Taiwan Electronics Manufacturing Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

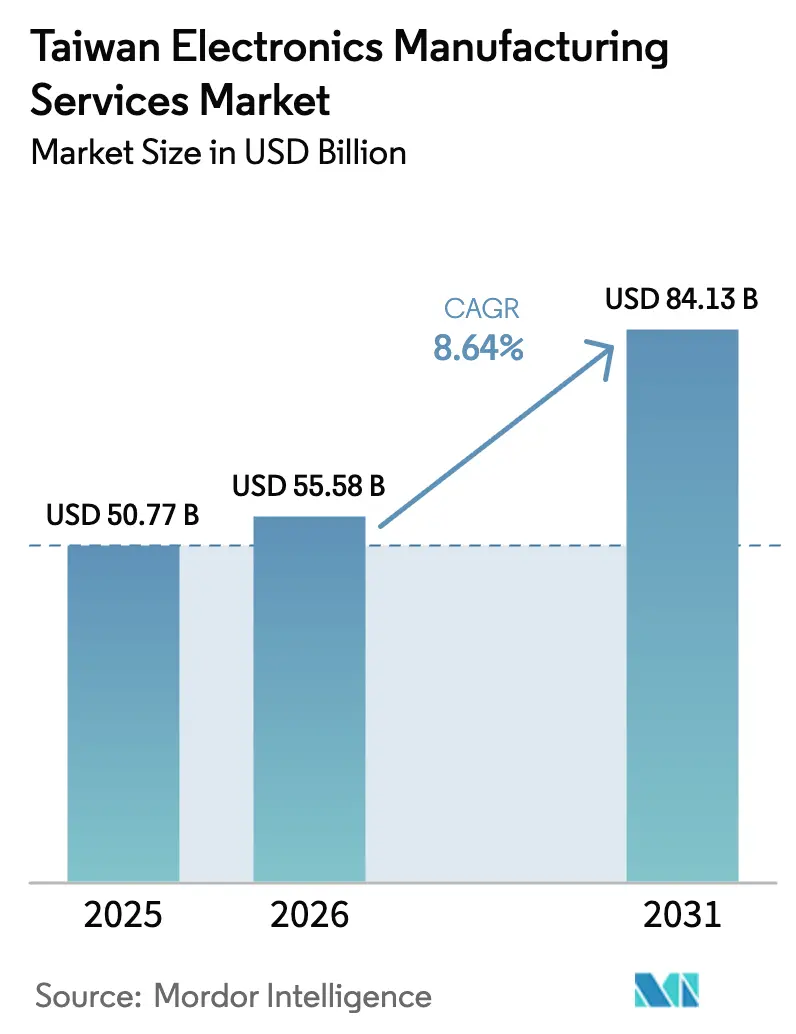

| Base Year Market Size (2025) | USD 50.77 Billion |

| Market Size (2026) | USD 55.58 Billion |

| Market Size (2031) | USD 84.13 Billion |

| Growth Rate (2026 - 2031) | 8.64% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Taiwan Electronics Manufacturing Services Market Analysis by Mordor Intelligence

The Taiwan electronics manufacturing services market size in 2026 is estimated at USD 55.58 billion, growing from 2025 value of USD 50.77 billion with projections showing USD 84.13 billion, growing at 8.64% CAGR over 2026-2031. The growth reflects the island’s shift toward complex applications such as AI servers, automotive domain controllers, and low-earth-orbit satellite payloads. Capital is moving from high-volume consumer devices to lower-volume, higher-margin programs that reward engineering depth and process control. While the island still accounts for roughly 40% of global notebook production and 25% of smartphone production, those shares are slipping as brand owners diversify production to Southeast Asia to hedge geopolitical risk. Profit resilience depends on how quickly incumbents scale advanced packaging, turnkey design services, and vertically integrated offerings that shorten time-to-market for global brands.

Key Report Takeaways

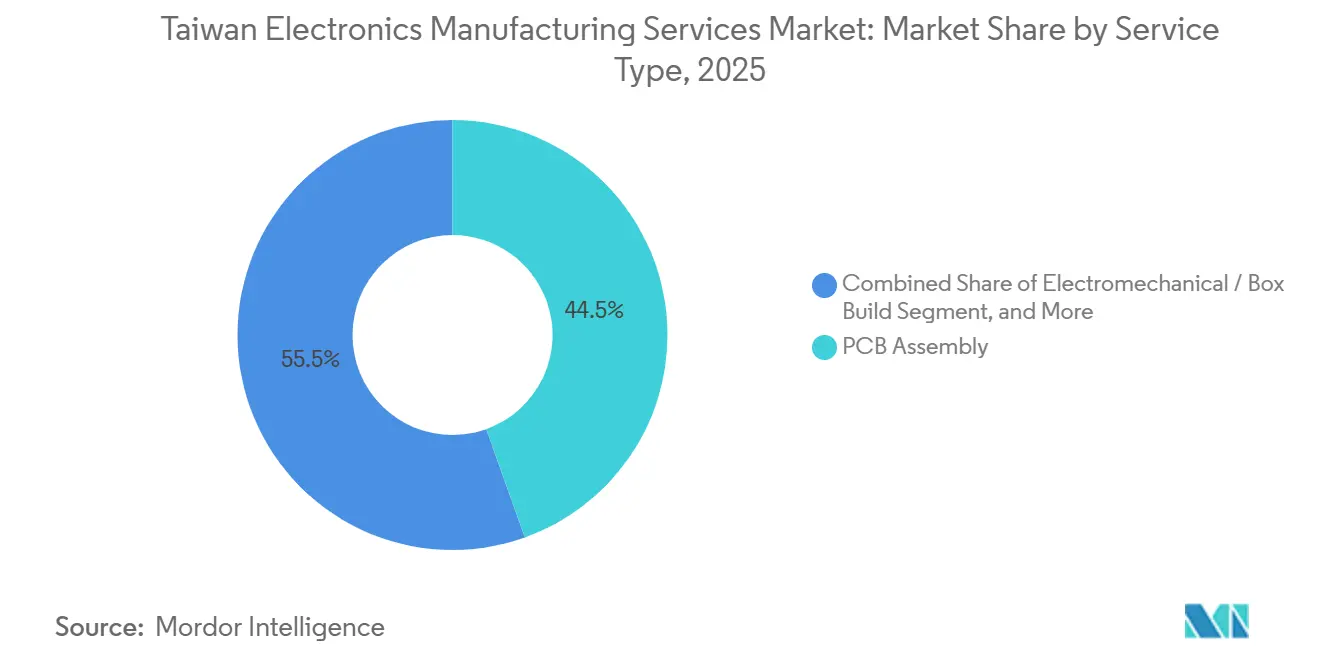

- By service type, PCB Assembly led with 44.52% of the Taiwan EMS market share in 2025; Electromechanical and Box Build services are forecast to expand at a 9.66% CAGR through 2031.

- By business model, Contract Manufacturing held 61.26% of the Taiwan EMS market share in 2025, while Hybrid and Turnkey models are projected to grow at a 9.21% CAGR to 2031.

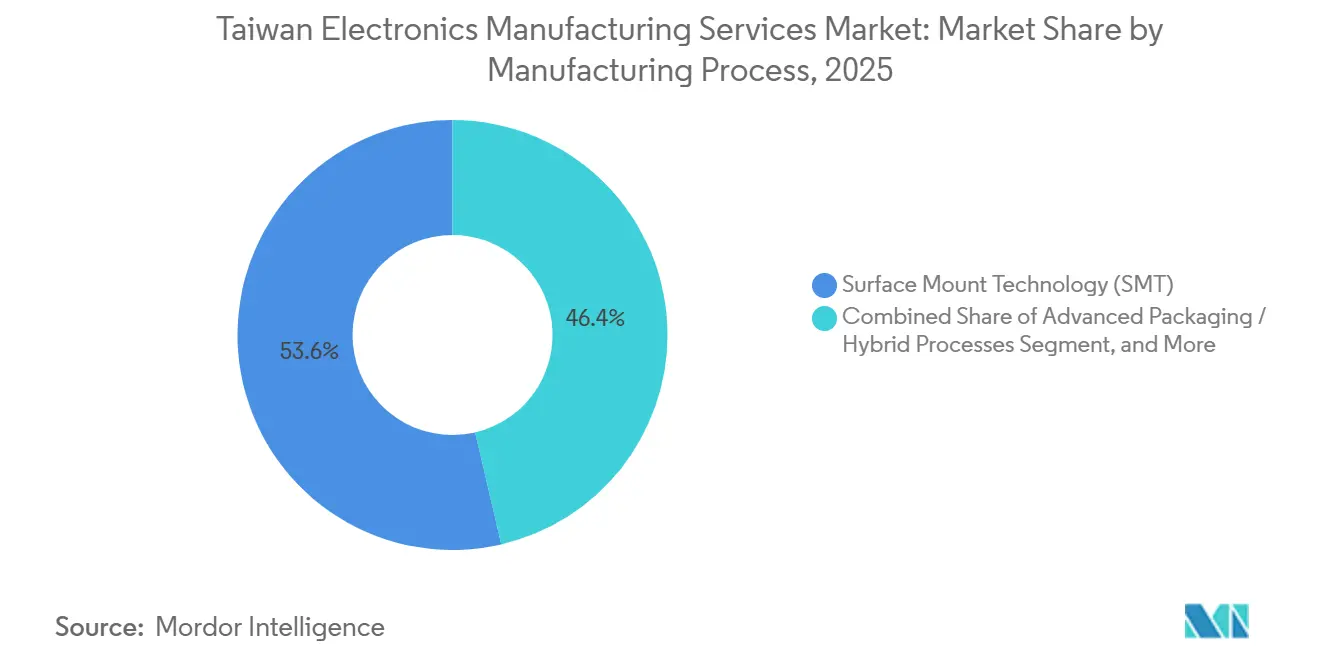

- By manufacturing process, Surface Mount Technology accounted for 53.64% of the Taiwan EMS market in 2025, and Advanced Packaging and Hybrid Processes are advancing at a 9.27% CAGR through 2031.

- By end-user, Consumer Electronics commanded 33.67% of the Taiwan EMS market share in 2025; Automotive is forecast to expand at a 10.39% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Taiwan contributes to a system defined not by any single country or region but by the interaction of many. The global electronics manufacturing services market data by Mordor Intelligence represents that combined structure.

Taiwan Electronics Manufacturing Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating 5G Handset Design Wins | +1.2% | Global, concentrated in Taiwan and China | Short term (≤ 2 years) |

| Growing Demand for Advanced PCB Assembly | +1.8% | Global, Taiwan core with spill-over to Asia-Pacific | Medium term (2-4 years) |

| Government Incentives for Reshoring | +1.0% | Taiwan national, early gains in Hsinchu, Taichung | Medium term (2-4 years) |

| Mainstreaming of Automotive Electronics | +2.1% | Global, strongest in North America and EU | Long term (≥ 4 years) |

| Rise of Low-Orbit Satellite Sub-Assemblies | +0.9% | Global, Taiwan and United States collaboration zones | Long term (≥ 4 years) |

| Expansion of Smart Factory Retrofits | +0.7% | Taiwan national, pilot sites in Taoyuan, Tainan | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerating 5G Handset Design Wins

Taiwanese EMS houses won design mandates for almost 180 million 5G smartphones in 2025, up from 140 million the year before, because brands needed suppliers that could integrate millimeter-wave antenna-in-package modules and vapor-chamber thermal solutions inside sub-7 mm profiles.[1]Foxconn Technology Group, “Investor Relations Presentation 2025,” FOXCONN.COM Foxconn and Pegatron installed automated optical inspection lines that pair real-time impedance testing with defect analytics, cutting ramp cycles from 12 weeks to 8 and pushing defect escape rates below 50 ppm. The shift toward standalone 5G core networks in North America and Europe is also lifting demand for small-cell base-station modules, a niche where Taiwanese providers own RF front-end integration IP. Regulatory pressure from 3GPP Release 17 and the U.S. FCC over-the-air testing rules raises the qualification bar, locking out less-capable competitors. Although volume growth moderates once global 5G penetration tops 70%, EMS firms expect to defend margins by layering software validation and field-failure analytics on each handset platform.

Growing Demand for Advanced PCB Assembly Capabilities

Artificial-intelligence accelerator cards and high-bandwidth-memory modules consumed 35% of Taiwan’s advanced PCB assembly capacity in 2025, up from 22% in 2023, as hyperscale operators scrambled for next-generation training clusters. Substrate supplier Unimicron reported order backlogs running into late-2026 and lifted ABF substrate prices by 18% because tighter layer counts pulled yields below 80%.[2]Unimicron Technology Corp., “Annual Report 2025,” UNIMICRON.COM EMS integrators responded with placement machines that handle 0.3 mm pitches and real-time X-ray laminography, services that command 12-15% price premiums over standard SMT lines. Capacity bottlenecks have shifted to chip-on-wafer-on-substrate and fan-out wafer-level packaging, prompting joint ventures between EMS firms and OSAT leaders to secure slots. Compliance with IPC-6012 Class 3 and AEC-Q100 rules now adds eight to 12 weeks to new-product introduction, but also raises switching costs, reinforcing Taiwan’s pricing power.

Government Incentives for High-End Manufacturing Reshoring

Taiwan’s Advanced Manufacturing Promotion Act grants tax credits covering up to 25% of capital spending on smart factories, advanced packaging, and carbon-neutral processes, drawing TWD 180 billion (USD 5.8 billion) in commitments during 2025.[3]Ministry of Economic Affairs, “Advanced Manufacturing Promotion Act Incentives,” MOEA.GOV.TW Early adopters in Hsinchu and Taichung installed cyber-physical production lines that cut changeover times by 60% and lowered scrap by 15%, reinforcing the island’s edge in high-mix, low-volume work. The incentives accelerate rooftop solar, battery storage, and renewable PPAs, helping EMS firms offset rising carbon fees that will triple by 2030. Industry lobbies are already pushing to extend the program beyond its 2030 sunset to match U.S. and EU subsidy regimes. By lowering after-tax hurdle rates, the scheme tilts new investment toward Taiwan even as brands diversify volume production to Southeast Asia.

Mainstreaming of Automotive Electronics in Taiwan’s Tier-1 Supply Chain

Shipments of automotive electronic control units from Taiwan rose 28% year-on-year to 42 million in 2025, reflecting OEM efforts to diversify away from slower-moving European tier-ones. Foxconn’s joint venture with Stellantis will deliver 2 million zonal domain controllers annually by 2028, consolidating up to 70 traditional ECUs into five modules and trimming wiring mass by 30 kg per vehicle. Lite-On and Delta Electronics leveraged power-electronics portfolios to win on-board charger and traction inverter programs that carry 18-22% gross margins, well above consumer-device averages. ISO 26262 ASIL-D and UNECE battery-safety rules elevate entry barriers, narrowing the competitive field to fewer than a dozen global suppliers. Long qualification cycles tie up working capital, but high margins and multi-year volume visibility justify the investment pivot toward autos.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tight Domestic Labor Market and Wage Pressures | -1.3% | Taiwan national, acute in Hsinchu and Taipei | Short term (≤ 2 years) |

| Intensifying ESG Compliance Costs | -0.8% | Taiwan national, spill-over to global operations | Medium term (2-4 years) |

| Volatility in Cross-Strait Geopolitics | -1.1% | Taiwan and China, indirect impact on global supply | Medium term (2-4 years) |

| Increasing Competition from Southeast Asia | -0.9% | Asia-Pacific regional, Vietnam, Thailand, Malaysia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tight Domestic Labor Market and Rising Wage Pressures

Taiwan’s electronics workforce contracted 3.2% in 2025, lifting the average monthly wage to TWD 52,000 (USD 1,690) and pushing vacancy rates for process engineers past 8%. Large EMS firms invested roughly USD 15 million in automation per 10,000 m² of floor space, but payback stretches beyond 3 years, and near-term margins have compressed by up to 2 percentage points. Smaller providers lacking scale relocated lines to Vietnam and Thailand, incurring one-off costs of USD 8-12 million each and seeing defect rates jump 20-30% during the first year of operation. Wage inflation is most acute in Hsinchu and Taipei, where semiconductor fabs outbid EMS houses for RF and signal-integrity engineers. Without demographic relief, labor scarcity could remain a structural drag through the decade.

Volatility in Cross-Strait Geopolitics

Intermittent military drills in the Taiwan Strait during 2025 led multinational customers to cap any single Taiwan site at 40% of product volume, pushing spillover orders to Vietnam, Thailand, and Mexico, even at 5-8% higher unit cost. Political-risk insurance premiums on Taiwan shipments jumped 20%, adding roughly USD 0.12 to notebook assembly cost and trimming already-thin margins. EMS firms rushed to certify mirror lines overseas but conceded some high-volume smartphone work to Chinese competitors able to guarantee uninterrupted flow. Financing costs also edged higher as lenders factored in geopolitical uncertainty, lengthening project-payback horizons. While complex, low-volume programs remain anchored in Taiwan, persistent tension could erode the island’s share in price-sensitive consumer hardware.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: PCB Assembly Anchors Revenue While Box Build Surges

PCB Assembly captured 44.52% of the market share in 2025, underscoring the Taiwan electronics manufacturing services market’s dense ecosystem of substrate makers and precision-inspection tool vendors. Electromechanical and Box Build services are on track for a 9.66% CAGR through 2031 as global automakers outsource ISO 26262-compliant ECU assembly. Pricing power rests on expertise in micro-via drilling, 0.3 mm ball-grid arrays, and real-time X-ray laminography that safeguard yields at high layer counts.

Growth momentum is shifting toward full-system integration. Automotive domain controllers, medical devices that must pass ISO 13485 audits, and low-earth-orbit satellite payloads all require enclosure fabrication, cable harnessing, and environmental stress screening within one factory. Taiwanese specialists bundle these steps, reducing customer lead times by 20% and capturing margins 300 basis points above bare-board assembly. As smart-factory retrofits embed digital twins and predictive analytics, service providers expect to push first-pass yield above 98%, reinforcing stickiness and expanding wallet share.

By Business Model: Contract Manufacturing Still Dominant, Hybrid Models Accelerate

Contract Manufacturing generated 61.26% of 2025 revenue, reflecting entrenched cost-plus programs in smartphones and notebooks. Nevertheless, Hybrid and Turnkey engagements are growing 9.21% annually because brand owners want partners to shoulder design-for-manufacture risk and compress development cycles from 18 months to under a year. In AI servers, Quanta now owns thermal and power-architecture design and licenses finished platforms to cloud providers, securing higher margins than traditional cost-plus jobs.

Original Design Manufacturing remains material at 28% of revenue, but its focus is narrowing to laptops, tablets, and networking gear. Hybrid models in automotive electronics often include value-sharing clauses that tie EMS compensation to vehicle production volumes, aligning incentives and boosting long-term revenue visibility. Intellectual property regimes in the United States and Europe determine whether EMS houses can assert design rights, thereby shaping negotiation leverage. The Taiwan electronics manufacturing services market thus continues to pivot from a capacity buffer to an innovation partner, deepening its strategic entanglement with global brands.

By Manufacturing Process: SMT Leads, Advanced Packaging Captures Premium Tiers

Surface Mount Technology generated 53.64% of 2025 process revenue, maintained by smartphones and notebooks that place over 1,200 parts per board at 60,000 cph. Through-Hole Technology held 18% because industrial controls and power supplies require mechanical robustness. Advanced Packaging and Hybrid Processes, however, are growing at a 9.27% CAGR as chiplet architectures demand fan-out wafer-level and chip-on-wafer-on-substrate connections that dissipate 400 W while maintaining signal integrity below 56 GHz loss tangent thresholds.

EMS integrators are buying micro-bump bonders, plasma desmear systems, and laser-assisted singulation lines to internalize these steps. The investment shifts margin upstream and trims lead times that previously stretched to 16 weeks. Advanced packaging also reduces bill-of-materials costs by integrating passive components into the package, a value proposition attractive to AI accelerator vendors racing to meet power and size targets. Consequently, Surface Mount’s share is expected to slip below 50% by 2031 as heterogeneous integration becomes mainstream.

By End-User: Consumer Electronics Dominates, Automotive Delivers Fastest Growth

Consumer Electronics accounted for 33.67% of the Taiwan electronics manufacturing services market share in 2025, with tablets and gaming consoles leading seasonal peaks. Mobile Devices contributed 22% but ceded share to Chinese assemblers as brands re-internalized final assembly. Computers accounted for 18% of revenue as AI-enabled PCs demanded new thermal solutions, while Industrial applications accounted for 12% on the back of IIoT edge gateways.

Automotive is forecast to grow 10.39% annually, the fastest among sectors, driven by battery-electric platforms and advanced driver-assistance systems that require domain controllers and high-speed sensor fusion modules. Communication infrastructure captured 8% as open RAN deployments scaled. Medical devices represented 5% but deliver 20-25% gross margins thanks to FDA and MDR compliance hurdles. Lighting and aerospace contributed the balance, with satellite subsystems offering high ticket prices and 30% gross margins despite low unit volumes. The diversification underscores the Taiwan EMS industry’s pivot from commodity hardware toward regulated, mission-critical domains.

Geography Analysis

Taiwan’s electronics manufacturing corridor stretches from Hsinchu through Taoyuan to Taichung, adjacent to leading semiconductor fabs and substrate plants. The cluster accounted for 18% of global EMS revenue in 2025, down from 21% in 2020, as customers diversified capacity to Vietnam, Thailand, and Mexico. Despite share erosion, the Taiwan EMS market benefits from co-location with foundries, enabling rapid design-to-production cycles for AI accelerators and chiplet-based modules.

Government policy seeks to defend this edge. The Advanced Manufacturing Promotion Act offers 25% tax credits on smart-factory and carbon-neutral capex, drawing USD 5.8 billion in commitments during 2025. Labor, however, is tightening; the working-age population is forecast to shrink 1.2% annually through 2030, and monthly wages already average USD 1,690, triple the levels in Vietnam or Thailand. Some mid-tier EMS firms have responded by setting up satellite plants in Mexico’s Bajío and Vietnam’s Bac Giang provinces, but they continue to rely on Taiwan for engineering prototypes and advanced packaging.

Cross-strait tensions layer additional risk. Military exercises in 2025 triggered supply-chain policies limiting any single site to 40% of total volume, pushing notebook orders to Indonesian and Indian plants even at higher cost. Insurance premiums on shipments to Taiwan rose 20%, trimming gross margins on high-volume consumer devices. Nonetheless, for high-layer-count PCBs, ABF substrates, and chip-on-wafer packages, customers still prefer Taiwanese capacity because alternate regions lack the precision tooling and yield management to hit 98% first-pass rates. The resulting bifurcation leaves Taiwan dominant in complex, low-volume programs while conceding commodity volumes to lower-cost geographies.

The electronics manufacturing services market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for Europe, Asia, and North America. This is complemented by country-specific insights for India, Thailand, France, United States, Singapore, and United Kingdom, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

The Taiwan EMS market remains moderately concentrated. Foxconn, Pegatron, Wistron, Quanta, and Compal controlled about 65% of 2025 revenue. Foxconn led with USD 180 billion, deploying USD 10 billion between 2024-2026 to build campuses in India, Vietnam, and Mexico that mirror Taiwan processes. Pegatron and Wistron are pivoting toward automotive domain controllers and AI servers where gross margins exceed 15%. Quanta’s USD 3.2 billion AI server deal with a U.S. cloud provider underscores this shift and will add 12% to its revenue by 2027.

Smaller specialists are carving niches. Universal Scientific Industrial and Accton Technology win design-rich mandates in electric vehicles and open-network switches by featuring faster decision cycles and tighter IP locks. Delta Electronics and Lite-On apply power-electronics portfolios to traction inverters and on-board chargers that must clear ISO 26262 ASIL-D thresholds. Competitive intensity is rising; notebook assembly ASPs fell 4% in 2025 as buyers exploited dual sourcing. Mid-tier players sold or shuttered low-margin lines. Wistron divested its notebook ODM business for USD 585 million to fund automotive and satellite bets.

Technology trends favor agile entrants. Digital twins, predictive analytics, and lot sizes of 100 units erode traditional scale advantages. Meanwhile, sustainability-linked contracts that guarantee carbon-neutral production can capture a 3-5% premium from European customers subject to extended producer-responsibility laws. These shifts imply ongoing fragmentation in commodity tiers and heightened rivalry for high-margin verticals.

Taiwan Electronics Manufacturing Services Industry Leaders

Foxconn Technology Group

Pegatron Corporation

Wistron Corporation

Quanta Computer Inc.

Compal Electronics Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: ASE Technology completed a TWD 45 billion (USD 1.46 billion) advanced-packaging plant in Kaohsiung dedicated to chip-on-wafer-on-substrate and fan-out wafer-level lines with 50,000-wafer monthly capacity.

- November 2025: Foxconn and Stellantis formed a joint venture to produce 2 million zonal domain controllers annually by 2028.

- October 2025: Pegatron invested TWD 28 billion (USD 910 million) to expand its Batam, Indonesia campus for smartphone and tablet assembly.

- September 2025: Quanta signed a USD 3.2 billion, three-year AI server supply agreement with a leading cloud provider.

Taiwan Electronics Manufacturing Services Market Report Scope

The Taiwan Electronics Manufacturing Services Market Report is Segmented by Service Type (Electronics Manufacturing Services, Engineering Services, Test and Development Implementation Services, Logistics Services, Other Service Types), Business Model (Contract Manufacturing (CM), Original Design Manufacturing (ODM), Hybrid / Turnkey / Other Business Models), Manufacturing Process (Surface Mount Technology (SMT), Through-Hole Technology (THT), Advanced Packaging / Hybrid Processes), End-user (Mobile Devices, Consumer Electronics, Computer, Industrial, Automotive, Communication, Lighting, Medical, Other End-users). The Market Forecasts are Provided in Terms of Value (USD).

| Electronics Manufacturing Services | PCB Assembly |

| Electromechanical Assembly/Box Build | |

| Prototyping | |

| Other Electronics Manufacturing Services | |

| Engineering Services | |

| Test and Development Implementation Services | |

| Logistics Services | |

| Other Service Types |

| Contract Manufacturing (CM) |

| Original Design Manufacturing (ODM) |

| Hybrid / Turnkey / Other Business Models |

| Surface Mount Technology (SMT) |

| Through-Hole Technology (THT) |

| Advanced Packaging / Hybrid Processes |

| Mobile Devices (Smartphones and Tablets) |

| Consumer Electronics |

| Computer (PCs/Desktop/Laptops) |

| Industrial |

| Automotive |

| Communication |

| Lighting |

| Medical |

| Other End-users |

| By Service Type | Electronics Manufacturing Services | PCB Assembly |

| Electromechanical Assembly/Box Build | ||

| Prototyping | ||

| Other Electronics Manufacturing Services | ||

| Engineering Services | ||

| Test and Development Implementation Services | ||

| Logistics Services | ||

| Other Service Types | ||

| By Business Model | Contract Manufacturing (CM) | |

| Original Design Manufacturing (ODM) | ||

| Hybrid / Turnkey / Other Business Models | ||

| By Manufacturing Process | Surface Mount Technology (SMT) | |

| Through-Hole Technology (THT) | ||

| Advanced Packaging / Hybrid Processes | ||

| By End-user | Mobile Devices (Smartphones and Tablets) | |

| Consumer Electronics | ||

| Computer (PCs/Desktop/Laptops) | ||

| Industrial | ||

| Automotive | ||

| Communication | ||

| Lighting | ||

| Medical | ||

| Other End-users |

Key Questions Answered in the Report

What is the current size of the Taiwan EMS market?

The Taiwan EMS market size is USD 55.58 billion in 2026 and is projected to grow to USD 84.13 billion by 2031.

Which segment is growing fastest within Taiwan’s EMS services mix?

Electromechanical and Box Build services are growing fastest, with a 9.66% CAGR through 2031.

How significant is automotive electronics for Taiwanese EMS providers?

Automotive electronics are forecast to expand at a 10.39% CAGR, making them the fastest-growing end-user segment and a key diversification avenue.

Why are advanced packaging capabilities critical for Taiwan EMS firms?

Chiplet architectures and AI accelerators require fan-out and chip-on-wafer processes that carry higher margins and reinforce Taiwan’s competitive edge in complex assemblies.

How are labor shortages affecting Taiwan EMS providers?

A shrinking workforce has lifted average monthly wages to USD 1,690, compressing margins and accelerating automation and overseas expansion.

What geopolitical factors influence customer sourcing strategies?

Cross-strait tensions have led many brands to cap Taiwan site exposure at 40% of volume, prompting parallel capacity builds in Vietnam, Thailand, and Mexico despite higher costs.

Page last updated on: