Transplant Drug Monitoring Assay Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 534.57 Million |

| Market Size (2031) | USD 891.59 Million |

| Growth Rate (2026 - 2031) | 10.77% CAGR |

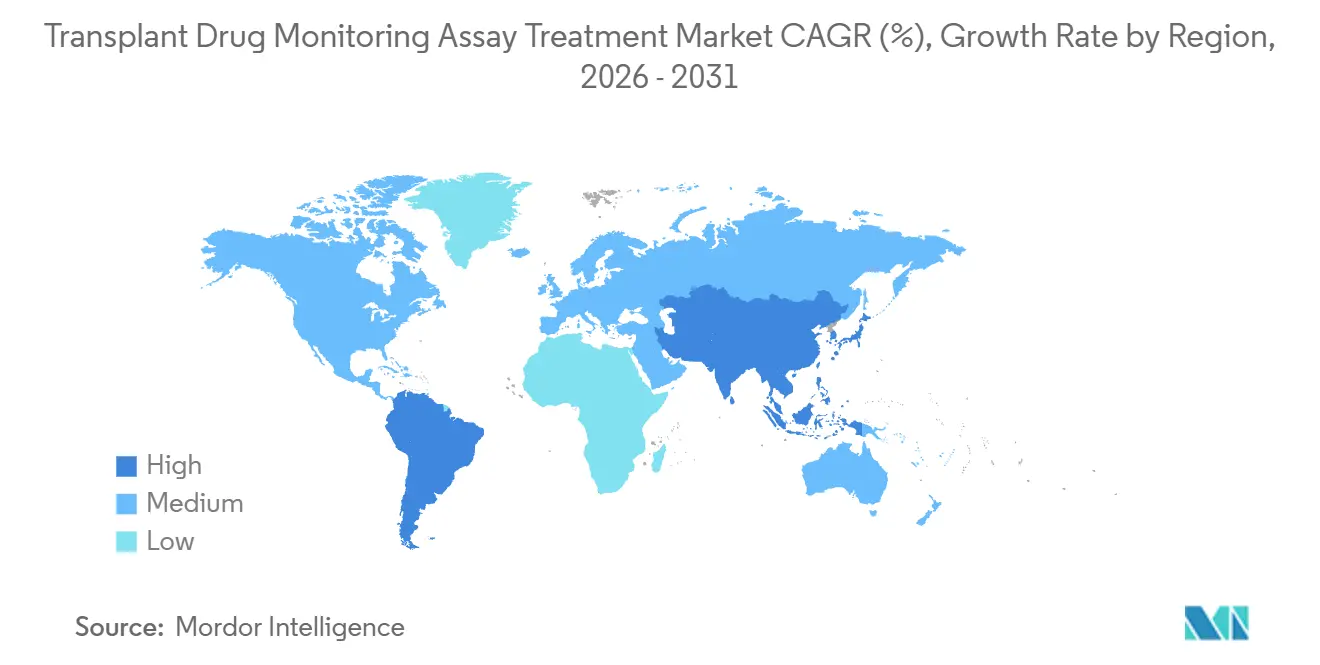

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Transplant Drug Monitoring Assay Treatment Market Analysis by Mordor Intelligence

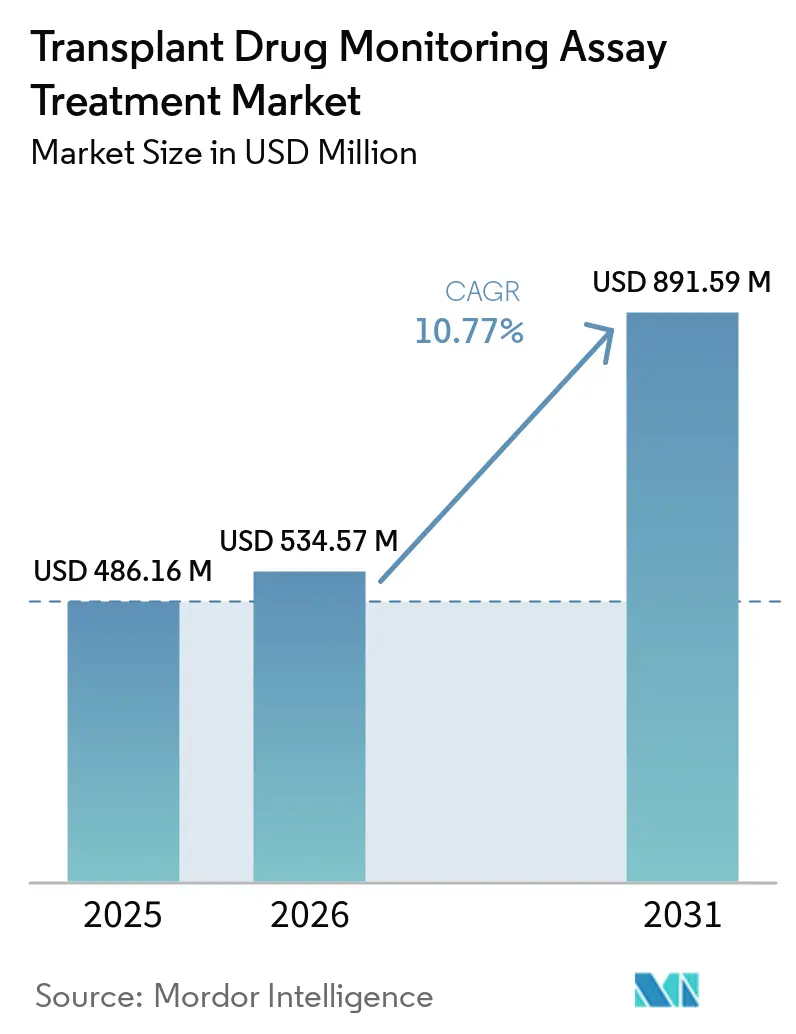

The Transplant Drug Monitoring Assay Treatment Market size is projected to be USD 486.16 million in 2025, USD 534.57 million in 2026, and reach USD 891.59 million by 2031, growing at a CAGR of 10.77% from 2026 to 2031.

Solid organ transplant volumes continue to expand, which keeps test demand resilient as long-term immunosuppression requires routine therapeutic drug monitoring across the patient life cycle. Momentum in automated LC-MS/MS solutions and broader immunoassay menus is lowering workflow barriers and enabling wider adoption in hospital and reference laboratories, which supports steady growth in the Transplant Drug Monitoring Assay Treatment market. Regulatory progress around CE-IVD certifications and moderate-complexity categorization for automated LC-MS/MS platforms is improving comparability and standardization, which reduces the operational burden on laboratories and strengthens test reliability at scale. Precision dosing software and data-driven dose titration are beginning to embed therapeutic drug monitoring into clinical decision support, which points to higher testing frequency in the acute post-transplant period at centers that implement these tools. The Transplant Drug Monitoring Assay Treatment market also benefits from microsampling pilots that reduce patient burden and broaden access in pediatric and remote settings, although reimbursement and validation frameworks continue to evolve.

Key Report Takeaways

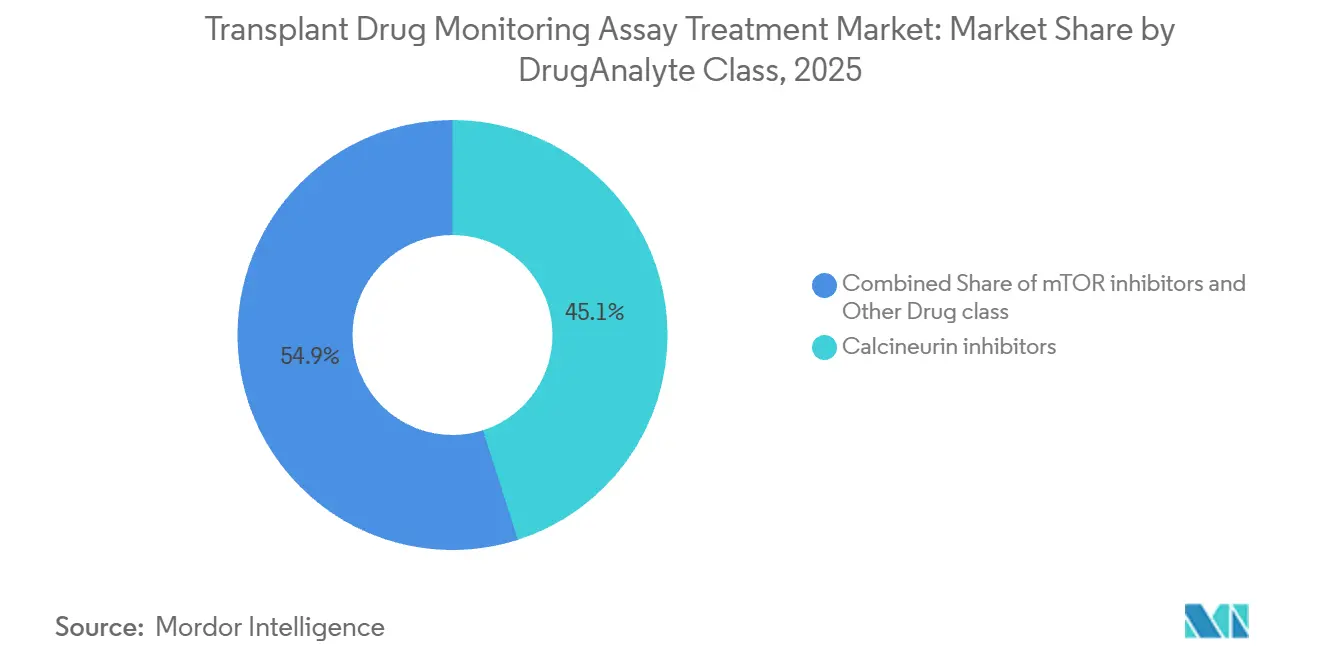

By drug or analyte class, calcineurin inhibitors led with 45.08% revenue share in 2025, while mTOR inhibitors are projected to grow at 11% CAGR through 2031.

By technology, immunoassay platforms held 56.13% share in 2025, while LC-MS/MS is projected to expand at 11.3% CAGR through 2031.

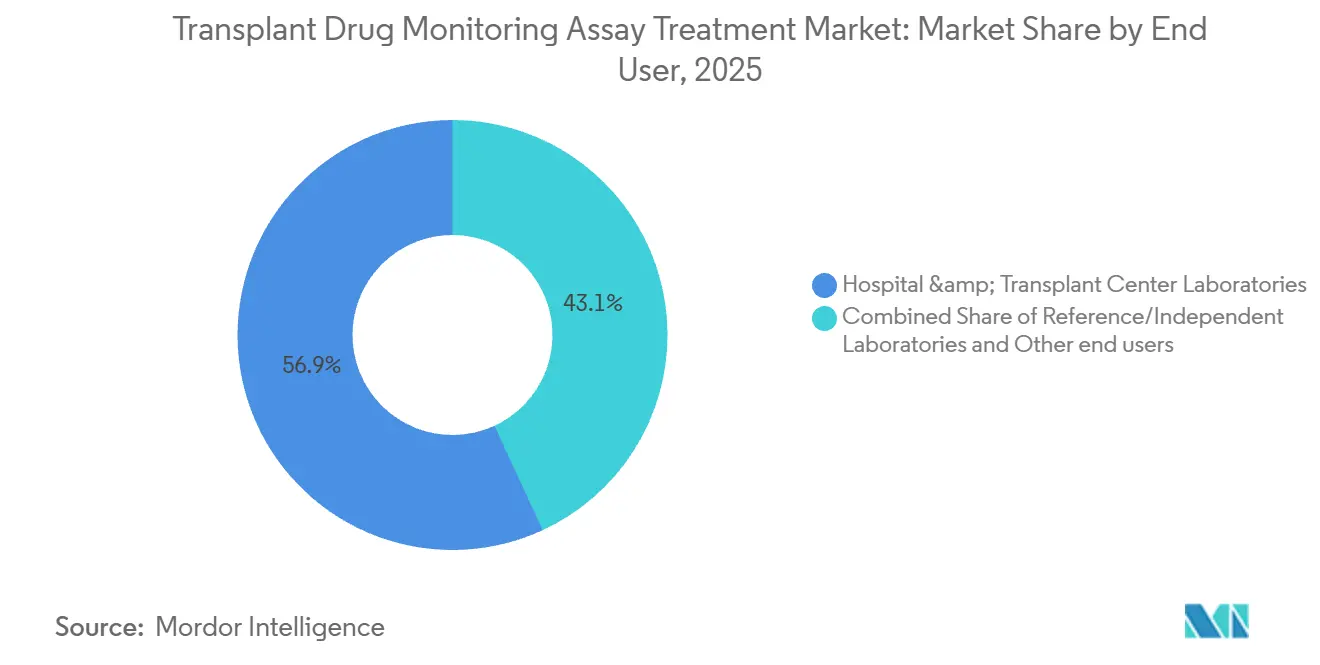

By end user, hospital and transplant center laboratories accounted for 56.89% of 2025 demand, while reference laboratories are projected to grow at 11.3% CAGR through 2031.

By transplant type, kidney procedures accounted for 48.22% of 2025 assay volumes, while hematopoietic stem cell transplant testing is projected to expand at 10.8% CAGR through 2031.

By geography, North America retained 51.11% share in 2025, while Asia Pacific is projected to grow at 11.5% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Transplant Drug Monitoring Assay Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising organ transplant volumes sustain TDM demand | +2.8% | Global, with concentration in North America, Europe, Asia Pacific | Medium term (2-4 years) |

| Guideline-mandated monitoring of calcineurin inhibitors | +2.1% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Broader analyzer menus and kit availability for immunoassays | +1.5% | Global | Short term (≤ 2 years) |

| Standardized, kit-based LC-MS/MS improves adoption and comparability | +2.4% | North America, Europe, APAC core | Medium term (2-4 years) |

| AI/Bayesian dosing workflows embedding TDM in clinical decision support | +1.2% | North America, Europe | Long term (≥ 4 years) |

| Microsampling and home-based collections increase test accessibility | +0.7% | Europe, APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Organ Transplant Volumes Sustain TDM Demand

Global solid organ transplant activity reached 173,727 in 2024, a 2% increase from 2023, and kidney and liver volumes continued to represent the largest procedure cohorts that require lifelong therapeutic drug monitoring of immunosuppressants. In the United States, more than 48,000 transplants were performed in 2024, and the national waiting list remained above 103,000 candidates, which signals durable demand for consistent drug exposure monitoring across pre- and post-transplant phases [1]Donate Life America, “National Donate Life Month 2025 Donation & Transplantation Statistics". Spain led deceased organ donation at 53.93 donors per million people, while Turkey and Saudi Arabia each exceeded 50 living donors per million, highlighting regional differences that shape testing volumes and platform mix across health systems. Hematopoietic stem cell transplant programs have raised testing frequency in the early post-transplant period, which intensifies tacrolimus trough-level monitoring to manage graft-versus-host disease risk in allogeneic recipients. A 2025 study showed that maintaining tacrolimus time-in-therapeutic-range at or above 75.9% during weeks 1 to 4 post-HSCT correlated with reduced Grade II-III acute GVHD, reinforcing the need for precise and frequent trough monitoring in critical early windows.

Guideline-Mandated Monitoring of Calcineurin Inhibitors

Tacrolimus trough monitoring is embedded in care pathways for solid organ and stem cell transplantation, and national protocols specify routine frequency in the first 6 months to avoid underexposure or overexposure that can lead to rejection or toxicity. A 2025 multi-center comparison reported clinically relevant discrepancies of 28% within the first 3 months and 37% after 3 months when comparing immunoassay and LC-MS/MS tacrolimus results in the same patients, which underscores why confirmatory strategies and consistent method use for each patient matter in practice [2]Ivo N. SahBandar et al., “Comparative Evaluation of Five Tacrolimus Assays in Transplant Recipients,” Frontiers in Transplantation". Modern LC-MS/MS methods have shown systematic negative bias of roughly 7.5% to 18.7% relative to immunoassays in certain implementations, which can create silent underdosing if therapeutic targets calibrated to older immunoassays are applied unchanged to mass-spectrometry results. NHS Scotland guidance sets monthly tacrolimus trough levels for the first 6 months with dose adjustments maintained under specialist oversight, which helps reduce misinterpretation in primary care and standardizes frequency during dose stabilization. Regulatory progress has reduced complexity in clinical labs as automated LC-MS/MS platforms moved into moderate-complexity CLIA categorization and IVDR Class C certifications expanded kit availability, which helps align workflows with guideline adherence at scale. Commercially harmonized immunoassays remain acceptable for routine monitoring when paired with backup LC-MS/MS for discordant cases, as highlighted by recent peer-reviewed assessments of assay bias and calibration practices.

Broader Analyzer Menus and Kit Availability for Immunoassays

Major manufacturers expanded menus between 2024 and 2026 so that tacrolimus, cyclosporine, sirolimus, and everolimus can be consolidated on single immunoassay platforms that fit routine hospital laboratory workflows. Abbott’s recent evaluations reported low bias for tacrolimus on the Alinity i platform compared with LC-MS/MS, which improves confidence at lower trough targets commonly used in CNI-minimization regimens. Siemens’ affinity chrome-mediated immunoassay on Dimension systems can deliver tacrolimus results in under 15 minutes at a 1 ng/mL limit of quantification, although heterophilic antibody interference calls for clear reflex pathways when unexpected values appear. Roche launched an automated cobas Mass Spec solution in December 2024 and expanded Ionify reagent packs to 39 therapeutic drug monitoring and hormone tests by December 2025, which provides a bridge between immunoassay-like workflows and mass-spec specificity for routine labs. Shimadzu received IVDR Class C certification in November 2025 for its DOSIMMUNE LC-MS/MS kit that quantifies four key immunosuppressants with rapid analysis, which strengthens standardized options under the EU’s IVDR regime.

Standardized, Kit-Based LC-MS/MS Improves Adoption and Comparability

Traceable calibrators and integrated kits are narrowing method-to-method variability in mass-spectrometry testing, which helps clinicians interpret results more consistently across sites. Waters’ MassTrak calibrators reported strong accuracy and precision across tacrolimus, cyclosporine, sirolimus, and everolimus when used with UPLC triple-quadrupole systems, which supports harmonization across laboratories that deploy a standardized workflow. Reducing a 2 ng/mL discrepancy around a 10 ng/mL target can be clinically meaningful, since dose changes are often triggered in narrow windows and false adjustments can cascade into rejection or toxicity. Kit-based solutions like Shimadzu DOSIMMUNE bundle calibrators, internal standards, mobile phases, and columns, which removes method development steps and makes LC-MS/MS more accessible to hospital labs. Roche’s Ionify reagent packs automate sample preparation and chromatography on the cobas Mass Spec solution, and the platform’s menu breadth has extended across immunosuppressants and antibiotics for consistent, automated TDM. Cross-vendor interlaboratory variability in 2025 showed proportional biases ranging between roughly 7.5% and 18.7% across LC-MS/MS implementations, which underscores why end-to-end kits can stabilize performance as adoption rises.

Restraints Impact Analysis*

| Restraint (as applicable in title case) | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Immunoassay cross-reactivity or bias versus LC-MS/MS specificity | -1.6% | Global | Short term (≤ 2 years) |

| Skilled-staff shortages and LC-MS/MS complexity slow adoption | -1.1% | APAC, Middle East & Africa, Latin America | Medium term (2-4 years) |

| Belatacept and other non-TDM regimens reduce test volumes in select centers | -0.4% | North America, Europe (select transplant centers) | Long term (≥ 4 years) |

| Inter-method variability and lack of harmonized ranges hinder switching | -0.9% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Immunoassay Cross-Reactivity or Bias Versus LC-MS/MS Specificity

Certain tacrolimus immunoassays can cross-react with metabolites, which can inflate results under specific clinical conditions and necessitate reflex testing when clinical context and measured levels diverge. Comparative evaluations have reported proportional positive bias for different immunoassays, although newer platforms such as Abbott Alinity i have reduced bias closer to LC-MS/MS benchmarks, which improves reliability at lower trough targets. Operational assessments from high-volume labs show that switching from LC-MS/MS to a modern immunoassay can cut turnaround time while maintaining analytical agreement for most samples, though a meaningful minority still fall outside LC-MS/MS confidence intervals and need follow-up. Early post-transplant dose titration intervals amplify the clinical risk from biased readings because physicians often act on narrow deltas in short time frames. LC-MS/MS resolves metabolite interference but introduces its own method setup complexity and interlaboratory variability, which reinforces the value of standardized kits and calibrators when results drive frequent dosing changes.

Skilled-Staff Shortages and LC-MS/MS Complexity Slow Adoption

High-complexity LC-MS/MS historically required specialist operators for method development, troubleshooting, and compliant data management, which concentrated capacity in reference laboratories and large academic centers. Manual extraction and batch processing can extend turnaround time to several hours in stat situations, which reduces clinical utility for same-day dose adjustments when compared with immunoassays. Automation is narrowing this gap as integrated mass-spectrometry platforms reduce hands-on time and deliver faster sample-to-result cycling in routine labs for multiple TDM analytes. IVDR-certified kits further accelerate verification by providing validated chromatography and mass-spectrometer parameters out of the box, which helps smaller centers avoid lengthy method development and validation cycles. The trade-off is reduced flexibility to add new analytes outside the vendor’s validated menu, which can slow adoption of niche drugs until vendor updates are available. Workforce limitations and infrastructure gaps in emerging markets heighten these barriers, which shape a gradual shift from reference-lab outsourcing to hybrid models that balance immunoassay stat capacity with centralized LC-MS/MS.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug/Analyte Class: Calcineurin Inhibitors Anchor Use, mTOR Inhibitors Gain

Calcineurin inhibitors accounted for 45.08% of the Transplant Drug Monitoring Assay Treatment market size in 2025 based on their first-line role in kidney, liver, heart, lung, and stem cell transplantation protocols. Tacrolimus remains the backbone of immunosuppression in kidney recipients and is used in more than 90% of cases in the United States, which translates into high assay frequency from the immediate post-transplant period to long-term maintenance [3]Preeti Patel and Preeti Rout, “Tacrolimus,” StatPearls, ncbi.nlm.nih.gov". The higher frequency of early-life monitoring and the need for narrow therapeutic ranges in select organs keep testing intense, which supports the leading share of calcineurin inhibitors within the overall mix. Lower bias on next-generation immunoassays has improved alignment with LC-MS/MS near standard tacrolimus targets, which sustains hospital lab reliance on fast immunoassays with selective reflex to LC-MS/MS when results and the clinical picture conflict. CNI-minimization protocols that target 3 to 5 ng/mL in the maintenance phase favor LC-MS/MS precision for dose titration at the low end of the range, which elevates the role of mass spectrometry without displacing the first-line status of CNIs.

mTOR inhibitors are projected to grow at 11% CAGR through 2031, supported by conversion strategies that protect renal function in patients with CNI-related nephrotoxicity. Evidence from clinical studies has documented renal function gains after sirolimus conversion in select patient profiles, which underpins protocolized switches in routine care for stable recipients. Everolimus paired with reduced-dose tacrolimus achieved lower viral infection rates in trials while maintaining eGFR outcomes, which broadens mTOR inhibitor appeal in high-viral-risk settings. Discontinuation rates due to adverse events and surgical wound concerns continue to limit adoption, yet the therapy class remains on a positive trajectory as clinicians tailor regimens by renal risk and infection history. Antimetabolites such as mycophenolic acid remain co-therapies without routine TDM, which caps their direct impact on assay volume. The Transplant Drug Monitoring Assay Treatment industry reflects these therapy shifts through rising complexity of CNI minimization and mTOR conversion protocols, which favor LC-MS/MS for low-range quantification and method consistency over time.

By Technology: Immunoassays Dominate Routine Workflows, LC-MS/MS Expands Standardized Footprint

Immunoassay platforms held 56.13% share of the Transplant Drug Monitoring Assay Treatment market size in 2025, as hospital labs prioritize 15 to 60 minute turnaround times and fully automated operations that align with chemistry workflows. Bias performance has improved on newer systems, which reduces the need for frequent confirmatory testing and supports rapid dose adjustment cycles during the early post-transplant period. Siemens’ ACMIA implementation delivers sub-15-minute results at 1 ng/mL sensitivity, which positions it as a practical option for stat testing in centers that maintain immunoassay-first pathways. Pre-analytical and interference management protocols remain necessary to address heterophilic antibodies and rare cross-reactivity events, which labs mitigate by retesting unexpected values with LC-MS/MS when appropriate.

LC-MS/MS is projected to expand at 11.3% CAGR through 2031 as standardized, kit-based solutions reduce method development and verification workloads. Roche’s cobas Mass Spec solution, launched in December 2024, and subsequent menu expansions across immunosuppressants and antibiotics brought automated mass spectrometry into routine labs that historically relied on immunoassays, which increases access to reference-quality specificity. Shimadzu’s IVDR Class C DOSIMMUNE kit reduces total analysis time per sample while bundling all reagents and validated methods, which further shortens the path from purchase to clinical go-live. Calibrators with traceability from global metrology frameworks enhance cross-site comparability, which strengthens the long-term case for LC-MS/MS when therapeutic targets are narrow or trending lower in maintenance protocols. The Transplant Drug Monitoring Assay Treatment industry is therefore balancing fast-turnaround immunoassays for stat needs with LC-MS/MS for confirmatory and low-range targets, which supports a hybrid testing model across hospital and reference laboratories.

By End User: Hospital Labs Lead Volumes, Reference Labs Capture Complex Testing

Hospital and transplant center laboratories accounted for 56.89% of total volumes in 2025 due to the clinical need for fast tacrolimus troughs in the immediate post-transplant period. Integrated reporting and clinical decision support are improving operational efficiency because results feed directly into predefined dose-titration rules in the EHR, which has been shown to increase the share of patients reaching target exposure early after transplantation. Smaller transplant programs maintain immunoassay-based stat capacity while reflexing questionable or ultra-low concentrations to mass spectrometry, which preserves same-day dose decision capability and keeps complex analyses centralized.

Reference and independent laboratories are projected to grow at 11.3% CAGR through 2031 as batch LC-MS/MS workflows remain cost-effective for regional networks and as hospitals outsource confirmatory testing under shared service agreements. High-throughput operations demonstrate that modern immunoassays can cut turnaround time versus manual LC-MS/MS while maintaining acceptable agreement for most cases, though a share of samples still requires confirmation. Academic and research laboratories continue to validate emerging analytes and novel exposure metrics, which includes intra-lymphocytic tacrolimus measurements that track closer to immunologic risk but are not ready for routine deployment due to workflow complexity. Across end users, the Transplant Drug Monitoring Assay Treatment market supports a complementary mix of on-site stat testing and outsourced confirmatory LC-MS/MS, which aligns with clinical urgency and cost optimization.

By Transplant Type: Kidney Dominates, HSCT Accelerates

Kidney transplantation accounted for 48.22% of 2025 assay volumes and remains the cornerstone of solid organ activity globally, which translates into the largest long-term maintenance cohort requiring routine monitoring. Global transplant counts increased in 2024, which adds to the installed base of recipients in the maintenance phase and supports sustained assay demand through the forecast period. Early-phase monitoring intensity is higher in liver recipients, while heart and lung recipients often maintain higher tacrolimus targets in the first months to manage rejection risk, which keeps testing clinically critical despite smaller procedure volumes in those organs.

Hematopoietic stem cell transplantation is projected to expand at 10.8% CAGR through 2031, supported by growth in allogeneic procedures for hematologic diseases and increasing adoption of haploidentical approaches. Tacrolimus-based graft-versus-host disease prophylaxis requires frequent trough monitoring through engraftment and the first 100 days, which can generate high assay counts per patient in the first year. Maintaining a high time-in-therapeutic-range in weeks 1 to 4 has been associated with lower rates of moderate acute GVHD, which underpins calls for precise monitoring and protocolized titration early after HSCT. Emerging protocols using post-transplant cyclophosphamide have shown better outcomes at higher tacrolimus exposure in week 3 and 4 windows, which extends the role of TDM across conditioning and donor types. The Transplant Drug Monitoring Assay Treatment industry is therefore shaped by a large kidney recipient base and a fast-growing HSCT segment where frequent, low-latency assays influence early outcomes.

Geography Analysis

North America retained 51.11% share in 2025 as high transplant volumes, broad hospital lab capacity, and active adoption of automated LC-MS/MS platforms reinforced demand for both immunoassay and mass-spec testing. The United States performed more than 48,000 transplants in 2024, and a national waiting list exceeding 103,000 candidates sustains ongoing demand for precise tacrolimus monitoring across the care continuum. FDA-cleared immunoassays and expanding automated mass-spec menus introduced by major diagnostics companies have improved analytical performance and workflow standardization, which reduces the operational burden on clinical labs. Studies implementing model-informed precision dosing in this region have shown better early target attainment with EHR-embedded algorithms, which aligns with the region’s emphasis on interoperability and clinical decision support.

Europe accounted for a significant portion of global revenues in 2025 and continues to evolve under the EU IVDR regime, which designates immunosuppressant tests as Class C and raises validation rigor. IVDR-certified LC-MS/MS kits and CE-marked automated mass-spectrometry systems have broadened standardized options for EU laboratories, which supports more consistent performance across sites. Spain leads deceased donation rates in the region, which helps sustain higher per-capita transplant activity and the associated need for reliable TDM at transplant centers nationwide. Guidance from European transplant societies balances cost considerations with accuracy by recommending LC-MS/MS for lower tacrolimus targets while preserving immunoassays for standard ranges, which reinforces hybrid testing strategies in clinical practice.

Asia Pacific is projected to grow at 11.5% CAGR through 2031 as transplant programs scale and governments broaden access to post-transplant monitoring. Infrastructure expansion and centralized reference laboratory networks support the roll-out of LC-MS/MS capacity in urban centers, while immunoassay-first models remain the norm for stat testing in most hospitals. Microsampling adoption studies in Europe and Asia point to strong patient preference and enable ambient shipping, which can extend reach into rural and remote settings even when cold-chain logistics are constrained[4]Solveig Thiele and Jonathan W. Martin, “Blood Microsampling Devices,” Environmental Science & Technology Letters". In the Middle East, high-volume transplant hospitals are deploying automated LC-MS/MS to strengthen analytical performance and reduce reliance on manual methods, which signals a region-wide shift toward standardized platforms where resources permit. In South America, public insurance coverage for select TDM tests at major urban hospitals supports access, while regional reference labs absorb more complex testing as hospitals maintain immunoassay stat capacity. Across regions, the Transplant Drug Monitoring Assay Treatment market reflects a consistent pattern of hybrid testing adoption, anchored by fast immunoassays near the bedside and standardized LC-MS/MS for confirmatory and low-range targets.

Competitive Landscape

The Transplant Drug Monitoring Assay Treatment market shows moderate consolidation, with four global diagnostics leaders collectively holding about 60% share in 2025 through combined immunoassay and LC-MS/MS portfolios, broad test menus, and long-term service contracts. Roche expanded its presence with the launch of the cobas Mass Spec solution in December 2024 and subsequent menu growth, which enabled routine laboratories to bring automated mass-spectrometry specificity into core operations. Abbott integrated improved tacrolimus immunoassay performance into the Alinity ecosystem, which strengthens procurement synergies across chemistry and immunoassay lines in consolidated hospital networks. Siemens Healthineers emphasized automated ACMIA workflows on Dimension systems, which eliminate manual pretreatment and support rapid turnaround times in high-throughput labs. Thermo Fisher extended into precision medicine with a pharmacogenetic LDT for CYP3A5, which supports genotype-informed initial tacrolimus dosing and complements ongoing therapeutic drug monitoring.

Mid-tier specialists compete on LC-MS/MS capital equipment, standardized reagent kits, and calibrators, which underpin reference-laboratory and hub-and-spoke deployment models. Shimadzu’s DOSIMMUNE kit obtained IVDR Class C certification, which shortens time-to-validation and enhances comparability across EU sites that adopt its standardized workflow. Waters advanced adjacent analytical capability with a new extended-range MALS detector for UHPLC and UPLC workflows that can accelerate characterization of large molecules and delivery systems, which may benefit academic medical centers and biopharmaceutical hubs that co-locate transplant programs with advanced analytics. Calibrator and quality-control vendors continue to promote traceability and cross-site reproducibility for immunosuppressant assays, which supports interlaboratory comparability and mitigates method-switching risks in longitudinal patient care.

Strategic moves across leading players center on standardization, automation, and decision support. Roche scaled the Ionify reagent pack menu to include antibiotic drug monitoring under a CE Mark, which establishes a broad automated TDM test menu on a single platform for routine laboratories. Shimadzu’s integrated LC-MS/MS kit reduces workload and accelerates IVDR-compliant adoption, which helps smaller and mid-sized labs implement mass spectrometry with fewer staffing constraints. Thermo Fisher’s genotype-informed LDT addresses the starting dose challenge for tacrolimus and aligns with the clinical shift toward MIPD-assisted titration, which reinforces a precision medicine trajectory across transplant centers. As a result, the Transplant Drug Monitoring Assay Treatment market is evolving from product-only differentiation toward integrated ecosystems that bundle analyzers, standardized kits, calibrators, and clinical software.

Transplant Drug Monitoring Assay Treatment Industry Leaders

Abbott

Siemens Healthineers

Thermo Fisher Scientific

Waters Corporation

F. Hoffmann‑La Roche Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Thermo Fisher launched the TacroType Pharmacogenetic Test as a CLIA LDT to identify CYP3A5 genotype for tacrolimus dose optimization at initiation.

- December 2025: Roche secured a CE Mark for an antibiotic drug monitoring reagent pack, expanding the cobas Mass Spec Ionify portfolio to 39 IVD tests that include immunosuppressants and antibiotics

- November 2025: Shimadzu obtained IVDR Class C certification for the DOSIMMUNE LC-MS/MS Immunosuppressant Analysis Kit to quantify tacrolimus, cyclosporine A, everolimus, and sirolimus in whole blood with rapid analysis.

- December 2024: Roche launched the cobas Mass Spec solution with CE Mark for the cobas i 601 analyzer and the first Ionify reagent pack for steroid hormones, with plans to expand to TDM and drugs-of-abuse testing.

Global Transplant Drug Monitoring Assay Treatment Market Report Scope

| Calcineurin inhibitors |

| mTOR inhibitors |

| Antimetabolites |

| Immunoassay |

| LC-MS/MS |

| Hospital & Transplant Center Laboratories |

| Reference/Independent Laboratories |

| Academic & Research Laboratories |

| Kidney |

| Liver |

| Heart |

| Lung |

| Hematopoietic Stem Cell Transplant (HSCT) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| United States | |

| Canada | |

| Mexico | |

| Germany | |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug/Analyte Class | Calcineurin inhibitors | |

| mTOR inhibitors | ||

| Antimetabolites | ||

| By Technology | Immunoassay | |

| LC-MS/MS | ||

| By End User | Hospital & Transplant Center Laboratories | |

| Reference/Independent Laboratories | ||

| Academic & Research Laboratories | ||

| By Transplant Type | Kidney | |

| Liver | ||

| Heart | ||

| Lung | ||

| Hematopoietic Stem Cell Transplant (HSCT) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| United States | ||

| Canada | ||

| Mexico | ||

| Germany | ||

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the Transplant Drug Monitoring Assay Treatment market size and growth outlook to 2031?

The Transplant Drug Monitoring Assay Treatment market size is USD 534.57 million in 2026 and is projected to reach USD 891.59 million by 2031 at a 10.8% CAGR.

Which segment leads by share within the Transplant Drug Monitoring Assay Treatment market?

Calcineurin inhibitors lead by share with 45.08% in 2025, supported by guideline-embedded tacrolimus monitoring across major transplant types.

Which technology is growing the fastest within the Transplant Drug Monitoring Assay Treatment market?

LC-MS/MS is the fastest-growing technology with a projected 11.3% CAGR through 2031, driven by standardized kits and automated mass-spectrometry platforms.

Which end-user group is expanding fastest in the Transplant Drug Monitoring Assay Treatment market?

Reference and independent laboratories are projected to grow at 11.3% CAGR as hospitals maintain immunoassay stat capacity and outsource confirmatory LC-MS/MS.

Which region shows the strongest growth potential through 2031?

Asia Pacific is projected to post the fastest growth at 11.5% CAGR, supported by scaling transplant programs and expanding laboratory infrastructure.

Which transplant type is expected to increase testing frequency the most?

Hematopoietic stem cell transplant testing is projected to expand at 10.8% CAGR due to intensive early-phase monitoring needs and growing allogeneic procedure volumes.

Page last updated on: