Telecom Identity And Authentication Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

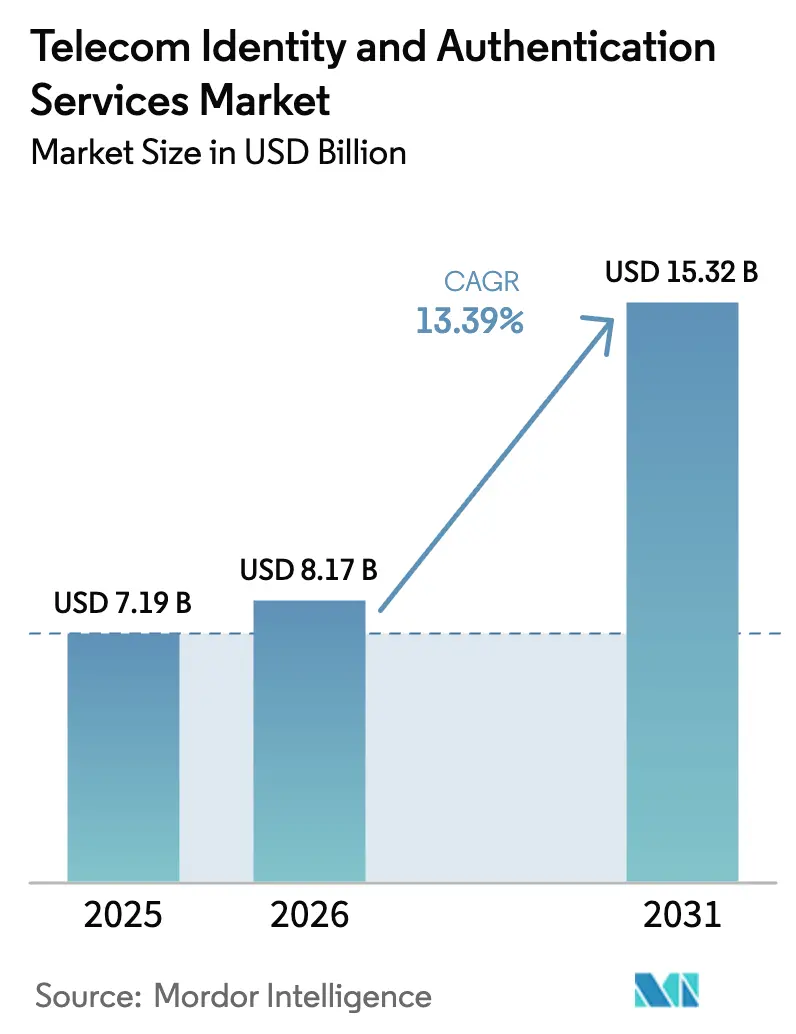

| Market Size (2026) | USD 8.17 Billion |

| Market Size (2031) | USD 15.32 Billion |

| Growth Rate (2026 - 2031) | 13.39% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Telecom Identity And Authentication Services Market Analysis by Mordor Intelligence

The Telecom Identity and Authentication Services Market size is projected to be USD 7.19 billion in 2025, USD 8.17 billion in 2026, and reach USD 15.32 billion by 2031, growing at a CAGR of 13.39% from 2026 to 2031. Strong demand for network-level verification, escalating SIM-swap fraud, and monetization pressure on mobile network operators (MNOs) are expanding the addressable base of enterprises that now treat programmable telecom credentials as a core security control. Solutions captured a significant share of revenue in 2025, though managed services are scaling faster because banks, retailers, and fintechs prefer turnkey integrations that bundle regulatory compliance and real-time fraud intelligence. Cloud deployments dominate because authentication workloads spike during peak payment windows and benefit from elastic scaling. Geographically, North America remains the largest revenue contributor, while Asia-Pacific is the fastest-growing region, driven by government digital-identity schemes that use carrier APIs. Competitive intensity is moderate: messaging aggregators such as Twilio, Sinch, and Infobip compete with specialist identity platforms such as Prove and Trulioo, while hardware security vendors, including Thales and IDEMIA, leverage secure-element expertise to launch embedded authentication offerings.

Key Report Takeaways

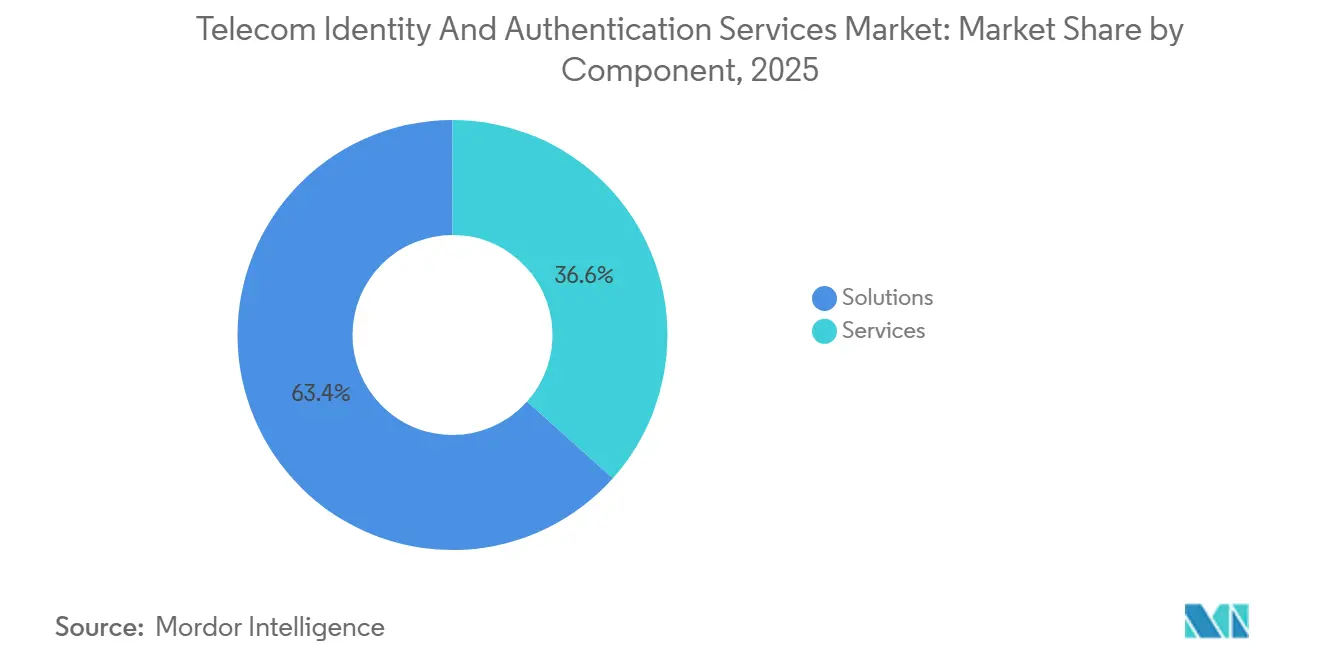

- By component, solutions led with 63.40% of the Telecom identity and authentication services market share in 2025, whereas services are projected to record the highest CAGR at 15.40% through 2031.

- By deployment mode, cloud accounted for 68.81% of the Telecom identity and authentication services market size in 2025 and is advancing at a 15.11% CAGR to 2031.

- By authentication type, SMS-based OTP held a 38.20% share of the Telecom identity and authentication services market in 2025, while API-based digital identity verification is forecast to expand at a 16.40% CAGR to 2031.

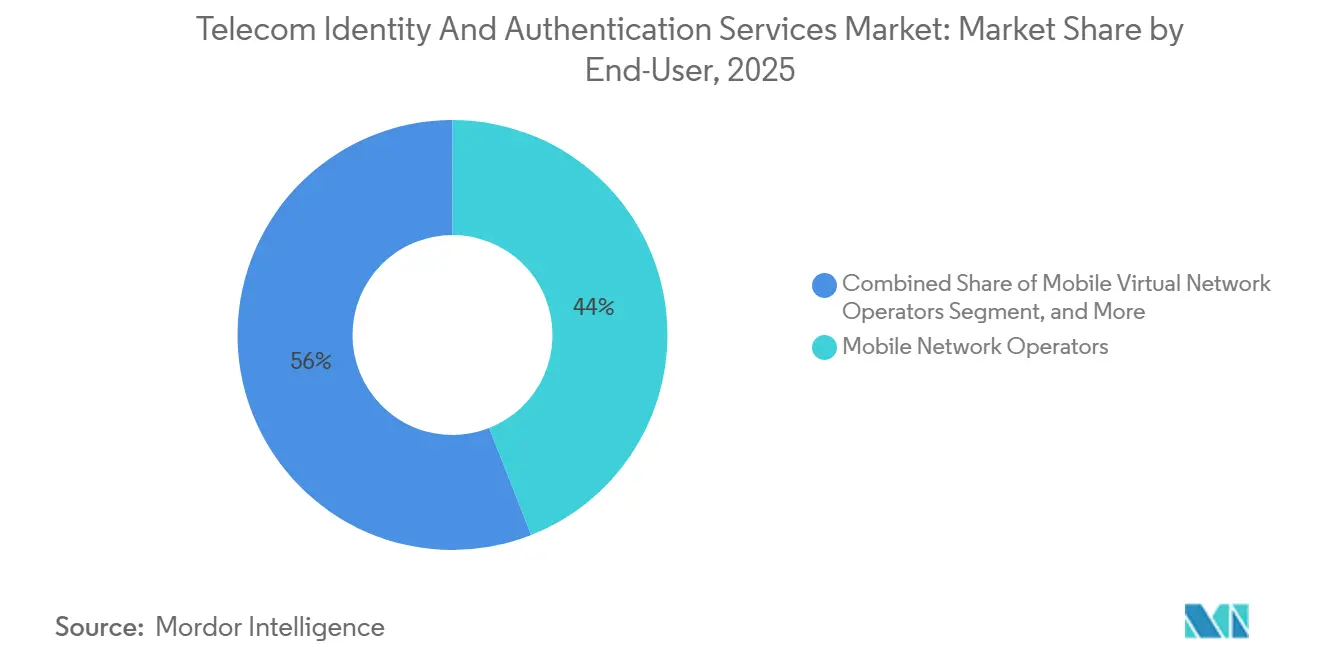

- By end user, MNOs captured 44.03% of revenue in 2025; however, enterprises are projected to post the fastest CAGR of 16.81% through 2031.

- By industry vertical, financial services led with 31.23% revenue share in 2025, and e-commerce and retail are poised to rise at a 17.04% CAGR through 2031.

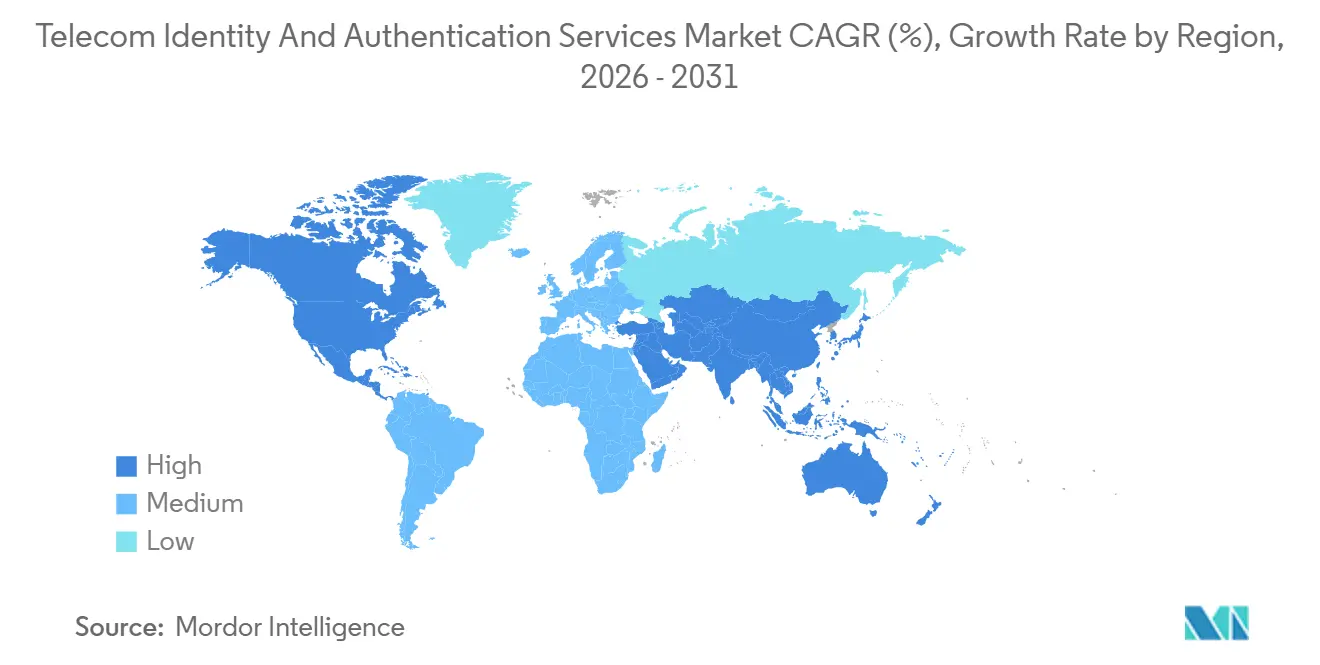

- By geography, North America contributed 36.22% revenue in 2025, whereas Asia-Pacific is set to register the fastest regional CAGR at 16.72% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Telecom Identity And Authentication Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Mobile Network Operator Digital Identity APIs | +2.8% | Europe and Asia-Pacific | Medium term (2-4 years) |

| Surge in SIM Swap and Account Takeover Fraud | +3.2% | North America and Europe | Short term (≤ 2 years) |

| Regulatory Mandates for Strong Customer Authentication | +2.5% | Europe, North America, Asia-Pacific | Medium term (2-4 years) |

| Rise of eSIM and IoT Device Authentication | +1.9% | Global, led by Asia-Pacific and North America | Long term (≥ 4 years) |

| Telco Adoption of Decentralized Identifier Frameworks | +1.4% | Europe and North America | Long term (≥ 4 years) |

| Monetization Pressure Leading to Identity-As-A-Service Offerings | +2.1% | Mature markets worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of MNO Digital-Identity APIs

MNOs are transforming subscriber data into programmable identity primitives. GSMA’s Mobile Connect reached 47 deployments across 31 countries by the end of 2025, giving enterprises a single contract for SIM-swap checks, device binding, and silent verification. Vodafone’s TrustHub, launched in February 2025, exposes RESTful APIs with 99.99% uptime SLAs, lowering integration friction for banks that must satisfy real-time fraud controls. Telefónica integrated the same capabilities into Azure Active Directory in June 2025, signaling that carrier authentication is becoming a cloud infrastructure feature rather than a siloed telecom service. Competition now centers on latency, fraud-signal breadth, and commercial transparency rather than mere connectivity. Over 2026-2027, additional European and Latin-American operators will federate APIs, further standardizing implementation and expanding geographic coverage.

Surge in SIM-Swap and Account-Takeover Fraud

SIM-swap incidents grew 48% in 2025, generating global losses above USD 2.7 billion, according to the FBI Internet Crime Report issued in March 2026.[1]FBI, “2025 Internet Crime Report,” March 2026, ic3.gov Attackers exploit social-engineering gaps at retail outlets to port numbers and intercept one-time codes, bypassing two-factor authentication. The U.S. FCC responded in November 2025 with rules that force carriers to apply multi-factor verification before processing SIM changes. T-Mobile rolled out Account Takeover Protection in January 2026, automatically pausing authentication for 24 hours after a SIM change to deter fraud. Cyber-insurers now require carrier-grade verification as a prerequisite for coverage, pushing enterprises to retire vulnerable SMS OTP flows in favor of silent network checks that validate SIM tenure, device fingerprinting, and recent porting events.

Regulatory Mandates for Strong Customer Authentication

Europe’s revised Payment Services Directive obligates strong customer authentication that combines at least two independent factors. The European Banking Authority clarified in April 2025 that SMS OTP alone is insufficient if the passcode reaches the initiating device, accelerating the pivot toward carrier verification that proves genuine possession.[2]European Banking Authority, “EBA Clarifies Strong Customer Authentication Requirements for Mobile Payments,” April 2025, eba.europa.eu India’s Reserve Bank followed up with digital lending rules in September 2025, requiring multi-factor verification before disbursement; the circular recognizes telecom-based proof of SIM ownership as compliant. Brazil’s Central Bank imposed similar checks for Pix instant payments in December 2025, compelling banks to hit carrier APIs for number ownership before lifting transaction ceilings. Collectively, these mandates convert authentication from optional risk control into obligatory compliance spending.

Rise of eSIM and IoT Device Authentication

eSIM connections surpassed 1.2 billion in 2025, erasing the physical SIM card as the classic possession token and forcing operators to issue cryptographic certificates that attest to device identity. Apple’s eSIM-only iPhone range, extended to 14 more countries in 2025, means carriers must migrate their validation logic from ICCID to device certificate checks. GSMA’s SGP.22 specification introduces operator-signed tokens, but roaming interoperability remains patchy when devices hop to foreign networks. On the IoT front, Vodafone trimmed handshake payloads from 4.2 KB to 380 bytes for NB-IoT modules in May 2025, prolonging battery life while upholding security guarantees. Over the long term, lightweight attestation will underpin billions of connected meters, vehicles, and sensors that cannot afford compute-intensive TLS exchanges.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Privacy Concerns Over Centralized Subscriber Data Repositories | –1.8% | Europe and North America | Short term (≤ 2 years) |

| Limited Awareness Among MVNOs and SMEs | –0.9% | Emerging markets worldwide | Medium term (2-4 years) |

| Complex Revenue-Sharing Models Between MNOs and Identity Aggregators | –1.3% | Global | Medium term (2-4 years) |

| Fragmented International KYC Standards | –1.1% | Cross-border finance sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Privacy Concerns Over Centralized Subscriber Data Repositories

The European Data Protection Board ruled in March 2025 that operators offering identity services are full data controllers, triggering GDPR duties such as data-protection impact assessments and breach notification within 72 hours.[3]European Data Protection Board, “Guidance on Telecom Operators as Identity Service Providers,” March 2025, edpb.europa.eu ETNO estimates that compliance overhead lifted operating costs by 22% for small carriers, discouraging some from launching identity APIs. Advocacy groups warn that a single breach could expose millions of subscriber records, enabling mass surveillance or fraud. Consequently, regulators push for tokenized confirmations that prove SIM possession without persisting personal identifiers, a design shift likely to slow platform rollouts in Europe and privacy-sensitive U.S. states through 2027.

Complex Revenue-Sharing Models Between MNOs and Identity Aggregators

Aggregators that broker access to multiple carrier APIs keep 30%-45% of enterprise spend, squeezing operator margins despite heavy investment in secure gateways and fraud analytics. Disagreements over fee splits delayed several European launches in 2025 as carriers pushed for higher shares, whereas aggregators argued their compliance expertise justifies current economics. The European Commission’s draft Digital Identity Wallet proposes regulated pricing caps, adding predictability but also limiting upside for MNOs. Divergent commercial terms mean enterprises still negotiate operator-by-operator, raising integration costs and elongating sales cycles, particularly for mid-market businesses with limited procurement bandwidth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Outpace Solutions Growth

Solutions accounted for only 63.40% of the Telecom identity and authentication services market revenue in 2025, yet the services segment is forecast to grow at a 15.40% CAGR and surpass Solutions by 2031. Enterprises choose managed authentication to avoid capital expenditure, obtain instant geographic reach across hundreds of operators, and outsource regulatory change management. Twilio’s USD 3.2 billion acquisition of Segment in 2025 bundled customer-data orchestration with number-based verification, illustrating the premium placed on integrated stacks that convert behavioral insights into adaptive authentication challenges.

Solutions remain essential for highly regulated verticals that cannot rely on multi-tenant clouds. Banks migrating mainframe applications or hospitals subject to data-sovereignty statutes deploy on-premises engines with direct SS7 access and dedicated hardware security modules. Even here, a subscription mindset is emerging: license agreements increasingly include continuous rule-set updates and 24/7 fraud-intelligence feeds, blurring the line between perpetual software and managed service. Consequently, vendors are refining hybrid models that deliver cloud analytics while processing sensitive payloads locally, preserving compliance without conceding scalability.

By Deployment Mode: Cloud Dominance Accelerates

Cloud deployments commanded 68.81% of the Telecom identity and authentication services market share in 2025 and will sustain double-digit growth at a 15.11% CAGR by 2031, as latency, elastic scaling, and geographic redundancy are non-negotiable for real-time payments. Sinch trimmed the average API response time from 340 ms to 180 ms after expanding its footprint to 18 additional AWS regions, delivering a measurable uplift in checkout conversion rates.

On-premise adoption shrinks each year but resists extinction in countries where national rules restrict cross-border data transfers. Defense agencies, critical-infrastructure operators, and sovereign cloud mandates in markets such as Germany and the United Arab Emirates keep a rump demand alive. Hybrid postures are popular: enterprises run decision engines behind corporate firewalls yet call cloud endpoints for SIM-swap checks, leveraging cached results to minimize external data transfer while sustaining sub-second user experiences.

By Authentication Type: API-Based Verification Disrupts OTP Dominance

SMS-based OTP still accounts for 38.20% of revenue, owing to universal handset support and zero onboarding friction. However, the digital identity verification API is expected to grow at a CAGR of 16.40% through 2031, as regulators deem OTPs insufficient for high-value transactions. Telesign’s January 2026 launch of its Silent Verification API cut average user step time from 18 seconds to 2 seconds, boosting conversion rates for ecommerce checkouts during flash-sale peaks.

Biometrics and hardware tokens occupy distinct niches. Face or fingerprint unlock is gaining favor in media-streaming apps, while FIDO-certified tokens are entrenched for privileged access to cloud infrastructure. Digital identity APIs synthesize multiple signals, SIM tenure, device fingerprint, and behavioral analytics into a composite risk score, pushing the market toward invisible, continuous authentication rather than discrete checkpoint challenges.

By End-User: Enterprises Challenge MNO Dominance

MNOs generated 44.03% of end-user revenue in 2025, tapping identity internally and as a wholesale product. Yet enterprises, from neobanks to online gaming platforms, are expected to overtake by 2031 with a CAGR of 16.81% as they assemble best-of-breed stacks that avoid single-carrier dependency. Microsoft’s 2025 integration of Telefónica APIs into Azure Active Directory enabled corporate accounts to demand SIM possession before opening sensitive SaaS dashboards, disintermediating traditional aggregators.

Mobile virtual network operators (MVNOs) and over-the-top (OTT) service providers form smaller but strategic cohorts. With no radio assets, they aggregate carrier APIs and focus on user-experience differentiation. Enterprise growth is further propelled by cyber-insurance clauses that shift breach liability to service providers that fail to deploy carrier-grade verification. This structural shift converts authentication from a cost center into a board-level risk-mitigation priority.

By Industry Vertical: Ecommerce Fraud Drives Retail Adoption

Financial Services led with a 31.23% revenue share in 2025 because payment regulations impose monetary penalties for weak authentication. Ecommerce and Retail segment is expected to drive growth at a 17.04% CAGR through 2031. Historically tolerant of password resets and simple OTP, now chase stronger methods as account-takeover fraud spikes during peak sales periods. U.S. retailers lost USD 9.1 billion to credential abuse in 2025, prompting platforms such as Shopify to pilot silent-verification plugins that curb cart abandonment without user-visible friction.

Government usage is scaling through digital wallet programs, EU eIDAS 2.0, and India’s Aadhaar-linked SIM binding, but remains fragmented by sovereign standards. Healthcare faces twin imperatives: remote-patient verification and HIPAA compliance, leading to hybrid flows that pair network checks with biometric face-matching. Media and Entertainment adopts telecom authentication to deter credential sharing as subscription growth slows, aligning security needs with revenue-protection goals.

Geography Analysis

North America contributed 36.22% of the Telecom identity and authentication services market revenue in 2025, anchored by early adoption of MFA mandates in banking and healthcare and supported by direct carrier aggregation that enables sub-second API calls across the United States and Canada. Widespread 5G rollout improves signal quality for silent verification, while cyber-insurance prerequisites compel enterprises to sunset legacy SMS OTP.

Europe’s growth is steadier but shaped by stringent privacy laws. The region benefits from harmonized PSD2 directives, yet implementation varies by country, adding complexity for cross-border ecommerce. Joint ventures such as the Orange and Deutsche Telekom European Identity Platform, announced in October 2025, aim to deliver a continent-wide wallet-compatible service that meets eIDAS 2.0 requirements, but the full rollout depends on member-state alignment.

Asia-Pacific, expanding at 16.72% CAGR, is propelled by India’s SIM binding requirement for high-value UPI transactions and Indonesia’s national digital ID that embeds telecom checks at onboarding. Chinese OEM dominance in the handset market is accelerating eSIM adoption, compelling carriers to rewrite their authentication logic for certificate-based validation. Meanwhile, emerging markets in Southeast Asia leapfrog straight to carrier APIs for KYC-lite onboarding of gig-economy workers, bypassing paper ID processes.

Competitive Landscape

The market is moderately concentrated, with the top 10 vendors accounting for more than 50% in 2025. Messaging aggregators (Twilio, Sinch, Infobip, Telesign) leverage global SMS reach to upsell silent verification and SIM-swap intelligence. Specialist identity platforms (Prove, Trulioo, 1Kosmos) differentiate via proprietary risk-scoring algorithms sourced from telecom and behavioral data. Hardware security majors (Thales, IDEMIA, Giesecke and Devrient) embed secure elements and eSIM profiles, offering end-to-end identity solutions from chip to cloud.

Strategic moves underscore platform convergence. Thales bought Prove Identity for USD 890 million in January 2026, marrying secure-element supply with an API layer that enterprises consume on demand. Sinch’s November 2025 purchase of Inteliquent gave it direct North-American voice and messaging trunks, improving delivery KPIs for time-sensitive verification codes. Telefónica aggregated 350 million subscribers under one Global Identity Platform in December 2025, pricing by transaction rather than per-country contracts to simplify enterprise adoption.

Technology roadmaps emphasize invisible, risk-based flows. Patent filings such as US11234567B2, granted to Prove in September 2025, detect SIM swaps in real time by correlating radio events with subscriber-record anomalies. Vendors invest heavily in machine-learning models that dissect telemetry from billions of authentication events, raising entry barriers for new challengers and locking in customers through continuously improving fraud-signal accuracy.

Telecom Identity And Authentication Services Industry Leaders

Boku Inc.

Infobip D.O.O.

Telesign Corporation

Sinch AB

Twilio Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Ooredoo Group has partnered with Aduna, a global network API aggregator, to offer its telecom API portfolio to businesses across the Middle East, North Africa, and beyond. This enables banks, fintech firms, e-commerce platforms, and digital service providers to integrate services like identity verification, SIM swaps, KYC, payments, and communications via standardized APIs, eliminating the need for local integrations or country-specific agreements.

- October 2025: IDEMIA Public Security North America has partnered with SLC Digital to integrate hardware-rooted digital identity into financial networks, telecom ecosystems, and regulated platforms. This collaboration combines IDEMIA’s identity proofing solutions with SLC’s SIM/eSIM-based Hardware Root of Trust (RoT) technology to deliver tamper-proof identity validation and secure communication channels.

Global Telecom Identity And Authentication Services Market Report Scope

The Telecom Identity and Authentication Services Market Report is Segmented by Component (Solutions, Services), Deployment Mode (On-premise, Cloud), Authentication Type (SMS-Based OTP, Mobile Biometrics, Multi-Factor Authentication Token, Digital Identity Verification API), End-User (Mobile Network Operators, Mobile Virtual Network Operators, Over-The-Top Service Providers, Enterprises), Industry Vertical (Financial Services, Ecommerce and Retail, Government and Public Sector, Healthcare, Media and Entertainment), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Solutions |

| Services |

| On-Premise |

| Cloud |

| SMS-Based OTP |

| Mobile Biometrics |

| Multi-Factor Authentication Token |

| Digital Identity Verification API |

| Mobile Network Operators |

| Mobile Virtual Network Operators |

| Over-The-Top Service Providers |

| Enterprises |

| Financial Services |

| Ecommerce and Retail |

| Government and Public Sector |

| Healthcare |

| Media and Entertainment |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of the Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Solutions | ||

| Services | |||

| By Deployment Mode | On-Premise | ||

| Cloud | |||

| By Authentication Type | SMS-Based OTP | ||

| Mobile Biometrics | |||

| Multi-Factor Authentication Token | |||

| Digital Identity Verification API | |||

| By End-User | Mobile Network Operators | ||

| Mobile Virtual Network Operators | |||

| Over-The-Top Service Providers | |||

| Enterprises | |||

| By Industry Vertical | Financial Services | ||

| Ecommerce and Retail | |||

| Government and Public Sector | |||

| Healthcare | |||

| Media and Entertainment | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of the Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the forecast value of the Telecom identity and authentication services market in 2031?

The market is projected to reach USD 15.32 billion by 2031, expanding at a 13.39% CAGR from 2026-2031.

Which authentication method is growing the fastest?

API-based digital identity verification is forecast to post a 16.40% CAGR to 2031 as enterprises replace SMS OTP.

Why are enterprises adopting managed services rather than in-house solutions?

Managed offerings bundle carrier integrations, fraud analytics, and compliance updates, sparing enterprises capital expenditure and specialized staffing.

Which region will see the highest growth?

Asia-Pacific is expected to record a 16.72% CAGR through 2031, propelled by government digital-identity programs and SIM-binding mandates.

How are regulatory mandates influencing adoption?

Rules such as Europe’s PSD2 and India’s digital-lending guidelines require strong customer authentication, making network-level verification a compliance imperative.

What role do eSIM and IoT play in future demand?

The shift to eSIM and the explosion of IoT connections necessitate lightweight, certificate-based authentication, opening new revenue streams for telecom identity APIs.

Page last updated on: