Telecom Subscriber Data Management Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 5.40 Billion |

| Market Size (2030) | USD 10.80 Billion |

| Growth Rate (2025 - 2030) | 14.87% CAGR |

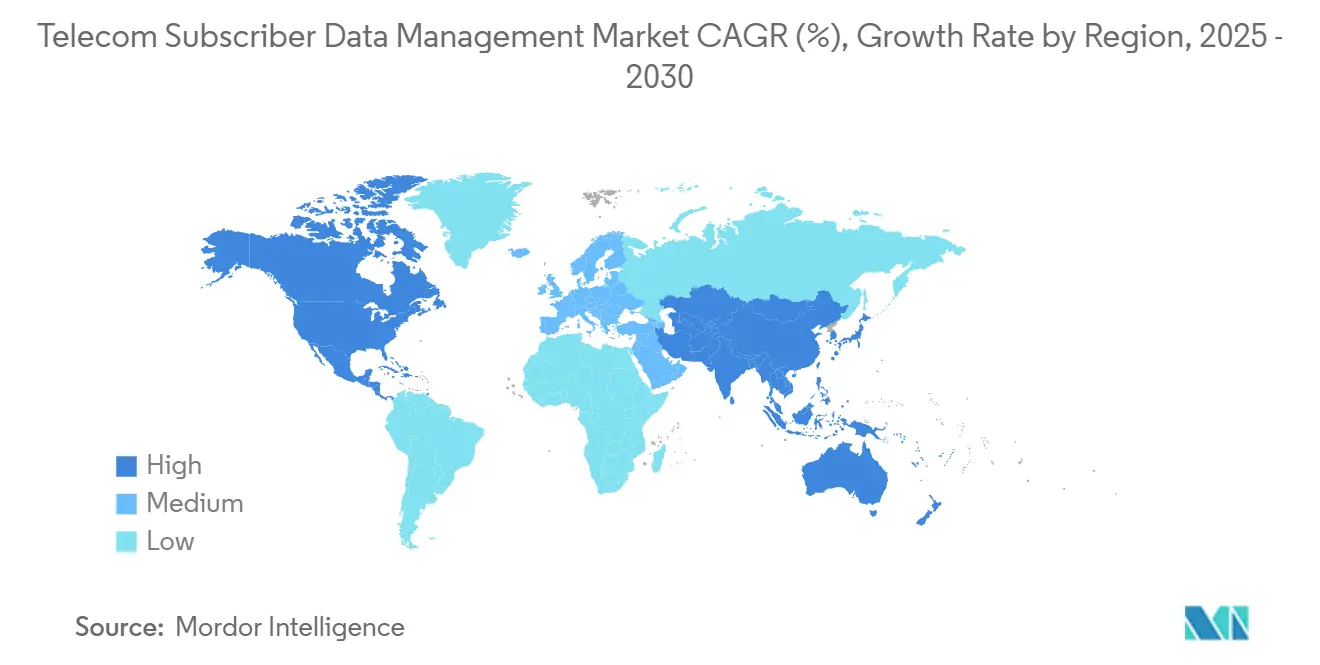

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

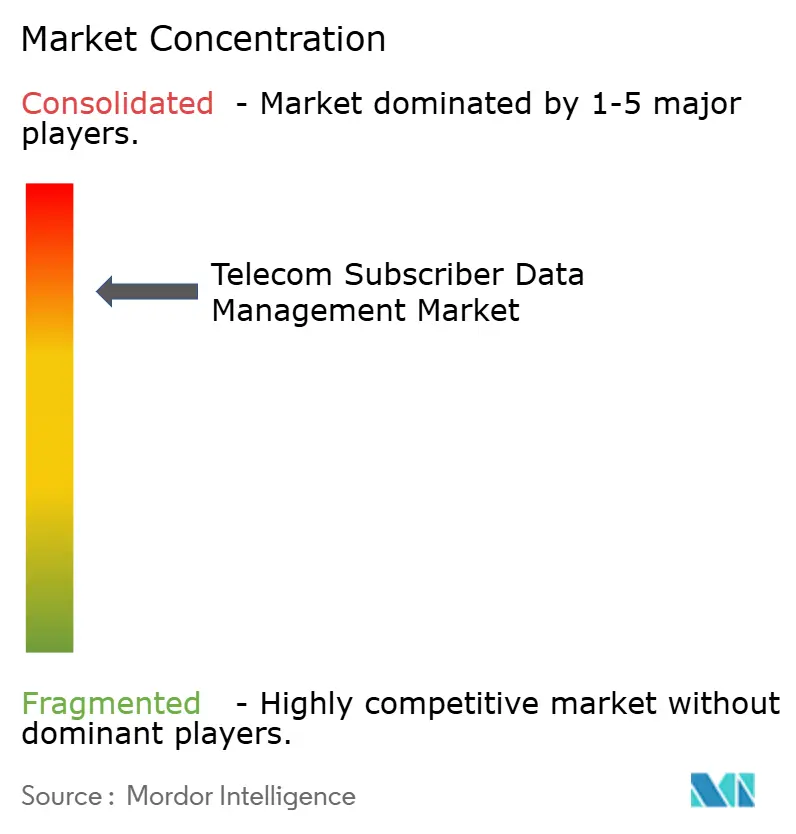

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Telecom Subscriber Data Management Market Analysis by Mordor Intelligence

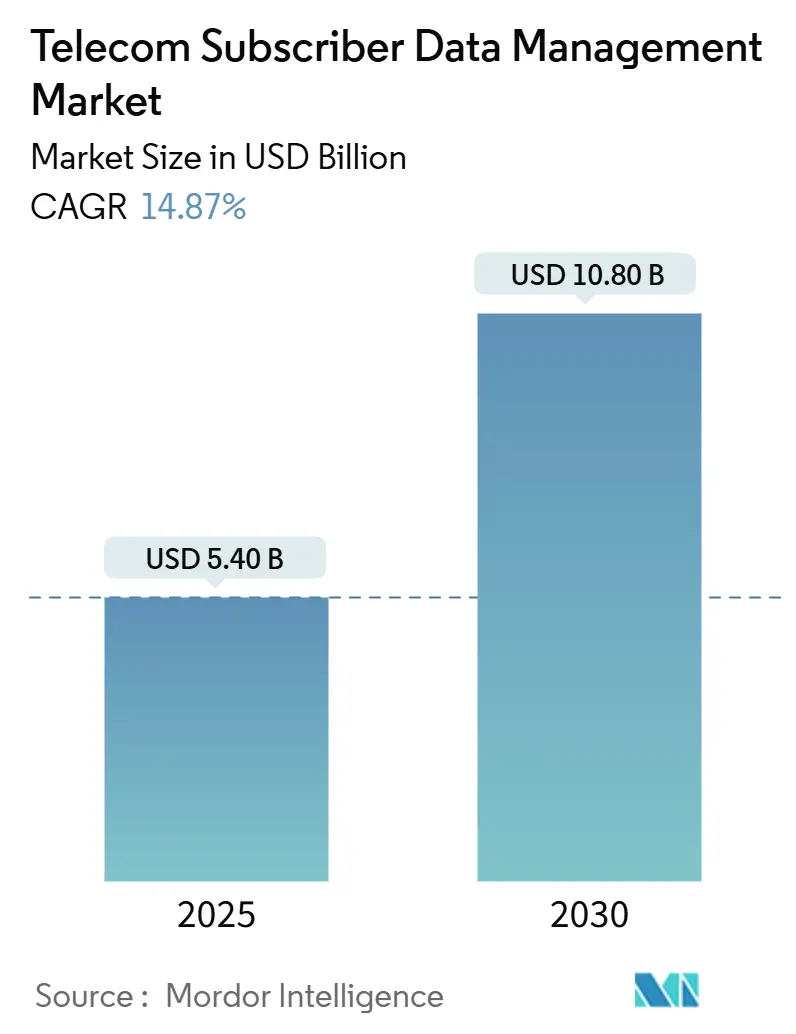

The Telecom Subscriber Data Management Market size is estimated at USD 5.40 billion in 2025, and is expected to reach USD 10.80 billion by 2030, at a CAGR of 14.87% during the forecast period (2025-2030). Operators are prioritizing unified data layers that can support billions of device identities, enable real-time policy enforcement, and facilitate authentication events. Cloud-native 5G standalone cores, network slicing, and edge computing all depend on horizontally scalable repositories that legacy HLR/HSS systems cannot support. Data-sovereignty mandates in Europe and the Asia Pacific reinforce demand for architectures that keep subscriber records within national borders while still enabling multi-cloud orchestration. Competitive intensity is heightening as vendors bundle subscriber-data functions with radio, transport, and analytics portfolios, while open-source initiatives lower entry barriers for challenger suppliers.

Key Report Takeaways

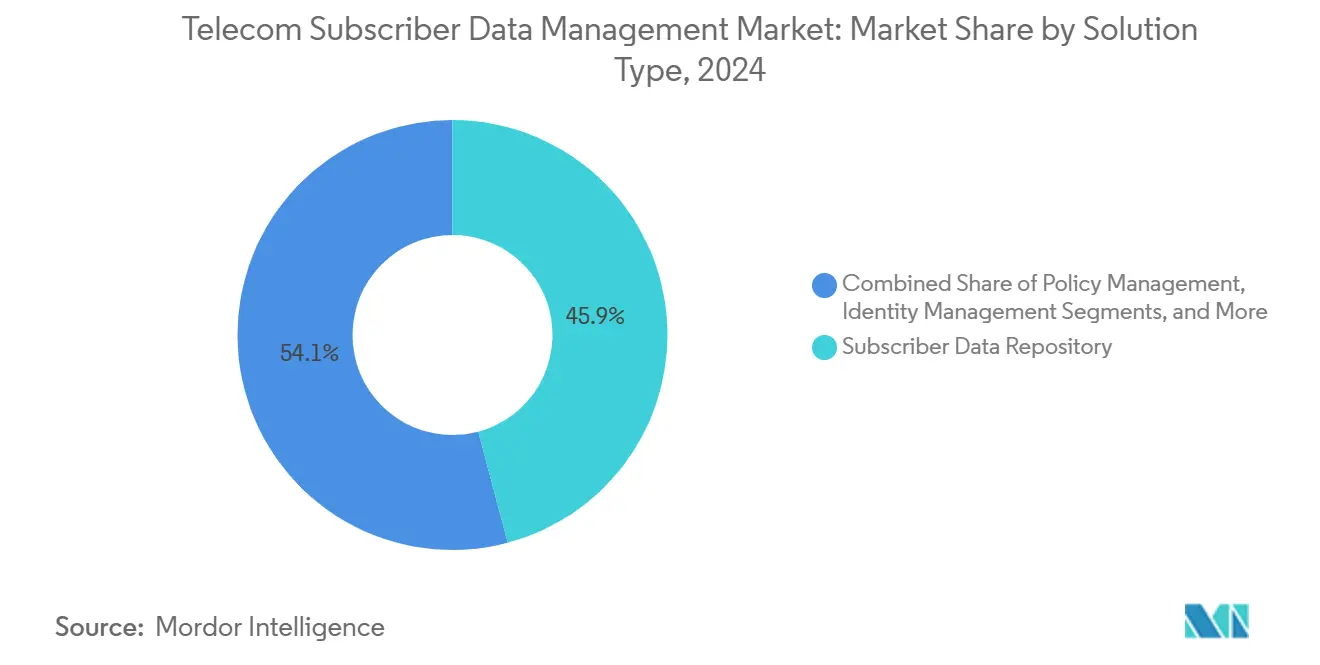

- By solution type, the subscriber data repository led with 45.87% of the Telecom Subscriber Data Management market share in 2024, while Identity Management is forecast to expand at a 15.37% CAGR through 2030.

- By deployment mode, cloud deployments accounted for 52.30% of the Telecom Subscriber Data Management market share in 2024, whereas hybrid architectures are projected to grow at a 16.77% CAGR through 2030.

- By organization size, large enterprises commanded 68.78% of the Telecom Subscriber Data Management market size in 2024; however, the SME segment is expected to grow at a 17.23% CAGR over the forecast period.

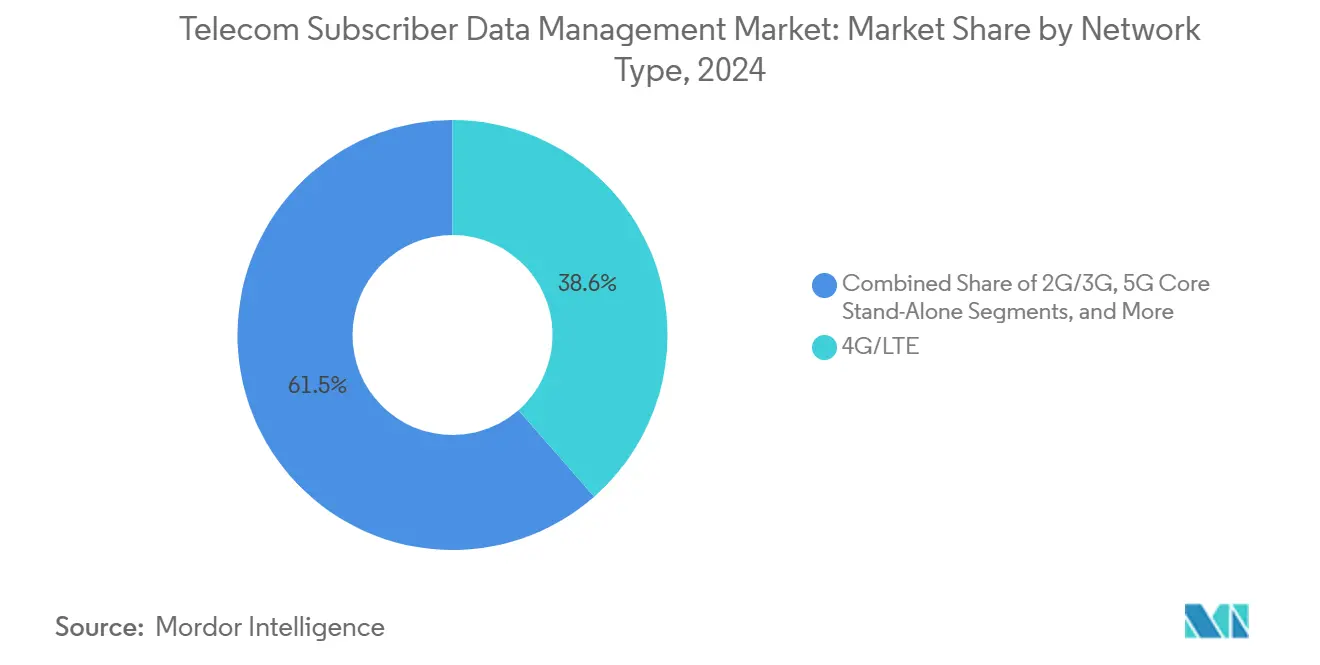

- By network type, 4G/LTE accounted for 38.55% of the Telecom Subscriber Data Management market share in 2024, while 5G core SA is expected to register an 18.72% CAGR through 2030.

- By end-user, Mobile Network Operators (MNOs) held 62.51% of the Telecom Subscriber Data Management market share in 2024; however, enterprises and IoT service providers are expected to post a 17.43% CAGR from 2024 to 2030.

- By geography, North America captured 33.60% of the Telecom Subscriber Data Management market size in 2024, whereas the Asia Pacific is expected to be the quickest-growing region at a 19.40% CAGR through 2030.

Global Telecom Subscriber Data Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid 5G Stand-Alone (SA) Core Rollouts | +3.2% | Global, with early concentration in North America, China, South Korea, and Gulf Cooperation Council markets | Medium term (2-4 years) |

| Surge in Mobile Data and Device Identities Requiring Unified Data Layers | +2.8% | Global, particularly acute in Asia Pacific and North America where IoT device counts exceed 10 billion | Long term (≥ 4 years) |

| Cloud-Native Network Functions (CNFs) Hitting Mainstream Deployments | +2.5% | North America and Europe leading, with Asia Pacific following as hyperscaler partnerships mature | Medium term (2-4 years) |

| Convergence of Fixed and Mobile Cores Among Tier-1 Operators | +1.9% | Primarily North America and Europe where incumbent telcos operate both wireline and wireless assets | Long term (≥ 4 years) |

| Edge-Enabled Personalized Slices Monetized Through SDM | +1.7% | Early adopters in Japan, South Korea, Germany, and select U.S. metro areas with enterprise 5G trials | Long term (≥ 4 years) |

| Telco-Grade AI/ML for Real-Time Subscriber Analytics | +2.1% | Global, with North America and China leading in AI infrastructure investment | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid 5G Stand-Alone (SA) Core Rollouts

T-Mobile completed its nationwide 5G SA network in 2024, triggering millisecond-level authentication requirements that can only be satisfied by modern Unified Data Repositories. [1]T-Mobile, “Nationwide 5G Standalone Coverage,” T-Mobile US, t-mobile.com China Mobile surpassed 1.5 million 5G SA base stations, necessitating UDR clusters that manage 1 billion subscribers and 10 billion IoT devices. Rakuten Mobile’s containerized UDM and UDR stack lowered the total cost of ownership by 40% compared with monolithic HSS estates. 3GPP Releases 16 and 17 formalized open interfaces, expediting deployments in markets where regulators favor vendor neutrality. Operators that delay SA migration risk forfeiting premium slicing and edge-computing revenues.

Surge in Mobile Data and Device Identities Requiring Unified Data Layers

Global mobile data traffic reached 120 exabytes per month in 2024, and cellular IoT connections topped 3 billion devices, each requiring real-time authentication and policy management. [2]Ericsson, “Ericsson Mobility Report,” Ericsson, ericsson.com Legacy HLR/HSS databases fragment subscriber context, forcing carriers to deploy multiple silos. Cloud-native repositories elastically scale to billions of records, consolidating fixed, mobile, and IoT identities while supporting fraud analytics. [3]Oracle, “Cloud Native Core,” Oracle Corporation, oracle.com eSIM profiles are forecast to exceed 6 billion by 2027, placing further strain on identity-management platforms. [4]GSMA, “eSIM Overview,” GSMA, gsma.com Unified data layers thus become pivotal for monetizing video, gaming, and augmented-reality traffic.

Cloud-Native Network Functions (CNFs) Hitting Mainstream Deployments

Containerized network functions on Kubernetes enable faster deployment of commercial workloads, reducing hardware footprints by 30%. AT&T migrated 75% of its core functions to cloud-native platforms by mid-2024, including UDM, enabling automated scaling during peak events. Dish Network’s greenfield 5G relies solely on containerized subscriber data repositories from Mavenir and AWS, demonstrating that hyperscaler partnerships can meet telco-grade reliability. DevSecOps skill shortages pose short-term hurdles, yet the long-run efficiency gains are compelling. Compliance with 3GPP service-based architecture mandates open APIs that monolithic HSS solutions cannot provide.

Convergence of Fixed and Mobile Cores Among Tier-1 Operators

Tier-1 operators, which run both wireline and wireless assets, now unify their subscriber databases to eliminate duplicate costs. Comcast’s Xfinity Mobile and Charter’s Spectrum Mobile integrate cable broadband with MVNO services, relying on a single UDR layers that serve both cable and mobile users. Telefónica’s UNICA Next spans on-premise and Google Cloud regions, allowing broadband and mobile profiles to share policy rules for seamless service bundling. Unified cores increase average revenue per user through convergent product offers while lowering operational complexity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Migration Costs from Legacy HLR/HSS to UDR | -2.3% | Global, with acute impact in Europe and North America where incumbent operators maintain extensive legacy estates | Short term (≤ 2 years) |

| Interoperability Issues Across Multi-Vendor 5G Cores | -1.8% | Global, particularly severe in markets pursuing Open RAN and best-of-breed strategies | Medium term (2-4 years) |

| Data-Sovereignty Rules Limiting Cross-Border Clouds | -1.2% | Europe, Asia Pacific (China, India, Indonesia), and Middle East with strict localization mandates | Long term (≥ 4 years) |

| Scarcity of Telco-Cloud DevSecOps Skills | -1.0% | Global, with talent concentration in North America and Western Europe exacerbating shortages elsewhere | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Migration Costs from Legacy HLR/HSS to UDR

Replacing legacy estates requires USD 50 million to USD 200 million in capital for a tier-1 operator, covering hardware, software, integration, and the cost of maintaining dual operation for several months. Telefónica allocated EUR 1.2 billion (USD 1.3 billion) for a multi-year subscriber-data migration across 17 markets. Data transfer risk is high because corrupted authentication keys could take down services nationwide. Smaller carriers often postpone projects, resulting in fragmented architectures that increase per-subscriber operating costs.

Interoperability Issues Across Multi-Vendor 5G Cores

Open RAN promises vendor freedom yet introduces integration friction. Dish Network spent months reconciling API mismatches between Mavenir’s UDM and AWS’s SMF during 2024 trials. 3GPP’s Nudr interface exists, but vendors embed proprietary performance tweaks that impair cross-compatibility in live loads. Every new software release triggers costly regression testing across all vendor combinations, delaying new-service launches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Identity Management Surges on eSIM Wave

Subscriber data repository solutions held 45.87% of the telecom subscriber data management market revenue in 2024. Identity Management is projected to be the growth engine, climbing at a 15.37% CAGR through 2030 as eSIM uptake, enterprise IoT authentication, and zero-trust security frameworks proliferate. The telecom subscriber data management market size for the identity management category is forecast to expand sharply as AAA servers and Diameter routing platforms authenticate millions of ephemeral connections.

Unified Data Management functions abstract subscriber context across legacy HLR, HSS, and cloud-native UDR sources, exposing a single API that eases incremental migration. Oracle, Cisco, and Nokia now position Diameter controllers as central signaling hubs that protect against roaming fraud while scaling past 200,000 transactions per second.

By Deployment Mode: Hybrid Gains as Latency Meets Economics

Cloud deployments controlled 52.30% of the telecom subscriber data management market share in 2024, primarily due to the hyperscaler's elasticity. Hybrid architectures will advance at a 16.77% CAGR because operators place latency-sensitive authentication on-premise while offloading analytics and billing to public clouds, achieving lower total cost without compromising ultra-reliable low-latency communications targets. The telecom subscriber data management market size for hybrid deployments is growing as carriers, such as Verizon, integrate AWS Wavelength edge nodes, meeting single-digit-millisecond thresholds for AR and industrial automation applications.

Private-cloud variants running on OpenStack or VMware also persist, especially in regions with strict data-residency rules. Orange’s Flexible Engine illustrates a model where operators host subscriber data functions in operator-controlled clouds, yet still expose APIs for enterprise private 5G clients.

By Organization Size: SMEs Accelerate via Managed Services

Large Enterprises generated 68.78% of Telecom Subscriber Data Management market revenue in 2024, largely due to tier-1 operator core revamps. Yet SMEs will grow at a 17.23% CAGR because managed-service providers bundle subscriber-data platforms with turnkey private 5G offers. The telecom subscriber data management market size for SME deployments benefits from neutral-host providers like Boldyn Networks, which remove upfront capital barriers through pay-as-you-go plans.

Government incentives under Germany’s Industry 4.0 and Japan’s Society 5.0 subsidize up to 50% of private network costs, including subscriber data management. As thousands of factories and warehouses connect robotics, sensors, and drones, scalable identity platforms that onboard devices within minutes become essential.

By Network Type: 5G SA Overtakes LTE Investment

4G/LTE remained the largest revenue contributor at 38.55% in 2024. However, 5G SA is expected to chart an 18.72% CAGR, reflecting the migration of operators to fully virtualized service-based interfaces and the decommissioning of non-standalone anchors. The telecom subscriber data management market share is shifting toward SA cores because network slicing, edge computing, and URLLC applications require real-time policy control, which legacy PCRF systems cannot provide.

Nationwide stand-alone launches in the United States and China already serve more than 300 million and 1 billion subscribers, respectively, driving UDR capacity planning into the tens of billions of records. Operators delaying the migration to standalone cores and unified data repositories risk losing access to revenue-generating features, including network slicing, edge computing, and ultra-reliable low-latency communications, which were introduced in the 3GPP Release 16 specification. Fixed-mobile convergence initiatives, such as Comcast's Xfinity Mobile and Charter's Spectrum Mobile, integrate cable broadband with MVNO services, necessitating subscriber-data platforms that unify wireline and wireless identities for seamless handoffs and consolidated billing.

By End-User: Enterprises and IoT Providers Gain Share

Mobile Network Operators accounted for 62.51% of the Telecom Subscriber Data Management market share in 2024, but Enterprises and IoT Service Providers are expected to register a 17.43% CAGR through 2030. Automotive, logistics, and smart-city projects increasingly build private 5G networks with isolated UDR clusters that guarantee sub-10-millisecond authentication. The Telecom Subscriber Data Management market size attached to enterprise deployments thus accelerates, aided by strict service-level agreements in manufacturing and healthcare.

IoT service providers, including Aeris, KORE, and Wireless Logic, deliver managed connectivity solutions for automotive telematics, smart meters, and asset tracking. These services require scalable subscriber-data platforms designed to support millions of low-power devices with intermittent connectivity. The transition from consumer-focused mobile broadband to mission-critical IoT applications has elevated subscriber data management from a back-office function to a critical, revenue-enabling platform. BMW’s Regensburg factory controls 5,000 robots and cameras using an on-premise UDR that secures every device identity, while the Port of Rotterdam manages 10,000 harbor sensors on a Nokia cloud-native UDM that supports millisecond handoffs.

Geography Analysis

North America generated 33.60% of Telecom Subscriber Data Management market revenue in 2024 on the back of Verizon, AT&T, and T-Mobile's nationwide 5G SA rollouts. The U.S. 5G Fund for Rural America unlocks USD 9 billion over a decade, prompting regional carriers to modernize subscriber databases. Canada’s Rogers and BCE spent CAD 60 billion (USD 44 billion) on 5G infrastructure, replacing legacy HSS systems with cloud-native UDM clusters to serve expansive geographic coverage. Mexico’s América Móvil initiated its migration to 5G SA in 2024 with Ericsson’s UDM for 80 million Telcel subscribers.

The Asia Pacific will be the fastest-growing region, with a 19.40% CAGR through 2030, driven by China Mobile’s billion-subscriber core, Reliance Jio’s cloud-native build in India, and Rakuten Mobile’s Kubernetes-based network in Japan. South Korea’s SK Telecom offers enterprise slices for autonomous vehicles that require real-time subscriber policy checks, while Australian operators are retrofitting their subscriber data stacks for eSIM and IoT authentication in mining and agriculture.

Europe enforces GDPR-compliant data residency, compelling operators like Deutsche Telekom to replicate subscriber records within every jurisdiction, thereby driving the adoption of on-premise and hybrid solutions. Middle East carriers follow sovereign-cloud mandates, investing USD 12 billion in 2024 to ensure national data remains local, thereby favoring private or hybrid clouds. Latin America and Africa are at earlier stages; yet, Brazil’s early 5G SA deployments and MTN Group’s trials in South Africa point to a future modernization.

Competitive Landscape

Global revenue concentration is moderate as Nokia, Ericsson, and Huawei collectively hold about 55% of the Telecom Subscriber Data Management market share through integrated 5G deals that bundle UDR, UDM, and PCF with radio and transport portfolios. Oracle and Cisco pursue best-of-breed overlays aimed at brownfield operators desiring multi-vendor cores. Challenger vendors such as Mavenir, Parallel Wireless, and IPLOOK leverage open-source blueprints from the Linux Foundation’s Magma project to ship lightweight, containerized subscriber-data functions that operate on commodity hardware, often at lower price points.

Strategic divergence is evident. Incumbents continue to pursue vertical integration, layering AI-driven analytics, such as Nokia’s AVA platform, on top of proprietary data stores to lock in customers. Challengers instead position horizontal, API-centric UDR modules that integrate with any vendor’s session-management or policy-control functions, appealing to operators that fear vendor lock-in. Huawei leads UDM-related filings, while Oracle and Cisco emphasize policy-management intellectual property.

Enterprise and private 5G demand creates a white-space opportunity for turnkey solutions that combine identity management, security, and lifecycle services. Dish Network’s selection of Mavenir over traditional suppliers in its U.S. build highlights a willingness among greenfield operators to forego legacy vendors in favor of cloud economics and agility.

Telecom Subscriber Data Management Industry Leaders

Nokia Oyj

Telefonaktiebolaget LM Ericsson (Ericsson)

Huawei Technologies Co., Ltd.

Oracle Corporation

Cisco Systems, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Huawei unveiled an AI Core Network that embeds autonomous generative capabilities for self-optimization and self-maintenance.

- December 2024: Ericsson secured a USD 500 million multi-year contract with Bharti Airtel to deploy cloud-native 5G cores, including Unified Data Management and Policy Control Functions, across India.

- May 2024: Mavenir received a USD 300 million investment from Koch Strategic Platforms to accelerate cloud-native subscriber-data and Open RAN development.

Global Telecom Subscriber Data Management Market Report Scope

The Telecom Subscriber Data Management Market Report is Segmented by Solution Type (Subscriber Data Repository [Home Subscriber Server (HLR/HSS), Unified Data Repository (UDR), Unified Data Management (UDM/UDSF)], Policy Management [Policy and Charging Rules Function (PCRF – 4G), Policy Control Function (PCF – 5G)], Identity Management [AAA and Diameter Routing, eSIM / Digital Identity Management], Location and Device Information), Deployment Mode (Cloud [Public Cloud, Private Cloud], On-Premise, Hybrid), Organization Size (Large Enterprises, Small and Medium Enterprises [SMEs]), Network Type (2G/3G, 4G/LTE, 5G Core Stand-Alone, Fixed/Wireline), End-user (Mobile Network Operators (MNOs), Mobile Virtual Network Operators (MVNOs), Enterprises / IoT Service Providers), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Subscriber Data Repository | Home Subscriber Server (HLR/HSS) |

| Unified Data Repository (UDR) | |

| Unified Data Management (UDM/UDSF) | |

| Policy Management | Policy and Charging Rules Function (PCRF – 4G) |

| Policy Control Function (PCF – 5G) | |

| Identity Management | AAA and Diameter Routing |

| eSIM / Digital Identity Management | |

| Location and Device Information |

| Cloud | Public Cloud |

| Private Cloud | |

| On-Premise | |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| 2G/3G |

| 4G/LTE |

| 5G Core Stand-Alone |

| Fixed/Wireline |

| Mobile Network Operators (MNOs) |

| Mobile Virtual Network Operators (MVNOs) |

| Enterprises / IoT Service Providers |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Singapore | |

| Malaysia | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Middle East |

| Africa |

| By Solution Type | Subscriber Data Repository | Home Subscriber Server (HLR/HSS) |

| Unified Data Repository (UDR) | ||

| Unified Data Management (UDM/UDSF) | ||

| Policy Management | Policy and Charging Rules Function (PCRF – 4G) | |

| Policy Control Function (PCF – 5G) | ||

| Identity Management | AAA and Diameter Routing | |

| eSIM / Digital Identity Management | ||

| Location and Device Information | ||

| By Deployment Mode | Cloud | Public Cloud |

| Private Cloud | ||

| On-Premise | ||

| Hybrid | ||

| By Organization Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

| By Network Type | 2G/3G | |

| 4G/LTE | ||

| 5G Core Stand-Alone | ||

| Fixed/Wireline | ||

| By End-user | Mobile Network Operators (MNOs) | |

| Mobile Virtual Network Operators (MVNOs) | ||

| Enterprises / IoT Service Providers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Singapore | ||

| Malaysia | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | |

| Africa | ||

Key Questions Answered in the Report

What is the projected value of the Telecom Subscriber Data Management market in 2030?

The market is forecast to reach USD 10.8 billion by 2030, growing at a 14.87% CAGR.

Which solution segment grows the fastest?

Identity Management is expected to post a 15.37% CAGR through 2030, driven by eSIM and IoT authentication needs.

Why are hybrid deployments gaining traction?

Hybrid models combine on-premise latency benefits with public-cloud economics, pushing their 16.77% CAGR forecast.

Which region expands most rapidly?

Asia Pacific is projected to lead with a 19.40% CAGR, reflecting large-scale 5G SA rollouts in China, India, and Japan.

How will enterprise demand influence vendor strategies?

Enterprises and IoT providers growing at 17.43% CAGR spur vendors to deliver turnkey, API-centric subscriber-data platforms.

Page last updated on: