Third-Party Risk Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

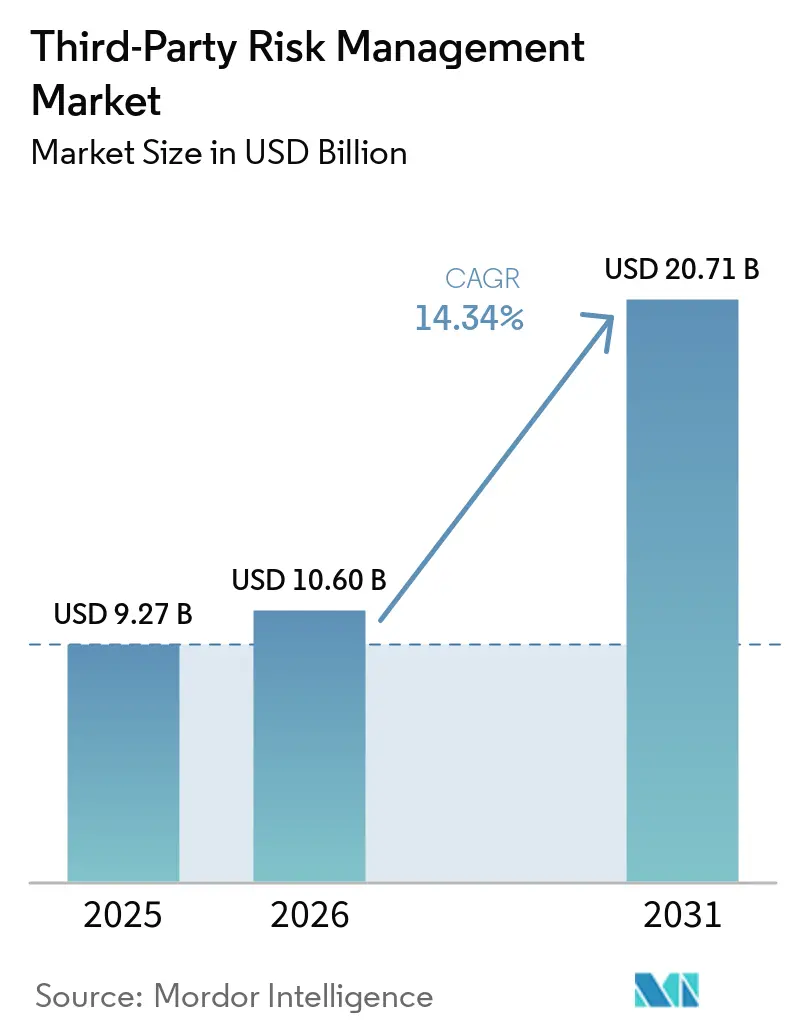

| Market Size (2026) | USD 10.60 Billion |

| Market Size (2031) | USD 20.71 Billion |

| Growth Rate (2026 - 2031) | 14.34% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Third-Party Risk Management Market Analysis by Mordor Intelligence

The third-party risk management market was valued at USD 9.27 billion in 2025 and is estimated to grow from USD 10.60 billion in 2026 to reach USD 20.71 billion by 2031, at a CAGR of 14.34% during the forecast period (2026-2031). Demand is rising because enterprise risk now extends well beyond internal systems and into vendor, supplier, and service provider environments, with third-party involvement appearing in a much larger share of confirmed breaches than before. That shift has moved the third-party risk management market beyond a compliance task and into board-level planning, which is widening spending across software, managed services, and continuous monitoring tools. Regulatory pressure is also becoming harder to defer, as digital resilience, outsourcing, and sector-specific cybersecurity rules now require more documented vendor oversight across multiple regions. Competition is split between specialist platforms that focus on vendor lifecycle automation and continuous monitoring, and larger GRC providers that use bundle-led selling to expand wallet share. Implementation cost, fragmented data, and weak evidence quality still slow adoption in parts of the third-party risk management market, but the move from static reviews to continuous, AI-supported monitoring is reshaping product design and acquisition strategy.

Key Report Takeaways

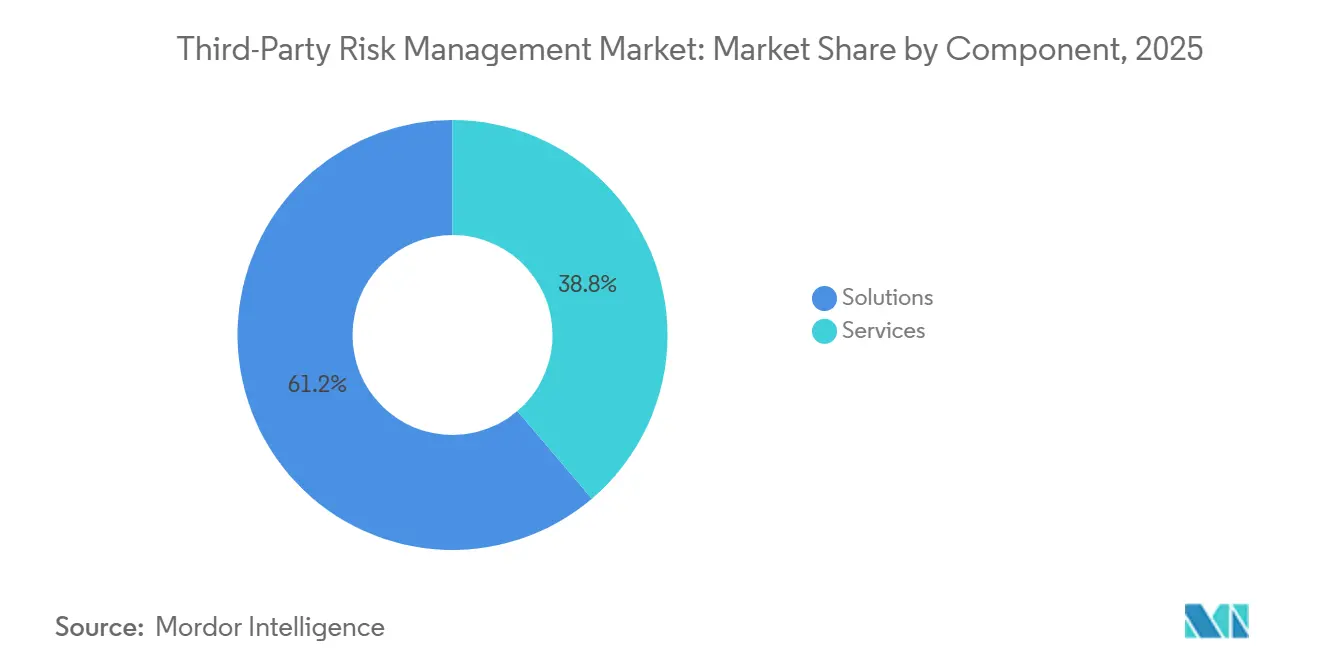

- By component, Solutions held 61.23% of the third-party risk management market size in 2025, while Services is projected to expand at a CAGR of 14.67% through 2031.

- By deployment model, Cloud held 57.45% of the third-party risk management market share in 2025 and is projected to grow at a CAGR of 14.89% through 2031.

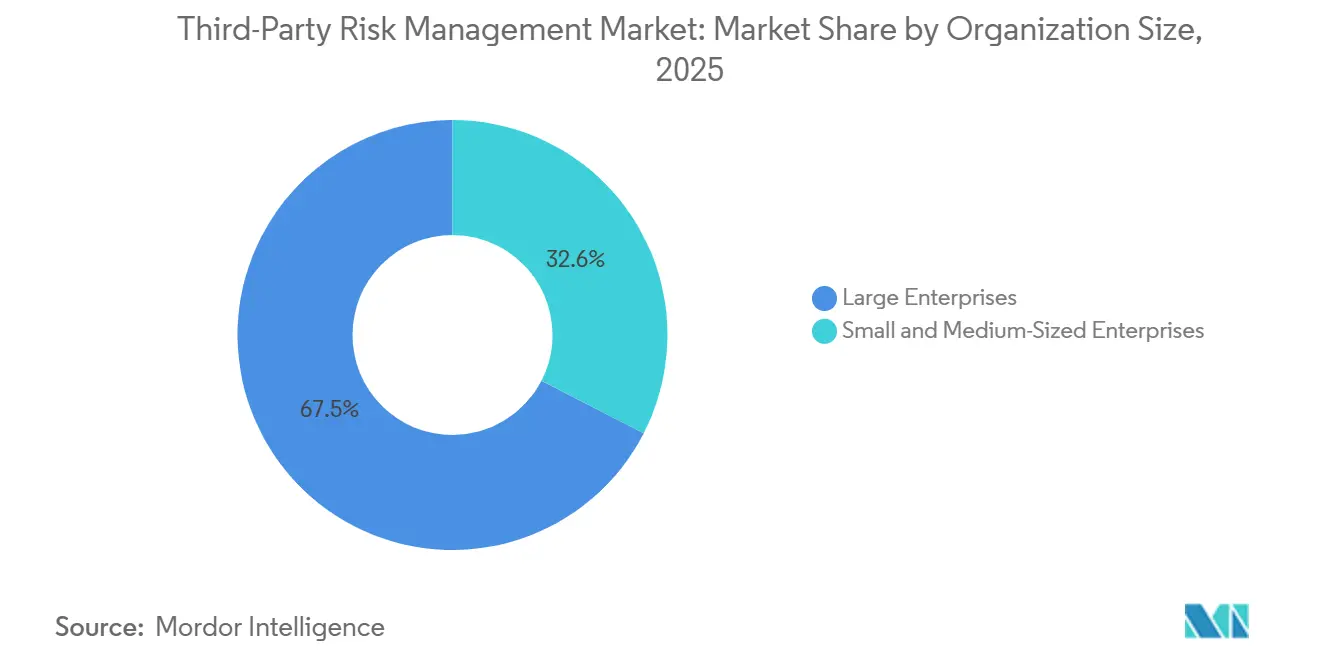

- By organization size, Large Enterprises accounted for 67.45% share in 2025, while SMEs are expected to record the highest CAGR of 14.76% through 2031.

- By end user industry, BFSI held 24.44% share in 2025, while Healthcare and Life Sciences is projected to expand at a CAGR of 14.89% through 2031.

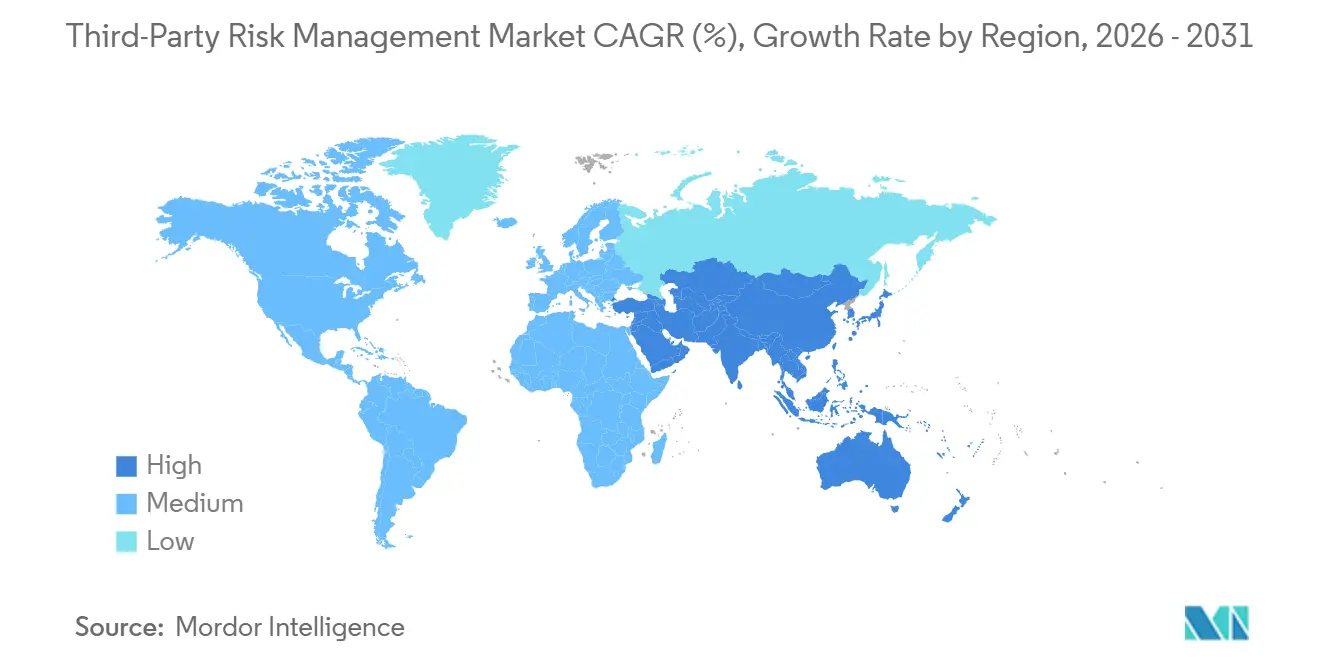

- By geography, North America accounted for 38.56% of the third-party risk management market in 2025, while Asia-Pacific is expected to register the fastest CAGR of 14.78% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Third-Party Risk Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Third-Party Cyberattacks and Ransomware Exposure | +3.2% | Global | Short term (≤ 2 years) |

| Tightening Digital Resilience and Outsourcing Regulations | +2.8% | Europe, North America, Asia-Pacific | Medium term (2-4 years) |

| Expanding Vendor Ecosystems Across Cloud and SaaS Environments | +2.1% | Global, led by North America and Asia-Pacific | Short term (≤ 2 years) |

| Shift From Periodic Reviews to Continuous Monitoring and Automation | +1.6% | Global | Short term (≤ 2 years) |

| Rising Need to Map Nth-Party and Concentration Risk | +1.1% | North America and European Union | Medium term (2-4 years) |

| AI Governance Obligations for Model, Data, and Service Providers | +0.9% | North America, European Union, Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Third-Party Cyberattacks and Ransomware Exposure

Attackers now target vendors more often because one compromised supplier can open paths into many customer environments, and that is raising urgency across the third-party risk management market. Third-party involvement appeared in 30% of confirmed breaches in the Verizon 2026 Data Breach Investigations Report, which marked a sharp increase from the prior year.[1]Verizon, “2026 Data Breach Investigations Report,” Verizon Business, verizon.com Large supply-chain and third-party compromises also rose sharply in recent years, which shows that vendor-linked exposure is becoming a durable part of enterprise cyber risk. Black Kite reported that the average number of downstream victims per third-party breach increased to 5.28 in 2025 from 2.56 in 2024, which reflects how failures now spread across connected ecosystems. SecurityScorecard also found that 41.4% of ransomware attacks originated through third-party vectors, and that pattern is pulling more sectors into formal vendor oversight programs within the third-party risk management market.

Tightening Digital Resilience and Outsourcing Regulations

Regulation is becoming one of the strongest spending triggers in the third-party risk management market because third-party oversight is now treated as a control that can be tested and audited. DORA entered application on January 17, 2025, and it requires EU financial entities to maintain a Register of Information, include minimum security clauses in critical ICT contracts, and monitor concentration risk on an ongoing basis.[2]European Parliament and Council of the European Union, “Digital Operational Resilience Act (DORA), Regulation (EU) 2022/2554,” EUR-Lex, eur-lex.europa.eu The Basel Committee published its Principles for the Sound Management of Third-Party Risk in December 2025, which raised the global baseline for banking-sector vendor governance and ongoing monitoring. Regulatory momentum is also spreading beyond Europe, as Japan's Financial Services Agency published a research report in April 2026 to study advanced TPCRM practices in the United States, the European Union, and the United Kingdom. New York's Department of Financial Services added further pressure in October 2025 with guidance on third-party service provider risk, reinforcing the need for documented and evidence-based oversight in the third-party risk management market.

Expanding Vendor Ecosystems Across Cloud and SaaS Environments

The number of vendors that enterprises must assess is growing faster than internal risk teams can scale, and that mismatch is creating sustained demand in the third-party risk management market. Thales reported in 2025 that enterprises used an average of 85 SaaS applications, which makes access control and data-flow visibility harder to manage across business units.[3]Thales Group, “Thales 2025 Global Cloud Security Study Reveals AI Tool Sprawl Security Gap,” Thales Group, thalesgroup.com Whistic reported that the average enterprise worked with 286 vendors in 2025, up 21% year over year, while only 29% could determine exposure at every stage of the vendor lifecycle. The same report showed that many companies already manage more than 100 vendors, which means manual review models are becoming harder to sustain. As partner networks keep expanding, the third-party risk management market is benefiting from buyer demand for automation that can widen coverage without matching increases in staffing.

Shift From Periodic Reviews to Continuous Monitoring and Automation

The move from annual reviews to continuous surveillance is one of the clearest changes in the third-party risk management market because vendor conditions can change much faster than a questionnaire cycle can capture. Mitratech reported in 2025 that 41% of organizations still relied on spreadsheets to assess third parties, which shows why many programs still struggle with stale evidence and slow follow-up. Product roadmaps are now shifting toward always-on models that ingest breach alerts, external risk signals, and compliance changes in real time. Vendors are also using AI-assisted workflows to automate scoring, escalation, and remediation steps that previously required repeated analyst intervention. This shift is changing team structure inside the third-party risk management market, as analysts spend less time on repetitive intake work and more time on governance, exception handling, and negotiation with critical vendors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Implementation and Integration Costs Across Siloed Risk Stacks | -2.6% | Global, most acute in SME markets | Short term (≤ 2 years) |

| Data Quality, Privacy, and Cross-Border Information Sharing Constraints | -1.8% | European Union, Asia-Pacific, Global | Medium term (2-4 years) |

| Low Trust in Static Questionnaires and Inconsistent Evidence Quality | -1.2% | Global | Short term (≤ 2 years) |

| Fragmented Ownership Across Procurement, Security, Legal, and Compliance | -0.9% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Implementation and Integration Costs Across Siloed Risk Stacks

Implementation remains a real barrier in the third-party risk management market because many buyers must connect TPRM platforms with procurement, ERP, contract management, and GRC systems that were not built around a shared data structure. Whistic reported that TPRM teams added an average of 3 full-time employees in 2025 at USD 109,000 per FTE, while 94% still said they could not assess all the vendors they wanted to review. That gap shows that software spend alone does not solve coverage problems when staffing, process design, and data cleanup are weak. The burden is heavier for smaller buyers, where first-year platform, setup, and labor costs can reach USD 40,000 to USD 80,000 and delay formal adoption in the third-party risk management market. As a result, many organizations continue to rely on spreadsheets or partial workflows, even when those approaches create slower response times and weaker audit evidence.

The third-party risk management market also faces a data problem because vendor risk decisions are only as strong as the evidence entering the platform. KPMG reported in 2026 that only 17% of organizations rated their TPRM data as fully reliable, which shows why confidence in vendor decisions remains uneven. Privacy rules add another layer of friction, as GDPR Article 28 limits what processor-related security information can be shared and documented across organizational boundaries. DORA increases the pressure by requiring more detailed oversight of ICT arrangements and concentration risk, including visibility into dependencies that some vendors still treat as commercially sensitive. These constraints slow automation in the third-party risk management market because teams must reconcile incomplete records, inconsistent questionnaire responses, and cross-border limits on evidence sharing before they can trust the output.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Anchor Programs, Services Accelerate Fastest

Solutions accounted for 61.23% of the third-party risk management market in 2025, which shows that buyers still prefer platform-led models for core vendor governance. Solutions remain central because enterprises want risk identification, scoring, workflow management, and reporting inside one operating layer rather than across disconnected tools. The strongest demand inside solutions is shifting toward continuous monitoring and intelligence features, as organizations move away from point-in-time assessments and toward persistent surveillance of vendor conditions. Risk identification and due diligence, along with assessment and scoring tools, still form the most widely adopted layers because they align directly with audit needs, onboarding controls, and evidence collection requirements in the third-party risk management market.

Services is the fastest-growing component, with the third-party risk management market size for services projected to expand at a CAGR of 14.67% from 2026 to 2031. Professional and managed services are gaining ground because many organizations still need outside support for questionnaire administration, due diligence execution, remediation tracking, and vendor follow-up. That demand is rising even where companies want to keep policy ownership and escalation authority in-house, which supports blended operating models across the third-party risk management industry. Managed offerings are also drawing interest from technology-led entrants that sell subscription-based lifecycle coverage, and that is putting pressure on project-heavy delivery models that scale more slowly in the third-party risk management market.

By Deployment Model: Cloud Leads and Sustains Dual Momentum

Cloud held 57.45% of the third-party risk management market share in 2025 and is also the fastest-growing deployment model, with a 14.89% CAGR through 2031. That combination shows that the third-party risk management market is consolidating around SaaS delivery rather than gradually shifting toward it. Cloud tools appeal to large enterprises and mid-sized buyers because they reduce infrastructure overhead, speed deployment, and support frequent updates to content, workflows, and integrations. The same buyer logic is helping vendors widen coverage across regions and customer sizes in the third-party risk management market.

On-premises remains relevant because some regulated financial institutions and defense organizations still require tighter control over data residency and local processing. That makes the deployment discussion less about replacement and more about how different workloads are split across environments in the third-party risk management market. Multi-cloud vendor ecosystems also create more third-party exposure, so the same cloud shift that enables platform delivery is also increasing the amount of vendor risk that customers must monitor. Many buyers are therefore keeping monitoring intelligence in the cloud while storing sensitive vendor records locally, which supports hybrid models across the third-party risk management industry.

By Organization Size: Large Enterprises Dominant, SMEs Close the Gap

Large enterprises represented 67.45% of the third-party risk management market in 2025 because they manage broad vendor networks and face heavier scrutiny from financial, cyber, and data protection regulators. These organizations often oversee hundreds or thousands of suppliers, technology partners, and service providers, which makes formal scoring, workflow control, and evidence retention harder to avoid. They also spend more on managed support and scalable assessment models because expanding coverage through hiring alone is slow and costly. This keeps large-account requirements at the center of product design in the third-party risk management market.

SMEs are the fastest-growing organization-size segment, with a CAGR of 14.76% expected through 2031 in the third-party risk management market. Purpose-built mid-market tools are helping this buyer group enter earlier because they promise faster rollout, lower upfront complexity, and pricing that sits below traditional enterprise tiers. Contract pressure also matters, as larger customers are embedding vendor security expectations into procurement terms and pulling smaller suppliers into formal assessment cycles. IBM noted in 2026 that attackers increasingly target smaller technology vendors as entry points into larger enterprise environments, which adds operational urgency to adoption in the third-party risk management market.

By End User Industry: BFSI Leads Spend, Healthcare Records Fastest Growth

BFSI held 24.44% of the third-party risk management market size in 2025, which reflects the sector's long history of prescriptive outsourcing and vendor oversight rules. The Basel Committee's December 2025 principles are expected to raise the compliance floor further in jurisdictions that previously relied on less structured guidance. That keeps banking and financial services as the most stable spending anchor in the third-party risk management market, especially where institutions must evidence due diligence, contract controls, ongoing monitoring, and exit planning. IT and telecom remains the second-largest spending area because software supply chain integrity and SaaS provider oversight have become central risk priorities as enterprise technology estates keep expanding. Government and defense, manufacturing, and energy and utilities also maintain meaningful demand, though each group approaches the third-party risk management market through a different mix of resilience, access control, and continuity requirements.

Healthcare and life sciences is the fastest-growing end user segment, with a CAGR of 14.89% projected through 2031 in the third-party risk management market. The 2024 Change Healthcare breach increased attention on vendor oversight, and the pending HIPAA Security Rule update is expected to push more safeguards into mandatory practice while increasing demands for written verification from business associates. Automated monitoring is gaining traction in this sector because manual reviews do not provide the speed needed to detect vendor signals in time-sensitive care and claims environments. Retail and consumer goods and manufacturing are also increasing spend as supply disruption and vendor concentration risk move the third-party risk management market further into procurement and finance decision-making.

Geography Analysis

North America accounted for 38.56% of the third-party risk management market share in 2025, supported by dense regulation, mature security spending, and a strong concentration of specialist vendors. The United States has shown especially strong demand for continuous monitoring because regulated sectors are moving beyond periodic checklist reviews and toward ongoing oversight of service providers. Updated NYDFS guidance issued in October 2025 reinforced that direction and kept third-party governance high on the agenda for licensed entities. Canada and Mexico are also becoming more relevant to the third-party risk management market as cross-border supply chains and nearshore operating models create new oversight requirements for parent companies and critical service providers.

Europe remained the second-largest regional block in the third-party risk management market and faced the sharpest near-term regulatory acceleration. DORA entered application across the European Union on January 17, 2025, and it introduced detailed requirements for ICT third-party registers, contractual provisions, concentration risk monitoring, and oversight of critical providers. In November 2025, the European supervisory framework moved further as the first cohort of critical third-party providers came under formal oversight, which is changing how financial entities structure programs and documentation in the third-party risk management market. Germany and the United Kingdom remain the largest national demand centers, while France, Italy, the Netherlands, and Spain continue to add compliance-led adoption across sectors beyond finance.

Asia-Pacific is the fastest-growing geography in the third-party risk management market, with a CAGR of 14.78% expected from 2026 to 2031. China, India, and Japan represent the largest demand pools, as digital supply chains broaden and regulators start to formalize expectations around third-party cyber risk. Japan's Financial Services Agency published a research report in April 2026 to study advanced TPCRM practices abroad, while SecurityScorecard found that Singapore recorded the highest third-party breach rate at 71.4% among the countries it analyzed in 2025. South America, the Middle East, and Africa remain smaller in current value, but the third-party risk management market is expanding there as privacy law enforcement, cloud governance, and supply-chain security expectations become more formal across enterprise buyers.

Competitive Landscape

The third-party risk management market is moderately fragmented, with competition split across full-lifecycle specialists, enterprise GRC suites with embedded modules, and point solutions focused on external risk intelligence. No single provider dominates all buyer groups, because customer needs vary widely by sector, deployment preference, regulatory burden, and vendor volume. Consolidation accelerated in 2026 as Diligent acquired 3rdRisk, SecurityScorecard acquired Driftnet, and Protecht acquired VISO TRUST, all within a short span and all aimed at capability expansion. Those transactions show that scale in the third-party risk management market now depends as much on workflow depth, AI capability, and intelligence coverage as it does on installed base.

Product differentiation is moving toward AI-native architecture, continuous monitoring, and faster risk-scoring workflows in the third-party risk management market. SecurityScorecard launched TITAN AI in March 2026 to replace manual third-party review work with continuous intelligence and automated response. Bitsight launched Security Posture Management in March 2026, combining cyber risk data, external exposure intelligence, business context, and AI-assisted remediation workflows. Buyers are increasingly rewarding vendors that can connect external threat signals with internal governance actions without forcing teams to move across multiple systems. That is pushing the third-party risk management market toward platforms that automate reassessment, escalation, and evidence handling rather than only collecting questionnaires.

White-space remains in the third-party risk management market around mid-market deployment, cross-border evidence standardization, and visibility into Nth-party dependencies beyond the third tier. Smaller vendors such as Panorays, UpGuard, and Venminder continue to gain attention by competing on ease of deployment and lower per-vendor economics. The managed services opportunity is also still open, as many organizations outsource or co-source parts of TPRM but only a small minority use fully managed lifecycle models. That mix keeps the third-party risk management market active for both platform vendors and service-led operators, while making rapid concentration unlikely in the near term.

Third-Party Risk Management Industry Leaders

NAVEX Global, Inc.

BitSight Technologies, Inc.

MetricStream, Inc.

LogicManager, Inc.

Intertek SAI Global Pty Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: SecurityScorecard completed the acquisition of UK-based Driftnet, a global internet scanning and threat intelligence startup. Driftnet's high-fidelity internet discovery engine is being integrated into SecurityScorecard's TITAN AI platform to deliver real-time third-party risk intelligence and pre-breach visibility for supply chain security teams.

- April 2026: Australian-based GRC platform Protecht Group acquired VISO TRUST, a US-based AI-powered TPRM platform specializing in third- to Nth-party risk management. The transaction extends Protecht's geographic footprint into North America and combines enterprise GRC capabilities with an AI-native TPRM assessment layer.

- April 2026: Bitsight achieved the highest possible scores across 11 criteria in the Forrester Wave evaluation, including top scores in Asset Discovery and Attribution, Vendor Discovery and Mapping, and Data Source Quality and Integrity, reinforcing its position as the primary continuous monitoring data layer for third-party risk programs.

- March 2026: SecurityScorecard unveiled TITAN AI at RSA Conference 2026, an AI-acceleration platform designed to replace reactive, manual TPRM workflows with continuous intelligence and automated risk response. The platform unifies threat intelligence and third-party risk data for real-time vendor scoring and supply chain incident containment.

Global Third-Party Risk Management Market Report Scope

The Third-Party Risk Management (TPRM) Market refers to the industry dedicated to solutions, services, and frameworks that help organizations identify, assess, monitor, and mitigate risks associated with external vendors, suppliers, partners, and service providers. This market encompasses software platforms, consulting services, and compliance tools that enable businesses to manage risks such as cybersecurity threats, regulatory non-compliance, operational disruptions, and reputational damage stemming from third-party relationships.

The Third-Party Risk Management Market Report is Segmented by Component (Solutions and Services), Deployment Model (Cloud and On-premises), Organization Size (Large Enterprises and Small and Medium-Sized Enterprises), End User Industry (BFSI, IT and Telecom, Healthcare and Life Sciences, Government and Defense, Retail and Consumer Goods, Manufacturing, and Energy and Utilities), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Solutions | Risk Identification and Due Diligence |

| Risk Assessment and Scoring | |

| Continuous Monitoring and Intelligence | |

| Workflow, Remediation, and Reporting | |

| Services | Professional Services |

| Managed Services |

| Cloud |

| On-premises |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| BFSI |

| IT and Telecom |

| Healthcare and Life Sciences |

| Government and Defense |

| Retail and Consumer Goods |

| Manufacturing |

| Energy and Utilities |

| Other End User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Component | Solutions | Risk Identification and Due Diligence |

| Risk Assessment and Scoring | ||

| Continuous Monitoring and Intelligence | ||

| Workflow, Remediation, and Reporting | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Model | Cloud | |

| On-premises | ||

| By Organization Size | Large Enterprises | |

| Small and Medium-Sized Enterprises | ||

| By End User Industry | BFSI | |

| IT and Telecom | ||

| Healthcare and Life Sciences | ||

| Government and Defense | ||

| Retail and Consumer Goods | ||

| Manufacturing | ||

| Energy and Utilities | ||

| Other End User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the third-party risk management market?

The third-party risk management market is estimated at USD 10.60 billion in 2026 and is projected to reach USD 20.71 billion by 2031 at a CAGR of 14.34%.

What is driving demand for third-party risk management platforms and services?

Demand is being driven by more vendor-linked cyber incidents, tighter digital resilience rules, larger SaaS and supplier ecosystems, and a shift toward continuous monitoring.

Which deployment model is leading adoption in third-party risk management?

Cloud leads with 57.45% share in 2025 and is also the fastest-growing deployment model, with a projected 14.89% CAGR through 2031.

Which organizations are buying the most third-party risk management solutions?

Large enterprises held 67.45% share in 2025 because they manage broader vendor networks and face heavier regulatory scrutiny.

Which end users are growing fastest in third-party risk oversight tools?

Healthcare and life sciences is the fastest-growing end user segment, with a projected 14.89% CAGR through 2031, while BFSI remained the largest at 24.44% share in 2025.

Which region leads global adoption and which region is expanding fastest?

North America led with 38.56% share in 2025, while Asia-Pacific is expected to record the fastest growth at a 14.78% CAGR through 2031.

Page last updated on: