Technical And Vocational Education Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

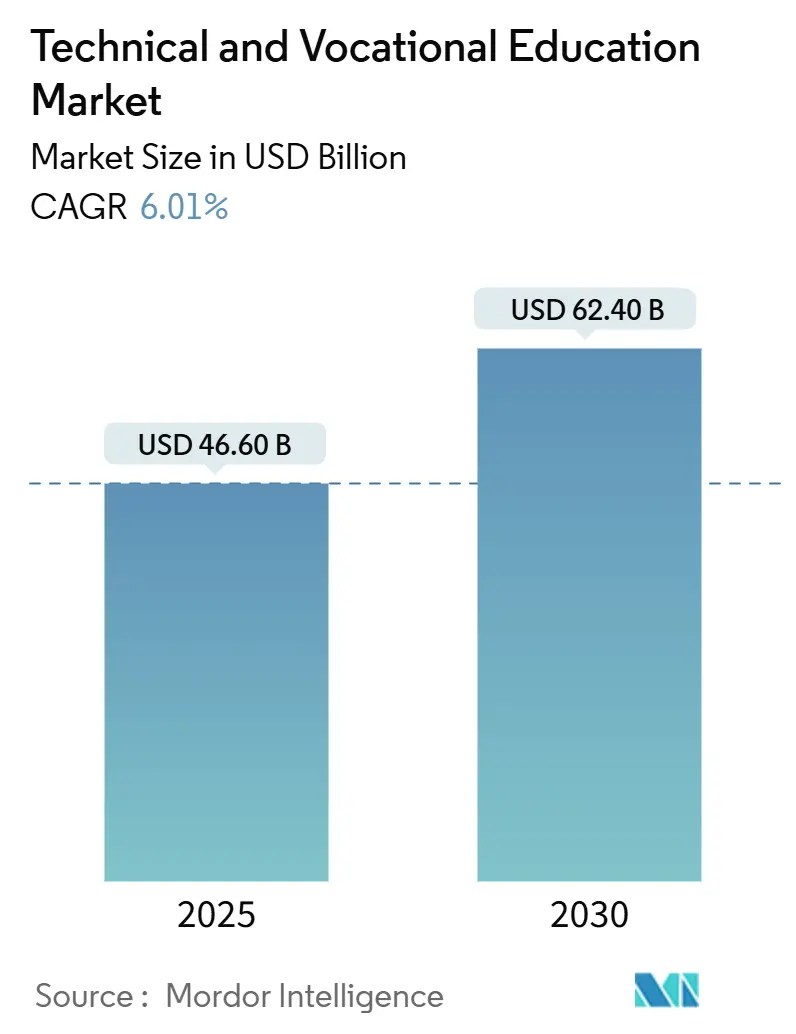

| Market Size (2025) | USD 46.60 Billion |

| Market Size (2030) | USD 62.40 Billion |

| Growth Rate (2025 - 2030) | 6.01% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

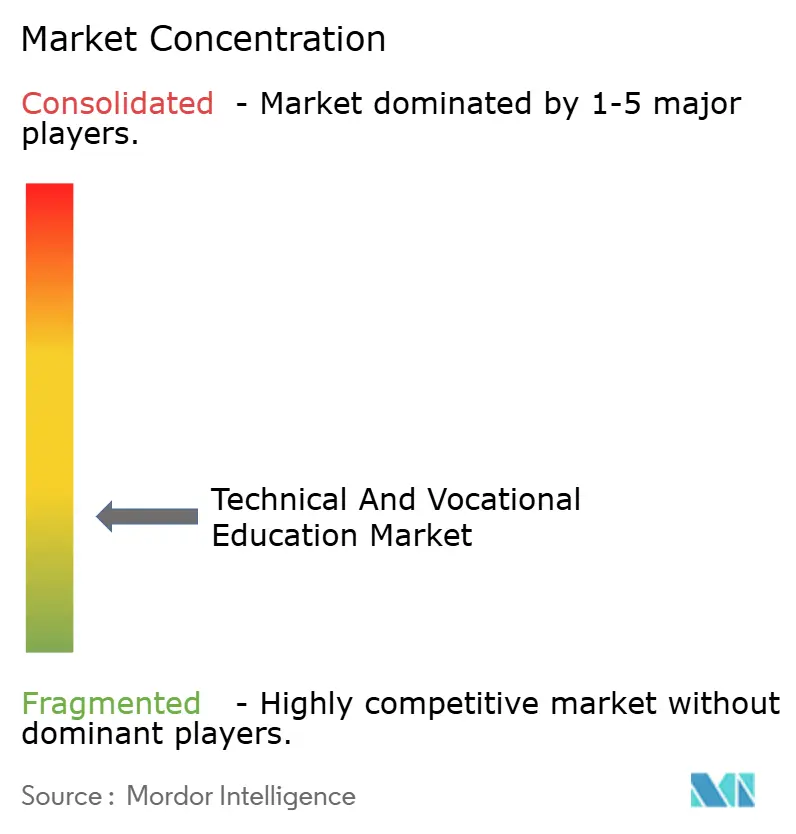

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Technical And Vocational Education Market Analysis by Mordor Intelligence

The technical and vocational education market size was USD 46.60 billion in 2025 and is projected to reach USD 62.40 billion by 2030, representing a 6.01% CAGR over the forecast period. Momentum stems from rapid industrial automation, which forces employers to retrain workers for higher-value tasks. Meanwhile, public investment programs in Australia, Germany, Singapore, and the United States inject unprecedented funding into reskilling initiatives. Expanding online platforms lower geographic and cost barriers, allowing learners to stack short credentials that align precisely with job vacancies. Regional policy frameworks such as the European Qualifications Framework and the ASEAN Qualifications Reference Framework add further impetus by improving cross-border recognition of vocational certificates. Meanwhile, technology vendors deploy artificial-intelligence tutoring systems and virtual-reality labs that compress training cycles while preserving the hands-on rigor demanded by employers.

Key Report Takeaways

- By program type, diplomas and certificates held 38.42% of the technical and vocational education market share in 2024, whereas online micro-credentials are projected to grow at a 7.40% CAGR to 2030.

- By delivery mode, classroom-based instruction commanded 49.18% share of the technical and vocational education market size in 2024; online learning is advancing at a 6.34% CAGR through 2030.

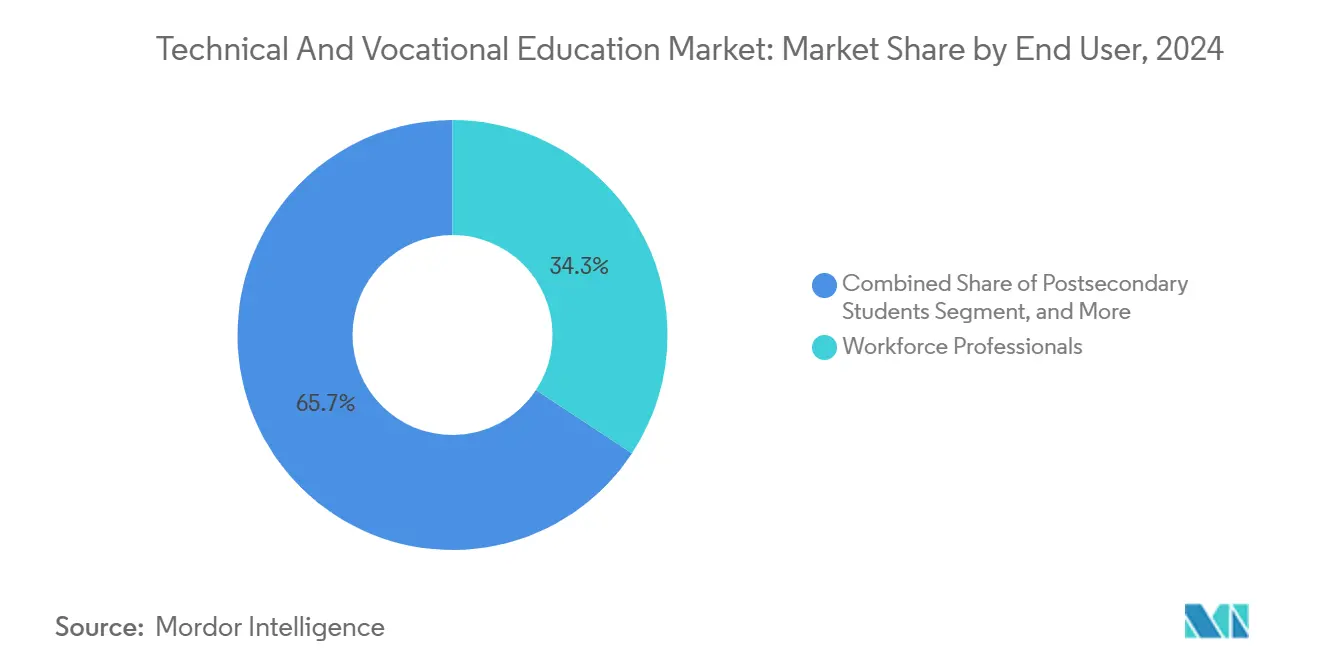

- By end user, workforce professionals accounted for 34.26% share of the technical and vocational education market size in 2024 and are expanding at an 8.01% CAGR to 2030.

- By funding source, public institutions contributed 46.76% of technical and vocational education market share in 2024, while corporate-sponsored programs post the fastest 6.76% CAGR through 2030.

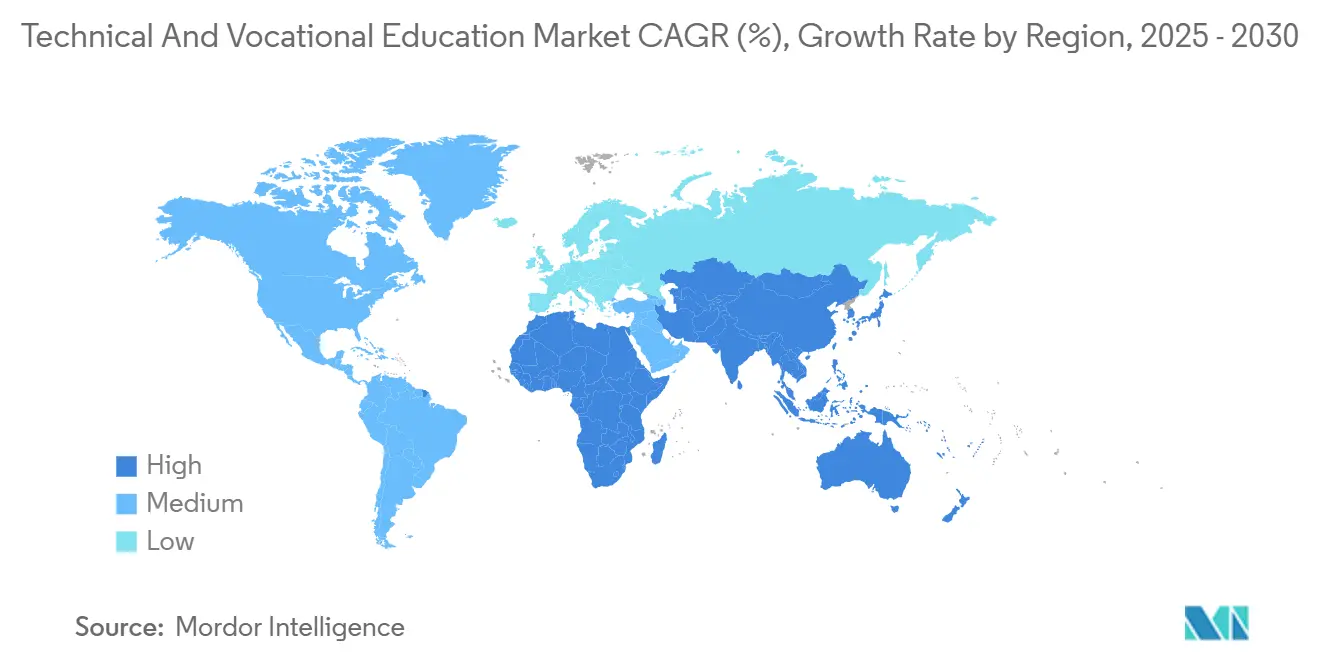

- By geography, Asia Pacific led with 32.84% technical and vocational education market share in 2024; the Middle East registers the highest 7.82% CAGR through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Technical And Vocational Education Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Funding Boosts for Workforce Upskilling | +1.8% | Global, with early gains in Australia, Germany, Singapore | Medium term (2-4 years) |

| Rapid Industrial Automation Creating Skills Gap | +1.5% | North America and EU, APAC manufacturing hubs | Short term (≤ 2 years) |

| Expansion of Online Learning Platforms | +1.2% | Global, spill-over to emerging markets | Short term (≤ 2 years) |

| Integration of Micro-Credentials into Corporate HR Systems | +0.9% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Youth Unemployment Surges in Sub-Saharan Africa | +0.4% | Africa core, limited spill-over | Long term (≥ 4 years) |

| Migration Policies Linking Work Visas to Recognized Vocational Certifications | +0.3% | Global, with concentration in developed economies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Funding Boosts for Workforce Upskilling

Australia’s National Skills Agreement commits USD 30 billion through 2029, Germany’s Federal Employment Agency raised vocational allocations 23% in 2024, and the U.S. Workforce Innovation and Opportunity Act disbursed USD 3.2 billion toward sector-focused training in 2024.[1]Australian Department of Education, “National Skills Agreement,” EDUCATION.GOV.AU Such large-scale public outlays acknowledge that mainstream schooling cannot keep pace with technological advancements, prompting governments to elevate vocational pathways as a cornerstone of their industrial strategy.

Rapid Industrial Automation Creating Skills Gap

In 2024, shipments of industrial robotics and installations in smart factories saw a significant uptick. However, manufacturers spanning from the U.S. to Germany are grappling with a shortage, reporting thousands of unfilled roles in mechatronics and maintenance. This shortage is attributed to the rapid pace of technological advancements, which has outpaced the availability of a skilled workforce capable of managing and maintaining these advanced systems. In response, vocational institutes are revamping their curricula, emphasizing industrial IoT diagnostics, collaborative robot programming, and predictive maintenance analytics, aiming to bridge this growing skills gap. These updated programs are designed to equip students with the technical expertise and practical knowledge required to meet the evolving demands of the industrial robotics and smart factory sectors.

Expansion of Online Learning Platforms

In 2024, UNESCO reported a 34% annual surge in online vocational enrollments. This growth reflects the increasing demand for flexible and accessible skill development opportunities across various industries. Hybrid models, which meld virtual simulations with brief in-center practicums, are achieving notable scale efficiencies by combining the convenience of online learning with the practical experience of in-person training. By the close of 2024, Coursera boasted 118 million participants in its professional certificate programs, highlighting the global endorsement of digital credentials by employers. This trend underscores the growing recognition of online platforms as credible and effective avenues for workforce upskilling and reskilling.

Migration Policies Linking Work Visas to Recognized Vocational Certifications

Canada, Germany, and Australia have begun awarding immigration points to applicants with internationally recognized TVET credentials. This policy shift underscores the growing importance of technical and vocational education and training in addressing global labor market demands. In response, source countries are reforming their curricula to align with global competency standards, aiming to boost worker mobility and ensure their workforce remains competitive in the international job market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Perception of Inferior Status Compared to Academic Pathways | -1.1% | Global, particularly acute in Asia and Europe | Long term (≥ 4 years) |

| Fragmented Qualification Frameworks Across Countries | -0.8% | Global, with concentration in developing economies | Medium term (2-4 years) |

| Rising Cost of Industry-Grade Training Equipment | -0.6% | Global, spill-over to resource-constrained institutions | Short term (≤ 2 years) |

| Data Privacy Regulations Limiting Learning Analytics in TVET | -0.3% | EU core, expanding to other developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Perception of Inferior Status Compared to Academic Pathways

OECD surveys show that many families still equate vocational tracks with lower prestige. In South Korea, only 23% of high school graduates chose TVET amid 47% youth unemployment in 2024.[2]OECD, “Education at a Glance 2024,” OECD.ORG This highlights the persistent stigma surrounding vocational education, which continues to deter students from pursuing these career pathways despite their potential to address labor market needs.

Fragmented Qualification Frameworks Across Countries

Only 34% of EU vocational certificates receive automatic recognition across member states. The European Commission, targeting a boost in this figure, plans to revise the European Qualifications Framework in 2025. This lack of automatic recognition creates significant challenges for multinational firms operating across borders. These companies are compelled to fund redundant training programs to ensure compliance with varying local regulatory requirements. Such duplicative efforts not only inflate operational costs but also slow down workforce mobility, limiting the ability of firms to efficiently allocate human resources across different regions. Addressing this issue through the proposed revisions could enhance labor market integration and reduce barriers to cross-border employment within the EU.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Program Type: Credentials Drive Modular Learning

Diplomas and certificates accounted for 38.42% of the technical and vocational education market share in 2024, reflecting institutional appetite for comprehensive multi-skill programs. The segment maintains relevance by incorporating capstone projects and employer-co-designed assessments that demonstrate work readiness to recruiters.[3]UNESCO Institute for Statistics, “Global Education Statistics,” UIS.UNESCO.ORG Online micro-credentials, however, post the strongest 7.40% CAGR as firms increasingly hire for verified capabilities rather than broad qualifications, pivoting the technical and vocational education market toward bite-sized, stackable learning pathways.

The micro-credential wave exemplifies how the technical and vocational education market adapts to shortening skill half-lives: learners assemble career “playlists” of cloud administration, data visualization, or renewable energy modules that can be refreshed annually. Google Career Certificates achieved 87% employer satisfaction rates, underscoring growing corporate trust in alternative credentials. Standards such as ISO 29993 enhance program credibility, while blockchain verification helps combat credential fraud, a key concern for employers.

By Delivery Mode: Digital Transformation Accelerates

Classroom delivery retained a 49.18% share of the technical and vocational education market size in 2024, as heavy-equipment operation, safety drills, and team troubleshooting still benefit from a physical presence. Yet virtual reality welding booths, remote labs, and AI-guided simulations drive a 6.34% CAGR for fully online programs, compressing costs and widening access.

Post-pandemic, 78% of institutions keep hybrid timetables that split theory online and practice in short bootcamps, proving especially effective for mid-career adults balancing work and study. The technical and vocational education market, therefore, gravitates toward a continuum where digital theory feeds directly into hands-on practicums, maximizing seat utilization and reducing equipment downtime.

By End User: Workforce Professionals Lead Demand

Workers already in employment represented 34.26% of the technical and vocational education market size in 2024 and form the fastest-expanding cohort with an 8.01% CAGR through 2030. Employers encourage mid-career reskilling as automation redefines roles, channeling staff into part-time evening or weekend programs that culminate in portable certifications.

Secondary-school TVET pathways enjoy steady state funding and gradually gain parity with academic streams as governments embed dual-training models. Postsecondary students increasingly view vocational routes as a cost-effective alternative to university, while the unemployed rely on publicly funded re-entry programs that align with regional industrial policies. Across all groups, the technical and vocational education market rewards flexible, competency-based progression over time-bound semesters.

By Funding Source: Corporate Investment Surges

Public funding accounted for 46.76% of the technical and vocational education market share in 2024, underscoring the sector’s socio-economic importance. Nonetheless, fledgling labor shortages push corporations to underwrite dedicated academies, driving a 6.76% CAGR in company-sponsored courses.

Amazon’s Career Choice program alone invested USD 1.2 billion in employee upskilling through 2024 and reports markedly higher retention among graduates. Private institutions cater to premium niches, such as aviation maintenance, while NGOs steer donor grants toward populations excluded from mainstream education. The resulting funding mosaic illustrates how the technical and vocational education market blends public good objectives with private ROI imperatives.

Geography Analysis

Asia Pacific commanded 32.84% of the technical and vocational education market share in 2024, propelled by China’s 44 million vocational learners on the National Smart Education Platform and India’s large-scale digital-skills missions.[4]Asian Development Bank, “Skills Development in Asia and the Pacific,” ADB.ORG Government subsidies, ultrafast industrial upgrading, and high secondary school participation sustain growth as enterprises clamor for automation, renewable energy, and semiconductor technicians.

North America and Europe hold substantial portions of the technical and vocational education market share, thanks to mature community college networks and employer tuition subsidies. The European Skills Agenda funds cross-border apprenticeship exchanges, while Canada’s immigration-linked credential system fuels demand among newcomers seeking rapid labor-market entry. Strict data-privacy laws may temper the adoption of analytics-heavy learning platforms; however, regional policy commitments to green and digital transitions support stable expansion.

The Middle East records the fastest 7.82% CAGR as Saudi Arabia, the UAE, and neighboring Gulf states diversify beyond hydrocarbons through Vision 2030 roadmaps that earmark billions for TVET infrastructure. New qualifications frameworks harmonize standards region-wide, enabling labor mobility across the Gulf Cooperation Council. Africa, while currently trailing in absolute enrollment, represents long-run opportunity: demographic bulges and urgent youth employment needs spur continental bodies to invest in low-cost, mobile-first vocational solutions.

Competitive Landscape

The technical and vocational education market remains fragmented, with no single provider controlling more than 5% of the global revenue. Legacy publishers, such as Pearson, pivot from textbook sales to skills-focused services, leveraging their deep curriculum libraries and accreditation expertise. Digital natives like Coursera and Udacity scale rapidly by partnering with multinational corporations for co-branded professional certificates, capturing the fastest-growing online micro-credential niche.

Regional champions thrive by tailoring content to local languages and regulatory nuances; for example, Singapore’s ITE Education Services exports dual-training models across ASEAN. Technology suppliers, including Microsoft and IBM, augment their cloud ecosystems with skills academies, thereby locking clients into platform-specific talent pipelines. Virtual-reality specialists provide turnkey simulators for welding, electrical, and healthcare programs, reducing entry costs for smaller institutions.

Strategic focus centers on AI-driven personalization, blockchain credential verification, and employer co-development of curricula. Providers also pursue outcome-based pricing, where fees hinge on graduate employment rates. Competitive intensity is expected to rise as ed-tech firms, equipment manufacturers, and traditional universities converge on the same lifelong-learning audiences.

Technical And Vocational Education Industry Leaders

Pearson plc

City and Guilds of London Institute

Coursera Inc.

Kaplan Inc.

Udacity, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: The European Union has unveiled the EUR 4.2 billion (USD 4.89 billion) Skills for Digital Transition Initiative, which spans AI, cybersecurity, and green technology.

- September 2025: Microsoft earmarked USD 1.8 billion for 25 new global Skills Centers, with initial sites in Indonesia and Kenya.

- August 2025: India launched the USD 2.1 billion National Digital Skills Mission to train 50 million citizens by 2030.

- July 2025: Amazon Web Services and UNESCO committed USD 500 million over five years to open cloud-computing centers in 15 developing countries.

Global Technical And Vocational Education Market Report Scope

| Diplomas and Certificates |

| Apprenticeships |

| Skills Training Courses |

| Online Micro-Credentials |

| Classroom-Based |

| Online |

| Blended |

| Secondary Education Students |

| Postsecondary Students |

| Workforce Professionals |

| Unemployed and Skill Switchers |

| Public Institutions |

| Private Institutions |

| Corporate-Sponsored Programs |

| Non-Profit and NGO-Run Programs |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Program Type | Diplomas and Certificates | |

| Apprenticeships | ||

| Skills Training Courses | ||

| Online Micro-Credentials | ||

| By Delivery Mode | Classroom-Based | |

| Online | ||

| Blended | ||

| By End User | Secondary Education Students | |

| Postsecondary Students | ||

| Workforce Professionals | ||

| Unemployed and Skill Switchers | ||

| By Funding Source | Public Institutions | |

| Private Institutions | ||

| Corporate-Sponsored Programs | ||

| Non-Profit and NGO-Run Programs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the forecast value of the technical and vocational education market by 2030?

The market is projected to reach USD 62.40 billion by 2030.

Which region currently holds the largest share of global enrollments?

Asia Pacific accounts for 32.84% of global enrollments, the highest regional share.

Which delivery mode is growing fastest within technical and vocational education?

Fully online programs are expanding at a 6.34% CAGR through 2030.

Why are micro-credentials gaining traction with employers?

They verify specific, job-ready competencies and can be updated quickly as technologies evolve.

How are governments supporting vocational upskilling?

Large-scale funding packages, such as Australia’s USD 30 billion National Skills Agreement and the EU’s EUR 4.2 billion digital transition fund, subsidize program expansion and infrastructure modernization.

Page last updated on: