Thailand Customer Data Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

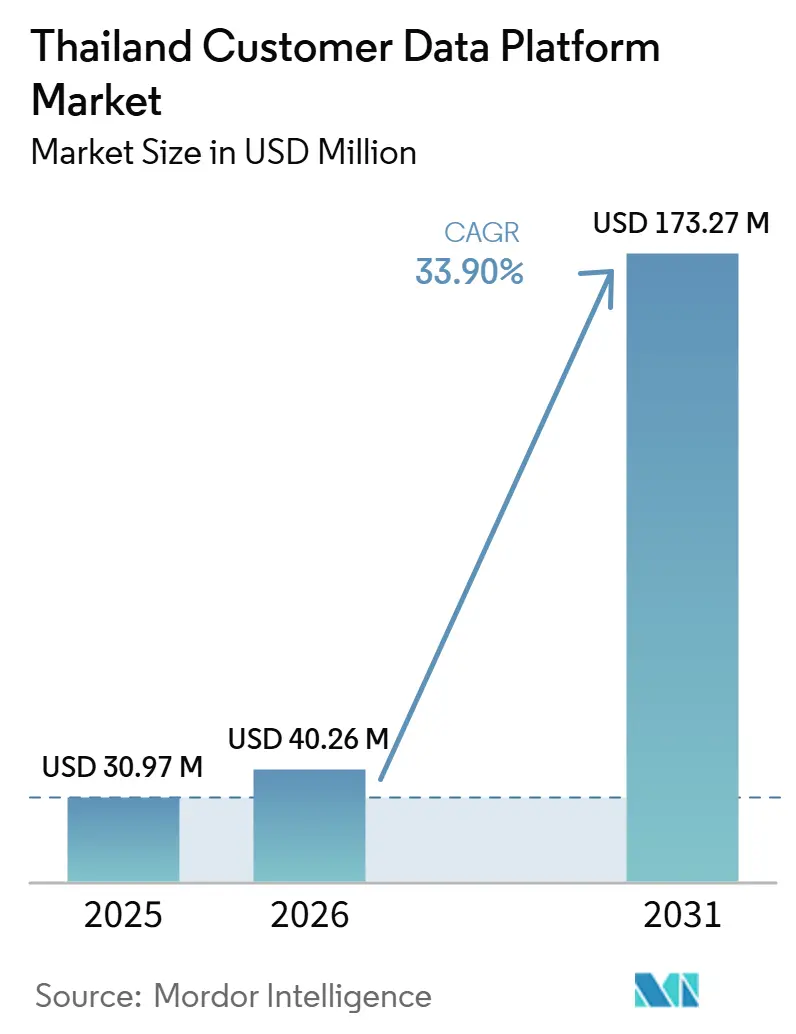

| Base Year Market Size (2025) | USD 30.97 Million |

| Market Size (2026) | USD 40.26 Million |

| Market Size (2031) | USD 173.27 Million |

| Growth Rate (2026 - 2031) | 33.90% CAGR |

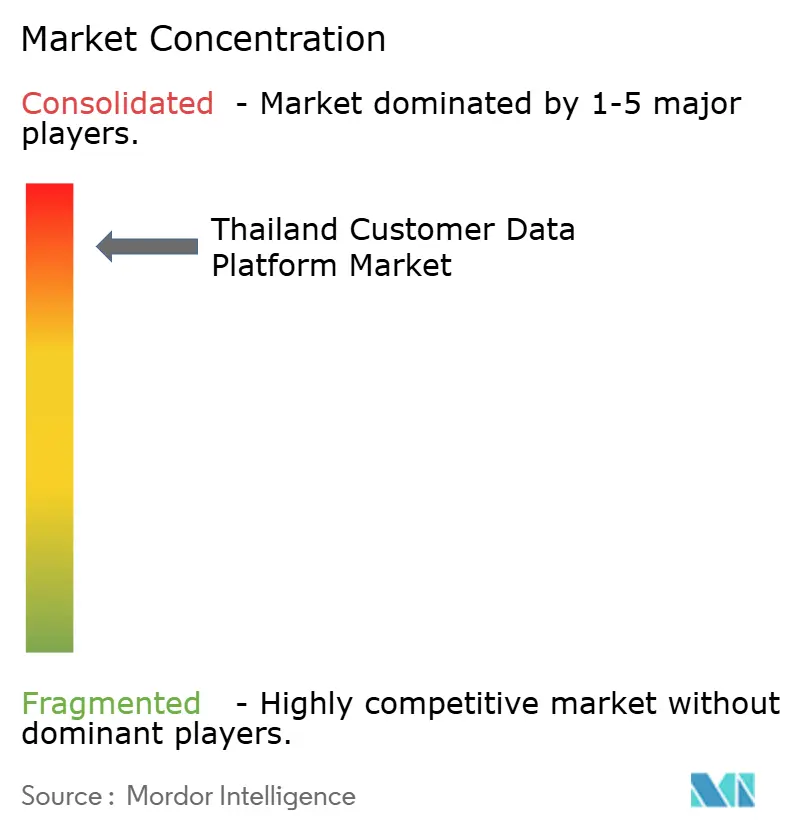

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Customer Data Platform Market Analysis by Mordor Intelligence

The Thailand customer data platform market size was valued at USD 30.97 million in 2025 and is estimated to grow from USD 40.26 million in 2026 to reach USD 173.27 million by 2031, at a CAGR of 33.90% during the forecast period 2026-2031. Thailand’s digital economy is expanding quickly, creating larger volumes of first-party customer data across online retail, mobile commerce, payments, and loyalty programs. The Thailand customer data platform market is also being shaped by LINE's strong role in daily customer engagement, as brands increasingly need a single system that can connect messaging identities with CRM records and offline transactions. Compliance needs have also risen in buying decisions as companies place greater focus on consent tracking, data residency, and auditability under Thailand’s PDPA framework. Global software providers, regional specialists, and Thai-native platforms are competing on connector depth, deployment speed, and local support, keeping the Thailand customer data platform market active across both enterprise and SME demand. The strongest white space remains outside Bangkok, where provincial digital adoption is improving, but many businesses still need lower-code platforms and managed implementation support.

Key Report Takeaways

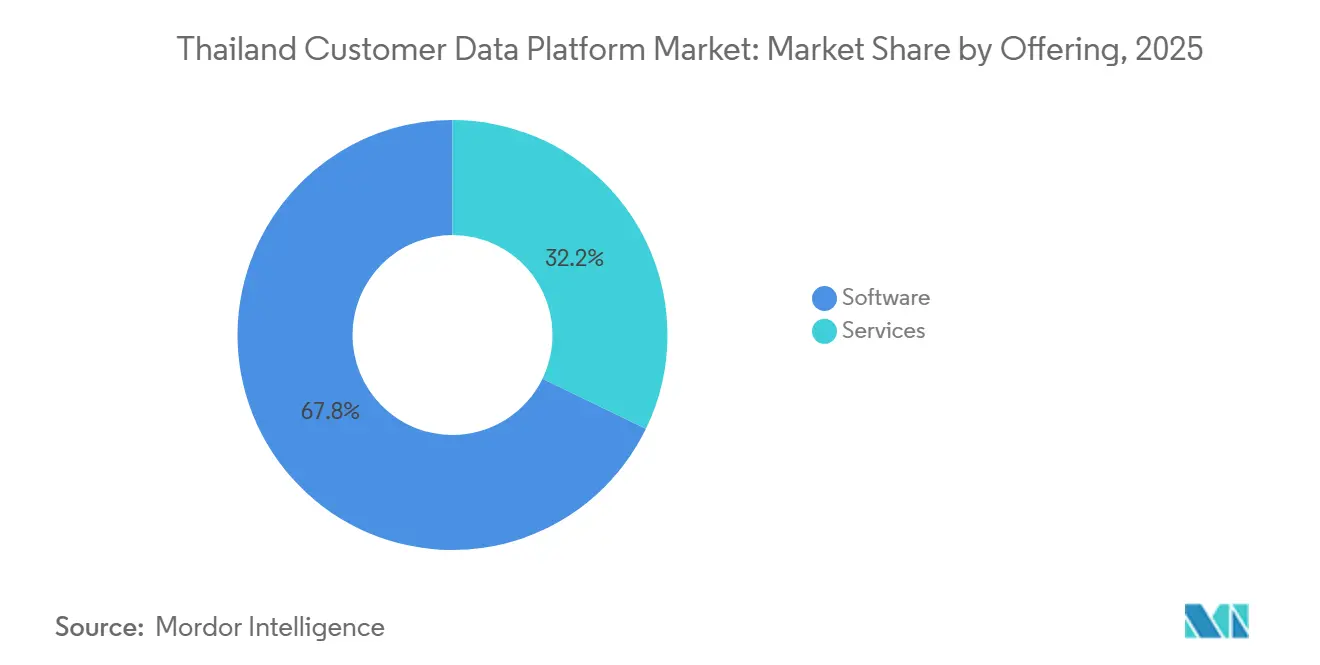

- By offering, software held 67.81% of Thailand customer data platform market share in 2025, while services is projected to expand at a 36.24% CAGR through 2031.

- By deployment mode, cloud accounted for 75.19% of the Thailand customer data platform market size in 2025, while hybrid is expected to grow at a 39.48% CAGR during 2026-2031.

- By organization size, large enterprises represented 61.74% of revenue in 2025, while SMEs are projected to record the fastest growth at a 37.81% CAGR through 2031.

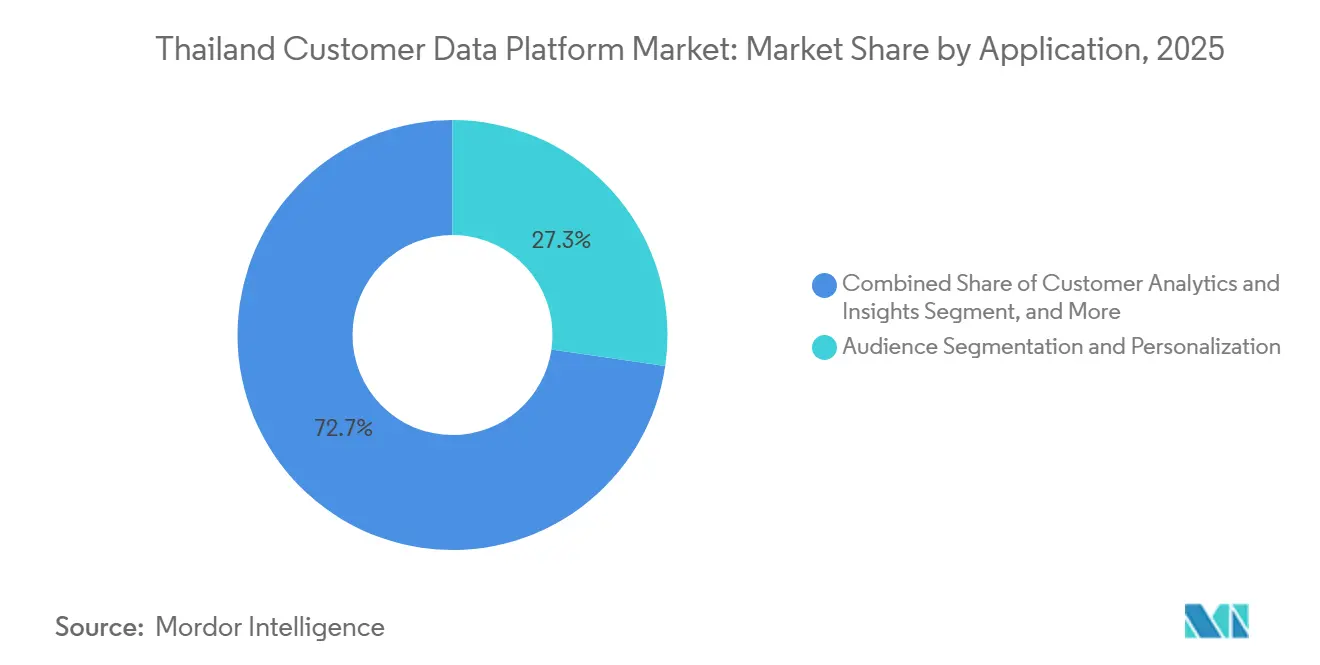

- By application, audience segmentation and personalization captured 27.31% of the Thailand customer data platform market size in 2025, while customer analytics and insights are expected to advance at a 40.62% CAGR through 2031.

- By end-user industry, retail and e-commerce held 29.83% of revenue in 2025, while media and entertainment is projected to expand at a 38.19% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Thailand Customer Data Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| LINE-Centric Engagement Requiring Unified Identity Resolution | +7.2% | National across retail, FMCG, and financial services | Short term (≤ 2 years) |

| Rapid Digital Commerce Adoption Among Thai Brands | +6.8% | National, concentrated in Bangkok, Chiang Mai, and Eastern Economic Corridor | Short term (≤ 2 years) |

| AI-Led Personalization Across Thai Omnichannel Journeys | +6.3% | National, spill-over to SEA regional deployments | Medium term (2-4 years) |

| PDPA-Driven Demand for Consent-Aware Customer Profiles | +5.4% | National, with early gains in financial and healthcare sectors | Medium term (2-4 years) |

| SME Migration to Low-Code Cloud CDPs | +4.1% | National, with early gains in Chonburi, Chiang Mai, and Phuket | Medium term (2-4 years) |

| Real-Time Activation of First-Party Data for Retention Marketing | +3.2% | National across e-commerce, telecom, and media verticals | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

LINE-Centric Engagement Requiring Unified Identity Resolution

LINE remained the main digital identity layer for Thai consumers in 2026, with 54 million users in the country and a penetration of above 80% of the population.[1] LY Corporation, “How LINE for Business in Thailand Drove 50% Sales Growth,” LY Corporation, lycorp.co.jp That scale makes unified identity resolution a core requirement in the Thailand customer data platform market, as brands need to connect LINE user IDs to CRM accounts, loyalty records, app activity, and store purchases into a single usable profile. The draft also showed that LINE’s MyCustomer environment accumulated 980 million data points, and that API message sends through LINE Official Accounts increased by 58%, highlighting how quickly customer interaction data is growing and becoming more complex. Vendors are therefore being evaluated less on general CDP claims and more on their ability to support real-time audience suppression, trigger activation, and identity stitching inside the LINE ecosystem. This gives the Thailand customer data platform market a local feature set that does not fully match standard global RFP templates, because LINE integration quality is now tied directly to campaign performance and data visibility. Antsomi’s launch of CDP 365 on LINE OA in Thailand also showed that specialized LINE-native offerings are entering the same buying cycle as broader global platforms.

Rapid Digital Commerce Adoption Among Thai Brands

Rapid growth in digital commerce is creating the strongest data volume tailwind for the Thailand customer data platform market, as every new customer action underscores the need for profile unification and live decisioning. The draft noted that Thailand’s e-commerce value reached USD 35.5 billion in 2025 and that online channels accounted for 11.4% of all retail sales, which raised the commercial cost of operating without a unified customer record. It also reported that 43.5 million Thai consumers shopped online, and that cross-border purchases accounted for 34% of total transactions, making customer matching and consent governance harder for businesses that still rely on disconnected CRM tools. THECA’s forward view that Thailand’s e-commerce value will reach THB 2 trillion (USD 60.8 billion) by 2030 points to a multi-year expansion in the volume of first-party event streams that brands must manage.[2]Thai E-Commerce Association, “Thailand's E-Commerce Value Set to Hit 1.07 Trillion Baht in 2025,” Nation Thailand, nationthailand.com As this transaction-based growth grows, the Thailand customer data platform market is shifting toward platforms built to reconcile web, app, payment, LINE, and store interactions in near real time rather than relying on older, rule-based marketing clouds. The result is a market where data orchestration is becoming central to customer retention, cross-sell execution, and visibility into repeat purchases across channels.

AI-Led Personalization Across Thai Omnichannel Journeys

AI-led personalization is adding momentum to the Thailand customer data platform market because brands now expect customer data systems to support more than simple reporting and list building. The draft linked this shift to high local AI usage and to rising consumer familiarity with algorithm-driven experiences, which is increasing expectations around timing, relevance, and message quality. In practice, AI use only becomes commercially useful when the underlying identity graph is complete, because fragmented profiles weaken recommendations, reduce prediction quality, and create inconsistent outreach across channels. EGG Digital’s work with Lotus on the My Shop Story campaign clearly showed this link, as CDP-driven first-party profiles combined with AI-generated narratives helped deliver a 25% coupon usage rate and a 25% uplift in spending per customer. That case matters for the Thailand customer data platform market because it shows that commercial value comes first from better customer data structure, and second from AI tooling. As more brands move from descriptive analytics to predictive and prescriptive customer actions, CDP quality is becoming a direct input into how well AI programs perform in live retail and loyalty environments.[3]EGG Digital, “EGG Digital and Lotus's Win Awards at MarTech Innovation Awards 2026,” EGG Digital, eggdigital.com

PDPA-Driven Demand for Consent-Aware Customer Profiles

PDPA enforcement is strengthening demand in the Thailand customer data platform market, as compliance functions are now treated as part of the core customer data architecture rather than as an external legal step. The draft recorded 8 administrative fines across 5 cases totaling THB 21.5 million (USD 663,000) by August 2025, and it also noted a THB 7 million (USD 216,000) fine in 2024 for security and governance failures. Those actions changed vendor evaluation criteria because platforms that can bind consent status to downstream activation and automatically suppress revoked records now carry a clear operational value. The September 2025 Binding Corporate Rules regime also raised the importance of data residency options for companies moving customer data across borders, especially for multinationals with regional operations. This is pushing the Thailand customer data platform market toward platforms with stronger audit trails, more robust policy controls, and greater flexibility in localized storage. It also means that procurement teams are increasingly viewing consent-aware customer profiles as a risk management requirement as much as a marketing capability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited In-House CDP Integration Talent Outside Bangkok | -2.4% | Tier 2 and Tier 3 cities, Chiang Mai, Khon Kaen, Hat Yai, Phuket | Medium term (2-4 years) |

| Fragmented Legacy MarTech Stacks Across Thai Mid-Market Firms | -1.8% | National, concentrated in mid-market firms outside the top 500 enterprises | Long term (≥ 4 years) |

| High Compliance and Localization Effort for Cross-Border Vendors | -1.1% | National, with specific impact on foreign vendors without in-country data residency | Medium term (2-4 years) |

| Data Quality Gaps From Multi-Source Thai Language and Offline Data | -0.9% | National across offline retail, regional chains, and provincial franchises | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited In-House CDP Integration Talent Outside Bangkok

Limited in-house integration capacity outside Bangkok remains a significant restraint on the Thailand customer data platform market, as many businesses still depend on a small pool of technical specialists for data engineering and stack integration work. A 2025 study in the Journal of Computer Science found that skills gaps and implementation risk were major barriers to advanced cloud adoption among Thai SMEs, and that this concern directly translates into longer onboarding cycles for CDP projects.[4]Science Publications, “Factors Influencing the Adoption of Cloud Computing for Thai SME Businesses,” Journal of Computer Science, thescipub.com This matters most in provincial cities, where businesses often need support for identity resolution, connector setup, and data governance but lack permanent internal teams to provide it. As enterprise rollouts in Bangkok absorb a large share of qualified talent, firms in Chiang Mai, Khon Kaen, and Chonburi face slower deployments and higher effective ownership costs. That makes the Thailand customer data platform market more favorable for vendors that offer low-code interfaces, pre-built connectors, and managed implementation models. It also explains, in clear terms, why provincial demand exists but does not always translate into rapid production deployments.

Fragmented Legacy MarTech Stacks Across Thai Mid-Market Firms

Fragmented legacy MarTech stacks continue to slow the Thailand customer data platform market because many mid-market firms still run customer data across separate POS systems, loyalty tools, campaign software, and local databases. The draft stated that implementation timelines can stretch from 3-6 months to 12-18 months when companies operate more than 5 disconnected systems, and that directly affects adoption velocity. The issue is not only technical, because every integration also requires governance review and a clear legal basis under the current PDPA environment. As a result, phased integration models often seem more practical than full platform replacement, especially for firms seeking faster time to value. This is also one reason the services layer is growing faster than software in the Thailand customer data platform market, because API alignment, governance design, and data mapping remain labor-intensive tasks. The structural result is slower adoption in parts of the mid-market, even when buyer interest in better customer intelligence is already present.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering, Services Gain Ground as Delivery Complexity Increases

Software accounted for 67.81% of revenue in 2025, indicating that core platform licensing remained the primary spending decision for most large buyers in the Thailand customer data platform market. This led to the need for a central system that could unify customer identities, create audiences, and support downstream activation from a single environment. Large enterprises in retail, BFSI, and telecom maintained software demand because they already had sufficient customer data scale to justify enterprise-grade platform investment. The software segment also remained visible in procurement because it represented the most direct budget line in large digital transformation programs and platform modernization plans. In that sense, software remained the anchor of the Thailand customer data platform industry even as service intensity began to rise across more deployments.

Services are projected to expand at a 36.24% CAGR through 2031, which shows that more buyers now recognize that value comes from execution quality as much as from software capability. The draft tied this pattern to implementation complexity because brands increasingly need support for connector setup, consent workflow design, analytics configuration, and activation logic. Adobe’s regional commentary in 2026 also suggested that Thai companies were moving more quickly toward broader customer experience stacks, which naturally raises demand for integration and advisory support. This should keep service revenue growing across healthcare, government, and regulated enterprise settings where governance and localization needs are heavier. Vendors that combine software with Thai-language implementation teams, pre-built local connectors, and stronger PDPA readiness are likely to hold a more durable position in the Thailand customer data platform market over the forecast period.

By Deployment Mode, Hybrid Builds a Balance Between Control and Scale

Cloud deployment accounted for 75.19% of the Thailand customer data platform market in 2025, making it the clear default option for most buyers entering the category. Its lead reflected the fact that many Thai organizations, especially SMEs, did not want to build and maintain dedicated infrastructure for customer data operations. Cloud delivery also aligned with the broader digital transformation cycle, as subscription pricing, faster updates, and easier connector deployment reduced upfront barriers to adoption. The June 2025 tax incentive for SME digital transformation further supported this direction by improving the business case for software-led modernization among smaller firms. In the base year, cloud therefore captured the largest adoption pool across both enterprise and emerging SME demand in the Thailand customer data platform market.

Hybrid is expected to grow at a 39.48% CAGR during 2026-2031, making it the fastest-growing deployment option in the Thailand customer data platform market. The main reason is that many organizations want to keep sensitive customer records within Thai jurisdiction while using public cloud resources to scale, improve cost efficiency, and accelerate campaign execution. This architecture is becoming more relevant for multinationals and regulated institutions that must align customer data use with local residency requirements and cross-border governance rules. On-premises deployment still has a role in healthcare systems, state-linked entities, and large financial institutions with existing data center infrastructure. Even so, the broader direction of the Thailand customer data platform market favors architectures that combine control with scalability instead of relying on a fully isolated environment.

By Organization Size, SMEs Add the Next Layer of Expansion

Large enterprises accounted for 61.74% of the Thailand customer data platform market in 2025, reflecting their stronger budgets and ability to manage multi-system integration projects. This segment was supported by deployments in retail groups, BFSI institutions, telecom operators, and large service organizations with clear needs around identity resolution and omnichannel coordination. The draft specifically referenced Salesforce deployments with Bumrungrad International Hospital and the Industrial Estate Authority of Thailand, demonstrating that enterprise demand spanned both commercial and institutional use cases. Large organizations also had the internal scale to treat CDP implementation as part of a wider data modernization program rather than as a stand-alone marketing tool purchase. That kept enterprise demand at the center of the Thailand customer data platform industry during the base year.

SMEs are projected to record a 37.81% CAGR through 2031, making them the fastest-growing segment in the Thailand customer data platform market. The strongest driver is policy support, because the June 2025 tax incentive lowered the financial burden of investing in qualifying digital tools and created a clearer path for first-time adoption. The draft also highlighted Thai-native low-code products such as ChocoCDP, dMASTER, and ConnectX, designed for local-language needs and for firms without dedicated data engineering teams. This local product fit matters because SMEs outside Bangkok often need easier interfaces, packaged onboarding, and subscription pricing that aligns with modest software budgets. As a result, the Thailand customer data platform market is likely to become more diverse in its customer mix over time, even if enterprise contracts still account for the larger revenue base.

By Application, Analytics Moves Closer to the Core Value Layer

Audience segmentation and personalization accounted for 27.31% of the market share in 2025, making it the largest application area in the Thailand customer data platform market. This lead made sense because segmentation is usually the first visible use case after a CDP goes live, and it often gives the fastest route to measurable commercial results. Retailers and e-commerce firms in particular relied on this use case because better targeting can quickly improve conversion rates, coupon usage, repeat purchases, and campaign efficiency. The segment also remained important because it serves as the bridge between unified customer profiles and real customer-facing execution across messaging, offers, and journey triggers. That kept segmentation and personalization at the center of the Thailand customer data platform market in the base year.

Customer analytics and insights are expected to grow at a 40.62% CAGR through 2031, making it the fastest-growing application group. Buyers are moving in this direction because they want more than audience creation and now expect churn prediction, next-best-action logic, and deeper behavioral interpretation from the same data foundation. The draft also noted that brands were moving from descriptive to predictive and prescriptive customer intelligence, which indicates a clear rise in analytic maturity. Consent and preference management is also drawing more attention as companies prepare for stricter governance and for stronger expectations around auditability and lawful use of customer data. The overall pattern suggests that the Thailand customer data platform market is shifting from simple data consolidation toward a model in which insight generation becomes a primary source of value creation.

By End-User Industry, Entertainment Narrows the Gap With Retail

Retail and e-commerce accounted for 29.83% of revenue in 2025, making it the leading vertical in the Thailand customer data platform market. That position reflected the sector’s early move into personalization, loyalty, and campaign measurement, where better customer data directly links to sales and margin outcomes. The draft highlighted major examples, such as Big C’s conversational AI shopping assistant and the development of the Amaze loyalty platform, both of which demonstrate how customer data infrastructure is moving closer to live commercial workflows. Retail also retained scale because it generates high-frequency interaction data across stores, apps, e-commerce, and loyalty programs, which makes profile unification especially valuable. This kept retail and e-commerce firmly ahead in the Thailand customer data platform market during the base year.

Media and entertainment is projected to expand at a 38.19% CAGR through 2031, which makes it the fastest-growing end-user segment. The main reason is that streaming services generate dense behavioral signals, including viewing time, content preference, and drop-off behavior, and that data becomes more valuable when tied to audience monetization and retention workflows. The draft also noted that Thailand had become ASEAN’s largest subscription video-on-demand market and that 70.7% of Thai internet users watched television via streaming services. BFSI, healthcare and life sciences, and IT and telecom remain important secondary verticals, while government and public administration are emerging as new demand centers as agencies modernize citizen-facing data systems. The result is a Thailand customer data platform market where the most attractive demand comes from sectors that produce high-frequency, consent-sensitive, and commercially actionable customer interaction data.

Geography Analysis

Bangkok remained the main center of deployment activity in 2025, because the largest enterprise buyers and the local operations of major international vendors were concentrated there. That concentration made the capital the primary base for account coverage, systems integration, and senior data governance support across the Thailand customer data platform market. Salesforce reinforced this pattern when it appointed Apisit Kuparatana as Country Leader and Managing Director for Thailand in October 2025 and later outlined plans for a Data and AI Center of Excellence before the end of 2026. Adobe’s regional approach also treated Bangkok as a key enterprise hub for Thailand, especially as AI-led customer experience programs expanded in 2026. This left Bangkok with the strongest concentration of current enterprise demand, implementation talent, and partner activity across the Thailand customer data platform market.

The provincial opportunity is strongest across the Eastern Economic Corridor, Chiang Mai, and major tourism and industrial centers, where SME density is high, but CDP penetration remains comparatively low. The main barriers are not weak digital interest, but the shortage of local integration talent and the presence of fragmented legacy customer systems outside the Bangkok enterprise base. The draft linked future expansion in these areas to the June 2025 tax incentive for SME digital transformation and to the estimated 3 million registered Thai SMEs outside the Bangkok metropolitan area. This creates a strong opening for Thai-language, low-code, and lower-cost platforms that can be deployed without heavy dependence on Bangkok-based consultants. The next wave of new logos in the Thailand customer data platform market is therefore likely to come from regional business corridors rather than from the already active enterprise core in the capital.

Thailand is also gaining importance in the regional picture, as the market’s 33.90% CAGR for 2026-2031 stood well above the Asia-Pacific benchmark cited in the draft. This faster pace reflects the combined effect of strong LINE usage, active PDPA enforcement, and fast digital commerce expansion, all of which create a more urgent need for identity resolution and governed activation. Cross-border deployments are becoming more important as brands operate across Thailand, Vietnam, Indonesia, and Malaysia, but those deployments now require clearer country-level storage and transfer controls. That trend supports additional demand for professional services and hybrid architecture design as the Thailand customer data platform market moves from local projects to regional customer data operating models.

Competitive Landscape

The competitive structure remained consolidated, with global vendors, regional specialists, and Thai-native platforms all competing for different buyer groups in the Thailand customer data platform market. Salesforce, Adobe, Oracle, SAP, Tealium, and Treasure Data were strongest in large-enterprise procurement because they offered full-stack capabilities and stronger integrations with existing CRM and ERP systems. Even so, the buying process in Thailand was more localized than in many other markets because LINE integration quality, Thai-language readiness, and local partner support directly affected implementation success. Treasure AI strengthened its enterprise position in July 2026 when it was recognized as a Leader in the 2026 IDC MarketScape for worldwide AI-enabled customer data platforms covering both B2C and B2B users. Insider also had measurable local traction in the draft’s vendor-tracking view, which showed that smaller specialist platforms could compete with larger suites in selected use cases.

Regional and local vendors are adding pressure in areas that global platforms do not always address well, especially where buyers need easier setup, lower cost, and stronger local data handling. ChocoCRM, dMASTER, and other Thai-native offerings were highlighted because they support local language requirements and help address data quality issues tied to Thai character encoding and address parsing. ChocoCRM’s regional customer base of more than 1,800 clients also suggested that local providers were building scale beyond niche pilot programs. Another important pattern is the convergence of CDP capability with loyalty infrastructure, which is bringing adjacent loyalty and CRM-led offerings into the same budget pool as stand-alone customer data platforms. That is changing the terms of competition in the Thailand customer data platform market, because buyers are increasingly comparing software ecosystems rather than just CDP modules.

Several strategic moves in 2026 showed how quickly competition was broadening beyond classic software licensing. Big C launched a Thai-language conversational shopping assistant on AWS in May 2026, which demonstrated how customer data activation was moving closer to live customer interaction and assisted commerce. Ascend Commerce and NTT DOCOMO signed a cooperation agreement in April 2026 to develop the Amaze platform into a leading loyalty and data system, which directly raised competitive pressure on international CDP vendors in retail. EGG Digital also entered a broad AI and data analytics alliance with Saha Group, TrueBusiness, and SoftBank in June 2026, showing that data activation capabilities were being embedded inside larger business ecosystems. This leaves the Thailand customer data platform market competitive but still open to vendors that can combine local execution, compliance-readiness, and measurable activation outcomes.

Thailand Customer Data Platform Industry Leaders

Salesforce, Inc.

Adobe Inc.

Oracle Corporation

SAP SE

Twilio Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Treasure AI recognized as a Leader in the 2026 IDC MarketScape for Worldwide AI-Enabled Customer Data Platforms for both B2C and B2B evaluations, according to Business Wire. The designation reflects the platform's integration of first-party, anonymous, and off-platform data into identity-resolved profiles supporting AI agent workflows across marketing, sales, and service, a capability configuration increasingly aligned with Thai enterprise requirements.

- June 2026: EDTH (Saha Group's digital investment arm) forged an AI and data analytics alliance with TrueBusiness, EGG Digital, and Japan's SoftBank Corp, per Bangkok Post. EGG Digital will deploy AI-driven data analytics and consumer intelligence solutions across Saha Group's operations, aiming to optimize media spending and personalize customer engagement at conglomerate scale, one of the largest first-party data integration commitments by a Thai industrial group.

- May 2026: Big C launched a conversational AI shopping assistant on AWS, announced by Amazon Web Services. The Thai natural-language shopping assistant serves over 20 million Big C customers and is built on customer behavioral data, demonstrating how retail CDP deployments are shifting from batch segmentation to real-time conversational activation.

- April 2026: CP Group's Ascend Commerce and NTT DOCOMO signed a business cooperation agreement to develop the Amaze loyalty platform, reported by Money and Banking Magazine. The collaboration integrates Amaze's 4 million members with DOCOMO's "Single ID Marketing" solution, aiming to position Amaze as Thailand's leading loyalty and data platform, a direct challenge to international CDP vendors in the retail omnichannel space.

Thailand Customer Data Platform Market Report Scope

The Thailand customer data platform (CDP) market refers to the ecosystem of software and associated services that enable organizations in Thailand to collect, unify, and manage customer data from multiple touchpoints into a single, persistent database. These platforms are designed to break down data silos, creating comprehensive customer profiles that can be leveraged for advanced audience segmentation, personalized marketing campaigns, customer journey orchestration, and predictive analytics. The market encompasses cloud, on-premises, and hybrid deployment models tailored to the operational needs of both large enterprises and SMEs across sectors such as retail, BFSI, healthcare, and IT. By integrating consent and preference management capabilities, CDPs help Thai businesses comply with evolving local data protection regulations while enhancing customer experience, driving brand loyalty, and improving overall marketing return on investment.

The Thailand Customer Data Platform Market Report is Segmented by Offering (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and SMEs), Application (Customer Data Collection and Profile Unification, Audience Segmentation and Personalization, Marketing Campaign and Customer Journey Orchestration, Customer Analytics and Insights, Consent and Preference Management, and Other Applications), and End-User Industry (Retail and E-Commerce, BFSI, Healthcare and Life Sciences, IT and Telecom, Media and Entertainment, Industrial Manufacturing, Government and Public Administration, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| SMEs |

| Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization |

| Marketing Campaign and Customer Journey Orchestration |

| Customer Analytics and Insights |

| Consent and Preference Management |

| Other Applications |

| Retail and E-Commerce |

| BFSI |

| Healthcare and Life Sciences |

| IT and Telecom |

| Media and Entertainment |

| Industrial Manufacturing |

| Government and Public Administration |

| Other End-User Industries |

| By Offering | Software |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| SMEs | |

| By Application | Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization | |

| Marketing Campaign and Customer Journey Orchestration | |

| Customer Analytics and Insights | |

| Consent and Preference Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| BFSI | |

| Healthcare and Life Sciences | |

| IT and Telecom | |

| Media and Entertainment | |

| Industrial Manufacturing | |

| Government and Public Administration | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the Thailand customer data platform market size in 2026 and how large will it be by 2031?

The Thailand customer data platform market was estimated at USD 40.26 million in 2026 and is forecast to reach USD 173.27 million by 2031, growing at a 33.90% CAGR.

Which offering type leads demand in Thailand customer data platform adoption?

Software led with 67.81% of revenue in 2025, because most large buyers still start with a core platform purchase before scaling service support.

Why does LINE matter so much for customer data platform deployments in Thailand?

LINE acts as a core digital identity channel in Thailand, so vendors need strong connector quality for identity matching, suppression, and live activation across LINE workflows.

Which deployment model is growing the fastest through 2031?

Hybrid is projected to grow the fastest at a 39.48% CAGR, because many organizations want both local control over sensitive data and cloud scalability.

Which customer group is expected to expand fastest in the coming years?

SMEs are expected to grow the fastest at a 37.81% CAGR, supported by tax incentives, lower-code tools, and more localized deployment options.

Which end-user sector is creating the strongest current revenue base?

Retail and e-commerce led with 29.83% of revenue in 2025, while media and entertainment is expected to post the fastest growth through 2031.

Page last updated on: