Size and Share of Thermal Interface Materials Market For DRAM Packaging

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

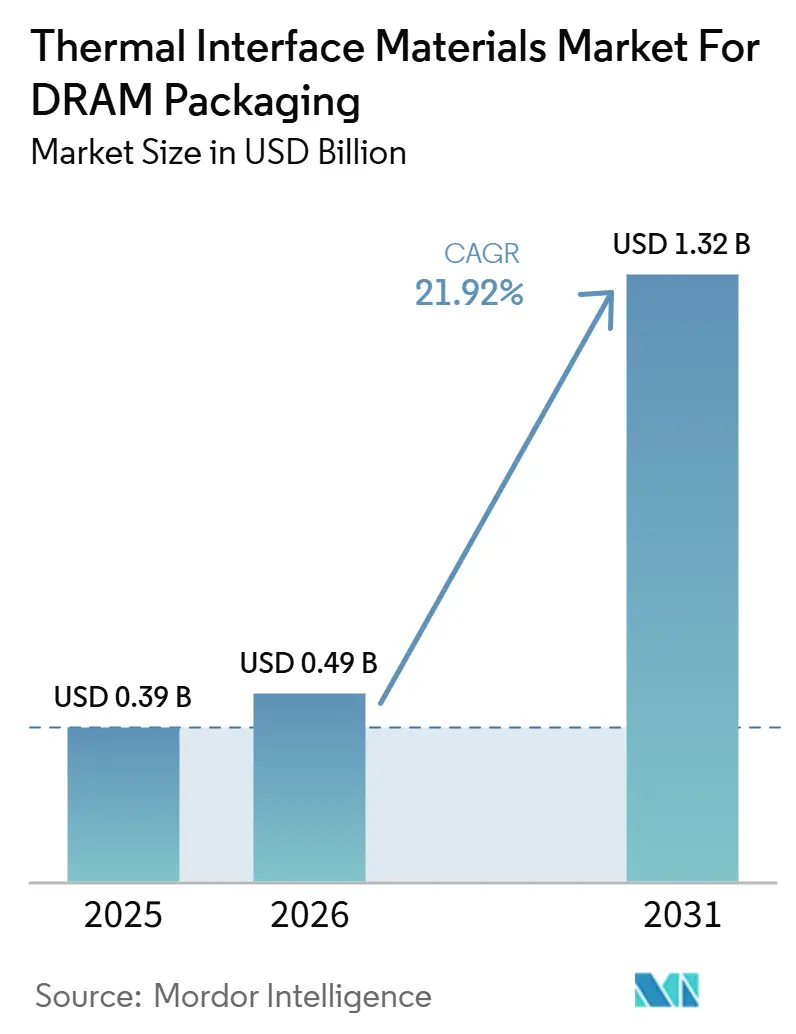

| Market Size (2026) | USD 0.49 Billion |

| Market Size (2031) | USD 1.32 Billion |

| Growth Rate (2026 - 2031) | 21.92% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analysis of Thermal Interface Materials Market For DRAM Packaging by Mordor Intelligence

The thermal interface materials market for DRAM packaging industry size was valued at USD 0.39 billion in 2025 and is estimated to grow from USD 0.49 billion in 2026 to reach USD 1.32 billion by 2031, at a CAGR of 21.92% during the forecast period 2026-2031. The thermal interface materials market for DRAM packaging industry is being lifted by the rapid rise in high-bandwidth memory content inside AI accelerators, where higher thermal design power is concentrating more heat into smaller package footprints. This pattern is tightening performance requirements across lid, die, and interconnect interfaces, which is moving supplier focus away from standard polymer materials and toward higher-conductivity, lower-outgassing, and more stable formulations. Asia-Pacific remained the center of demand because memory manufacturing and advanced packaging capacity are concentrated in South Korea, Taiwan, Japan, and China, while North America is gaining momentum from AI infrastructure investment and reshoring efforts. Competitive activity in the thermal interface materials market for DRAM packaging industry remains centered on large specialty materials companies with qualified positions at memory manufacturers, even as smaller firms target niche interface points with newer carbon-based and nanostructured products. Cost pressure in silicone and filler inputs, together with long qualification cycles in advanced packaging lines, is slowing supplier rotation, but the thermal performance gap in next-generation DRAM packages still leaves meaningful room for product upgrades and co-designed material solutions.

Key Report Takeaways

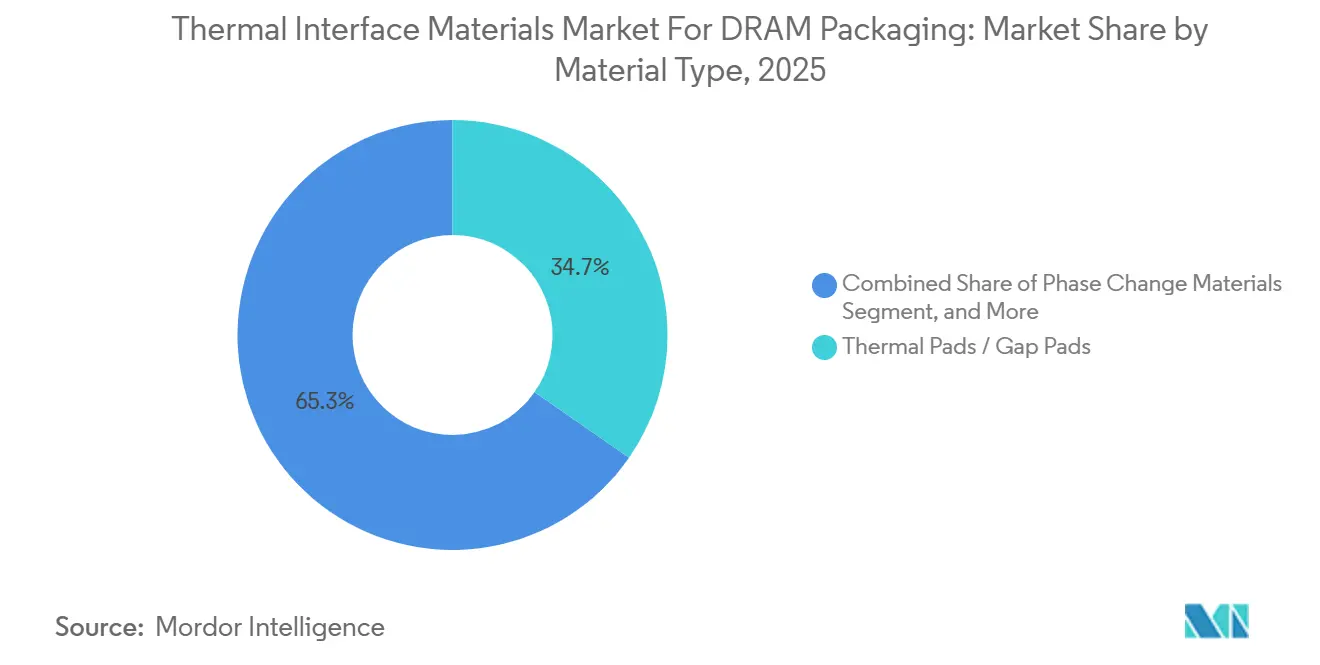

- By material type, thermal pads and gap pads held 34.67% share of the thermal interface materials market for DRAM packaging industry in 2025, while thermal gels and dispensable gap fillers are projected to expand at a 22.15% CAGR through 2031.

- By DRAM packaging and product application, server DRAM modules accounted for 38.56% of 2025 revenue in the thermal interface materials for DRAM packaging market, while HBM stacks are expected to advance at a 22.75% CAGR through 2031.

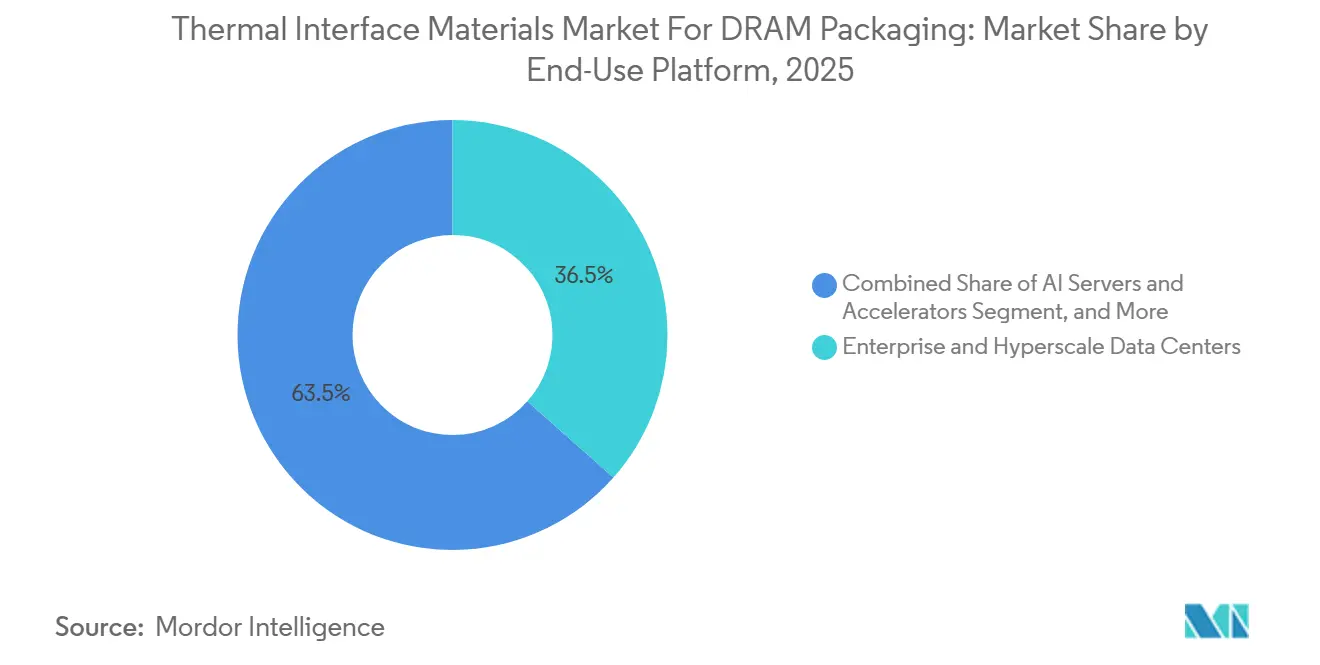

- By end-use platform, enterprise and hyperscale data centers represented 36.54% share of the thermal interface materials market for DRAM packaging industry in 2025, while AI servers and accelerators remained the fastest-growing platform through 2031.

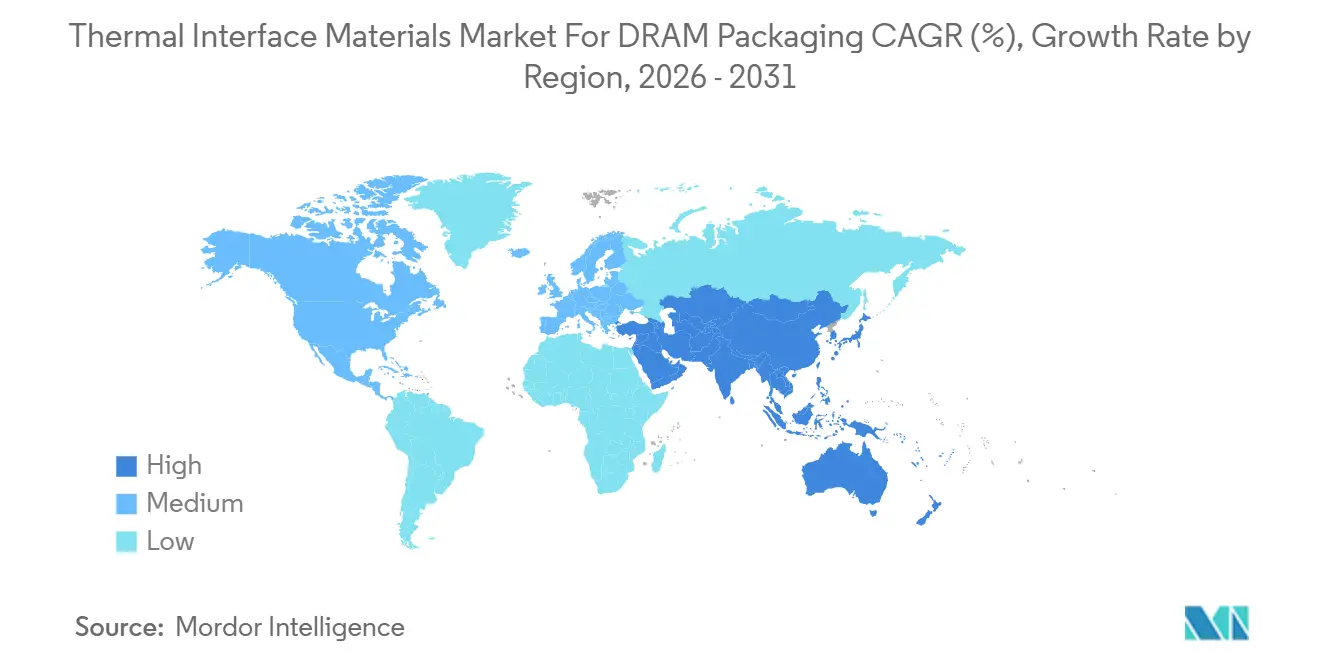

- By geography, Asia-Pacific held 82.67% of 2025 revenue, while North America is projected to record the highest CAGR at 22.87% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Insights and Trends of Thermal Interface Materials Market For DRAM Packaging

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising HBM Stack Height and D2D Heat Density | +5.5% | Global, with core volume in South Korea, Taiwan, and China | Short term (≤ 2 years) |

| Shift to Hybrid Bonding and Thermal Co-Optimization | +4.8% | Asia-Pacific core, with spillover to North America | Medium term (2-4 years) |

| Expansion of AI Server Memory Content Per System | +4.2% | North America and Asia-Pacific, with secondary exposure in Europe | Short term (≤ 2 years) |

| Reliability Requirements in 24/7 Enterprise Memory Systems | +3.1% | Global, with early gains in North America and Germany | Medium term (2-4 years) |

| High Thermal Conductivity Demand in Ultra-Thin Interface Gaps | +2.4% | Asia-Pacific, with spillover to North America and Europe | Long term (≥ 4 years) |

| Qualification of Silicone-Free and Low-Outgassing TIM Formulations | +1.6% | Global, with early concentration in Taiwan and the United States | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising HBM Stack Height and D2D Heat Density

The thermal interface materials market for DRAM packaging industry is responding directly to the rise in stacked memory architectures, where more dies are being placed within tighter vertical limits. Taller HBM structures increase serial thermal resistance from the lower dies to the package lid, which makes heat removal harder even when external cooling improves.[1]Siemens EDA, “HBM3e and HBM4 IC Design Guide for Next-Generation High Bandwidth Memory,” Siemens EDA, blogs.sw.siemens.com Siemens EDA noted that HBM4 design targets raise both stack height and I/O density, which increases localized heat concentration in the die-to-die physical layer. Imec showed the scale of this thermal challenge in 2025, reporting a peak GPU temperature of 141.7°C in a 3D HBM-on-GPU setup without mitigation, versus 69.1°C in a 2.5D baseline. SK hynix responded in May 2026 by introducing its iHBM solution with integrated cooling elements in the D2D PHY area, which cut thermal resistance by 30% while staying compatible with existing System-in-Package structures. As a result, the thermal interface materials market for DRAM packaging industry is moving toward materials that can support tighter gaps, more stable bond lines, and higher conductivity at multiple interface positions inside the package.

Shift To Hybrid Bonding and Thermal Co-Optimization

The thermal interface materials market for DRAM packaging industry is also being reshaped by the move from thermal compression bonding toward hybrid copper bonding in advanced memory assembly. This shift changes where heat builds up and how material selection affects both package integrity and thermal performance. A 2025 review in Electronics described how SiCN dielectrics, nano-twinned copper, and polymer composites each bring different tradeoffs in thermal resistance, warpage control, and coefficient of thermal expansion mismatch. Imec’s cross-technology co-optimization work showed that hybrid-bonded 3D systems can move closer to 2.5D thermal behavior when technology and system cooling decisions are modeled together, not in isolation.[2]Imec, “Imec Mitigates Thermal Bottleneck in 3D HBM-on-GPU Architectures Using System-Technology Co-Optimization,” Imec, imec-int.com That development is splitting product demand into separate tracks for intra-stack materials and lid-interface materials, which makes supplier portfolios more specialized. In practical terms, the thermal interface materials market for DRAM packaging industry is seeing procurement shift from a single material decision toward a broader package-level thermal design decision.

Expansion of AI Server Memory Content Per System

The thermal interface materials market for DRAM packaging industry is benefiting from the rapid increase in memory content per AI server system, which raises both material volume per unit and performance requirements per interface. NVIDIA stated in 2026 that its Vera Rubin platform carries 288 GB of HBM4 per GPU, while the full NVL72 rack reaches 20.7 TB of HBM4, which shows how quickly memory density is moving upward in AI systems. Higher HBM content does not only increase chip count, it also expands the number of thermally sensitive junctions that must remain stable during sustained operation. That matters because the package must manage more heat across a denser memory footprint without allowing drift in bond-line thickness or outgassing behavior. The effect is especially strong in rack-scale AI infrastructure, where heat from memory, interconnects, and compute dies accumulates across tightly packed modules. For that reason, the thermal interface materials market for DRAM packaging industry is being driven as much by the memory content in each deployed system as by overall accelerator shipment growth.

Reliability Requirements In 24/7 Enterprise Memory Systems

The thermal interface materials market for DRAM packaging industry is also being supported by stricter reliability standards in enterprise and hyperscale memory environments that run near thermal limits for long periods. A 2026 study in Energies found that server-oriented memory liquid cooling performance remained sensitive to memory-side thermal resistance across several cold plate approaches, which points back to interface material behavior as a critical control point. In these environments, pump-out, delamination, and bond-line drift matter as much as bulk conductivity because the interface must hold performance through repeated thermal cycling. That is increasing demand for materials with verified long-term stability, especially in platforms that use liquid cooling or face high humidity exposure. It also favors suppliers that can show repeatable durability data across realistic server duty cycles, not only laboratory conductivity figures. This is keeping the thermal interface materials market for DRAM packaging industry aligned with premium formulations that can support both temperature margin control and long service life.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost Pressure from Premium Filler and Resin Inputs | -3.2% | Global, concentrated in Asia-Pacific supply chains | Short term (≤ 2 years) |

| Qualification Risk in Advanced DRAM Packaging Lines | -2.6% | Global, with concentration in South Korea and Taiwan | Medium term (2-4 years) |

| Substrate Warpage and Process Window Narrowing | -1.8% | Asia-Pacific core, with spillover to North America | Medium term (2-4 years) |

| Competition from Integrated Cooling and Package-Level Thermal Designs | -1.2% | Global, with early design wins in South Korea and the United States | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cost Pressure from Premium Filler And Resin Inputs

The thermal interface materials market for DRAM packaging industry faces clear cost pressure from premium fillers and silicone-based carrier systems used in high-performance formulations. Shin-Etsu announced in April 2026 that it would raise prices on all silicone products by 10% or more, citing crude oil and naphtha cost increases linked to Middle East supply conditions.[3]Shin-Etsu Chemical Co., Ltd., “Silicone Price Revision Notice,” Shin-Etsu Chemical Co., Ltd., shinetsusilicone-global.com That matters because silicone-based systems still account for much of the qualified material base in DRAM packaging. The effect is stronger in thinner bond lines, where high-purity and tightly controlled filler systems are needed to keep performance stable in compact geometries. Larger suppliers can absorb some of this pressure through scale and broader sourcing networks, while smaller formulators have less room to protect margins. As a result, the thermal interface materials market for DRAM packaging industry is seeing higher input costs reinforce incumbent strength at the same time that next-generation products require more specialized ingredients.

Qualification Risk in Advanced DRAM Packaging Lines

The thermal interface materials market for DRAM packaging industry also remains constrained by long and demanding qualification processes in advanced memory packaging lines. New formulations must prove thermal performance, contamination control, and bond-line stability before they can displace established materials in high-volume production. The burden is heavier in HBM and other advanced DRAM packages because tighter thermal margins leave less room for drift over repeated cycling and extended workloads. That slows supplier rotation even when technical performance looks strong at the development stage. It also means that the packaging roadmap can move to a new memory generation before a new material has completed adoption at the previous node. This timing risk keeps the thermal interface materials market for DRAM packaging industry favorable to suppliers with embedded engineering support and prior qualification history at major memory makers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Gel-Dispensing Momentum Challenges Established Pad Formats

Thermal pads/gap pads held 34.67% of the thermal interface materials market for DRAM packaging industry share in 2025, which kept them as the leading material category. Their strong position came from established use in server DRAM modules and enterprise memory systems, where consistent bond-line control and easier handling remained valuable. They also fit well with automated assembly flows and support rework needs better than several alternative formats. That combination kept pad-based products central to conventional DRAM module assembly even as packaging demands became more complex. The thermal interface materials for DRAM packaging market still relies on these formats where manufacturability and qualification history matter as much as peak conductivity.

Thermal gels and dispensable gap fillers are forecast to grow at a 22.15% CAGR through 2031, reflecting their better fit with tighter interface geometries in HBM stacks and 2.5D interposer-based packages. Dow’s launch of DOWSIL TC-3120 Thermal Gel in May 2026 showed how suppliers are positioning dispensable chemistries for dense, high-speed electronics with lower oil bleeding and lower condensed outgassing. Phase change materials are also gaining ground in lid-interface positions because they reduce pump-out risk during repeated cycling. Greases and pastes continue to serve conventional server platforms, but they face more pressure in advanced nodes where bond-line variation and migration risk are less acceptable. The Others category remains small in current revenue, yet it is drawing attention because carbon-based, graphite-based, and other novel materials could address interface positions that standard polymer systems serve less effectively.

By DRAM Packaging / Product Application: HBM Stacks Redefine TIM Performance Ceilings

Server DRAM modules accounted for 38.56% of the thermal interface materials for DRAM packaging market size in 2025, which made them the largest application segment. Their lead rested on the broad installed base of DDR5 RDIMM and LRDIMM platforms across enterprise servers. This segment remains commercially important because it combines high shipment volume with well-established assembly practices and long qualification cycles. Even so, its growth is slower than the broader thermal interface materials for DRAM packaging market because packaging complexity is rising faster in AI-focused memory configurations. Conventional server memory will therefore remain a volume anchor, but it will not define the upper end of future material performance requirements.

HBM stacks are projected to advance at a 22.75% CAGR through 2031, which makes them the fastest-growing application area in the thermal interface materials for DRAM packaging market. Their growth reflects the shift toward memory-on-package designs in AI accelerators and high-performance computing systems, where die count and thermal density both keep rising. Advanced DRAM packages are expanding for similar reasons because 2.5D and near-memory architectures create additional thermal interfaces that standard DIMM formats do not require. CXL-attached DRAM modules remain early in adoption, but Micron has said CXL bits will represent 31% of total server DRAM bits by 2028, and Marvell launched its Structera S 30260 switch in March 2026 to support rack-level memory pooling. Client DRAM modules remain a smaller and steadier opportunity, where thermal needs are lower and cost discipline carries more weight than premium performance.

By End-Use Platform: Data Center Concentration Masks an Emerging Workstation Opportunity

Enterprise and hyperscale data centers held 36.54% of 2025 revenue, which made them the largest end-use platform in the thermal interface materials market for DRAM packaging industry. Their lead reflects continuous buildout of dense computing environments that rely on DRAM-heavy server configurations and advanced cooling methods. These deployments keep thermal interface performance under closer scrutiny because material limits can affect uptime, throttling behavior, and service intervals. The thermal interface materials for DRAM packaging market therefore sees data centers as both the largest demand pool and the strictest validation environment for premium products. Qualification success in this platform often shapes supplier credibility across adjacent memory-intensive applications.

AI servers and accelerators are the fastest-growing platform in the thermal interface materials for DRAM packaging market because each system combines higher memory density with greater sustained heat load. NVIDIA’s 2026 Vera Rubin NVL72 platform, with 20.7 TB of HBM4 per rack, illustrates how quickly package-level thermal demands are scaling in AI infrastructure. High-performance computing platforms share many of the same material needs because they also push sustained workloads through memory-dense package designs. High-end workstations, client PCs and notebooks, and industrial and embedded systems remain secondary demand pools, but they still matter because they support broad shipment volume and introduce separate needs such as low outgassing and contamination control. That quieter demand from industrial and embedded platforms is becoming more relevant where optical, telecom, and edge AI hardware is being paired with memory-intensive computing modules.

Geography Analysis

Asia-Pacific held 82.67% of the thermal interface materials market for DRAM packaging industry market share in 2025, which made the region the clear center of global demand. This concentration reflects the geographic clustering of DRAM production, HBM assembly, and advanced outsourced semiconductor assembly and test capacity across South Korea, Taiwan, Japan, and China. South Korea remains the most important country position because Samsung Electronics and SK hynix combine large HBM output with direct involvement in next-generation package thermal design. SK hynix’s 2026 iHBM launch shows how memory producers in the region are shaping both package architecture and the interface material requirements that sit around it. Taiwan adds further weight through its advanced packaging ecosystem, where interposer-based assembly and co-packaged structures increase the number of thermally sensitive interfaces that must be managed.

Japan supports the thermal interface materials market for DRAM packaging industry through high-purity materials supply and memory-related packaging operations, while China is expanding its position through domestic OSAT growth and localization efforts. At the same time, Asia-Pacific still depends on imported high-performance formulations in some premium applications, especially where specialized filler systems or low-outgassing behavior are required. North America is forecast to grow at a 22.87% CAGR through 2031, which makes it the fastest-rising regional market. This growth is being driven by AI infrastructure investment, custom qualification needs from hyperscalers, and policy support for domestic semiconductor capacity. Carbice’s partnership with DarkNX in February 2026 and its U.S. Navy qualification contract in April 2026 reflect how North American suppliers are targeting premium thermal positions that require high reliability and application-specific validation.

Demand in North America is concentrated more in qualification, deployment, and performance assurance than in large-scale DRAM die production, which lifts value intensity per approved material. Europe remains a smaller but stable part of the thermal interface materials market for DRAM packaging industry, supported by enterprise data center demand and specialized industrial computing uses. European customers place greater emphasis on compliance-sensitive formulations, which keeps interest high in silicone-free and low-outgassing products. The Rest of the World remains a smaller revenue pool, but countries in Southeast Asia and India could add relevance as packaging ambitions grow and regional electronics manufacturing broadens.

Competitive Landscape

The thermal interface materials market for DRAM packaging industry remains moderately consolidated, with a limited group of large specialty materials suppliers holding most qualified positions in high-volume memory packaging lines. Their advantage comes from established formulations, scale in raw material sourcing, and qualification history at major memory manufacturers. In this market, technical performance alone is rarely enough to displace an incumbent because suppliers also need contamination control, reliability data, and packaging support capability. That raises entry barriers and slows share movement even when newer material platforms show strong lab results. As a result, the thermal interface materials market for DRAM packaging industry continues to favor companies that can pair materials development with application engineering and production support.

Strategic moves in 2025 and 2026 show that incumbents are trying to secure future positions by aligning product development with AI and advanced packaging needs. Dow launched DOWSIL TC-3120 Thermal Gel in May 2026 for dense electronics and high-speed data applications, which signals a direct effort to address tighter thermal requirements in next-generation server and module interfaces. 3M joined both the US-JOINT Consortium in February 2025 and the JOINT3 semiconductor packaging consortium in September 2025, which shows a strategy built around deeper participation in back-end packaging development rather than stand-alone product selling. Large suppliers are therefore pushing to be part of process definition earlier in the design cycle, where qualification advantage can be locked in before volume ramps begin. This approach supports pricing power because approved materials in critical interfaces are harder to replace than standard catalog products.

Smaller challengers are pursuing narrower parts of the tthermal interface materials market for DRAM packaging industry where the incumbent product base is less fixed. Carbice has moved its vertically aligned carbon nanotube platform through both commercial and defense validation channels, including its DarkNX partnership and its U.S. Navy award in 2026. NovoLINC raised new capital in December 2025 to scale a nanostructured thermal interface platform for AI accelerator and data center use, which points to continuing interest in specialized TIM1 opportunities. Mitsubishi Chemical Group and Boston Materials also formed a strategic collaboration in December 2025 around liquid metal thermal materials for semiconductor packaging, which shows that alternative chemistries are still attracting investment. Even with these moves, the thermal interface materials market for DRAM packaging industry is not yet showing a clear break in incumbent control, because qualification depth and installed relationships still matter more than early-stage novelty.

Leaders of Thermal Interface Materials Market For DRAM Packaging

Henkel AG and Co. KGaA

3M

The Dow Chemical Company

Shin-Etsu Chemical Co., Ltd.

Indium Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: SK hynix launched the iHBM solution, embedding silicon-based integrated cooling elements (ICEs) directly in the D2D PHY area of the HBM package, reducing thermal resistance by 30% versus conventional designs. The solution, based on Mass Reflow Molded Underfill (MR-MUF) wafer-level packaging, is compatible with existing System-in-Package architectures and is targeted for HBM5 deployment in AI data centers.

- May 2026: Dow launched DOWSIL TC-3120 Thermal Gel, with approximately 12 W/m·K thermal conductivity, the highest among Dow's commercially available silicone gels, and designed to minimize oil bleeding and condensed outgassing for 800G and 1.6T optical modules, dense electronics, and high-speed data applications. The product targets module-to-heatsink interfaces in AI data center servers.

- March 2026: Marvell Technology launched the Structera S 30260, a 260-lane CXL switch enabling rack-level memory pooling, with customer sampling expected in Q3 2026. This CXL infrastructure advancement creates new TIM qualification requirements for CXL memory controller and module interface positions, signaling an emerging demand segment.

- February 2026: Carbice announced a strategic partnership with DarkNX, a digital infrastructure company building over 300 MW of AI data center capacity, with Carbice serving as system-level thermal interface solutions expert spanning chip-level cooling through critical interface positions, and supporting long-term performance validation in high-density AI workloads.

Scope of Report on Thermal Interface Materials Market For DRAM Packaging

The Thermal Interface Materials Market For DRAM Packaging Industry refers to the specialized industry segment focused on the development and application of thermal interface materials (TIMs) that enhance heat dissipation and thermal management in Dynamic Random-Access Memory (DRAM) modules during packaging and operation.

The Thermal Interface Materials Market For DRAM Packaging Industry Report is Segmented by Material Type (Thermal Greases and Pastes, Phase Change Materials, Thermal Gels / Dispensable Gap Fillers, Thermal Pads / Gap Pads, and Others (Graphite / Carbon-Based TIMs, Advanced Nano-Composite TIMs)), DRAM Packaging / Product Application (HBM Stacks, Advanced DRAM Packages, Server DRAM Modules, Client DRAM Modules, and CXL Attached DRAM Modules), End-Use Platform (AI Servers and Accelerators, High-Performance Computing, Enterprise and Hyperscale Data Centers, High-End Workstations, Client PCs and Notebooks, and Industrial and Embedded Computing), and Geography (North America, Europe, Asia-Pacific, Rest of the World). The Market Forecasts are Provided in Terms of Value (USD).

| Thermal Greases and Pastes |

| Phase Change Materials |

| Thermal Gels / Dispensable Gap Fillers |

| Thermal Pads / Gap Pads |

| Others (Graphite / Carbon-Based TIMs, Advanced Nano-Composite TIMs) |

| HBM Stacks |

| Advanced DRAM Packages |

| Server DRAM Modules |

| Client DRAM Modules |

| CXL Attached DRAM Modules |

| AI Servers and Accelerators |

| High-Performance Computing |

| Enterprise and Hyperscale Data Centers |

| High-End Workstations |

| Client PCs and Notebooks |

| Industrial and Embedded Computing |

| North America | |

| Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| Taiwan | |

| Rest of Asia-Pacific | |

| Rest of the World |

| By Material Type | Thermal Greases and Pastes | |

| Phase Change Materials | ||

| Thermal Gels / Dispensable Gap Fillers | ||

| Thermal Pads / Gap Pads | ||

| Others (Graphite / Carbon-Based TIMs, Advanced Nano-Composite TIMs) | ||

| By DRAM Packaging / Product Application | HBM Stacks | |

| Advanced DRAM Packages | ||

| Server DRAM Modules | ||

| Client DRAM Modules | ||

| CXL Attached DRAM Modules | ||

| By End-Use Platform | AI Servers and Accelerators | |

| High-Performance Computing | ||

| Enterprise and Hyperscale Data Centers | ||

| High-End Workstations | ||

| Client PCs and Notebooks | ||

| Industrial and Embedded Computing | ||

| By Geography | North America | |

| Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| Taiwan | ||

| Rest of Asia-Pacific | ||

| Rest of the World | ||

Key Questions Answered in the Report

What is the current and forecast value of the thermal interface materials for DRAM packaging space?

The thermal interface materials for DRAM packaging market was valued at USD 0.39 billion in 2025, reached USD 0.49 billion in 2026, and is forecast to reach USD 1.32 billion by 2031 at a 21.92% CAGR.

Which material category leads demand in DRAM package thermal interfaces?

Thermal pads and gap pads led with 34.67% of 2025 revenue because they remain well qualified in server DRAM modules and enterprise memory systems.

Which application is growing fastest through 2031?

HBM stacks are the fastest-growing application, with a projected 22.75% CAGR, as AI accelerators increase stacked memory content and package-level heat density.

Why is Asia-Pacific so dominant in this field?

Asia-Pacific held 82.67% of 2025 revenue because HBM production, advanced DRAM assembly, and major packaging ecosystems are concentrated in South Korea, Taiwan, Japan, and China.

What is driving supplier competition in advanced memory thermal materials?

Competition is centered on qualification depth, reliability under cycling, and the ability to support tighter interfaces in HBM, CXL, and advanced server platforms.

Where is the next major regional growth opportunity?

North America is the fastest-growing region, with a projected 22.87% CAGR through 2031, driven by AI data center buildouts, custom qualification needs, and reshoring support.

Page last updated on: