Switzerland CRM Marketing Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

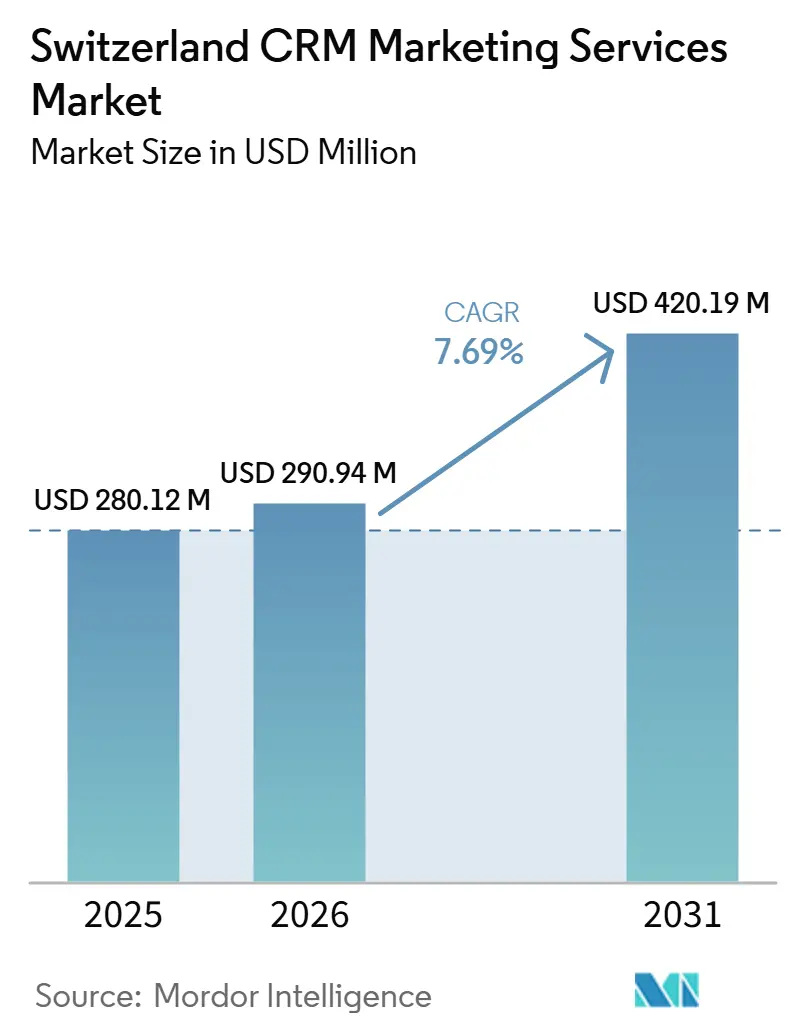

| Base Year Market Size (2025) | USD 280.12 Million |

| Market Size (2026) | USD 290.94 Million |

| Market Size (2031) | USD 420.19 Million |

| Growth Rate (2026 - 2031) | 7.69% CAGR |

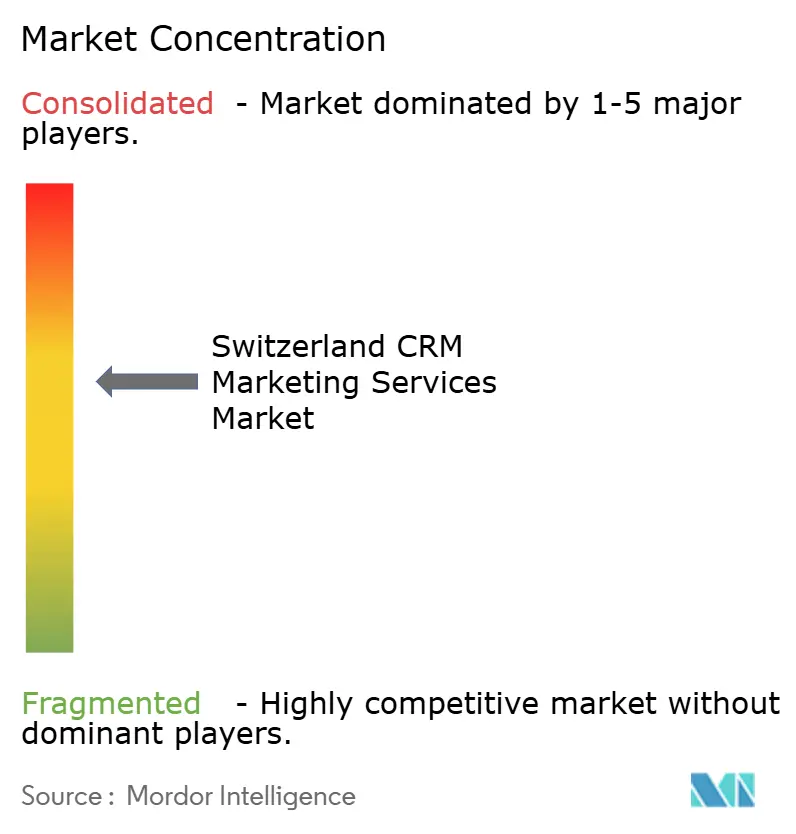

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Switzerland CRM Marketing Services Market Analysis by Mordor Intelligence

The Switzerland CRM Marketing Services Market size was valued at USD 280.12 million in 2025 and estimated to grow from USD 290.94 million in 2026 to reach USD 420.19 million by 2031, at a CAGR of 7.69% during the forecast period 2026-2031. The Switzerland CRM Marketing Services Market is expanding because companies are using CRM-linked marketing services to increase revenue productivity in a high-cost operating environment, rather than treating CRM as a basic contact management tool. Demand is also rising because customer engagement programs in Switzerland must work across German, French, and Italian language contexts, which increases the need for more coordinated campaign planning, data handling, and service execution. The shift toward consent-first customer data management is making CRM programs more central to commercial decision-making, especially where customer communications must remain auditable and locally compliant. Competitive conditions are moderate in large enterprise accounts, where global platforms support complex programs, while the mid-market remains more fragmented, as Swiss-hosted and multilingual providers still hold a strong position in regulated and localization-heavy use cases. The Switzerland CRM Marketing Services Market is also being shaped by the shortage of platform-certified CRM and MarTech talent, which is slowing some in-house programs while creating stronger demand for managed services, implementation support, and long-term operating partnerships.

Key Report Takeaways

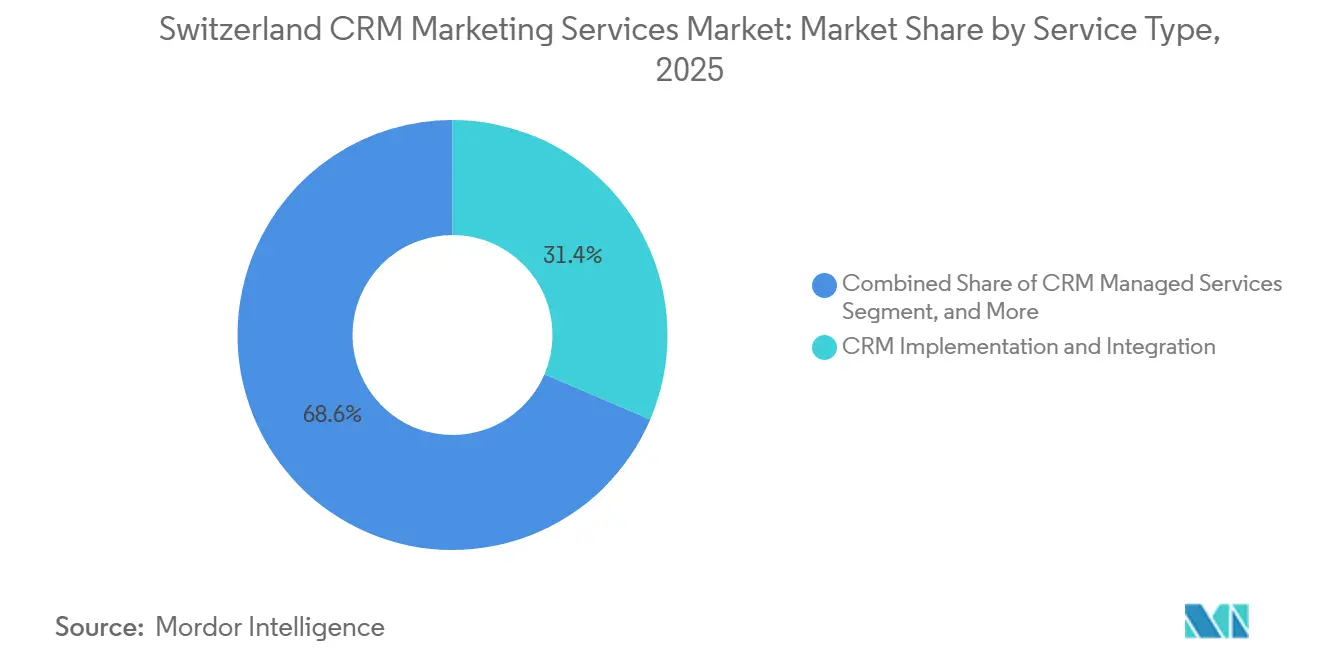

- By service type, CRM Implementation and Integration held 31.42% of the Switzerland CRM Marketing Services Market in 2025, while CRM Managed Services is projected to expand at a 9.81% CAGR through 2031.

- By enterprise size, large enterprises accounted for 64.81% share in 2025, while small and medium enterprises are expected to record the highest CAGR of 9.24% through 2031.

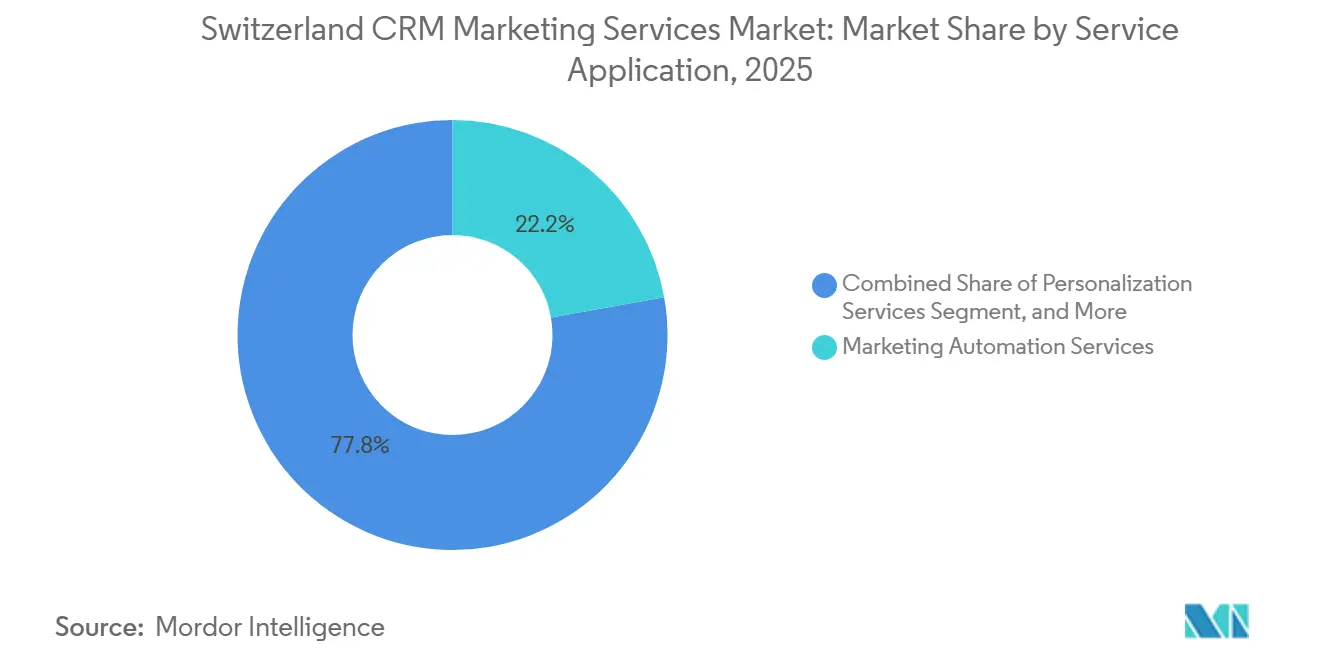

- By service application, Marketing Automation Services captured 22.19% share in 2025, while Personalization Services is projected to grow at a 9.68% CAGR through 2031.

- By end-user industry, BFSI held 26.74% share in 2025, while Retail and E-commerce is projected to advance at an 8.93% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Switzerland CRM Marketing Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Personalized Omnichannel Campaign Orchestration | +2.1% | National, with strongest demand in Zurich, Geneva, and Basel commercial corridors | Short term (≤ 2 years) |

| Growing Shift Toward First-Party Data Activation | +1.6% | National, with early adoption concentrated in BFSI and Retail clusters across German-speaking Switzerland | Medium term (2-4 years) |

| Need for Consent-Driven Lifecycle Marketing in Regulated Industries | +1.4% | National, nDSG and revFADP compliance obligations apply uniformly across all cantons | Short term (≤ 2 years) |

| Increasing Use of AI to Automate Segmentation and Next Best Action | +1.2% | National, with higher AI maturity in large enterprises in Zurich and Lausanne | Medium term (2-4 years) |

| High Cost Pressure on Swiss Commercial Teams | +0.6% | National, with wage pressure most visible in Zurich, Zug, and Geneva | Long term (≥ 4 years) |

| Multilingual Customer Journeys Across Cantons and Border Regions | +0.4% | National, with spillover into French-speaking Alsace and Italian-speaking Lombardy border zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Personalized Omnichannel Campaign Orchestration

Swiss enterprises are moving away from isolated channel campaigns and toward CRM environments that coordinate email, mobile, web, and branch interactions across the full customer journey. Switzerland’s multilingual setting makes this shift even more urgent, as customer behavior differs across German-, French-, and Italian-speaking markets, reducing the value of static campaign templates. Customer experience and personalization were identified as leading priorities for Swiss marketing decision-makers in 2026, indicating that buyers are focusing on operational execution rather than solely testing new ideas.[1]Serviceplan Group Switzerland, “CMO Barometer 2026, Schweizer Marketing-Entscheider Zwischen Vorsicht Und KI,” House of Communication Switzerland, house-of-communication.com This is raising the bar for service providers, as buyers increasingly expect pre-integrated orchestration models rather than disconnected platform deployments. It also favors providers that can connect in-store, online, and service-center activity to centralized CRM triggers while adapting campaigns for canton-level language realities.

Growing Shift Toward First-Party Data Activation

The Switzerland CRM Marketing Services Market is seeing stronger demand for loyalty programs, preference centers, and progressive profiling tools as enterprises seek to manage customer data assets directly within CRM workflows. This change is especially evident in banking, where the Swiss Bankers Association stated that using general relationship data for the personalized marketing of third-party products requires explicit customer consent beyond standard onboarding terms.[2]Swiss Bankers Association, “Guideline, Handling Data in Day-to-Day Business,” Swiss Banking, swissbanking.ch As a result, first-party data activation is becoming less of a campaign issue and more of a structural CRM design issue. This is creating longer-term demand for CRM migration, modernization, and data architecture services, as consent capture, storage, and activation now need to work together within the same operating model. The Switzerland CRM Marketing Services Market is therefore benefiting from a broader move toward trust-led customer engagement, where better-governed first-party data supports stronger personalization over time.

Need for Consent-Driven Lifecycle Marketing In Regulated Industries

Regulated sectors are placing a heavier weight on consent architecture because CRM communications now need to remain transparent, traceable, and easy to defend during internal review. In Swiss financial services, this need is reinforced by the way customer data use, auditability, and operational controls are tied to day-to-day marketing execution. Valiant Bank AG’s selection of the BSI Customer Suite in October 2025 showed how strongly data residency and Swiss-only storage now influence CRM platform choices in regulated accounts.[3]BSI Software AG, “Personalized Customer Experiences at Valiant with the BSI Customer Suite,” BSI Software AG, bsi-software.com The same pressure applies in healthcare and life sciences, where customer and patient communications must be clearly separated by purpose inside the CRM environment. This is pushing the Switzerland CRM Marketing Services Market toward a two-track structure, where global platforms compete for complex enterprise mandates and Swiss-aligned providers gain traction where local storage and audit readiness matter more.

Increasing Use of AI to Automate Segmentation and Next Best Action

The Switzerland CRM Marketing Services Market is also being lifted by stronger enterprise interest in AI-driven segmentation, orchestration, and next-best-action workflows. Microsoft reported in April 2025 that 52% of Swiss organizations used AI agents to automate entire business processes, ahead of both the global and European averages.[4]Microsoft Switzerland, “2025 Work Trend Index, Swiss Organizations Lead in AI Adoption, 52% Automate Entire Business Processes, Surpassing Global and European Averages,” Microsoft Switzerland News Center, news.microsoft.com At the same time, the IMC-HSG AI Marketing Executive Pulse 2025 found that Swiss companies expected to increase AI budgets by 67% over the next 2 to 5 years, while only 12% of executives used AI tools daily in 2025. That gap between investment intent and everyday execution is creating a practical role for CRM implementation partners to turn AI features into operational segmentation models and campaign logic. It also strengthens the case for managed service contracts, as model tuning, governance, and campaign optimization are becoming ongoing operational tasks rather than one-off deployment projects.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Privacy and Consent Management Complexity | -1.4% | National, most acute in BFSI clusters in Zurich, Geneva, and Basel, and in healthcare hubs in Basel and Bern | Short term (≤ 2 years) |

| Shortage of CRM and MarTech Operations Talent | -1.0% | National, particularly severe in high-cost cantons of Zurich, Zug, and Geneva | Medium term (2-4 years) |

| Fragmented Legacy Sales and Service Stacks | -0.6% | National, with highest fragmentation in industrial manufacturing and mid-market firms outside Zurich | Long term (≥ 4 years) |

| High Integration Cost for Midmarket Deployments | -0.5% | National, and more visible among SMEs in non-metropolitan cantons with tighter IT budgets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Privacy and Consent Management Complexity

The Switzerland CRM Marketing Services Market faces slower deployment cycles because privacy and consent controls now affect the structure of CRM programs at a detailed operational level. Swiss organizations are more cautious because the revised law places individual accountability at the center of compliance decisions, and non-compliance can trigger fines of up to CHF 250,000 (USD 282,500). The October 2025 guidance around cookies and consent further narrowed the room for weak transparency practices across digital customer touchpoints. This means many firms need more legal review, more configuration work, and stronger internal approval before they activate new CRM journeys. Mid-market companies feel this restraint more sharply because they often rely on service providers to deliver both technical execution and compliance discipline within a single engagement.

Shortage of CRM And Martech Operations Talent

The Switzerland CRM Marketing Services Market is also constrained by a shortage of platform-certified CRM and MarTech specialists who can support both technical and commercial execution. The challenge is broader than headcount, as many programs also need bilingual or trilingual operators to manage campaigns across German-, French-, and Italian-speaking customer bases. The IMC-HSG AI Marketing Executive Pulse 2025 showed that many Swiss companies were still early in their practical AI adoption, indicating that platform capabilities are advancing faster than in-house operating readiness. This shortage slows new program launches and increases reliance on external partners for compliance monitoring, campaign operations, and AI-enabled optimization. Over time, it supports growth in managed services, but in the near term, it limits how quickly some buyers can expand CRM marketing activity with internal teams alone.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Managed Services Gain Ground As Core Implementations Mature

CRM Implementation and Integration held 31.42% of the Switzerland CRM Marketing Services Market share in 2025, which reflected the continued scale of platform migration and stack consolidation work across Swiss enterprises. The leading position of this segment came from the difficulty of connecting major CRM platforms to Switzerland-specific ERP environments, compliance controls, and multilingual data structures. Helvetia Schweiz’s move from SAP CRM to a Salesforce-based sales and marketing platform demonstrated how broad these projects can be, spanning partner relationship management, campaign migration, field sales enablement, and change management. Strategy and consulting services remained important at the front end because buyers still needed operating model decisions before platform work could begin. Training and support also became relevant after deployment, as many teams were still learning to apply AI-enabled CRM features in day-to-day marketing work.

CRM Managed Services is projected to grow at a 9.81% CAGR from 2026 to 2031, which made it the fastest-expanding service type in the Switzerland CRM Marketing Services Market. This growth is tied to talent shortages, rising compliance overhead, and the operational demands of AI-augmented customer engagement programs. Buyers are increasingly outsourcing ongoing campaign management, model tuning, data governance, and audit-readiness instead of building large in-house teams for every workflow. The revised compliance environment also supports this trend because periodic reviews of data handling, consent flows, and architecture controls are becoming part of normal CRM operations. As a result, managed services are moving from a support role to a core operating model for companies that want stable execution without carrying full internal capability across every platform layer.

By Enterprise Size: Large Enterprises Lead Today While SMEs Accelerate Faster

Large enterprises accounted for 64.81% of the Switzerland CRM Marketing Services Market in 2025, reflecting the scale and complexity of CRM programs inside financial institutions, pharmaceutical companies, and premium consumer brands. These organizations often run multi-language, multi-entity, and multi-segment customer programs, which increases both project size and service intensity. Larger Swiss firms also showed stronger use of proprietary AI models inside marketing functions, which pointed to a deeper level of CRM maturity than in smaller accounts. Their spending profile supports longer implementation cycles, wider integration scopes, and more advanced personalization requirements. It also helps large enterprises remain the anchor customers for the enterprise tier of the Switzerland CRM Marketing Services Market.

Small and medium enterprises are projected to grow at a 9.24% CAGR from 2026 to 2031, making them the fastest-growing enterprise segment. This growth reflects a structural shift, as cloud-native tools have lowered the entry barriers to CRM marketing deployment. The Swiss SME association reported that the share of Swiss SMEs using AI for customer relationship management rose from 16% in 2024 to 20% in 2025, with marketing automation and targeted advertising showing the strongest momentum. Compliance also plays a role because smaller firms that once relied on spreadsheets are moving into consent-capable CRM systems to document customer data handling more clearly. This means SME demand is no longer only a cost-driven adoption story, and it is increasingly linked to formalization, auditability, and easier access to scalable customer engagement tools.

By Service Application: Personalization Becomes More Strategic Than Basic Automation

Marketing Automation Services held 22.19% of the service application segment in 2025, indicating that scheduled campaigns, email journeys, and lead-scoring programs were already well established among Swiss enterprise buyers. In the Switzerland CRM Marketing Services Market, this segment benefited from years of workflow digitization in customer acquisition and retention programs. Automation still matters, but it is no longer enough on its own, as buyers now expect more adaptive customer journeys built on real-time behavioral signals. Omnichannel engagement is therefore becoming increasingly important as firms seek to connect web activity, app usage, and physical channel interactions into a single customer view. Customer analytics and insight services support that shift because boards want clearer evidence of ROI before approving larger CRM budgets. The segment remains important, but its role is now more foundational than differentiating.

Personalization Services is projected to expand at a 9.68% CAGR from 2026 to 2031, making it the fastest-growing application area in the Switzerland CRM Marketing Services Market. This growth reflects the combination of richer first-party data environments and stronger use of AI-enabled decisioning tools. Merkle’s Swisscard case study showed how previously disconnected data can be integrated into a CDP that supports real-time, channel-specific personalization at scale. Campaign management services also remain relevant because multilingual execution in Switzerland often requires culturally adapted content for German-, French-, and Italian-speaking customer groups. That language complexity supports a service premium in Switzerland because the work involves more than translation and requires market-specific configuration, approval logic, and campaign handling.

By End-User Industry: BFSI Holds The Largest Share While Retail And E-Commerce Expands Fastest

BFSI accounted for 26.74% of the Switzerland CRM Marketing Services Market size in 2025, which reflected Switzerland’s position as a major financial center and the sector’s high compliance burden. Banks and insurers need CRM programs that can support growth, retention, and personalization while remaining aligned with customer consent and operational control requirements. The PostFinance deployment of SAS Customer Intelligence illustrated the scale of these programs, with lifecycle campaigns serving 3 million customers and using event-based triggers linked to life-stage changes. Raiffeisen Switzerland’s use of BSI Customer Suite also showed the value of unified customer data views and Swiss-territory data storage in service operations. Healthcare and life sciences followed as another important vertical because customer and patient communication workflows need careful separation by purpose and data category. This raises service complexity and supports longer project durations in that vertical.

Retail and E-commerce is projected to grow at an 8.93% CAGR from 2026 to 2031, making it the fastest-growing end-user group in the Switzerland CRM Marketing Services Market. Swiss retailers are investing more in loyalty-linked CRM programs as cross-border digital competition increases pressure on retention and repeat purchase behavior. Information technology and telecom buyers are also active because subscriber lifecycle management, churn control, and customer support automation depend heavily on CRM-led engagement workflows. Industrial manufacturers are adopting these services for B2B retention programs, although fragmented legacy systems still make deployments slower and more customized. Government and public administration is emerging as a smaller but meaningful user group because multilingual constituent communication remains a practical need across federal and canton-level interactions. Other end users, including luxury goods, hospitality, and education, are adopting at different speeds based on digital maturity, internal skills, and the need for compliant customer communications.

Geography Analysis

German-speaking Switzerland held the largest share of demand in 2025, supported by the concentration of financial institutions, pharmaceutical activity, and precision manufacturing across Zurich, Basel, Bern, and St. Gallen. Zurich functions as the main CRM and digital transformation hub because large enterprise buying decisions, multinational headquarters, and higher-value implementation mandates are concentrated there. Basel adds a distinct demand profile, as healthcare and life sciences organizations require tighter controls over data use, customer communication, and workflow validation. The region also benefits from a stronger base of implementation and activation partners that can extend global CRM platforms into localized service engagements. The Switzerland CRM Marketing Services Market, therefore, draws a large part of its enterprise-scale demand from the German-speaking side of the country, where technical complexity and contract values are typically higher.

French-speaking Switzerland, centered on Geneva and Lausanne, represents a different demand mix shaped by private banking, international organizations, and multinational brand operations. CRM programs in this region often need to support both French and English communications, which increases review requirements and broadens service scope. The compliance burden can also be heavier because multinational clients may align Swiss customer programs with broader European operating standards simultaneously. Demand becomes even more complex near bilingual canton boundaries, where campaign templates, consent flows, and reporting views often need to work across multiple language contexts.

The Italian-speaking Ticino remains the smallest linguistic region, accounting for 8% of the national population, yet it holds a distinct place in the Switzerland CRM Marketing Services Market because of its proximity to Lombardy and its wider Italian commercial links. Companies based in Ticino often need CRM programs that support cross-border customer relationships, which raises the value of providers with both localization depth and regulatory awareness. This regional structure creates opportunities for firms to serve all 3 major language markets with native campaign execution rather than translated templates. That white-space remains important because competitors focused mainly on German-language channels do not fully address the needs of the French-speaking and Italian-speaking customer base.

Competitive Landscape

The Switzerland CRM Marketing Services Market remained moderately concentrated at the enterprise tier, where Salesforce, SAP, Oracle, and Adobe supported large implementation mandates, while the broader mid-market and SME layers stayed fragmented across Swiss-hosted and regional specialists. This structure means global platform strength matters in large accounts, but local credibility still matters in regulated and multilingual projects. Salesforce strengthened its position through Agentforce 360, which reached general availability in October 2025 and expanded AI-native workflow support across CRM, sales, and service functions. The company also extended that strategy in January 2026 by launching the Agentforce Sales app on the ChatGPT platform, which lowered adoption friction by placing CRM intelligence in a tool many users already worked in. These moves showed that competitive advantage in the Switzerland CRM Marketing Services Market is shifting toward platform ecosystems that combine automation, agentic workflows, and easier daily access.

Adobe also reinforced its competitive position in 2026 by rebranding Experience Cloud as CX Enterprise and expanding agency and technology partnerships around agentic customer experience orchestration. SAP deepened its offering in April 2026 through its partnership with Google Cloud, bringing multi-agent AI to SAP Customer Experience and SAP Engagement Cloud, with broader customer availability planned for the second half of 2026. These strategic moves show that leading vendors are competing less on core workflow coverage and more on how well AI, orchestration, and governance are built into the platform itself. The Switzerland CRM Marketing Services Market is therefore rewarding providers that can combine technical scale with simpler deployment paths for complex customer programs.

At the same time, Swiss-native and Swiss-aligned providers still hold meaningful competitive ground where data residency and sector trust matter most. BSI Software demonstrated this with customer wins such as Valiant Bank AG and Raiffeisen Switzerland, where Swiss-territory storage and unified customer views were central to the buying decision. This indicates that the Switzerland CRM Marketing Services Market does not operate as a simple local extension of global CRM competition. Providers that combine AI capability, multilingual execution, and credible Swiss compliance positioning still have room to win share, especially in regulated mid-market accounts and service-heavy personalization programs.

Switzerland CRM Marketing Services Industry Leaders

Salesforce, Inc.

SAP SE

HubSpot, Inc.

Adobe Inc.

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Adobe confirmed general availability of its CX Enterprise skills and MCP servers within Anthropic's Claude Enterprise and Microsoft 365 Copilot, alongside co-developed agentic experience orchestration frameworks with Accenture Song, Omnicom, Stagwell's Code and Theory, and WPP. These integrations embed Adobe CX Enterprise directly into the most widely deployed enterprise AI infrastructure, materially expanding the addressable deployment footprint for Adobe's CRM marketing capabilities, including in Switzerland's multinational enterprise sector.

- April 2026: Adobe completed its acquisition of Semrush Holdings, strengthening CX Enterprise with brand visibility and AI-discoverability capabilities at a time when AI-interface-mediated customer discovery is reshaping top-of-funnel CRM marketing strategy. The combination positions Adobe to offer Swiss enterprise buyers a unified platform spanning content creation, campaign orchestration, and search visibility management under a single contract.

- April 2026: SAP SE and Google Cloud expanded their partnership to deploy multi-agent AI within the SAP Customer Experience and SAP Engagement Cloud solutions, enabling joint customers to execute complex marketing strategies powered by unified data across both ecosystems. The capability targets marketing use cases and is planned for general customer availability in the second half of 2026, with multi-agent orchestration designed to extend across the broader SAP CX portfolio.

- April 2026: Braze delivered a new suite of agentic AI capabilities, including an enhanced BrazeAI Decisioning Studio and AI Agent Console, designed to automate the full customer engagement lifecycle from audience targeting through conversion and long-term loyalty. These releases position Braze as a platform capable of competing for enterprise CRM marketing mandates previously dominated by Salesforce and Adobe, particularly among mid-market Swiss buyers.

Switzerland CRM Marketing Services Market Report Scope

The Switzerland CRM Marketing Services Market Report is Segmented by Service Type (CRM Strategy and Consulting, CRM Implementation and Integration, CRM Migration and Modernization, CRM Managed Services, and CRM Training and Support), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Service Application (Customer Acquisition, Customer Retention and Loyalty, Campaign Management Services, Marketing Automation Services, Customer Analytics and Insights, Omnichannel Customer Engagement, and Personalization Services), and End-user Industry (Banking, Financial Services, and Insurance (BFSI), Healthcare and Life Sciences, Information Technology and Telecom, Retail and E-commerce, Industrial Manufacturing, Government and Public Administration, and Other End-user Industries). The Market Forecasts are Provided in Terms of Value (USD).

The Switzerland CRM Marketing Services Market encompasses the range of professional, managed, and support services provided to organizations in Switzerland to help them strategize, implement, optimize, and maintain CRM systems specifically for marketing functions. This market excludes the actual CRM software licenses or platform subscriptions (SaaS/on-premise), focusing entirely on the human expertise, consulting, and outsourced operations required to leverage these technologies effectively.

| CRM Strategy and Consulting |

| CRM Implementation and Integration |

| CRM Migration and Modernization |

| CRM Managed Services |

| CRM Training and Support |

| Large Enterprises |

| Small and Medium Enterprises |

| Customer Acquisition |

| Customer Retention and Loyalty |

| Campaign Management Services |

| Marketing Automation Services |

| Customer Analytics and Insights |

| Omnichannel Customer Engagement |

| Personalization Services |

| Banking, Financial Services, and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Information Technology and Telecom |

| Retail and E-commerce |

| Industrial Manufacturing |

| Government and Public Administration |

| Other End-user Industries |

| By Service Type | CRM Strategy and Consulting |

| CRM Implementation and Integration | |

| CRM Migration and Modernization | |

| CRM Managed Services | |

| CRM Training and Support | |

| By Enterprise Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Service Application | Customer Acquisition |

| Customer Retention and Loyalty | |

| Campaign Management Services | |

| Marketing Automation Services | |

| Customer Analytics and Insights | |

| Omnichannel Customer Engagement | |

| Personalization Services | |

| By End-user Industry | Banking, Financial Services, and Insurance (BFSI) |

| Healthcare and Life Sciences | |

| Information Technology and Telecom | |

| Retail and E-commerce | |

| Industrial Manufacturing | |

| Government and Public Administration | |

| Other End-user Industries |

Key Questions Answered in the Report

What is the current and forecast size of the Switzerland CRM marketing services space?

The Switzerland CRM Marketing Services Market was valued at USD 280.12 million in 2025, is estimated at USD 290.94 million in 2026, and is projected to reach USD 420.19 million by 2031 at a 7.69% CAGR.

Which service type is growing the fastest in Switzerland?

CRM Managed Services is the fastest-growing service type, with a projected CAGR of 9.81% from 2026 to 2031, driven by talent shortages and the need for ongoing optimization and compliance support.

Which enterprise group drives the most demand?

Large enterprises led demand in 2025 with a 64.81% share because they run more complex, multi-language, and compliance-heavy CRM programs.

Why is personalization gaining so much importance in Switzerland?

Personalization Services is projected to grow at a 9.68% CAGR because Swiss companies are moving beyond basic automation and using better first-party data and AI tools for more targeted engagement.

Which end-user sector contributes the most revenue?

BFSI held the largest end-user share at 26.74% in 2025, supported by Switzerland’s financial services base and the need for audit-ready customer communication systems.

What is creating the biggest challenge for market expansion?

Data privacy complexity and the shortage of CRM and MarTech talent are the main constraints because they extend implementation timelines and increase reliance on external service partners.

Page last updated on: