Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

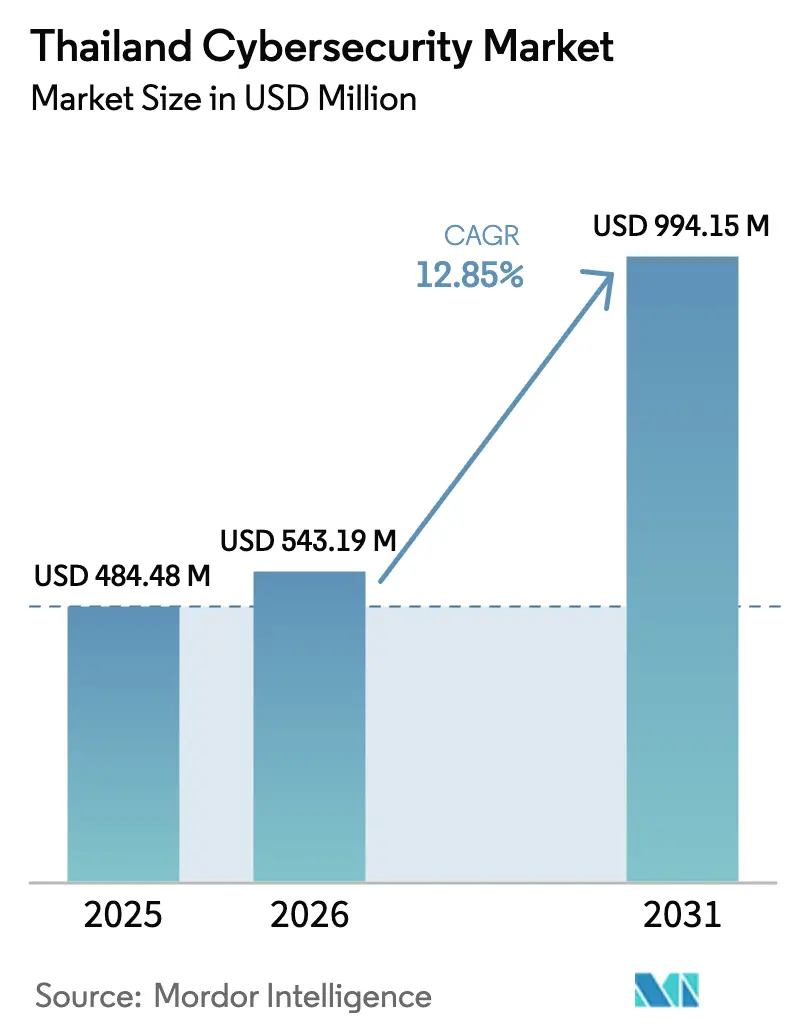

| Base Year Market Size (2025) | USD 484.48 Million |

| Market Size (2026) | USD 543.19 Million |

| Market Size (2031) | USD 994.15 Million |

| Growth Rate (2026 - 2031) | 12.85% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Cybersecurity Market Analysis by Mordor Intelligence

The Thailand cybersecurity market size was valued at USD 484.48 million in 2025 and is estimated to grow from USD 543.19 million in 2026 to reach USD 994.15 million by 2031, at a CAGR of 12.85% during the forecast period (2026-2031). A mandatory shift toward AI-native defenses by banks preparing for virtual-bank launches, strict data-localization clauses tied to the Personal Data Protection Act, and the government’s Cloud First policy are expanding addressable demand faster than local talent pipelines can scale. Hyperscalers that opened in-country regions in 2025 supply the elastic infrastructure needed for real-time payment screening and zero-knowledge authentication, while ransomware-as-a-service syndicates keep breach headlines in the news cycle and sustain urgency around managed detection and response. As telecom operators bundle security into 5G connectivity packages and industrial estates digitize production lines, spend is spreading beyond the Bangkok core into the Eastern Economic Corridor, closing the historical urban-rural usage gap. Overall, competitive intensity is climbing, yet service uptake outpaces product refreshes because enterprises prefer outcome-based contracts that offset skills shortages.

Key Report Takeaways

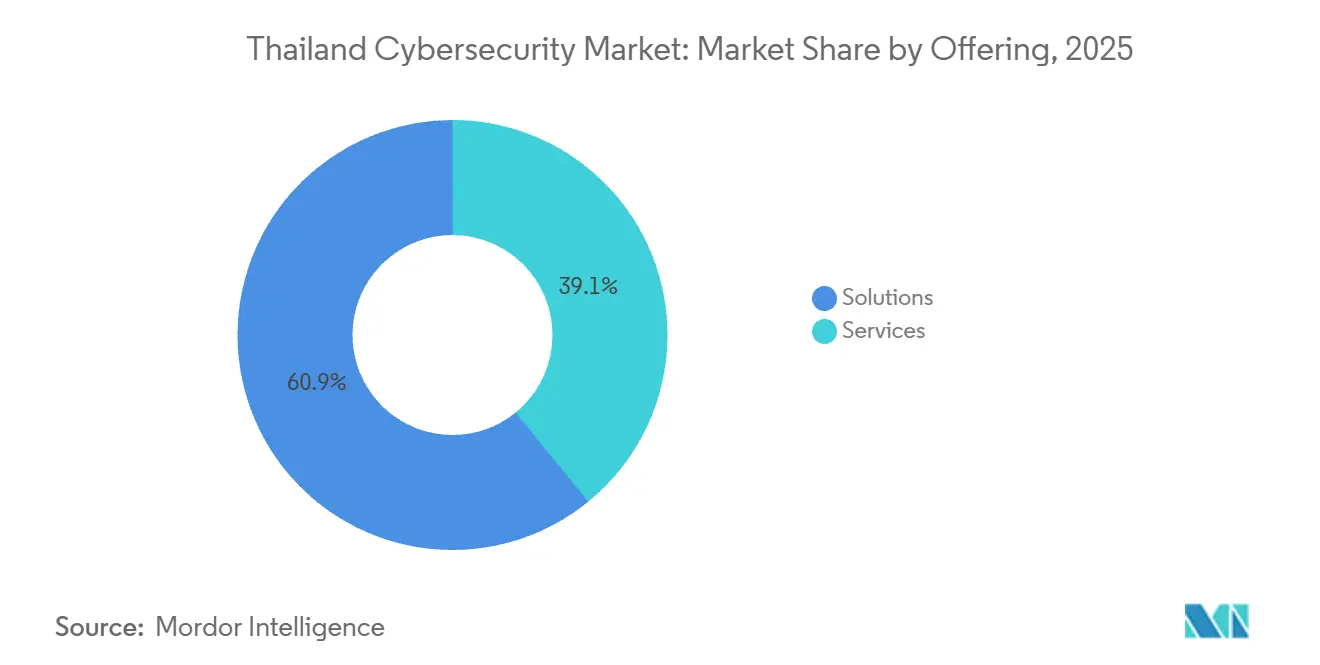

- By offering solutions, the company commanded a 60.88% share in 2025, while services are projected to grow at a 13.64% CAGR through 2031.

- By deployment mode, on-premises installations accounted for 64.27% of the Thailand cybersecurity market in 2025, whereas cloud security is forecast to grow at a 13.71% CAGR through 2031.

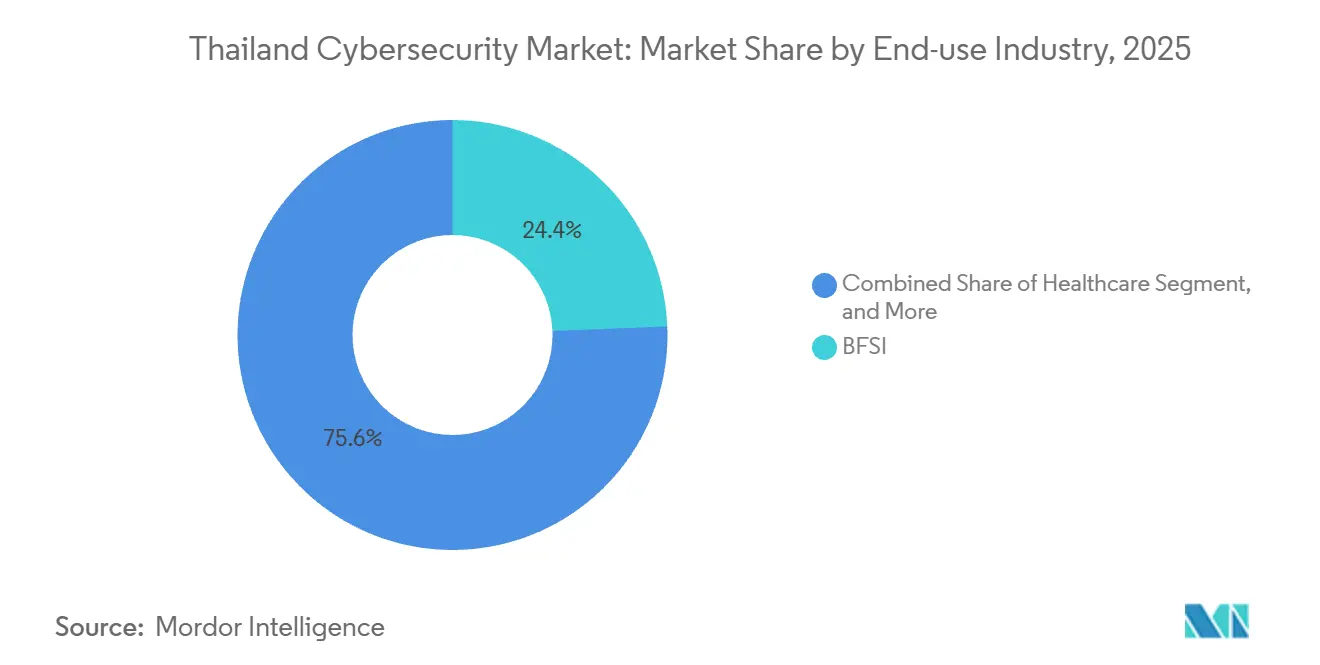

- By end-use industry, BFSI accounted for 24.36% of market share in 2025, while healthcare is expected to register the fastest growth at a 13.26% CAGR over 2026-2031.

- By enterprise size, large enterprises held 65.67% of market share in 2025, whereas small and medium enterprises are projected to post a 13.83% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Thailand Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Digital-Banking Adoption in Thai BFSI | +2.8% | National, concentrated in Bangkok metropolitan area and provincial banking hubs | Medium term (2-4 years) |

| Fast-Track Government Cloud Migration (G-Cloud and NDID) | +2.3% | National, with early adoption in central government agencies and state enterprises | Short term (≤ 2 years) |

| 5G Rollout Spurring IoT-Edge Security Demand | +1.9% | National, with concentration in Eastern Economic Corridor industrial zones | Medium term (2-4 years) |

| Surge in Ransomware-as-a-Service Attacks on SMEs | +1.7% | National, with higher incidence in Bangkok, Chiang Mai, Phuket commercial districts | Short term (≤ 2 years) |

| Stricter PDPA Data-Localization Enforcement | +1.5% | National, affecting multinational enterprises with regional data centers | Long term (≥ 4 years) |

| Real-Time Payment Fraud Driving AI-Based SOC Demand | +1.4% | National, focused on financial services and e-commerce sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Digital-Banking Adoption in Thai BFSI

Four virtual-bank licenses issued in 2025 put Thailand on course for commercial launches in Q2-Q3 2026, prompting incumbents to inject AI into fraud-detection workflows so that anomalous transfers are blocked within milliseconds rather than overnight batches.[1]Bank of Thailand, “Virtual Banking Licenses and Digital Transformation Initiatives,” bot.or.th Investment levels support the shift: Siam Commercial Bank and SCBX earmarked a combined THB 18.4 billion for cloud-native platforms that embed security at the API layer.[2]SCBX, “Annual Report 2024,” scbx.com PromptPay already flags more than 1,000 suspicious transactions every day, and the new PCI DSS 4.0.1 clause on continuous control validation further elevates operational visibility standards.[3]PCI Security Standards Council, “Payment Card Industry Data Security Standard Version 4.0.1,” pcisecuritystandards.org Consequently, demand is tilting toward outcome-based managed detection and response as banks hedge against hiring constraints. The trend deepens the Thailand cybersecurity market reliance on service partners that can maintain 24 × 7 security-operations-center coverage.

Fast-Track Government Cloud Migration (G-Cloud And NDID)

The Cloud First directive obliges ministries to default to sovereign cloud unless national-security waivers apply, and a three-tier classification model specifies encryption levels for public, sensitive, and secret workloads. National Telecom’s data-center arm monetized THB 1.49 billion of hosting fees in 2023, showing early fiscal upside for state-owned capacity. Meanwhile, NDID exceeded 40 million verified identities in 2025 and is piloting zero-knowledge-proof log-ins, cutting the data disclosure surface that attackers normally probe. The Electronic Transactions Development Agency’s plan to oblige e-marketplaces to validate seller IDs further lifts demand for identity-verification APIs. Because only a handful of local firms can deliver cryptographic key escrow at scale, global providers entering the Thailand cybersecurity market gain an early credibility boost.

5G Rollout Spurring IoT-Edge Security Demand

True Corporation’s merger with dtac combined 3,650 engineers and pooled 700 MHz plus 2.1 GHz assets, enabling nationwide radio-resource slicing for latency-sensitive industrial internet deployments. The telecom regulator has ordered 2G and 3G sunsets by Q3 2026, pushing legacy machine-to-machine traffic into 5G standalone cores that isolate slices based on risk. Inside the Eastern Economic Corridor, a 200-hectare Digital Park invites cybersecurity pilots ranging from autonomous AGVs to predictive maintenance, yet many factories still segregate operational-technology networks, creating blind spots. True’s CyberSafe package shows how carriers are bundling anomaly detection into consumer and small-business broadband, a move that enlarges the Thailand cybersecurity market without customers procuring separate tools. The National Cyber Security Committee’s new critical-infrastructure rules add urgency by mandating risk classification for OT assets.

Surge In Ransomware-As-A-Service Attacks on SMEs

The Ministry of Labor breach in July 2025, linked to Devman, leaked 300 GB and ended in a USD 15 million ransom note, spotlighting small-budget agencies that still rely on basic firewalls. ThaiCERT’s multiple 2025-2026 alerts on MongoDB and aviation systems underscore that misconfigurations, not zero-day exploits, drive most local incidents. Cross-border scam rings cause daily losses above THB 80 million, and the Royal Thai Police is now correlating call detail records with fraud logs through an AI engine hosted on True’s network. SMEs, which form 99% of businesses, spend just 0.2% of revenue on security, a level Fortinet labels inadequate to fund endpoint detection or round-the-clock monitoring. As ransomware kits commoditize payload delivery, managed detection providers that speak Thai and offer pay-as-you-go models are poised to capture latent demand in the Thailand cybersecurity market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Thai-Language Cybersecurity Talent | -1.8% | National, with acute shortages in Bangkok, Chiang Mai, and Eastern Economic Corridor | Long term (≥ 4 years) |

| Price-Sensitive SME Buyer Behavior | -1.3% | National, concentrated in provincial SME clusters outside Bangkok | Medium term (2-4 years) |

| Underinsured Cyber Incidents due to PDPA Liability Gaps | -0.9% | National, affecting enterprises without dedicated risk-management functions | Long term (≥ 4 years) |

| OT Security Integration Complexities in EEC Factories | -0.7% | Eastern Economic Corridor industrial estates in Rayong, Chonburi, Chachoengsao | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Thai-Language Cybersecurity Talent

By 2025 only 431 professionals in Thailand held CISSP credentials, up by just 12% year on year and nowhere near the 10,000-certificate goal set for 2026. The National Cyber Academy has schooled more than 100,000 people, yet 72% of enterprises still cite staffing gaps as an operational risk. Cloud and AI security expertise top recruiting wish lists, but universities graduate fewer than 2,000 infosec majors annually, and multinationals offer salaries SMEs cannot match. Banks are sponsoring private curricula with Mandiant, keeping skills locked inside finance while healthcare and manufacturing scramble for bilingual analysts. Until more Thai-language threat feeds and playbooks emerge, human capital scarcity will temper the Thailand cybersecurity market growth potential.

Price-Sensitive SME Buyer Behavior

Average security spend at Thai SMEs remains at 0.2% of revenue, a ceiling that limits adoption of endpoint detection, SIEM, or managed SOC subscriptions. The July 2025 ransomware hit on the Ministry of Labor illustrated how budget-constrained entities lean on outdated perimeter defenses that fail against lateral movement. Insurers now insist on continuous control monitoring before underwriting cyber policies, and the resulting audit fees deter cash-strapped retailers from seeking coverage. ETDA’s draft rule compelling e-marketplaces to verify seller IDs imposes further compliance cost that many provincial platforms perceive as punitive. This dual pressure prolongs a two-speed Thailand cybersecurity market in which global enterprises adopt zero-trust while neighborhood firms gamble on minimal defenses.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Gain As Outsourcing Offsets Talent Gaps

Solutions dominated spending with a 60.88% slice of the Thailand cybersecurity market share in 2025, anchored by long-installed firewalls and endpoint suites. Yet services are projected to outpace products at a 13.64% CAGR as boards confront the 72% operational-risk exposure tied to empty analyst seats. Managed detection, incident response, and vulnerability management contracts provide immediate coverage without HR overhead, and local integrators weave Thai-language threat feeds into dashboards to satisfy auditors. Network and endpoint security remain the largest solution buckets, propelled by True-dtac’s 5G rollout and the regulator’s imminent 2G-3G switch-off that pushes device fleets onto new attack surfaces.

Cloud security is moving at the fastest clip, fueled by the Cloud First mandate and PDPA localization clauses that reroute traffic to sovereign regions. Identity and access management gains extra momentum from NDID’s 40-million-user milestone, spurring banks and e-tailers to federate logins via government APIs. Meanwhile, virtual banks slated for 2026 require AI-native fraud engines that embed security checks directly into the API flow, nudging developers toward DevSecOps. Data-protection tools also benefit as telemedicine platforms expand patient-record exchange, cementing encryption and key-governance requirements in hospital budgets.

By Deployment Mode: Sovereignty Mandates Accelerate Hybrid Adoption

On-premise estates still held 64.27% of Thailand cybersecurity market size in 2025 because critical-information-infrastructure owners rely on physical appliance chains for regulatory comfort. However, cloud-based controls are set to climb at a 13.71% CAGR thanks to ETDA’s stricter localization guidance and the arrival of new hyperscaler regions. AWS committed USD 5 billion to a three-zone Bangkok region, Microsoft is rolling out a sovereign cloud with Gulf and True IDC, and Google Cloud inked a data-residency pact with Gulf Edge.

National Telecom’s government cloud supports ministries, but capacity limits slow migration and force agencies into hybrid topologies that juggle ISO 27001 gear on-premise with SaaS in public cloud. The National Cyber Security Agency’s Cybershield platform, co-engineered with Palo Alto Networks and Google, provides unified telemetry across both domains, helping auditors reconcile alerts in one pane. Financial and healthcare players increasingly view hybrid as a forever state, valuing the elasticity of cloud for compute-heavy analytics while pinning sensitive workloads behind local HSMs.

By End-Use Industry: Healthcare Surges As Telemedicine Expands Attack Surface

BFSI accounted for 24.36% of 2025 spend as real-time payment fraud demanded AI-driven SOC tooling that checks beneficiary accounts against watchlists in microseconds. The increasing sophistication of cyber threats has made it imperative for financial institutions to adopt advanced security measures. Siam Commercial Bank alone invested THB 4.358 billion during 2023-2024 in cloud refits that integrate security at the code level. These investments highlight the growing emphasis on proactive measures to safeguard digital transactions and customer data.

Healthcare is on course for the speed lane, with a 13.26% CAGR to 2031 as the Mor Prom Plus telemedicine app and the Health Link interoperability program widen the clinical data pipe. Provincial hospitals lag in encrypting records, making them ripe targets for ransomware, and the WHO digital-health framework now flags encryption and access control as baseline obligations. IT-telecom spend also stays elevated, buoyed by network operators hardening 5G standalone cores. Manufacturing in the Eastern Economic Corridor edges upward as factory owners integrate OT sensors with corporate IT, but fragmented tooling still hinders unified visibility.

By End-User Enterprise Size: SME Growth Reflects Ransomware Urgency

Large enterprises controlled 65.67% of outlays in 2025, leveraging certified staff and global vendor catalogs. Yet SMEs are forecast to climb at a market-leading 13.83% CAGR, pushed by ransomware-as-a-service blasts that exploit outdated Windows builds. The July 2025 Devman attack on the Ministry of Labor highlighted how mid-tier bodies suffer when incident response is ad-hoc.

Telecom-bundled SOC offerings, such as CyberSafe, lower entry barriers by fusing network telemetry with AI classifiers that roll out across Wi-Fi routers without manual tuning. ETDA’s looming know-your-seller rule also acts as a carrot-and-stick, pushing online shops to adopt identity-verification services or face penalties. Over time, SME spend will narrow the historical gap, reshaping the Thailand cybersecurity market revenue mix toward a more balanced profile.

Geography Analysis

Bangkok and its surrounding provinces generated more than 60% of 2025 cybersecurity spend, owing to the head-office clustering of banks, telecom groups, and ministries. The Thailand cybersecurity market, however, is beginning to decentralize as industrial investors focus on the Eastern Economic Corridor across Rayong, Chonburi, and Chachoengsao. Digital Park Thailand’s 200-hectare campus offers 5G sandboxes for autonomous logistics pilots, incentivizing vendors to set up local SOC extensions.

Provincial adoption remains hamstrung by the Thai-language talent shortage and SME budget caps, but the National Cyber Security Agency and ISC2 are co-funding scholarship programs and open-source playbooks to help level the field. These initiatives aim to address the skill gap and provide accessible resources for smaller enterprises to improve their cybersecurity posture. Despite those efforts, the CISSP population rose only to 431 by end-2025, indicating slow progress and highlighting the need for sustained efforts to build a robust cybersecurity workforce.

Hyperscaler regions in Bangkok shorten latency for fraud-analytics engines and enable compliance with ETDA localization clauses. Meanwhile, True-dtac’s radio network consolidation routes low-latency backhaul into industrial estates, yet OT and IT teams still use separate dashboards, a gap that integrators now target with converged platforms. Cross-border scam traffic entering from neighboring countries continues to drive joint police-carrier operations that deploy call-detail AI scrubbing, adding a public-safety dimension to regional demand.

Competitive Landscape

Thailand cybersecurity market competition remains moderately fragmented. Multinational brands Cisco, Palo Alto Networks, Fortinet, Check Point, Trend Micro, CrowdStrike, and Microsoft retain a significant share of large-enterprise budgets, but local integrators differentiate through Thai-language threat intelligence and on-site incident response. MFEC, for instance, booked THB 994.9 million in cybersecurity revenue for 2023, with a 16.3% gross margin, leveraging Elite Reseller status with Fortinet and Premier Consulting credentials with Microsoft.

Hyperscaler momentum is reshaping go-to-market models. AWS invested USD 5 billion in its Bangkok region, Microsoft committed USD 2.85 billion for a sovereign cloud with Gulf and True IDC, and Google Cloud signed a residency pact with Gulf Edge. These platforms offer native security stacks, GuardDuty, Defender, and Chronicle that partners can resell, intensifying price competition. Concurrently, the National Cyber Security Agency’s Cybershield program standardizes public-sector monitoring on Palo Alto and Mandiant tooling, reducing vendor fragmentation inside government.

White-space opportunities cluster around operational-technology defense for EEC factories and cyber-insurance underwriting frameworks. Telecom operators such as True demonstrate ambition by validating Level 4 network autonomy that self-remediates threats, illustrating how connectivity providers can embed security directly in transport layers. Certification badges, notably ISO 27001 and continuous PCI DSS 4.0.1 compliance, remain table stakes for bidders in banking and payment-processing RFPs. Overall, scale advantages matter, yet local language, sovereign hosting, and managed-service depth increasingly dictate contract wins in the Thailand cybersecurity market.

Thailand Cybersecurity Industry Leaders

IBM Corporation

Cisco Systems Inc

Check Point Software Technologies Ltd.

Trend Micro Incorporated

CrowdStrike Holdings, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: The Royal Thai Police partnered with True Corporation to deploy AI-driven threat detection that correlates call-detail records with fraud reports, targeting scam losses above THB 80 million per day.

- January 2026: ThaiCERT issued an advisory on MongoDB misconfiguration risks, urging enterprises to harden access controls and enable encryption.

- November 2025: True Corporation validated Level 4 service-assurance autonomy, introducing an AI engine that self-remediates network threats without manual intervention.

- October 2025: Microsoft, Gulf, and True IDC announced a sovereign cloud region backed by USD 2.85 billion in capital, aligning with PDPA data-residency expectations.

Thailand Cybersecurity Market Report Scope

IT advancements, communication technologies, and smart energy grids are transforming the landscapes of nearly every country's essential infrastructure and commercial networks. Rapidly changing technology, however, brings with it rapidly advancing hazards. Cybersecurity solutions assist a company in monitoring, detecting, reporting, and countering cyber threats, including internet-based attempts to damage or disrupt information systems, hack critical data using spyware and malware, and exploit vulnerabilities through phishing, to protect data confidentiality. The study's market size is based on end-user spending on cybersecurity systems and services.

The Thailand Cybersecurity Market Report is Segmented by Offering (Solutions, and Services), Deployment Mode (On-Premise, Cloud), End-use Industry (IT and Telecom, BFSI, Healthcare, Industrial Manufacturing, Retail and E-commerce, Energy and Utilities, Aerospace, Military and Defense, and Other End-use Industries), End-User Enterprise Size (Large Enterprises, and Small and Medium Enterprises). The Market Forecasts are Provided in Terms of Value (USD).

By Offering

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security | |

| Endpoint Security | |

| Services | Professional Services |

| Managed Services |

By Deployment Mode

| On-Premise |

| Cloud |

By End-use Industry

| IT and Telecom |

| BFSI |

| Healthcare |

| Industrial Manufacturing |

| Retail and E-commerce |

| Energy and Utilities |

| Aerospace, Military and Defense |

| Other End-use Industries |

By End-User Enterprise Size

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security | ||

| Endpoint Security | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | On-Premise | |

| Cloud | ||

| By End-use Industry | IT and Telecom | |

| BFSI | ||

| Healthcare | ||

| Industrial Manufacturing | ||

| Retail and E-commerce | ||

| Energy and Utilities | ||

| Aerospace, Military and Defense | ||

| Other End-use Industries | ||

| By End-User Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

Key Questions Answered in the Report

How fast is spending on managed security services growing in Thailand?

Services revenue is projected to rise at a 13.64% CAGR through 2031, outpacing product sales as boards outsource detection and response to fill talent gaps.

Which sector invests the most in cyber defenses?

BFSI led 2025 spending with a 24.36% share, driven by real-time payment fraud prevention and upcoming virtual-bank launches.

Why is healthcare emerging as the fastest-growing customer group?

The Mor Prom Plus telemedicine app and Health Link data-sharing framework expose more patient records to online channels, pushing healthcare security budgets to a 13.26% CAGR.

What drives cloud-security adoption despite on-premise dominance?

PDPA data-localization clauses and new in-country regions from AWS, Microsoft, and Google enable compliant hybrid architectures that expand cloud security at a 13.71% CAGR.

How are telecom operators capitalizing on cyber demand?

True Corporation bundles its CyberSafe AI engine with broadband and 5G plans, using network telemetry to offer automated threat detection to SMEs.

What is the biggest bottleneck to wider cybersecurity uptake in provincial Thailand?

A shortage of Thai-language professionals and price sensitivity among SMEs limit adoption, keeping talent and budget concentrated in Bangkok.

Page last updated on: