Thin Film Solar PV Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

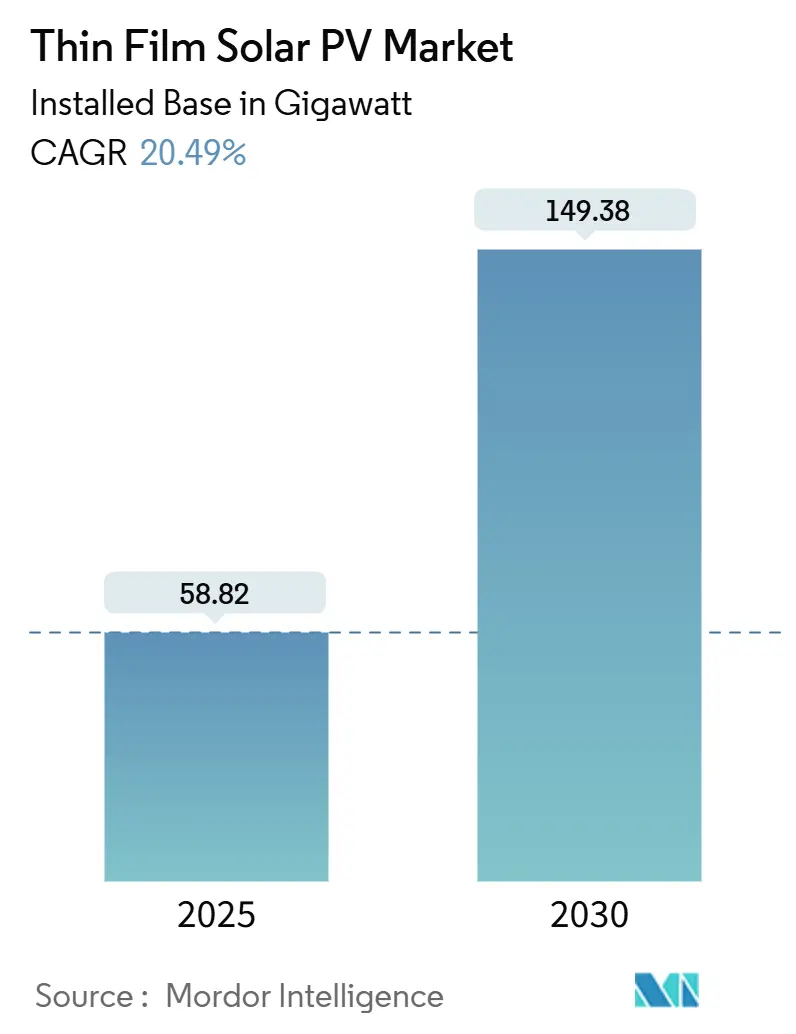

| Market Volume (2025) | 58.82 gigawatt |

| Market Volume (2030) | 149.38 gigawatt |

| Growth Rate (2025 - 2030) | 20.49% CAGR |

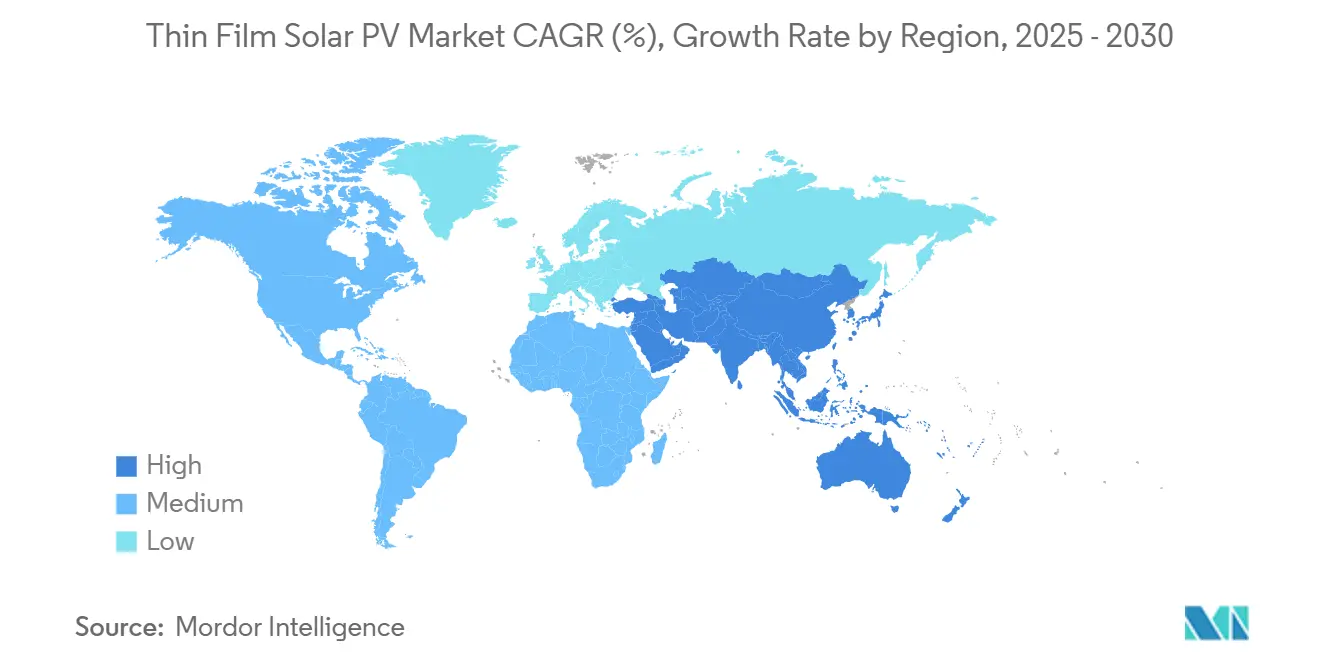

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

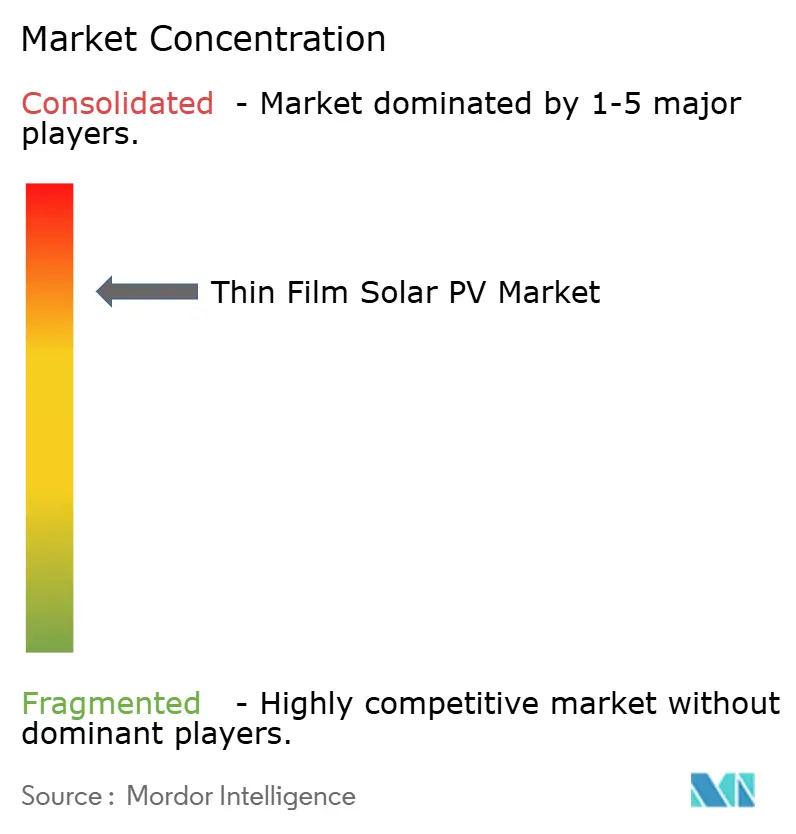

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Thin Film Solar PV Market Analysis by Mordor Intelligence

The Thin Film Solar PV Market size in terms of installed base is expected to grow from 58.82 gigawatt in 2025 to 149.38 gigawatt by 2030, at a CAGR of 20.49% during the forecast period (2025-2030).

Breakthrough tandem-cell efficiencies, aggressive decarbonization laws, and the ability to perform in high-temperature or low-light settings continue to make thin-film technologies more competitive than crystalline silicon. Regional policy tailwinds, such as the U.S. Inflation Reduction Act production tax credits, have mobilized multi-billion-dollar expansions of domestic capacity, while the EU Solar Standard mandates rooftop solar on new buildings from 2026, creating demand for lightweight, flexible modules.[1]SolarPower Europe, “European Parliament agrees on the EU Solar Standard,” solarpowereurope.org Supply-chain realignments are underway as China tightens export controls on cadmium telluride, indium, and tellurium, prompting Saudi Arabia and India to announce 30 GW and 10 GW local manufacturing plans, respectively. Competitive intensity is moderate: First Solar remains the leading CdTe producer, yet Oxford PV, Tandem PV, and other perovskite innovators are scaling commercialization, drawing significant venture funding and strategic partnerships.

Key Report Takeaways

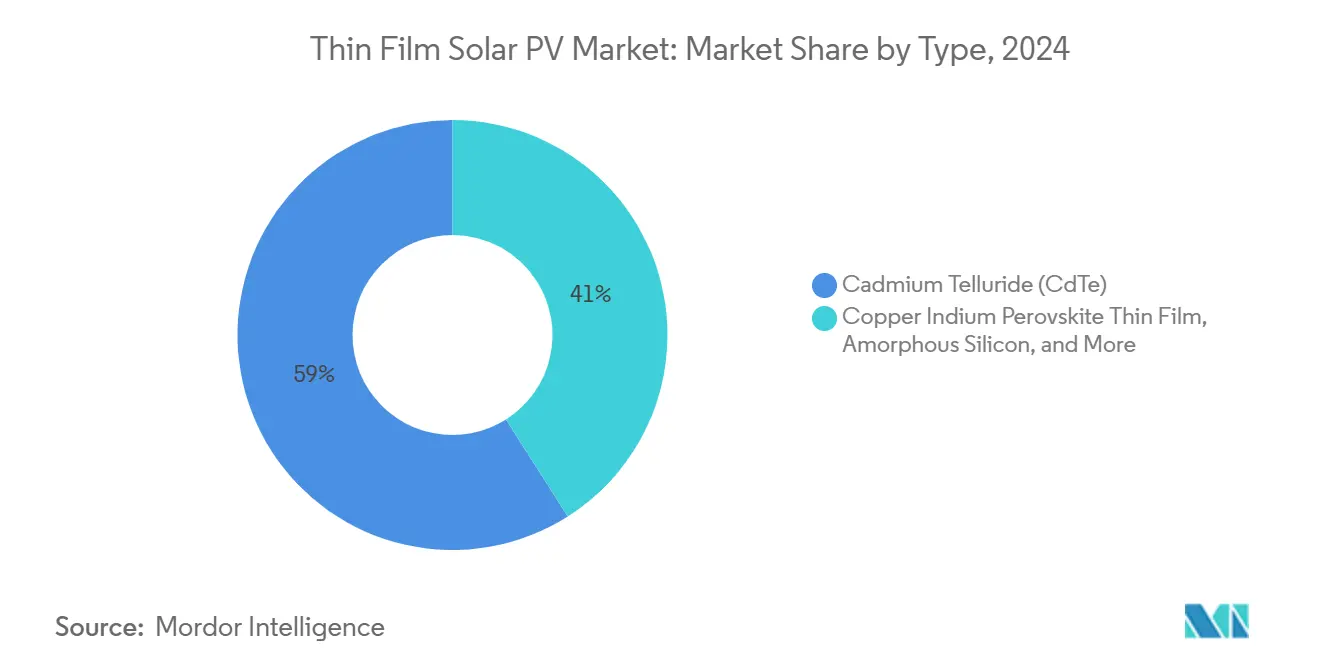

- By type, cadmium telluride led with 59% of the thin film solar PV market share in 2024; perovskite thin film is forecast to advance at a 38% CAGR between 2025-2030.

- By substrate, rigid glass captured 68% share of the thin film solar PV market size in 2024, while flexible plastic substrate is projected to expand at a 31% CAGR through 2030.

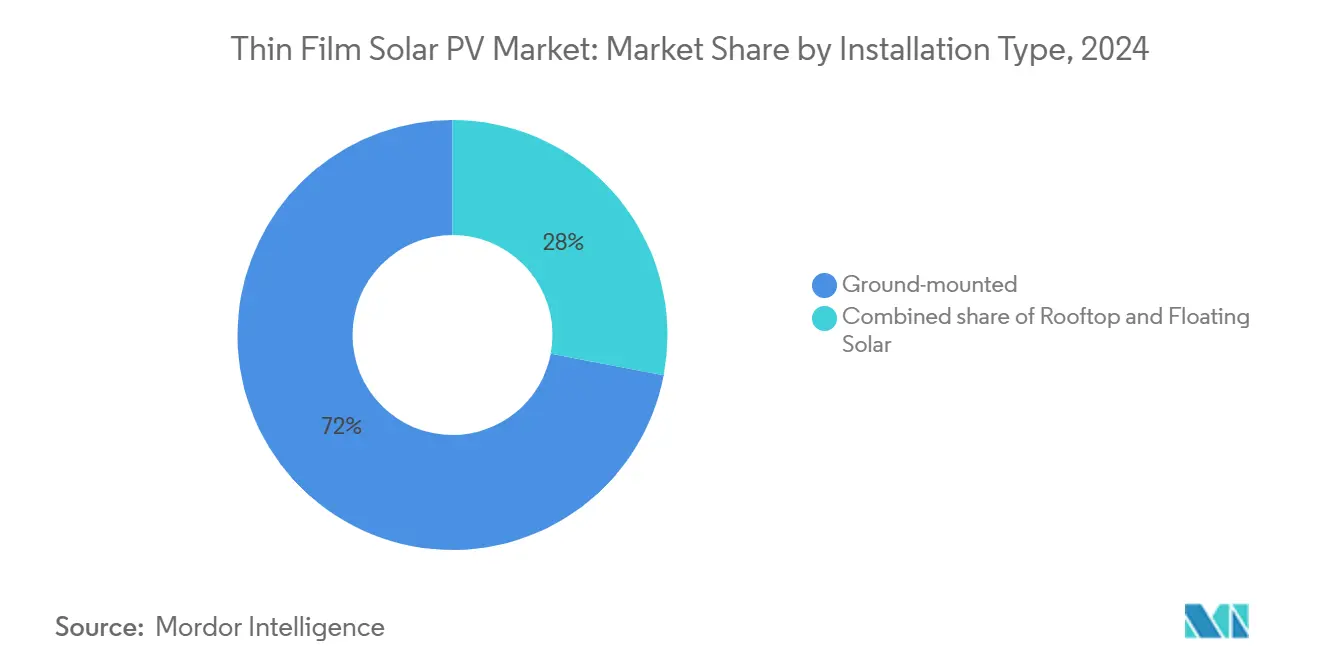

- By installation type, ground-mounted systems held a 72% share in 2024; rooftop installations are poised for a 33% CAGR to 2030.

- By application, utility-scale power plants commanded a 66% share of the thin-film solar PV market size in 2024, whereas building-integrated PV is set to grow at a 30% CAGR through 2030.

- By geography, North America accounted for 45% of the thin-film solar PV market share in 2024; Asia-Pacific is expected to record the fastest 35% CAGR during 2025-2030.

Global Thin Film Solar PV Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining LCOE of thin-film modules | +3.2% | Global (highest in APAC & MEA) | Medium term (2-4 years) |

| Aggressive national solar targets & incentives | +4.1% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Superior performance in high-temperature & low-light locales | +2.8% | MEA, APAC, South America | Medium term (2-4 years) |

| Rapid adoption in lightweight & flexible products | +3.5% | Europe & North America early adopters | Short term (≤ 2 years) |

| Off-grid demand for IoT & agri-solar micro-power | +1.9% | APAC, Africa, rural Americas | Long term (≥ 4 years) |

| Break-through perovskite tandem efficiencies > 30% | +4.8% | North America & EU leaders | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Declining LCOE of Thin-Film Modules

Manufacturing innovations have pushed the levelized cost of electricity for thin film modules below crystalline silicon in select climates, enabling utility-scale projects to sign record-low power purchase agreements. Series 7 CdTe modules from First Solar illustrate the trend, while roll-to-roll deposition techniques slash capex for emerging perovskite lines. Scale-up in India, Alabama, and Louisiana adds multi-gigawatt capacity, lowering unit costs further. Combined with anti-reflective coatings that cut LCOE by another 2%, the economic case for thin film PV deepens across desert, tropical, and diffuse-light sites.

Aggressive National Solar Targets & Incentives

Policy makers are creating an immediate demand pull. The EU Solar Standard mandates rooftop solar on all new buildings from 2026, favoring lighter, architecturally integrated modules. Japan earmarked USD 1.5 billion for ultra-thin perovskite R&D to secure 20 GW by 2040.[2]Harry Dempsey, “Japan’s $1.5 bn bet on ultra-thin solar cells,” ft.com Meanwhile, Section 45X tax credits in the United States delivered USD 857 million to First Solar for 2024 output, underpinning fresh investment in domestic lines. Saudi Arabia’s 30 GW manufacturing plan and India’s 10 GW announcement further illustrate how incentives translate into capacity pipelines.

Superior Performance in High-Temperature & Low-Light Locales

Thin film modules maintain higher yields when ambient temperatures exceed 40 °C, a critical advantage for Middle East projects forecast to top 100 GW by 2030.[3]Rystad Energy, “Solar PV to help meet soaring Middle East power demand,” rystadenergy.com Floating solar pilots in Asia show 0.6%-4.4% energy gains due to evaporative cooling. Material advances, such as germanium selenide absorbers reaching 80% photon absorption, keep pushing cell response under oblique or diffuse light.

Rapid Adoption in Lightweight & Flexible Solar Products

Architects and product designers are now specifying flexible thin film laminates for façades, curtain walls, and portable gear. European BIPV installs cost EUR 2,500-8,300/kWp, yet offset façade cladding costs, narrowing true premiums. Automotive OEMs test perovskite films on vehicle roofs for auxiliary charging, while Korean labs reported 23.64% efficiency tandem cells that survived 100,000 flex cycles. Partnerships such as Power Roll–Amcor target roll-fed solar film production for packaging and IoT devices.[4]Ross Kit Million, “Power Roll partners with Amcor on solar PV film tech,” solarpowerportal.co.uk

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cadmium/selenium toxicity concerns | -2.1% | EU and North America primarily, expanding globally | Long term (≥ 4 years) |

| Efficiency gap vs. top-tier crystalline-Si modules | -3.4% | Global, with strongest impact in utility-scale applications | Medium term (2-4 years) |

| Critical-mineral (In, Te) supply-chain volatility | -2.8% | Global, with acute impact in North America and Europe | Short term (≤ 2 years) |

| Limited project-finance bankability track-record | -1.9% | Emerging markets primarily, with spillover to developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cadmium/Selenium Toxicity Concerns

European rules on cadmium in consumer goods oblige CdTe manufacturers to maintain closed-loop recycling schemes and specialized disposal, adding cost and complexity. China’s February 2025 export controls on CdTe compounds underscored geopolitical risk, jolting module procurement schedules for PV. First Solar answers with 95% material recovery and cradle-to-cradle certification, but smaller firms struggle to match such compliance investments. Alternative perovskite, organic, or CIGS-based chemistries help alleviate toxicity pressure, yet scaling them demands fresh capital.

Efficiency Gap vs. Top-Tier Crystalline-Si Modules

Mainstream crystalline modules now clear 25% commercial efficiency, outperforming many thin film lines that average 18%-22%.[5]NREL, "Best Research-Cell Efficiency Chart," nrel.gov Land-constrained utility developers, therefore, gravitate to silicon unless thin film offers cost or temperature advantages. The gap is closing: tungsten-disulfide CIGS prototypes hit 25.7% efficiency in late 2024. Oxford PV’s tandem modules match premium silicon, and multi-junction roadmaps chart a route to 30%+. Until volume yields surpass silicon, some developers will remain wary.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Perovskite Commercialization Accelerates

Cadmium telluride retained 59% thin film solar PV market share in 2024, anchored by First Solar’s gigawatt-scale fabs and record 22.6% cell efficiency. In parallel, perovskite thin film is projected to grow at a 38% CAGR through 2030, capturing demand for higher efficiency and lightweight formats. The thin film solar PV market size for perovskite is expected to reach double-digit gigawatt scale by 2030, underpinned by Oxford PV’s commercial shipments and Tandem PV’s U.S. capacity build. CIGS remains relevant thanks to its compatibility with flexible substrates and new efficiency milestones, while amorphous silicon and organic PV continue to serve ultra-thin niche uses.

Perovskite momentum stems from easier band-gap tuning and low-temperature processing. Oxford PV’s 26.9% residential panels validated bankability, while Helmholtz-Zentrum Berlin’s tandem research shows a pathway to 30% efficiencies. Investors poured capital into vapor-phase and roll-to-roll lines that promise low capex per watt. Policy makers support diversification away from Cd-bearing chemistries, further lifting perovskite’s prospects within the thin film solar PV market.

By Substrate: Flexibility Drives Adoption

Rigid glass substrates held 68% share of the thin film solar PV market size in 2024, due to proven durability in utility fields. Flexible plastic substrates are on track for a 31% CAGR, fueled by BIPV façades, tents, and transport roofs. Metal foils provide a middle ground between glass and sturdier than polymers, for aerospace and vehicle skins needing high puncture resistance.

New polyimide and fluoropolymer films now tolerate soldering temperatures and ultraviolet exposure comparable to tempered glass. DuPont’s Tedlar frontsheets offer weight savings without sacrificing weatherability, while Korean tandem cells on 1.4-µm polyimide maintained 97.7% output after 100,000 bends. These breakthroughs expand design latitude and lower balance-of-system costs, supporting broader deployment within the thin-film solar PV market.

By Installation Type: Rooftop Momentum Builds

As utility developers tapped cheap desert land, ground-mounted arrays commanded 72% of the 2024 volume. Rooftop deployments, however, are projected to log a 33% CAGR as the EU Solar Standard and similar state codes mandate on-site generation. Although nascent, floating solar benefits from thin film’s lighter weight, simplifying anchoring and boosting cooling-related yield gains.

Automated mounting tracks and factory-prefabricated laminates cut rooftop labor hours significantly. For floating systems, spectrum-selective coatings and salt-spray-resistant encapsulants enhance durability. As distributed generation gains policy favor, rooftops and reservoirs will represent the fastest-scaling opportunities across the thin-film solar PV market.

By Application: BIPV Becomes a Growth Engine

Utility-scale power plants still accounted for 66% of 2024 demand, leveraging economies of scale and streamlined PPAs. Building-integrated PV is forecast for a 30% CAGR, spurred by façade retrofits and net-zero building codes. Commercial & industrial rooftops adopt thin film to combat thermal losses, while residential owners appreciate design flexibility and low wind loading. Semi-transparent modules unlock agrivoltaic and greenhouse installations.

Regulators view BIPV as an energy and building-materials solution, improving the total cost. Manufacturers now offer color-matched perovskite shingles and adhesive laminates, widening aesthetic appeal. Portable electronics, transportation roofs, and IoT chargers add incremental gigawatts yet serve as high-margin showcases for thin film versatility in the broader thin film solar PV market.

Geography Analysis

North America retained 45% thin-film solar PV market share in 2024 as First Solar’s U.S. fabs scaled to 14 GW and generated USD 857 million in Section 45X credits. Utility pipelines in the Southwest exploit thin film’s superior heat tolerance, while Canada and Mexico integrate agrivoltaic pilots that pair flexible laminates with drip-irrigation frames. Federal incentives, local-content rules, and a maturing recycling ecosystem underpin a resilient regional outlook.

Asia-Pacific is the fastest-growing region, tracking a 35% CAGR through 2030. Japan’s USD 1.5 billion perovskite push aligns with its 20 GW 2040 target, while China’s scale allows rapid price declines even as export controls nudge buyers toward diversification. India’s announced 10 GW thin film facility and Southeast Asia’s tariff-free trade blocs invite new fabs, spreading supply-chain risk. The region’s thin-film solar PV market is projected to surpass North America by 2028.

Europe’s regulatory activism ensures stable demand despite modest domestic manufacturing. The EU Solar Standard creates a structural pull for BIPV and rooftop solutions, fortifying prospects for Swedish and French gigafactories that pledge low-carbon footprints powered by renewable grids. Southern Europe exploits thin film’s high-temperature resilience, while the Nordics pilot transparent façades for daylight-rich offices. Though smaller today, the Middle East and Africa combine vast irradiance with sovereign drive, Saudi Arabia’s 30 GW commitment signals the next frontier in the thin-film solar PV market.

Competitive Landscape

The competitive field remains moderately concentrated. First Solar’s integrated CdTe model spans R&D to recycling, yielding a USD 23.3 billion backlog and 95% material recovery credibility. Its acquisition of Evolar imprints European know-how on tandem development. Oxford PV’s record 26.9% module and Tandem PV’s venture-financed U.S. line headline perovskite challengers, while Midsummer and SAEL scale CIGS and CdTe capacity in Europe and India.

Strategic moves cluster around three themes: 1) capacity expansion in incentive-rich countries, 2) M&A to lock up IP on tandem architectures, and 3) partnerships to co-develop flexible substrates. First Solar plans Alabama and Louisiana lines; Oxford PV collaborates with Meyer Burger for perovskite-silicon pathways; Power Roll teams with Amcor to commercialize printable films. Venture capital interest rebounded, with USD 50 million for Tandem PV and more than USD 1 billion disclosed for APAC manufacturing start-ups.

White-space opportunities exist in BIPV cladding, agrivoltaic laminates, and mobility chargers where few incumbents possess optimized products. Players who master roll-to-roll deposition and low-temperature processing may leapfrog existing efficiency metrics while slashing capital intensity. Over the forecast horizon, technology convergence toward perovskite-based tandems is expected to drive further consolidation within the thin-film solar PV market.

Thin Film Solar PV Industry Leaders

-

First Solar Inc.

-

Hanergy Thin Film Power Group Ltd

-

Solar Frontier K.K.

-

Sharp Corporation

-

Kaneka Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: SAEL announced a USD 954 million investment in a 10 GW thin film plant in India, broadening non-Chinese supply.

- July 2025: First Solar asserted ownership of TOPCon patents, expanding its photovoltaic IP portfolio.

- March 2025: Tandem PV raised USD 50 million to establish U.S. perovskite manufacturing.

- September 2024: Oxford PV began commercial shipments of perovskite modules.

Global Thin Film Solar PV Market Report Scope

Thin-film solar PV (photovoltaic) panels utilize thin layers of photovoltaic material, deposited on substrates such as glass, plastic, or metal. These lightweight and often flexible panels present a cost-effective alternative to traditional silicon panels. However, they typically offer lower efficiency and a shorter lifespan. Constructed from diverse semiconductor materials, thin-film panels include options like amorphous silicon (a-Si), cadmium telluride (CdTe), and copper indium gallium selenide (CIGS).

The global thin film solar PV market is segmented by Type, Substrate, Installation Type, Application, and geography. By type, the market is segmented into cadmium telluride, perovskite thin film, amorphous silicon, organic/polymer, and more. By substrate, the market is segmented into rigid glass substrate and metal foil substrate. By installation type, the market is segmented into ground-mounted, rooftop, and floating solar. By application, the market is segmented into utility-scale power plants, building-integrated PV, residential rooftop, and more. The report also covers the market sizes and forecasts for the global thin film solar PV market across major countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of capacity (GW).

| Cadmium Telluride (CdTe) |

| Copper Indium Gallium Selenide (CIGS) |

| Amorphous Silicon (a-Si) |

| Perovskite Thin Film |

| Organic/Polymer (OPV) |

| Multi-junction Tandem Thin Film |

| Rigid Glass Substrate |

| Flexible Plastic Substrate |

| Metal Foil Substrate |

| Ground-mounted |

| Rooftop |

| Floating Solar |

| Utility-Scale Power Plants |

| Commercial and Industrial Rooftop |

| Residential Rooftop |

| Building-Integrated PV (BIPV) |

| Portable and Consumer Electronics |

| Transportation and Automotive Solar Roofs |

| Off-grid and Remote Power (IoT, Agri-solar) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type | Cadmium Telluride (CdTe) | |

| Copper Indium Gallium Selenide (CIGS) | ||

| Amorphous Silicon (a-Si) | ||

| Perovskite Thin Film | ||

| Organic/Polymer (OPV) | ||

| Multi-junction Tandem Thin Film | ||

| By Substrate | Rigid Glass Substrate | |

| Flexible Plastic Substrate | ||

| Metal Foil Substrate | ||

| By Installation Type | Ground-mounted | |

| Rooftop | ||

| Floating Solar | ||

| By Application | Utility-Scale Power Plants | |

| Commercial and Industrial Rooftop | ||

| Residential Rooftop | ||

| Building-Integrated PV (BIPV) | ||

| Portable and Consumer Electronics | ||

| Transportation and Automotive Solar Roofs | ||

| Off-grid and Remote Power (IoT, Agri-solar) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the thin film solar PV market by 2030?

The thin film solar PV market size is forecast to reach 149.38 GW by 2030, growing at a 20.49% CAGR for 2025-2030.

Question Why are perovskite tandem modules important to future growth?

Perovskite tandems already achieve 26.9% commercial efficiency and are on track for 30%+, narrowing the efficiency gap with crystalline silicon while offering lighter, flexible form factors.

How does the EU Solar Standard influence demand?

The 2026 mandate for rooftop solar on new EU buildings could add 150-200 GW of cumulative installations, favoring lightweight thin film modules suited to architectural integration.

Which region shows the fastest growth rate?

Asia-Pacific is poised for a 35% CAGR through 2030, underpinned by Japan’s perovskite investments, India’s manufacturing build-out, and Southeast Asian diversification.

What are the main restraints facing thin film technologies?

Key challenges include cadmium toxicity regulations affecting CdTe and the current efficiency lag relative to top-tier crystalline-silicon modules, although tandem advances are closing the gap.

How concentrated is the competitive landscape?

The market scores 8 / 10 for concentration: leaders such as First Solar and Oxford PV hold strong positions, yet emerging firms funded by fresh capital continue to erode share.

Page last updated on: