Taiwan Printed Circuit Board Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

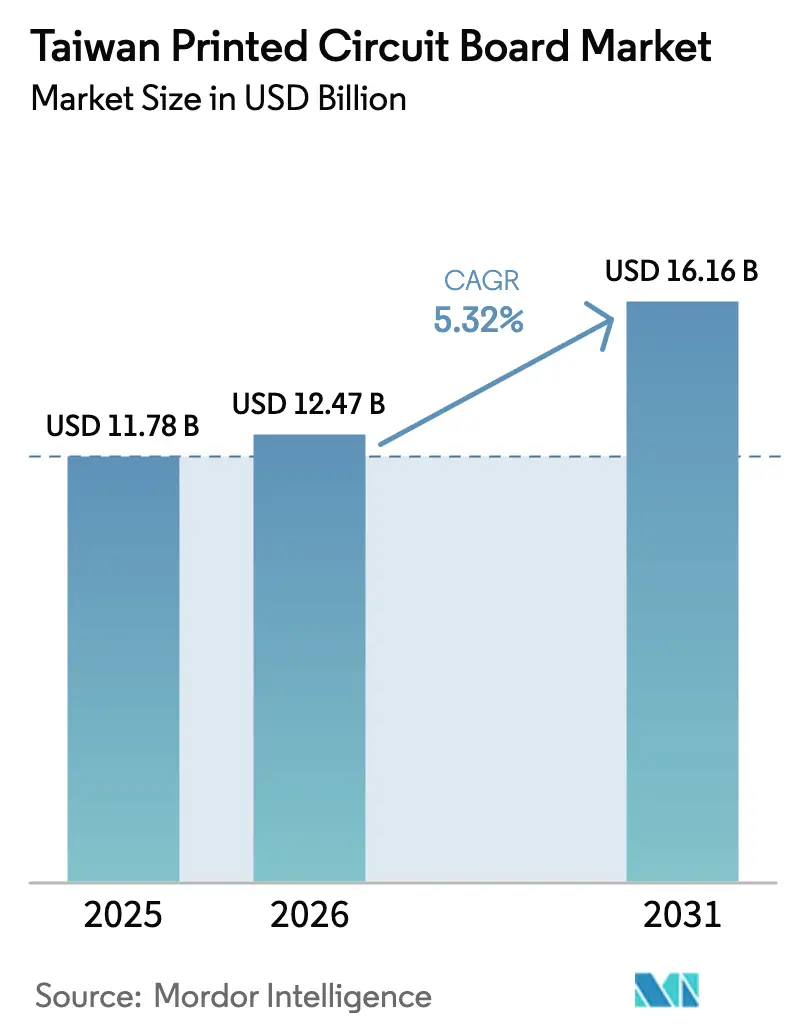

| Base Year Market Size (2025) | USD 11.78 Billion |

| Market Size (2026) | USD 12.47 Billion |

| Market Size (2031) | USD 16.16 Billion |

| Growth Rate (2026 - 2031) | 5.32% CAGR |

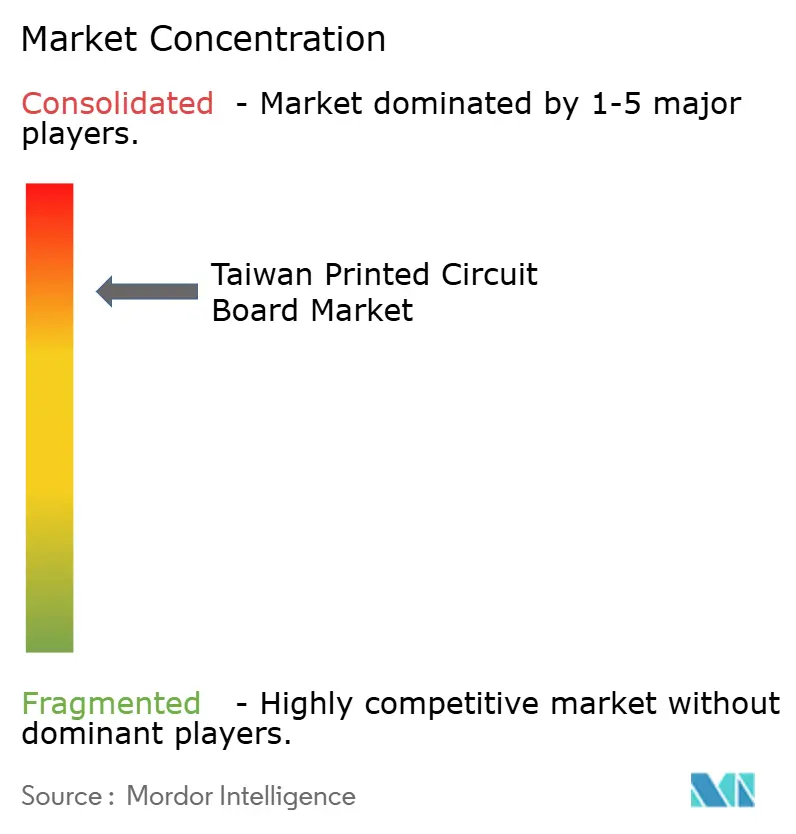

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Taiwan Printed Circuit Board Market Analysis by Mordor Intelligence

The Taiwan printed circuit board market size is expected to increase from USD 11.78 billion in 2025 to USD 12.47 billion in 2026 and reach USD 16.16 billion by 2031, growing at a CAGR of 5.32% over 2026-2031. Sustained outlays for artificial intelligence servers, advanced packaging, and 5G infrastructure anchor the growth trajectory. Flexible circuit demand accelerates as foldable smartphones and wearable devices move from premium niches into mainstream price tiers, while high-speed low-loss laminates gain favor inside 800G and 1.6T optical transceivers. Investments by Taiwan Semiconductor Manufacturing Company (TSMC) to lift CoWoS packaging throughput cascade into larger substrate orders, reinforcing a value migration from commodity rigid boards to premium IC substrates. Meanwhile, government incentives that reward low-emission production help offset inflation in copper and epoxy resin prices, encouraging capital expenditure on energy-efficient etching, lamination, and wastewater treatment lines.

Key Report Takeaways

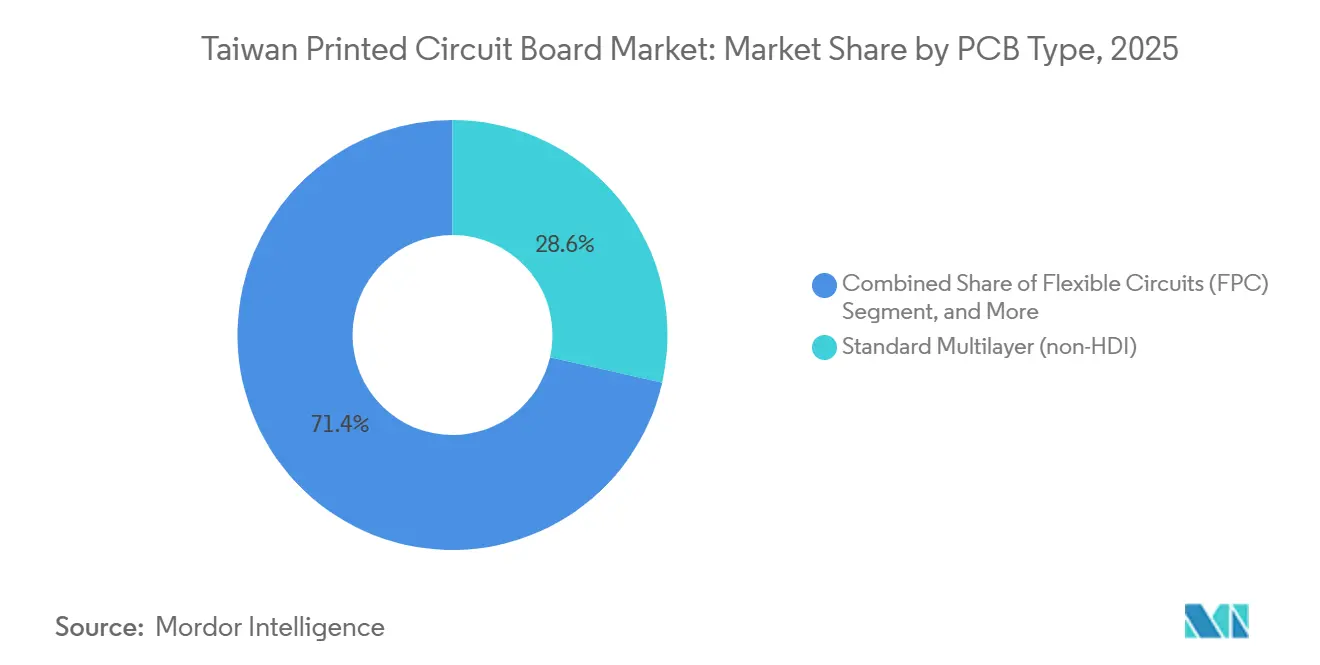

- By PCB type, Standard Multilayer boards led with 28.56% of the Taiwan printed circuit board market, yet Flexible Circuits are forecast to record the fastest 6.87% CAGR through 2031.

- By substrate material, Glass Epoxy FR-4 held 43.62% of the Taiwan printed circuit board (PCB) market share in 2025, whereas High-Speed Low-Loss laminates are poised to expand at a 6.31% CAGR to 2031.

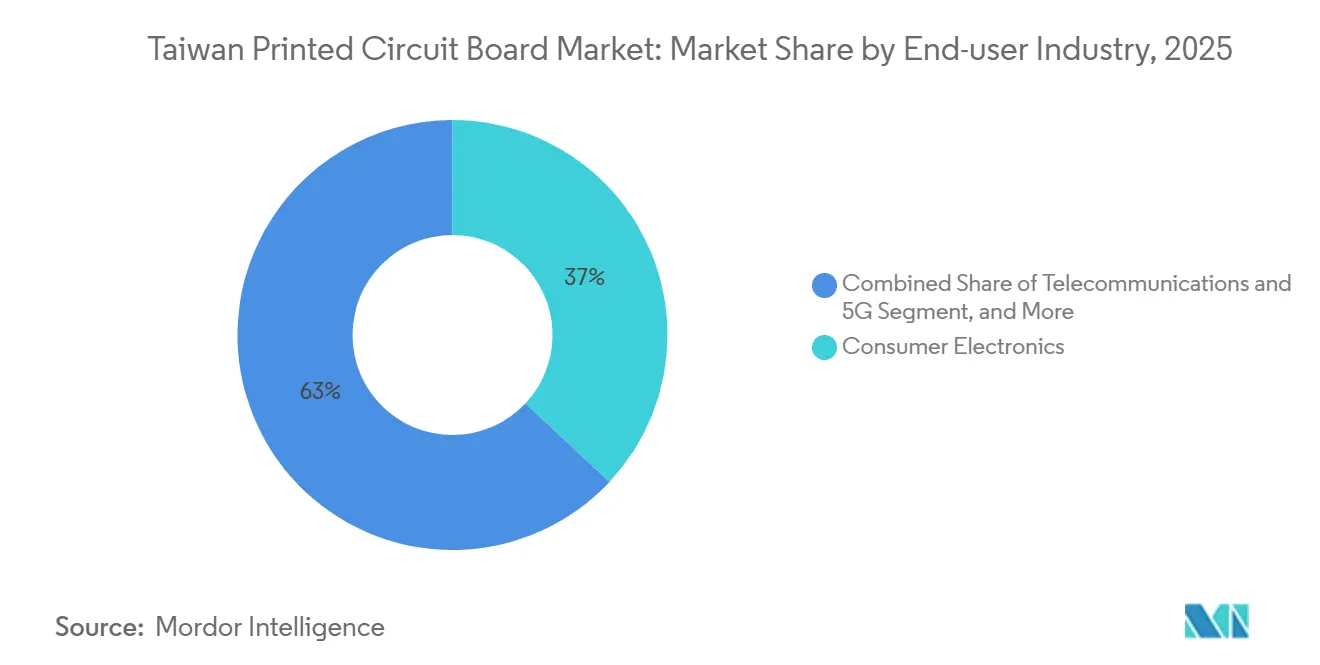

- By end-user industry, Consumer Electronics accounted for 36.98% of the Taiwan PCB market share in 2025, while Telecommunications and 5G applications are projected to register the highest CAGR of 7.11% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Taiwan Printed Circuit Board Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Global Demand for AI Servers and HPC Systems | +1.8% | Global, with concentration in North America and Taiwan domestic data centers | Medium term (2-4 years) |

| Continued Growth in Automotive ADAS and EV Platforms | +1.2% | Global, with early traction in China and European Union; Taiwan suppliers serving Japanese and Korean OEMs | Long term (≥ 4 years) |

| Expansion of 5G Base-Station Deployment in Taiwan | +0.9% | National, with accelerated rollout in Taipei, Taichung, Kaohsiung metropolitan areas | Short term (≤ 2 years) |

| Consumer Shift to Foldable and Wearable Devices | +0.7% | Global, led by Asia-Pacific smartphone brands and North American tech giants | Medium term (2-4 years) |

| On-shoring of Advanced IC Substrate Capacity by Taiwanese Foundries | +1.1% | National, with spillover to Southeast Asian satellite facilities | Medium term (2-4 years) |

| Government Incentives for Green Manufacturing and Low-Emission PCB Lines | +0.5% | National, with pilot programs in Taoyuan and Hsinchu industrial parks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Global Demand for AI Servers and HPC Systems

Hyperscale data centers are deploying Nvidia GB200 and GB300 racks that embed USD 35,000 to USD 70,000 of power-supply boards per unit, pushing Taiwanese fabricators to qualify 20-layer to 40-layer platforms using M7 and M8 laminates.[1]DIGITIMES staff, “Taiwan PCB Industry Sees Strong Growth in 2025 Driven by AI Server Demand,” DIGITIMES, digitimes.com TSMC’s plan to raise CoWoS packaging throughput from 60,000 wafers per month in 2025 to more than 100,000 in 2026 directly lifts organic interposer demand for Unimicron and Zhen Ding. The Taiwan Printed Circuit Association expects 11-12% growth in shipments in 2026, driven mainly by AI server backlogs. Substrate suppliers now co-design thermal and signal-integrity pathways with chipmakers, a higher-margin collaboration model that improves contract stickiness.

Continued Growth in Automotive ADAS and EV Platforms

Electric vehicles average USD 275 of PCB content, nearly triple internal-combustion levels, spurring Taiwanese suppliers holding IATF 16949 certification to prioritize battery-management, inverter, and radar boards. Third-quarter 2025 automotive PCB shipments dipped 4.3% following subsidy withdrawals in the United States and the European Union, yet long-term forecasts remain positive as global brands roll out Level-3 autonomous models. Foxconn’s MIH platform illustrates Taiwan’s opportunity to supply software-defined vehicle architectures that require multi-gigabit signal integrity across vehicle domains. Automotive-grade boards demand extended temperature windows and thicker copper weights, technical hurdles that favor incumbent Taiwanese fabricators.

Expansion of 5G Base-Station Deployment in Taiwan

The Ministry of Digital Affairs reports 97% population coverage in late 2024, backed by Chunghwa Telecom, Taiwan Mobile, and Far EasTone, each using low-loss laminates for 3.5 GHz and 28 GHz radios. The government earmarked NTD 27 billion for infrastructure between 2025 and 2030, subject to a 40% domestic-content rule, creating a captive market for RF and power-amplifier substrates. An additional NTD 1.5 billion supports 6G research into integrated sensing and reconfigurable surfaces, foreshadowing higher layer counts and tighter impedance targets for next-generation boards.

Consumer Shift to Foldable and Wearable Devices

Augmented-reality smart-glasses shipments accelerate as GIS, Porotech, and Foxconn prepare mass production for late 2026. HTC’s VIVE Eagle launched in August 2025 at NTD 15,600, sourcing flexible circuits from Flexium. Flexible PCB output grew 4.1% year over year in 2025, masking strategic importance for ultra-thin, high-bend-radius designs required by foldables. Taiwanese vendors invest in robotic-arm flex harnesses to protect margins against mainland competition.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Copper and Epoxy Resin Prices | -0.9% | Global, with acute impact on Taiwan fabricators due to import dependence | Short term (≤ 2 years) |

| Rising Labor Costs and Skilled-Worker Shortage | -0.6% | National, concentrated in Taoyuan, Hsinchu, and Kaohsiung manufacturing zones | Medium term (2-4 years) |

| Increasing Stringency of Taiwan's Environmental Regulations | -0.4% | National, with pilot enforcement in designated industrial parks | Long term (≥ 4 years) |

| Geopolitical Supply-Chain Risks from Cross-Strait Tensions | -0.7% | National, with spillover to multinational customers diversifying suppliers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Copper and Epoxy Resin Prices

Copper spot prices climbed nearly 40% in 2025 as South American mine disruptions converged with EV demand, while epoxy resin followed petrochemical feedstock spikes. Taiwan imports most of its copper foil and glass fabric, exposing fabricators to currency fluctuations. Commodity rigid-board makers struggle to pass costs through to clients, forcing capacity cuts and delaying equipment upgrades. Larger producers employ hedging and multi-year procurement contracts, but sector margins remain compressed until raw-material markets normalize.

Rising Labor Costs and Skilled-Worker Shortage

Manufacturing job vacancies hit 1.02 million in October 2024, with a 1.54 job-to-applicant ratio, the highest since 2001.[2]Ministry of Labor, Taiwan, “Labor Statistics for November 2024,” mol.gov.tw Average monthly earnings climbed 4.36% year over year to NTD 52,136 in November 2024.[3]Directorate-General of Budget, Accounting and Statistics, “Earnings and Productivity Statistics for November 2024,” dgbas.gov.tw Strict visa quotas constrain inflows of foreign technicians, intensifying competition for optical-inspection and laser-drilling specialists. Fabricators deploy robotics and machine-vision QC to contain payroll growth, but high upfront costs extend payback periods.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By PCB Type: Premium IC Substrates Gain Momentum

Standard Multilayer boards captured 28.56% of the Taiwan printed circuit board market share in 2025, yet Flexible Circuits are pacing the field with a 6.87% CAGR through 2031. IC Substrate suppliers benefit directly from the expansion of the Taiwan PCB market, driven by CoWoS and other heterogeneous integration schemes. Mainland competitors continue to squeeze margins in Rigid 1-2 Sided categories, encouraging Taiwanese firms to exit low-complexity SKUs.

Rigid-Flex designs marry mechanical stability with pliable interconnects, gaining traction in aerospace avionics and implantable devices. High-Density Interconnect boards extend smartphone main-logic density, while niche metal-core and ceramic boards serve power modules and LED arrays. Flexible Circuit output rose 4.1% year over year in 2025, a figure that understates its strategic role in foldables and robotics. IC Substrates command the highest average selling price, and their contribution to the Taiwan PCB market is expected to rise in proportion to advanced packaging wafer starts.

By Substrate Material: High-Speed Low-Loss Laminates Outperform

Glass Epoxy FR-4 remained the workhorse at 43.62% share in 2025, yet High-Speed Low-Loss laminates are forecast to post a 6.31% CAGR, reflecting data-center optical upgrades. The Taiwan PCB market size for laminates suitable for 10 GHz-plus signaling will more than double by 2031 as switch ASICs adopt 224 G lanes. Polyimide films underpin flexible circuits in wearables and foldables, while ABF and BT resins enable advanced IC substrates that integrate logic dies with high-bandwidth memory.

Consumption of M7 and M8 copper-clad laminates expanded 40% in 2025, mirroring AI server board layer counts. Copper foil thickness is trending downward to 12 and 9 micron gauges, reducing skew in high-speed lanes. Packaging Resin demand intensifies as Taiwanese fabricators localize ABF capacity, eroding Japanese incumbents’ share. Altogether, these shifts indicate that premium material value pools are capturing a rising share of the total Taiwan printed circuit board market.

By End-User Industry: Telecommunications Surges Ahead

Consumer Electronics still represents 36.98% of 2025 revenue, but Telecommunications and 5G applications are projected to compound at 7.11% through 2031, the fastest among all verticals. Data-center and HPC orders tied to AI inference workloads will push the segment’s share of the Taiwan PCB market size above 20% by 2031. Automotive demand remains highly sensitive to policy incentives, yet the long-term increase in content per electric vehicle sustains a healthy pipeline for IATF 16949-certified shops.

Industrial automation, renewable energy inverters, and healthcare imaging drive steady, margin-accretive demand for thick-copper and biocompatible boards. Aerospace and defense volumes are modest but deliver attractive pricing due to ITAR and MIL-STD compliance requirements. Overall, shifting end-user dynamics diversify revenue streams and reduce reliance on consumer devices, cushioning the Taiwan printed circuit board market against cyclical handset swings.

Geography Analysis

The Hsinchu and Taoyuan corridor accounts for roughly half of Taiwan's PCB market thanks to its proximity to TSMC’s packaging fabs, laminate suppliers, and precision-tool vendors. Co-location shortens prototype lead times from weeks to days, cementing Taiwan’s role as the preferred hub for advanced substrate development. Municipal incentives reimburse up to 15% of capital outlays for green facilities, reinforcing the geographic clustering effect.

Geopolitical risks associated with cross-strait tensions are driving companies to build operational redundancy. Unimicron, Zhen Ding, and Nan Ya PCB are actively setting up parallel production capacities in Thailand, Vietnam, and Poland to ensure uninterrupted delivery of shipments to their clients. Although these expansions result in additional fixed costs, they also enable the companies to capitalize on the growing local demand for automotive and consumer electronics printed circuit boards (PCBs).

Established clusters face the brunt of labor tightness, prompting some mid-tier producers to seek out inland counties where wages are more affordable. The Climate Change Response Act, emphasizing water-use reduction and carbon accounting, is steering the industry towards closed-loop rinsing and cogeneration. With the surge in environmental compliance costs, areas boasting established waste-treatment infrastructure are finding themselves at a competitive advantage.

Competitive Landscape

The top five domestic producers capture just under 50% of output, pointing to moderate concentration. Unimicron lifted 2024 revenue 25.1% on AI substrate orders, while Zhen Ding advanced 18.3% on flexible-circuit growth. Compeq and Tripod lean on automotive and smartphone contracts, respectively, whereas Nan Ya PCB pivots toward ABF substrates for 3 nm chips. Mainland Chinese rivals seize market share in rigid commodity boards, incentivizing Taiwanese leaders to prioritize substrates and HDI.

Strategic moves highlight the ongoing transformation within the industry. In January 2026, Unimicron announced an investment of USD 200 million to expand its ABF capacity, signaling its commitment to meeting growing demand. In December 2025, Zhen Ding secured a significant USD 500 million contract to supply AI server boards, further solidifying its position in the market. Kinsus entered into a collaboration with a Japanese materials company to jointly develop finer-line ABF technologies, showcasing its focus on innovation. Additionally, smaller players such as Gold Circuit Electronics are emphasizing the production of quick-turn prototypes as a strategy to differentiate themselves in an increasingly competitive landscape.

Process technology emerges as a pivotal arena. While tier-one houses leverage laser direct imaging and sequential lamination for 18-micron line widths, their mid-tier counterparts remain anchored to photolithography. Certifications like IATF 16949 and ISO 13485 pose significant hurdles for new entrants. Meanwhile, niches such as ceramic substrates for silicon-carbide power devices and ultra-thin flex for implants hint at potential shifts in future rankings.

Taiwan Printed Circuit Board Industry Leaders

Unimicron Technology Corporation

Zhen Ding Technology Holding Limited

Compeq Manufacturing Co., Ltd.

Nan Ya Printed Circuit Board Corporation

Kinsus Interconnect Technology Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Unimicron Technology will boost ABF substrate capacity 30% with a USD 200 million Taoyuan investment; initial output slated for Q3 2026.

- December 2025: Zhen Ding Technology signed a USD 500 million multiyear deal with a North American hyperscaler to supply AI server power boards, requiring dedicated Taoyuan lines.

- November 2025: Nan Ya PCB installed a sequential lamination line in Kunshan, China, increasing HDI capacity 20%; full ramp expected Q2 2026.

- October 2025: Kinsus Interconnect Technology partnered with a Japanese materials supplier to develop next-generation ABF substrates for 3 nm and 2 nm logic; pilot production H1 2026.

Taiwan Printed Circuit Board Market Report Scope

The Taiwan Printed Circuit Board Market Report is Segmented by PCB Type (Standard Multilayer (non-HDI), Rigid 1-2 Sided, High-Density Interconnect (HDI), Flexible Circuits (FPC), IC Substrates (Package Substrates), Rigid-Flex, Other PCB Types), Substrate Material (Glass Epoxy (FR-4), High-Speed Low-Loss, Polyimide (PI), Packaging Resins (BT / ABF), Other Substrate Materials), and End-user Industry (Consumer Electronics, Computing and Data Centers, Telecommunications and 5G, Automotive and EV, Industrial and Power, Healthcare / Medical, Aerospace and Defense, Other End-user Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Standard Multilayer (non-HDI) |

| Rigid 1-2 Sided |

| High-Density Interconnect (HDI) |

| Flexible Circuits (FPC) |

| IC Substrates (Package Substrates) |

| Rigid-Flex |

| Other PCB Types |

| Glass Epoxy (FR-4) |

| High-Speed / Low-Loss |

| Polyimide (PI) |

| Packaging Resins (BT / ABF) |

| Other Substrate Materials |

| Consumer Electronics |

| Computing and Data Centers |

| Telecommunications and 5G |

| Automotive and EV |

| Industrial and Power |

| Healthcare / Medical |

| Aerospace and Defense |

| Other End-user Industries |

| By PCB Type | Standard Multilayer (non-HDI) |

| Rigid 1-2 Sided | |

| High-Density Interconnect (HDI) | |

| Flexible Circuits (FPC) | |

| IC Substrates (Package Substrates) | |

| Rigid-Flex | |

| Other PCB Types | |

| By Substrate Material | Glass Epoxy (FR-4) |

| High-Speed / Low-Loss | |

| Polyimide (PI) | |

| Packaging Resins (BT / ABF) | |

| Other Substrate Materials | |

| By End-user Industry | Consumer Electronics |

| Computing and Data Centers | |

| Telecommunications and 5G | |

| Automotive and EV | |

| Industrial and Power | |

| Healthcare / Medical | |

| Aerospace and Defense | |

| Other End-user Industries |

Key Questions Answered in the Report

How large is the Taiwan PCB market in 2026?

The Taiwan PCB market size stands at USD 12.47 billion in 2026 and is projected to expand at a 5.32% CAGR to 2031.

Which PCB type is growing fastest in Taiwan?

Flexible Circuits lead growth with a forecast 6.87% CAGR through 2031, fueled by foldable smartphones and wearables.

What material segment is gaining share in high-speed data applications?

High-Speed Low-Loss laminates are projected to grow at 6.31% CAGR as 800G and 1.6T optics demand lower signal loss.

Why are IC substrates strategically important?

IC substrates enable heterogeneous integration in CoWoS and similar packages, command premium pricing, and benefit directly from TSMC’s capacity ramp.

How are Taiwanese PCB makers mitigating geopolitical risk?

Leading firms are adding redundant capacity in Thailand, Vietnam, and Poland to reassure multinational customers of supply continuity.

Page last updated on: