Tensor Processing Unit (TPU) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

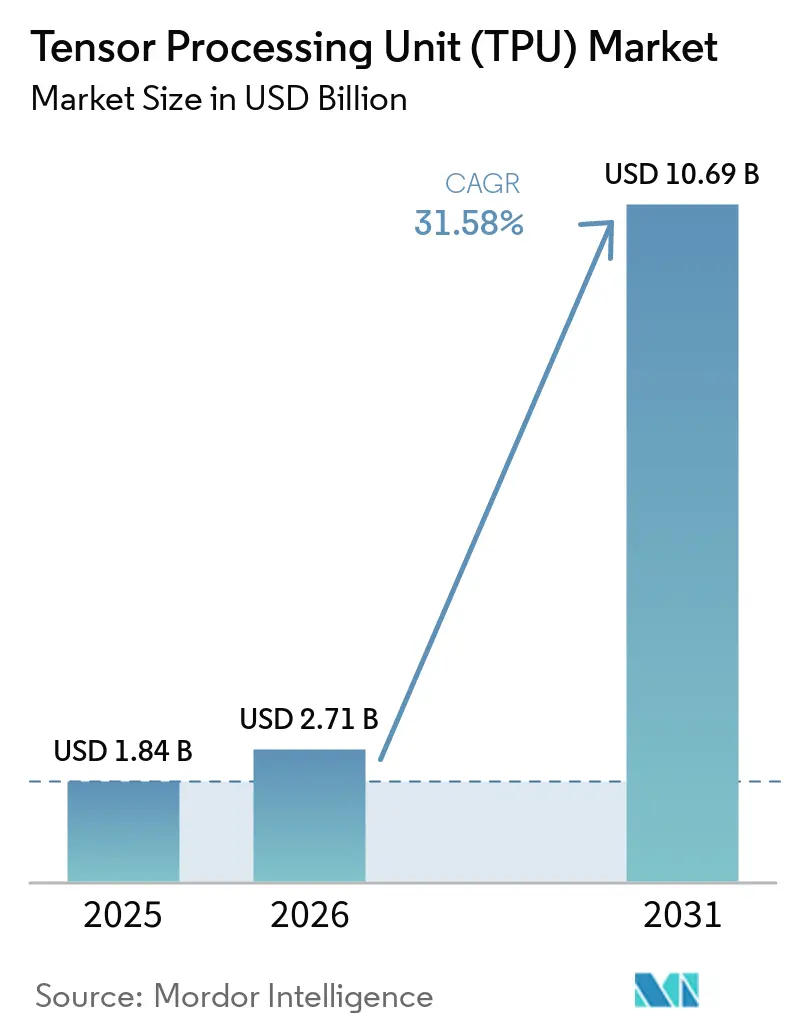

| Market Size (2026) | USD 2.71 Billion |

| Market Size (2031) | USD 10.69 Billion |

| Growth Rate (2026 - 2031) | 31.58% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tensor Processing Unit (TPU) Market Analysis by Mordor Intelligence

The tensor processing unit (TPU) market size was valued at USD 1.8 billion in 2025 and is forecast to reach USD 10.7 billion by 2031, at a CAGR of 31.6% over 2026-2031. The tensor processing unit (TPU) market is expanding as generative AI workloads move from pilot use into large-scale production environments. The market is also being reshaped by a clear move from training-led infrastructure planning toward inference-led silicon design. Power limits in major data center hubs are making performance per watt a more important buying factor across the tensor processing units (TPUs) market. Google LLC’s launch of separate training and inference chips in 2026 shows that product roadmaps are now being aligned to distinct AI compute stages rather than a single general accelerator path. The next phase of the tensor processing unit market will depend on how quickly enterprise buyers move past hyperscaler-led adoption and accept the software and integration trade-offs associated with non-CUDA environments.

Key Report Takeaways

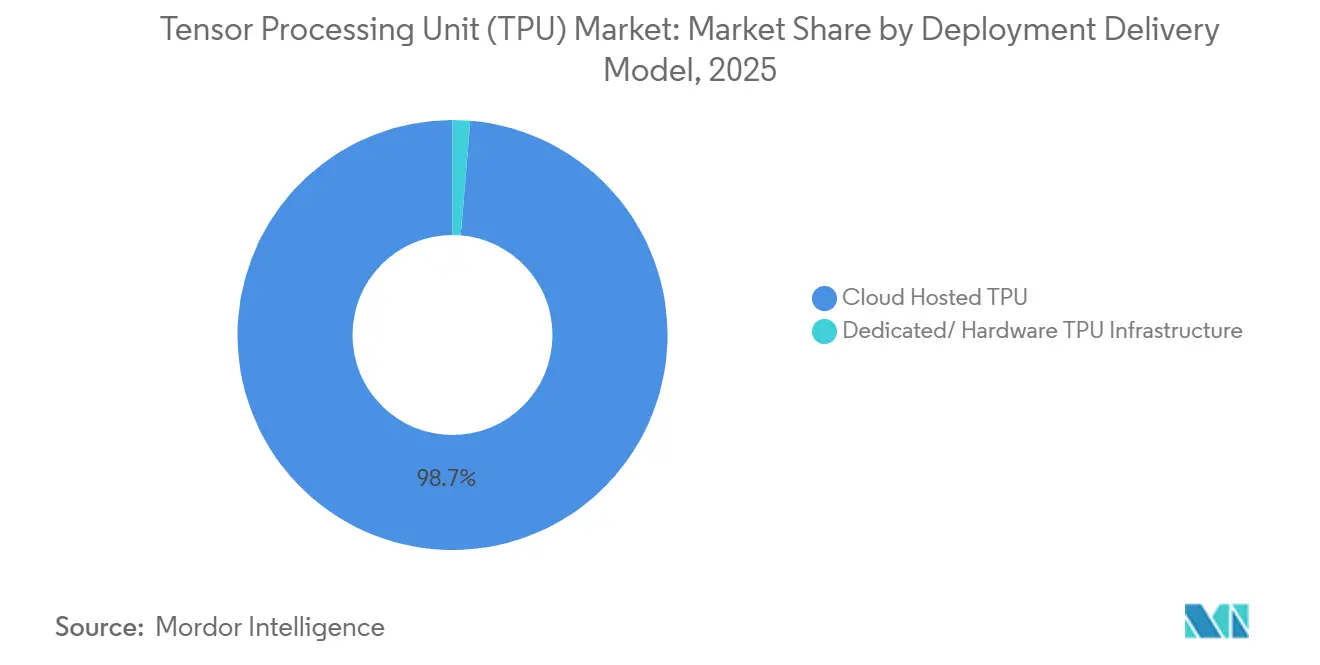

- By deployment model, cloud-hosted TPUs held 98.68% of revenue of the tensor processing unit (TPU) market in 2025, while dedicated or hardware TPU infrastructure is projected to expand at a 32.5% CAGR through 2031 in the tensor processing units market.

- By workload, inference accounted for 52.87% of revenue of the tensor processing units (TPUs) market in 2025, while training remained a critical secondary workload, and inference is forecast to grow at the fastest 32.7% CAGR through 2031.

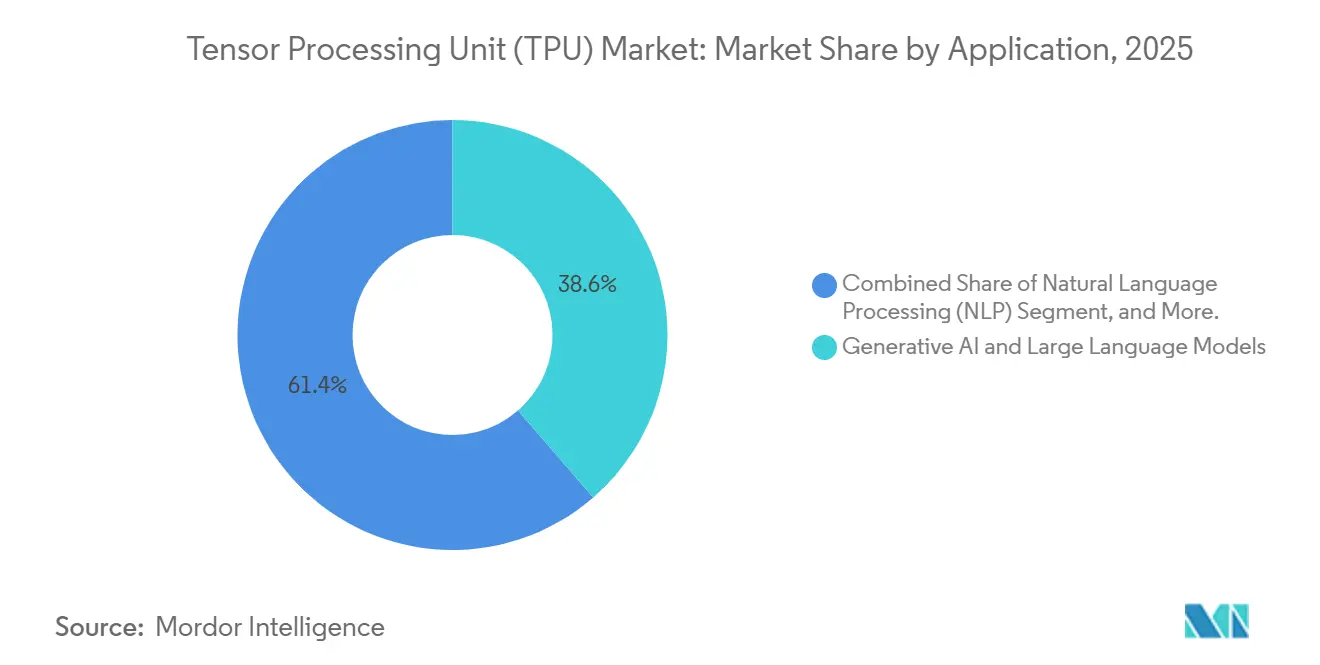

- By application, generative AI and large language model workloads captured 38.64% of revenue of the tensor processing units market in 2025, while NLP is projected to record the highest 33.6% CAGR through 2031 in the TPUs Market.

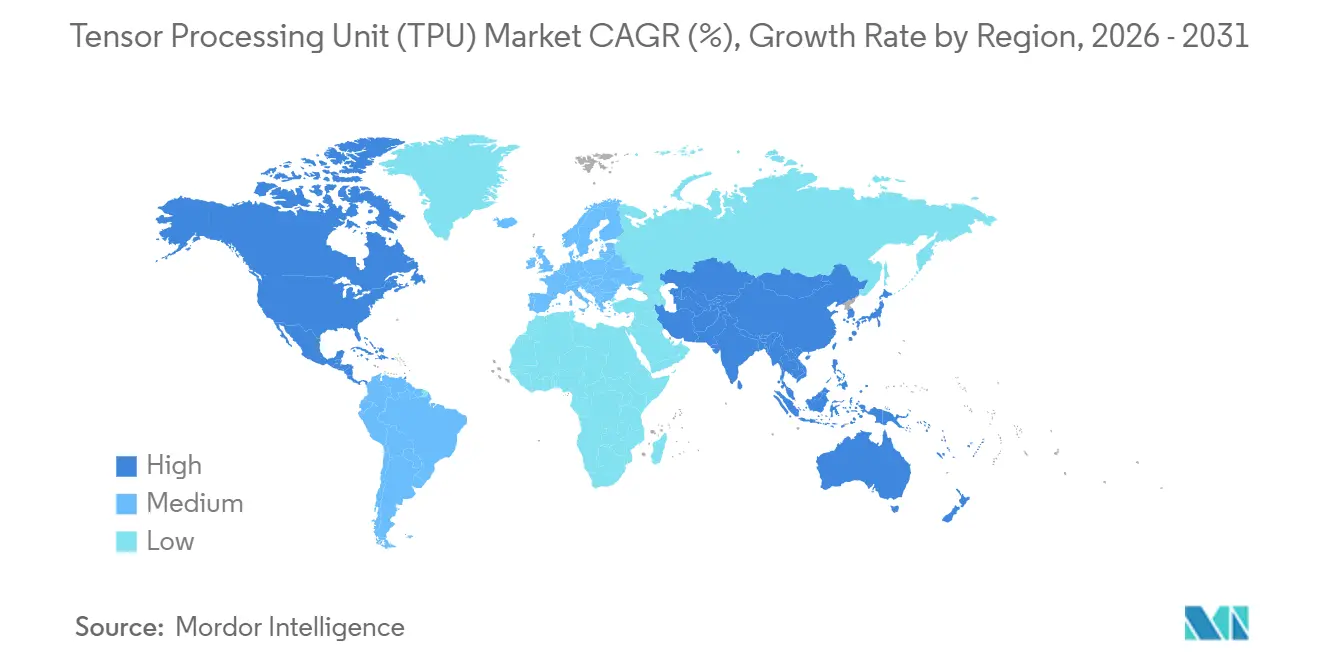

- By geography, North America held 35.72% of revenue in 2025 in the tensor processing unit market, while Asia-Pacific is forecast to grow at the fastest 33.8% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Tensor Processing Unit (TPU) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Enterprise GenAI Training and Inference Build-Out | +7.8% | Global, led by North America and Asia-Pacific | Short term (≤ 2 years) |

| Energy-Efficient AI Compute Demand in Power-Constrained Data Centers | +5.5% | North America, Europe, Asia-Pacific | Medium term (2–4 years) |

| Inference-First Architecture Shift for Agentic AI | +4.9% | Global, concentrated in North America | Short term (≤ 2 years) |

| Cloud TPU Access Reducing AI Infrastructure Entry Barriers | +3.6% | Global, with early gains in Southeast Asia and South America | Medium term (2–4 years) |

| Edge AI Rollout for Low-Latency On-Device Inference | +2.6% | Asia-Pacific core, spill-over to Middle East and Africa | Long term (≥ 4 years) |

| Multi-Supplier AI Silicon Sourcing by Hyperscalers and Sovereign Clouds | +2.2% | Global, with national programs in EU, Canada, and GCC nations | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Enterprise GenAI Training and Inference Build-Out

The tensor processing unit (TPU) market is benefiting from the fact that large generative AI systems now require multi-year compute planning rather than short-term capacity rentals. Google LLC’s TPU 8t superpod delivers 121 ExaFlops across 9,600 chips and is built to scale through the Virgo Network, which shortens training cycles for frontier models and supports much larger cluster designs.[1]Google LLC, “TPU 8t and TPU 8i Technical Deep Dive,” Google Cloud Blog, cloud.google.com Anthropic expanded its Google Cloud relationship in October 2025 and secured access to up to 1 million TPU chips, which shows that leading model developers are locking in TPU capacity as a strategic supply decision. That shift supports broader demand across fabrication, memory, networking, and cloud orchestration inside the tensor processing units (TPUs) market. It also raises the threshold for new entrants, because buyers with very large AI roadmaps increasingly favor platforms that can provide both current volume and a credible next-generation path.

Energy-Efficient AI Compute Demand in Power-Constrained Data Centers

The tensor processing unit (TPU) market is also gaining support from buyers who now treat energy efficiency as a core infrastructure requirement rather than a secondary feature. Google LLC stated that Ironwood delivered 2x the performance per watt compared to Trillium and was 30x more power-efficient than the first Cloud TPU from 2018.[2]Google LLC, “Ironwood TPUs Deliver 3.7x Carbon Efficiency Gains,” Google Cloud Blog, cloud.google.com In April 2026, Google LLC also reported that Ironwood improved compute carbon intensity by 3.7x compared with TPU v5p, which strengthens the case for TPU deployment in constrained power markets. The 8th-generation TPU 8t and TPU 8i continued that trajectory, delivering up to 2x better performance per watt than Ironwood, showing that efficiency gains are being carried forward from one release cycle to the next. As the tensor processing unit (TPU) market grows, this energy profile provides operators with a clearer path to adding AI capacity without relying solely on new power allocations.

Inference-First Architecture Shift for Agentic AI

The tensor processing units (TPUs) market is moving toward inference-led demand because production AI systems now spend more time serving requests than training base models. Google LLC’s launch of a dedicated TPU 8i for inference, separate from the training-focused TPU 8t, shows that the tensor processing units market is now being planned around two distinct hardware roles. TPU 8i includes 384 MB of on-chip SRAM, 288 GB of HBM, and a new Collectives Acceleration Engine that reduces on-chip latency by up to 5x for demanding inference tasks. Its Boardfly network topology also reduces the maximum network diameter from 16 to 7 hops, helping lower communication overhead for complex inference patterns. This matters because the tensor processing unit (TPU) market is no longer driven only by model creation; it is increasingly shaped by the steady, repeated cost of production inference.

Cloud TPU Access Reducing AI Infrastructure Entry Barriers

Cloud delivery remains one of the clearest adoption enablers in the tensor processing unit (TPU) market because it separates AI compute access from direct data center ownership. Enterprises can use current TPU generations on Google Cloud without taking on the hardware procurement, packaging, and systems integration burden associated with dedicated clusters. That matters for research groups, mid-sized enterprises, and public institutions that need frontier-class compute but lack hyperscaler-scale infrastructure teams. Anthropic’s long-term cloud TPU commitment also shows that cloud access is not limited to smaller buyers; it is becoming a strategic consumption model even for the largest AI developers.[3]Anthropic PBC, “Anthropic to Expand Use of Google Cloud TPUs and Services,” Google Cloud Press Corner, googlecloudpresscorner.com As a result, the TPUs market is expanding beyond direct in-house deployments and reaching buyers who would otherwise remain outside the addressable base.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Software-Portability Gap Versus CUDA-First Stacks | -3.5% | Global | Medium term (2–4 years) |

| High Capital Intensity and Integration Complexity | -2.8% | Global, acute in South America and Middle East and Africa | Long term (≥ 4 years) |

| GPU and Alternative Accelerator Competition | -2.1% | Global | Short term (≤ 2 years) |

| Advanced Packaging and HBM Bottlenecks | -1.6% | Global, primarily impacting TSMC CoWoS capacity in Taiwan | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Software-Portability Gap Versus CUDA-First Stacks

The largest adoption drag in the tensor processing unit (TPU) market remains the software portability gap between TPU environments and CUDA-first development practices. Enterprise AI teams often build around mature GPU libraries, familiar optimization workflows, and long-standing internal expertise, which raises the cost of moving workloads to a different stack. Google LLC continues to position Pathways, JAX, and XLA as a coordinated software layer across its AI systems, but this still requires many buyers to adapt tooling, testing, and deployment processes to a new operating model. This issue is especially evident in organizations that run mixed infrastructure and cannot justify a separate engineering path for a single accelerator family. Until portability improves further, the TPUs market will continue to face slower external uptake than its hardware metrics alone might suggest.

High Capital Intensity and Integration Complexity

The tensor processing unit (TPU) market also faces a practical limit in the cost and complexity of dedicated deployment. Google LLC’s AI Hypercomputer approach combines TPU pods, networking, memory, and orchestration into a tightly connected environment, and the performance gains come from that full-system design rather than a simple plug-and-play device swap. That structure works well for large buyers with specialized platform teams, but it is harder for smaller enterprises and institutions to absorb. Rapid product cadence adds another layer of difficulty because buyers must manage transition planning across multiple TPU generations in a short time window. This means the tensor processing units market will likely keep expanding first through cloud channels, while dedicated infrastructure remains concentrated among organizations that can manage long planning cycles and deep technical integration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment / Delivery Model: Cloud Dominance Persists as Dedicated Infrastructure Gains Strategic Traction

Cloud-hosted TPUs commanded 98.68% of deployment revenue in 2025 and captured the largest tensor processing unit (TPU) market share by delivery model. This dominance reflects the maturity of TPU-as-a-service and the practical advantage of accessing current chip generations without a long procurement cycle. Google LLC’s Ironwood platform scaled to 9,216 chips with 1.8 petabytes of shared HBM, enabling cloud users to access very large training and inference environments via a managed route. Anthropic’s agreement to access up to 1 million TPUs through Google Cloud also reinforced that the tensor processing units (TPUs) market is being shaped by long-duration cloud commitments, not only spot demand.[4]Anthropic PBC, “Anthropic to Expand Use of Google Cloud TPUs and Services,” Google Cloud Press Corner, googlecloudpresscorner.com

Dedicated or hardware TPU infrastructure is forecast to grow at a 32.5% CAGR through 2031, making it the fastest-growing delivery segment from a small base. This part of the tensor processing unit (TPU) industry is being supported by sovereign compute priorities, data residency needs, and research environments that require stronger workload isolation. Buyers in this segment are not only seeking raw performance but also repeatable operating conditions and greater direct control over utilization. Even so, the tensor processing units market remains cloud-led because dedicated systems still demand larger capital budgets, deeper engineering capacity, and tighter alignment with Google LLC’s software environment.

By Workload: Inference Establishes Structural Leadership as Agentic Deployments Scale

Inference accounted for 52.87% of total revenue in 2025 and represented the largest share of the tensor processing unit (TPU) market by workload. It is also the fastest-growing workload category, with a projected 32.7% CAGR through 2031. This shift reflects the fact that production AI systems now generate large volumes of repeated inference activity after models are deployed. Google LLC’s TPU 8i was built for that pattern, with higher on-chip memory, strong bandwidth, and lower latency features that target sustained serving efficiency.

Inference is taking the lead because production agents, assistants, search systems, and recommendation engines continuously consume compute after launch. The separate TPU 8i roadmap signals that Google LLC expects inference demand in the TPUs market to remain large enough to justify a distinct product family. Training still held 48% of the market in 2025 and remains strategically important because new frontier models continue to grow in scale. TPU 8t, with 121 ExaFlops per 9,600-chip superpod and a design path toward 1-million-chip scaling, keeps training central to the tensor processing unit (TPU) market even as inference becomes the larger revenue pool.

By Application: Generative AI Anchors Demand While NLP Expands the Fastest

Generative AI and large language model workloads held 38.64% of total application revenue in 2025, making them the largest application block in the tensor processing unit (TPU) market. That position reflects how closely Google LLC’s silicon roadmap is tied to large-scale model serving, enterprise retrieval workflows, and ongoing model iteration in production. In this part of the tensor processing unit (TPU) market, the link between hardware design and model behavior is especially important, as infrastructure buyers increasingly seek stable support for very large context windows and high request concurrency. The segment also benefits from the fact that generative AI is now moving from experimentation into repeat business use cases across search, coding, translation, and enterprise knowledge retrieval.

NLP is projected to grow at a 33.6% CAGR through 2031, making it the fastest-growing application segment in the tensor processing unit (TPU) market. Enterprise RAG systems, compliance monitoring, semantic search, and real-time translation are pushing steady demand for low-latency token generation at scale. Computer vision also remains important because TPU SparseCore was designed to handle large embedding workloads used in ranking and recommendation systems. HPC, data analytics, and autonomous systems round out the application mix, while Coral and edge-oriented TPU tools widen the use of TPU-based inference outside centralized cloud clusters.

Geography Analysis

North America accounted for 35.72% of revenue in 2025 and was the largest regional market for tensor processing units (TPUs). The region led because it combined hyperscaler headquarters, frontier model developers, and an enterprise base that adopted cloud AI infrastructure early. Google LLC’s internal AI programs and the wider Google Cloud ecosystem provided North America with a deep installed base of TPUs for training and inference. Anthropic’s October 2025 expansion with Google Cloud added another major demand signal from a leading model developer with large-scale compute needs. Even as the tensor processing unit (TPU) market broadens globally, North America is likely to remain the revenue leader because the region still concentrates the largest buyers, software talent pools, and commercial AI deployment activity.

Asia-Pacific is forecast to expand at a 33.8% CAGR through 2031 and is the fastest-growing region in the tensor processing units (TPUs) market. The region plays a dual role as both a fast-growing consumption base and a core production node in the broader AI hardware chain. National AI programs, manufacturing digitization, and cloud adoption across major Asian economies are widening the regional demand base for TPU-backed services. At the same time, the region remains closely tied to the semiconductor, packaging, and memory layers that support the global tensor processing unit TPU market.

Europe holds a meaningful position in the tensor processing unit (TPU) market, but growth is moderated by compliance-heavy procurement, data residency rules, and a more structured public-sector buying process. These conditions do not reduce demand, but they often lengthen deployment cycles and favor tightly governed cloud-delivery models. The Middle East and Africa remain an emerging regional opportunity, where sovereign AI agendas are beginning to support cloud consumption and selective infrastructure investment. South America remains the smallest regional market because hyperscaler infrastructure depth is still limited, and advanced hardware deployment costs remain high. Even so, the TPUs market is beginning to build an early base in these regions through cloud access, which lowers entry barriers for enterprise users who cannot justify a dedicated hardware investment.

Competitive Landscape

The tensor processing unit (TPU) market is highly concentrated and remains centered on Google LLC, which designed the architecture, iterated it across multiple generations, and commercialized it at scale through Google Cloud. That position gives Google LLC a hardware-software advantage that rivals still find difficult to match. In April 2026, Google LLC introduced TPU 8t for frontier training and TPU 8i for low-latency inference, which showed a clearer split between the two main demand paths inside the tensor processing unit (TPU) market. The same launch also highlighted a broader design network around Google LLC, with Broadcom and MediaTek tied into different parts of the new TPU generation. AWS Trainium, Microsoft Maia, and Meta MTIA are widening the competitive field, but the tensor processing units (TPUs) market still revolves around Google LLC’s installed base, cloud reach, and software maturity.

White-space opportunities in the tensor processing units market remain strongest in workloads where general GPU ecosystems are less efficient or less tailored to the task. Recommendation, ranking, and embedding-heavy systems are a good example because TPU SparseCore was built to address these patterns directly. Supply constraints still affect every custom AI silicon vendor, which means scale advantages and long supplier relationships matter as much as raw chip design. That dynamic favors established participants in the TPUs market because they can coordinate design, packaging, networking, and cloud delivery more effectively than newer challengers.

Google LLC also strengthened its position with a series of product and ecosystem moves across 2025 and 2026. Ironwood reached general availability in November 2025 and extended Google LLC’s inference and reinforcement learning profile with stronger performance per watt. In April 2026, Google LLC expanded the surrounding stack with new Axion-based virtual machines, which helped address preprocessing and system-balancing issues related to TPU utilization. Anthropic’s commitment to further expand its use of Google Cloud TPUs further reinforced Google LLC’s commercial pull in the tensor processing unit (TPU) market by turning one of the world’s most compute-intensive AI developers into a large, long-term platform customer.

Tensor Processing Unit (TPU) Industry Leaders

Google LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Google LLC unveils its eighth-generation TPU family, TPU 8t and TPU 8i, at Google Cloud Next. TPU 8t, designed by Broadcom, delivers 121 ExaFlops per 9,600-chip superpod with near-linear scaling to 1 million chips. TPU 8i, designed by MediaTek, provides 80% better performance per dollar for inference with 384 MB on-chip SRAM and a new Collectives Acceleration Engine targeting agentic AI workloads. Both chips deliver up to 2x better performance per watt versus Ironwood.

- April 2026: Google LLC publishes Ironwood's compute carbon intensity metrics, reporting a 3.7x improvement versus TPU v5p measured in January 2026, including embodied and operational lifecycle emissions. This establishes the industry's first systematically reported AI chip lifecycle carbon benchmark.

- October 2025: Anthropic announces a landmark expansion of its Google Cloud TPU partnership, securing access to up to 1 million TPU chips, worth tens of billions of dollars, with more than 1 gigawatt of capacity scheduled to come online in 2026. Anthropic cited TPU price-performance and energy efficiency as decisive procurement factors.

- November 2025: Google LLC announces the general availability of Ironwood, its seventh-generation TPU, optimized for inference and reinforcement learning at scale. Ironwood scales to 9,216 chips, accessing 1.8 petabytes of shared HBM via a 9.6 Tb/s Inter-Chip Interconnect, delivers 2x performance per watt versus Trillium, and is 30x more power-efficient than the first Cloud TPU from 2018.

Global Tensor Processing Unit (TPU) Market Report Scope

The Tensor Processing Unit (TPU) Market Report is Segmented by Deployment/Delivery Model (Cloud-Hosted TPU, and Dedicated/Hardware TPU Infrastructure), Workload (Training, and Inference), Application (Generative AI and Large Language Models, Computer Vision, Natural Language Processing (NLP), High-Performance Computing (HPC), Data Analytics, and Other Applications [Autonomous Systems, Predictive Analytics, etc.]), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud-Hosted TPU |

| Dedicated / Hardware TPU Infrastructure |

| Training |

| Inference |

| Generative AI and Large Language Models |

| Computer Vision |

| Natural Language Processing (NLP) |

| High-Performance Computing (HPC) |

| Data Analytics |

| Other Applications (Autonomous Systems, Predictive Analytics, etc.) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Taiwan | |

| Rest of Asia-Pacific | |

| Middle East and Africa | |

| South America |

| By Deployment / Delivery Model | Cloud-Hosted TPU | |

| Dedicated / Hardware TPU Infrastructure | ||

| By Workload | Training | |

| Inference | ||

| By Application | Generative AI and Large Language Models | |

| Computer Vision | ||

| Natural Language Processing (NLP) | ||

| High-Performance Computing (HPC) | ||

| Data Analytics | ||

| Other Applications (Autonomous Systems, Predictive Analytics, etc.) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Taiwan | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | ||

| South America | ||

Key Questions Answered in the Report

How large is the tensor processing unit (TPU) market expected to become by 2031?

The tensor processing unit (TPU) market is forecast to reach USD 10.7 billion by 2031 from USD 1.8 billion in 2025, growing at a 31.6% CAGR over 2026-2031.

Which workload is leading revenue growth for TPUs?

Inference led revenue with 52.87% share in 2025 and is also the fastest-growing workload, with a projected 32.7% CAGR through 2031.

Why does cloud deployment dominate TPU use?

Cloud-hosted TPUs held 98.68% of deployment revenue in 2025 because they give buyers access to current hardware without direct capital spending or deep integration work.

Which region is growing the fastest for TPU demand?

Asia-Pacific is the fastest-growing region and is projected to expand at a 33.8% CAGR through 2031, supported by AI infrastructure build-out and its role in the semiconductor supply chain.

What is the main barrier to wider enterprise uptake?

The largest barrier is still software portability, because many enterprise AI stacks remain optimized for CUDA-based workflows and that raises migration cost and complexity.

What is driving TPU adoption in 2026 and beyond?

The main drivers are hyperscaler-scale generative AI deployment, rising inference demand, and the need for better compute efficiency under tight data center power limits.

Page last updated on: