Thermoplastic Elastomers In Medical Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

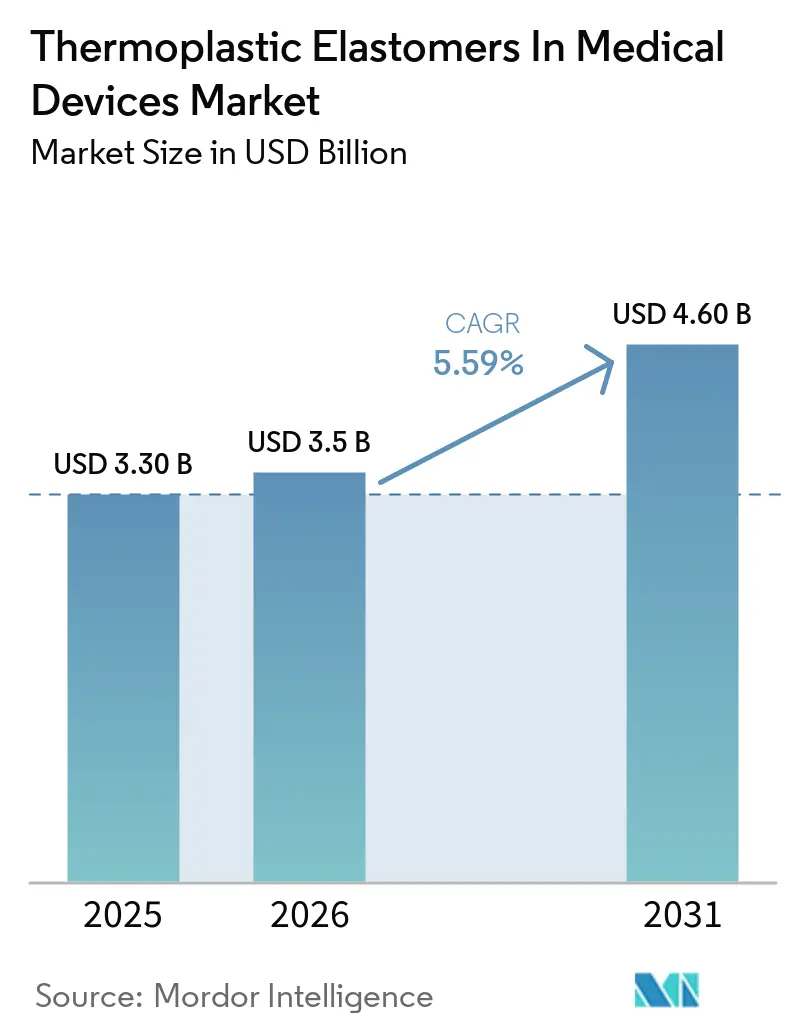

| Market Size (2026) | USD 3.5 Billion |

| Market Size (2031) | USD 4.60 Billion |

| Growth Rate (2026 - 2031) | 5.59% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thermoplastic Elastomers In Medical Devices Market Analysis by Mordor Intelligence

The Thermoplastic Elastomers In Medical Devices Market size was valued at USD 3.30 billion in 2025 and is estimated to grow from USD 3.5 billion in 2026 to reach USD 4.60 billion by 2031, at a CAGR of 5.59% during the forecast period (2026-2031).

Demand is increasing as Europe has officially scheduled sunset dates for di(2-ethylhexyl) phthalate (DEHP). Health systems are prioritizing minimally invasive catheter therapies that require flexible and kink-resistant shafts. Additionally, home-care technologies, such as insulin pumps, now demand gamma-stable, skin-safe elastomers. Suppliers with medical-device regulation (MDR) ready portfolios are gaining market share as original-equipment manufacturers (OEMs) accelerate reformulation timelines to less than three years. The thermoplastic elastomers in medical devices market is also benefiting from overmolding innovations, which integrate seals, grips, and strain-relief features into a single part. This reduces total assembly steps by up to 40% while enhancing reliability. North America remains the largest revenue center, but Asia-Pacific’s high-volume disposables production and growing adoption of continuous glucose monitors are driving the fastest growth.

Key Report Takeaways

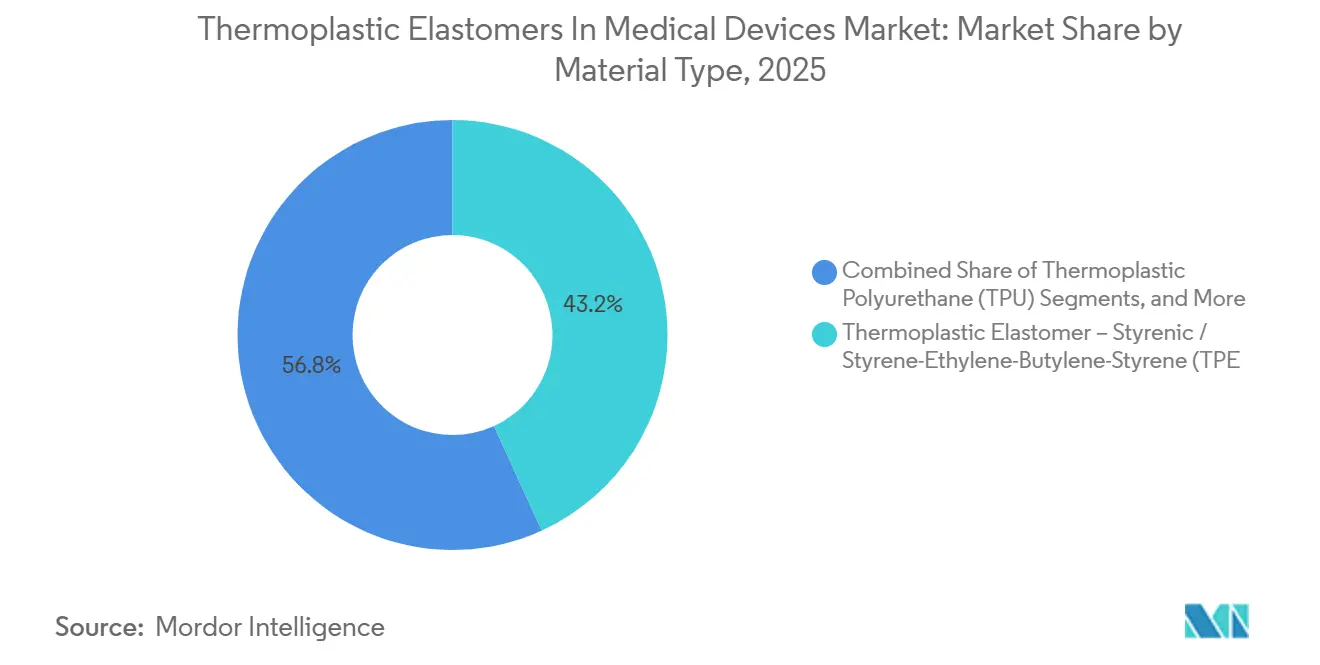

- By material type, thermoplastic elastomer – styrenic / styrene-ethylene-butylene-styrene (TPE-S/SEBS) captured 43.18% of the thermoplastic elastomers in the medical devices market share in 2025. Thermoplastic Polyurethane (TPU) is projected to expand at 7.12% during 2027-2031.

- By application, catheters & tubing commanded 31.30% of market share in 2025; wearables and skin-contact interfaces are advancing at a 7.34% CAGR through 2031.

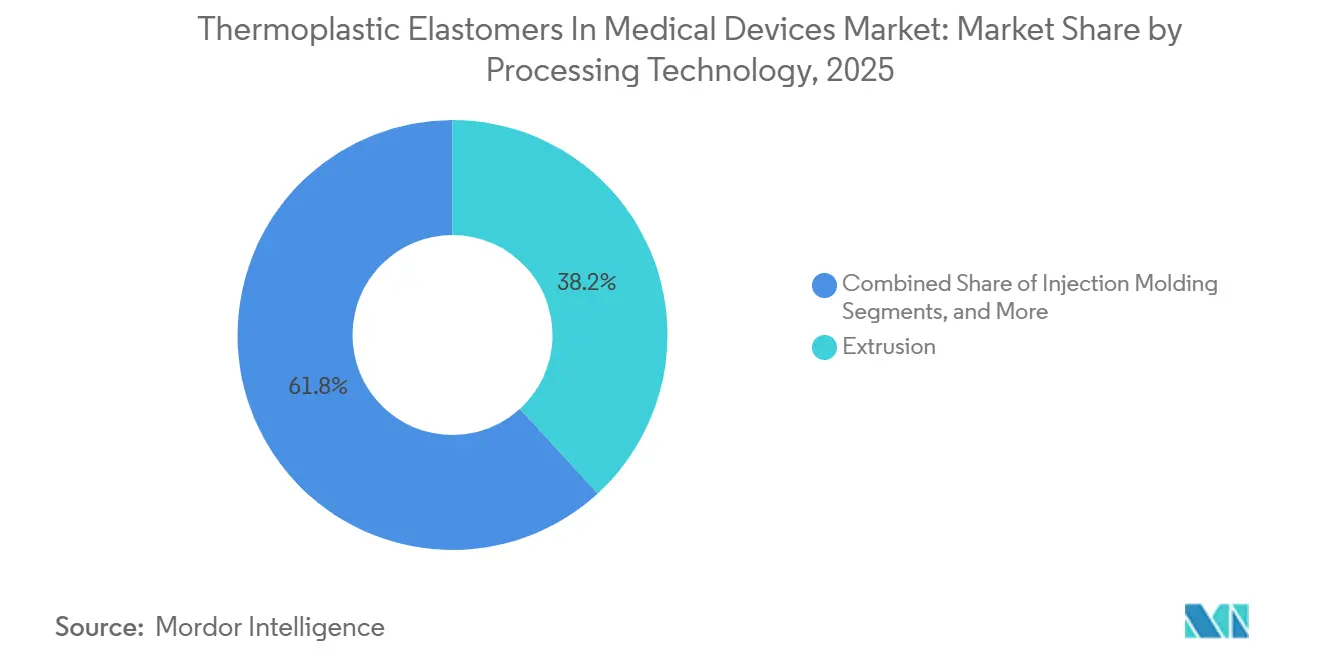

- By processing technology, extrusion held 38.19% of the thermoplastic elastomers in the medical devices market size in 2025 and is projected to expand at 7.41% during 2027-2031.

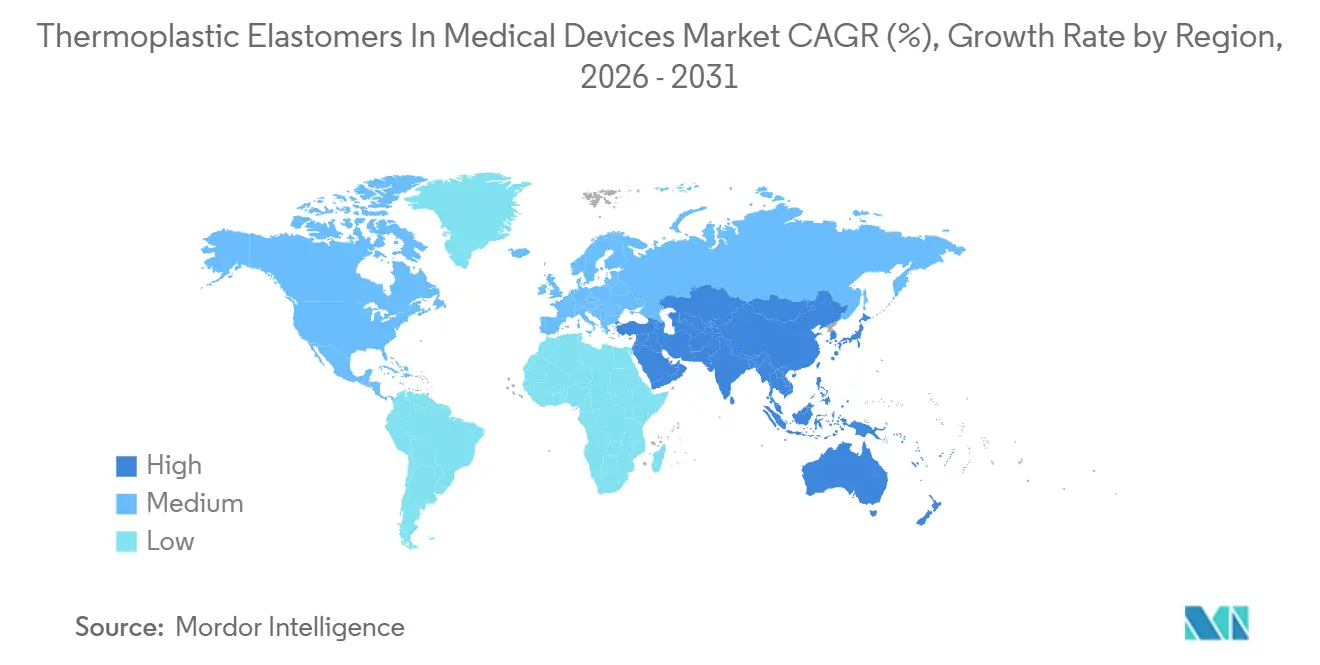

- By geography, North America captured 36.33% of market share in 2025, while Asia-Pacific is forecast to expand at a 7.63% CAGR between 2027 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Thermoplastic Elastomers In Medical Devices Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Shift Away from PVC/phthalates in sensitive uses | +1.2% | Europe, North America | Medium term (2-4 years) |

| Growth in minimally invasive, catheter-based therapies | +1.5% | Global, with concentration in North America, Europe, Asia-Pacific urban centers | Long term (≥ 4 years) |

| Expansion of wearable and home-care devices | +1.3% | North America, Europe, Asia-Pacific (Japan, South Korea) | Medium term (2-4 years) |

| OEM change-control burden under EU MDR favors stable suppliers | +0.6% | Europe, spillover to North America | Short term (≤ 2 years) |

| Overmolding-driven part consolidation (Bonding To PP/PA) | +0.8% | Global, early adoption in Europe and North America | Medium term (2-4 years) |

| Gamma-stable transparent TPEs enabling PVC-free IV/tubing | +0.9% | Global, led by Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift Away from PVC/Phthalates in Sensitive Uses

European Regulation 2023/2482 identifies DEHP as a substance of concern, setting a final application deadline of January 1, 2029, for medical devices containing DEHP. This provides OEMs with a 36-month window to reformulate, prompting a shift toward SEBS and thermoplastic polyurethane (TPU) alternatives that eliminate plasticizer leaching concerns.[1]European Chemicals Agency, “Substance Infocard – Bis(2-ethylhexyl) phthalate (DEHP),” echa.europa.eu Guidance issued in 2024 requires a benefit-risk analysis for devices releasing more than 10 µg/kg body weight/day of plasticizer, effectively disqualifying traditional PVC lines.[2]European Commission, “Regulation (EU) 2023/2482 – DEHP Sunset Date and Restrictions,” ec.europa.eu North American manufacturers are aligning their timelines with European counterparts to maintain global consistency, driving a collective shift in the thermoplastic elastomers in the medical devices market toward phthalate-free materials.

Growth in Minimally Invasive, Catheter-Based Therapies

Catheter laboratories are expanding their range of cardiovascular, neurovascular, and urological procedures, which rely on kink-resistant, pushable shafts. Polyether block amide (PEBA) compounds, such as Pebax Rnew, reduce advancement force by 50% compared to nylon 12, minimizing vessel trauma and shortening procedure times. Flexural-fatigue testing demonstrates that PEBA shafts endure 10,000 cycles at 90-degree bends, nearly tripling the lifespan of conventional polyurethane catheters, supporting broader adoption in same-day discharge environments. FDA 510(k) pathways enable manufacturers to update catheter designs using existing master files, reducing approval times by half and driving further penetration in the thermoplastic elastomers in medical devices market.

Expansion of Wearable and Home-Care Devices

In 2026, continuous glucose monitor shipments exceeded 12 million units, with each patch requiring multiple grams of skin-contact SEBS or TPU. HEXPOL’s Mediprene A2 line, introduced in late 2024, spans Shore A 25-65 and complies with ISO 10993-10 sensitization protocols, enabling 14-day wear cycles without causing skin irritation. A capital investment of USD 5.4 million at the Åmål, Sweden facility has increased annual medical-grade TPE capacity to 80,000 tonnes, ensuring supply for the rapidly growing thermoplastic elastomers in medical devices market. End-users value SEBS adhesive interfaces for their balanced adhesion, which holds at 0.5-1.5 N/cm and releases atraumatically, differentiating them from silicone gel systems.

OEM Change-Control Burden Under EU MDR Favors Stable Suppliers

Article 120 of the Medical Device Regulation classifies resin changes as significant modifications, requiring new documentation, clinical evaluations, and notified-body reviews. A 2025 survey indicated that 68% of European OEMs delayed material upgrades to avoid an additional 12-24 months of regulatory work. As a result, incumbent suppliers capable of delivering drop-in grades with identical extractables-and-leachables (E&L) profiles are securing contracts, consolidating power in the thermoplastic elastomers in medical devices market among seven global producers.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| E&L validation and sterilization-induced property shifts | -0.9% | Global, particularly stringent in Europe and North America | Medium term (2-4 years) |

| Cost premium vs PVC and silicone in volume applications | -0.7% | Global, most acute in price-sensitive markets (Asia-Pacific, Latin America) | Short term (≤ 2 years) |

| OEM material change-control under MDR extends timelines | -0.14% | Global, particularly stringent in Europe and North America | Medium term (2-4 years) |

| Supply-chain fragility for medical-grade resins, sterilization bottlenecks | -0.5% | Global, most acute in price-sensitive markets (Asia-Pacific, Latin America) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

E &L Validation and Sterilization-Induced Property Shifts

ISO 10993-18:2020 requires detailed chemical-profile testing, with each E&L program costing approximately USD 300,000 and taking nine months to complete. Gamma sterilization at 50 kGy can decrease the tensile strength of unmodified PEBA by 25%, prompting compounders to include antioxidant packages, which subsequently introduce new extractables.[3]International Council for Harmonisation, “ICH Q3E Draft Guidance on Extractables and Leachables,” ich.org Ethylene-oxide sterilization leaves residual ethylene chlorohydrin, which must remain below 4 µg/device under ISO 10993-7:2024 limits. These scientific and regulatory challenges extend development timelines, restraining near-term growth of the thermoplastic elastomers in the medical devices market.

Cost Premium vs PVC and Silicone in Volume Applications

Medical-grade SEBS is priced at approximately USD 4.50-7.00/kg, nearly three times the cost of flexible PVC. While TPE overmolding can eliminate assembly steps and reduce total system costs by up to 15%, it requires capital investment in two-shot equipment, which costs between USD 200,000 and 500,000 per press. For commodity items such as 15 billion syringe plungers produced annually, even a USD 0.02 material cost difference can result in USD 300 million in global expenditure. This economic disparity limits the adoption of thermoplastic elastomers in medical devices, particularly in price-sensitive developing regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: SEBS Leads, PEBA Accelerates on Catheter Demand

In 2025, styrenic block copolymers accounted for 43.18% of the thermoplastic elastomers in medical devices market size due to their cost-effective transparency and 50 kGy gamma stability. PEBA is expected to grow at an annual rate of 7.12% through 2031, driven by the increasing demand for neurovascular and peripheral-vascular catheters requiring ultra-thin, kink-resistant walls. Arkema’s bio-based Pebax Rnew 30R53, with 30% castor-oil content, achieves Shore D 53 hardness, aligning with EU Green Deal procurement rules. TPU held 22% of revenue in 2025, preferred for infusion-set tubing designed to withstand pump-driven abrasion for seven days of wearable use. TPE-E and TPC are suitable for autoclave applications up to 121 °C, although their ester linkages limit gamma stability. TPV and TPO remain below 8%, constrained by opacity and higher extractables.

By Application: Wearables Outpace Legacy Tubing Growth

Catheters and tubing contributed 31.3% of 2025 revenue, reflecting steady demand from cardiovascular and dialysis procedures. However, wearables and skin-contact interfaces are growing 175 basis points faster than the overall thermoplastic elastomers in the medical devices market and are expected to capture a larger share of material tonnage by 2031. Continuous-glucose-monitor shipments, supported by China’s 2025 reimbursement policy, require multi-layer SEBS adhesive gaskets that maintain tackiness while lifting cleanly after 14 days.

Wearables & skin-contact interfaces, which hold an 7.34% share, benefit from overmolding to offset LSR pricing, but broader adoption depends on OEMs’ willingness to invest in two-shot presses. Pharmaceutical vial stoppers require TPE grades capable of withstanding over 50 autoclave cycles, driving demand for TPE-E compounds that maintain dimensional stability under steam.

By Processing Technology: Injection Molding Gains on Part Consolidation

Extrusion accounted for 38.19% of 2025 processing-technology revenue, as it remains the primary method for IV and dialysis tubing production. Injection molding, however, is growing at 7.41% through 2031, as medical-device engineers increasingly evaluate total landed costs rather than focusing solely on resin prices. A two-shot press can produce an insulin-pen barrel with an integrated grip in 45 seconds, compared to 90 seconds for separate molding and assembly, reducing labor costs by 35-40%.

Geography Analysis

In 2025, North America accounted for 36.33% of the revenue in the thermoplastic elastomers for medical devices market. This dominance is supported by key clusters in Minnesota, Massachusetts, and California, where industry leaders such as Medtronic, Abbott, and Boston Scientific are scaling new catheter and wearable lines under FDA scrutiny. Meanwhile, Europe, contributing a steady 28% to the market revenue, maintains its position due to stricter MDR documentation, which benefits established material suppliers capable of providing comprehensive E&L dossiers. Asia-Pacific, currently holding 26% of the market, is expected to drive growth, with an expansion rate of 7.63% projected through 2031.

The region's growth is driven by three key factors. Firstly, with China and India promoting local sourcing, Teknor Apex's 2026 joint venture, PolyTek, with DCM Shriram, is set to streamline operations. Their in-region compounding reduces lead times by six weeks. Secondly, as reimbursement for continuous-glucose monitoring expands, millions more lives are covered, encouraging sensor manufacturers to localize assembly. Lastly, Japanese and South Korean OEMs are focusing on high-purity grades; suppliers meeting ISO 10993-18 standards can secure price premiums of 10-15%.

In contrast, Latin America and the combined regions of the Middle East & Africa account for a mere 8% of the thermoplastic elastomers in medical devices market revenue. High import duties and a limited installed base discourage investments in advanced two-shot injection presses. Additionally, while legacy PVC remains acceptable for short-term consumables, it is notable that major multinationals might redirect surplus capacity from the West to these regions. This shift could occur once DEHP sales face restrictions in Europe and North America.

Competitive Landscape

HEXPOL, Teknor Apex, KRAIBURG TPE, Avient, and BASF dominate the thermoplastic elastomers in medical devices market, collectively holding a majority share of the global medical-grade capacity. The market's power dynamics are influenced by the inertia of the Medical Device Regulation (MDR), where switching resin grades necessitates new reviews by notified bodies, a process that can extend up to two years. In a strategic move, HEXPOL is reorganizing in 2026, consolidating 14 of its plants under a unified quality management system. This change will facilitate the transfer of master batches across plants without the need for separate registrations and will streamline audits from original equipment manufacturers (OEMs).

Key strategies in the market include vertical integration, as seen with GEON’s acquisition of Foster Corporation in 2025; geographic expansion, highlighted by Teknor Apex’s joint venture with PolyTek in India; and a push for sustainability, exemplified by Arkema’s introduction of a 30% bio-based version of Pebax Rnew. Patent applications are increasingly centered on silane-modified SEBS, which allow for primer-free bonding, and on antioxidant chemistries that preserve gamma clarity while adhering to ISO 10993-18 extractables limits. While smaller players like RTP Company are carving out a niche by providing bespoke grades with a minimum order of 500 kg, accelerating prototype iterations for med-tech startups, they still operate on a smaller scale compared to the industry's integrated giants.

Looking ahead, the market's focus will likely shift to additive-manufacturing filaments that meet ISO 13485 certification and ultra-soft Shore 00 wearables designed for 30-day skin contact. Both innovations will necessitate new sensitization protocols. Suppliers who achieve early acceptance from notified bodies in these emerging niches stand to gain premium margins, potentially shifting the market share further towards these innovation frontrunners.

Thermoplastic Elastomers In Medical Devices Industry Leaders

BASF SE

Covestro AG

Kraton Corporation

Lubrizol Corporation

Teknor Apex Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: GEON Performance Solutions acquired Arkadia Plastics, adding 15,000 tonnes of annual compounding in Mexico and China to shrink trans-Pacific lead times by 4-6 weeks.

- March 2026: HEXPOL AB consolidated 14 global plants into the Hexpol Thermoplastics division, reducing OEM qualification timelines by up to 12 weeks through unified MDR files.

- February 2025: Prism Worldwide and Sherwood Industries partnered to introduce recycled-content TPE sheets for automotive bin mats and consumer products, demonstrating cross-industry circularity potential.

- January 2025: GEON Performance Solutions purchased Foster Corporation, adding 12,000 tonnes of ultrapure medical-grade capacity in Connecticut and deepening its Thermoplastic Elastomers in Medical Devices market footprint.

Global Thermoplastic Elastomers In Medical Devices Market Report Scope

As per the scope of the report, thermoplastic elastomers (TPEs) are critical in medical device design, offering the flexibility of rubber with the processability of plastics. They enable, via injection molding or extrusion, soft-touch ergonomics, overmolding on rigid substrates, and high-purity, biocompatible, sterilizable (EtO, gamma) components. TPEs are ideal replacements for latex and PVC due to low extractables/leachables and recyclability.

The thermoplastic elastomers in the medical devices market are segmented by material type, application, processing technology, and geography. By material type, the market includes styrenic thermoplastic elastomers / styrene-ethylene-butylene-styrene (TPE-S/SEBS), thermoplastic polyurethane (TPU), amide-based thermoplastic elastomers/polyether block amide (TPE-A/PEBA), polyester-based thermoplastic elastomers / thermoplastic copolyester (TPE-E/TPC), thermoplastic vulcanizate (TPV), and thermoplastic polyolefin (TPO). By application, the market is categorized into catheters & tubing, syringes & plungers, stoppers & seals, connectors & device housings, and wearables & skin-contact interfaces. By processing technology, the market is segmented into extrusion, injection molding, blow molding & film, overmolding & 2K, and additive/other. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Thermoplastic Elastomer - Styrenic / Styrene-Ethylene-Butylene-Styrene (TPE-S/SEBS) |

| Thermoplastic Polyurethane (TPU) |

| Thermoplastic Elastomer - Amide / Polyether Block Amide (TPE-A/PEBA) |

| Thermoplastic Elastomer - Polyester / Thermoplastic Copolyester (TPE-E/TPC) |

| Thermoplastic Vulcanizate (TPV) |

| Thermoplastic Polyolefin (TPO) |

| Catheters & Tubing |

| Syringes & Plungers |

| Stoppers & Seals |

| Connectors & Device Housings |

| Wearables & Skin-Contact Interfaces |

| Extrusion |

| Injection Molding |

| Blow Molding & Film |

| Overmolding & 2K |

| Additive / Other |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Material Type | Thermoplastic Elastomer - Styrenic / Styrene-Ethylene-Butylene-Styrene (TPE-S/SEBS) | |

| Thermoplastic Polyurethane (TPU) | ||

| Thermoplastic Elastomer - Amide / Polyether Block Amide (TPE-A/PEBA) | ||

| Thermoplastic Elastomer - Polyester / Thermoplastic Copolyester (TPE-E/TPC) | ||

| Thermoplastic Vulcanizate (TPV) | ||

| Thermoplastic Polyolefin (TPO) | ||

| By Application | Catheters & Tubing | |

| Syringes & Plungers | ||

| Stoppers & Seals | ||

| Connectors & Device Housings | ||

| Wearables & Skin-Contact Interfaces | ||

| By Processing Technology | Extrusion | |

| Injection Molding | ||

| Blow Molding & Film | ||

| Overmolding & 2K | ||

| Additive / Other | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the Thermoplastic Elastomers in Medical Devices market be by 2031?

The Thermoplastic Elastomers in Medical Devices market size is projected to reach USD 4.6 billion by 2031, expanding at a 5.59% CAGR over 2027-2031.

Which material currently leads commercial adoption?

Styrenic block copolymers accounted for 43.18% of 2025 revenue, the largest single share in the Thermoplastic Elastomers in Medical Devices market.

What is the fastest-growing application segment through 2031?

Wearables and skin-contact interfaces are advancing at a 7.34% CAGR, outpacing the broader Thermoplastic Elastomers in Medical Devices market.

Why is Asia-Pacific important for future growth?

Regional manufacturing mandates, rising reimbursement for diabetes wearables, and new joint ventures position Asia-Pacific to grow at 7.63% and narrow the gap with North America.

Which sterilization method drives material differentiation?

Gamma irradiation at 50 kGy rewards SEBS grades that retain tensile and optical properties, prompting OEMs to specify validated gamma-stable formulations.

What regulatory factor most influences supplier selection?

EU MDR Article 120 treats resin substitutions as significant changes, so OEMs prefer suppliers that already hold MDR-compliant dossiers to avoid 12-24 months of re-validation.

Page last updated on: