Telecom Edge Infrastructure Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

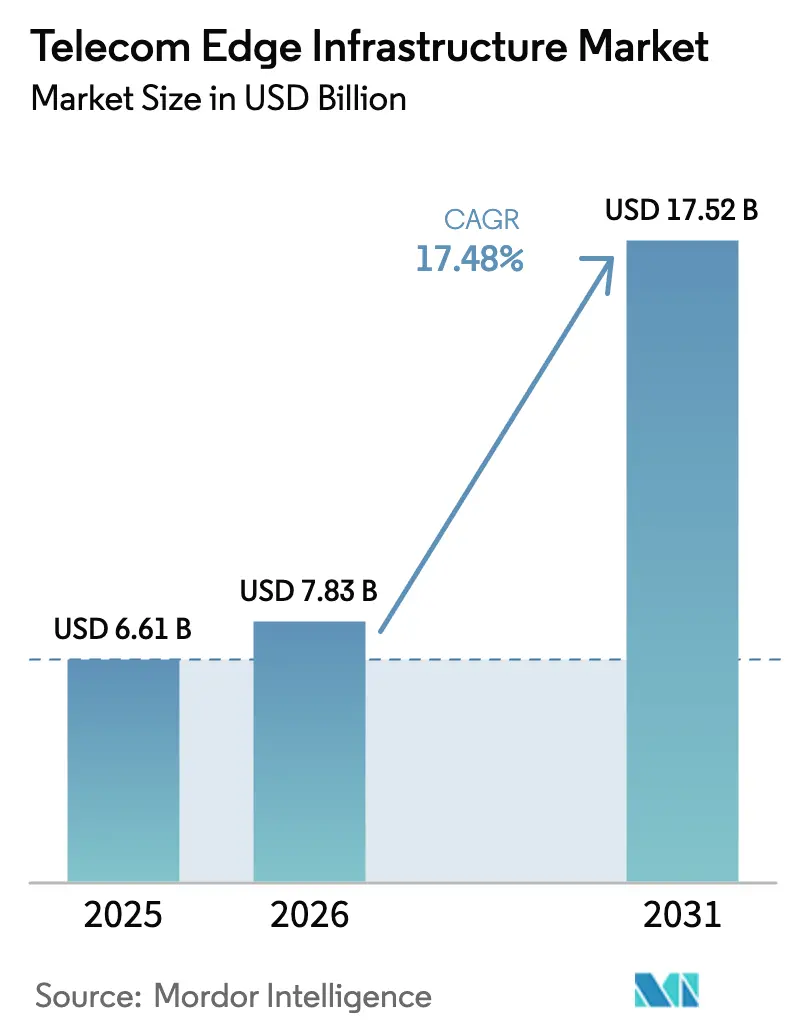

| Market Size (2026) | USD 7.83 Billion |

| Market Size (2031) | USD 17.52 Billion |

| Growth Rate (2026 - 2031) | 17.48% CAGR |

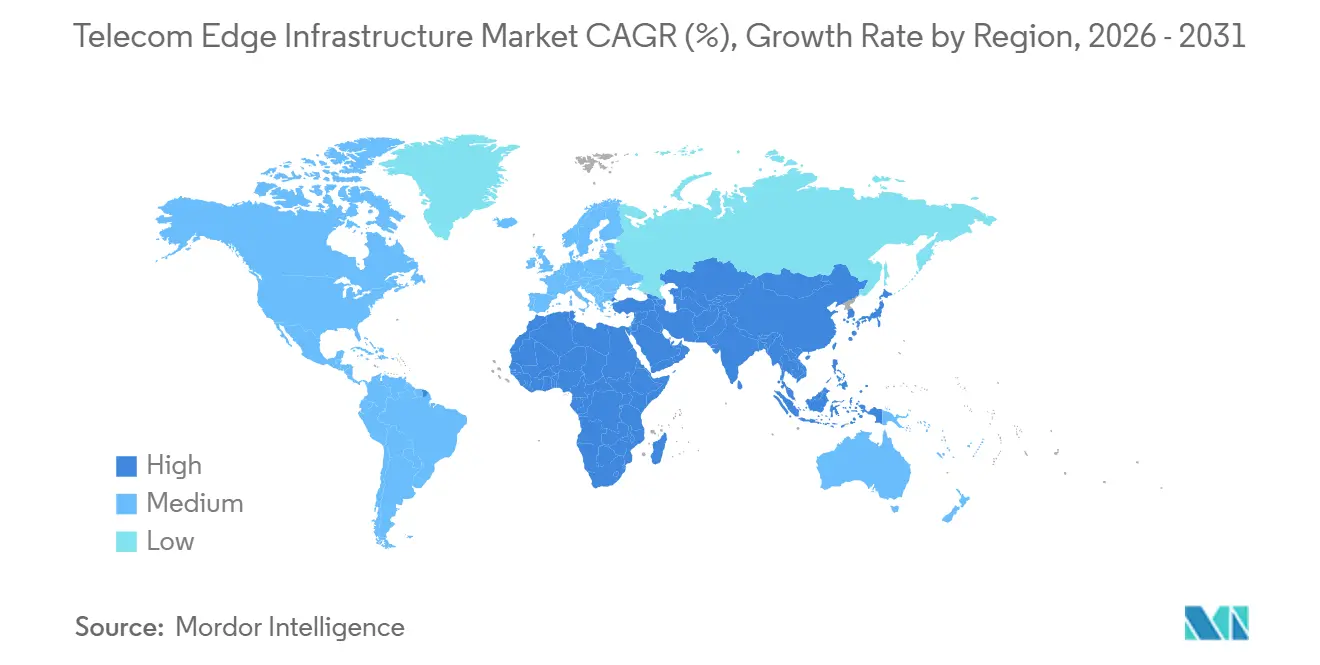

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

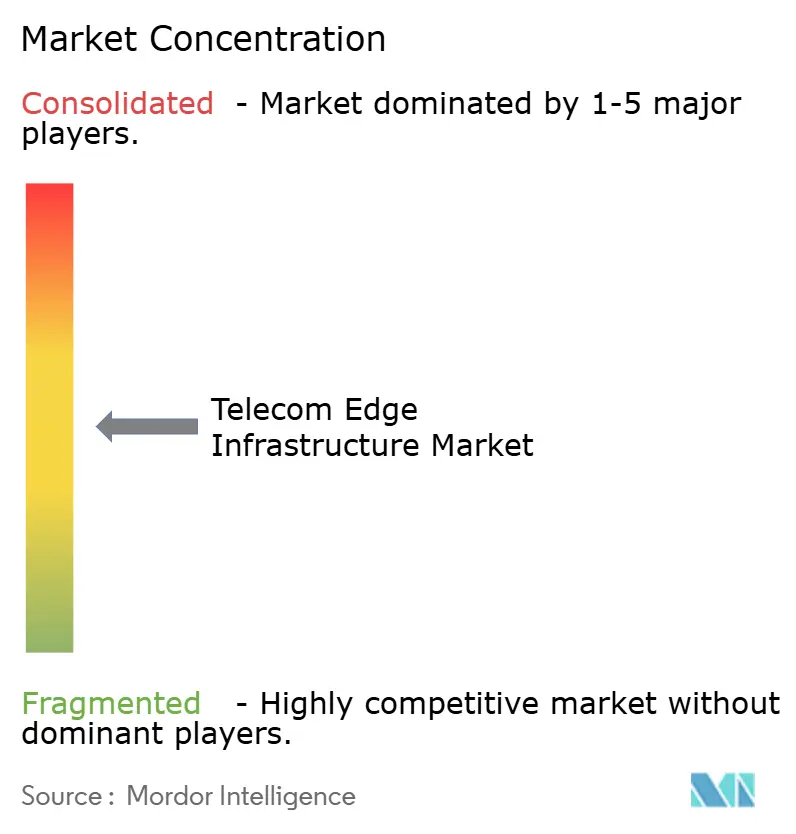

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Telecom Edge Infrastructure Market Analysis by Mordor Intelligence

The Telecom Edge Infrastructure Market size is expected to grow from USD 6.61 billion in 2025 to USD 7.83 billion in 2026 and is forecast to reach USD 17.52 billion by 2031 at 17.48% CAGR over 2026-2031. Rising traffic from 5G devices, tighter latency targets for factory automation, and tier-1 operator capital re-allocation toward micro-edge nodes underpin this acceleration. Hardware still dominates spending, yet software-defined network functions and orchestration platforms are capturing incremental value as carriers shift from purpose-built appliances to cloud-native workloads. Hyperscale cloud providers are embedding compute at cell-site distances, giving enterprises quick access to sub-10 millisecond round-trip latency and tilting the balance of power away from traditional equipment vendors. Regulatory deadlines for gigabit connectivity and data residency add urgency, while energy-saving RAN controllers improve total cost of ownership and reinforce the business case for distributed deployments.

Key Report Takeaways

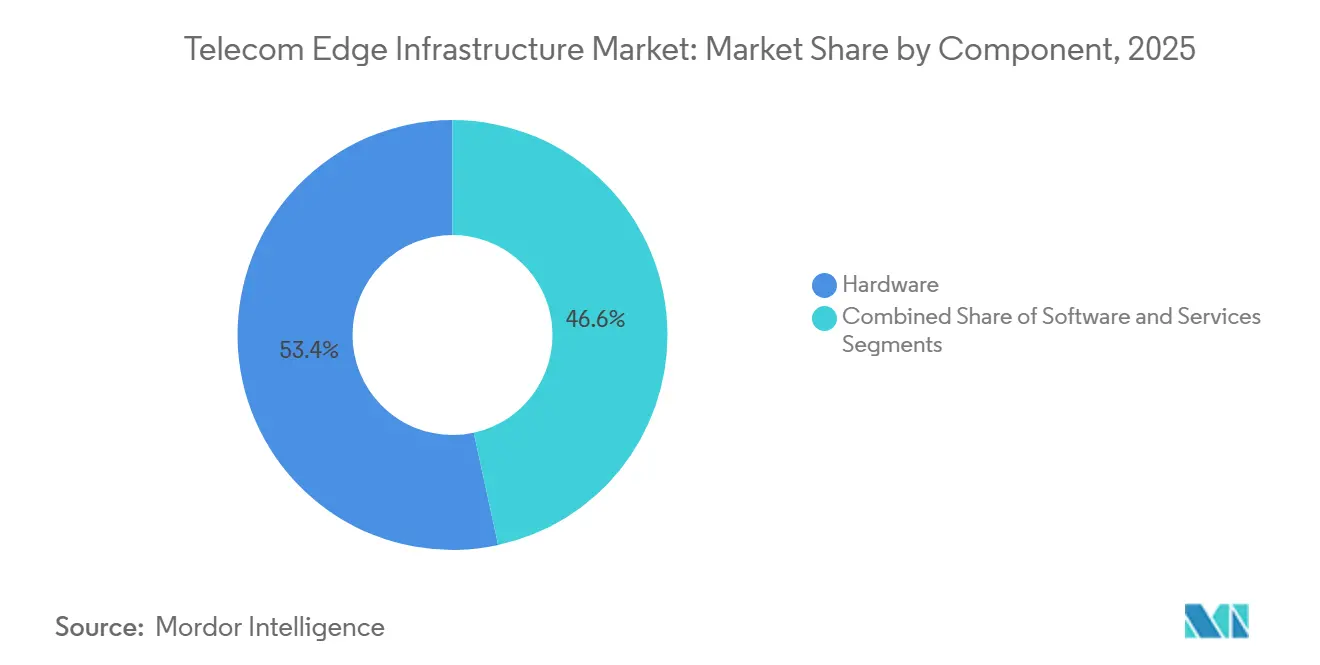

- By component, Hardware led with 53.41% revenue share in 2025, whereas Software is projected to grow at 20.88% CAGR through 2031.

- By edge location, Macro / Micro Cell Sites led with 33.24% revenue share of the telecom edge infrastructure market in 2025, whereas Enterprise On-prem Edge is projected to grow at 22.02% CAGR through 2031.

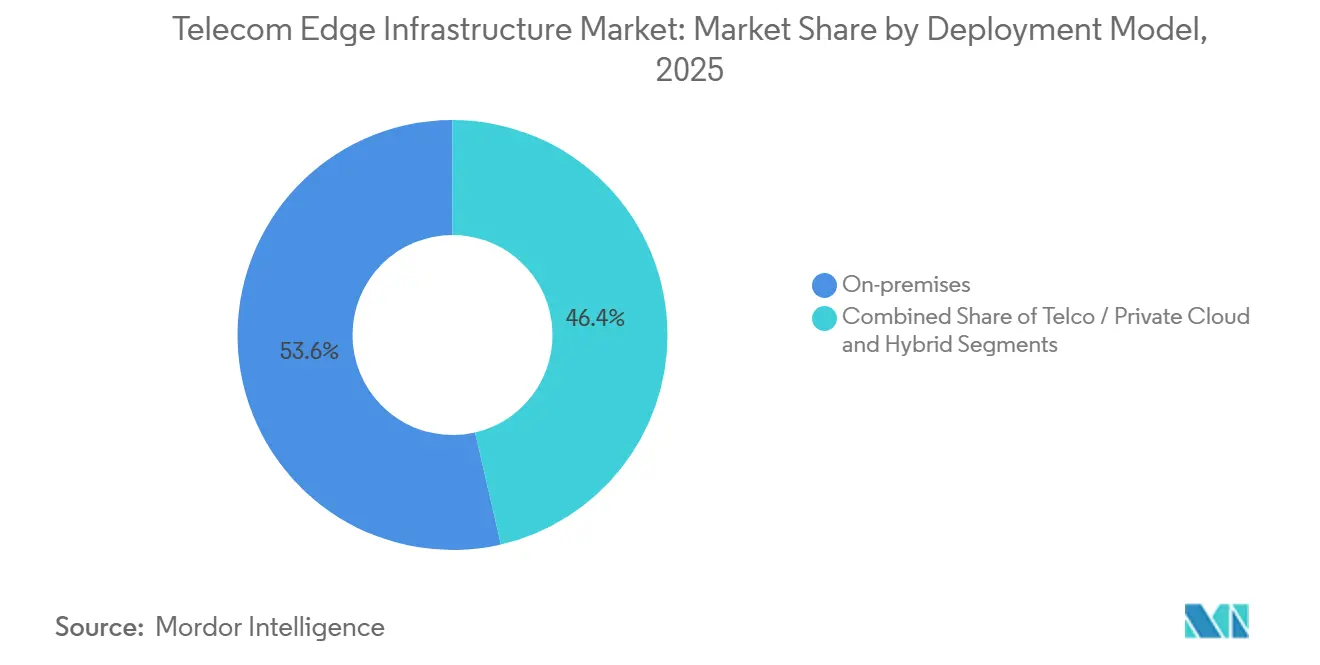

- By deployment model, On-premises led with 53.62% revenue share in 2025, whereas Hybrid is projected to grow at 20.53% CAGR through 2031.

- By application, Enhanced Mobile Broadband (eMBB) accounted for 61.33% of 2025 revenue; Mission-Critical/URLLC workloads are advancing at a 20.42% CAGR through 2031.

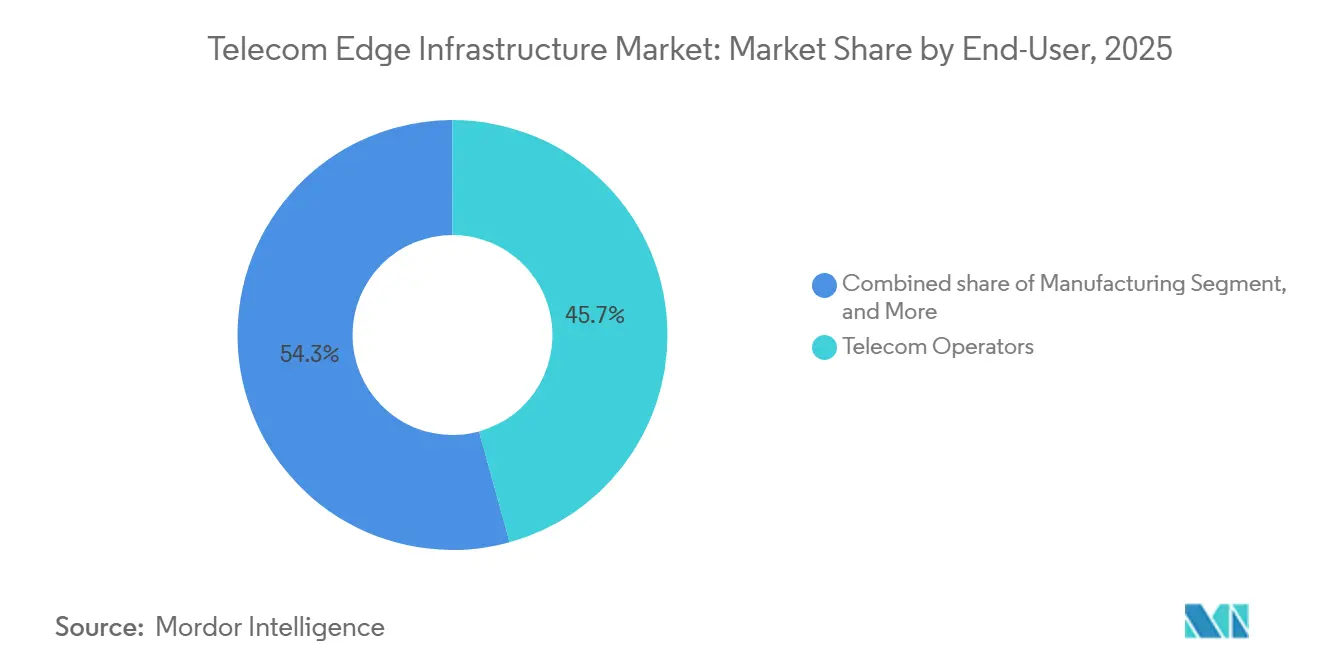

- By end-user industry, Telecom Operators captured 45.72% of 2025 spend; Manufacturing is set to expand at 22.35% CAGR through 2031.

- By geography, Asia-Pacific accounted for 42.52% of 2025 revenue and recorded the highest forecast CAGR of 21.61% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Telecom Edge Infrastructure Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G NR Roll-Out Acceleration | +4.2% | Global, with APAC and North America leading deployment density | Medium term (2-4 years) |

| Surge in Ultra-Low-Latency Enterprise Use-Cases | +3.8% | North America, Europe, APAC manufacturing hubs (China, Japan, South Korea) | Medium term (2-4 years) |

| Private 5G and Campus Networks Adoption | +3.5% | Global, concentrated in manufacturing, healthcare, logistics sectors | Long term (≥4 years) |

| Telco CAPEX Shift Toward Distributed Cloud Architecture | +2.9% | Global, led by tier-1 operators in North America, Europe, APAC | Long term (≥4 years) |

| RAN Intelligent Controller (RIC) Enabling Agile Edge Apps | +2.1% | North America, APAC (Japan, South Korea), Europe | Medium term (2-4 years) |

| Micro-Edge Sustainability Incentives (Renewable Power) | +1.7% | Europe, North America, APAC (Australia, Japan) | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

5G NR Roll-Out Acceleration

Standalone 5G migration is advancing faster than initial operator forecasts, compressing the schedule for edge node deployment. China recorded 79% standalone penetration by late 2025, while India reached 49.2% and Singapore 37%. The decoupling between marketing claims and core-network upgrades is evident in the 192 operators globally that committed to a standalone architecture, compared with 384 commercial 5G launches. Standalone cores unlock network slicing and URLLC services, sharpening demand for distributed compute. Japan’s full-stack virtualized network achieved roughly 20% energy savings after the activation of the RAN Intelligent Controller, illustrating parallel opex benefits. Operators that defer standalone upgrades risk ceding industrial clients to rivals able to guarantee deterministic latency.[1]GSMA Intelligence, “Standalone 5G Adoption Statistics,” gsma.com

Surge in Ultra-Low-Latency Enterprise Use-Cases

Manufacturing, healthcare, and energy firms now require sub-10-millisecond latency for closed-loop control and teleoperation. A 2025 time-sensitive networking trial achieved 122-nanosecond synchronization over 5G, enabling robotic assembly that once relied on industrial Ethernet. Food-processing plants using private 5G with on-prem edge compute issued predictive-maintenance alerts in 6 milliseconds, cutting unplanned downtime. Remote surgery experiments established a 1-5 millisecond latency ceiling for haptic feedback, unachievable from centralized clouds hundreds of kilometers away. Above 90% of enterprises piloting private 5G reported payback within 12 months, driven more by productivity gains than by connectivity cost reductions. The telecom edge infrastructure market is therefore extending beyond early adopters into mainstream operational technology buyers.[2]Nokia, “Private 5G Networks ROI Survey,” nokia.com

Private 5G and Campus Networks Adoption

Industrial companies treat private 5G as a strategic production asset. A leading aerospace manufacturer integrated augmented-reality work instructions and autonomous guided vehicles on a licensed spectrum network at two U.K. sites. In Germany, automotive plants replaced wired inspection lines with computer vision running on edge compute, improving quality while meeting data-sovereignty mandates. Regulations such as GDPR and China’s Personal Information Protection Law reward local processing, reinforcing demand for campus nodes. Operators offer managed private networks, yet enterprises wield stronger negotiating power because they increasingly buy equipment directly and hire systems integrators for support.

Telco CAPEX Shift Toward Distributed Cloud Architecture

Tier-1 carriers are reallocating capital from centralized data centers to thousands of micro edges. A U.S. operator partnered with two hyperscalers to embed compute at cell sites, targeting autonomous vehicles and gaming. A European incumbent is extending edge coverage across its national footprints to secure sub-20-millisecond service-level guarantees for logistics clients. Microsites lack the economies of scale enjoyed by hyperscale facilities, so selective urban deployments yield faster payback. This pattern foretells a clustered edge topology that privileges dense metros and industrial corridors over sparsely populated regions.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Standards Across MEC and Open RAN Stacks | -2.8% | Global, particularly affecting multi-vendor deployments | Medium term (2-4 years) |

| High Upfront Site Power and Cooling Costs | -2.3% | Global, acute in emerging markets with unreliable grid infrastructure | Short term (≤2 years) |

| Limited Edge-To-Core Orchestration Skill-Set Among CSPs | -1.6% | Global, more pronounced in tier-2 and tier-3 operators | Long term (≥4 years) |

| Fiber Backhaul Bottlenecks in Emerging Economies | -1.4% | Sub-Saharan Africa, South America, rural Asia-Pacific | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Fragmented Standards Across MEC and Open RAN Stacks

Parallel standard bodies publish overlapping specifications that rarely interoperate cleanly. PlugFest testing in 2025 revealed integration failures topping 30% for multi-vendor RAN elements. Operators often maintain separate orchestration planes for each supplier’s edge platform, inflating both capital and engineering costs. Vertical integration can reduce risk but raises fears of vendor lock-in. The absence of a unified framework delays broad adoption and cools investment appetite.

High Upfront Site Power and Cooling Costs

Typical macro sites provision only 5-10 kW for radios, yet an edge compute stack can double that draw. Upgrading electrical feeds, installing HVAC units, and adding backup generation can exceed USD 100,000 per urban site. Emerging markets battle intermittent power grids, forcing carriers to install diesel or battery backups that further elevate costs. Renewable options mitigate opex over time, but they require additional permitting and real estate. These economics limit universal roll-outs and steer carriers toward revenue-dense metro clusters.[3]Vertiv, “Edge Site Power and Cooling Economics,” vertiv.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Orchestration Outpaces Hardware Growth

Software captured the fastest growth, rising 20.88% through 2031, while hardware retained 53.41% of 2025 revenue. The telecom edge infrastructure market size for software is projected to expand as virtualized user-plane functions and firewalls migrate to Kubernetes containers, freeing operators from proprietary appliances. Universal customer-premises equipment and white-box servers commoditize hardware, lowering margins yet enlarging the pool of suppliers. Orchestration platforms from multiple vendors abstract complexity, cutting service introduction cycles from months to weeks. Integration and managed-service offers remain vital because most carriers lack in-house cloud engineering skills, positioning system integrators to capture a rising share of spending.

A secondary trend sees chip manufacturers bundling accelerator cards with open-source frameworks, simplifying deployment and boosting performance. Hardware vendors respond by shipping ruggedized edge servers built for harsh cell-site environments. The telecom edge infrastructure market continues to balance between cost-optimizing commodity gear and premium, integrated stacks packaged with lifecycle services that de-risk adoption for conservative network operators.

By Edge Location: Enterprise On-Premises Edge Surges

Macro and micro sites still lead deployments, yet on-premises enterprise locations are forecast to grow at 22.02%, reflecting surging interest from factories, hospitals, and ports. The telecom edge infrastructure market share for enterprise sites is set to grow as private networks handle machine control loops on plant floors. Aggregation hubs fill a performance gap for workloads tolerant of sub-20 millisecond latency, while refurbished central offices drive cost-efficient regional coverage.

Private industrial clients prize deterministic performance and data sovereignty, pushing them to self-host compute or contract specialized integrators. Telecom operators counter with managed private 5G to defend relevance, but intense price competition shrinks gross margins. White-box gear and open-source management stacks lower entry barriers, encouraging plant owners to experiment with multi-vendor architectures.

By Deployment Model: Hybrid Architectures Gain Traction

On-premises deployments held 53.62% market share in 2025, but hybrid models are climbing at 20.53% as enterprises blend control with flexibility. Workloads hop between local nodes and telco edges according to latency targets, cost, or data-residency rules. A growing number of firms are adopting platform-as-a-service offerings from hyperscalers that deliver identical APIs across on-premises, telco edge, and public cloud, minimizing refactoring.

Billing remains complex because traffic may traverse three ownership domains during a single session. Operators and cloud providers negotiate revenue splits tied to service-level performance. Hybrid viability depends on consistent orchestration and holistic security frameworks. The telecom edge infrastructure industry, therefore, invests heavily in multi-cluster Kubernetes management and zero-trust policy engines to maintain compliance across locations.

By Application: Mission-Critical URLLC Expands Beyond Early Pilots

Enhanced mobile broadband still drives volume, yet mission-critical and URLLC workloads post the highest growth at 20.42%. Factory control systems, remote surgery, and autonomous vehicles demand round-trip latency under 5 milliseconds with five-nines reliability. The telecom edge infrastructure market for URLLC remains smaller today, but each project commands higher average revenue because clients pay for guaranteed uptime rather than consumed bandwidth.

Industrial buyers weigh the cost of downtime above connectivity fees. Operators shift to outcome-based contracts that penalize missed latency targets. Hardware makers integrate time-sensitive networking support, while chipset vendors release deterministic scheduling primitives in 5G Advanced. The URLLC expansion is driving investment toward GPUs and FPGA accelerators at cell sites to sustain real-time analytics and computer vision inference.

By End-User Industry: Manufacturing Leads Enterprise Adoption

Manufacturing is the fastest-growing enterprise vertical, with a 22.35% CAGR, overtaking telecom operators as the primary driver of private edge deployments beyond 2027. The automotive, electronics, and process industries embrace computer vision inspection, autonomous material handling, and predictive maintenance. The telecom edge infrastructure market size for manufacturing projects is forecast to widen as plants retrofit legacy equipment with wireless sensors.

Healthcare follows as hospitals require local processing for medical imagery and robotic surgery. Media firms deploy edge nodes to support live sports production and cloud gaming. Logistics companies turn to edge for warehouse automation, fleet coordination, and port operations. Retail, energy, and public-sector projects remain smaller in value, yet cumulative demand contributes to a diverse pipeline that insulates suppliers from sector-specific downturns.

Geography Analysis

Asia-Pacific leads adoption, accounting for 42.52% of 2025 revenue and a forecast CAGR of 21.61%. Nationwide 5G coverage in China, Japan, and South Korea, underpinned by dense fiber backhaul, supports large-scale edge nodes inside smart-manufacturing clusters. India rolls out standalone 5G across tier-1 and tier-2 cities, though rural fiber scarcity tempers uniform distribution. Southeast Asian smart-city programs in Singapore and Thailand accelerate public-sector edge spending.

North America contributes roughly one-quarter of revenue. U.S. operators deploy thirty-plus metro edge zones to target gaming, computer vision, and retail analytics. Canada builds private networks in automotive and aerospace plants, leveraging government incentives for digital transformation. Operators differentiate through service-level agreements that guarantee sub-20 millisecond latency across hybrid footprints.

Europe records a similar aggregate share, spurred by the Digital Decade requirement for gigabit coverage. Germany, France, and Spain focus on industrial and automotive corridors, while the Nordics exploit abundant renewable energy to offer carbon-neutral edge hosting. Standards fragmentation and spectrum licensing complexities introduce integration delays, yet robust fiber infrastructure smooths long-run scaling.

The Middle East and Africa see uneven progress. Gulf states leverage high disposable income and government diversification agendas to deploy smart-city edge platforms. Sub-Saharan Africa endures fiber gaps, forcing operators to concentrate on macro-site deployments and satellite backhaul for edge outreach. South America gains momentum in Brazil and Argentina, where urban 5G coverage and industrial interest coincide, though regulatory uncertainty around spectrum caps slows multi-country expansion.

Competitive Landscape

Competition spans radio hardware, orchestration software, and application platforms, producing a moderately fragmented arena. Legacy RAN suppliers retain share in baseband and antennas but face erosion as operators embrace white-box hardware and open interfaces. Hyperscalers embed compute directly inside carrier networks, winning orchestration control and developer mindshare. Their scale economies and global API consistency position them to seize application-layer revenues once exclusive to telecom suppliers.

Open RAN specialists are penetrating rural and enterprise markets, packaging flexible pricing and disaggregated components. Yet their share remains low because large operators still prioritize proven performance and strict supply-chain vetting. Semiconductor vendors and server makers are piling into the space with accelerator cards and ruggedized edge servers, aiming to commoditize hardware and shift value upstream.

Patent filings on distributed scheduling, network slicing, and AI-driven optimization surge, indicating intense R&D investment. Consolidation appears likely over the forecast horizon as hyperscalers acquire niche orchestration vendors and carriers streamline multi-vendor estates to lower integration costs. Barriers to exit remain low for software startups, keeping innovation velocity high and pressuring incumbents to release roadmap updates every six months.

Telecom Edge Infrastructure Industry Leaders

Telefonaktiebolaget LM Ericsson

Nokia Corporation

Huawei Technologies Co., Ltd.

Cisco Systems, Inc.

Samsung Electronics Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Nokia signed a multi-year contract with Bharti Airtel to roll out cloud-native edge platforms in 15 Indian cities, targeting sub-20 millisecond enterprise latency.

- January 2026: Ericsson won a USD 1.2 billion order from China Mobile to supply Cloud RAN and edge compute across three provinces.

- December 2025: AWS expanded Wavelength zones to 12 additional cities in Europe and Asia-Pacific, extending single-digit-millisecond coverage.

- October 2025: Samsung partnered with Verizon to virtualize 10,000 U.S. cell sites using off-the-shelf servers.

Global Telecom Edge Infrastructure Market Report Scope

The Telecom Edge Infrastructure Market Report is Segmented by Component (Hardware, Software, and Services), Edge Location (Macro/Micro Cell Sites, Aggregation Hubs, Central Offices, Regional Data Centers, and Enterprise On-prem Edge), Deployment Model (On-premises, Telco/Private Cloud, and Hybrid), Application (eMBB, Massive IoT, and Mission-critical/URLLC), End-user Industry (Telecom Operators, Manufacturing, Healthcare, Media and Entertainment, Transportation and Logistics, and Other End-user Industries), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Hardware | Edge Servers |

| uCPE / White-box | |

| RAN Distributed Units (DU) | |

| Software | Virtualized Network Functions |

| Edge Orchestration Platforms | |

| Services |

| Macro / Micro Cell Sites |

| Aggregation Hubs |

| Central Offices |

| Regional Data Centers |

| Enterprise On-prem Edge |

| On-premises |

| Telco / Private Cloud |

| Hybrid |

| Enhanced Mobile Broadband (eMBB) |

| Massive IoT (mMTC) |

| Mission-critical / URLLC |

| Telecom Operators |

| Manufacturing |

| Healthcare |

| Media and Entertainment |

| Transportation and Logistics |

| Other end-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of the Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Hardware | Edge Servers | |

| uCPE / White-box | |||

| RAN Distributed Units (DU) | |||

| Software | Virtualized Network Functions | ||

| Edge Orchestration Platforms | |||

| Services | |||

| By Edge Location | Macro / Micro Cell Sites | ||

| Aggregation Hubs | |||

| Central Offices | |||

| Regional Data Centers | |||

| Enterprise On-prem Edge | |||

| By Deployment Model | On-premises | ||

| Telco / Private Cloud | |||

| Hybrid | |||

| By Application | Enhanced Mobile Broadband (eMBB) | ||

| Massive IoT (mMTC) | |||

| Mission-critical / URLLC | |||

| By End-user Industry | Telecom Operators | ||

| Manufacturing | |||

| Healthcare | |||

| Media and Entertainment | |||

| Transportation and Logistics | |||

| Other end-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of the Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the telecom edge infrastructure market in 2031?

The market is expected to reach USD 17.52 billion by 2031, reflecting an 17.48% CAGR from 2026 to 2031.

Which region is expected to grow the fastest through 2031?

Asia-Pacific leads with a 21.61% CAGR, driven by dense 5G deployments and manufacturing demand in China, Japan, and India.

Why are enterprises adopting private 5G and on-premises edge nodes?

Enterprises need sub-10 millisecond latency, strict data sovereignty, and control over industrial processes, benefits hard to guarantee on shared public networks.

How are hyperscalers influencing the telecom edge infrastructure market?

Providers such as AWS, Microsoft, and Google embed compute within carrier networks, capturing orchestration and application revenues that were traditionally held by equipment vendors.

What are the main barriers to widespread edge roll-out?

Fragmented standards, high site power and cooling costs, limited orchestration skills among smaller operators, and fiber backhaul gaps in emerging markets.

Page last updated on: