Synthetic Gypsum Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.05 Billion |

| Market Size (2031) | USD 2.46 Billion |

| Growth Rate (2026 - 2031) | 3.73% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Synthetic Gypsum Market Analysis by Mordor Intelligence

The Synthetic Gypsum Market size is expected to grow from USD 1.98 billion in 2025 to USD 2.05 billion in 2026 and is forecast to reach USD 2.46 billion by 2031 at 3.73% CAGR over 2026-2031. The synthetic gypsum market has moved beyond its earlier role as a disposal outlet for industrial byproducts and now functions as a feedstock for wallboard, cement, and select agricultural applications. Growth is shaped by a supply-and-demand imbalance: downstream users require stable calcium sulfate inputs, while Flue Gas Desulfurization (FGD) output in developed economies has plateaued after years of rapid growth. Sustainability standards in construction and tighter waste regulations are broadening acceptance of recycled and secondary gypsum streams, supporting the synthetic gypsum market as traditional utility-linked supply becomes less certain. Phosphogypsum processing and agricultural applications are expanding producers' end markets, reducing dependence on a single construction cycle and maintaining commercial relevance across more regions. Competition remains moderate, as a few large wallboard and cement groups set quality and scale standards, while regional suppliers compete on proximity, transport costs, and access to compliant feedstock.

Key Report Takeaways

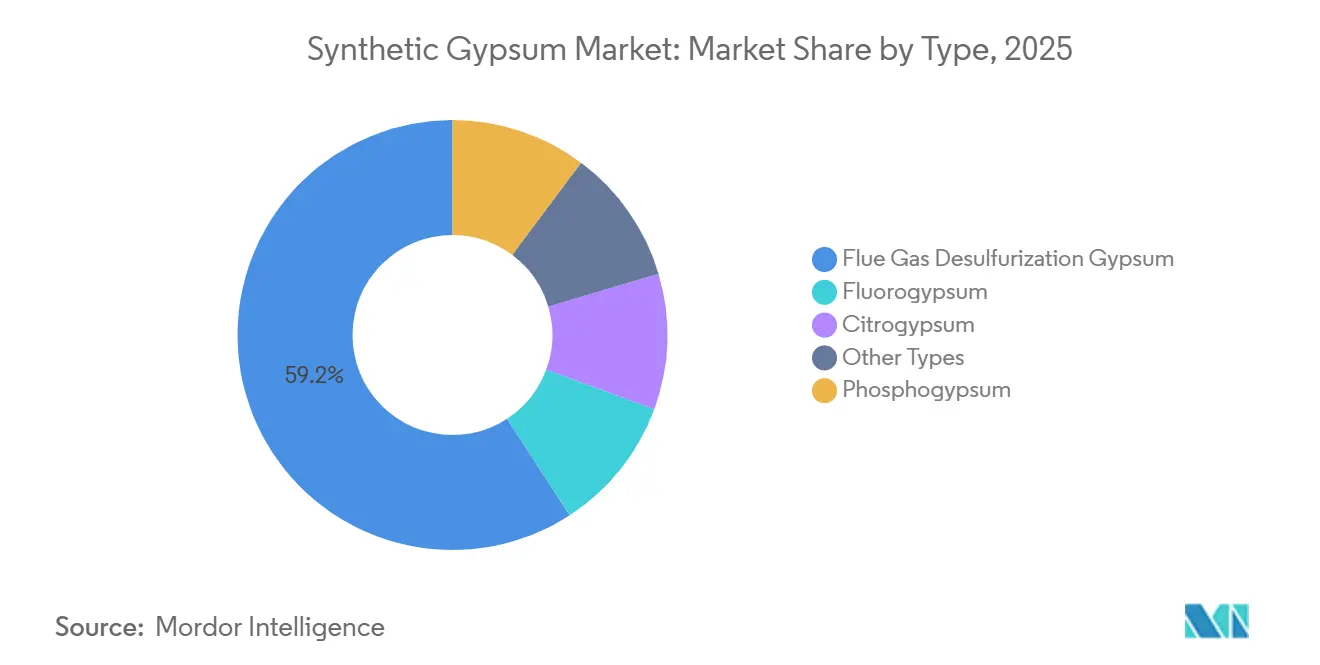

- By type, Flue Gas Desulfurization Gypsum held 59.17% of the synthetic gypsum market share in 2025, while phosphogypsum is projected to expand at a 4.55% CAGR through 2031.

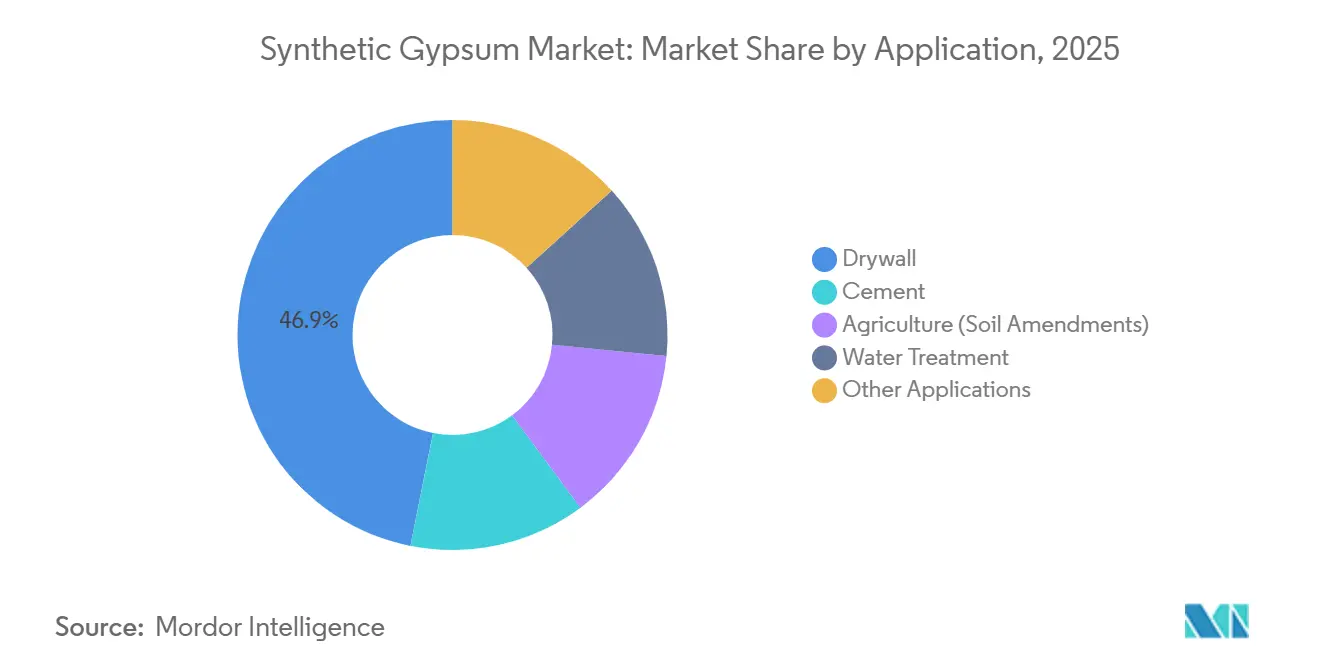

- By application, drywall accounted for 46.88% of the synthetic gypsum market size in 2025, while agriculture, soil amendment, is forecast to grow at a 4.37% CAGR through 2031.

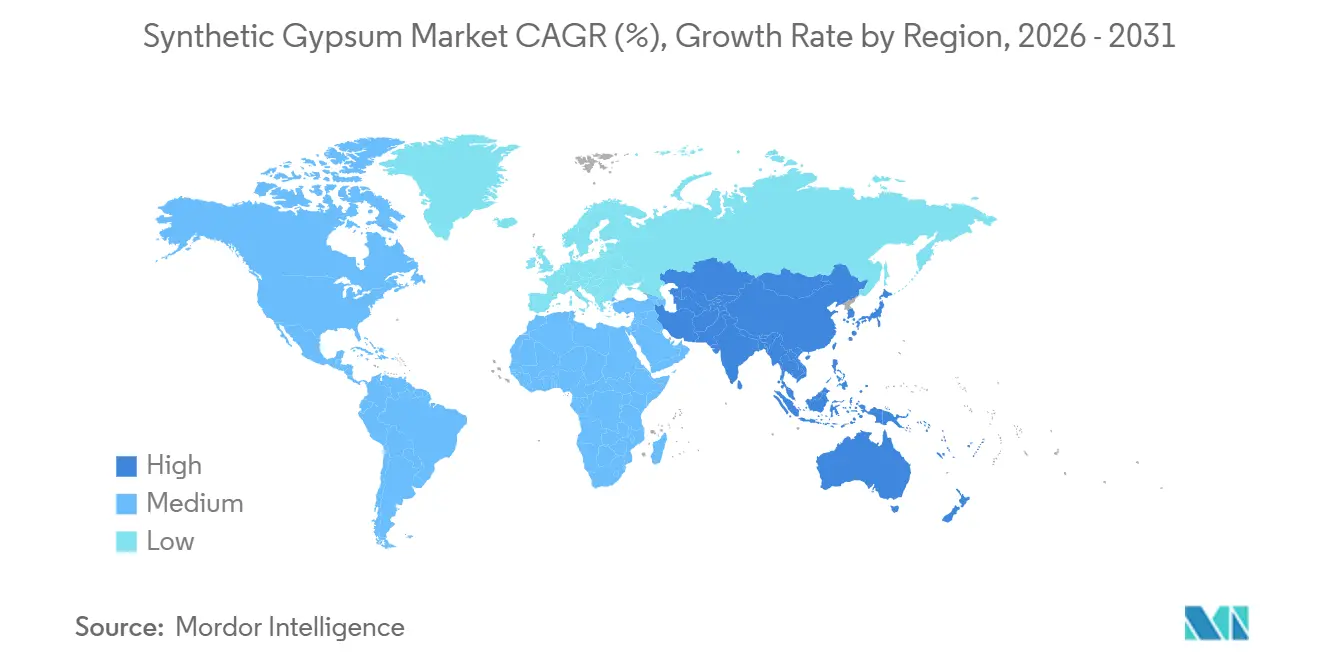

- By geography, Asia-Pacific held 39.51% share of the synthetic gypsum market size in 2025 and is also projected to grow at a 4.82% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Synthetic Gypsum Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Preference for Sustainable Building Materials | +0.7% | Global, with peak demand intensity in North America and European green-building markets | Long term (≥ 4 years) |

| Coal Plant FGD Systems Generating Consistent Supply | +0.6% | Asia-Pacific core, India, and Southeast Asia, with residual gains in North America | Medium term (2-4 years) |

| Cement Producers Securing Supplementary Gypsum Supply | +0.4% | Global, especially Asia-Pacific and South America, where clinker output is expanding | Medium term (2-4 years) |

| Soil Amendment Demand from Agricultural Producers | +0.5% | Brazil, India, the United States, Southeast Asia | Long term (≥ 4 years) |

| Tightening Circular Economy Regulations | +0.4% | EU, Canada, with spillover to the Middle East and Africa | Short term (≤ 2 years) |

| Emerging Waste Valorization Business Models | +0.3% | Global, with early adoption in Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Preference for Sustainable Building Materials

The synthetic gypsum market is seeing a procurement shift that places greater weight on recycled content, traceability, and reduced landfill exposure in building materials. Certification systems such as Leadership in Energy and Environmental Design (LEED) and BREEAM reward materials with validated recycled content, making synthetic gypsum more attractive to developers and public buyers who must document environmental performance. In 2025, the United States Geological Survey (USGS) estimated synthetic gypsum at 39% of total US domestic gypsum supply, indicating that the material holds a substantial operational role rather than a marginal sustainability position. This installed base is significant because large wallboard producers and construction buyers can expand secondary gypsum use without redesigning end products or changing core specifications. Buying decisions are increasingly tied to compliance, reporting, and portfolio standards rather than short-term raw material price spreads alone, which supports a more stable demand floor for the synthetic gypsum market.

Coal Plant Flue Gas Desulfurization (FGD) Systems Generating Consistent Supply

The synthetic gypsum market remains heavily dependent on flue gas desulfurization (FGD) systems, and this link continues to be a positive supply factor in regions where coal capacity remains active or where scrubber compliance is expanding. US synthetic gypsum production held steady at an estimated 17 million metric tons in both 2024 and 2025, indicating that North America retained a mature but stable supply base during that period. In Asia, new or retrofitted scrubber systems can still add usable gypsum volumes to markets with growing construction demand. That regional split keeps the synthetic gypsum market uneven, as the same utility technology supports expansion in South and Southeast Asia while offering only replacement-level support in developed power systems. Producers that can connect downstream plants to the lowest-cost compliant FGD supply will retain a logistical and margin advantage as regional supply patterns continue to diverge.

Soil Amendment Demand from Agricultural Producers

The synthetic gypsum market is gaining traction in agriculture, where soil improvement has become a practical route for secondary gypsum utilization rather than a niche application. Research published in Frontiers in Soil Science in 2026 found that phosphogypsum reduced soil sodium adsorption ratios by up to 69%, improved soil structure metrics, and raised barley grain yields by 21% to 39% across tested application rates. The same review noted that more than 300 million tons of phosphogypsum are generated each year globally, while only 14% is reused, indicating a large supply available for agricultural use where regulation permits. The International Fertilizer Association has also identified soil rehabilitation, mine backfill, and related secondary uses as areas moving into broader commercial scope, which supports the synthetic gypsum market by expanding the range of potential off-takers[1]International Fertilizer Association, “From Waste to Inventory, Phosphogypsum,” International Fertilizer Association, fertilizer.org. Agricultural demand is shaped by soil quality requirements and input performance, which can support the synthetic gypsum market even when construction activity slows during a given cycle.

Tightening Circular Economy Regulations

The synthetic gypsum market is also being supported by regulations that discourage landfilling and encourage closed-loop material use in the construction chain. Austria's Recycled Gypsum Regulation took effect on April 1, 2025, followed by a full gypsum landfill ban from January 1, 2026, creating a direct compliance requirement for collection, sorting, and reprocessing capacity. This type of policy change requires prompt action, as recyclers, plasterboard producers, and demolition contractors all need operational channels capable of handling gypsum waste within regulated timelines. It also provides the synthetic gypsum market with a new institutional demand base, as the use of secondary gypsum becomes tied to legal obligations and procurement systems rather than voluntary preference alone. Once these systems are established, they tend to persist, meaning the synthetic gypsum market can continue to benefit from circularity regulations well beyond the initial compliance deadline.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Coal Phase-Down Eroding Flue Gas Desulfurization (FGD) Gypsum Supply | -0.8% | Europe and North America most acutely, with Germany, the UK, and Canada leading | Short-term (≤ 2 years), intensifying long-term |

| Contaminant and Radioactivity Concerns in Phosphogypsum | -0.5% | The United States most restrictive, with the EU variable by member state, and global trade spillover | Medium term (2-4 years) |

| Handling, Drying, and Logistics Cost Pressures | -0.3% | Inland markets globally, with South America, the Middle East, and Africa, are particularly exposed | Medium term (2-4 years) |

| Quality Variability and Verification Challenges | -0.2% | Global, more pronounced in markets with multiple FGD or phosphogypsum source types | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Coal Phase-Down Eroding FGD Gypsum Supply

The decline of coal-fired power generation in developed economies presents a significant structural challenge to the synthetic gypsum market, as FGD gypsum supply is directly tied to the presence and operating rates of scrubbed coal plants. This issue is most acute in regions where downstream wallboard and cement capacity remains large, but the upstream utility base is shrinking faster than alternative gypsum streams can scale. As coal plants close, buyers lose a nearby source that had long offered predictable purity, contract visibility, and favorable transport economics. The impact on the synthetic gypsum market includes reduced local availability and greater reliance on longer-haul sourcing, imported material, or higher-cost recycled streams that require additional verification before use. This supply shift can narrow the cost gap between synthetic and mined gypsum in some locations, weakening one of the cost advantages that supported broad FGD adoption.

Contaminant and Radioactivity Concerns in Phosphogypsum

The synthetic gypsum market is further constrained by the uneven acceptance of phosphogypsum, particularly in regions where regulators apply strict rules on radioactivity and contaminant management. Research published in the Journal of Radioanalytical and Nuclear Chemistry in 2025 confirmed that 80%-90% of radium isotopes in phosphate rock precipitate as phosphogypsum, while associated uranium, thorium, and other radionuclide profiles vary with rock origin and plant conditions. The commercial challenge extends beyond radionuclides, as heavy metals such as cadmium, lead, zinc, and arsenic can complicate classification and end-use approval across countries. Environmental Technology & Innovation documented treatment approaches such as water washing, flotation, and microbially induced calcium carbonate precipitation in 2026, but also noted that large-scale adoption remains a work in progress[2]Y. Wang et al., “Impurity Removal from Phosphogypsum, Mechanisms, Treatment Technologies, and Challenges for Sustainable Utilization,” Environmental Technology & Innovation, doi.org . This leaves the synthetic gypsum market with a fragmented regulatory landscape, where some regions can expand phosphogypsum use faster than others, slowing the pace at which this feedstock can offset declining FGD supply.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: FGD Dominance Masks Rising Phosphogypsum Potential

FGD gypsum held 59.17% of the market in 2025, making it the largest type segment in the synthetic gypsum market. This position reflects consistent particle characteristics, established supply chains from utility sites to board and cement plants, and a long track record in high-volume construction applications. In the United States, synthetic gypsum production was estimated at 17 million metric tons in both 2024 and 2025, underlining the scale that FGD-derived material contributes to the North American supply base. Fluorogypsum and citrogypsum remained much smaller streams, serving specialized applications where impurity control is more important than total volume. Although limited in scale, these types indicate that the synthetic gypsum market encompasses a broader range of materials than the wallboard-centered FGD segment alone.

Phosphogypsum is projected to grow at a 4.55% CAGR through 2031, making it the fastest-growing type in the synthetic gypsum market. Material that was previously stockpiled in stacks is increasingly being evaluated as a usable feedstock for agriculture, construction, and selected industrial applications. The International Fertilizer Association reported that more than 300 million tons of phosphogypsum are generated every year and that only 14% is reused, leaving a large resource base available if quality and regulatory requirements are met. Treatment methods such as washing, flotation, and biological approaches are also improving the commercial case for higher-value applications, particularly where buyers require greater confidence in contaminant control. The type segment therefore reflects a clear transition, with the largest feedstock tied to a maturing utility base and the fastest-growing feedstock tied to improving treatment capability and broader acceptance across the synthetic gypsum market.

By Application: Construction Holds the Volume Base While Agriculture Adds Growth

Drywall accounted for 46.88% of demand in 2025, making it the largest application in the synthetic gypsum market. This position reflects the close alignment between FGD gypsum quality and plasterboard manufacturing requirements, where consistency, stable chemistry, and reliable contract supply are key considerations. The application also benefits from the established operating history of wallboard plants that are already equipped to process synthetic gypsum within their existing production lines. Cement remained another major outlet, and the United States Geological Survey (USGS) identified it as one of the primary uses of synthetic gypsum in the United States, where gypsum serves as a set retarder in Portland cement production. Water treatment remained a smaller application but maintained a technically distinct role in the synthetic gypsum market, where sulfate balance and process control support continued use.

Agriculture and soil amendment is forecast to grow at a 4.37% CAGR through 2031, making it the fastest-growing application in the synthetic gypsum market. Field results published in Frontiers in Soil Science showed that phosphogypsum application at 3-6 t/ha reduced soil bulk density and improved water infiltration in irrigated land. The same source linked phosphogypsum use to improved structural performance in salt-affected soils, which is relevant in regions where agricultural productivity is constrained by soil degradation rather than nutrient availability alone. The International Fertilizer Association identified Brazil, the United States, and India as active markets for agricultural use, indicating a broad global base rather than a single-country pattern. This combination of established construction demand and growing agronomic adoption gives the synthetic gypsum market a more balanced application profile than in earlier years.

Geography Analysis

Asia-Pacific accounted for 39.51% of revenue in 2025 and is projected to grow at a 4.82% CAGR through 2031, making it the largest and fastest-growing regional market for synthetic gypsum. China remains the region's largest demand center, as its wallboard and cement value chains can absorb substantial synthetic gypsum volumes within large construction-linked manufacturing networks. India presents a notable supply-and-demand combination, as flue gas desulfurization (FGD) installations at coal plants support byproduct generation, while cement and wallboard producers require reliable gypsum inputs to expand end markets. Japan and South Korea represent a more mature segment of the regional market, with technically disciplined processing standards that support quality requirements in higher-value board manufacturing. Vietnam, Indonesia, and Bangladesh strengthen the medium-term outlook, as tightening emissions controls and steady construction demand are expected to support wider use of synthetic gypsum across the region.

North America remains one of the most technically integrated regions in the synthetic gypsum market, with long-standing links between FGD producers and board manufacturers. In 2025, the United States Geological Survey (USGS) estimated synthetic gypsum at 39% of the total US domestic gypsum supply, confirming the central role of synthetic gypsum in the country's broader gypsum system. The same publication reported wallboard sales of 26 billion square feet against panel manufacturing capacity of 34 billion square feet per year, reflecting the scale of installed downstream demand capable of absorbing qualified material. In June 2026, Knauf Group's USG Corporation, through CGC Inc., opened a CAD 210 million (~USD 148.85 million) wallboard plant in Wheatland County, Alberta, targeting lower carbon emissions, lower water use, and zero manufacturing waste to landfill. Canada and Mexico add depth to the regional market, but the United States remains the largest operating benchmark for synthetic gypsum in North America.

Europe presents a more complex environment for the synthetic gypsum market, as strong downstream demand coincides with a tightening long-term FGD supply base and a growing emphasis on recycling. Austria illustrates the policy direction: its 2025 recycled gypsum framework and 2026 landfill ban were followed by the opening of the GzG Gipsrecycling GmbH plant in Stockerau, which has an annual capacity of 60,000 tons and can supply Saint-Gobain plasterboard production with up to 40% recycled material. South America is gaining relevance as Brazil's phosphogypsum base supports both agricultural and construction applications, while Etex has committed EUR 65 million to gypsum board expansion across Peru, Chile, and Argentina through 2026 and 2027. The Middle East and Africa remain smaller in revenue terms, though construction programs, cement capacity additions, and wider adoption of emissions control systems continue to support gradual market expansion.

Competitive Landscape

The synthetic gypsum market is moderately fragmented, with a small group of established materials companies shaping the largest wallboard and cement-linked demand channels. Knauf Group, Saint-Gobain, and Holcim hold strong strategic positions through their downstream reach, product qualification history, and ability to source large volumes for board and cement operations. A broader mid-tier, including BNBM Group, Yoshino Gypsum, Georgia-Pacific, Etex Group, and American Gypsum, prevents the market from becoming overly concentrated, as these players remain important in national and regional demand centers. Competition is therefore driven less by branding and more by feedstock security, transport efficiency, and the ability to consistently meet plant-level quality targets. This makes local operating discipline especially important in a business where freight costs and material consistency can quickly affect profit outcomes.

Vertical integration remains one of the clearest strategic patterns in the synthetic gypsum market, as companies that connect feedstock sources to downstream plants reduce handling risk and gain better control over delivered costs. This model is evident in relationships where utility-linked gypsum streams move under structured supply arrangements into board and cement plants that require stable chemistry and dependable scheduling. Another active strategy involves investing in circular processing infrastructure to capture more gypsum value from construction waste and reduce exposure to volatile primary supply. In October 2025, PORR, Saint-Gobain, and Saubermacher opened Austria's first gypsum-to-gypsum recycling plant, creating a closed-loop system with rail logistics and recycled content integration into new plasterboard production. This development is significant for the synthetic gypsum market because it demonstrates how competitive advantage can now come from waste-handling capabilities and compliance with recycling requirements, rather than solely from access to conventional flue gas desulfurization (FGD) material.

Technology is also becoming a more visible competitive factor in the synthetic gypsum market, particularly in phosphogypsum treatment and qualification. Environmental Technology & Innovation has documented growing work on impurity removal through water washing, flotation, and biomineralization, suggesting that feedstock upgrading may become a stronger basis for differentiation in the coming years. In June 2026, Knauf Group and CGC Inc. (CGC) strengthened their North American position with the opening of an Alberta wallboard plant, adding capacity with a strong sustainability profile within a mature regional system. Etex also expanded its regional manufacturing footprint through announced gypsum board investments in Peru, Chile, and Argentina, demonstrating that capacity addition remains a practical competitive response in markets with room for downstream growth. These developments indicate that the synthetic gypsum market is being shaped by a combination of scale, recycling capability, and process knowledge, rather than by a single dominant competitive model.

Synthetic Gypsum Industry Leaders

USG Corporation

Knauf Group

Saint-Gobain

Georgia-Pacific Gypsum LLC

HOLCIM

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Knauf Group's USG Corporation, through its Canadian division CGC Inc., opened a CAD 210 million (USD 147.8 million) wallboard manufacturing plant in Wheatland County, Alberta. The facility targets 20% lower carbon emissions, 25% lower water usage, and zero manufacturing waste to landfill. It adds capacity in Western Canada as part of a broader CAD 325 million (USD 228.73 million) North American investment program.

- October 2025: Austria's first gypsum-to-gypsum recycling plant, GzG Gipsrecycling GmbH, opened in Stockerau with an annual capacity of 60,000 tons. The plant is a joint venture of PORR, Saint-Gobain, and Saubermacher. It processes construction and demolition gypsum waste into recycled material, which Saint-Gobain incorporates at up to 40% into new plasterboard production at its Bad Aussee facility, establishing a closed-loop supply chain supported by dedicated rail logistics.

Global Synthetic Gypsum Market Report Scope

Synthetic gypsum is a high-purity, man-made calcium sulfate dihydrate produced as a by-product of industrial manufacturing. It is chemically identical to natural gypsum and is primarily used as a substitute for it.

The synthetic gypsum market is segmented by type, application, and geography. By type, the market is segmented into flue gas desulfurization gypsum, phosphogypsum, fluorogypsum, citrogypsum, and other types. By application, the market is segmented into drywall cement, agriculture (soil amendments), water treatment, and other applications. The report also covers market size and forecasts for synthetic gypsum across 16 countries in major regions. The market sizes and forecasts are provided in terms of value (USD).

| Flue Gas Desulfurization Gypsum |

| Phosphogypsum |

| Fluorogypsum |

| Citrogypsum |

| Other Types |

| Drywall |

| Cement |

| Agriculture (Soil Amendments) |

| Water Treatment |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Flue Gas Desulfurization Gypsum | |

| Phosphogypsum | ||

| Fluorogypsum | ||

| Citrogypsum | ||

| Other Types | ||

| By Application | Drywall | |

| Cement | ||

| Agriculture (Soil Amendments) | ||

| Water Treatment | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is current market size of Synthetic Gypsum Market?

The Synthetic Gypsum Market size is expected to grow from USD 1.98 billion in 2025 to USD 2.05 billion in 2026 and is forecast to reach USD 2.46 billion by 2031 at 3.73% CAGR over 2026-2031.

Which type leads to global consumption today?

FGD gypsum led by type with a 59.17% share in 2025, mainly because it has long-established use in wallboard and cement applications.

Which application is growing the fastest?

Agriculture, soil amendment, is the fastest-growing application with a 4.37% CAGR through 2031, supported by stronger evidence for soil structure improvement and yield benefits.

Why does Asia-Pacific hold the leading regional position?

Asia-Pacific held 39.51% of revenue in 2025 and is projected to grow at 4.82% CAGR through 2031 because the region combines large construction demand with continuing FGD-linked supply in several countries.

Page last updated on: