Synthetic Absorbable Sutures Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.33 Billion |

| Market Size (2031) | USD 5.30 Billion |

| Growth Rate (2026 - 2031) | 9.75% CAGR |

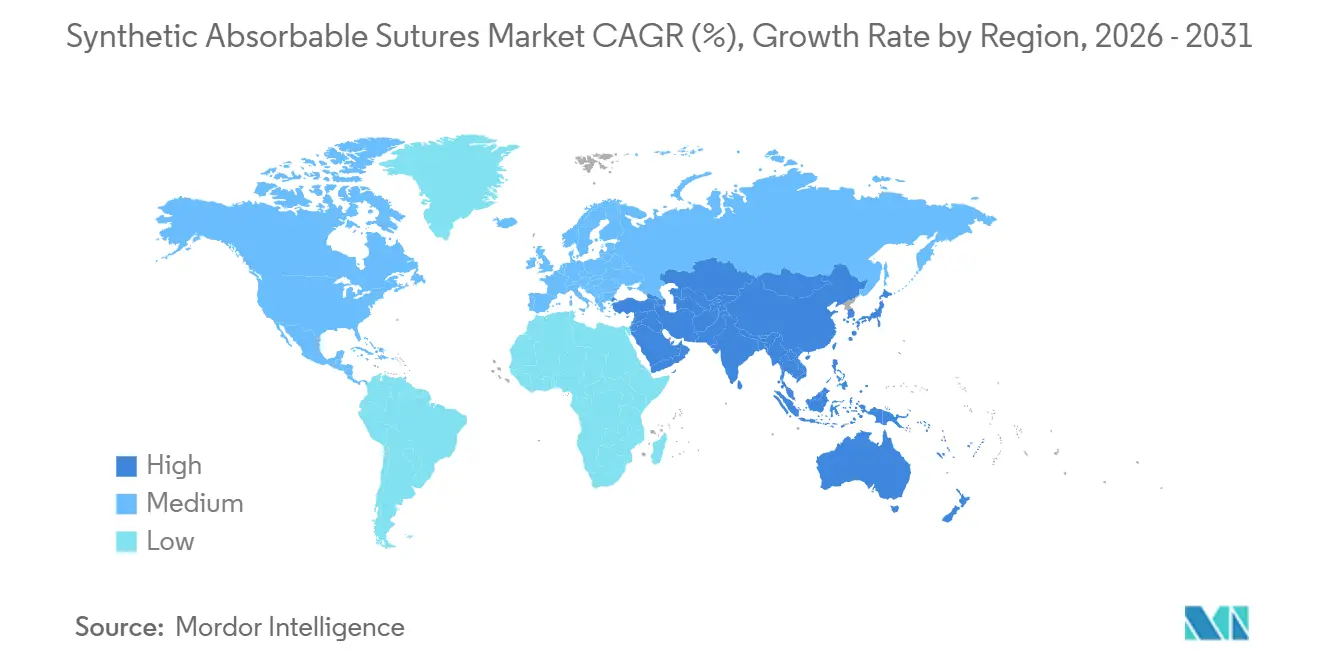

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

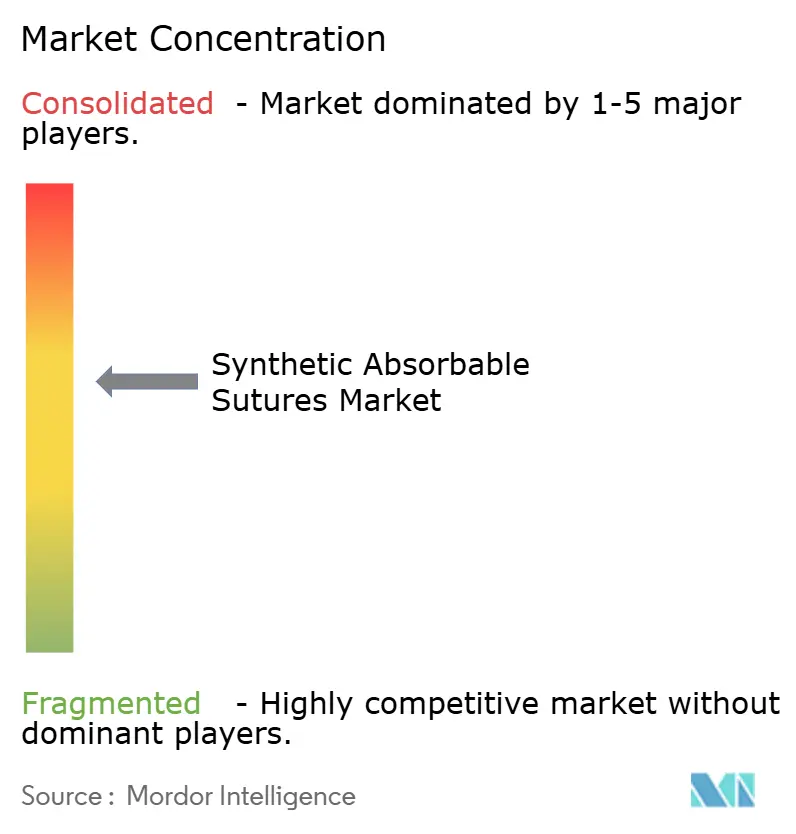

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Synthetic Absorbable Sutures Market Analysis by Mordor Intelligence

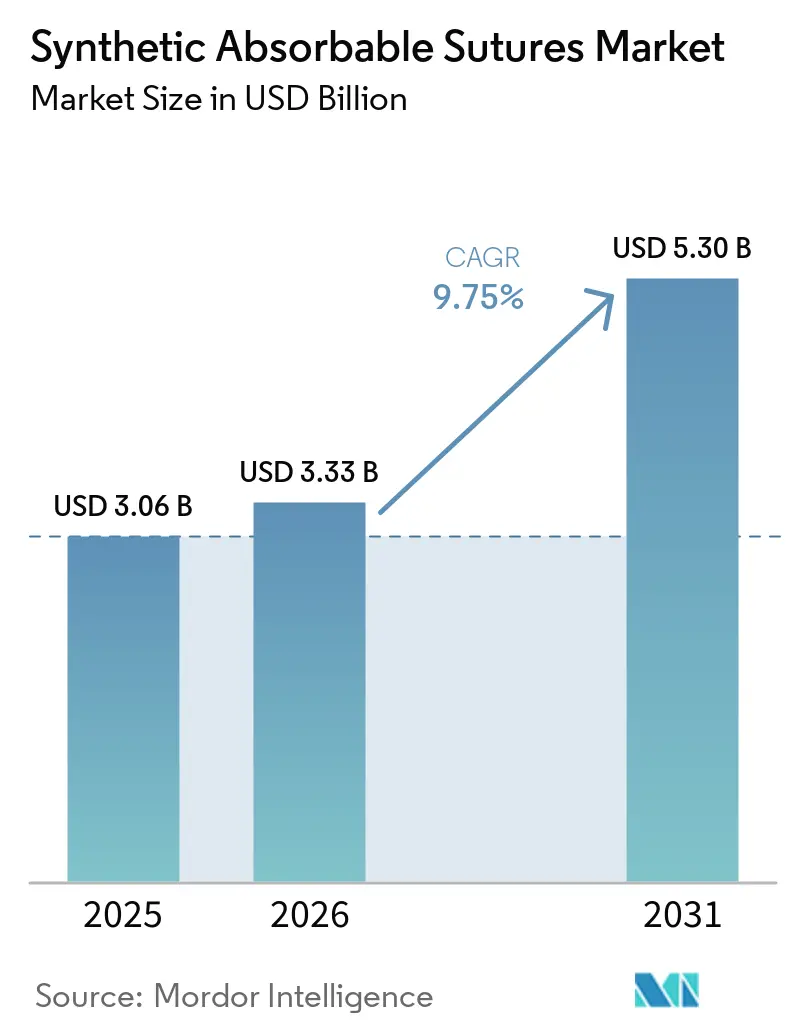

The Synthetic Absorbable Sutures Market size is projected to be USD 3.06 billion in 2025, USD 3.33 billion in 2026, and reach USD 5.30 billion by 2031, growing at a CAGR of 9.75% from 2026 to 2031.

Steady growth reflects larger surgical volumes worldwide, rapid adoption of minimally invasive and robotic techniques, and clinical mandates that favor antibacterial-coated closure devices to reduce infection risk. Robust hospital expansion in Asia and the return of elective procedures after the pandemic further raise demand, while product innovation—in barbed, knot-less, and antimicrobial sutures enables price premiums amid tender-driven cost pressure. At the same time, new U.S. ethylene oxide emissions rules tighten sterilization capacity and could create periodic supply disruptions. Competing closure modalities, notably staplers, tissue adhesives, and energy-based devices, are carving out share in procedures where speed or hemostasis outweighs suture handling advantages.

Key Report Takeaways

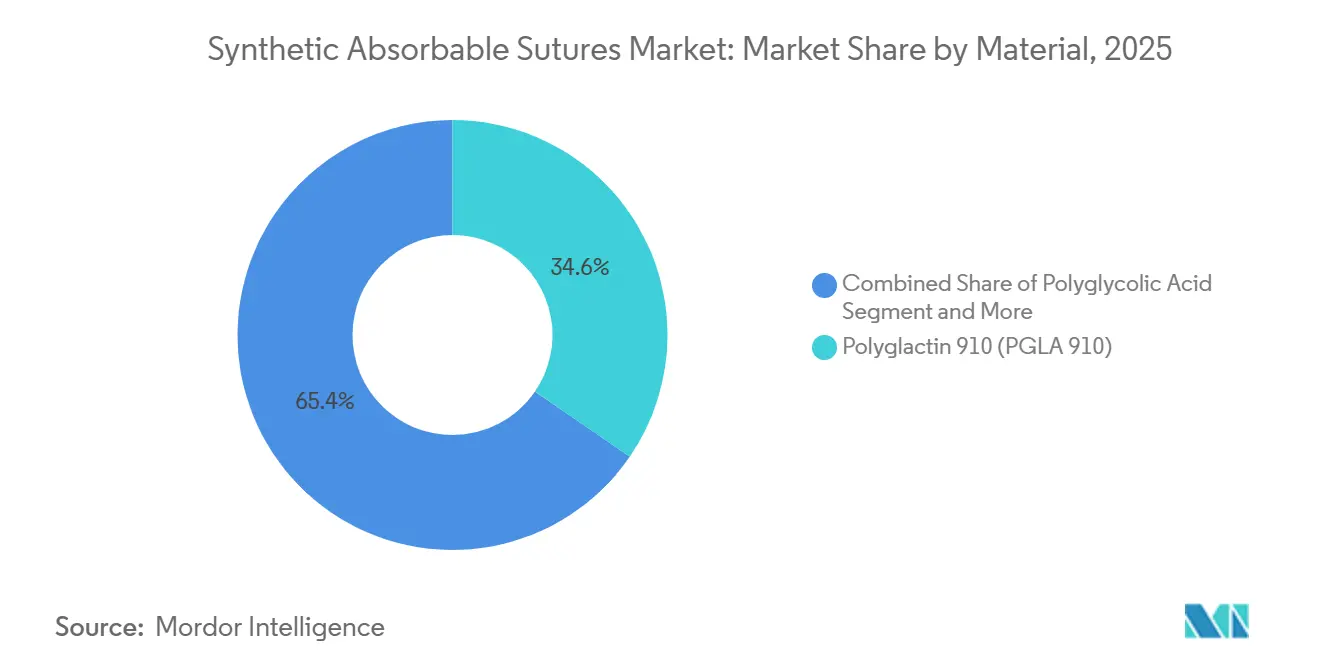

- By material, Polyglactin 910 held 34.58% of the synthetic absorbable sutures market share in 2025, yet poliglecaprone 25 is forecast to post the fastest CAGR of 10.54% to 2031.

- By application, orthopedic surgery accounted for 37.16% of the synthetic absorbable sutures market in 2025, whereas gynecology & obstetrics is projected to expand at a 10.25% CAGR through 2031.

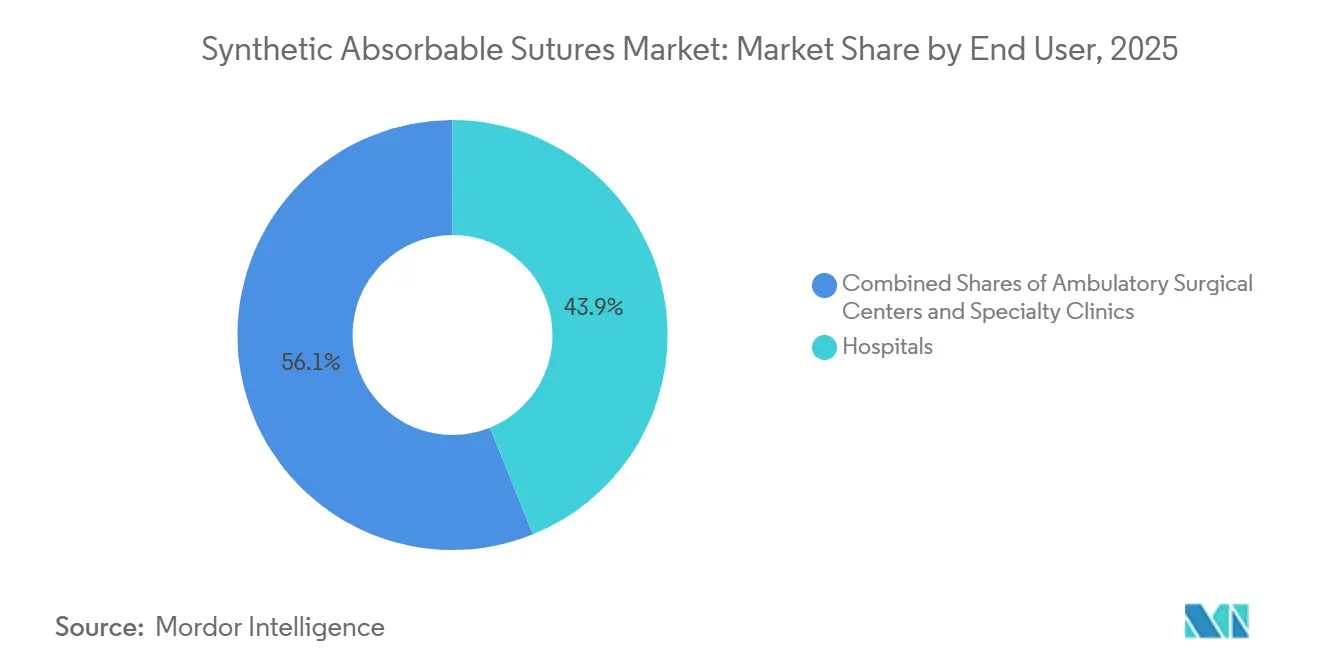

- By end user, hospitals accounted for 43.89% of end-user revenue in 2025, while ambulatory surgical centers are advancing at a 10.47% CAGR.

- By geography, North America accounted for 46.46% of global revenue in 2025, yet Asia-Pacific is expected to grow at a 10.01% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Synthetic Absorbable Sutures Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising surgical procedure volumes and aging populations | +2.8% | Global, with concentration in North America, Europe, and Asia-Pacific (China, India, Japan) | Long term (≥ 4 years) |

| Migration to minimally invasive and outpatient surgeries | +2.1% | North America and Europe (ASC penetration), Asia-Pacific (laparoscopic adoption) | Medium term (2-4 years) |

| Adoption of antibacterial absorbable sutures to cut SSI risk | +1.6% | Global, with early adoption in North America and Western Europe | Medium term (2-4 years) |

| Orthopedic and cardiovascular surgery burden expanding closure demand | +1.4% | North America, Europe, Asia-Pacific (aging demographics) | Long term (≥ 4 years) |

| Rapid uptake of knotless/barbed absorbable sutures in robotic/MIS closures | +1.2% | North America, Europe, select Asia-Pacific markets (robotic surgery hubs) | Short term (≤ 2 years) |

| OEM/private-label capacity in EMs accelerating synthetic absorbables penetration | +0.9% | Asia-Pacific (India, China), Middle East, Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Surgical Procedure Volumes And Aging Populations

Procedure counts climb as populations age and chronic disease prevalence rises. Italy performed 122,777 elective total hip arthroplasties in 2023, up 80% since 2001, and models predict a further 20% rise by 2050. India’s healthcare market reached USD 638 billion in 2025, and private systems plan 34,000 new beds by FY2029, supporting more elective surgeries. Growing diabetic and cardiovascular patient pools heighten demand for absorbable closure products with controlled degradation.

Migration To Minimally Invasive And Outpatient Surgeries

Robotic and laparoscopic approaches now require monofilament or barbed sutures, reducing the number of knot-tying steps. A U.S. review of 224,307 robotic cases showed that the use of knotless devices tripled in colorectal surgery and cut operating-room time by up to 19.1 minutes, without increased complications. Ambulatory surgical centers leverage these efficiencies and benefit from reimbursement parity that drives more same-day procedures.

Adoption Of Antibacterial Absorbable Sutures To Cut SSI Risk

Surgical site infections add a mean USD 20,785 in treatment costs and extend length of stay by 9.7 days, according to the CDC’s National Healthcare Safety Network analysis of 2019-2022 data. The 2025 JAMA meta-analysis of 31 randomized trials (17,968 patients) showed triclosan-coated sutures cut infection incidence by 25% and prevented 39 cases per 1,000 procedures. A U.K. cost-utility model comparing Vicryl Plus with uncoated Vicryl in colorectal surgery reported net savings of GBP 91 per case, supporting a break-even premium of 42% for antibacterial sutures. WHO and NICE guidelines endorse routine use of antibacterial sutures in clean-contaminated and contaminated wounds, yet procurement teams in some hospitals hesitate over triclosan’s environmental persistence and resistance potential.

Rapid Uptake Of Knotless/Barbed Absorbable Sutures In Robotic/MIS Closures

Surgeons performing robotic colorectal, hysterectomy, ventral-hernia, and bariatric procedures increasingly specify knotless absorbable sutures because barbed designs grip tissue along the entire throw and eliminate intracorporeal knot tying, a step that can add several minutes per layer in confined endoscopic fields. STRATAFIX and V-Loc products eliminate intracorporeal knotting, delivering 17-23 minute savings per case and potential USD 640-2,158 cost cuts per procedure [1]Barbara H. Johnson et al., “Trends in adoption of knotless tissue control devices in robotic surgery,” J Comp Eff Res, pmc.ncbi.nlm.nih.gov. Price premiums and learning curves remain adoption hurdles, but high-volume centers value throughput gains.

European robotic centers report a similar learning-curve trajectory, with barbed closures now embedded in enhanced-recovery-after-surgery (ERAS) protocols that target earlier ambulation and shorter lengths of stay, reinforcing administrative support for the price premium that remains 20-40% above braided alternatives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from staplers, adhesives, and energy-based closure | -1.8% | Global, with higher impact in North America and Europe (advanced surgical technologies) | Medium term (2-4 years) |

| Tender-driven price pressure and commoditization | -1.3% | Europe, Asia-Pacific, Latin America (public procurement systems) | Short term (≤ 2 years) |

| EtO sterilization rules raising compliance costs and lead-time risks | -1.2% | Global, with concentration in North America (EPA regulations), spillover to Europe and Asia-Pacific | Medium term (2-4 years) |

| Regulatory scrutiny of triclosan and divergent hospital antimicrobial policies | -0.9% | North America and Europe (environmental and clinical policy debates) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Competition From Staplers, Adhesives, And Energy-Based Closure

Fibrin glues could reach USD 934.68 million by 2029 and cut OR time in hernia repair, eye surgery and vascular work. Staplers speed thoracic procedures, while ultrasonic sealers remove the need for ligatures. Sutures keep their edge where tension distribution or slow absorption is vital, and vendors now bundle sutures with hemostatics to defend share.

Tender-Driven Price Pressure And Commoditization

EU hospitals aggregate multi-year bids that shave up to 50% off list prices, squeezing margins on mature materials such as polyglactin 910. India’s state tenders reward lowest bidders meeting basic quality, hastening the shift to OEM supply. Brands argue premium coatings cut infection costs, yet proof must be quantified or buyers walk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Monofilament Momentum Fuels Poliglecaprone 25

Polyglactin 910 accounted for 34.58% of 2025 revenue in the synthetic absorbable sutures market. The material’s braided structure assures knot security, but its surface harbors bacteria. Surgeons are now pivoting toward monofilaments such as Poliglecaprone 25, forecast to grow at a 10.54% CAGR. This shift underpins the long-term expansion of the synthetic absorbable sutures market size among minimally invasive closures. Polydioxanone retains a premium niche in orthopedic and cardiovascular work because its 180-day retention profile supports tissue remodeling.

Innovation centers on antimicrobial layering and barbed geometry: Meril’s 2024 New Edge Sutures fuse silicon multi-coating with a patented point to lessen tissue drag. Research into chlorhexidine-impregnated glycomer 631 threads signals next-wave differentiation.

By Application: Cesarean Growth Boosts Gynecology & Obstetrics

Orthopedic surgery accounted for 37.16% of the synthetic absorbable sutures market revenue in 2025, driven by the high prevalence of joint replacement [2]Enrico Ciminello et al., “Total hip arthroplasty in Italy,” springer.com. Gynecology & obstetrics, however, is the fastest-growing field, with a 10.25% CAGR, as global cesarean rates are expected to surge by 2030. Hospitals favor absorbable monofilaments for uterine and perineal closure to avoid removal and lower postpartum pain. The synthetic absorbable sutures market size for obstetric use benefits from these policy shifts. Meanwhile, cardiovascular closures require long-lasting polymers, and laparoscopic general surgery increasingly uses barbed monofilaments that balance tension without knots.

By End User: ASC Volumes Rise On Same-Day Demand

Hospitals still account for 43.89% of revenue because complex cases remain inpatient. Yet ambulatory surgical centers are compounding at 10.47% and now buy direct, pressing for discounts while standardizing suture formularies. Specialty clinics dermatology, dental, cosmetic expand steadily as office-based procedures multiply and seek fast-absorbing monofilaments.

Geography Analysis

North America accounted for 46.46% of 2025 revenue, with the United States relying on antibacterial and barbed products to mitigate infection penalties under value-based purchasing [3]U.S. ENVIRONMENTAL PROTECTION AGENCY, “Final Amendments to Air Toxics Standards for Ethylene Oxide Commercial Sterilization Facilities,” epa.gov. EPA’s 90% ethylene oxide cut widens interest in hydrogen peroxide sterilization, yet may raise costs in the near term.

Europe shows mature procedure volumes; centralized tenders squeeze prices, but MDR barriers shelter established brands. B. Braun’s Aesculap unit posted EUR 2.16 billion (USD 2.54 billion) in revenue and is pushing barbed Symmcora lines alongside biosurgicals. Asia-Pacific is the fastest-growing region at a 10.01% CAGR. India’s med-tech push and Healthium’s new plant in Sri City illustrate OEM capacity gains and export ambitions. Chinese tender systems favor domestic labels, while Japan and Australia retain premium barbed uptake. The Middle East & Africa and South America contribute smaller shares, but pockets such as GCC cesarean demand and Brazilian obstetrics sustain volume where currency swings permit.

Competitive Landscape

Five players, Johnson & Johnson, Medtronic, B. Braun, Corza Medical, and Healthium, account for the majority of the synthetic absorbable sutures market revenue. Ethicon leverages Vicryl Plus, while Medtronic’s V-Lok realizes operating-room savings, helping defend price premiums. Healthium, backed by FDA and EU-MDR clearances, scales six Indian factories and 85 patents to challenge incumbents on both price and innovation. White-space innovations orbit non-triclosan antimicrobial coatings and smart sensing sutures that signal infection or strain.

Synthetic Absorbable Sutures Industry Leaders

Johnson & Johnson

B. Braun

Corza Medical

Healthium

Medtronic, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Healthium Medtech signed an MoU to build a second Sri City unit, investing INR 150 crore (USD 18 million) to expand suture and mesh capacity.

- March 2026: Healthium closed the Paramount Surgimed surgical asset purchase, adding 250 million devices per year across 100+ export markets.

- July 2025: Corza Medical unveiled an expanded Onatec ophthalmic suture line of nearly 130 products.

Global Synthetic Absorbable Sutures Market Report Scope

As per the scope of the report, Synthetic absorbable sutures are man-made surgical threads designed to hold body tissues together temporarily before being broken down and absorbed through a process called hydrolysis. Unlike natural absorbable sutures like catgut, which are digested by enzymes, synthetic versions use water to penetrate and break down their polymer structure, typically resulting in lower tissue reactivity and more predictable absorption rates.

The synthetic absorbable sutures market is segmented by material, application, end user, and geography. Based on material, the market is segmented into polyglactin 910 (PGLA 910), polyglycolic acid (PGA), poliglecaprone 25 (PGCL), polydioxanone (PDO), polyglyconate, and glycomer 631. By applications, the market is segmented into general surgery, orthopedic surgery, cardiovascular & thoracic surgery, gynecology & obstetrics, gastrointestinal & colorectal, plastic & reconstructive, and others. By end user, the market is segmented into hospitals, ambulatory surgical centers (ASCs), and specialty clinics.

Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Polyglactin 910 (PGLA 910) |

| Polyglycolic Acid (PGA) |

| Poliglecaprone 25 (PGCL) |

| Polydioxanone (PDO) |

| Polyglyconate |

| Glycomer 631 |

| General Surgery |

| Orthopedic Surgery |

| Cardiovascular & Thoracic Surgery |

| Gynecology & Obstetrics |

| Gastrointestinal & Colorectal |

| Plastic & Reconstructive |

| Other Applications |

| Hospitals |

| Ambulatory Surgical Centers (ASCs) |

| Specialty Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Material | Polyglactin 910 (PGLA 910) | |

| Polyglycolic Acid (PGA) | ||

| Poliglecaprone 25 (PGCL) | ||

| Polydioxanone (PDO) | ||

| Polyglyconate | ||

| Glycomer 631 | ||

| By Application | General Surgery | |

| Orthopedic Surgery | ||

| Cardiovascular & Thoracic Surgery | ||

| Gynecology & Obstetrics | ||

| Gastrointestinal & Colorectal | ||

| Plastic & Reconstructive | ||

| Other Applications | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers (ASCs) | ||

| Specialty Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will global demand for synthetic absorbable sutures be by 2031?

It is projected to reach USD 5.30 billion, up from USD 3.33 billion in 2026 on a 9.75% CAGR.

Which material is growing fastest in hospital closures?

Poliglecaprone 25, a monofilament that reduces tissue drag, is advancing at a 10.54% CAGR through 2031.

Why are ambulatory surgical centers important buyers for sutures?

Reimbursement parity and same-day discharge drive more minimally invasive cases into ASCs, supporting a 10.47% CAGR for their suture purchases.

What regulation is reshaping U.S. sterilization of sutures?

EPA rules finalized in 2024 mandate 90% ethylene-oxide emission reductions, increasing compliance costs and prompting shifts to hydrogen-peroxide sterilization.

Page last updated on: