Thermoelectric Modules Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

| Growth Rate | 7.24% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thermoelectric Modules Market Analysis by Mordor Intelligence

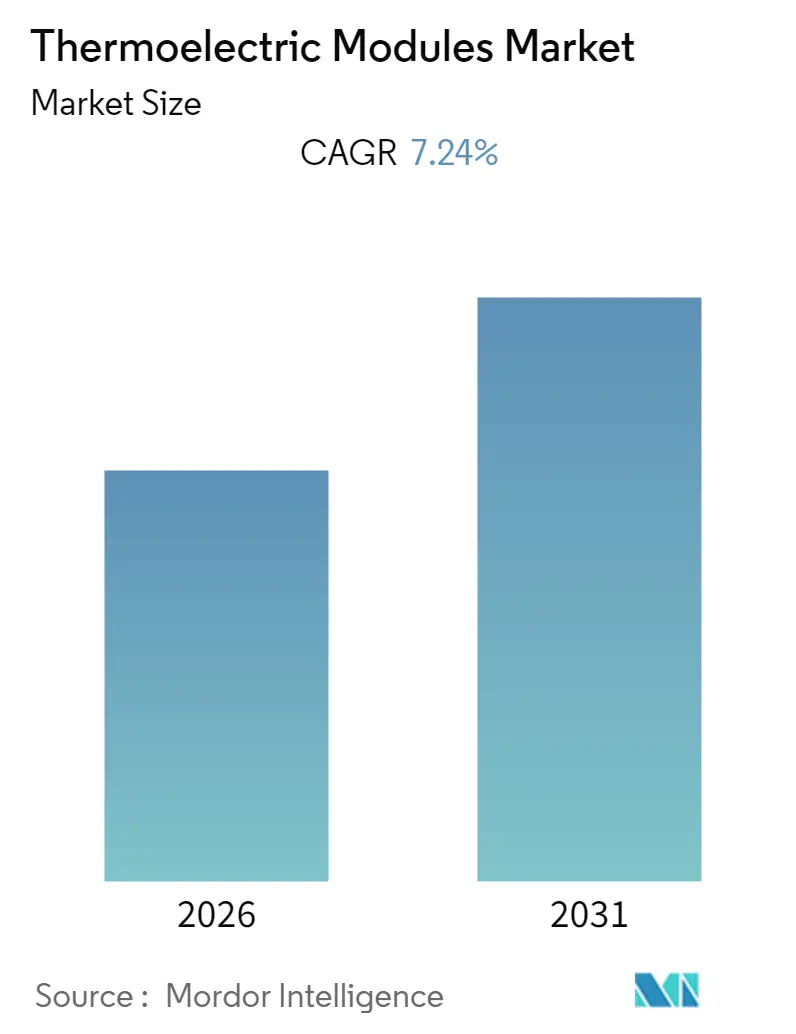

The Thermoelectric Modules Market size is expected to register a CAGR of 7.24% during the forecast period.

The automotive segment is likely to witness significant growth during the forecast period.

Lately, mRNA vaccine technology has seen major improvements due to various technologies, such as CRISPR, leading to widespread commercial production. Furthermore, it indicates a shift toward such kinds of vaccines in the future. However, mRNA vaccines are stored strictly under cold temperatures to prevent their deterioration, which will present significant opportunities to micro thermoelectric module players involved in the market.

The Asia-Pacific region is likely to be the fastest-growing market during the forecast period owing to its significant manufacturing capacity and rising demand.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Thermoelectric Modules Market Trends and Insights

Automotive Segment to Witness Significant Growth

The automotive sector is growing globally and undergoing a significant shift toward electric-based propulsion. Furthermore, manufacturers are introducing new features in the vehicles, such as ventilated seats, multiple zone climate control, better air conditioning, and better engine temperature control.

In 2020, globally, around 78 million motor vehicle units were produced compared to 92 million units in the preceding year. This decline was expected to be temporary and did not reflect the true growth of the market since it was impacted by the COVID-19 pandemic. As mentioned above, these automotive vehicles employ micro thermoelectric modules to control the temperature efficiently.

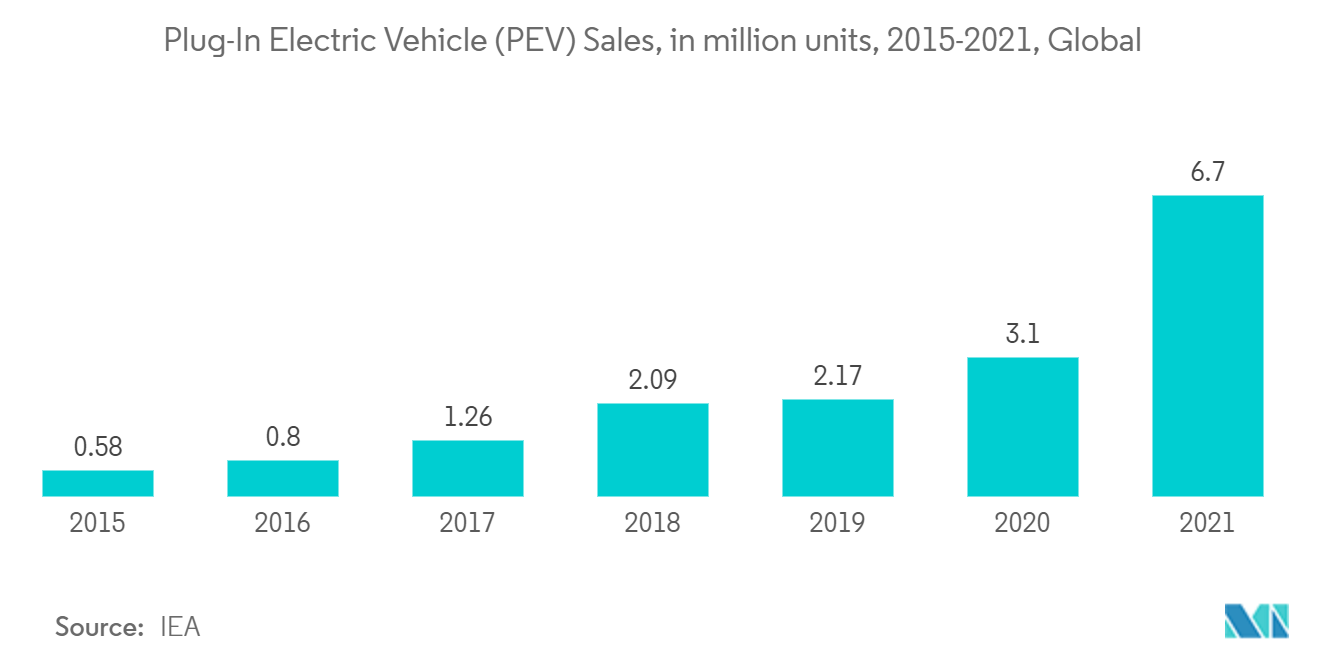

As part of the shift toward electric-based propulsion, battery temperature is required to be regulated for efficient operations. As per a forecast, the number of electric vehicles in 2025 is expected to be around 54 million units compared to 12 million units in 2021. This is likely to drive the micro thermoelectric module market, in turn, during the forecast period.

In November 2021, Tesla Inc. announced plans to invest up to CNY 1.2 billion (USD 187.91 million) to expand production capacity at its Shanghai factory. Tesla's Shanghai factory was designed to make up to 500,000 cars a year and currently has the capacity to produce Model 3 and Model Y vehicles at a rate of 450,000 total units a year.

In August 2021, Toyota announced its new BEV series, Toyota bZ, and established a full line-up of electrified vehicles. A concept version of the first model in the series was unveiled at Auto Shanghai, and 15 BEVs are expected to be introduced globally by 2025.

Thus, owing to the abovementioned factors and in line with the growth of the automotive sector, the thermoelectric market is also expected to grow.

Asia-Pacific to be the Fastest-growing Region

The Asia-Pacific region is home to the largest chunk of the world's population and countries with the highest economic growth rates. The countries in the region are witnessing the increasing adoption of electric vehicles, developing cold chains for food security and other applications, and advancements in healthcare technologies and equipment, such as organ transportation and preservation systems.

The government of China is encouraging people to adopt electric vehicles. The country has already made plans to phase out diesel fuel, which runs the current generation of commercial vehicles, such as trucks. The country is planning to ban diesel and petrol vehicles completely by 2040. China is a key player in the global electric bus market, and it is anticipated to sustain its dominance during the forecast period. In May 2020, more than 420,000 electric buses were in use in China, which amounted to about 99% of the global fleet. The keen focus on electrification of public transit with prevalent subsidies and national regulations is a major factor contributing to the high market share held by China in the global electric bus market.

India, as of 2020, had 8,200 cold storage facilities, of which 75% are suitable only for single commodities, mainly potatoes. The number of cold storage facilities is likely to rise significantly due to the surge in online grocery, processed foods, and pharmaceutical sales. These new use cases will result in multiple smaller cold-storage facilities in the cities to ensure efficient last-mile delivery.

Furthermore, APAC is growing significantly in the organ preservation space. The surging incidence rate of various organ failures in the region and increasing healthcare expenditure is expected to boost the market's growth. Moreover, due to the economic upturn in the region, the demand for advanced treatments has witnessed a surge. These organ preservation systems employ micro thermoelectric modules to regulate the temperature, which is critical for organ life, and, in turn, is likely to aid the growth of the micro thermoelectric modules market.

Thus, owing to the abovementioned factors, the Asia-Pacific region is likely to be the fastest-growing regional market during the forecast period.

Value Chain Analysis

The thermoelectric module (TEM) value chain starts upstream with thermoelectric material preparation, notably high-purity bismuth telluride (Bi2Te3), followed by ceramic substrate production and metallization/vacuum film coating, then precision assembly into single-stage and multi-stage modules. In the midstream, manufacturers and vertically integrated suppliers (for example, Ferrotec Corporation) convert these inputs into standardized and custom TEMs, while specialized module providers such as Sheetak, Crystal Ltd, and SCTBNORD support application-specific designs that prioritize compact form factors, reliability, and rapid prototyping.

Downstream, TEMs are integrated with thermal interface materials, heat sinks, and control electronics into cooling or power-generation subsystems, then distributed through direct OEM relationships and electronics/thermal management channels. Demand pull comes from precision thermal control use cases including semiconductor equipment cooling and temperature cycling, optoelectronics, automotive thermal management, and medical diagnostics. Supplier moves that bundle modules with matched control electronics (for example, a June 2026 single-source TEC module plus controller partnership announced by Sheetak) reflect a shift from component supply toward integrated, easier-to-deploy subsystems for industrial and IoT deployments.

Competitive Landscape

The thermoelectric modules market is partially fragmented. Some of the major players involved in the market are CUI Devices, Thermonamic Electronics (Jiangxi) Corp. Ltd, TEC Microsystems, KELK Ltd, and Guangdong Fuxin Technology Co. Ltd.

Thermoelectric Modules Industry Leaders

CUI Devices

TEC Microsystems

KELK Ltd.

Thermonamic Electronics (Jiangxi) Corp., Ltd.

Guangdong Fuxin Technology Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: TEC Microsystems GmbH significantly expanded and updated its MC06 thermoelectric module series to include more than 500 variants. The broader configuration range supports tighter fit to end-equipment thermal and form-factor requirements, helping OEMs reduce redesign cycles when selecting modules for different cooling loads. This reinforces the supplier position in applications where qualification and repeatability are critical.

- January 2026: Sheetak launched the muCENTUM miniature thermoelectric cooler series for precision temperature control in optoelectronics. The release focuses on compact, high-precision thermal stabilization needs, which can shorten integration timelines for photonics and sensing hardware. It also points to continued product innovation centered on miniaturization and application-specific performance.

- September 2024: E-ThermoGentek Co., Ltd. announced the S1alpha Series, an ultra-compact stand-alone power supply for IoT applications with an optimized power circuit for thermoelectric generation, developed in collaboration with Murata Manufacturing Co., Ltd. The collaboration links thermoelectric energy harvesting to established electronics component ecosystems, supporting faster adoption in sensor and predictive-maintenance nodes. It also broadens the downstream pull for thermoelectric technologies beyond cooling into power-generation modules and systems.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as revenues generated from thermoelectric modules used to move heat (cooling or heating) or to convert a temperature difference into electrical power, sold across industrial and commercial end users and counted at the module level.

Scope exclusions: We exclude full systems that only integrate modules (finished coolers, refrigerators, chillers, or complete generators) unless the thermoelectric module value is separately identifiable.

Segmentation Overview

- Stage

- Single Stage

- Multi Stage

- Functionality

- General Purpose

- Deep Cooling

- End Use Aplication

- Aerospace and Defense

- Automotive

- Consumer Electronics

- Heathcare

- Food and Beverages

- Energy and Utility

- Referigerant and Chillers

- Other End Use Applications

- Geography

- North America

- Europe

- Asia-Pacific

- South America

- Middle-East

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the foundation for volumes, end-use demand signals, and realistic pricing bands that can be defended. We reviewed public sources such as US DOE and national energy agencies for thermal efficiency program materials, USITC and UN Comtrade style trade statistics for shipment direction checks, and ISO/IEC aligned standards references that clarify operating ranges and test conditions.

To keep assumptions anchored to what manufacturers can actually supply, we also used company filings, annual reports, and investor presentations that discuss product mix and capacity moves, along with reputable electronics and thermal engineering journals for material and performance trend context. Where needed, a paid subscription for company financials and a patent database were used to map active innovation and to sanity check the pace of adoption. The sources listed here are illustrative, and many other public materials were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on confirming what is actually shipped as a module, typical price ranges by specification, and how demand changes by application (cooling versus power generation). We spoke with a mix of manufacturers, distributors, system integrators, and large end users across APAC, EMEA, and the Americas to close gaps from desk findings and recheck key assumptions before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 13% | APAC: 49% |

| Mid tier: 55% | Functional/Unit leaders: 40% | EMEA: 33% |

| Smaller Players: 14% | Managers: 47% | Americas: 18% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up approach, where end-use demand pools were reconstructed from application adoption signals and then converted into module value using price and specification weights. On the top-down side, we used indicators such as electronics production intensity, automotive thermal management penetration, medical and laboratory equipment demand, and refrigeration and chiller retrofits, which are then translated into likely module unit requirements by application.

Selective bottom-up checks were used to keep totals realistic, including sampled supplier revenue splits, channel discussions on average selling price movements, and volume sense checks tied to capacity additions and lead-time discussions. For forecasting, we used scenario analysis supported by a light multivariate view that links demand to a few drivers, such as industrial output, EV and advanced electronics builds, and the pace of energy efficiency investments. Where bottom-up detail was missing for smaller geographies, gaps were handled through proxy adoption rates and pricing ladders that were validated in interviews, followed by a consistency pass against trade flow direction and end-use growth rates.

Data Validation & Update Cycle

Outputs were checked through triangulation across independent signals, including cross-checking implied module shipments against application-level demand indicators and sanity testing price progression versus known material and manufacturing constraints. Any large variance by region or end use triggered a second look at assumptions, followed by a peer review step so calculations and logic were reverified before sign-off.

The report is refreshed annually, and interim updates are made when there are material events such as major capacity expansions, sharp input cost moves, or policy changes tied to energy efficiency. Before delivery, we do a fresh review pass so clients receive the most current version of the dataset and narrative.

Mordor Intelligence's Thermoelectric Modules Market Sizing Compared With Other Published Estimates

Published market sizes for thermoelectric modules often vary because the boundary of what counts as a module sale is not always consistent, and because pricing and adoption assumptions can be handled differently across applications. Differences also come from the choice of base year, currency timing, and how quickly older assumptions are refreshed when end-use demand shifts.

Trade-direction checks and application demand signals (such as electronics output and automotive thermal management penetration) are the evidence that keep Mordor Intelligence's estimate tied to module-only revenues rather than finished cooling or power systems, which can inflate totals when bundled values are counted.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.53 B (2024) | |

| Industry Publisher A | USD 0.52 B (2024) | Uses a broader type split that can mix module formats with adjacent thermoelectric subassemblies, and the definition does not clearly separate module value from integrated device pricing in some end uses. |

| Industry Publisher B | USD 0.64 B (2025) | Starts from a later base year with a higher near-term growth assumption, and does not clearly state how ASP changes are applied across cooling, heating, and power generation use cases. |

The spread across sources mainly comes down to scope boundaries and how quickly price and adoption assumptions are updated when end-use demand changes. By keeping the model traceable to demand indicators, module unit needs, and practical pricing checks, the final number stays repeatable and easier to explain during planning discussions.

Key Questions Answered in the Report

What is the current Micro Thermoelectric Modules Market size?

The Micro Thermoelectric Modules Market is projected to register a CAGR of 7.24% during the forecast period (2026-2031)

Who are the key players in Micro Thermoelectric Modules Market?

CUI Devices, TEC Microsystems, KELK Ltd., Thermonamic Electronics (Jiangxi) Corp., Ltd. and Guangdong Fuxin Technology Co., Ltd. are the major companies operating in the Micro Thermoelectric Modules Market.

Which is the fastest growing region in Micro Thermoelectric Modules Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Micro Thermoelectric Modules Market?

In 2025, the North America accounts for the largest market share in Micro Thermoelectric Modules Market.

What years does this Micro Thermoelectric Modules Market cover?

The report covers the Micro Thermoelectric Modules Market historical market size for years: 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Micro Thermoelectric Modules Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: