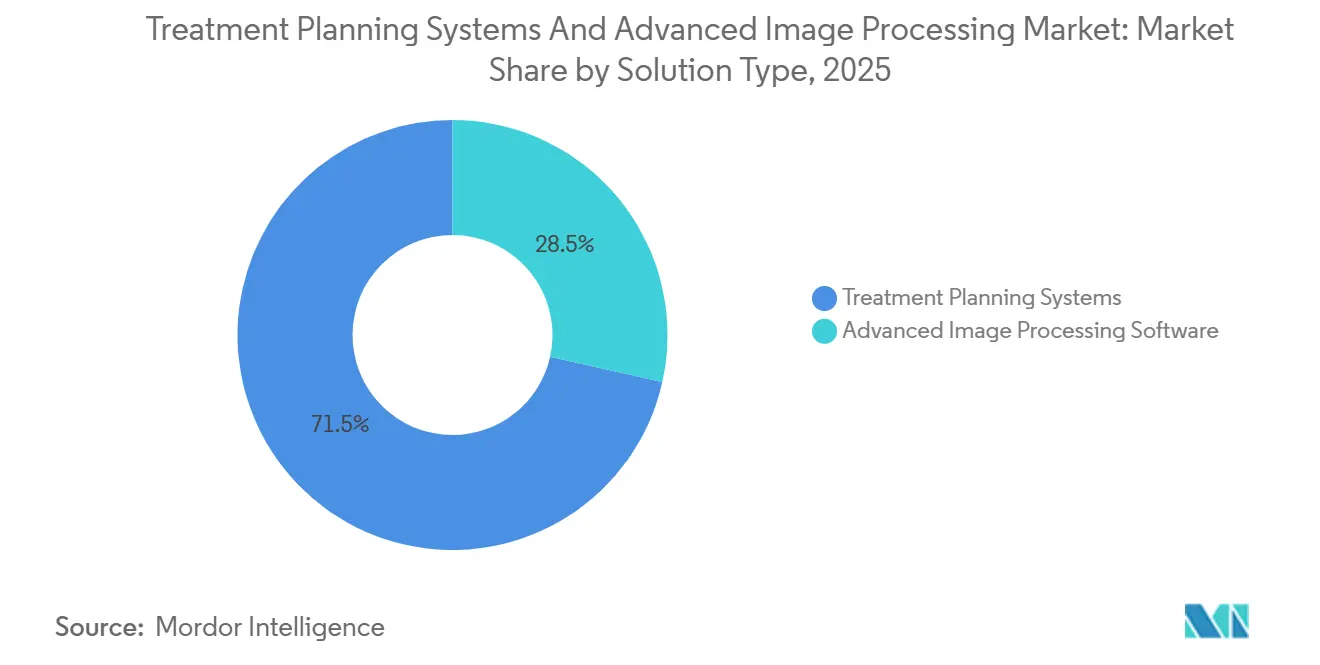

- By solution type, traditional planning suites held 71.55% revenue share in 2025, whereas advanced image-processing modules are expanding at 16.25% CAGR.

- By modality, photons led with 48.23% of the treatment planning systems market share in 2025, while proton and heavy-ion modules are advancing at a 13.15% CAGR.

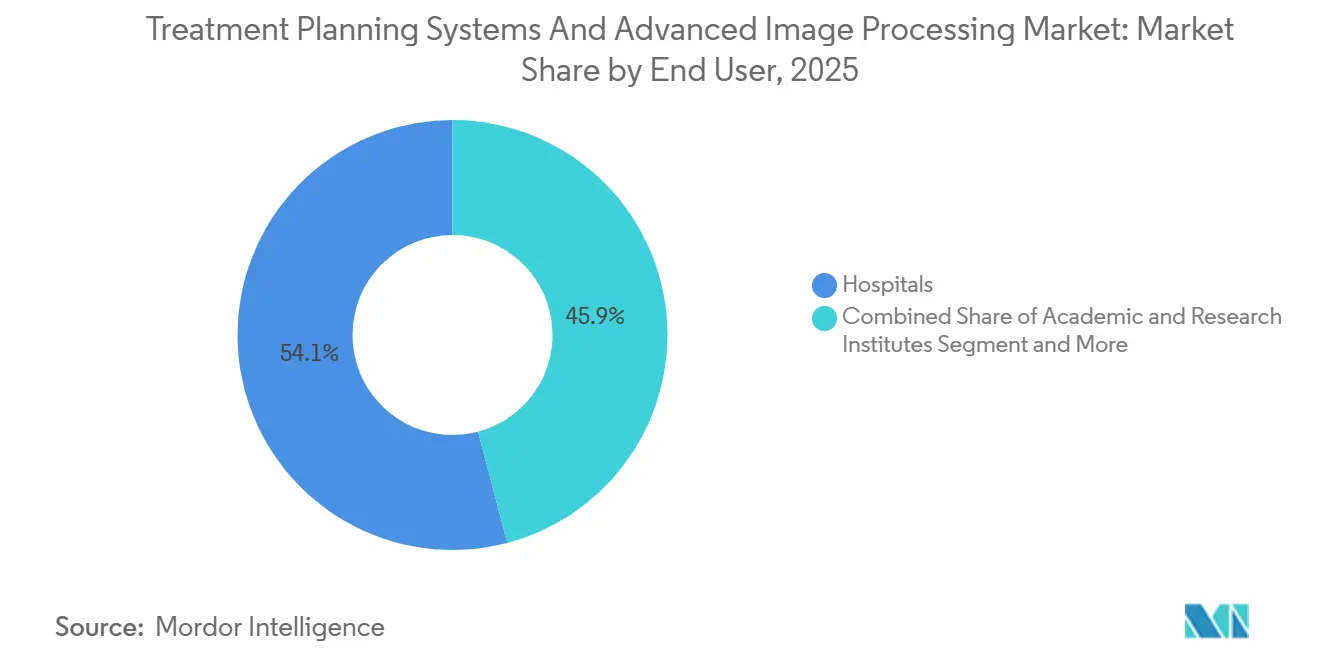

- By end user, hospitals commanded 54.15% revenue in 2025 and academic institutes recorded the highest projected CAGR at 11.51% through 2031.

- By deployment, on-premise installations accounted for 82.35% of the treatment planning systems market size in 2025, yet cloud subscriptions are forecast to grow at 18.11% CAGR to 2031.

- By geography, North America captured 45.25% of revenue in 2025; Asia-Pacific is the fastest-growing region at 11.02% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Treatment Planning Systems And Advanced Image Processing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-driven adaptive radiotherapy planning | +1.8% | North America & Western Europe | Medium term (2-4 years) |

| Wider reimbursement for proton therapy | +1.5% | North America, Japan, South Korea, Germany | Short term (≤ 2 years) |

| Integration of imaging and planning on single cloud platform | +1.3% | North America, Europe, Australia | Medium term (2-4 years) |

| Vendor-neutral oncology informatics ecosystems | +1.1% | Global | Long term (≥ 4 years) |

| Growing adoption of synthetic CT from MRI | +1.2% | North America, Europe, select APAC | Medium term (2-4 years) |

| Demand for ultra-fast GPU-based Monte Carlo algorithms | +1.0% | Global proton & heavy-ion sites | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI-Driven Adaptive Radiotherapy Planning

Artificial intelligence now reduces the multi-hour dose-optimization loop to sub-15-minute cycles, enabling same-day plan adjustments when daily cone-beam CT reveals anatomical change. Mid-tier hospitals therefore offer adaptive treatments without expanding physicist headcount. The FDA’s January 2025 draft guidance classifies algorithm-triggered plan edits as software-as-a-medical-device, favoring vendors with established compliance infrastructure[1]Food and Drug Administration, “Draft Guidance on AI Planning Software,” fda.gov. Yet payers await randomized evidence of long-term outcomes before issuing premium codes, slowing deployment in cost-sensitive systems. Vendors are financing multi-center trials to close this gap, but data maturity will extend into the medium term.

Wider Reimbursement for Proton Therapy

CMS broadened proton coverage in March 2024 to hepatocellular, esophageal, and selected pancreatic tumors, followed by TRICARE and Japan’s health ministry in 2025. Particle-therapy centers are therefore ordering planning modules that calculate variable relative biological effectiveness and provide automated photon-versus-proton comparison dashboards. Rapid coverage expansion accelerates return on capital for compact superconducting cyclotrons and sustains double-digit software demand through 2028.

Integration of Imaging & Planning on Single Cloud Platform

HL7 FHIR-based interoperability mandates in the United States Core Data for Interoperability v6 allow contouring directly on cloud-hosted PET-CT without DICOM export. Siemens Healthineers and other vendors launched browser-based dose engines that eliminate local GPU workstations, cutting upfront costs while enabling multi-site physics oversight. However, ransomware risks drove the FDA to draft more stringent cybersecurity guidance in late 2024, adding compliance costs and lengthening procurement cycles for risk-averse providers.

Vendor-Neutral Oncology Informatics Ecosystems

The mCODE FHIR guide and TEFCA framework standardize radiation-therapy data objects, dismantling proprietary integration moats. Academic centers now run RayStation for photons, IBA myQA for protons, and legacy linacs from Varian or Elekta without interface fees. This modularity erodes maintenance renewals for hardware-linked suites and opens white space for software-only entrants.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital costs and long ROI cycles | -0.9% | Emerging markets & rural U.S. | Short term (≤ 2 years) |

| Shortage of trained dosimetrists/physicists | -0.7% | Sub-Saharan Africa, Southeast Asia, Latin America | Long term (≥ 4 years) |

| Cyber-security concerns in cloud-deployed TPS | -0.5% | North America & Europe | Medium term (2-4 years) |

| Limited evidence on long-term benefit of AI auto-planning | -0.4% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Costs & Long ROI Cycles

Standalone photon suites cost roughly USD 250,000 and integrated proton platforms exceed USD 1.5 million, producing 5-7-year payback windows under declining fee schedules[2]American Society for Radiation Oncology, “Practice Economics Survey 2024,” astro.org. Subscription pricing spreads expense but shifts revenue risk to vendors, lowering near-term earnings visibility.

Shortage of Trained Dosimetrists/Medical Physicists

Workforce growth of 2.3% trails software deployment growth, leaving plans underserved in low-income regions. IEC 62083 : 2025 obliges a physicist sign-off on every AI-generated plan, constraining automation’s labor-saving promise.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Unbundling Accelerates Software Specialization

Traditional suites accounted for 71.55% revenue during 2025, reflecting their role as the de facto engine for beam geometry, dose constraints, and quality assurance. Still, advanced image-processing modules are expanding at 16.25% CAGR, the quickest pace across the treatment planning systems market. Providers prioritize deformable registration, synthetic CT, and AI contouring modules that install beside legacy engines, avoiding risky forklift upgrades while boosting throughput. Elekta’s maintenance renewals dropped 8% in fiscal 2025 because customers migrated to best-of-breed imaging plug-ins[3]Elekta AB, “Annual Report 2025,” elekta.com. Meanwhile, agile vendors like Brainlab gained share by offering cloud dashboards that compare rival plans side-by-side.

Innovators exploit vendor-neutral APIs to insert micro-services—auto-segmentation, plan comparison, bladder-dose alerts—into existing workflows. As hospitals seek line-item flexibility, modular buying will push traditional suite share below two-thirds by 2031. Subscription pricing also lowers entry hurdles for emerging markets, aligning cost with case volume and enlarging the addressable base for the treatment planning systems market.

By Modality: Particle Therapy Drives Planning Complexity

Photon techniques, including IMRT and VMAT, represented 48.23% of deployments in 2025 because of the installed linear-accelerator fleet. Proton and heavy-ion centers are multiplying, driving a 13.15% CAGR for particle-therapy software. Asia-Pacific governments fund large facilities, while U.S. academic hubs install compact cyclotrons that need Monte-Carlo pencil-beam calculators. Vendors must maintain distinct engines yet ensure a single user experience across modalities, making interoperability a strategic imperative within the treatment planning systems market.

Brachytherapy planning is shrinking as SBRT replaces implant procedures, though hybrid boost strategies keep niche demand alive. Carbon-ion planning remains confined to Japan and Germany but commands premium maintenance fees because of algorithmic complexity. Photon vendors race to integrate particle options to retain enterprise deals, while pure-play proton specialists pitch best-in-class physics accuracy to new builds.

By End User: Academic Institutes Pioneer Adaptive Protocols

Hospitals delivered 54.15% of 2025 revenue, standardizing multi-site networks on unified interfaces for centralized review. Yet academic and research institutes grow fastest at 11.51% CAGR as they validate adaptive protocols, feed AI datasets, and publish peer-reviewed evidence that influences payer policy. Academic demand for scripting hooks and custom optimizers favors open platforms like Elekta Monaco, while hospitals focus on turnkey automation.

Dedicated cancer centers face bundling payment pressure, delaying refresh cycles; nevertheless, subscription models unlock cloud adoption where on-premise capex is prohibitive. Partnerships between AI startups and universities hasten algorithm validation, ensuring early market traction for disruptive features within the treatment planning systems industry.

By Deployment Model: Cloud Migration Reshapes Pricing

On-premise software captured 82.35% revenue in 2025, reflecting legacy preference for local data custody. Cloud subscriptions, however, are rising at 18.11% CAGR as GPU costs shift to operational spend, suiting ambulatory centers and rural hospitals. Siemens’ browser-based dose engine cuts upfront investment from USD 300,000 to USD 5,000 monthly, highlighting the opex appeal.

Compliance worries slow enterprise migrations, yet hybrid models—compute in cloud, PHI on-site—balance risk and savings. As cybersecurity frameworks mature and insurers underwrite cloud risk, subscription penetration will accelerate, further diluting monolithic license sales and expanding recurring revenue in the treatment planning systems market.

Geography Analysis

North America controlled 45.25% revenue in 2025. Early adopters benefit from CMS proton coverage expansion that spurred a 19% annual jump in proton-planning modules. Canada’s provincial networks deploy cloud suites for centralized physics oversight across sparse geographies. Mexico’s shortage of board-certified physicists slows uptake of adaptive features, prompting interest in AI decision-support triage to stretch workforce capacity.

Asia-Pacific posts the fastest 11.02% CAGR through 2031. China’s CNY 4.2 billion (USD 580 million) proton build-out funds eight tier-2 city centers, each specifying vendor-agnostic planning stacks. Japan’s expanded proton reimbursement for lung cancer triggered six new sites, accelerating software orders. South Korea’s National Cancer Center implemented Varian Eclipse proton modules in 2025, setting a benchmark for pediatric brain-tumor care. India’s Ayushman Bharat program finances 22 new linear-accelerator centers, creating downstream demand for cost-efficient cloud planners.

Europe maintains solid share as Germany, the United Kingdom, and France adopt strict CE-mark oversight for AI planning tools, favoring vendors with mature quality systems. DICOM-RT and FHIR policies encourage modular selection, while carbon-ion initiatives in Germany require ultra-precise dose engines. Middle East & Africa grapple with physicist scarcity and lengthier device approvals, though the UAE’s streamlined 15-month process offers a regional foothold for early movers. South America gains momentum after ANVISA cut clearance times to 12 months, enabling São Paulo and Rio de Janeiro hospitals to upgrade aging suites without multiyear delays.

Competitive Landscape

The market remains moderately concentrated. Varian, Elekta, RaySearch, and Brainlab together hold a sizeable share, but erosion is clear. Equipment incumbents acquire niche firms—Elekta bought DOSIsoft—to plug image-processing gaps and defend maintenance revenue. Siemens cross-sells planners into radiology accounts using its syngo.via imaging footprint. Disruptors court academic centers with Python scripting and clinical-trial data hooks, trading early access for anonymized datasets that train next-gen AI.

Performance leadership now hinges on GPU-accelerated Monte Carlo and workflow-embedded plan-comparison dashboards. Vendors embracing open APIs position best for the shift toward vendor-neutral, cloud-distributed ecosystems. As subscription adoption rises, revenue visibility improves yet total contract value shrinks, pressing incumbents to monetize analytics, quality assurance, and decision support alongside core dose engines within the treatment planning systems market.

Treatment Planning Systems And Advanced Image Processing Industry Leaders

Siemens Healthineers

Elekta AB

RaySearch Laboratories

Philips Healthcare

Brainlab AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: ConcertAI’s TeraRecon unveiled TeraRecon AV, an AI-enabled visualization suite enhancing diagnostic precision across PET-CT fusion workflows.

- May 2025: RaySearch released RayStation v2025 with machine-learning-driven auto-planning and support for upright patient positioning.

Global Treatment Planning Systems And Advanced Image Processing Market Report Scope

As per the scope of the report, Treatment Planning Systems (TPS) are sophisticated software tools used in medical procedures, particularly in radiation therapy, to develop precise treatment plans tailored to individual patient anatomy and pathology. Advanced Image Processing involves the use of computational techniques to enhance, analyze, and interpret medical images, enabling better visualization, segmentation, and accuracy in diagnosis and treatment planning.

The segmentation for the treatment planning systems and advanced image processing market is categorized by solution type, modality, end user, deployment model, and geography. By solution type, the market includes treatment planning systems and advanced image processing software. By modality, it is segmented into photon (IMRT/VMAT, SBRT), proton and heavy-ion, brachytherapy, and others (SRS, high-energy electrons). By end user, the market is divided into hospitals, dedicated cancer centers, and academic and research institutes. By deployment model, it is classified into on-premise and cloud-based. Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The Market Forecasts are Provided in Terms of Value (USD).

| Treatment Planning Systems |

| Advanced Image Processing Software |

| Photon (IMRT/VMAT, SBRT) |

| Proton & Heavy-Ion |

| Brachytherapy |

| Others (SRS, High-energy Electrons) |

| Hospitals |

| Dedicated Cancer Centers |

| Academic & Research Institutes |

| On-premise |

| Cloud-based |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Solution Type | Treatment Planning Systems | |

| Advanced Image Processing Software | ||

| By Modality | Photon (IMRT/VMAT, SBRT) | |

| Proton & Heavy-Ion | ||

| Brachytherapy | ||

| Others (SRS, High-energy Electrons) | ||

| By End User | Hospitals | |

| Dedicated Cancer Centers | ||

| Academic & Research Institutes | ||

| By Deployment Model | On-premise | |

| Cloud-based | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the treatment planning systems market in 2026?

The treatment planning systems market size reached USD 3.06 billion in 2026 and is set to grow steadily at a 9.15% CAGR.

Which segment is growing fastest within treatment planning?

Advanced image-processing software, including AI-driven auto-segmentation and synthetic CT, is expanding at 16.25% CAGR.

What drives demand for proton-therapy planning software?

Expanded reimbursement in the United States and Japan plus new center construction in China and South Korea are boosting proton-specific planning demand.

Why are hospitals moving to cloud-based planning platforms?

Subscription pricing shifts expense from capital to operating budgets, while web-based dose engines eliminate costly GPU workstations.

What are the key barriers to wider AI auto-planning adoption?

Limited prospective clinical evidence, stricter FDA cybersecurity rules, and mandatory physicist oversight slow broad implementation.

Page last updated on: