Therapeutic Hypothermia Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 344.47 Million |

| Market Size (2031) | USD 473.87 Million |

| Growth Rate (2026 - 2031) | 6.59% CAGR |

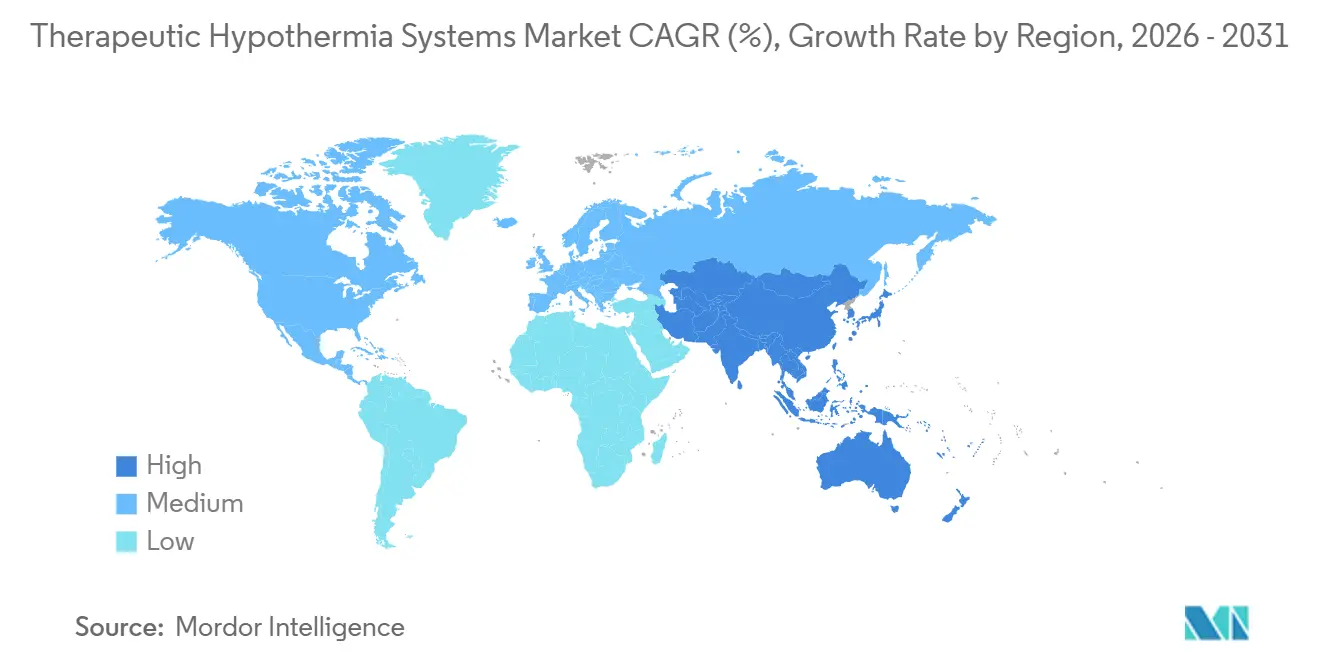

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

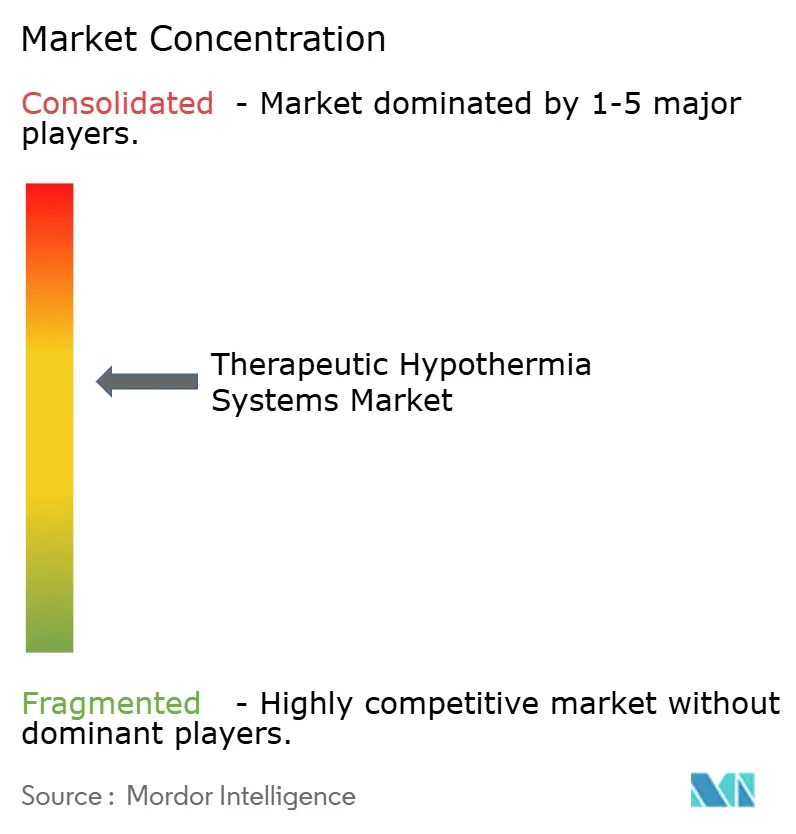

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Therapeutic Hypothermia Systems Market Analysis by Mordor Intelligence

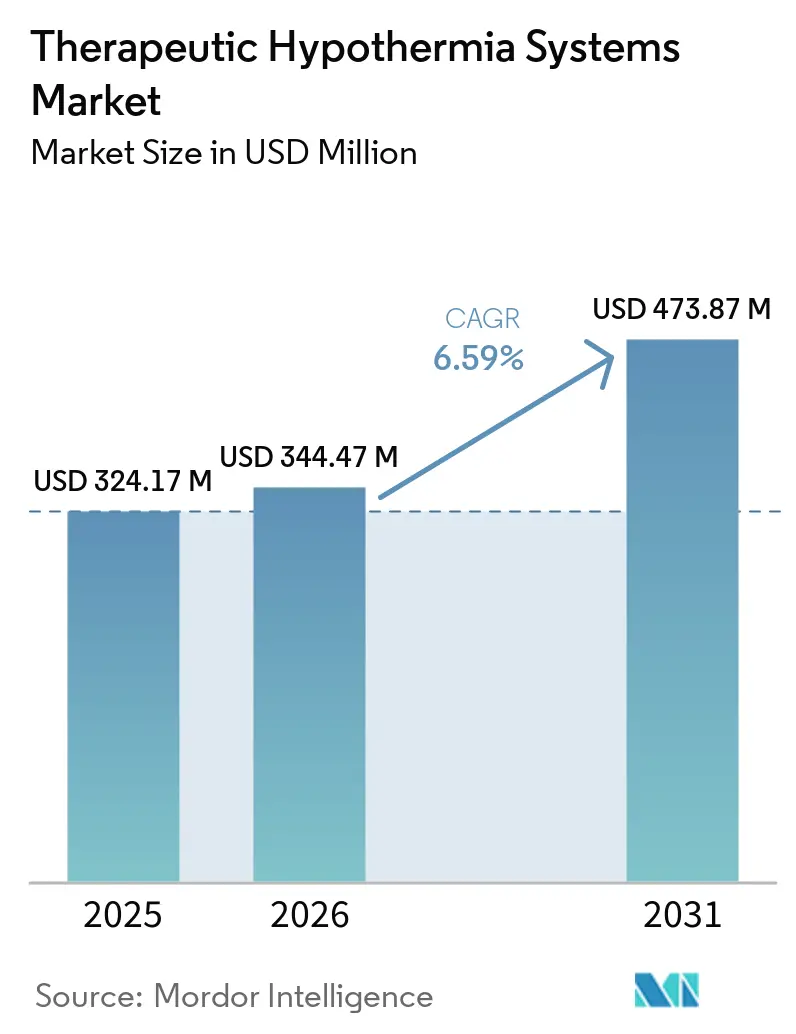

The Therapeutic Hypothermia Systems Market size was valued at USD 324.17 million in 2025 and is estimated to grow from USD 344.47 million in 2026 to reach USD 473.87 million by 2031, at a CAGR of 6.59% during the forecast period (2026-2031).

Changing clinical evidence has redirected investment from deep cooling at 33 °C to controlled normothermia and active fever prevention, widening the relevant patient pool and boosting demand for modular temperature-management consoles. Device recalls have forced hospitals to diversify supplier panels, accelerating the entry of surface, esophageal and immersion systems that reduce central-line complications and nursing workload. Neonatal hypoxic-ischemic encephalopathy (HIE) protocols sustained growth for head-cooling and whole-body cradle platforms, especially in Asia-Pacific NICUs equipped through public health-funded expansions. Meanwhile, North America retained the largest share thanks to over 350,000 annual out-of-hospital cardiac arrests (OHCA) and well-defined reimbursement for targeted temperature management.

Key Report Takeaways

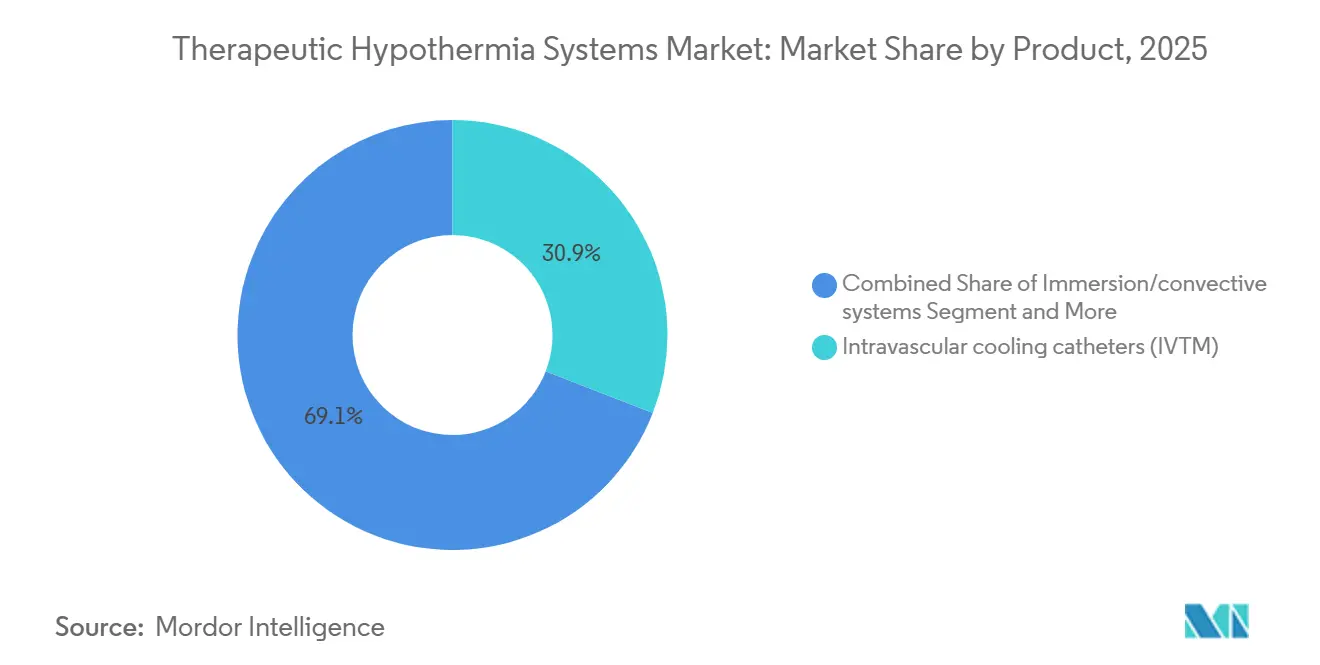

- By product category, intravascular catheters led with 30.91% of therapeutic hypothermia systems market share in 2025, while immersion and convective platforms are forecast to expand at a 7.22% CAGR through 2031.

- By application, fever control in traumatic brain injury dominated with a 45.61% revenue share in 2025; neonatal HIE is projected to advance at a 7.12% CAGR to 2031.

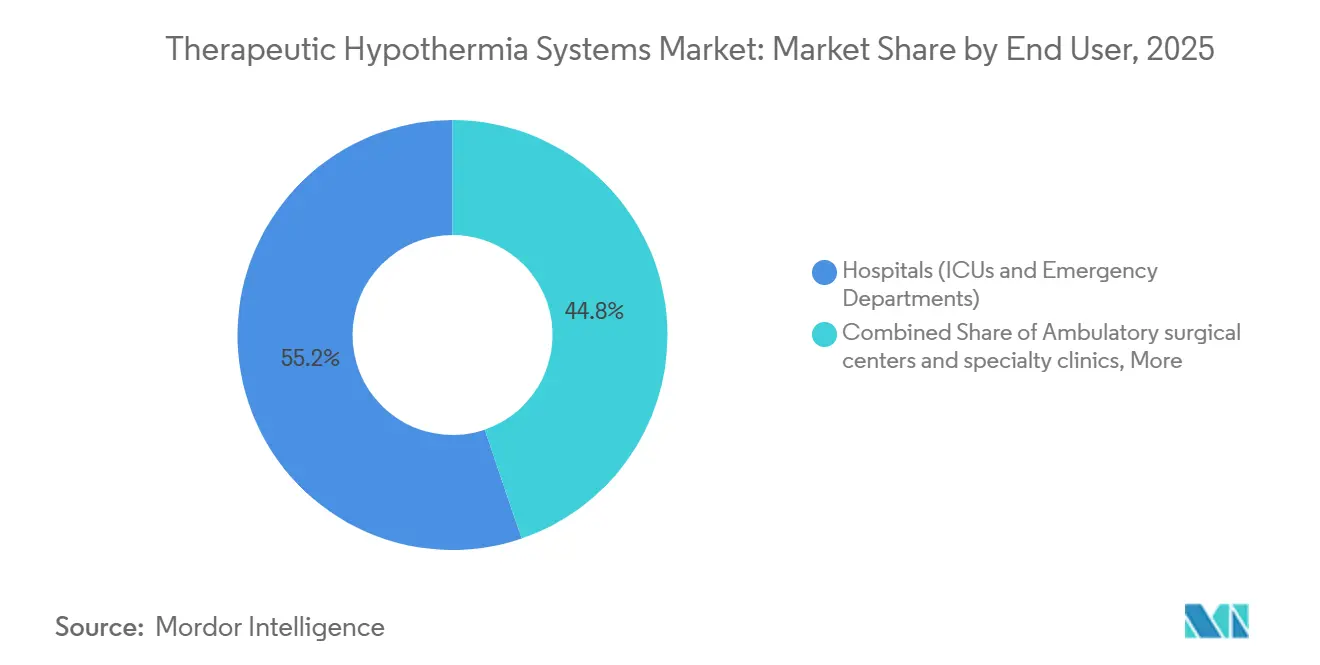

- By end user, hospitals and emergency departments accounted for 55.21% of the therapeutic hypothermia systems market size in 2025, whereas ambulatory surgical centers are set to grow at 8.53% through 2031.

- By geography, North America commanded 45.35% of revenue in 2025, and Asia-Pacific is expected to register the fastest 8.3% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Therapeutic Hypothermia Systems Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-cardiac arrest temperature control codified in AHA/ERC protocols | +1.2% | North America, Europe | Medium term (2-4 years) |

| Neonatal HIE hypothermia standardized at 33-34 °C for 72 hours within 6 hours | +1.4% | Global; fastest uptake in Asia-Pacific | Long term (≥4 years) |

| High OHCA and neuro emergencies keep TTM demand elevated | +0.9% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Asia-Pacific critical-care expansion and protocol adoption | +1.5% | Asia-Pacific, spillover Middle East & Africa | Long term (≥4 years) |

| Shift to controlled normothermia and fever prevention | +0.8% | Global | Short term (≤2 years) |

| Esophageal TTM adoption integrates OR-ICU workflows | +0.6% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Post-Cardiac Arrest Temperature Control Codified in AHA/ERC Protocols

AHA 2025 Advanced Cardiovascular Life Support guidance preserved a Class I recommendation for temperature control within 32-36 °C for at least 24 hours, while the 2025 ERC-ESICM update emphasized fever prevention for 72 hours. North American ICUs still rely on intravascular catheters for precise core cooling, but many European units now favor surface pads that sustain normothermia without the infection risk of venous access. A 2025 survey of 1,200 European ICUs reported that one-third had adopted the new ERC practice, propelling demand for gel-free adhesive pads. Vendors therefore market consoles able to switch between deep cooling and normothermia, aligning with divergent regional protocols. Compliance with IEC 60601 electrical safety norms remains mandatory across markets, bolstering buyer confidence.

Neonatal HIE Hypothermia Standardized at 33-34 °C

The American Academy of Pediatrics reaffirmed the HIE cooling window in 2026, citing a 25% reduction in mortality or disability at 18 months when therapy starts within 6 hours of birth and lasts 72 hours[1]American Academy of Pediatrics, “Therapeutic Hypothermia for Neonatal HIE,” aap.org. India’s National Neonatology Forum endorsement in 2024 catalyzed demand for locally built cradle systems priced below USD 1,000, replacing improvised ice packs in tier-2 hospitals. Asia-Pacific NICU upgrades underscore the need for readily deployable devices that integrate rectal probes and servo regulators. Yet, uptake remains patchy in sub-Saharan Africa, where WHO 2024 guidelines still recommend passive cooling when servo-control is unavailable. Continuous temperature monitoring and trained staff thus remain critical barriers.

High Incidence of OHCA and Neuro Emergencies Sustains Demand

AHA’s 2026 statistics count over 350,000 annual OHCAs in the United States alone, with neurologically favorable discharge in only 6.8-13.5% of cases. Even modest outcome gains keep targeted temperature management embedded in multimodal post-resuscitation bundles. Parallel neuro-ICU demand arises because up to 70% of traumatic brain injury admissions develop fever, for which normothermia pads outperform antipyretic drugs. Although the 2024 COOLHEAT stroke trial showed no clinical benefit from deep cooling, hospitals still purchase surface systems for fever control across neurological etiologies. Therefore, broader disease incidence, rather than hypothermia efficacy alone, underpins the therapeutic hypothermia systems market.

Asia-Pacific Healthcare Expansion Accelerates Uptake

India earmarked INR 37,000 crore (USD 4.4 billion) in 2025-2026 for ICU and neonatal bed creation, lifting console installations in public hospitals. BrainCool AB gained Malaysian clearance for IQool in 2025 and partnered with ZOLL for ASEAN distribution, doubling regional pad sales to 10,000 units in 2024. Yet heterogeneity persists: Japan’s aging population values precise normothermia systems, while Bangladesh relies on gel-pack cradles due to per-capita spend below USD 50. Regional growth therefore hinges on modular platforms adaptable to divergent reimbursement models under the ASEAN Medical Device Directive.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| TTM2-era evidence de-emphasizes deep hypothermia at 33 °C | -0.7% | Europe, Australasia, Global | Short term (≤2 years) |

| Hypothermia-related arrhythmias and adverse events | -0.4% | Global | Medium term (2-4 years) |

| Recall-driven downtime and safety notices | -0.5% | North America, Europe | Short term (≤2 years) |

| High system cost restricts LMIC adoption | -0.8% | Asia-Pacific, MEA, Latin America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

TTM2-Era Evidence De-Emphasizes Deep Hypothermia

The TTM2 trial, reinforced by 2024 subgroup analysis, confirmed no survival benefit from 33 °C versus normothermia after cardiac arrest[2]New England Journal of Medicine, “Targeted Temperature Management (TTM2),” nejm.org. European and Australasian ICUs rapidly updated protocols, curbing demand for high-intensity catheter systems. With less aggressive cooling, hospitals reduce disposable catheter spend of USD 1,500-2,500 per case in favor of reusable pads. Vendors now highlight fever prevention features rather than neuroprotection, reshaping marketing narratives across the therapeutic hypothermia systems market.

Hypothermia-Related Arrhythmias and Adverse Events

Hypothermia increases bradyarrhythmia and electrolyte disturbances; TTM2 linked deeper cooling to more hemodynamic instability. Centres lacking seasoned TTM teams hesitate to adopt 33 °C targets, and new ESICM guidance recommends multimodal anti-shiver regimens involving buspirone and meperidine, further elevating care complexity. These extra pharmacologic steps heighten cost and staff burden, dampening unit-level enthusiasm.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Intravascular Precision Leads as Immersion Gains

In 2025, intravascular catheters generated 30.91% of therapeutic hypothermia systems market revenue thanks to rapid 2.5 °C-per-hour cooling and servo accuracy of ±0.2 °C. Yet safety recalls and thrombotic risk diverted many European ICUs toward water-circulating pads and gel-free blankets, accelerating surface-system shipments. Immersion and convective devices, priced below USD 10,000, are projected to grow at a 7.22% CAGR, targeting cost-conscious hospitals in Latin America and Southeast Asia. Esophageal platforms such as ensoETM offer continuous OR-to-ICU control and avoid central-line infections, appealing to electrophysiology labs. Selective head caps remain a neonatal niche, yet the dominant intravascular share highlights clinicians’ trust in core-target accuracy when deep cooling is still required.

Although performance shifts favor lower-cost alternatives, many centers keep catheter consoles to manage outlier cases needing aggressive target drops. ZOLL’s 2024 integrated Thermogard console, which toggles between catheter and pad circuits, exemplifies hybrid design that future-proofs procurement decisions. The therapeutic hypothermia systems industry therefore faces dual pressures: sustain premium consumable yield while proving life-cycle cost advantages against rising immersion-system incumbents.

By Application: Neurogenic Fever Dominates while Neonatal HIE Accelerates

Traumatic brain injury and stroke-related fever suppression accounted for 45.61% of 2025 revenue, reflecting 70% fever incidence among neuro-ICU patients. Post-arrest cooling share shrank after TTM2, but retained procedural value for the 8-18% of OHCA survivors requiring intensive care. Neonatal HIE remains the fastest-growing sub-segment at 7.12% CAGR, buoyed by AAP’s 2026 reaffirmation and Asia-Pacific NICU expansions. Conversely, large-vessel stroke cooling adoption slowed after COOLHEAT’s neutral outcomes and EuroHYP-1’s pneumonia uptick.

As protocols pivot from hypothermic neuroprotection to fever prevention, device utilization patterns change. Surface pads generate higher procedure counts at lower intensity, while consumable catheters face shrinking volumes. Precision-medicine studies in Japan now tailor targets to 34-35 °C based on arrest-to-ROSC interval, signaling nuanced future demand. In neonatal care, cradle vendors integrate servo controls and passive phase-change backups to ensure safe temperature curves even during power outages, strengthening market resilience in LMICs.

By End User: Hospitals Anchor Volume, ASCs Surge

Hospitals and EDs represented 55.21% of therapeutic hypothermia systems market size in 2025 because ICUs remain the locus for acute cardiac and neuro cases. Academic medical centers lead uptake due to multidisciplinary teams trained in anti-shiver protocols and hemodynamic optimization. Ambulatory surgical centers are forecast to grow 8.53% through 2031 as esophageal devices support cardiac ablation and outpatient spine surgeries without adding central-line risk. EMS remains an experiment; the 2024 PRINCESS trial found no survival gain from field cooling, dampening appetite for pre-hospital systems.

Resource constraints shape deployment: high-income hospitals use closed-loop consoles with 24/7 nurse surveillance, while LMIC facilities opt for low-tech cradles and manual probe checks. As value-based care spreads, vendors emphasize shorter ICU stays and infection reduction to justify capital expense in both inpatient and outpatient settings.

Geography Analysis

North America retained 45.35% of 2025 revenue, underwritten by more than 350,000 OHCAs per year, DRG-based reimbursement and a dense network of Level I trauma centers. A 2025 survey revealed 60% of U.S. ICUs shifted to normothermia within 18 months of TTM2, spurring surface-pad sales. Recall-driven diversification also helped newer entrants secure contracts as hospitals reduced single-vendor dependency.

Europe follows ERC guidance favoring fever suppression for 72 hours and has consequently leaned into non-invasive pads and immersion baths. Yet Germany and Switzerland still procure catheter consoles for centers performing percutaneous coronary interventions around the clock. IEC-60601 and MDR requirements keep barriers high for small suppliers, but BrainCool AB’s 2023 IQool update showed that safety-centric brands can win adoption across Scandinavian stroke units[3]BrainCool AB, “Regulatory Approval in Malaysia,” braincool.se.

Asia-Pacific is pacing the therapeutic hypothermia systems market at an 8.3% CAGR through 2031, lifted by ICU bed additions in China and India, Malaysia’s 2025 IQool clearance and neonatal HIE protocols across ASEAN. However, markets are bifurcated: Japan’s stroke-heavy demographic relies on normothermia pads, whereas Bangladesh and Sri Lanka depend on sub-USD 1,000 passive cradles due to constrained capital budgets. The Gulf states in the Middle East are expanding critical-care capacity, and Qatar’s 2025 registry reported a 17.8% discharge survival comparable to high-income benchmarks. In South America, Brazil and Argentina anchor demand, but currency swings hamper long-term procurement planning. Overall, regulatory harmonization is advancing faster than reimbursement unification, leaving vendors to tailor financing schemes per country.

Competitive Landscape

No single company controls a major portion of global revenue, giving the therapeutic hypothermia systems market a moderately fragmented profile. ZOLL Medical’s 2024 Thermogard console that blends catheter and pad circuits illustrates the pivot toward multipurpose systems that future-proof against shifting clinical guidelines. BrainCool AB used its clean safety record and 2025 Malaysian clearance to sign ASEAN distribution with ZOLL, showing how partnerships can unlock new regions without heavy capex. Recall fatigue benefitted such challengers; a quarter of U.S. hospitals reported canceling or delaying orders for recalled devices in 2025.

Esophageal platforms, led by Attune Medical, are carving perioperative niches where forced-air warmers may aerosolize pathogens, and bundling strategies with Cincinnati Sub-Zero aim to penetrate the USD 4.6 billion patient-warming sector. Frugal innovators Phoenix Medical Systems and Pluss Advanced Technologies exploit LMIC price sensitivities by offering phase-change cradles under USD 1,000, a tactic that could backflow into mature markets as hospitals pursue low-capital redundancy solutions. Regulatory hurdles, FDA 21 CFR 820, ISO 13485 and IEC 60601, protect incumbents but also signal quality assurance, steering buyers toward certified brands after recent recalls.

As evidence de-emphasizes deep hypothermia, vendors race to highlight normothermia and warming capabilities, broadening their addressable procedures per console. Closed-loop automation and cloud analytics that document compliance may emerge as differentiators, reducing nurse workload and justifying premium pricing even when cooling intensity declines.

Therapeutic Hypothermia Systems Industry Leaders

ZOLL Medical Corporation (Asahi Kasei)

Gentherm Incorporated

BrainCool AB

Becton, Dickinson and Company

Belmont Medical Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: The American Academy of Pediatrics (AAP) revised its clinical guidance on therapeutic hypothermia treatments for children diagnosed with neonatal hypoxic-ischemic encephalopathy (HIE).

- January 2026: Bridge to Life received FDA De Novo clearance for VitaSmart hypothermic oxygenated perfusion, the first U.S.-approved system for donor-liver HOPE preservation, after demonstrating graft-function gains in a 219-patient pivotal trial.

Global Therapeutic Hypothermia Systems Market Report Scope

As per the scope of the report, therapeutic hypothermia systems are medical devices designed to induce and maintain controlled cooling of a patient's body temperature. They are used primarily to reduce metabolic rate and protect vital organs, especially the brain, following conditions such as cardiac arrest, stroke, or traumatic brain injury.

The segmentation for the therapeutic hypothermia systems market is categorized by product, application, end user, and geography. By product, the market includes intravascular cooling catheters (IVTM), surface systems (water-circulating pads, blankets, and garments), esophageal temperature management devices, selective head cooling caps, and immersion and convective systems. By application, it covers post-cardiac arrest, neonatal hypoxic-ischemic encephalopathy (HIE), ischemic stroke, and traumatic brain injury (TBI) and neurogenic fever. By end user, the market is segmented into hospitals, including ICUs and emergency departments, ambulatory surgical centers and specialty clinics, emergency medical services (pre-hospital), and academic and research institutes. By geography, the market spans North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Intravascular cooling catheters (IVTM) |

| Surface systems (water-circulating pads/blankets/garments) |

| Esophageal temperature management devices |

| Selective head cooling caps |

| Immersion/convective systems |

| Post-cardiac arrest |

| Neonatal hypoxic-ischemic encephalopathy (HIE) |

| Ischemic stroke |

| Traumatic brain injury (TBI) and neurogenic fever |

| Hospitals (ICUs and Emergency Departments) |

| Ambulatory surgical centers and specialty clinics |

| Emergency medical services (pre-hospital) |

| Academic and research institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Intravascular cooling catheters (IVTM) | |

| Surface systems (water-circulating pads/blankets/garments) | ||

| Esophageal temperature management devices | ||

| Selective head cooling caps | ||

| Immersion/convective systems | ||

| By Application | Post-cardiac arrest | |

| Neonatal hypoxic-ischemic encephalopathy (HIE) | ||

| Ischemic stroke | ||

| Traumatic brain injury (TBI) and neurogenic fever | ||

| By End User | Hospitals (ICUs and Emergency Departments) | |

| Ambulatory surgical centers and specialty clinics | ||

| Emergency medical services (pre-hospital) | ||

| Academic and research institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the therapeutic hypothermia systems market in 2026?

The therapeutic hypothermia systems market size is projected at USD 344.47 million for 2026, rising toward USD 473.87 million by 2031 at a 6.59% CAGR.

Which product category currently leads sales?

Intravascular cooling catheters captured 30.91% of therapeutic hypothermia systems market share in 2025, reflecting their precision for core temperature control.

What is the fastest-growing application?

Neonatal hypoxic-ischemic encephalopathy devices are advancing at a 7.12% CAGR through 2031 as more NICUs adopt the 33-34 degree Celsius, 72-hour protocol.

Which region will post the highest growth?

Asia-Pacific is forecast to outpace all regions with an 8.3% CAGR through 2031, driven by ICU expansion in China and India and broader protocol adoption.

Why are hospitals diversifying suppliers?

A series of FDA Class I and II recalls between 2024-2026 prompted 40% of U.S. hospitals to reduce single-vendor dependence, opening space for new entrants with strong safety records.

How will guideline changes affect device demand?

The shift from deep hypothermia to controlled normothermia broadens the addressable patient base but favors lower-cost surface and esophageal systems over premium intravascular catheters.

Page last updated on: