Topical Wound Agents Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 2.07 Billion |

| Market Size (2031) | USD 2.95 Billion |

| Growth Rate (2026 - 2031) | 7.33% CAGR |

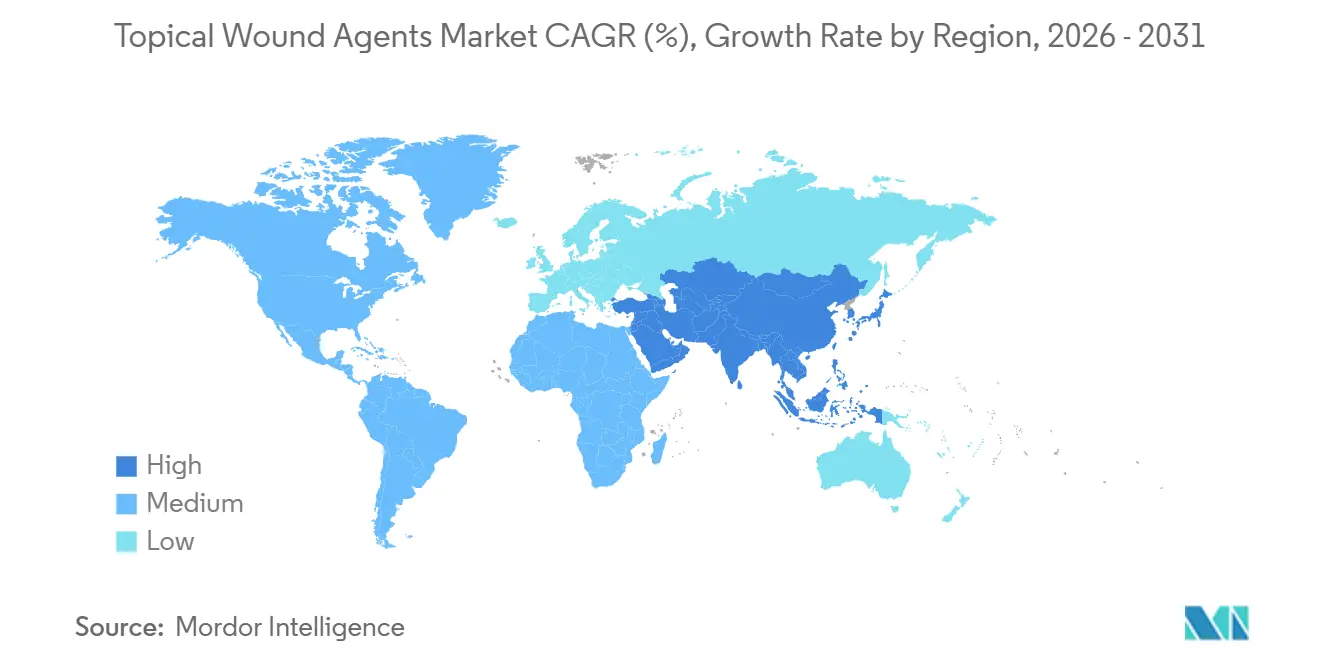

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Topical Wound Agents Market Analysis by Mordor Intelligence

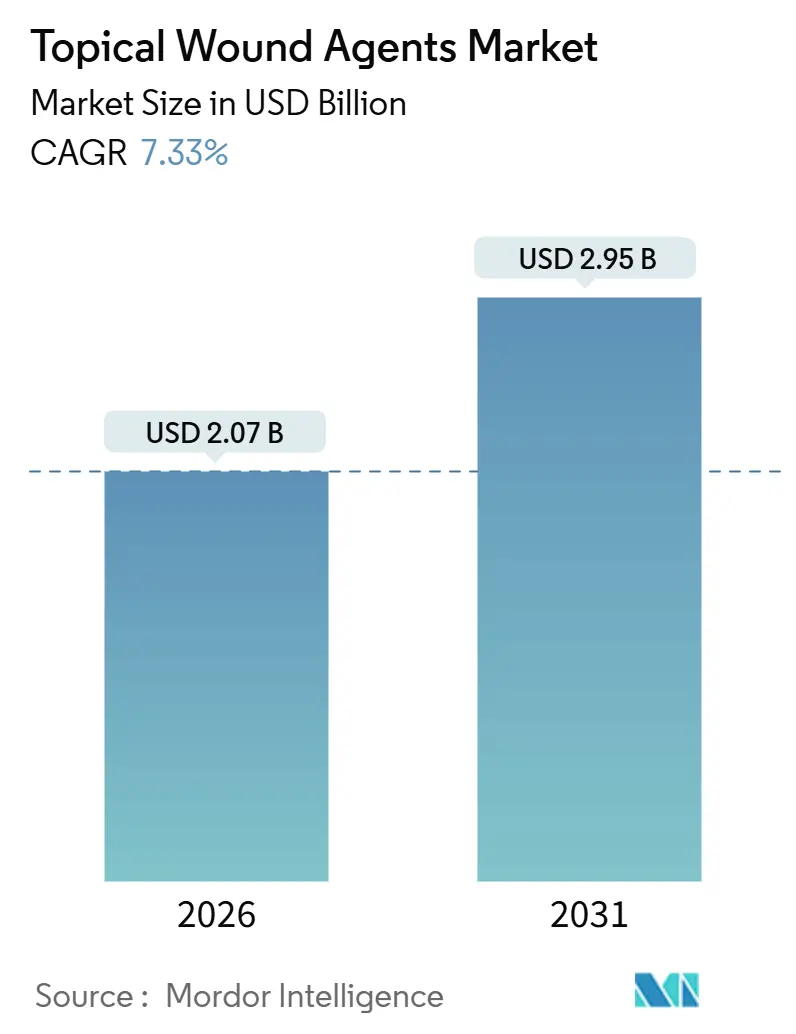

The Topical Wound Agents Market size is estimated at USD 2.07 billion in 2026, and is expected to reach USD 2.95 billion by 2031, at a CAGR of 7.33% during the forecast period (2026-2031).

The growth in the market blends faster approvals for nanotech antiseptics with stricter antimicrobial-stewardship limits on legacy topical antibiotics, nudging buyers toward silver, iodine, and recombinant biologic options.[1]Food and Drug Administration, “Antimicrobial Stewardship Programs in Hospitals,” FDA, fda.gov Providers are also aligning formularies with diabetic-ulcer evidence that supports growth-factor gels able to curb amputation rates, while hospitals favor no-touch sprays that meet infection-control targets set after 2024 CDC hand-hygiene audits. E-pharmacy laws now active in 28 U.S. states let pharmacists ship prescription-strength debriders directly to patients, accelerating direct-to-consumer uptake.[2]Centers for Medicare & Medicaid Services, “National Health Expenditure Data,” CMS, cms.gov Asia-Pacific stimulus programs that subsidize domestic production of silver sulfadiazine and collagenase are driving regional price competition and underpin the fastest geographic CAGR. All told, payers, regulators, and manufacturers are reshaping product portfolios toward multi-mechanism antimicrobials, enzymatic options, and value-priced generics, themes that will continue to guide the topical wound agents market through 2031.

Key Report Takeaways

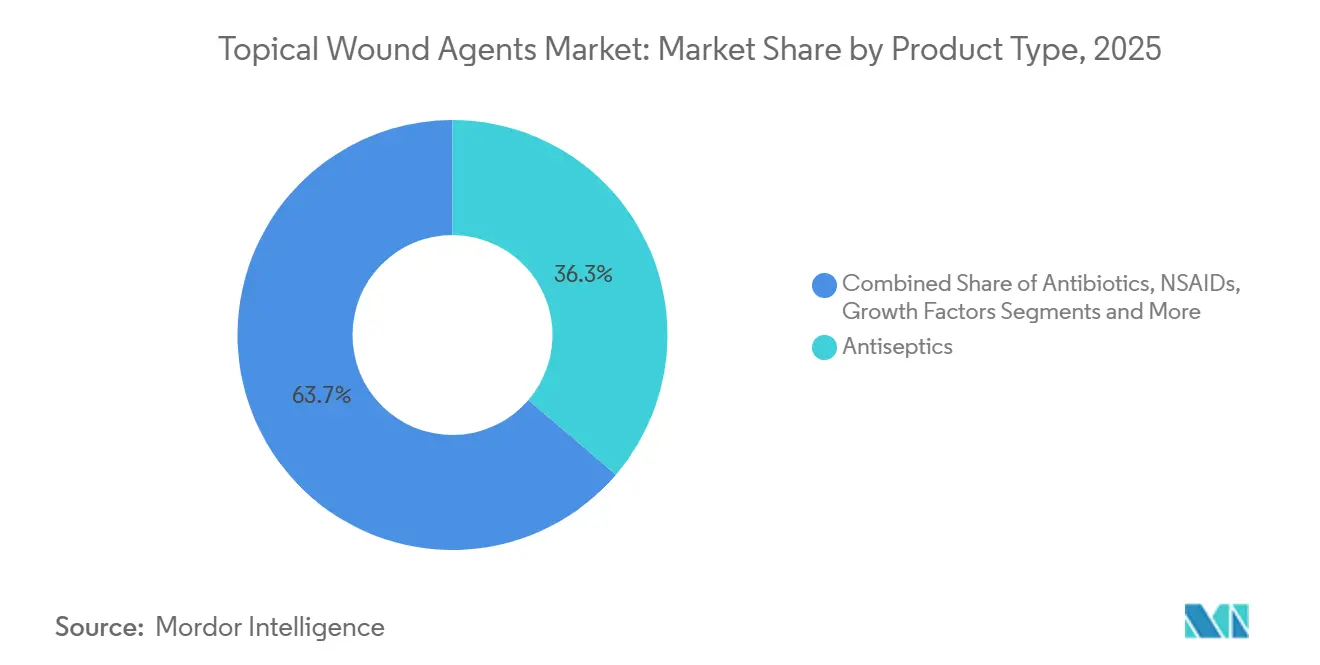

- By product type, antiseptics led with 36.25% revenue in 2025, while growth factors are forecast to climb at an 11.67% CAGR to 2031.

- By dosage form, gels secured 42.56% of topical wound agents market share in 2025 and sprays are set to grow the quickest at 12.04% CAGR through 2031.

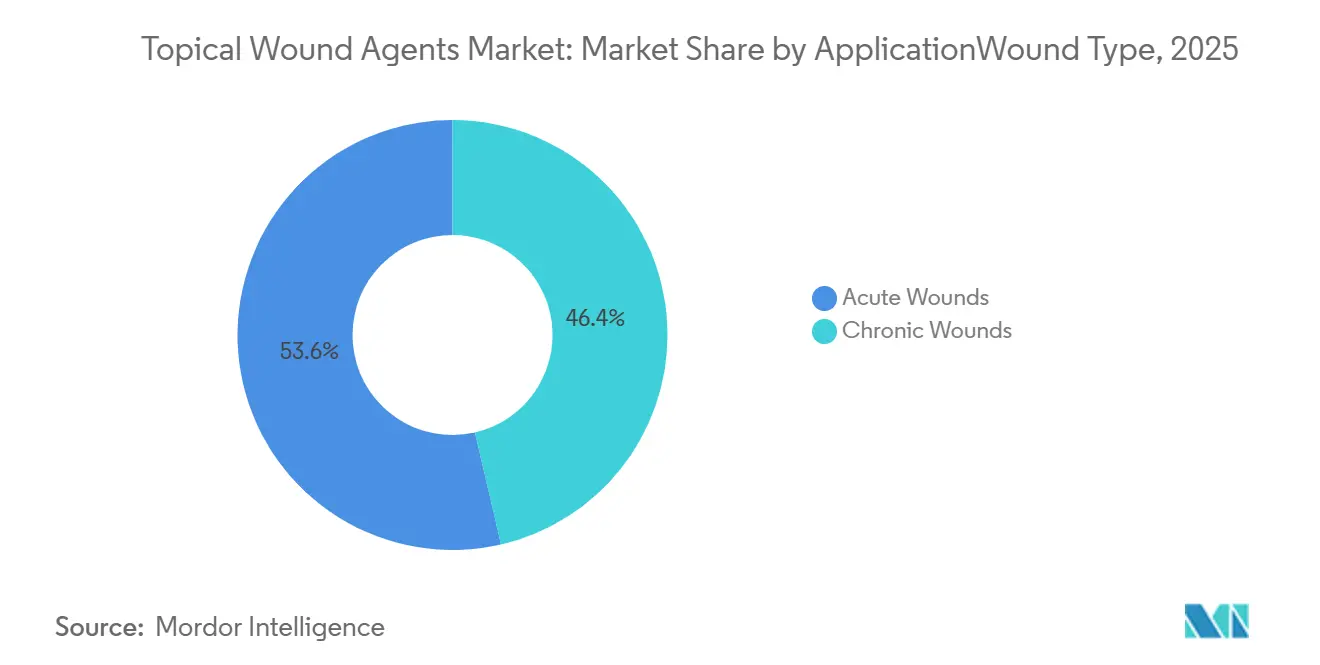

- By application, acute wounds accounted for 53.62% of 2025 value, whereas chronic wounds treatments will register the steepest 10.55% CAGR to 2031.

- By distribution channel, hospital pharmacies held 44.25% share in 2025, yet online pharmacies will expand at an 11.95% CAGR on the back of new e-pharmacy licenses.

- By geography, North America contributed 37.26% of 2025 revenue, while Asia-Pacific will post the highest 9.57% regional CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Topical Wound Agents Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic wounds | +1.8% | Global, acute in North America, Europe, urban Asia-Pacific | Long term (≥ 4 years) |

| Growing volume of surgical and traumatic injuries | +1.2% | North America, Europe | Medium term (2-4 years) |

| Expansion of home-healthcare and self-treatment channels | +1.5% | North America, Europe, metro Asia-Pacific | Medium term (2-4 years) |

| Tele-enabled remote wound-monitoring platforms | +0.9% | North America, Western Europe | Short term (≤ 2 years) |

| Nanotech-enabled antimicrobial formulations with fast-track approvals | +1.3% | FDA and EMA markets, spillover to ASEAN & LATAM | Short term (≤ 2 years) |

| Asia-Pacific localization incentives boosting domestic manufacturing | +1.1% | India, China, South Korea, Vietnam | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Wounds

More people are living longer with diabetes and vascular disease, and that yields a steady flow of hard-to-heal ulcers that demand complex topical regimens. In 2024, 37 million adults had an active diabetic foot ulcer, and half of all non-traumatic amputations occurred in diabetic patients. Rural U.S. counties typically see 18-24 months between ulcer onset and a first wound-clinic visit, so a small lesion often progresses into a deep infection requiring enzymatic debriders and growth-factor gels. CDC data show that seniors make up 29% of diagnosed diabetics yet drive 48% of advanced topical-agent spending because comorbidities heighten dosage intensity.[3] Centers for Disease Control and Prevention, “National Diabetes Statistics Report,” CDC, cdc.gov At-home pressure-ulcer care is rising with Medicare discharges, lifting demand for spray antiseptics that caregivers can apply without sterile technique. Together these factors add consistent lift to the topical wound agents market.

Growing Volume of Surgical and Traumatic Injuries

Roughly 50 million inpatient surgeries occur yearly in the United States, and up to 2.5 million of these develop surgical-site infections that require topical antimicrobials. Hospital formularies are replacing triple-antibiotic ointments with silver-nanoparticle gels in response to FDA stewardship guidance that discourages broad empiric antibiotic use. Road-traffic injuries further expand demand in Asia-Pacific and Africa, where vehicle deaths remain high relative to car ownership. Burn units increasingly discharge partial-thickness cases on day 1 because silver-sulfadiazine creams and nanosilver gels can be self-managed at home, moving volumes from inpatient settings to retail and online channels. All told, surgery and trauma are dependable feeders for the topical wound agents market.

Expansion of Home-Healthcare and Self-Treatment Channels

Medicare home-health spending hit USD 21.3 billion in 2024, and topical agents ranked third among skilled-nursing services. Payers save about USD 15,000 for every avoided readmission, so they endorse caregiver-friendly products such as foams and sprays. Newly harmonized state e-pharmacy rules enable pharmacists to consult by video and mail prescription collagenase ointment directly to patients. Spray delivery minimizes application errors by non-professionals, a key feature as more chronic-wound patients recover at home. These trends jointly widen the end-user base for the topical wound agents market.

Tele-Enabled Remote Wound-Monitoring Platforms

Medicare clarified in 2024 that remote wound monitoring qualifies for RPM reimbursement when data are collected at least 16 days per month. Clinicians can now escalate therapy within 48 hours of seeing stalled healing online rather than waiting weeks for an office visit. A Diabetes Care trial reported 34% faster healing when therapy adjustments were guided remotely versus standard care. Academic medical centers are early adopters, but fee-for-service clinics lag because fewer outpatient visits mean fewer billable events. Even so, the ability to fine-tune topical regimens in real time underpins better outcomes and lifts recurring demand for higher-value formulations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced formulations | −0.8% | North America, Europe | Medium term (2-4 years) |

| Stringent and lengthy regulatory approval pathways | −0.6% | North America, Europe, Japan | Long term (≥ 4 years) |

| Escalating antimicrobial-resistance stewardship limits | −0.7% | Global, strictest in EU and U.S. | Short term (≤ 2 years) |

| Supply-chain volatility for bio-polymer feedstocks | −0.5% | Europe, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Formulations

Becaplermin gel lists at more than USD 1,800 for 15 g, yet Medicare caps reimbursement at USD 1,200–1,400, so clinics either absorb 30% of the cost or postpone use until cheaper agents fail. November 2024 coverage decisions further removed payment for many biologic skin substitutes, making step-therapy around collagenase ointment a new norm. Generic silver creams now sell for USD 3 in India, widening the price gulf between antiseptics and biologics. Absent comparable outcome data, payers resist high-ticket items, which tempers overall topical wound agents market growth.

Stringent and Lengthy Regulatory Approval Pathways

FDA stewardship guidance now demands sub-5% systemic absorption plus in-vitro durability against resistant organisms, requirements older triple-antibiotic ointments cannot meet without new trials. Europe’s 2024 update to bacterial-infection guidelines obliges sponsors to run 500-patient resistance-monitoring studies, adding USD 2-3 million in post-market work. MDR 2017/745 also raised the bar for combination dressings, stretching launch timelines by up to a year. These hurdles deter incremental innovation and slow the introduction of new entrants into the topical wound agents industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Biologics Gain Momentum While Antiseptics Dominate

The topical wound agents market size for antiseptics was anchored by a 36.25% share in 2025, yet growth factors will post an 11.67% CAGR to 2031, the swiftest among all categories. Hospital formularies carry antiseptics as first-line because they cover broad microbial spectra, but accountable-care organizations increasingly reimburse growth factors once debriders or antiseptics stall healing. Becaplermin’s 15% absolute uplift in wound-closure rates supports its premium even under step-therapy rules, though utilization sits at only 8–10% of eligible cases due to cost hurdles.

Antibiotics held roughly one-fifth of 2025 revenue, but new FDA stewardship demands mean culture confirmation precedes use, stretching initiation by two days. Enzymatic debriders—chiefly collagenase—control 12–14% share and will grow near 10% CAGR as payers view them as cost-effective alternatives to pricey biologics. NSAIDs remain a small niche, checked by 2024 label warnings on fixed drug eruptions. Honey, hypochlorous solutions, and nitric-oxide gels round out the portfolio at a combined low-teens share but attract R&D for their biofilm-disruption properties.

By Dosage Form: Sprays Leap Ahead Under Infection-Control Norms

Gels delivered 42.56% of topical wound agents market share in 2025 and remain popular for moisture balance and dressing compatibility. Yet sprays will sprint at a 12.04% CAGR through 2031 because they avoid direct hand-to-wound contact, an asset after CDC audits showed only 68% hand-hygiene compliance in surgery suites. Uniform aerosol coverage also trims dosing variability and empowers self-care for patients with limited dexterity. Creams and ointments, still staples in OTC shelves, compete on price rather than innovation, so volume rises yet revenue lags. Powders and foams serve specialized cavities and exudative wounds, while solutions maintain their role in pre-op prep and irrigation.

By Application/Wound Type: Diabetic Foot Ulcers Propel Chronic Segment

Acute wounds generated 53.62% of 2025 demand, but diabetic-foot-ulcer spending inside the chronic-wound bucket will climb at 10.55% CAGR, the sharpest in the forecast. The International Diabetes Federation warns that diabetes prevalence could hit 643 million adults by 2030. Each amputation drives a 5-year mortality near 45%, so clinicians aim to intervene earlier with enzymatic and growth-factor gels. Pressure-ulcer incidence is falling thanks to hospital protocols, moderating its relative weight. Venous leg ulcers advance modestly as evidence prioritizes compression therapy over drugs, while surgical and traumatic wounds expand in line with procedure volumes but shift usage toward home settings.

By Distribution Channel: E-Pharmacies Reshape Access

Hospital pharmacies commanded 44.25% of 2025 revenue, anchored by post-operative and high-acuity dispensing, yet online pharmacies will grow at 11.95% CAGR as more states adopt standardized e-pharmacy rules. Pew Research found that 42% of U.S. adults 50-64 bought medicines online in 2024, up sharply from two years earlier. Mail delivery of collagenase and growth factors at 15–25% lower out-of-pocket cost is especially attractive to high-deductible plan members. Retail drugstores still move high-volume OTC antiseptics for lacerations, but reimbursement pressure squeezes their prescription margins. Long-term-care and military channels grow in step with institutional census.

Geography Analysis

North America generated 37.26% of global sales in 2025 and should log a 6–7% CAGR to 2031 as Medicare reimbursement caps prompt value hunts. The United States alone captures more than four-fifths of regional revenue, with patchwork payer formularies presenting tactical pricing opportunities. Canada and Mexico add steady, policy-driven growth as they widen coverage for silver creams and collagenase ointment.

Asia-Pacific will outpace every region with a 9.57% CAGR, propelled by PLI subsidies that lower API costs and by China’s Green Channel, which drops approval cycles from 24 to 12 months. Indian-made silver-sulfadiazine now sells for USD 3 domestically, exerting grey-market pressure on imported brands. Japan maintains the highest per-capita consumption in the zone, thanks to universal cover for advanced agents and an aging population.

Europe supplied roughly one-quarter of 2025 revenue and continues to grow at 6–7% CAGR, even though MDR compliance slows launches. Germany leads on the back of statutory insurance, while the United Kingdom shifts guidelines toward nanosilver for burns. Cost-effectiveness committees in France and Italy are capping high-priced biologics, nudging clinicians to enzyme-based therapies. The Middle East, Africa, and South America collectively contribute just under one-tenth of sales but grow near 8–9% CAGR as Saudi Arabia and Brazil modernize hospital formularies.

Competitive Landscape

The topical wound agents market is moderately concentrated. Smith & Nephew’s Santyl still owns about two-thirds of U.S. enzymatic-debridement sales, safeguarded by robust Medicare coverage. Mölnlycke poured USD 15 million into MediWound in March 2025 to co-develop bromelain-based debriders that could halve treatment time compared with collagenase. Generic producers in India and China flood the silver-sulfadiazine segment, aided by FDA fast-track guidance that approved 14 generics in 2024 alone. Patent filings tilt toward delivery-system innovation—spray pumps, sustained-release gels—rather than new APIs, underscoring a shift toward usability and infection control. Quality-management certification under ISO 13485 remains a costly entry barrier, indirectly protecting incumbent share.

Topical Wound Agents Industry Leaders

Smith & Nephew plc

Mölnlycke Health Care AB

Coloplast A/S

ConvaTec Group plc

Solventum

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: BD introduced the CE-marked Surgiphor Surgical Wound Irrigation System across select European countries, offering a ready-to-use solution aimed at debris removal during surgery.

- July 2025: Pelthos Therapeutics began U.S. distribution of Berdazimer (ZELSUVMI) 10.3% gel for molluscum contagiosum in patients aged one year and older.

- June 2025: SolasCure secured FDA Fast-Track Designation for Aurase Wound Gel to treat calciphylaxis ulcers, expediting its clinical-development timeline.

- March 2025: Mölnlycke Health Care invested USD 15 million in MediWound to co-develop bromelain-derived enzymatic therapeutics targeting faster debridement kinetics.

Global Topical Wound Agents Market Report Scope

A topical wound agent is a preparation, such as a cream, gel, spray, or ointment, applied directly to a wound to create an optimal healing environment. It supports debridement, combats infections, and promotes tissue regeneration. These agents are used to manage various wound types, ranging from minor skin issues to chronic ulcers, by providing moisture, antimicrobials, or growth factors.

The Topical Wound Agents Market Report is segmented by Product Type, Dosage Form, Application/Wound Type, Distribution Channel, and Geography. By Product Type, the market is segmented into Antiseptics, Antibiotics, NSAIDs, Growth Factors, Enzymatic Debriders, and Others. By Dosage Form, the market is segmented into Creams, Gels, Sprays, Powders, Ointments, Solutions & Liquids, and Foams & Films. By Application/Wound Type, the market is segmented into Chronic Wounds and Acute Wounds. By Distribution Channel, the market is segmented into Hospital Pharmacies, Retail Pharmacies & Drugstores, Online Pharmacies, and Others. By Geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| Antiseptics |

| Antibiotics |

| NSAIDs |

| Growth Factors |

| Enzymatic Debriders |

| Others |

| Creams |

| Gels |

| Sprays |

| Powders |

| Ointments |

| Solutions & Liquids |

| Foams & Films |

| Chronic Wounds | Diabetic Foot Ulcers |

| Pressure Ulcers | |

| Venous Leg Ulcers | |

| Other Chronic Wounds | |

| Acute Wounds | Surgical & Traumatic Wounds |

| Burns | |

| Lacerations & Abrasions | |

| Others |

| Hospital Pharmacies |

| Retail Pharmacies & Drugstores |

| Online Pharmacies |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Antiseptics | |

| Antibiotics | ||

| NSAIDs | ||

| Growth Factors | ||

| Enzymatic Debriders | ||

| Others | ||

| By Dosage Form | Creams | |

| Gels | ||

| Sprays | ||

| Powders | ||

| Ointments | ||

| Solutions & Liquids | ||

| Foams & Films | ||

| By Application / Wound Type | Chronic Wounds | Diabetic Foot Ulcers |

| Pressure Ulcers | ||

| Venous Leg Ulcers | ||

| Other Chronic Wounds | ||

| Acute Wounds | Surgical & Traumatic Wounds | |

| Burns | ||

| Lacerations & Abrasions | ||

| Others | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies & Drugstores | ||

| Online Pharmacies | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the topical wound agents market?

The market is valued at USD 2.07 billion in 2026 and is projected to reach USD 2.95 billion by 2031.

Which product category is growing fastest?

Growth-factor gels are expected to expand at an 11.67% CAGR through 2031.

Why are sprays gaining traction in hospitals?

Sprays enable no-touch application, supporting infection-control goals and reducing cross-contamination risk.

Which region is forecast to lead growth?

Asia-Pacific will record the highest regional CAGR at 9.57% due to manufacturing incentives and faster approvals.

How will e-pharmacies influence distribution?

State-level licensing now lets pharmacists deliver prescription debriders directly to patients, driving an 11.95% CAGR for online channels.

What keeps antibiotic ointment growth subdued?

Stricter FDA and EMA stewardship rules require culture confirmation and resistance tracking, steering usage toward antiseptics instead.

Page last updated on: