Taiwan HBM Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

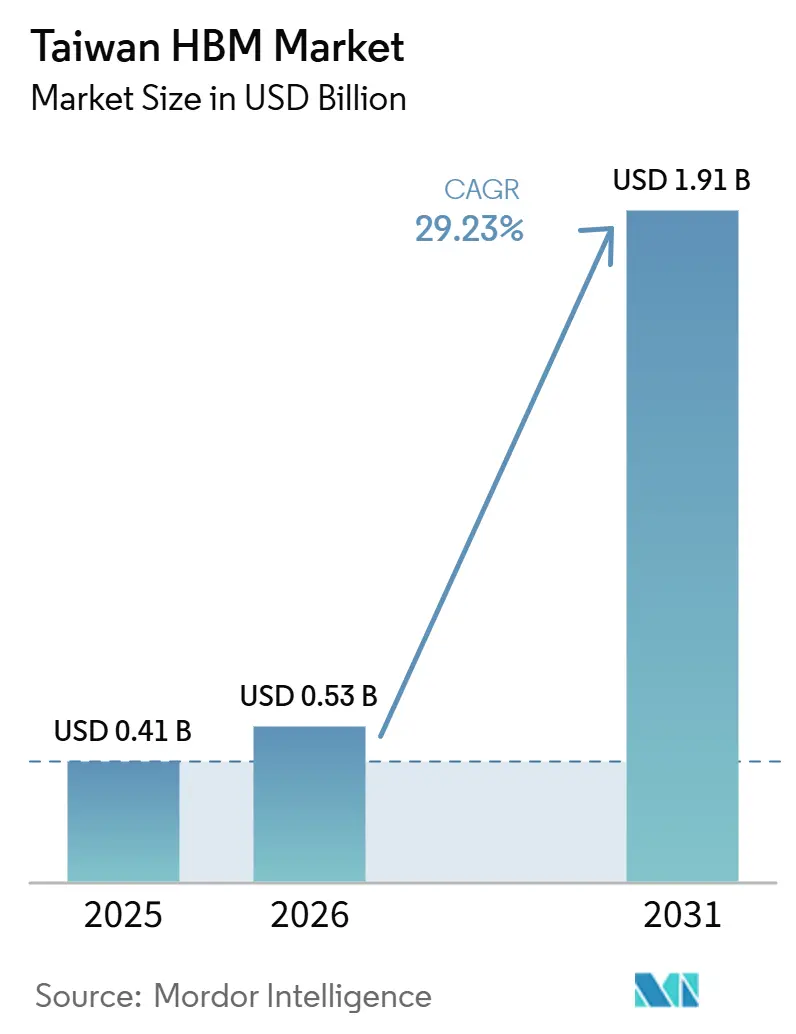

| Base Year Market Size (2025) | USD 0.41 Billion |

| Market Size (2026) | USD 0.53 Billion |

| Market Size (2031) | USD 1.91 Billion |

| Growth Rate (2026 - 2031) | 29.23% CAGR |

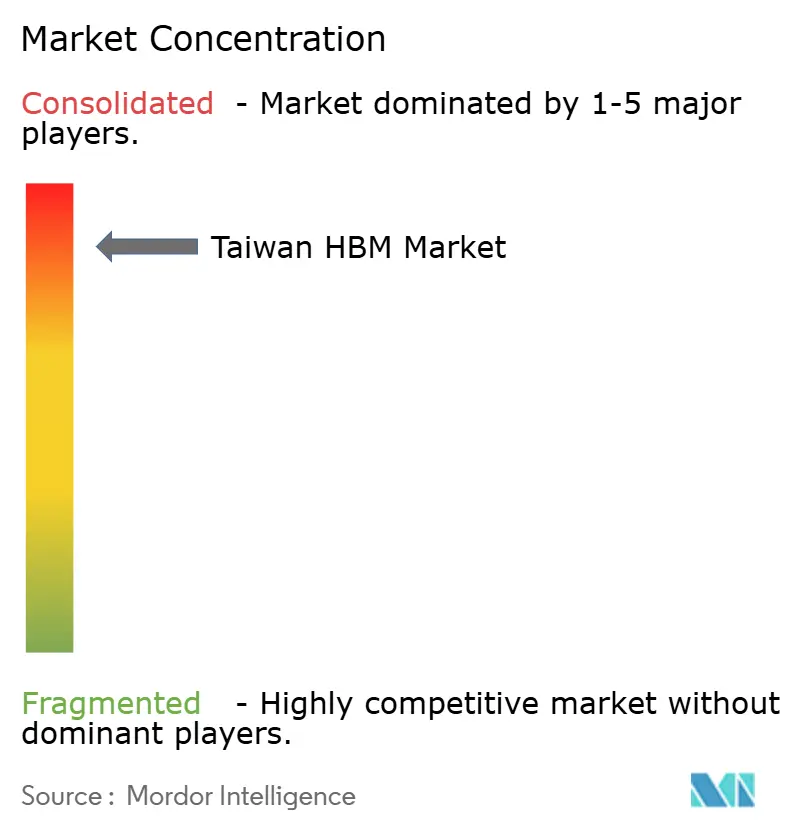

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Taiwan HBM Market Analysis by Mordor Intelligence

The Taiwan HBM market size was valued at USD 0.41 billion in 2025 and is projected to reach USD 1.91 billion by 2031, growing at a CAGR of 29.23% during 2026-2031. The expansion rests on Taiwan's role as the main advanced packaging base where imported HBM stacks are turned into finished AI accelerator modules for global deployment. Demand is rising because each new accelerator generation uses more memory capacity, higher bandwidth, and tighter processor-to-memory integration than the last one. The revenue pool is centered on packaging conversion rather than memory fabrication, which gives Taiwan a strong position in value capture but also keeps it exposed to upstream supply concentration among foreign memory vendors. Companies are responding with aggressive capacity additions, longer equipment commitments, and closer partnerships with hyperscalers and chip designers that need secure packaging access. The outlook remains strong, but the pace of expansion will still depend on how quickly packaging bottlenecks ease, how HBM4 moves into wider production programs, and how much of the future package mix stays within the current interposer-led model.

Key Report Takeaways

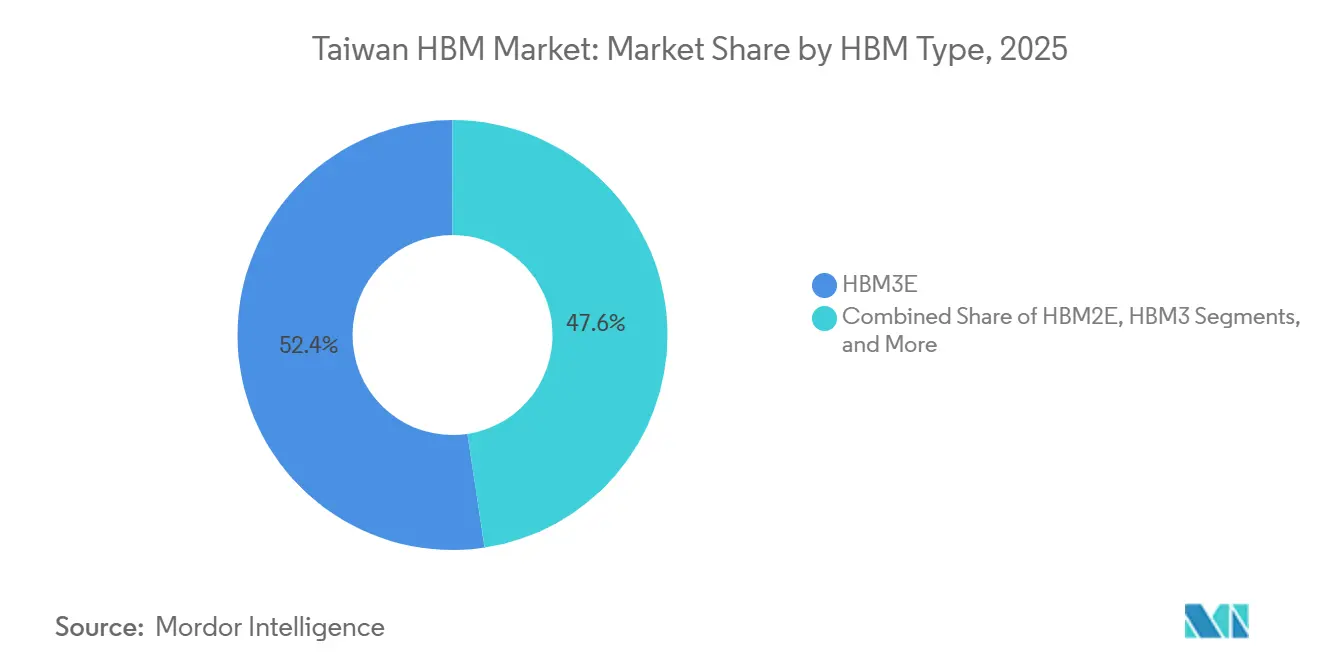

- By HBM type, HBM3E held 52.38% of the Taiwan HBM market share in 2025, while HBM4 is projected to expand at a 30.01% CAGR through 2031.

- By technology node, 1β and beyond accounted for 47.51% of the market in 2025 and is projected to grow at a 29.89% CAGR through 2031.

- By end use industry, data centers accounted for 87.59% of the Taiwan HBM market size in 2025 and are projected to expand at a 30.18% CAGR through 2031.

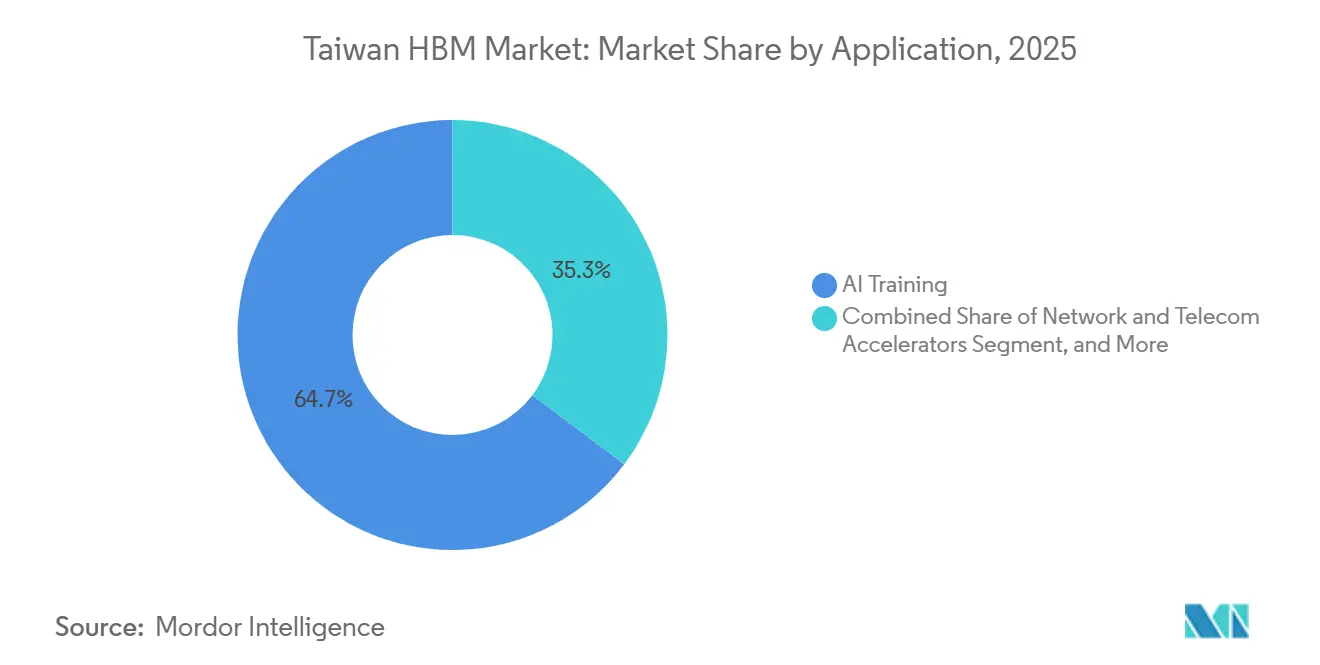

- By application, AI training led with 64.73% share in 2025, while AI inference is projected to grow at a 30.09% CAGR through 2031.

- By packaging type, 2.5D interposer-based packaging commanded 87.54% share in 2025, while hybrid and next-generation advanced packaging is projected to advance at a 29.77% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Taiwan HBM Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| CoWoS Capacity Expansion in Taiwan | +7.5% | Taiwan, Hsinchu, Taoyuan, Southern Science Park, Chiayi | Short term (≤ 2 years) |

| Rising HBM Content Per AI Accelerator | +6.2% | Global, concentrated in Taiwan as packaging hub | Medium term (2-4 years) |

| HBM4 Qualification and Migration Cycle | +4.1% | Global supply chain, Taiwan packaging integration | Short term (≤ 2 years) |

| Hyperscaler and ASIC Demand Pull | +3.5% | Global demand, captured through Taiwan supply chain | Medium term (2-4 years) |

| Local Advanced Packaging Ecosystem Density | +1.5% | Taiwan-centric, with spillover to Singapore and Japan | Long term (≥ 4 years) |

| Taiwan-Based Memory R&D Localization | +1.0% | Taiwan, Taichung, Miaoli, Hsinchu, Zhudong | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

CoWoS Capacity Expansion in Taiwan

CoWoS capacity expansion is the strongest near-term force inside the Taiwan HBM market because revenue is recognized only when HBM and processors move through qualified packaging lines at scale. TSMC's CoWoS output rose sharply from 2023 through 2025, and the company is targeting another step up by the end of 2026 as multiple sites ramp in parallel. The company said in May 2026 that CoWoS yield had exceeded 98% and that annual technology updates would continue for the next 5 years, which lowers execution risk as volume rises. New capacity in southern Taiwan and Chiayi matters because it converts booked customer demand into billable packaging activity without waiting for new end uses to emerge. This keeps utilization high and provides the Taiwan HBM market a direct path from capex deployment to revenue capture once allocations are committed. The practical result is that new tools do not need to create demand; they mainly need to catch up with demand that already exists across AI infrastructure programs.

Rising HBM Content Per AI Accelerator

Rising HBM content per AI accelerator lifts the Taiwan HBM market even when shipment growth is uneven because each unit now carries far more memory than earlier generations did. NVIDIA's B200 GPU integrates 192GB of HBM3E across 8 stacks, and the GB200 NVL72 system carries 13.4TB of HBM3E across 72 GPUs NVIDIA. That shift means a stable number of accelerator shipments can still generate more packaging cycles, more substrate requirements, and more testing steps across Taiwan's supply chain. The effect is structural because memory density is tied to model size, throughput targets, and power efficiency rather than to temporary promotional demand. As customers move from one accelerator generation to the next, Taiwan captures a larger portion of the total hardware value that must pass through advanced packaging. This is why the Taiwan HBM market benefits from architecture decisions made by chip designers even before new fabs or new end markets appear.

HBM4 Qualification and Migration Cycle

The HBM4 migration cycle is adding a fresh layer of demand to the Taiwan HBM market because it combines a memory generation shift with new packaging and process requirements. Samsung said in February 2026 that it started mass production and commercial shipments of HBM4, using a 4nm logic base die and transfer speeds of 11.7 Gbps with capability up to 13 Gbps. This matters because Taiwan captures not only packaging revenue but also more foundry-linked activity when the base die sits closer to the local ecosystem. Qualification work also pulls customers into earlier planning cycles, which helps secure capacity and deepen ties between memory suppliers, foundries, and packaging firms. As HBM4 volume rises, the Taiwan HBM market stands to benefit from both a richer process mix and a faster commercial refresh cycle.

Hyperscaler and ASIC Demand Pull

Demand from hyperscalers and custom accelerator programs is widening the customer base for the Taiwan HBM market beyond a single GPU roadmap. Cloud and platform companies now need secure HBM access for both training clusters and production inference systems, which increases the number of programs that depend on Taiwan's packaging footprint. NVIDIA's supply-chain spending in Taiwan climbed to USD 100-150 billion by May 2026, which shows the scale of infrastructure commitments already flowing through the local semiconductor base. AMD also said in May 2026 that it would invest more than USD 10 billion across Taiwan's ecosystem, with advanced packaging and interconnect collaboration named as priority areas.[1]AMD, “AMD Announces More Than $10 Billion in Taiwan Ecosystem Investments to Accelerate AI Infrastructure,” GlobeNewswire, globenewswire.com This broader customer mix improves demand visibility because delays in one program are less likely to freeze the full revenue stream. It also makes the Taiwan HBM market more resilient, since capacity can be redirected across GPU, ASIC, and mixed-accelerator projects rather than being tied to a single narrow buyer group.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advanced Packaging Bottlenecks | -3.8% | Taiwan-centric, with spillover to OSAT partners regionally | Short term (≤ 2 years) |

| High Qualification and Yield Risk | -2.4% | Global HBM supply chain, Taiwan integration node most exposed | Medium term (2-4 years) |

| Supplier Concentration in Upstream HBM Supply | -1.6% | Korea-origin risk, realized through Taiwan's packaging dependency | Medium term (2-4 years) |

| Export Control and Customer Allocation Constraints | -1.2% | Global, particularly affecting allocations through Taiwan to end markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Advanced Packaging Bottlenecks

Advanced packaging bottlenecks remain the most immediate break on the Taiwan HBM market because qualified tool capacity expands more slowly than customer demand. CoWoS lines require long equipment lead times, tight process control, synchronized substrate and test availability, so capacity additions do not translate into usable output right away. TSMC and Amkor announced a 10-year partnership in June 2026 to expand advanced packaging and testing in Arizona, which shows how customers are looking for extra capacity corridors outside Taiwan even though local execution stays central. The bottleneck also affects pricing and allocation because customers with earlier commitments or stronger relationships can secure access before smaller programs do. Overflow demand gives OSAT partners more room to participate, but it does not remove the basic constraint at the leading edge where most high-value packages are qualified. Until equipment, substrates, and trained labor scale together, the Taiwan HBM market will keep growing below the level that end demand alone would justify.

High Qualification and Yield Risk

High qualification and yield risk is the second major restraint because taller stacks, finer interconnects, and tighter thermal conditions make each HBM generation harder to commercialize at scale. The challenge grows when defects from memory production appear only after a stack reaches advanced packaging, because that can turn expensive interposers and logic die into scrap. Samsung's shift to commercial HBM4 and the broader move toward more advanced base-die integration show how much tighter the process window has become. Export control rules from the U.S. Bureau of Industry and Security also add compliance friction for parts of the value chain, especially when customers serve restricted destinations. For Taiwan, this means packaging economics still depend in part on upstream discipline at memory vendors outside the island. The Taiwan HBM market therefore carries execution risk that is not fully visible in capacity figures alone.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By HBM Type: HBM3E Leads Current Revenue While HBM4 Drives the Next Expansion Cycle

HBM3E captured 52.38% of the Taiwan HBM market share in 2025, which made it the commercial base for current revenue and the format around which most near-term packaging plans were organized. Its lead came from sustained demand for NVIDIA's Blackwell platform and from large customers securing supply and packaging allocations before many systems entered full deployment. The segment also benefited from the practical advantage of being a proven format, because buyers needed immediate volume rather than waiting for the next memory generation to mature. This kept legacy transitions orderly, with HBM2E and HBM3 still serving maintenance needs and selected mid-tier accelerator programs during the changeover period. In effect, HBM3E gave the Taiwan HBM market a stable operating core as the broader AI hardware cycle accelerated.

HBM4 is projected to expand at a 30.01% CAGR through 2031, making it the main growth engine in the Taiwan HBM market over the forecast period. Samsung said in February 2026 that it began mass production and commercial shipments of HBM4, which confirms that the segment has moved from roadmap discussion to commercial execution. The transition matters for Taiwan because every new memory generation increases the need for fresh qualification work, tighter packaging coordination, and closer alignment with processor release schedules. It also raises the value of local integration capabilities, since base-die work, packaging flow changes, and thermal management become more important as stack complexity increases. As a result, the Taiwan HBM industry is not only handling higher volumes, it is also processing a richer mix of technical work as HBM4 gains ground.

By Technology Node: Leading-Edge DRAM Processes Reinforce Growth and Local Value Capture

The 1β and beyond segment accounted for 47.51% of the Taiwan HBM market in 2025 and is forecast to grow at a 29.89% CAGR through 2031, indicating that the leading node is also the strongest growth center. This pattern indicates that buyers are actively moving toward the most advanced DRAM processes rather than simply maintaining a legacy mix with incremental improvement. Leading-edge nodes matter because they support the higher bandwidth density and power efficiency that recent AI accelerators require at both rack and cluster scale. Older nodes remain relevant for cost-sensitive programs and some mid-range workloads, but their role is narrowing as customer roadmaps settle around HBM3E and HBM4. The Taiwan HBM market, therefore, benefits when the technology mix shifts upward, because the highest-value packaging and integration work sits closest to the leading edge.

The second layer of growth comes from the HBM4 base die, which draws Taiwan further into the product's technical core rather than leaving the island focused only on packaging conversion. SK hynix said in April 2024 that it partnered with TSMC to strengthen HBM leadership through base-die collaboration for HBM4, which anchors more foundry activity in Taiwan.[2]SK hynix, “SK Hynix Partners With TSMC to Strengthen HBM Technological Leadership,” SK hynix Newsroom, news.skhynix.com That change adds a new revenue stream inside the Taiwan HBM market because process migration at the memory layer now pulls in more logic-related work from local suppliers. It also shortens the gap between technology transition and commercial capture, since each node step can create foundry and packaging demand in parallel. The Taiwan HBM industry thus becomes more exposed to fast refresh cycles, but it also gains more ways to monetize each generational shift.

By End Use Industry: Data Centers Keep Their Dominant Position and Set the Growth Pace

Data centers accounted for 87.59% of the Taiwan HBM market in 2025, and the same segment is projected to grow at a 30.18% CAGR through 2031, making it both the largest and fastest-growing end use. The segment dominates because AI training clusters, inference clusters, and rack-scale server systems consume far more HBM per deployment than other electronics categories. NVIDIA's GB200 NVL72 platform alone integrates 13.4TB of HBM3E across 72 GPUs, which illustrates how quickly memory demand compounds at the system level. This concentration keeps the Taiwan HBM market closely linked to hyperscaler capex, cloud buildouts, and accelerator launch schedules. It also helps explain why packaging access and customer allocation decisions matter so much, since a small number of large programs can absorb a very large share of qualified capacity.

The rest of the market, including consumer electronics, automotive electronics, and telecommunications infrastructure, is smaller today but still important for the next stage of diversification. These areas reflect where premium graphics, edge AI, and advanced in-vehicle compute may drive incremental demand as HBM-linked architectures spread beyond the largest data center deployments. Taiwan's government is also backing a broader semiconductor base through policies that reinforce the island's strategic position in AI-era supply chains. That support does not change the current concentration, but it strengthens the longer-term operating base of the Taiwan HBM market as new end uses develop.

By Application: Training Anchors Current Demand While Inference Broadens the Revenue Base

AI training accounted for 64.73% of the Taiwan HBM market in 2025, maintaining its leading position, as frontier model development still depends on very high memory bandwidth and capacity. The application remains central because training large models requires dense memory access across many accelerators, and that design logic continues to support HBM-heavy systems. HPC servers, graphics, and visualization provide a meaningful secondary demand layer, especially where performance needs are high, and memory throughput directly affects output quality or runtime. Network and telecom accelerators remain small, yet they matter because AI processing is moving toward more distributed infrastructure rather than solely centralized clusters. Together, these patterns keep the Taiwan HBM market rooted in high-performance compute even as the mix inside that compute base changes.

AI inference is forecast to grow at a 30.09% CAGR through 2031, making it the fastest-expanding application in the Taiwan HBM market. The reason is that inference moves from limited trials to persistent production use, where many deployed systems need stable memory throughput and low response times every day. That shift broadens demand beyond a handful of major training clusters and creates a larger installed base of hardware that still needs advanced memory. It also improves revenue resilience because inference deployments are spread across more customers, more facilities, and more refresh cycles than single buildout programs. For the Taiwan HBM market, this means growth will depend not only on headline training clusters but also on the steady operational scaling of commercial AI services.

By Packaging Type: Interposer-Based Packaging Dominates Today While New Formats Build a Future Option Set

The 2.5D interposer-based packaging segment commanded 87.54% of the Taiwan HBM market share in 2025, underscoring how deeply current AI accelerators still rely on the CoWoS-centered integration model. This segment leads because it is already qualified for the highest-value processor and HBM combinations, and customers prefer a proven route when deployment schedules are tight. The model also reinforces Taiwan's role, as the most advanced packages require close coordination among foundry, packaging, test, substrate, and equipment teams within the same ecosystem. TSMC said in May 2026 that it planned annual CoWoS updates for the next 5 years and was targeting a 14x reticle-size version with 20 HBM stacks in 2028. That roadmap extends the life of the dominant architecture and keeps it at the center of near-term revenue capture in the Taiwan HBM market.

Hybrid and next-generation advanced packaging is projected to grow at a 29.77% CAGR through 2031, making it the main emerging format despite starting from a smaller base. Its appeal comes from the opportunity to reduce costs, expand format flexibility, and serve programs that may not require the full complexity of today's interposer-heavy approach. AMD said in May 2026 that it would invest more than USD 10 billion across Taiwan's semiconductor ecosystem, including collaboration with ASE, SPIL, and Powertech on next-generation interconnect and panel-based EFB processes. Those efforts show that the Taiwan HBM industry is building alternative packaging options before customers demand a large-scale shift away from the current leader. The result is a market structure where today's revenue remains concentrated, but tomorrow's competitive pressure is already taking shape inside the same ecosystem.

Geography Analysis

Taiwan accounted for the full Taiwan HBM market in 2025, and most of that value was concentrated in a few science park corridors where packaging, test, substrate, and foundry assets were tightly clustered. Hsinchu remained the core decision center for advanced packaging operations, while Taoyuan, central Taiwan, Chiayi, and southern science parks supported production expansion and adjacent supply work. This clustering matters because qualification cycles are faster when equipment vendors, substrate makers, OSAT sites, and foundry teams can coordinate within the same operating network. The Taiwan HBM market also benefits from lower logistics friction under this model, since sensitive components move shorter distances between manufacturing stages. Micron said its cumulative investment in Taiwan had reached TWD 1.4 trillion (USD 43.88 billion) by January 2026, indicating that memory-related activity on the island extends beyond packaging support alone.

Taiwan sits at the integration point of a triangular supply structure that connects Korean and U.S. memory suppliers, U.S. chip designers, and Taiwan-based packaging and test lines. HBM stacks from SK hynix, Samsung, and Micron are shipped to Taiwan for assembly with GPUs and custom accelerators, after which they are delivered as deployable AI hardware for global infrastructure programs. That conversion role gives the Taiwan HBM market a strong claim on value-added activity, even though the underlying DRAM wafers are largely made outside the island. TSMC and Amkor signed a 10-year partnership in June 2026 to expand advanced packaging and testing in Arizona, which shows that customers want a secondary footprint while still relying on Taiwan for present scale.[3]Amkor Technology, “TSMC and Amkor Technology Announce Long Term Partnership to Accelerate Advanced Packaging in the United States,” Amkor Technology Investor Relations, ir.amkor.com Even with that push, equivalent density outside Taiwan will take time because other regions still need to assemble several separate capabilities that already coexist in one place on the island.

Within Taiwan, the north retains deep test and substrate density, while the south is taking the heaviest CoWoS expansion and newer large-scale packaging investment. Miaoli is becoming more important as Micron expands the Tongluo cluster for advanced DRAM and HBM-related production activity, which adds a new layer to the geographic map. This regional specialization helps the Taiwan HBM market because each area contributes a different operational strength instead of competing over the same narrow function. The end result is an ecosystem that is compact enough for fast execution and broad enough to absorb future shifts in packaging, test, and memory-related workloads.

Competitive Landscape

The Taiwan HBM market is concentrated at the packaging integration tier, but less so in substrates, test, materials, and support services. TSMC holds the strongest position because leading-edge CoWoS remains the main qualified route for combining advanced processors with HBM at commercial scale. The company said in May 2026 that CoWoS yield had exceeded 98% and that annual technology updates would continue for the next 5 years, reinforcing its operating lead. This gives large customers a clear reason to secure capacity early, since substitution options at the very top end remain limited. It also means pricing power and customer access are shaped more by qualified capacity than by the number of participants listed across the broader chain.

Below TSMC, the field includes ASE Technology Holding, SPIL, Powertech Technology, and other OSAT players that support overflow packaging, test, fan-out development, and adjacent assembly work. These companies matter because the Taiwan HBM market needs more than one capacity layer, especially when demand spikes beyond what a single packaging route can absorb. AMD's May 2026 plan to invest more than USD 10 billion across Taiwan, including collaborations with ASE, SPIL, and Powertech, shows how customers are actively building a broader partner base to meet next-generation packaging needs. Micron's Tongluo expansion and Samsung's HBM4 commercial rollout also show that memory suppliers are moving faster to secure their position around the same AI infrastructure cycle. These moves expand the support structure around the Taiwan HBM market without changing the fact that the highest-value integration work remains concentrated.

The main strategic patterns are early capacity reservation, deeper collaboration across memory, foundry, and packaging layers, and selective geographic diversification. The TSMC-Amkor Arizona partnership shows the diversification track, while the SK hynix-TSMC base-die partnership shows how technical coordination is becoming a competitive tool in its own right.[4]SK hynix, “SK Hynix Partners with TSMC to Strengthen HBM Technological Leadership,” SK hynix Newsroom, news.skhynix.com This creates a landscape where leadership depends on know-how, yield discipline, and customer qualification status as much as on simple factory scale. Smaller players still have openings in lower-cost package formats, substrate support, and specialized testing, but the center of value in the Taiwan HBM market remains tightly held.

Taiwan HBM Industry Leaders

NVIDIA Corporation

Taiwan Semiconductor Manufacturing Company Limited

Micron Technology, Inc.

SK hynix Inc.

Samsung Electronics Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: TSMC and Amkor Technology signed a 10-year agreement to expand advanced semiconductor packaging and testing in Arizona, with TSMC procuring packaging and test services from Amkor's USD 7 billion Peoria campus targeting 2028 output. The deal codified a long-term capacity-sharing model intended to create a complete U.S.-based supply chain for AI chip assembly.

- May 2026: AMD announced more than USD 10 billion in investments across Taiwan's semiconductor ecosystem, including collaboration with ASE and SPIL on next-generation wafer-based 2.5D Elevated Fanout Bridge interconnect technology and qualification of the industry's first panel-based EFB process with Powertech.

- April 2026: Global Unichip Corporation demonstrated a 12 Gbps HBM4 IP platform at the TSMC 2026 North America Technology Symposium, integrating a full-function HBM4 controller and PHY IP with partner HBM4 memory via TSMC CoWoS on the N3P process. HBM4E IP targeting 16 Gbps was announced for Q2 2026 release.

- March 2026: Micron Technology completed its USD 1.8 billion acquisition of PSMC's Tongluo P5 semiconductor facility in Miaoli County, Taiwan, immediately initiating cleanroom retrofitting for advanced DRAM and HBM production. Construction of a second comparable facility at the same campus is scheduled to begin before the end of fiscal 2026, doubling the site's cleanroom area.

Taiwan HBM Market Report Scope

The Taiwan HBM Market refers to the market for high-bandwidth memory (HBM) products and related solutions in Taiwan. The market scope includes HBM technologies, components, and applications across industries such as data centers, artificial intelligence, high-performance computing, graphics processing, and advanced semiconductor manufacturing.

The Taiwan HBM Market Report is segmented by HBM type (HBM2E, HBM3, HBM3E, and HBM4), Technology Node (1X/1Y Nodes, 1Z Node, 1α (1-Alpha), and 1β and Beyond), End Use Industry (Data Centers, Consumer Electronics, Automotive Electronics, Telecommunication Infrastructure, and Other End-User Industries), Application (AI Training, AI Inference, HPC Servers, Graphics and Visualization, and Network and Telecom Accelerators) and Packaging Type (2.5D Interposer-Based Packaging, Fan-Out Advanced Packaging, and Hybrid/Next-Generation Advanced Packaging). The Market Forecasts are Provided in Terms of Value (USD).

| HBM2E |

| HBM3 |

| HBM3E |

| HBM4 |

| 1X/1Y Nodes |

| 1Z Node |

| 1α (1-Alpha) |

| 1β and Beyond |

| Data Centers |

| Consumer Electronics |

| Automotive Electronics |

| Telecommunication Infrastructure |

| Other End-User Industries |

| AI Training |

| AI Inference |

| HPC Servers |

| Graphics and Visualization |

| Network and Telecom Accelerators |

| 2.5D Interposer-Based Packaging |

| Fan-Out Advanced Packaging |

| Hybrid/Next-Generation Advanced Packaging |

| By HBM Type | HBM2E |

| HBM3 | |

| HBM3E | |

| HBM4 | |

| By Technology Node | 1X/1Y Nodes |

| 1Z Node | |

| 1α (1-Alpha) | |

| 1β and Beyond | |

| By End Use Industry | Data Centers |

| Consumer Electronics | |

| Automotive Electronics | |

| Telecommunication Infrastructure | |

| Other End-User Industries | |

| By Application | AI Training |

| AI Inference | |

| HPC Servers | |

| Graphics and Visualization | |

| Network and Telecom Accelerators | |

| By Packaging Type | 2.5D Interposer-Based Packaging |

| Fan-Out Advanced Packaging | |

| Hybrid/Next-Generation Advanced Packaging |

Key Questions Answered in the Report

What is the current size and outlook for the Taiwan HBM market?

The Taiwan HBM market size was USD 0.41 billion in 2025 and is projected to reach USD 1.91 billion by 2031 at a 29.23% CAGR during 2026-2031.

Why do data centers dominate HBM demand in Taiwan?

Data centers held 87.59% of demand in 2025 because AI training and inference systems use very large memory capacity per server and per rack.

Which HBM type leads today, and which one is growing fastest?

HBM3E led with 52.38% share in 2025, while HBM4 is projected to post the fastest growth at a 30.01% CAGR through 2031.

Why is CoWoS capacity so important for future growth?

Taiwan captures much of its value through advanced packaging conversion, so added CoWoS capacity directly affects how much booked HBM demand can be turned into shipped AI hardware.

What is the biggest near-term risk to expansion?

Advanced packaging bottlenecks are the most immediate risk because tool lead times, substrate availability, and labor readiness can delay usable output even when end demand stays strong.

How are leading companies adjusting their strategies in Taiwan?

TSMC is expanding CoWoS and updating the platform annually, AMD is backing multiple packaging partners with more than USD 10 billion of ecosystem investment, and Amkor and TSMC are building an additional U.S. packaging path.

Page last updated on: