Tooth Filling Materials Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.61 Billion |

| Market Size (2031) | USD 3.55 Billion |

| Growth Rate (2026 - 2031) | 6.35% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tooth Filling Materials Market Analysis by Mordor Intelligence

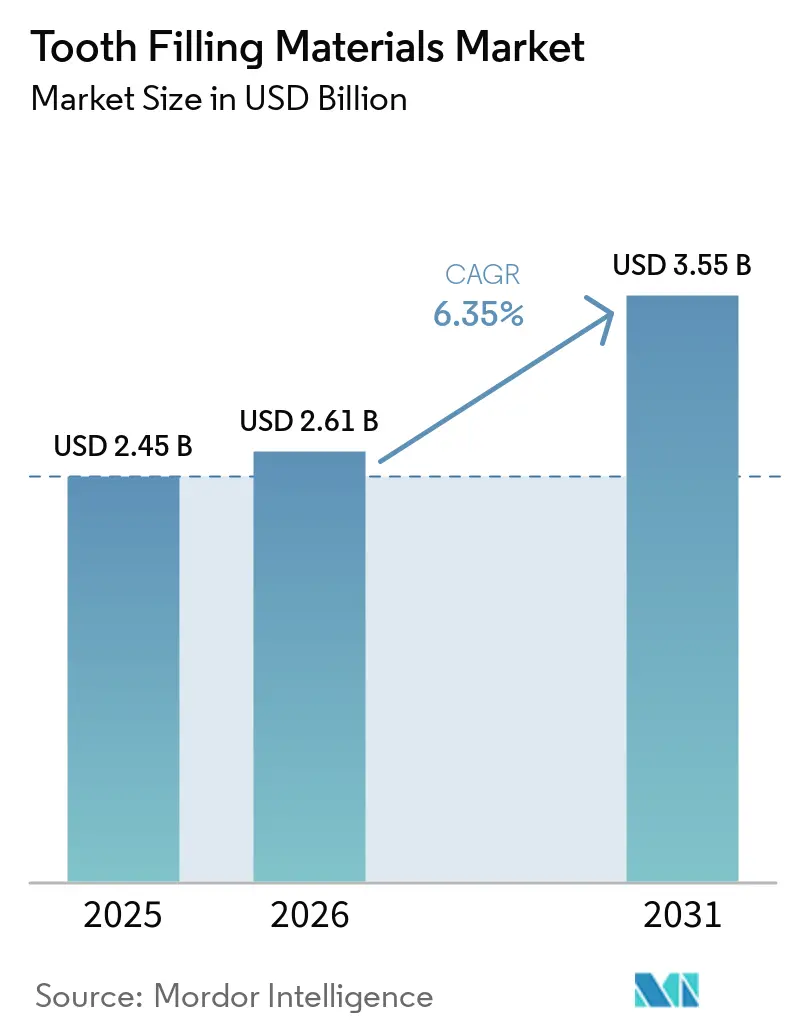

The Tooth Filling Materials Market size is projected to expand from USD 2.45 billion in 2025 and USD 2.61 billion in 2026 to USD 3.55 billion by 2031, registering a CAGR of 6.35% between 2026 to 2031.

A multi-factor push from mercury regulation, rapid product innovation, and digitization of restorative workflows is expanding material choice and clinical use cases in general practice and specialty clinics. Shifts in patient preference toward esthetic, tooth colored outcomes continue to move posterior restorations toward composites and glass ionomers. Procurement behavior is changing as DSOs centralize buying and standardize simplified shade composites and universal adhesives. High-income markets are advancing indirect inlays and onlays through scanner adoption, while public health and rural sites continue to rely on direct composites and glass ionomer strategies.

Key Report Takeaways

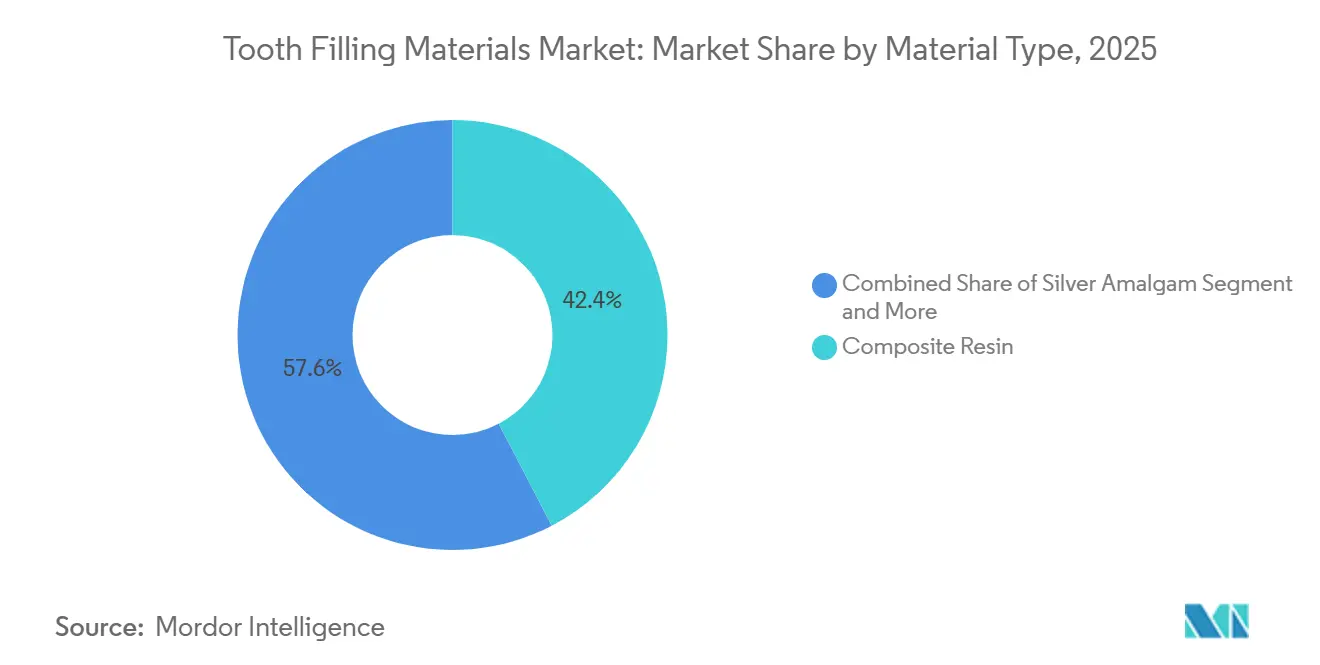

- By material type, composite resin led with 42.37% share in 2025, while silver amalgam recorded the highest projected CAGR at 7.32% through 2031 in the tooth filling materials market.

- By filling type, direct fillings held 58.41% share in 2025, while indirect fillings are projected to expand at an 8.89% CAGR through 2031 in the tooth filling materials market.

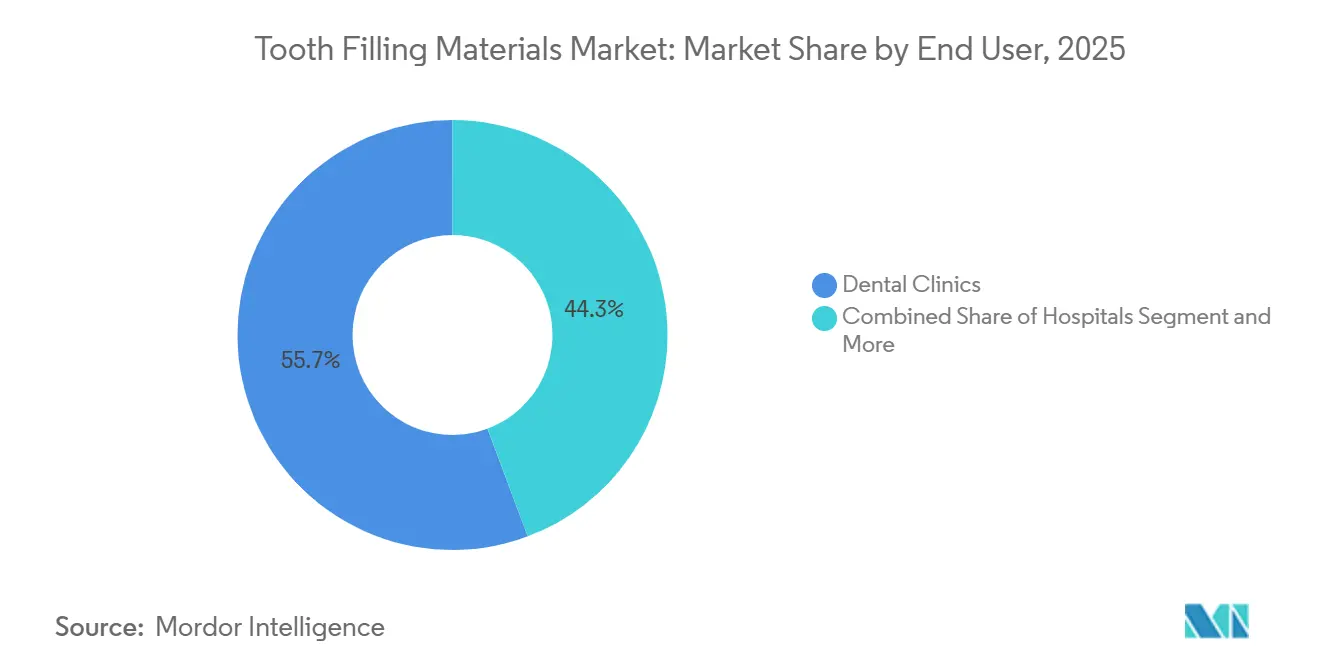

- By end user, dental clinics accounted for 55.70% share in 2025, while hospitals are forecast to grow at a 10.34% CAGR through 2031.

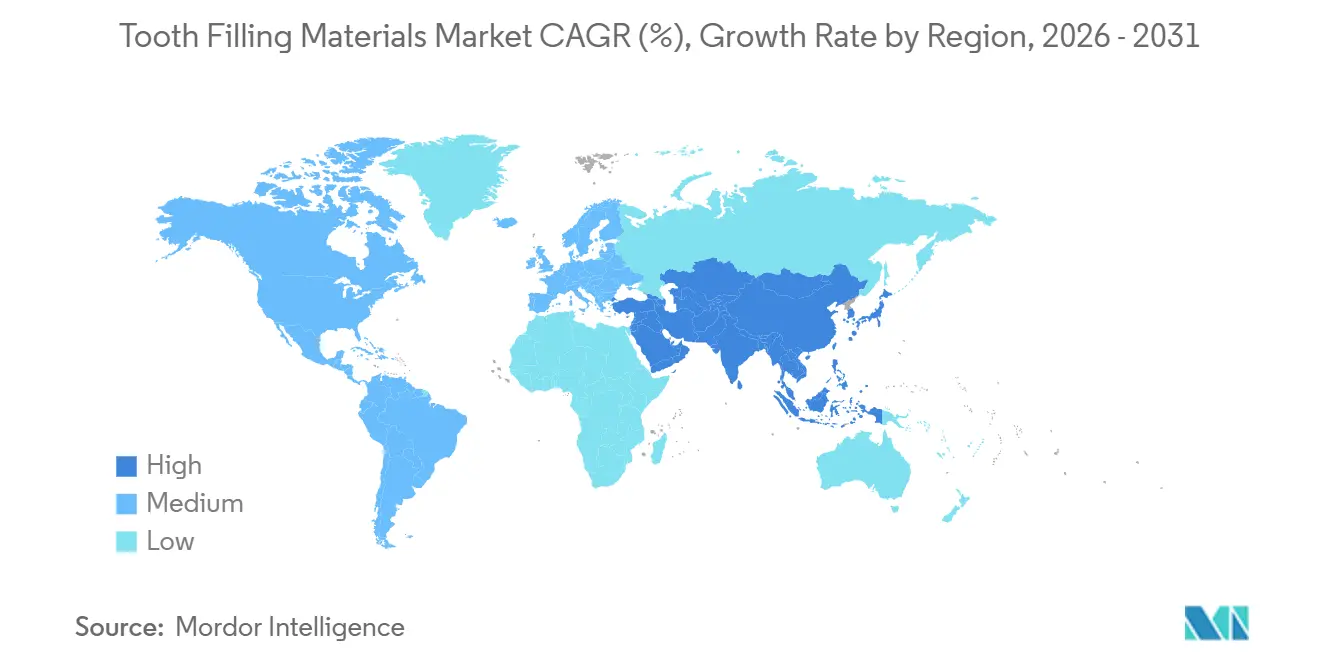

- By geography, North America held 39.41% share in 2025, while the Asia-Pacific is projected to grow at a 12.84% CAGR through 2031 in the tooth filling materials market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Tooth Filling Materials Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Global Caries Burden Sustaining Restorative Demand | + 1.2% | Global, pronounced in low/middle-income nations lacking preventive infrastructure | Long term (≥ 4 years) |

| Rising Preference for Aesthetic, Tooth-Colored Restorations | + 1.5% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Aging Population and Greater Oral-Health Awareness Increasing Procedure Volumes | + 0.9% | OECD nations, emerging middle-class cohorts in India, Brazil, Southeast Asia | Long term (≥ 4 years) |

| Rapid Innovation in Composites, Glass Ionomers, And Universal Adhesives | + 1.3% | Global, led by early adoption in North America, Western Europe | Short term (≤ 2 years) |

| Amalgam Phase-Down/Ban Accelerating Shift to Mercury-Free Materials | + 1.4% | EU, North America (IHS), select Asia-Pacific markets enforcing Minamata Convention | Short term (≤ 2 years) |

| Digitization Expanding Indirect Inlays/Onlays and Resin/Ceramic Blocks | + 0.8% | High-income markets with CAD/CAM penetration, spillover to metropolitan clinics in APAC, Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Global Caries Burden Sustaining Restorative Demand

Untreated dental caries in permanent teeth remains the most prevalent health condition worldwide, with the WHO reporting nearly 3.7 billion people affected and 2.4 billion adults carrying untreated decay by age 70 based on Global Burden of Disease assessments.[1]World Health Organization, “Global Burden of Oral Diseases,” World Health Organization This persistent burden keeps baseline procedures steady even as preventive programs scale in high fluoridation regions and school-based initiatives expand. Urbanization and increased access to sugar-dense diets are increasing risk in emerging markets at the same time that insurance coverage and income growth enable more restorative care. Insurance gaps in large national schemes continue to delay treatment in underserved populations, which drives steady use of glass ionomer and direct composites once access improves. Evidence on older adults shows high rates of missing and decayed teeth in the United States, underscoring retreatment needs in seniors and medically complex patients who often face xerostomia, which compounds caries risk.

Rising Preference for Aesthetic, Tooth Colored Restorations

Consumer expectations and social media visibility are shaping demand for natural-looking anterior and posterior restorations that blend with surrounding dentition. Simplified shade composite systems and improved translucency control are reducing the trade-off between efficiency and esthetics in busy practices. For example, Ivoclar’s universal composite system introduced in 2025 uses engineered translucency shift to support bulk placement while achieving dentin-like opacity after cure, which fits high-throughput clinical schedules.[2]Ivoclar, “Tetric Family Scientific Report Vol. 01/2025,” Ivoclar Universal adhesives with reliable bonding to enamel and dentin further streamline esthetic workflows and help clinicians maintain predictable results across variable clinical conditions.[3]Kuraray Noritake Dental, “CLEARFIL Universal Bond Quick 2 Product Information,” Kuraray Noritake Dental As practitioners gravitate toward systems that achieve shade coverage with fewer SKUs and shorter placement time, the tooth filling materials market continues to favor esthetic resin-based options in both general dentistry and cosmetic practices.

Rapid Innovation in Composites, Glass Ionomers, and Universal Adhesives

Composite chemistry is advancing beyond 2 mm incremental layering, with bulk fill formulations enabling deeper cures while controlling shrinkage stress and maintaining wear resistance. Solventum’s composite portfolio features stress-relieving monomer systems and optimized fillers designed for 4.5 mm single-step placement in posterior Class I and II restorations, which shortens chair time without requiring a capping layer in many cases.[4]Solventum, “Filtek Bulk Fill and Stress-Relieving Monomer Technology,” New universal adhesives reduce steps by combining etch, prime, and bond, and some systems eliminate traditional dwell times due to higher hydrophilicity monomers that enable rapid dentin infiltration and immediate light curing, which improves per patient cycle time in high volume clinics. On the glass ionomer side, peer-reviewed studies report large gains in compressive strength and fluoride release using ionogel, titanium hydroxide, and nanosilver-doped bioactive components, supporting expanded use in posterior load-bearing scenarios where recharge and chemical adhesion are clinical priorities.[5]Royal Society of Chemistry, “Materials Advances Article on Glass Ionomer Reinforcement,” Royal Society of Chemistry These developments widen material choice and enable more tailored strategies for high caries risk and xerostomic patients, which supports sustained growth in the tooth filling materials market.

Amalgam Phase Down/Ban Accelerating Shift to Mercury Free Materials

Global policy is tightening around mercury use in dentistry, with COP6 of the Minamata Convention adopting a ban on the manufacture and trade of amalgam effective January 1, 2035, and with the European Union enforcing a comprehensive ban as of 2025. In the United States, the Indian Health Service announced it will end the use of amalgam in all IHS and tribal dental programs by 2027, which accelerates transitions to composites and glass ionomers in public systems. Some suppliers have continued limited amalgam availability during transition windows, while planning exits aligned with treaty timelines. Short-term stockpiling in markets without immediate bans can create a temporary lift for legacy alloys prior to an expected demand decline as inventories cycle out and procurement rules tighten. These regulatory shifts reinforce a durable mix shift in the tooth filling materials market toward mercury-free materials and adhesives that support efficient, esthetic restorations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Advanced Materials and Limited Reimbursement for Elective Restorations | - 0.9% | Emerging markets, U.S. Medicare-age patients without supplemental dental coverage | Long term (≥ 4 years) |

| Safety/Regulatory Scrutiny of Monomers and MDR/FDA Compliance Burden | - 0.7% | EU, North America, ripple effects in markets exporting to these regions | Medium term (2-4 years) |

| Polymerization Shrinkage and Technique Sensitivity Driving Secondary Caries/Retreatments | - 0.5% | Global, particularly in public health/DSO high-volume settings with variable operator skill | Medium term (2-4 years) |

| Time and Skill Intensity for Multi-Layer Esthetic Composites in Public/DSO Settings | - 0.4% | Price-sensitive markets, community health centers, rural clinics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Materials and Limited Reimbursement for Elective Restorations

Premium composites, bulk fill systems, and CAD/CAM milled blocks carry higher acquisition costs than basic alternatives, which can strain budgets in public clinics and among fee-for-service patients without robust insurance. Gaps in adult dental coverage in many geographies push price sensitivity, which drives clinicians to balance esthetics, speed, and unit cost when selecting restorative materials. Hospitals and community clinics must weigh capital purchases for digital workflows against the patient mix and reimbursement structures available in their states and regions. Policy changes that allow coverage where dental care is clinically linked to medical treatment can improve access, but these pathways remain narrow, and documentation requirements may add administrative burden. As a result, procurement committees often prioritize universal adhesives and simplified shade composites that standardize training and reduce wastage. However, broader adoption of advanced indirect materials can lag in cost-constrained settings, which moderates growth in the tooth-filling materials market.

Safety/Regulatory Scrutiny of Monomers and MDR/FDA Compliance Burden

Material safety reviews and device classification frameworks require ongoing testing and documentation, which can extend time to market and raise compliance costs. Manufacturers supplying the European Union must maintain technical documentation, clinical evaluation, and post-market clinical follow-up aligned to MDR, which can be especially burdensome for smaller suppliers. Exporters to the United States also align with device-level quality and labeling standards, and changes to risk communications for specific chemistries can drive rapid portfolio adjustments. The resulting compliance overhead can slow the release cadence of new monomers and fillers, focusing launches on higher volume universal systems where return on investment is more secure. In turn, regulatory headwinds temper the rate at which niche formulations enter the tooth filling materials market, even as mainstream systems continue to improve.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Composite Resin Dominance Amid Bulk Fill and Simplified Shade Innovations

Composite resin held the leading position in 2025 with 42.37% share as continuous gains in filler technology, polymerization chemistry, and shade simplification reinforced clinician preference for esthetic and efficient workflows. The segment continues to benefit from bulk fill composites that enable deeper cures and from universal adhesives that shorten bonding steps across a wide set of indications. Solventum’s composite families feature stress-relieving monomer systems and single-step placement up to 4.5 mm, which helps clinics manage throughput without compromising wear performance in posterior restorations. Ivoclar’s 2025 universal composite system uses a designed translucency transition during cure to improve blending and depth of cure, paired with high-output light activation to accelerate placement in bulk. These designs fit general practice needs for predictable shade matching with fewer SKUs, while also supporting Class I and Class II applications in busy appointment schedules. The tooth filling materials market sees higher adoption of simplified shade systems in DSOs and group practices that standardize inventory and training.

Glass ionomer cements are broadening their role as studies show significant improvements in compressive strength and fluoride release when nanoparticle and bioactive additives are used. One peer-reviewed study reported compressive strength that met and exceeded ISO thresholds for posterior use with ionogel and titanium hydroxide additives. At the same time, another showed nanosilver-doped bioactive glass ionomer with higher cumulative fluoride release than conventional formulations. These features make glass ionomers attractive in older adults and high caries risk patients who benefit from chemical adhesion and fluoride recharge. In premium indirect care, lithium disilicate and hybrid ceramics support inlays and onlays that can be fabricated chairside, although capital costs limit adoption in lower volume clinics. Silver amalgam shows a temporary lift in certain markets due to transition planning and inventory behavior, but regulatory timelines point to a secular shift to mercury-free options through 2031.

By Filling Type: Direct Fillings’ Chairside Convenience Versus Indirect Fillings’ CAD/CAM Driven Precision

Direct fillings held 58.41% of the tooth filling materials market share in 2025 due to single-visit placement, lower cost of materials, and minimal equipment needs in general practice. Bulk fill composites reduce layer counts and improve efficiency, while universal adhesives speed bonding on varied tooth substrates. Solventum’s bulk fill systems are engineered to deliver reliable depth of cure and controlled shrinkage stress, which makes posterior Class II restorations more predictable in high-throughput settings. Adhesive advances with higher hydrophilicity monomers enable rapid dentin penetration and immediate light curing, which eliminates dwell time and reduces per restoration chair time in independent evaluations. These step savings align with clinic economics and lower training burdens for associates and new graduates.

Indirect fillings are growing as scanners, cloud design platforms, and chairside mills compress the traditional impression-to-delivery timeline. The tooth filling materials market size for indirect fillings is projected to expand at 8.89% CAGR through 2031 as more practices adopt CAD/CAM for inlays and onlays that demand precise occlusion and margins. Dentsply Sirona’s scanner and cloud suite allow real-time case sharing with labs, which reduces remake risk and accelerates turnarounds for esthetic indirect cases. Evidence on lithium disilicate crowns and resin matrix ceramics shows clinically acceptable marginal gaps and high fracture resistance that exceed typical occlusal loads, which supports conservative overlays in premolars and molars. Additive manufacturing is also progressing, with printed resin blocks that reach high compressive and tensile strength when bonded with MDP-containing adhesives, although cost and finishing workflows still shape adoption. Capital costs for scanners and mills remain a constraint in rural and solo practices, which sustains direct composite dominance in those settings even as metropolitan and DSO clinics scale indirect workflows.

By End User: Dental Clinics’ Volume Leadership Versus Hospitals’ Integration into Primary Care Pathways

Dental clinics accounted for 55.70% of the tooth filling materials market in 2025 due to specialized chairside equipment, optimized operatory layouts, and practitioner focus that supports productive schedules. Cloud-connected ecosystems that integrate scanners, design, and communication are oriented to clinic networks that centralize equipment management. Dentsply Sirona’s enterprise modules enable DSOs to coordinate labs and devices across locations, which aligns with standardized material formularies and purchasing. Vendors with portfolios that span endodontic to restorative steps are leaning into integrated workflows to increase share of wallet in clinics. Preventive gains may delay some direct restorations, but increased awareness and screening keep procedure pipelines steady in insured cohorts.

Hospitals are advancing faster at a 10.34% growth rate through 2031 as oral health integrates into broader chronic disease management and perioperative protocols. Policy signals that link dental interventions to medical indications are enabling limited coverage in targeted cases, which supports restorative capacity inside hospital networks and affiliated clinics. Program models for older adults and dually eligible patients are emphasizing medically necessary care, while xerostomia and root caries in seniors sustain demand for fluoride-releasing materials. In parallel, dental laboratories and in-house hospital labs are navigating evolving documentation rules for custom-made devices in Europe, with professional bodies advocating proportionate requirements that preserve access and limit cost escalation.

Geography Analysis

North America held 39.41% of the tooth filling materials market share in 2025, as high per capita dental spending, private insurance, and early adoption of premium composites and scanners sustained demand. The region continues shifting to mercury-free materials, with the Indian Health Service moving to end amalgam use by 2027 in federal and tribal care, which guides procurement and training toward composites and glass ionomers. DSOs drive standard formularies and bulk buying, which support simplified shade composites and universal adhesives. Digitally enabled practices connect scanners to cloud platforms to coordinate with labs, while fee-for-service and rural sites maintain a direct composite focus where capital budgets are limited.

Europe is defined by regulatory momentum that removed amalgam from routine care by 2025, which accelerates a transition to composites and glass ionomers across public and private systems. Adoption of universal adhesives and simplified shade composites is strong in Western Europe, where clinics favor predictable esthetics and reduced procedure time. Implementation of device documentation and post-market follow-up requirements continues to shape supplier participation, with professional organizations engaging regulators on proportionate expectations for dental labs and custom-made devices. The region also uses chairside milling and CAD/CAM workflows in metropolitan areas, though smaller clinics may pursue labs for pressed or milled ceramics depending on case complexity.

Asia-Pacific leads future expansion with a projected 12.84% CAGR as middle-class growth, urban insurance pilots, and clinical infrastructure investments lift restorative volumes. Regional enforcement aligned to the Minamata Convention reinforces a shift to mercury-free materials, which benefits suppliers with broad composite and adhesive portfolios. Japan, Australia, and South Korea maintain advanced adoption of digital workflows in larger practices. At the same time, public health programs across parts of Southeast Asia apply atraumatic restorative techniques with glass ionomers in community settings. Studies on printed resin blocks and lithium disilicate support confidence in indirect overlays where scanner penetration is rising, although capital costs continue to modulate adoption by market tier.

Competitive Landscape

The tooth filling materials market is moderately consolidated at the top with a cluster of multinational manufacturers and a long tail of regional suppliers. Top global dental brands sustain positions through integrated portfolios that cover adhesive, composite, glass ionomer, and indirect CAD/CAM material systems. Product strategies focus on streamlined workflows, including universal adhesives compatible with multiple etching modes and simplified shade composites that reduce SKUs and training complexity for DSOs and large group practices. Vendors also emphasize incremental improvements in shrinkage stress and wear, which support longer-lasting posterior restorations and fewer postoperative sensitivities in general practice.

Digitally connected ecosystems create switching costs by linking scanners, design software, and chairside or lab milling to proprietary material families and validated workflows. Dentsply Sirona’s cloud and scanner suite exemplifies this approach, enabling real-time collaboration and quality control between clinics and labs that standardize on compatible blocks and cements. Clinical evidence for resin matrix ceramics and lithium disilicate overlays continues to support adoption for conservative indirect restorations, which ties material selection to digital investments in high-volume urban clinics. In parallel, research on advanced glass ionomers is improving posterior suitability and reinforcing their role in geriatric and community programs, which sustains a multi-material mix by indication and patient profile.

Regulatory policy is a defining feature of competition as suppliers time portfolio updates to comply with mercury bans and to meet documentation and post-market follow-up expectations in the EU and exporting markets. Public health systems and DSOs concentrate purchasing, which pressures price and favors platforms that standardize technique across teams. Companies that align clinical evidence, regulatory compliance, and cloud-connected workflows are best positioned to expand share as clinics adopt universal adhesives and simplified bulk fill composites. The Tooth filling materials market, therefore, rewards vendors with credible science, dependable training support, and seamless integration into existing clinical and digital workflows.

Tooth Filling Materials Industry Leaders

Coltene Holding AG

Dentsply Sirona Inc.

Ivoclar Vivadent AG

GC Corporation

Solventum

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: The Indian Health Service (IHS), U.S. Department of Health and Human Services, announced it will cease use of mercury-containing dental amalgam in all IHS and tribal dental programs by 2027, transitioning to mercury-free restorative materials. The decision aligns with U.S. Food and Drug Administration guidance, raising concerns about mercury accumulation and recommending non-mercury materials for high-risk populations.

- March 2025: Ivoclar Vivadent AG launched Tetric Plus, a simplified universal composite system featuring four cluster shades covering all 16 VITA classical shades, 4mm bulk-fill capability, and 3-second curing time with Bluephase PowerCure. The product integrates patented Visual Transformation Technology (VTT), which provides 36% translucency pre-polymerization for reliable depth-of-cure and reduces to 13% post-polymerization for natural dentin-mimicking opacity.

- February 2025: Dentsply Sirona highlighted the 15-year milestone of SDR bulk-fill composite technology, emphasizing its continued use in direct restorative procedures and tooth fillings. The company reported that the technology had been used in more than 135 million restorations globally and remained a key component of its restorative materials portfolio.

Global Tooth Filling Materials Market Report Scope

As per the scope of the report, tooth filling materials are biocompatible restorative substances used to repair cavities and damaged tooth structures. They include composites, glass ionomers, ceramics, amalgam, gold, and emerging bioactive materials designed to restore function and aesthetics. This market reflects the demand for durable, aesthetic, and minimally invasive dental restorations, driven by rising caries prevalence and patient preference for tooth‑colored fillings.

The tooth filling materials market is segmented by material type, filling type, end user, and geography. By material type, the market is segmented into composite resin, silver amalgam, glass ionomer, gold fillings, ceramics, and others. By filling type, direct fillings and indirect fillings. By end user, the market is segmented into dental Clinics, hospitals, and dental laboratories. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and market trends for 17 countries across major regions worldwide. The report offers market value (in USD) for the above segments.

| Composite Resin |

| Silver Amalgam |

| Glass Ionomer |

| Gold Fillings |

| Ceramics |

| Others |

| Direct Fillings |

| Indirect Fillings |

| Dental Clinics |

| Hospitals |

| Dental Laboratories |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Material Type | Composite Resin | |

| Silver Amalgam | ||

| Glass Ionomer | ||

| Gold Fillings | ||

| Ceramics | ||

| Others | ||

| By Filling Type | Direct Fillings | |

| Indirect Fillings | ||

| By End User | Dental Clinics | |

| Hospitals | ||

| Dental Laboratories | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the tooth filling materials market growth outlook through 2031?

It is expected to increase from USD 2.61 billion in 2026 to USD 3.55 billion by 2031 at a 6.35% CAGR based on current forecasts.

Which segments are expanding fastest within the tooth filling materials market?

Indirect fillings are projected to grow at 8.89% CAGR, hospitals at 10.34% CAGR, and Asia-Pacific at 12.84% CAGR through 2031, reflecting digitization and access improvements.

How are global mercury policies affecting restorative choices?

The Minamata Convention decision and the EU ban are accelerating a shift to mercury free materials, while the U.S. Indian Health Service will end amalgam use by 2027, reinforcing composites and glass ionomers.

What factors are driving adoption of simplified shade and bulk fill composites?

Clinics want faster placement and reliable esthetics; universal adhesives and engineered translucency systems reduce steps and SKUs while maintaining depth of cure and blending.

Where do glass ionomers fit in current restorative practice?

Reinforced glass ionomers with improved strength and high fluoride release are gaining use in geriatric and high caries risk patients where chemical adhesion and recharge are clinical priorities.

How is digitization changing restorative workflows in the tooth filling materials market?

Intraoral scanners, cloud design, and chairside milling shorten turnaround for inlays and onlays, though capital costs channel adoption to DSOs and metropolitan practices while direct composites remain prevalent elsewhere.

Page last updated on: