Trauma And Extremities Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

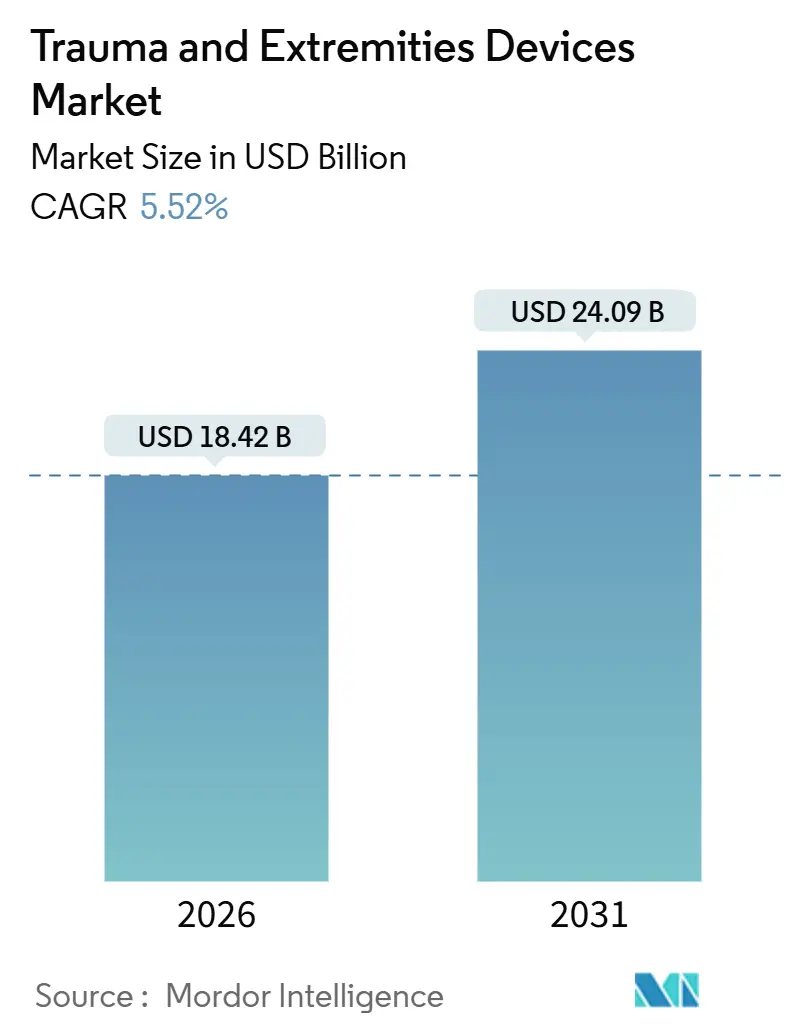

| Market Size (2026) | USD 18.42 Billion |

| Market Size (2031) | USD 24.09 Billion |

| Growth Rate (2026 - 2031) | 5.52% CAGR |

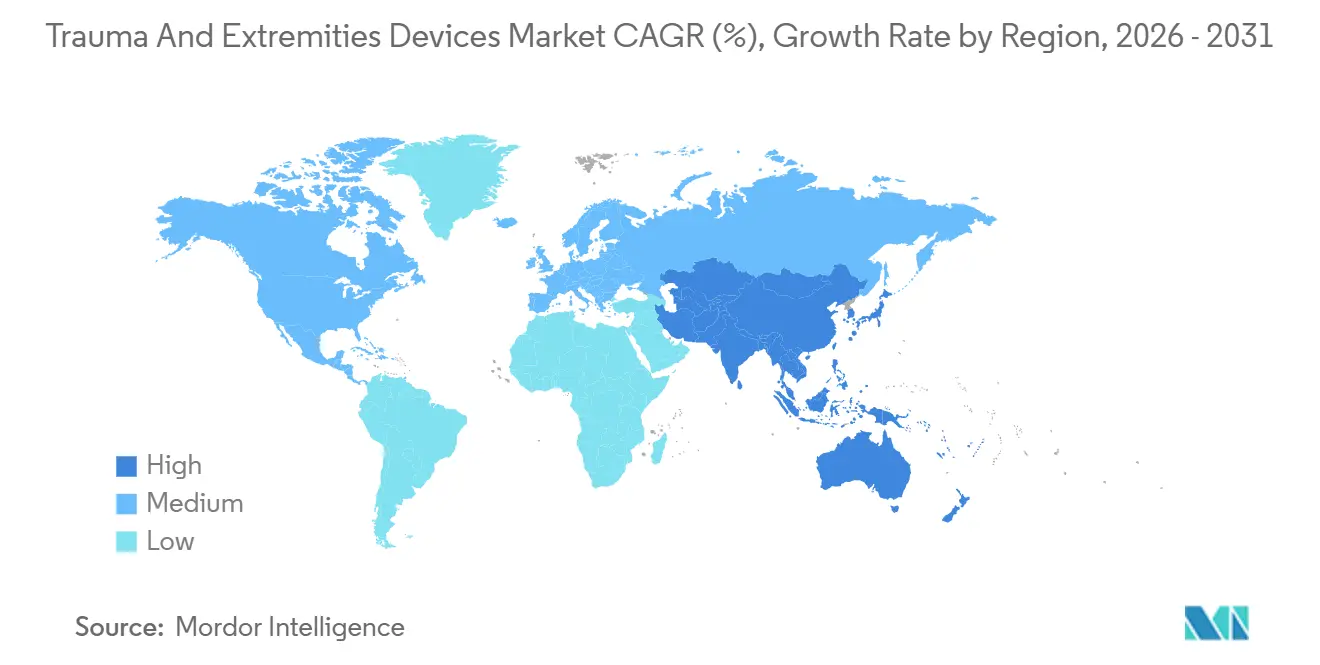

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Trauma And Extremities Devices Market Analysis by Mordor Intelligence

The Trauma And Extremities Devices Market size is estimated at USD 18.42 billion in 2026, and is expected to reach USD 24.09 billion by 2031, at a CAGR of 5.52% during the forecast period (2026-2031).

Population aging is accelerating fragility fractures, road-traffic trauma remains high despite safer vehicles, and hospitals are adopting patient-specific implants that command premium prices yet improve outcomes. Internal fixation keeps long-bone surgery reliable, while external fixation grows on demand for soft-tissue preservation. Bioabsorbable polymers, artificial-intelligence planning tools, and sensor-enabled constructs are redefining product differentiation, prompting incumbents to bundle hardware with digital services. Asia-Pacific is scaling trauma capacity fastest, but reimbursement advantages keep North America the near-term revenue leader.

Key Report Takeaways

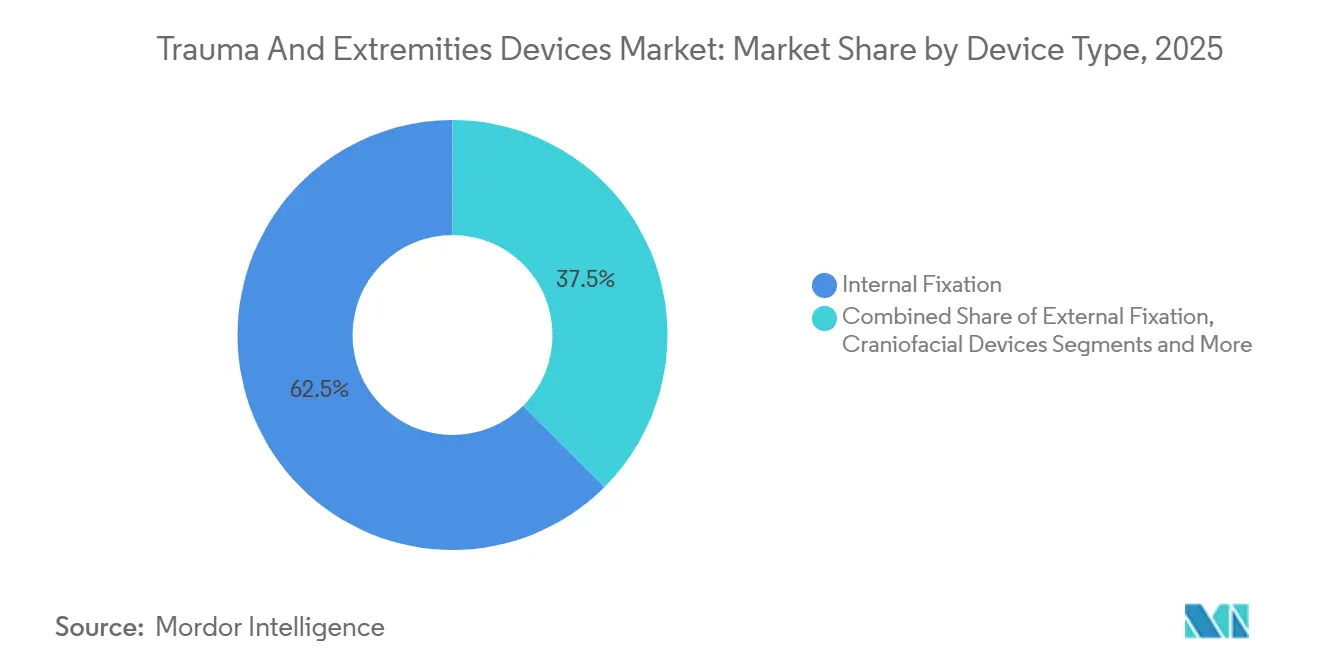

- By device type, internal fixation captured 62.55% of the trauma and extremities devices market share in 2025, whereas external fixation is forecast to expand at an 8.25% CAGR through 2031.

- By injury location, lower extremities held 53.53% revenue share in 2025, while upper extremities are projected to grow at an 8.85% CAGR through 2031.

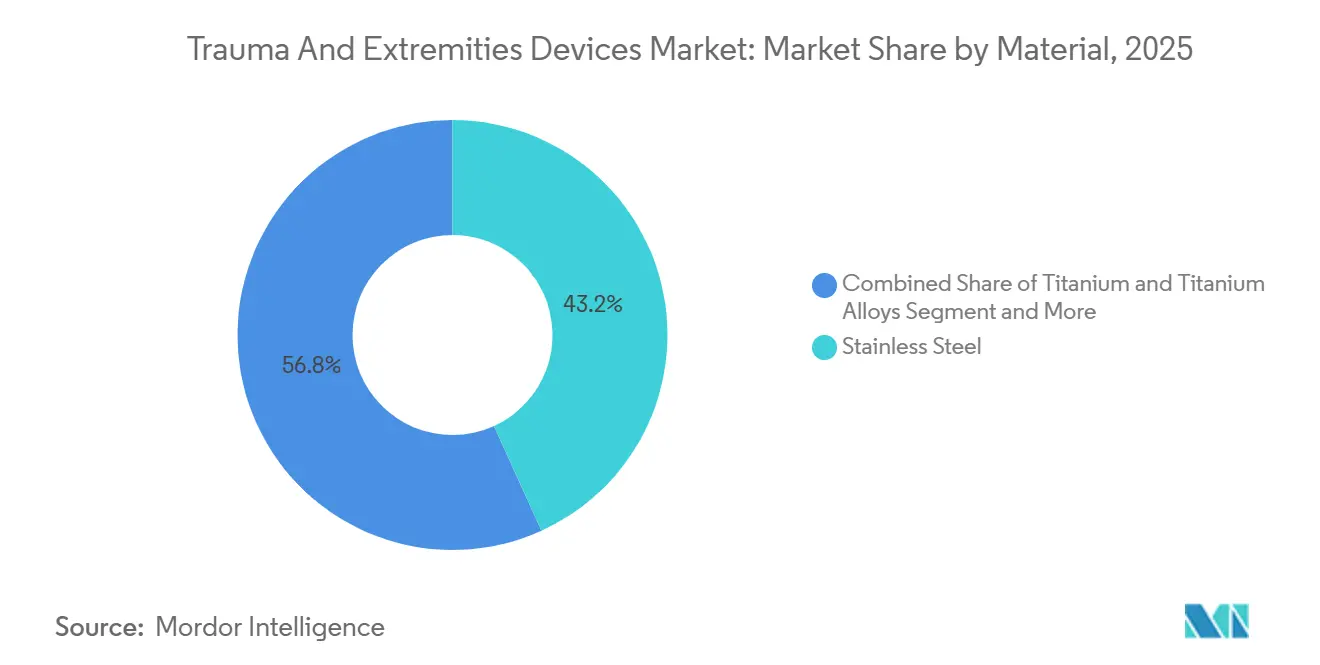

- By material, stainless steel accounted for a 43.23% share of the trauma and extremities devices market size in 2025, and bioabsorbable polymers are advancing at a 9.15% CAGR toward 2031.

- By end user, hospitals led with 46.25% revenue share in 2025, whereas ambulatory surgical centers record the highest projected CAGR at 8.21% through 2031.

- By geography, North America commanded 39.15% revenue in 2025, while Asia-Pacific is poised for the fastest regional growth at an 8.51% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Trauma And Extremities Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of road accidents and sports injuries | +1.2% | Global, acute in South Asia, Sub-Saharan Africa, Latin America | Short term (≤ 2 years) |

| Growing geriatric population and fragility fractures | +1.5% | North America, Europe, East Asia | Long term (≥ 4 years) |

| Advances in minimally invasive fixation and biomaterials | +0.9% | Early adoption in North America and EU, widening in Asia-Pacific | Medium term (2–4 years) |

| Favorable reimbursement in high-income markets | +0.7% | North America, Western Europe, Australia | Short term (≤ 2 years) |

| Real-time sensor-enabled smart implants | +0.4% | Pilot programs in North America and EU, gradual uptake in Asia-Pacific | Long term (≥ 4 years) |

| AI-driven planning and 3-D-printed patient-specific implants | +0.6% | North America and EU; select tertiary centers in Asia-Pacific | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Road Accidents and Sports Injuries

Road-traffic collisions continue to generate a large share of fracture surgery worldwide. The World Health Organization reports 1.19 million annual deaths and 20 million to 50 million non-fatal injuries, with pedestrians, cyclists, and motorcyclists exceeding half of all fatalities. Low- and middle-income countries carry more than 90% of this burden, reflecting infrastructure gaps and limited emergency care. Sports participation is also increasing, driving upper-extremity injuries treated with contoured plates and minimally invasive screws. Emerging economies experience simultaneous motorization and active-lifestyle trends, ensuring consistent demand for trauma hardware even as safety features reduce injury severity in high-income regions.

Growing Geriatric Population and Fragility Fractures

The International Osteoporosis Foundation calculates up to 37 million fragility fractures per year among adults aged 55 and older, and hip-fracture incidence is expected to nearly double by 2050. National registries such as the United Kingdom’s NHFD record 72,000 to 76,000 hip fractures annually, with 12-month mortality above 22%. Surgeons increasingly rely on cephalomedullary nails and locking plates to secure osteoporotic bone, yet healing remains challenging when bone quality is poor. Pharmaceutical therapies help, but uneven uptake leaves fixation devices as the clinical mainstay for an aging world.

Advances in Minimally Invasive Fixation and Biomaterials

Minimally invasive plate osteosynthesis lowers soft-tissue disruption and shortens operative times. Peer-reviewed studies in 2024 and 2025 show union rates above 95% and 20% to 30% reductions in surgery duration compared with open techniques. Bioabsorbable polymers such as polylactic acid remove the need for hardware extraction, which is valuable for pediatric cases and patients sensitive to metal. The U.S. Food and Drug Administration cleared several polymer screw and plate systems in 2024, confirming regulator confidence in their safety. Stainless steel and titanium remain essential for high-load fractures, but premium materials like PEEK and nitinol are gaining niche adoption where radiolucency or shape memory offers clear clinical benefit.

AI-Driven Planning and 3-D-Printed Patient-Specific Implants

Artificial-intelligence software now analyzes CT scans to recommend implant size, trajectory, and screw placement, cutting operative time by up to 25% and improving reduction quality in complex fractures. Three-dimensional printing delivers custom guides and implants that fit anatomical outliers, a breakthrough for pelvic and acetabular cases. Regulatory approval paths remain demanding, but adoption is accelerating in academic centers that can invest in printers and surgeon training. Manufacturers that integrate planning software with their implant lines capture loyalty from high-acuity hospitals, while vendors lacking digital portfolios face price pressure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced implants in LMICs | −0.8% | Sub-Saharan Africa, South Asia, parts of Latin America | Medium term (2–4 years) |

| Lengthening regulatory approval timelines | −0.5% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| Sustainability scrutiny on single-use metallic kits | −0.3% | EU, North America, selected Asia-Pacific markets | Long term (≥ 4 years) |

| Competition from orthobiologic and regenerative therapies | −0.4% | Early adoption in North America and Europe | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Implants in LMICs

Locking plates, bioabsorbables, and custom devices often cost more than annual household income in many lower-income regions. The World Health Organization estimates that 5 billion people still lack affordable surgical care, and orthopedics represents a sizable share of this gap. India and China are building domestic factories that cut prices by nearly half, yet quality oversight varies. Multinational tiered-pricing schemes gain limited traction because hospitals focus on upfront expense. Modular fixation sets that reduce inventory needs present a middle path, but stainless steel will stay dominant where budgets remain tight.

Lengthening Regulatory Approval Timelines

Stricter evidence requirements prolong time-to-market. FDA 510(k) submissions that once closed quickly now demand extra bench data, and legacy devices in Europe must be re-certified under the Medical Device Regulation, causing backlogs that add one to two years before launch[1]U.S. Food and Drug Administration, “510(k) Clearances – Orthopedic Devices,” fda.gov. China offers fast-track routes for innovative devices, yet foreign vendors still perform local trials that add another 18-plus months. Companies with strong regulatory teams can absorb the cost; startups find barriers steep, reinforcing market concentration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: External Fixation Gains Ground

Internal fixation devices controlled 62.55% of the trauma and extremities devices market in 2025. Plates, screws, and intramedullary nails remain the backbone of long-bone surgery, with locking technology enabling rigid fixation in osteoporotic bone. External fixation, by contrast, will post an 8.25% CAGR due to its value in contaminated wounds, damage-control orthopedics, and elective limb-lengthening. Surgeons now combine minimal internal fixation with hybrid frames that preserve soft tissue while allowing precise adjustments post-operatively.

Modern carbon-fiber frames are radiolucent, enabling continuous imaging without frame removal, and modular designs support reuse in resource-limited hospitals. In 2025 peer-reviewed studies reported union rates matching internal systems in carefully selected fractures, reshaping perceptions that frames are only temporary. Growth in outpatient trauma surgery also favors lightweight external solutions that simplify inventory at ambulatory centers.

By Injury Location: Upper Extremities Accelerate

Lower-extremity trauma generated 53.53% of 2025 revenue, driven by weight-bearing demands for femoral, tibial, and ankle fractures. Hip fractures are particularly burdensome; United Kingdom registry data document up to 76,000 cases annually, with mortality still exceeding 22%. Upper-extremity devices, however, will record the fastest 8.85% CAGR through 2031. Distal radius fractures dominate emergency rooms, and volar locking plates outperform casts in displaced injuries. Proximal humerus fractures rise with people staying active later in life, amplifying demand for contoured shoulder plates.

Workplace accidents and recreational sports both contribute, while minimally invasive pinning and arthroscopic techniques shorten recovery times and align with ambulatory care models. Implant firms respond with low-profile plates and variable-angle locking screws tuned to the fine bone stock of the wrist, hand, and shoulder.

By Material: Bioabsorbable Polymers Disrupt Incumbents

Stainless steel held 43.23% share in 2025 due to predictable strength and low cost. Titanium follows for its corrosion resistance and bone-friendly modulus. Bioabsorbable polymers, though, will compound at 9.15% as patients and payers avoid second surgeries to remove metal. The U.S. FDA cleared several polylactic-acid systems in 2024, validating mechanical reliability in selected fracture loads.

Clinical trials published in 2025 showed comparable union rates to metallic screws in syndesmosis and pediatric forearm fractures, but stress-bearing long-bones still rely on metal. PEEK delivers radiolucency valuable in follow-up imaging, while nitinol contributes shape memory for dynamic compression. Arrival of controlled-degradation copolymers could further shift share toward absorbables in the trauma and extremities devices market.

By End User: Ambulatory Surgical Centers Reshape Care Delivery

Hospitals retained 46.25% of market revenue in 2025, reflecting their indispensability for multi-injury trauma and patients with comorbidities. Yet ambulatory surgical centers will post an 8.21% CAGR, propelled by CMS decisions in 2024 and 2025 that added fracture fixation procedures to the outpatient-eligible list[2]Centers for Medicare & Medicaid Services, “ASC Covered Procedures List Updates 2024-2025,” cms.gov.

Studies during 2024 verified that infection rates and functional outcomes match inpatient settings, while costs fall 30% to 50%. Implant vendors now ship pre-sterilized, single-use kits that meet tight turnover schedules at ASCs, a trend likely to accelerate the migration of moderate-complexity trauma cases away from full-service hospitals.

Geography Analysis

North America contributes the largest regional revenue, representing 39.15% of the trauma and extremities devices market in 2025. Ample insurance coverage, trauma-registry networks, and early access to AI planning tools underpin continued hardware demand. Hospitals also adopt sensor-enabled implants sooner, supported by reimbursement codes for remote monitoring.

Europe follows with steady demand tempered by Medical Device Regulation costs that slow new launches. National health systems there use registry data to benchmark performance, nudging suppliers toward value-based contracts. Germany, France, and the United Kingdom remain the top three European spenders, while Eastern Europe shows catch-up growth as hospitals modernize.

Asia-Pacific is the growth engine, advancing at an 8.51% CAGR through 2031. China funds trauma centers under its Five-Year Health Plan, and priority review channels drop device approval times to near U.S. norms. India widens insurance coverage under Ayushman Bharat, spurring procedure volumes even in tier-two cities. Local manufacturers in both countries price stainless-steel implants 40% to 60% below imports. Japan’s rapidly aging society keeps hip-fracture volumes high, although reimbursement pressures encourage day-surgery solutions. Australia and South Korea mirror North American adoption curves, while Southeast Asian nations upgrade surgical capacity more slowly. The Middle East invests in medical-tourism hubs that require premium implants, and selective African markets pilot modular fixation kits supported by donor funding.

Competitive Landscape

The trauma and extremities devices market remains moderately concentrated. The top five companies—Stryker, Zimmer Biomet, Johnson & Johnson’s DePuy Synthes, Smith & Nephew, and Medtronic—control a large revenue block through global sales networks and multi-year bundled deals with health systems. Zimmer Biomet’s ZBEdge platform links implant telemetry with analytics, steering design refinements and cementing customer loyalty.

Mergers and acquisitions target orthobiologics and digital surgery. Zimmer Biomet’s 2024 purchase of Embody added collagen-based grafts that complement fixation hardware. Smith & Nephew formed a 2024 partnership to build low-cost implants in India, defending share against domestic entrants. Medtronic secured CE Mark for a bioabsorbable screw system in 2024, signaling commitment to absorbable technology[3]Medtronic, “Bioabsorbable Polymer Screw System CE Mark Approval,” medtronic.com.

Niche players expand in focused domains. Bioretec reports promising pediatric fracture data for its absorbable nails, gaining early adopter clinics. Acumed pushes anatomically contoured wrist and shoulder plates, while Orthofix adds connected bone-growth stimulators that collect compliance data. Digital-health startups link wearable sensors with implant loads, aiming to predict hardware failure and cut revision costs. Regulatory hurdles and capital intensity limit new entrants, but technology convergence keeps competitive pressure high.

Trauma And Extremities Devices Industry Leaders

Stryker

Zimmer Biomet

Johnson & Johnson

Smith & Nephew

Medtronic

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Arthrex launched Synergy Power, a battery-powered handpiece system designed for sports, arthroplasty, trauma, and distal-extremity procedures.

- May 2025: OrthoPediatrics expanded its Trauma and Deformity line with the 3P Pediatric Plating Platform Hip System, aiming at surgically challenging adolescent hips.

Global Trauma And Extremities Devices Market Report Scope

As per the scope of the report, trauma and extremities devices are medical tools and equipment used in the management, stabilization, and treatment of injuries to the limbs and other extremities resulting from trauma. These devices are designed to immobilize, support, or facilitate surgical intervention for fractures, dislocations, soft tissue injuries, and other extremity-related trauma.

The trauma and extremities devices market is segmented by device type into internal fixation devices, external fixation devices, craniofacial devices, long-bone stimulation, and others; by injury location into lower extremities, upper extremities, and pelvic injuries; by material into stainless steel, titanium and titanium alloys, bioabsorbable polymers, and other advanced materials such as PEEK and nitinol; by end user into hospitals, ambulatory surgical centers, specialty/orthopedic clinics, and others; and by geography into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The Market Forecasts are Provided in Terms of Value (USD).

| Internal Fixation Devices |

| External Fixation Devices |

| Craniofacial Devices |

| Long-Bone Stimulation |

| Others |

| Lower Extremities |

| Upper Extremities |

| Pelvic |

| Stainless Steel |

| Titanium & Titanium Alloys |

| Bioabsorbable Polymers |

| Other Advanced Materials (PEEK, Nitinol) |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty/Orthopedic Clinics |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Device Type | Internal Fixation Devices | |

| External Fixation Devices | ||

| Craniofacial Devices | ||

| Long-Bone Stimulation | ||

| Others | ||

| By Injury Location | Lower Extremities | |

| Upper Extremities | ||

| Pelvic | ||

| By Material | Stainless Steel | |

| Titanium & Titanium Alloys | ||

| Bioabsorbable Polymers | ||

| Other Advanced Materials (PEEK, Nitinol) | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty/Orthopedic Clinics | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the trauma and extremities devices market in 2026?

The trauma and extremities devices market size is USD 18.42 billion in 2026.

What is the expected CAGR for trauma hardware through 2031?

Market revenue is forecast to grow at a 5.52% CAGR from 2026 to 2031.

Which segment shows the fastest growth rate?

External fixation devices lead with an 8.25% CAGR because surgeons need soft-tissue-sparing stabilization.

Which region is expanding fastest?

Asia-Pacific is projected to post an 8.51% regional CAGR as China and India scale hospital capacity.

Why are bioabsorbable polymers gaining adoption?

They remove the need for implant-removal surgery, improving convenience and lowering healthcare costs, especially for pediatric and upper-extremity cases.

How are ambulatory surgical centers influencing device demand?

ASC procedure lists now include fracture fixation, shifting moderate-complexity surgery out of hospitals and boosting demand for pre-sterilized, single-use implant kits.

Page last updated on: