Switzerland Customer Data Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

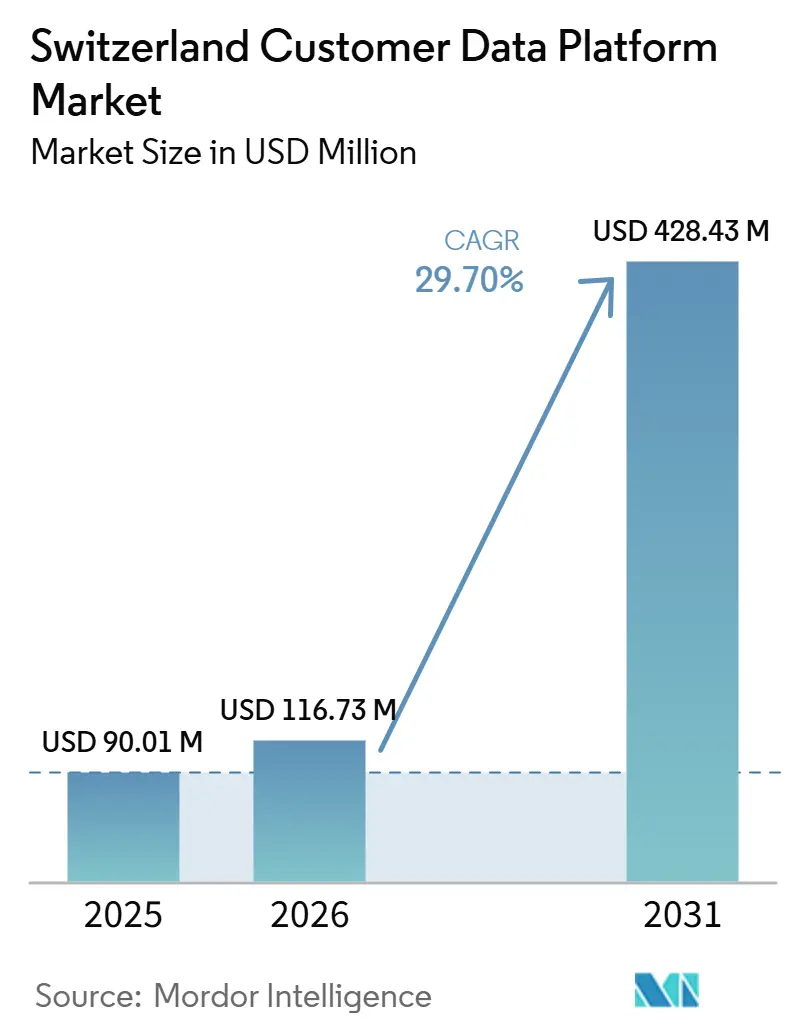

| Base Year Market Size (2025) | USD 90.01 Million |

| Market Size (2026) | USD 116.73 Million |

| Market Size (2031) | USD 428.43 Million |

| Growth Rate (2026 - 2031) | 29.70% CAGR |

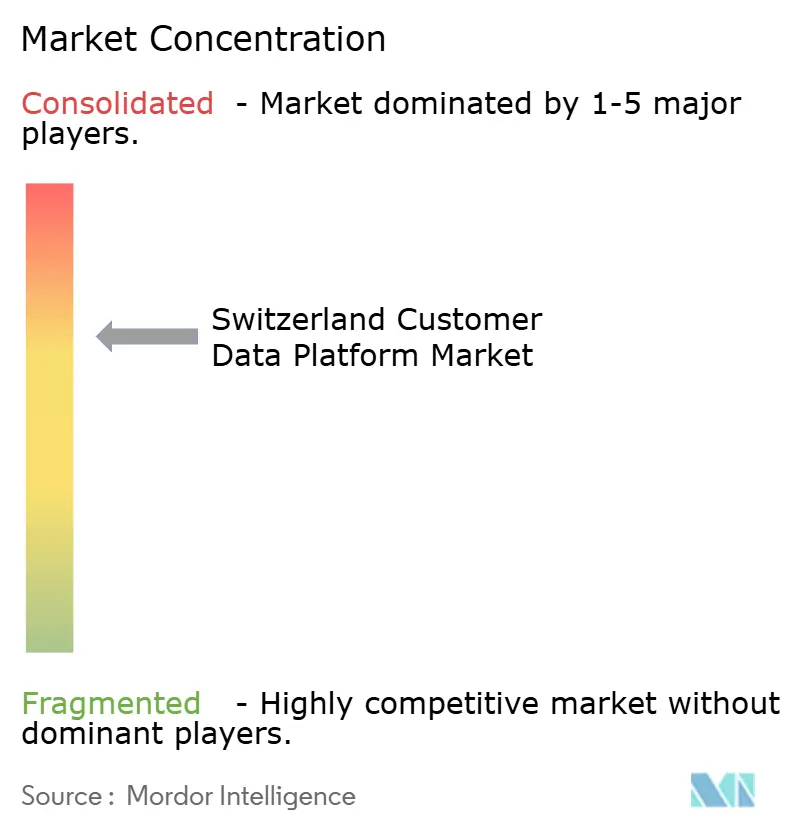

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Switzerland Customer Data Platform Market Analysis by Mordor Intelligence

The Switzerland customer data platform market size was valued at USD 90.01 million in 2025, USD 116.73 million in 2026, and is forecast to reach USD 428.43 million by 2031 at a CAGR of 29.70% from 2026 to 2031. Growth is being supported by stronger first-party data needs, continued modernization of data architecture in Swiss financial services, and stricter expectations around consent handling under the revised Swiss privacy framework. The country’s mix of banking, pharmaceuticals, and luxury retail gives the Switzerland customer data platform market a high concentration of enterprise demand despite its smaller national scale. Companies operating across Switzerland and the European Union also need data practices that work across more than one regulatory setting, which keeps identity resolution and consent-led design high on procurement agendas. Buyers are showing a clear preference for modular and composable platforms that can fit into existing CRM, ERP, and cloud environments without forcing full system replacement. Competition is therefore centered on global suite vendors with deep installed bases and specialist providers that can offer flexibility, data residency support, and faster activation for real-time personalization.

Key Report Takeaways

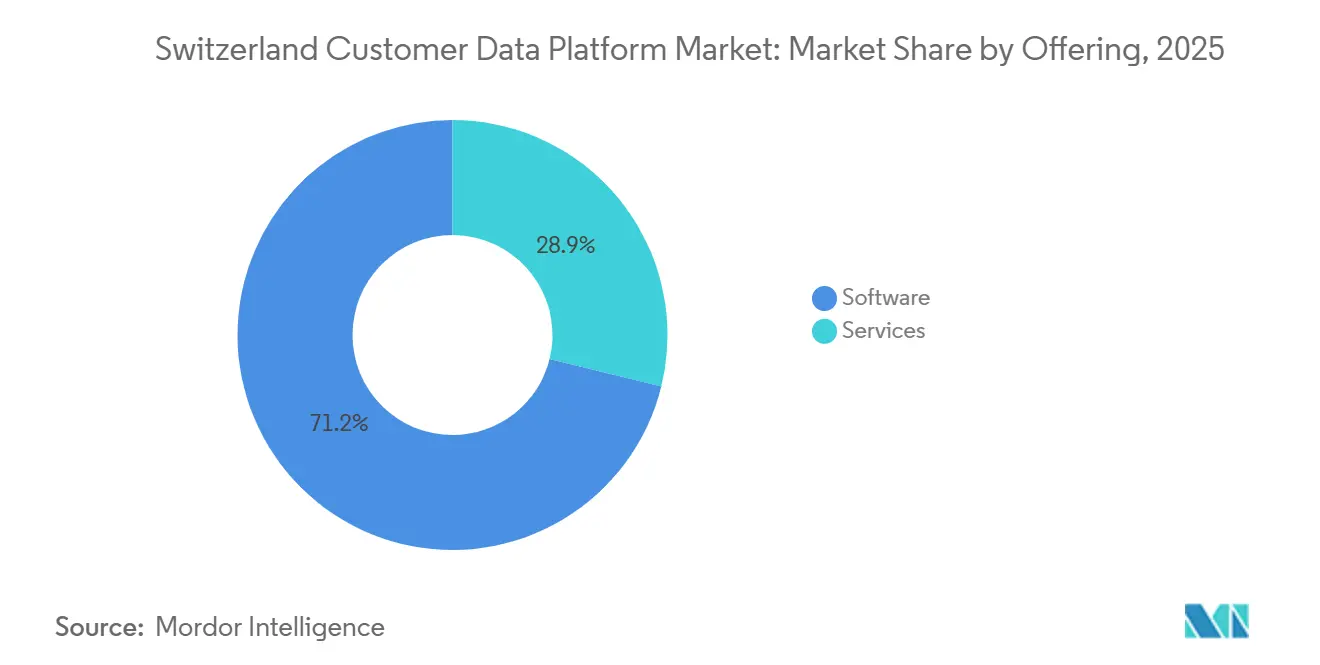

- By offering, software held 71.15% of revenue in Switzerland customer data platform market in 2025, while services are projected to expand at a 32.11% CAGR through 2031.

- By deployment mode, cloud accounted for 68.83% of revenue in 2025, while the same segment is projected to record the fastest growth at a 33.83% CAGR through 2031.

- By organization size, large enterprises held 63.19% of the Switzerland customer data platform market share in 2025, while small and medium enterprises are projected to expand at a 32.76% CAGR through 2031.

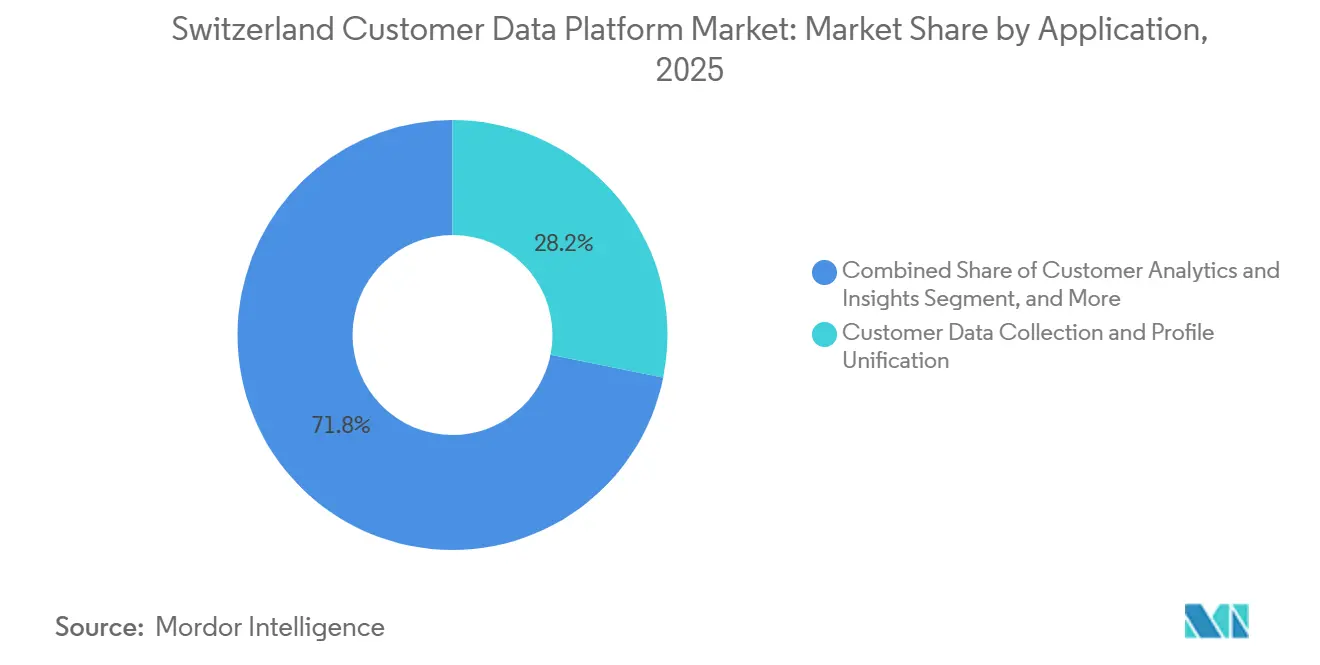

- By application, customer data collection and profile unification accounted for 28.16% share of the Switzerland customer data platform market size in 2025, while audience segmentation and personalization are projected to grow at a 34.26% CAGR through 2031.

- By end-user industry, retail and e-commerce held 24.76% of revenue in 2025, while healthcare and life sciences is projected to advance at a 34.61% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Switzerland Customer Data Platform Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising Need for Unified Customer Identity Resolution | +6.2% | Global, concentrated in Switzerland's BFSI and pharmaceutical clusters | Medium term (2-4 years) |

| Accelerating First-Party Data Activation Across Channels | +5.8% | Global, with early gains in Switzerland's retail and e-commerce sectors | Short term (≤ 2 years) |

| Swiss Privacy Compliance Driving Consent-Centric Architecture | +5.1% | National, with spillover to Swiss-EU cross-border firms | Medium term (2-4 years) |

| Growing Demand for Real-Time Personalization in High-Trust Sectors | +4.7% | National, concentrated in Zurich, Basel, and Geneva | Medium term (2-4 years) |

| Data Sovereignty Preference for Swiss and EU Hosting | +3.4% | National, with dual-hosting compliance demands across Swiss and EU regulatory zones | Long term (≥ 4 years) |

| Greater Use of Composable CDPs With Existing CRM and MarTech Stacks | +2.9% | Global, with early adoption among Swiss mid-market enterprises | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Need for Unified Customer Identity Resolution

Swiss financial institutions and pharmaceutical companies manage customer interactions across many channel systems that still hold incomplete identity records. In the Switzerland customer data platform market, this fragmentation weakens attribution, creates inconsistent engagement, and limits the value of consent-governed customer records. Swisscard AECS GmbH reported 73% attribution accuracy from the first touchpoint to a qualified credit application after its customer data platform program with Merkle, and it identified more than 40,000 end-to-end customer journeys within 6 months of activation.[1]Merkle, “Swisscard - Data-Driven Transformation,” Merkle, merkle.com That kind of outcome makes identity resolution useful far beyond campaign reporting, because the same profile layer can support onboarding, service routing, and governance tasks in regulated environments. The Switzerland customer data platform market is therefore moving toward a model where unified identity is treated as core operating infrastructure instead of a secondary marketing add-on.

Accelerating First-Party Data Activation Across Channels

The Switzerland customer data platform market is benefiting from a broader shift toward first-party data workflows that connect owned customer signals to activation across media, CRM, and on-site engagement. As Swiss companies collect more consented data through their own digital and physical touchpoints, the value of a platform that can organize and activate those records in near real time rises quickly. Adobe’s Real-Time CDP Collaboration launch in 2025 reflected this direction by enabling privacy-preserving first-party data collaboration across brands, publishers, and major data environments such as Snowflake and AWS.[2]Adobe Inc., “Adobe Announces General Availability of Real-Time CDP Collaboration for Brands to Jointly Drive Ad Performance in a Privacy-First Landscape,” Adobe Newsroom, news.adobe.com That shift favors operators that already built strong data capture foundations in 2024 and 2025, because each new interaction can sharpen segmentation and improve orchestration quality. The result is a compounding advantage for early adopters, which helps sustain momentum in the Switzerland customer data platform market.

Swiss Privacy Compliance Driving Consent-Centric Architecture

The revised Swiss privacy framework has pushed consent design and data governance closer to the center of CDP buying decisions in Switzerland. The nFADP requires organizations to take a more structured approach to handling personal data, and that requirement is especially important when operators work across sensitive categories or cross-border environments. Swiss government guidance for small and medium businesses also makes clear that the new law changes how companies need to think about data protection responsibilities in day-to-day digital operations. In the Switzerland customer data platform market, this has raised demand for platforms that can link identity resolution with granular consent records rather than treating consent as a separate legal file. Vendors that can show Swiss-ready governance, sensitive data controls, and practical support for compliance-led activation are likely to stay better positioned as procurement standards tighten.

Growing Demand For Real-Time Personalization in High-Trust Sectors

The Switzerland customer data platform market is also being lifted by demand for real-time personalization in sectors where customer trust is central to retention and growth. In banking, insurance, healthcare, and premium retail, outbound engagement needs to be relevant and fast, but it also needs to reflect live permission status and strong data handling discipline. That combination pushes buyers toward platforms that can enrich profiles and check consent status within the same operating flow, which narrows the set of acceptable vendors. Adobe’s April 2026 launch of CX Enterprise Coworker showed how vendors are extending CDP capability into real-time orchestration with structured and unstructured customer data brought together inside one environment. As the Switzerland customer data platform market matures, vendors that can combine speed, governance, and activation in one cycle are better placed to win larger enterprise programs.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High Integration Complexity With Legacy Banking, Retail, and ERP Systems | -3.2% | National, most acute in Switzerland's BFSI and industrial manufacturing sectors | Medium term (2-4 years) |

| Limited Internal CDP Skills in Mid-Market Enterprises | -2.6% | National, most pronounced in Swiss German-speaking SME clusters | Short term (≤ 2 years) |

| Elevated Privacy Review and Legal Approval Cycles | -2.1% | National, with dual-compliance friction for Swiss firms operating under both nFADP and GDPR | Medium term (2-4 years) |

| Fragmented Customer Data Ownership Across Business Units | -1.8% | Global, with structural complexity in Switzerland's decentralized banking and retail organizations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Integration Complexity With Legacy Banking, Retail, and ERP Systems

Legacy banking platforms, retail systems, and ERP environments remain a major practical barrier for the Switzerland customer data platform market. Many Swiss enterprises still hold customer, transaction, pricing, and service data across separate technology layers that were not designed to work as a single real-time system. This raises integration costs, lengthens implementation timelines, and delays the point at which a signed CDP program starts delivering measurable value. FINMA’s continued emphasis on digitalization and data-based supervision shows why regulated institutions continue to invest in data capabilities, but it also underscores the complexity of the operating environment that those firms need to modernize. The Switzerland customer data platform market will continue to face this restraint until vendors and implementation partners reduce the custom work required to connect older core systems with modern activation layers.

Limited Internal CDP Skills in Mid-Market Enterprises

Limited in-house expertise is another clear brake on the Switzerland customer data platform market, especially outside the largest enterprise accounts. Mid-market organizations often need help with data modeling, workflow design, multilingual campaign logic, and ongoing CDP operations after the initial deployment is complete. That is one reason vendors are introducing tools meant to lower the technical burden for operating complex customer data environments. Treasure Data’s launch of Treasure Code in February 2026 was positioned around this need by allowing teams to manage data workflows, segment logic, and customer journeys with natural language instructions inside a code-based operating model. Until more Swiss mid-market firms develop stronger day-to-day CDP capability, the Switzerland customer data platform market is likely to stay tilted toward managed support, bundled solutions, and slower iteration outside the large enterprise segment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Dominance Reflects Platform-First Procurement Logic

Software accounted for 71.15% of revenue in the Switzerland customer data platform market in 2025, which shows that buyers still place the platform layer ahead of services when building customer data capability. That preference is strongest in banking, pharmaceuticals, and retail, where enterprises want a governed data foundation before they expand into activation, analytics, or AI-led automation. Buyers also favor modular architecture that can work with existing CRM, ERP, and warehouse tools instead of forcing a full replacement of the current stack. Adobe’s April 2026 expansion of Real-Time CDP functions through CX Enterprise Coworker reinforced this software-first pattern by linking structured and unstructured data inside a broader customer experience platform.

Services are projected to grow at a 32.11% CAGR from 2026 to 2031, which keeps the support layer important even as software remains dominant. The Switzerland customer data platform industry still requires implementation help, integration support, operating discipline, and change management, especially when buyers lack mature internal teams. Treasure Data’s Treasure Code launch points to the same issue, because tools that simplify operations still do not remove the need for setup, governance, and ongoing adaptation.[3]Treasure Data, “Treasure Data Unveils Treasure Code, Bringing Agentic AI to Customer Data Operations,” Treasure AI Press Releases, treasure.ai This means the Switzerland customer data platform market should continue rewarding vendors and partners that can pair strong product capability with practical services that help clients move from deployment to measurable use.

By Deployment Mode: Cloud Preference Anchored By Sovereignty Infrastructure

Cloud held 68.83% of the Switzerland customer data platform market size in 2025, which reflects the scalability and operating flexibility that cloud-native environments offer to enterprises handling large profile volumes. This preference is strengthened by the need to connect customer data across channels without adding too much internal infrastructure overhead. FINMA’s digital and supervisory direction keeps domestic data governance and operational oversight important for regulated institutions, which shapes where sensitive data environments are hosted and managed. Google Cloud’s work with AXA Switzerland also shows that large financial services organizations are already building broader AI and data transformation programs on cloud infrastructure in the country.

Cloud is also the fastest-growing deployment mode, with a projected 33.83% CAGR through 2031 in the Switzerland customer data platform market. That growth is supported by the fact that firms can now pursue residency-aware cloud models while still keeping sensitive governance and compliance requirements in view. On-premises deployments remain relevant where data egress restrictions are stricter, but they are likely to stay limited to narrower use cases. Hybrid models also remain useful, because they let firms keep sensitive elements closer to internal control while moving analytics and activation workloads into more flexible environments under the revised Swiss data protection framework. The Switzerland customer data platform market therefore continues to favor vendors that can support cloud scale without weakening sovereignty or compliance discipline.

By Organization Size: Large Enterprises Hold the Lead While SMEs Accelerate

Large enterprises held 63.19% of the Switzerland customer data platform market share in 2025, which reflects the capital intensity and organizational complexity of full CDP programs. These buyers already have deeper governance structures, larger technology budgets, and more established relationships with major software and cloud providers. They are also more likely to operate across many business units and customer touchpoints, which makes the value of unified data architecture easier to justify. In the Switzerland customer data platform market, it keeps banking, pharmaceutical, and premium retail enterprises at the front of spending.

Small and medium enterprises are projected to grow at a 32.76% CAGR through 2031, which makes them the faster-moving size segment even from a smaller base. Entry barriers are easing as more vendors package CDP capability into simpler bundles, managed models, and tools that reduce technical workload. SAP has also continued to emphasize governed data harmonization and embedded AI within broader business suites, which supports a more structured route into customer data activation for companies that already rely on SAP environments.[4]SAP SE, “Haleon Chooses SAP Solutions to Accelerate Growth Through Technology,” SAP News Center, news.sap.com The Switzerland customer data platform industry is therefore broadening beyond the largest accounts, although mid-market users will still depend more heavily on guided onboarding and external support than large enterprises.

By Application: Data Unification Anchors Demand While Personalization Leads Growth

Customer data collection and profile unification was the largest application in 2025, with a 28.16% revenue share in the Switzerland customer data platform market. That ranking shows that many buyers are still solving the foundation problem first, which is creating one governed, persistent customer record from many fragmented sources. The revised Swiss privacy framework adds weight to this use case because data handling, consent, and identity need to work together in a controlled operating model. Government guidance for smaller businesses also reinforces that stronger protection practices now need to be built into ordinary digital processes rather than handled only at the legal review stage.

Audience segmentation and personalization is projected to grow at a 34.26% CAGR through 2031, which makes it the fastest-rising application in the Switzerland customer data platform market. That shift usually comes after the first stage of deployment, when firms have already completed enough profile unification to support more active campaign and journey use. Custobar’s work with Schuhhaus Walder AG, which unified 200,000 customer profiles across physical stores and a Shopware 6 e-commerce platform, shows the kind of omnichannel activation that becomes possible once the data layer is in place. As a result, campaign orchestration and consent-led activation are becoming more commercially important inside the Switzerland customer data platform market as earlier deployments move into a more mature operating phase.

By End-User Industry: Retail Leads Revenue While Healthcare and Life Sciences Grows Fastest

Retail and e-commerce held 24.76% share of the Switzerland customer data platform market size in 2025, which made it the largest end-user segment. Switzerland’s retail structure combines dense physical networks with steady digital commerce activity, and that creates strong demand for unified customer records that work across store, web, and loyalty channels. The country’s multilingual consumer environment adds another layer, because retailers often need localized activation from a shared profile base. Custobar’s Schuhhaus Walder AG deployment reflects this operational need by connecting in-store and e-commerce customer data into one environment for omnichannel use.

Healthcare and life sciences are projected to expand at a 34.61% CAGR through 2031 in the Switzerland customer data platform market. This segment is being supported by stronger patient engagement needs and stricter handling of sensitive personal data under Swiss privacy law. BFSI remains one of the most important demand centers, with CDP use tied to onboarding, attribution, product relevance, and churn reduction, and the Swisscard program is a clear example of measurable impact in that environment. Manufacturing and public administration remain smaller but developing areas, especially where organizations want more direct and consent-governed digital engagement with customers, partners, or citizens.

Geography Analysis

The Switzerland customer data platform market size stood at USD 90.01 million in 2025, and its geographic pattern is shaped more by regulation and sector clustering than by the scale of the national population. Switzerland operates with a privacy framework that is closely aligned with European practice while still retaining its own legal requirements, which creates a distinct operating setting for domestic and cross-border data programs. This gives the Switzerland customer data platform market a different demand profile from neighboring European markets, because buyers need platforms that can support both growth and legal control. Zurich remains the main spending center, supported by banking, insurance, and large corporate demand, while Basel and Geneva matter for pharmaceuticals and luxury retail activity.

The Switzerland customer data platform market is also tied closely to cross-border data movement and infrastructure decisions. Companies that work across Switzerland and the European Union need architectures that can keep customer identity, consent, and activation aligned across more than one regulatory setting.[5]Swiss Federal Department of Economic Affairs, Education and Research, “New Federal Act on Data Protection (nFADP),” KMU Admin, kmu.admin.ch FINMA’s focus on digitalization and data-led supervision keeps data control and operating resilience important for financial institutions, which directly affects where cloud-based customer data environments can gain traction. Google Cloud’s published work with AXA Switzerland shows that large Swiss insurers are already using domestic cloud and AI infrastructure to improve operational processes and customer interaction workflows. This wider infrastructure base supports cloud CDP adoption, but it also keeps vendor scrutiny high in regulated sectors.

Regional demand inside Switzerland is not uniform, even within a compact national market. German-speaking commercial zones often place more weight on integration with established ERP and enterprise data environments, while French-speaking organizations tend to show stronger alignment with global marketing cloud ecosystems. Industrial areas such as Winterthur, St. Gallen, and Ticino are starting to widen the use of CDPs beyond the standard banking and retail footprint as firms explore more direct digital engagement. Ticino also adds relevance for Italian-language configurations tied to cross-border commercial activity. Taken together, these patterns mean the Switzerland customer data platform market rewards vendors that can combine compliance support, multilingual configuration, and flexible implementation models across a small but high-value geography.

Competitive Landscape

The Switzerland customer data platform market is moderately concentrated, with Salesforce, Adobe, and SAP holding strong positions in large enterprise accounts because they already sit inside broader CRM, ERP, and marketing technology environments. That installed-base advantage raises switching costs and gives the largest vendors a practical edge in regulated and systems-dense customer environments. At the same time, specialist and composable providers still compete by offering stronger interoperability, usage flexibility, and less dependence on one software ecosystem. This split keeps the Switzerland customer data platform market active at both the suite-vendor level and the specialist architecture level. Buyers are therefore not choosing only on feature depth, because deployment fit, governance readiness, and operating model support also matter.

Adobe strengthened its position in April 2026 when it introduced CX Enterprise Coworker on the Adobe Experience Platform, extending Real-Time CDP with harmonized unstructured data profiles, broader reporting, and multi-agent workflow support. SAP also reinforced its data harmonization strategy in March 2026 through Haleon’s adoption of SAP Business Suite and SAP Business Data Cloud, which underlined SAP’s push to connect governed enterprise data with embedded AI capabilities. Treasure Data added another competitive signal in February 2026 with Treasure Code, which aimed to simplify CDP operations through an AI-native command-line interface for workflows, segment logic, and journey management. These moves show that competition in the Switzerland customer data platform market is shifting from simple data unification toward governed automation and easier operating models. Vendors that cannot show progress in both control and activation are likely to find it harder to stand apart.

The strongest white-space areas remain healthcare, multilingual mid-market deployments, and composable activation models built around existing cloud data foundations. Healthcare is important because sensitive data rules make governance capability more central to buying decisions than in many other customer environments. Mid-market demand is also meaningful because many Swiss firms still need simpler onboarding and more guided day-to-day operation than large enterprises do. That leaves room for vendors that can reduce operating complexity without stripping out compliance control. Overall, the Switzerland customer data platform market continues to favor providers that combine installed-base strength or architectural flexibility with clear proof that they can support Swiss regulatory, linguistic, and enterprise requirements.

Switzerland Customer Data Platform Industry Leaders

Adobe Inc.

Salesforce, Inc.

Tealium, Inc.

SAP SE

SAS Institute Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Adobe unveiled CX Enterprise Coworker at Adobe Summit, an agentic AI system built on the Adobe Experience Platform that extends Adobe Real-Time CDP with harmonized unstructured data profiles, expanded audience-level reporting across major digital destinations, and multi-agent orchestration via Model Context Protocol (MCP) and Agent2Agent (A2A) standards. The launch integrates with AI infrastructure from AWS, Anthropic, Google Cloud, Microsoft, and OpenAI, directly relevant to Swiss enterprises managing multi-format customer data across BFSI and healthcare.

- March 2026: SAP SE announced Haleon's adoption of SAP Business Suite, including the SAP Business Data Cloud solution to harmonize SAP and third-party data in a governed single source of truth with embedded AI and agentic AI capabilities. The deal underscores SAP's strategy of positioning CDP-adjacent data harmonization within enterprise data platforms, with direct relevance to Swiss multinational pharmaceutical and consumer health clients.

- February 2026: Treasure Data launched Treasure Code, an AI-native command-line interface enabling CDP operations teams to manage data workflows, segment logic, and customer journeys as code using natural language instructions with Claude Code integration. The tool is designed to reduce the technical barrier for CDP operations in enterprises with established data engineering practices, addressing the skill gap that constrains mid-market Swiss CDP adoption.

- February 2025: Adobe announced general availability of Real-Time CDP Collaboration in the United States, enabling advertisers and publishers to collaborate on first-party data within a privacy-preserving clean room environment, with integrations including Snowflake, AWS, LiveRamp, and TransUnion. The clean room data collaboration model addresses the first-party data activation challenge facing Swiss retailers and media companies operating in a consent-regulated environment.

Switzerland Customer Data Platform Market Report Scope

The Switzerland customer data platform market is defined as the market for platforms and services that collect, integrate, and consolidate customer data from multiple sources into unified, centralized customer profiles. These platforms enable identity resolution, real-time data integration, segmentation, personalization, and analytics, helping Swiss enterprises deliver consistent omnichannel customer experiences. The market is influenced by Switzerland’s strong financial services sector, advanced digital adoption, and strict compliance requirements under the EU GDPR and the Swiss Federal Act on Data Protection (FADP). It also focuses on secure, AI-driven personalization and scalable martech solutions across industries such as banking, retail, and healthcare.

The Switzerland Customer Data Platform Market Report is Segmented by Offering (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid) Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Customer Data Collection and Profile Unification, Audience Segmentation and Personalization, Marketing Campaign and Customer Journey Orchestration, Customer Analytics and Insights, Consent and Preference Management, and Other Applications), and End-User Industry (Retail and E-Commerce, Banking, Financial Services, and Insurance (BFSI), Healthcare and Life Sciences, IT and Telecom, Media and Entertainment, Industrial Manufacturing, Government and Public Administrationm and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization |

| Marketing Campaign and Customer Journey Orchestration |

| Customer Analytics and Insights |

| Consent and Preference Management |

| Other Applications |

| Retail and E-Commerce |

| Banking, Financial Services, and Insurance (BFSI) |

| Healthcare and Life Sciences |

| IT and Telecom |

| Media and Entertainment |

| Industrial Manufacturing |

| Government and Public Administration |

| Other End-User Industries |

| By Offering | Software |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization | |

| Marketing Campaign and Customer Journey Orchestration | |

| Customer Analytics and Insights | |

| Consent and Preference Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| Banking, Financial Services, and Insurance (BFSI) | |

| Healthcare and Life Sciences | |

| IT and Telecom | |

| Media and Entertainment | |

| Industrial Manufacturing | |

| Government and Public Administration | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current and forecast value of the Switzerland customer data platform space?

It was valued at USD 90.01 million in 2025, and reaches USD 116.73 million in 2026, and is forecast to reach USD 428.43 million by 2031, growing at a 29.70% CAGR from 2026 to 2031.

Which offering leads spending in Switzerland customer data platforms?

Software led spending with a 71.15% revenue share in 2025, showing that buyers still prioritize the platform layer before services.

Why is cloud deployment gaining so much traction in Switzerland?

Cloud held 68.83% share in 2025 and is projected to grow at a 33.83% CAGR because it offers scale, faster activation, and better fit with modern data infrastructure, while vendors also support data residency and governance needs.

Which application is growing the fastest in Switzerland customer data platforms?

Audience segmentation and personalization is the fastest-growing application, with a projected 34.26% CAGR through 2031, as earlier deployments move from profile building into active campaign use.

Which end-user group is creating the most revenue and which is growing the fastest?

Retail and e-commerce led with 24.76% share in 2025, while healthcare and life sciences is projected to grow the fastest at a 34.61% CAGR through 2031.

What is the main barrier slowing adoption among mid-sized Swiss companies?

The biggest barriers are integration complexity and limited internal CDP skills, which increase reliance on managed services, guided onboarding, and bundled technology models.

Page last updated on: