Telehandlers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 8.38 Billion |

| Market Size (2031) | USD 11.22 Billion |

| Growth Rate (2026 - 2031) | 6.01% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Telehandlers Market Analysis by Mordor Intelligence

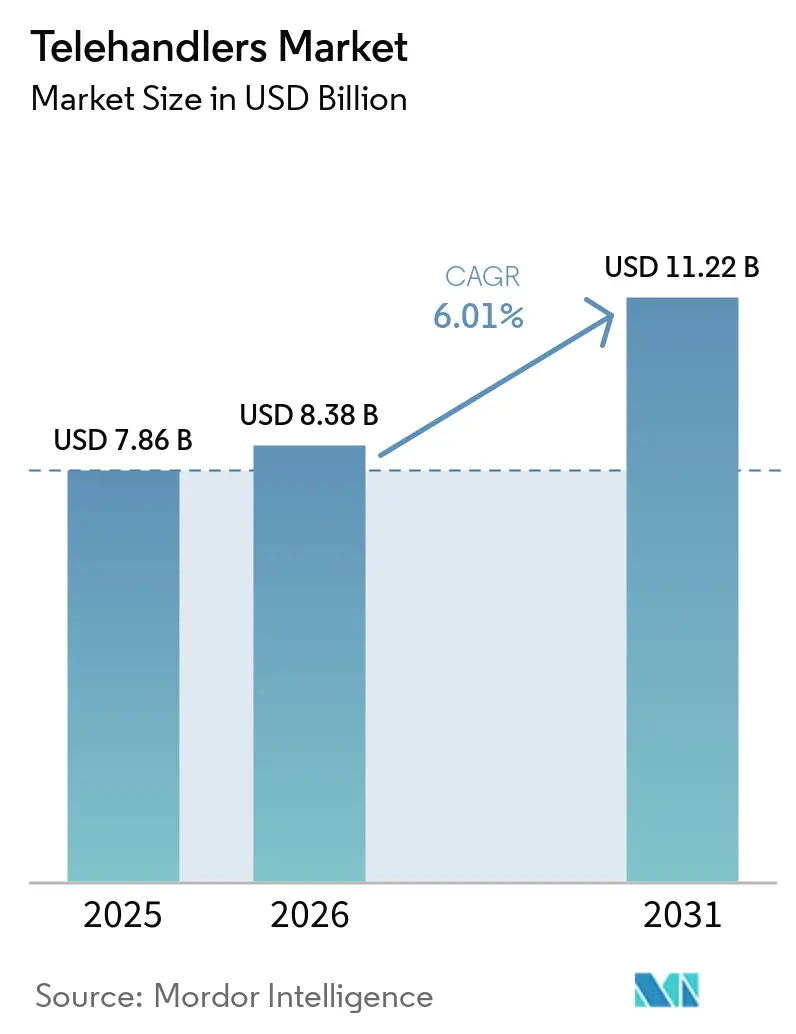

The telehandlers market size was valued at USD 7.86 billion in 2025 and is estimated to grow from USD 8.38 billion in 2026 to reach USD 11.22 billion by 2031, at a CAGR of 6.01% during the forecast period 2026-2031. The telehandlers market is benefiting from steady construction activity tied to urban development, broader use of mechanized handling on farms, and a stronger shift toward rental-led fleet deployment. Public infrastructure spending in Asia-Pacific, South America, and the Middle East is supporting equipment demand, while labor cost pressure in agriculture is making mechanized lifting and handling more necessary across several operating environments. In Europe and North America, tighter emissions rules are shortening the usable life of older diesel fleets and pushing buyers toward newer compliant machines, hybrid options, and electric platforms. The telehandlers market is also seeing competition move beyond lifting capacity, as buyers now weigh telematics, attachment flexibility, uptime support, and electrification roadmaps more closely when selecting suppliers. Even with supply pressure on steel and hydraulic systems and uncertainty around used-equipment values during fleet electrification, the telehandlers market retains a solid demand base that supports growth above broader GDP trends through 2031.

Key Report Takeaways

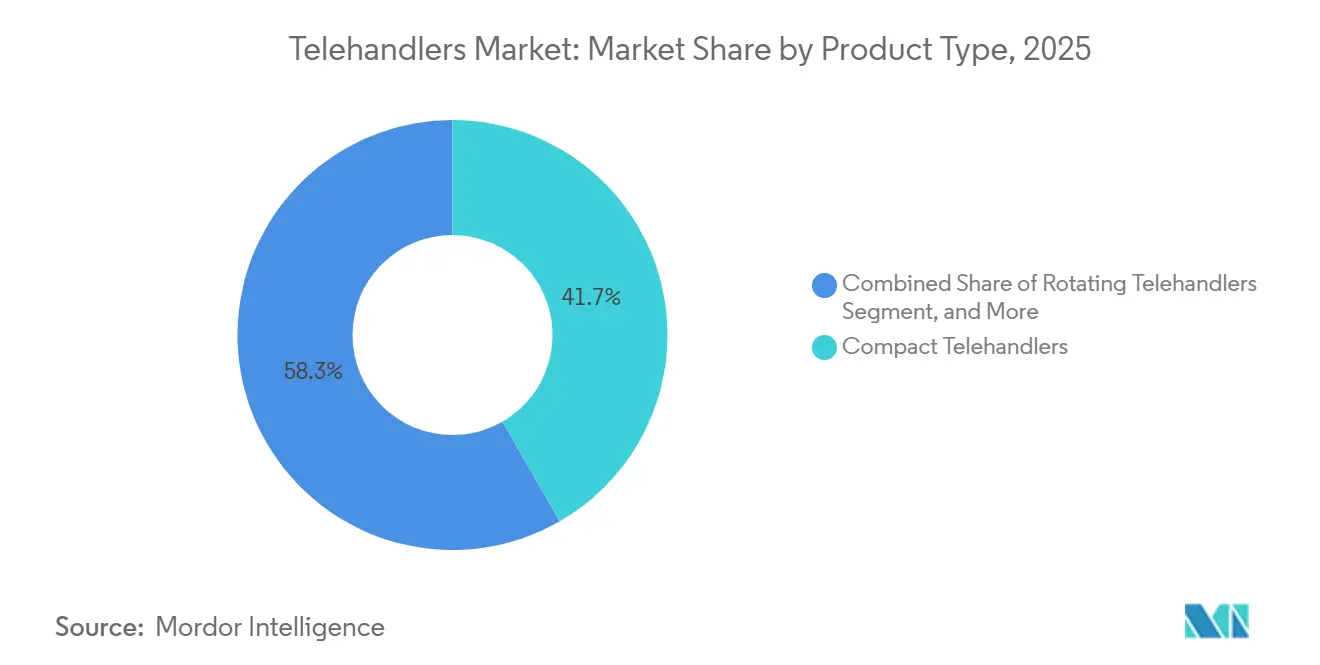

- By product type, compact telehandlers led with 41.68% share in the telehandlers market in 2025, while rotating telehandlers recorded the highest projected CAGR at 7.24% through 2031.

- By lift height, the 6-10 m segment accounted for 38.84% of the telehandlers market size in 2025, while above 10 m units are projected to advance at 7.87% CAGR through 2031.

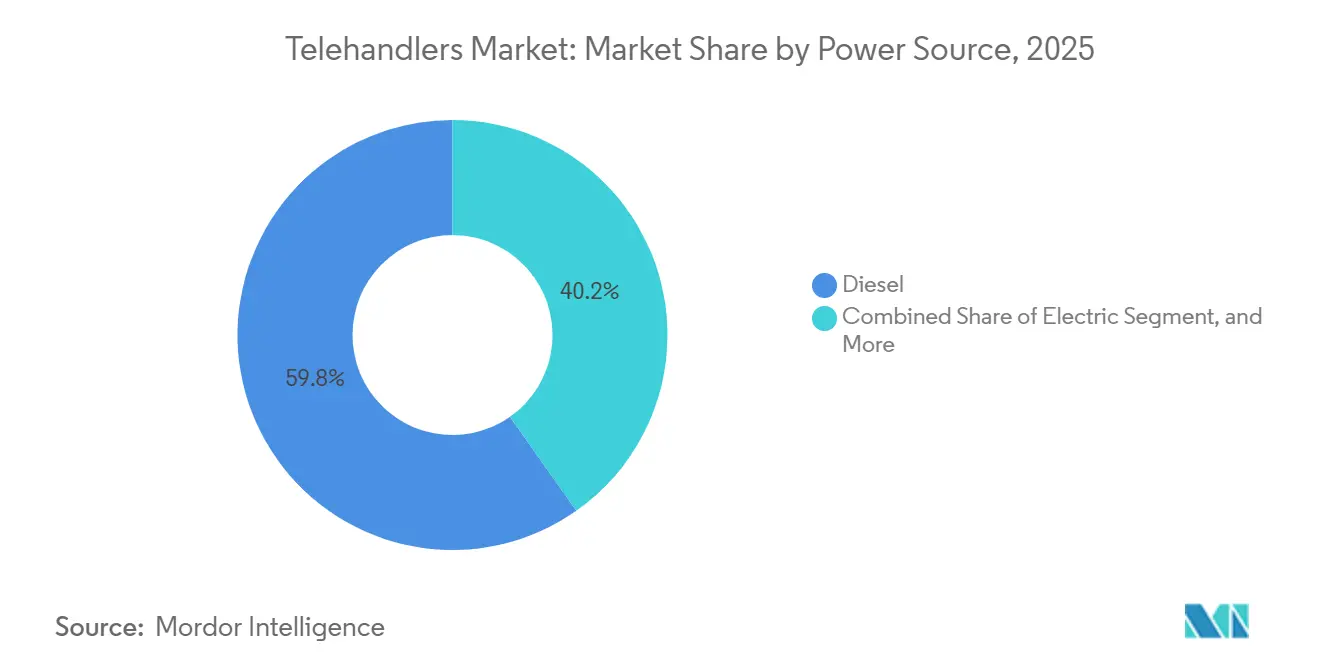

- By power source, diesel units held 59.77% share in the telehandlers market in 2025, while electric telehandlers posted the fastest projected CAGR at 8.12% through 2031.

- By application, construction represented 45.16% of the telehandlers market size in 2025, while logistics and industrial material handling are expected to grow at 8.43% CAGR through 2031.

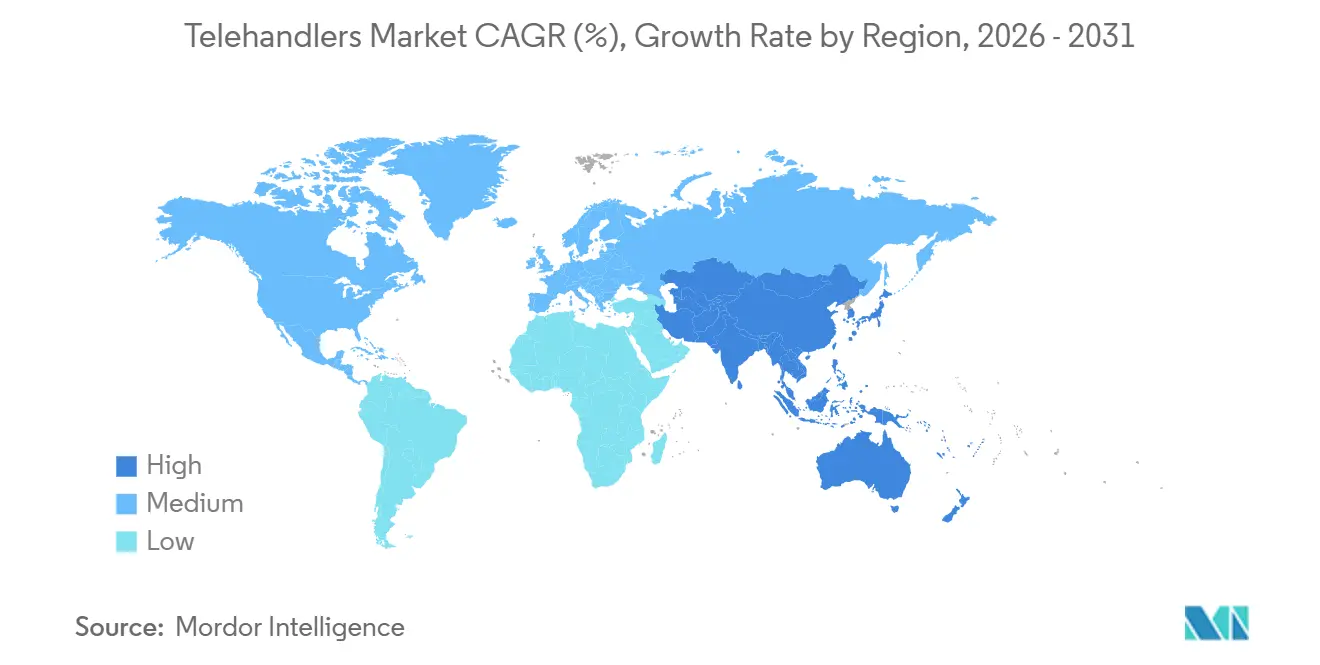

- By geography, Asia-Pacific held 31.58% of telehandlers market share in 2025 and is forecast to expand at 7.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Telehandlers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rental Fleet Expansion Across Construction and Agriculture | +1.5% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Infrastructure and Industrial Project Execution Demand | +1.3% | Asia-Pacific core, spill-over to South America and Middle East | Medium term (2-4 years) |

| Agricultural Mechanization and Labor Substitution | +1.0% | Europe, South America, and South and Southeast Asia | Medium term (2-4 years) |

| Electric Telehandler Adoption in Emission-Sensitive Sites | +0.8% | Europe and North America, expanding to APAC urban cores | Long term (≥ 4 years) |

| Rotating Telehandler Uptake for Crane Substitution | +0.6% | North America and Europe, emerging in Middle East | Medium term (2-4 years) |

| Attachment-Led Multi-Use Utilization Gains | +0.4% | Global, strongest in rental-intensive markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rental Fleet Expansion Across Construction and Agriculture

The telehandlers market is being shaped in a major way by rental companies that now treat telehandlers as core fleet assets rather than occasional additions. This is especially visible in North America and Europe, where fleet operators rely on telematics to track utilization, schedule maintenance, and keep machines in active circulation for longer periods. That model helps large buyers place repeat orders with more predictable replacement cycles, which gives OEMs better production visibility and steadier factory loading. The telehandlers market also benefits because rental fleets often favor better-specified units with stronger uptime tools, which raises the value of each sale even when unit growth moderates. Attachment flexibility adds to this effect, since rental customers want machines that can shift between forks, buckets, work platforms, and handling tools without losing productivity. CanLift Equipment’s USD 10 million fleet expansion with JLG in May 2025 showed how telematics and fleet diagnostics are now part of the buying decision, not just an added feature.

Infrastructure and Industrial Project Execution Demand

The telehandlers market continues to draw support from large project pipelines that need repeated lifting, placement, and material positioning over long execution periods. Demand is no longer centered only on conventional building construction, because industrial facilities, logistics parks, grid projects, and large public works all create sustained machine use. Asia-Pacific remains central to this pattern, with China and India supporting volume demand through transport, logistics, and urban development programs. The telehandlers market also gains when contractors need fewer machine changes on site, which increases interest in rotating units and higher-reach models that can cover more tasks during the same project cycle. This demand profile is helping above 10 m machines grow faster, since high-rise work, turbine servicing, and industrial shutdown activity all need greater reach and positioning capability. The result is a more value-focused order mix, where buyers place more weight on reach, stability, and jobsite versatility than on basic lifting performance alone.

Agricultural Mechanization and Labor Substitution

The telehandlers market is also being supported by farm operators who are moving from labor-heavy handling methods toward more mechanized daily operations. This is most visible in livestock, dairy, grain, and bale handling, where telehandlers are used for feed movement, stacking, loading, and yard work across long operating hours. The telehandlers market gains further when farms choose more capable machines, since that widens the role of a single unit across feeding, storage, and seasonal material movement. France remained a strong example in 2025, with 4,791 agricultural telehandler registrations, while machines above 4 tons and 7 m grew faster than the wider base, showing a move toward more capable farm equipment. OEMs are also adding operating intelligence that fits farm use, which makes the machine more valuable beyond lifting alone. Kramer’s integrated dynamic weighing system, highlighted at Bauma 2025, reflects this direction because weighing accuracy can support feed control and reduce waste during routine operations.

Electric Telehandler Adoption in Emission-Sensitive Sites

The telehandlers market is seeing a more structural change as electric platforms move from niche deployments into broader fleet planning. This shift is being driven by emission-sensitive urban worksites, indoor operations, and fleet owners that want lower maintenance exposure and better compliance readiness. EU Regulation 2025/14 and Stage V rules are helping accelerate this change by making compliance and road-use planning more important in European fleet decisions. The telehandlers market is also opening a new path through retrofit programs, because some fleet operators want lower-emission machines without full replacement spending. Manitou’s published lifecycle comparison for the MLT 625e showed 78% lower lifetime CO2 and lower maintenance needs than the diesel equivalent, which gives buyers a clearer economic case for electrified platforms. Manitou also disclosed real-world testing of a retrofit electric telehandler in 2025, which suggests that electrification may reach installed fleets as well as new-equipment demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Acquisition and Lifecycle Service Costs | -1.0% | Global, most acute in emerging economies and SME operator segments | Short term (≤ 2 years) |

| Skilled Operator and Safety Compliance Constraints | -0.8% | Global, most pronounced in South Asia, Africa, and South America | Medium term (2-4 years) |

| Residual Value Volatility During Fleet Electrification | -0.6% | North America and Europe | Long term (≥ 4 years) |

| Hydraulic Component and Boom Steel Supply Risk | -0.4% | Global, most acute in North America due to tariff exposure | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Acquisition and Lifecycle Service Costs

The telehandlers market still faces a clear barrier where upfront equipment cost is high relative to operator cash flow, especially among smaller contractors and family-run farms. Compact entry models remain more accessible, but advanced 5-6 ton units and high-reach machines require much larger capital commitments that many smaller buyers cannot absorb easily. This pushes a larger share of the telehandlers market toward rental channels and delays replacement cycles in direct ownership segments. Compliance engineering also adds cost, since newer diesel platforms need more complex after-treatment systems and service requirements under modern emissions rules.[1]Caterpillar Inc., “Emission Standards: Managing the Challenging Transition From EU Stage IIIA to EU Stage V in Europe,” Caterpillar, cat.comAt the same time, the used-equipment market is adjusting to the pace of electrification, which makes residual values harder to read for smaller operators and finance providers. Supply pressure on hydraulics, structural steel, and boom components adds another layer of risk, because cost volatility can narrow margins for OEMs and keep selling prices elevated.

Skilled Operator and Safety Compliance Constraints

The telehandlers market is also constrained by the availability of trained operators who can use newer machines safely and productively. This issue becomes more serious as telehandlers add rotating booms, load monitoring, attachment recognition, and other machine intelligence that increases the training requirement per unit. The telehandlers market feels this most in high-growth regions where equipment uptake is rising faster than vocational training capacity, including parts of South Asia, Africa, and South America. Safety rules in Europe and the United States also add time, documentation, and certification needs that can slow deployment across job sites and rental fleets. OEMs are responding by building more guidance into the machine, including automated boom functions and operator-support systems that reduce manual complexity.[2]JCB, “JCB Launches New Loadall 546-70 and 555-70 Telescopic Handlers,” JCB, jcb.com Even so, the gap between machine capability and operator readiness remains a practical limit on how fast new purchases can turn into productive utilization.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Compact Machines Lead While Rotating Units Gain Share Rapidly

Compact telehandlers held 41.68% of the telehandlers market share in 2025, making them the volume leader within the telehandlers market because they fit the widest range of jobsite and farm conditions. Their smaller footprint suits dense urban sites, narrow farm lanes, indoor-adjacent work areas, and facilities where overhead clearance is limited. This broad usability gives compact machines a durable installed base across construction, agriculture, and mixed rental fleets. The telehandlers industry also favors this segment because rental companies can place compact units across more customer profiles without narrowing the use case too much. In France, compact and agricultural positioning remained strong for established brands, with Manitou accounting for 31.1% of agricultural telehandler registrations in 2025 and Manitou plus JCB together reaching 57.4% of that market.

High-reach and heavy-lift machines serve a smaller base in unit terms, but they carry higher revenue per machine and are often selected for rental-grade work where the duty cycle is more intense. That makes them important to the telehandlers market even when their absolute volume is lower than that of compact models. Rotating telehandlers are the fastest-growing product category and are forecast to expand at 7.24% CAGR through 2031. Demand is rising because contractors want one machine to cover more lifting and access functions on a busy site, which helps reduce equipment coordination and improve utilization. The telehandlers market is therefore shifting toward more feature-rich rotating models, especially where attachment ecosystems, telematics, and higher reach can support premium rental pricing. Compact leadership should remain intact over the near term because the installed use base is broad and replacement demand is recurring. Even so, the balance of value creation in the telehandlers market is moving gradually toward rotating platforms, where customers are more willing to pay for multifunction capability and site efficiency. This mix change matters because it supports revenue growth even if the volume shift remains measured.

By Lift Height: Mid-Range Heights Anchor Volume While High-Reach Units Drive Value Growth

The 6-10 m segment accounted for 38.84% of the telehandlers market size in 2025, which made it the broadest volume band in the telehandlers market. That range covers routine residential and commercial construction work, standard stacking tasks on farms, and warehouse replenishment needs that do not require crane-level reach. Rental fleets favor this class because it can serve the largest variety of users without creating major transport or site-access issues. Machines below 6 m hold a smaller but steady role in constrained spaces, indoor-adjacent work, heritage structures, underground repair, and greenhouse settings. The telehandlers market continues to rely on this mid-range specification because it balances reach, versatility, and fleet productivity better than any other height band.

Above 10 m units are forecast to grow at 7.87% CAGR through 2031, which makes them the fastest-growing lift-height segment in the telehandlers market. Their use is expanding in high-rise construction, wind-energy service work, industrial shutdowns, and other applications where reach and stable placement matter more than simple load movement. OEM development activity follows that demand. JCB’s November 2025 launch of the Loadall 546-70 and 555-70 expanded its 7 m range to 5.5-ton capacity and added load-sensing hydraulics and automated boom controls, showing how manufacturers are lifting capability within higher-value specifications.[3]CB, “JCB Previews New Compact Loadall 526-60 and 530-60 Telehandlers,” JCB, jcb.com The telehandlers industry is using this segment to improve margin quality, since higher-reach units normally support stronger pricing and more specialized fleet demand. This part of the telehandlers market is also where electrification and advanced controls are likely to become more visible over time, especially in urban and indoor-sensitive projects. While volume remains centered in the 6-10 m range, the value mix is moving upward as contractors seek machines that can replace more specialized lifting equipment in selected tasks.

By Power Source: Diesel Remains the Volume Backbone as Electric Gains Structural Momentum

Diesel telehandlers accounted for 59.77% of telehandlers market size in 2025, which kept them as the main powertrain across the telehandlers market. Buyers still rely on diesel for strong torque, longer runtime, easier refueling, and dependable use on remote sites where charging access is limited. This is particularly relevant in rural construction, field agriculture, brownfield work, and heavy-duty outdoor applications. In Europe, the shift from older engines to Stage V-compliant machines supported replacement demand as operators moved away from less compliant equipment generations. Hybrid platforms sit between the two ends of the market and remain most relevant where operators want lower emissions without giving up full-day operating flexibility.

Electric telehandlers are projected to grow at 8.1% CAGR through 2031, making them the fastest-expanding power source in the telehandlers market. This growth is being supported by low-emission job sites, indoor handling requirements, falling battery costs, and increasing OEM investment in dedicated electric designs. Manitou’s corporate materials show that the MLT 625e can reduce lifetime CO2 by 78% and cut maintenance needs versus the diesel equivalent, which strengthens the ownership case in emission-sensitive settings.[4]Manitou Group, “2024 Universal Registration Document,” Manitou Group, manitou-group.com The telehandlers market is also moving past new-machine electrification alone, as retrofit activity starts to create a secondary route for lower-emission fleet conversion. As battery performance improves, the practical operating window for electric units should continue to widen in construction, logistics, and agricultural work that stays within predictable daily duty cycles.Diesel should remain the volume base through the forecast period because infrastructure and remote-site work still depend on its operating profile. Even so, the telehandlers market is building a longer-term shift in which electric models take a steadily larger role in urban fleets, regulated regions, and indoor material handling.

By Application: Construction Anchors Demand as Logistics Emerges as the Fastest-Growing Vertical

Construction represented 45.16% of the telehandlers market size in 2025, which kept it as the leading use case across the telehandlers market. Building construction uses telehandlers for facade materials, roofing supplies, and mechanical or electrical modules, while infrastructure work increasingly needs higher-reach and heavier-capacity units. This broad base gives construction the largest share because it combines ongoing urban building work with public project pipelines. Agriculture remains another major outlet, with telehandlers used in livestock yards, dairy units, crop storage, bale handling, and bulk material movement. The telehandlers industry continues to depend on both construction and agriculture because these two verticals provide the widest recurring use base for compact, mid-range, and specialized machines.

Logistics and industrial material handling is forecast to grow at 8.43% CAGR through 2031, making it the fastest-growing application within the telehandlers market. Growth is tied to e-commerce distribution centers, large-format warehouses, and industrial facilities that need repeated high-cycle lifting with tighter noise and indoor-air requirements. Electric telehandlers are especially relevant in this setting because operators want lower emissions inside enclosed buildings and fewer restrictions around worker comfort. The telehandlers market is also becoming more attractive to logistics users because telematics, payload visibility, and attachment control can improve inventory movement and reduce misplaced loads. SANY’s global telehandler positioning includes industrial manufacturing and port-logistics applications, which shows that major OEMs see this vertical as an important expansion path beyond traditional construction demand. This application mix matters because it broadens end-use demand and lowers dependence on any single construction cycle. It also shifts part of the telehandlers market toward higher-precision handling, electric operation, and software-supported fleet management as logistics users place more weight on uptime and flow efficiency.

Geography Analysis

North America held 31.58% share in 2025, while Asia-Pacific is expected to post the fastest regional CAGR at 7.18% through 2031. China and India anchor demand because both countries continue to create equipment needs across construction, logistics, and public works. The telehandlers market is also gaining from rising penetration in Southeast Asia, where urban growth and agricultural modernization are widening the addressable user base. Compact units fit many of these use cases well because they suit dense work zones and mixed farm operations. Japan and South Korea remain more mature markets, with stronger mechanization levels and a clearer preference for cleaner and more technically advanced fleets.

Europe remains the most technically mature region in the telehandlers market, with emissions compliance, fleet renewal, and electrification moving faster than in most other regions. EU Stage V pushed buyers toward newer machine generations, while EU Regulation 2025/14 added a more harmonized framework for non-road mobile machinery that circulates on public roads. France, the UK, Germany, and Italy remain central markets in the region. France registered 4,791 agricultural telehandlers in 2025, and the strongest movement came from heavier and taller agricultural units, which points to ongoing mechanization and higher machine capability on farms. North America also remains a large and structurally important part of the telehandlers market because rental penetration is high and newer projects increasingly demand better-specified fleets.

South America, the Middle East, and Africa remain important frontier zones for the telehandlers market, though each is at a different stage of adoption. South America draws support from agribusiness investment and selected mining and infrastructure activity, while the Middle East is driven more by large construction programs and long-duration project work. Saudi Arabia and the UAE are central to that regional demand because large sites need heavy material positioning at height across wide project footprints. Africa is still earlier in its development cycle, but South Africa, Egypt, and Nigeria are creating a latent base for telehandlers as mining, infrastructure, and urbanization expand. The telehandlers market could deepen more quickly in these regions if OEMs strengthen local service coverage, parts availability, and operator support.

Competitive Landscape

The telehandlers market is moderately concentrated, with a core group of global OEMs that includes JCB, Manitou, Caterpillar, Merlo, and Bobcat, alongside a wider field of European specialists and growing Chinese participants. This structure keeps the telehandlers market competitive without making it highly fragmented, because scale still matters in manufacturing, distribution, and after-sales support. Product competition is no longer centered only on lift height and capacity. Buyers now compare electrification plans, telematics capability, attachment range, and service support more closely when choosing between brands. That shift is raising the value of software, diagnostics, and machine intelligence across the telehandlers market.

JCB has responded by putting more operating support into the machine itself. Its higher-specification Loadall agricultural models launched in November 2025 included IntelliAssist automated boom controls, while the previewed compact Loadall 526-60 and 530-60 models for 2026 added a redesigned cab, more glass area, lower interior noise, and upgraded display options. Manitou has taken a broader platform approach in the telehandlers market through its EUR 460 million (USD 535 million) investment program, which includes a mechanical-welding plant in Candé, a lithium-ion battery plant in Castelfranco, and the May 2025 acquisition of Sitia’s robotics division to support autonomous material-handling development. These moves show that leading suppliers are competing through manufacturing control, battery capability, and software-linked product development rather than through mechanical specifications alone. Wacker Neuson and Kramer are also pushing differentiation through weighing and electric-platform innovation, which supports more precise handling and cleaner operation in selected end uses.

The telehandlers market also has open space in retrofit electrification, indoor logistics-focused compact electric units, and underserved emerging regions where service networks are still thin. Chinese manufacturers are important to watch because they are extending both product reach and geographic coverage. XCMG now presents telehandlers ranging from 10-17 m of lift height and supports them with a wide attachment offering, which strengthens its ability to compete in more than one use case. SANY is taking a similar path by positioning telehandlers for construction, industrial manufacturing, and port-logistics use, which broadens its addressable demand base. The telehandlers market should therefore remain active and innovation-led, but leadership will continue to favor OEMs that can pair equipment breadth with strong service infrastructure and digital fleet support.

Telehandlers Industry Leaders

J C Bamford Excavators Ltd.

Caterpillar Inc.

Manitou BF SA

Bobcat Company

Terex Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Lingong Group, alongside its subsidiaries Shandong Lingong Construction Machinery (SDLG) and Lingong Heavy Machinery (LGMG), is set to make its global debut at CONEXPO-CON/AGG 2026, following a recent consolidation and brand refresh.

- February 2026: SANY Marine, the port machinery business unit of SANY Group, unveiled a strategic partnership with Construction Equipment Australia (CEA), a division of the CFC Group, during its Global Customer Summit & Smart E-Product Launch. This alliance aims to introduce SANY's telehandlers and material handlers to Australia's expanding material handling sector, emphasizing a blend of robust durability and cutting-edge innovation, specifically designed for the Australian market's needs.

- May 2025: CanLift Equipment invested USD 10 million in partnership with JLG Industries, adding more than 70 machines including rotating telehandlers and ultra-compact telehandlers, with ClearSky Smart Fleet and SkyPower cited as key differentiators for its Canadian rental fleet.

- May 2025: Manitou Group acquired the robotics division of Sitia, including intellectual property and 7 specialist engineers, and created Manitou Group Robotics to accelerate autonomous material-handling development aligned with its LIFT 2030 strategy.

Global Telehandlers Market Report Scope

The Telehandlers Market covers telescopic material-handling machines that combine forklift lifting with crane-like reach through an extendable boom. These machines are used to lift, move, and place heavy loads at height or across hard-to-reach areas in construction, agriculture, and industrial operations.

The Telehandlers Market is Segmented by Product Type (Compact Telehandlers, High-Reach Telehandlers, and Heavy-Lift Telehandlers), Lift Height (Below 6 Meters, 6-10 Meters, and Above 10 Meters), Power Source (Diesel, Hybrid, and Electric), Application (Construction, Agriculture, Mining and Quarries, and Logistics and Industrial Material Handling), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value in USD.

| Compact Telehandlers |

| High-Reach Telehandlers |

| Heavy-Lift Telehandlers |

| Below 6 Meters |

| 6-10 Meters |

| Above 10 Meters |

| Diesel |

| Hybrid |

| Electric |

| Construction | Building Construction |

| Infrastructure and Civil Works | |

| Agriculture | Livestock and Dairy |

| Crop and Bulk Material Handling | |

| Mining and Quarries | |

| Logistics and Industrial Material Handling |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Product Type | Compact Telehandlers | |

| High-Reach Telehandlers | ||

| Heavy-Lift Telehandlers | ||

| By Lift Height | Below 6 Meters | |

| 6-10 Meters | ||

| Above 10 Meters | ||

| By Power Source | Diesel | |

| Hybrid | ||

| Electric | ||

| By Application | Construction | Building Construction |

| Infrastructure and Civil Works | ||

| Agriculture | Livestock and Dairy | |

| Crop and Bulk Material Handling | ||

| Mining and Quarries | ||

| Logistics and Industrial Material Handling | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the expected value of telehandlers by 2031?

The telehandlers market is projected to reach USD 11.22 billion by 2031, up from USD 8.38 billion in 2026, at a 6.01% CAGR over 2026-2031.

Which region leads telehandlers demand?

North America led in 2025 with 31.58% share and is also the fastest-growing regional segment with a 7.18% CAGR through 2031.

Which product category is growing fastest in telehandlers?

Rotating telehandlers are the fastest-growing product type, with projected growth of 7.24% CAGR through 2031.

Why are electric telehandlers gaining traction?

Electric models are benefiting from emissions rules, indoor-use requirements, and lower maintenance needs, and the segment is forecast to grow at 8.12% CAGR through 2031.

Which application creates the most demand for telehandlers?

Construction remained the largest application in 2025 with 45.16% share, supported by both building work and infrastructure projects.

What is the main competitive shift among telehandler manufacturers?

Competition is moving from pure lift capacity toward telematics, electrification, attachments, and total ownership value, with leaders investing in batteries, automation, and machine intelligence.

Page last updated on: