Surgical Procedures Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

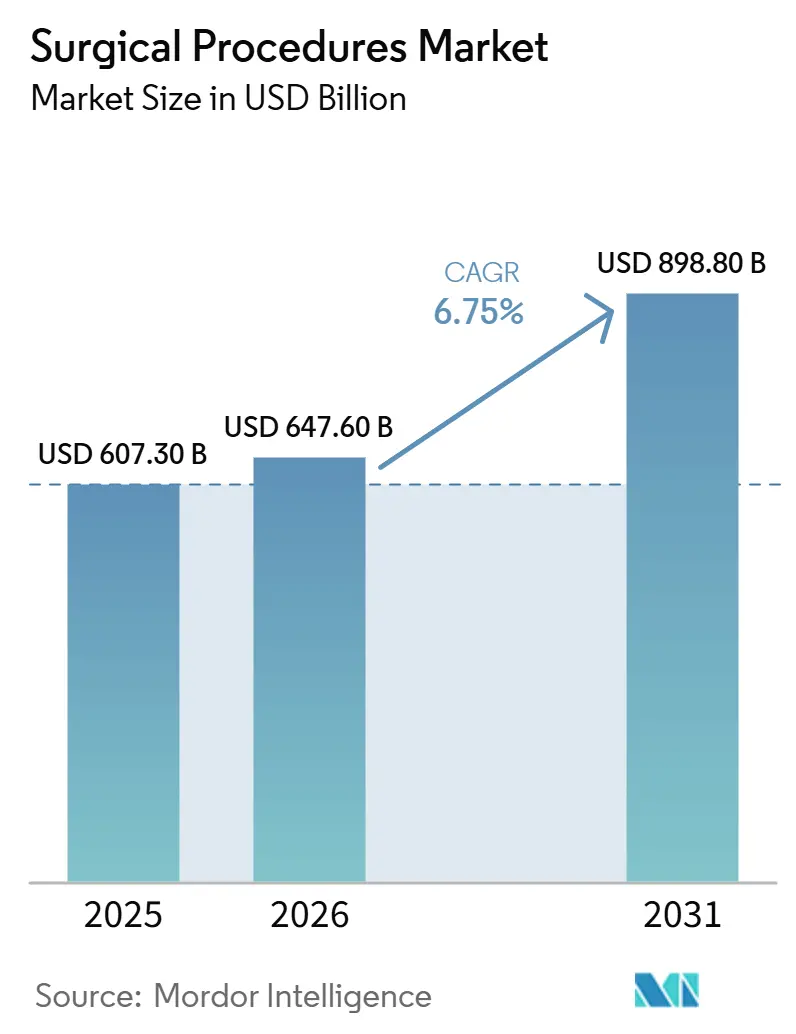

| Market Size (2026) | USD 647.60 Billion |

| Market Size (2031) | USD 898.80 Billion |

| Growth Rate (2026 - 2031) | 6.75% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Surgical Procedures Market Analysis by Mordor Intelligence

The Surgical Procedures Market size is expected to increase from USD 607.30 billion in 2025 to USD 647.60 billion in 2026 and reach USD 898.80 billion by 2031, growing at a CAGR of 6.75% over 2026-2031.

The surgical procedures market is being supported by a steady rise in chronic disease cases, especially in cardiovascular, metabolic, and orthopedic care, where one diagnosis often leads to more than one intervention over time. The surgical procedures market is also shifting toward outpatient delivery, as regulatory support and payer incentives continue to move eligible procedures away from inpatient hospitals and into ambulatory settings. Robotic and minimally invasive platforms are widening procedure access, while also helping providers manage throughput, recovery times, and operating room use more efficiently across the surgical procedures market. Aging populations are adding another layer of demand because older patients now undergo more primary procedures, more revisions, and more repeat interventions than before. Competitive activity in the surgical procedures market remains high because device makers, hospital operators, and enabling technology companies are all trying to secure a stronger place in procedure growth, even as workforce pressure and operating room bottlenecks still limit available capacity.

Key Report Takeaways

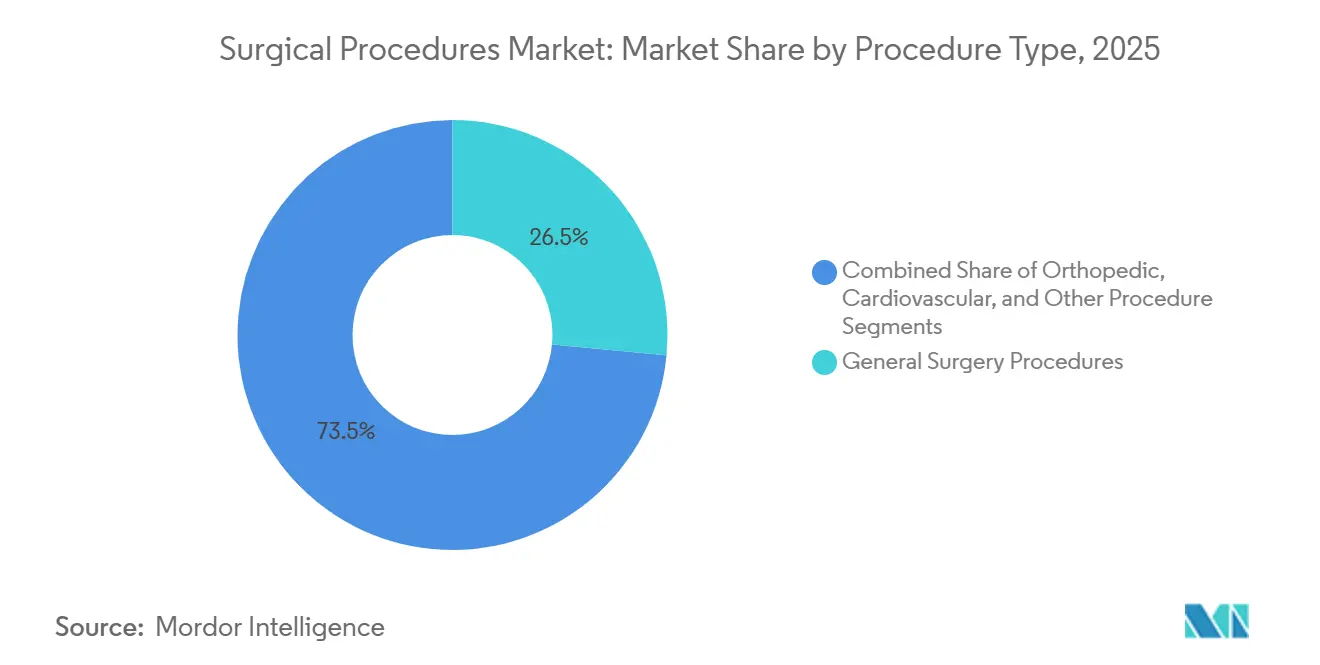

- By procedure type, general surgery held 26.51% of revenue in 2025, while orthopedic procedures are projected to grow at a 7.36% CAGR through 2031.

- By surgical setting, hospitals held 67.73% of the surgical procedures market share in 2025, while ambulatory surgical centers are projected to expand at a 7.53% CAGR through 2031.

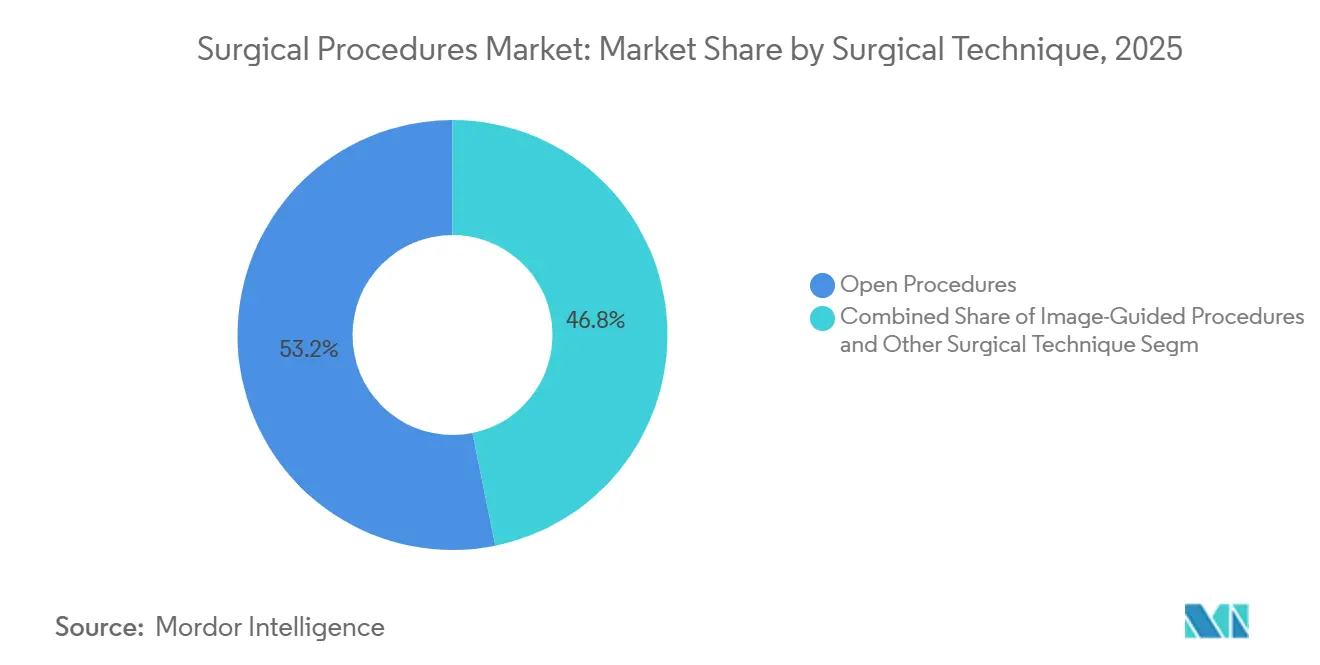

- By surgical technique, open procedures accounted for 53.19% of the Surgical procedures market size in 2025, while robotic-assisted procedures are forecast to grow at a 12.16% CAGR through 2031.

- By patient segment, adult patients accounted for 61.28% of the Surgical procedures market share in 2025, while geriatric patients are projected to grow at a 7.45% CAGR through 2031.

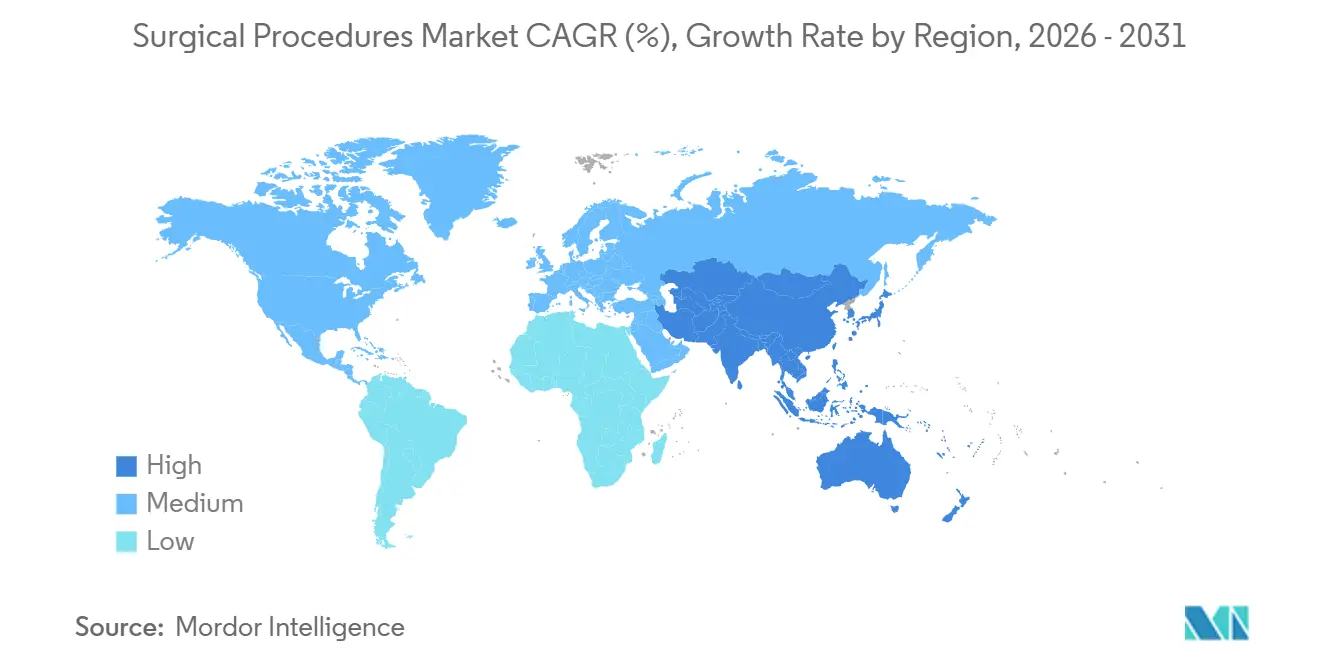

- By geography, North America held 41.38% of the Surgical procedures market size in 2025, while Asia-Pacific is forecast to expand at a 7.87% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Surgical Procedures Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Chronic Disease Burden | +1.8% | Global, concentrated in North America, Europe, and high-density APAC markets including China and India | Long term (≥ 4 years) |

| Shift to Ambulatory Surgery Settings | +1.0% | North America, Western Europe, and emerging APAC | Medium term (2-4 years) |

| Expansion of Minimally Invasive and Robotic Surgery | +1.3% | Global, with highest impact in North America, Germany, Japan, and South Korea | Long term (≥ 4 years) |

| Aging Population Raising Backlog and Re-treatment Rates | +1.0% | Global, highest in Japan, Western Europe, and North America | Long term (≥ 4 years) |

| Payer Pressure on Procedure Mix and Outcomes Documentation | +0.2% | North America and Western Europe | Medium term (2-4 years) |

| Growth of Specialty Hospitals and Dedicated Surgical Centers | +0.4% | North America, GCC, and India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Chronic Disease Burden Driving the Number of Surgeries

Cardiovascular disease remains one of the strongest demand anchors for the surgical procedures market because it continues to generate a large flow of interventional and surgical cases across health systems. The surgical procedures market is also being lifted by metabolic conditions, because rising type 2 diabetes and morbid obesity are increasing the need for bariatric, orthopedic, and cardiovascular procedures within the same patient journey. This pattern matters because one patient often moves through several specialties, which raises total procedure use beyond what isolated disease counts suggest. The Society of Thoracic Surgeons stated in its 2026 update that the Adult Cardiac Surgery Database tracks more than 8.6 million cardiac surgeries in the United States, which shows the depth and persistence of this procedure base.[1]The Society of Thoracic Surgeons Adult Cardiac Surgery Database: 2026 Update on Outcomes and Research Better chronic disease documentation also makes repeat procedures more visible, which strengthens the measured outlook for the surgical procedures market over time.

Shift From Inpatient to Ambulatory Surgery Settings

The move from inpatient hospitals to ambulatory surgical centers has become a structural growth driver for the surgical procedures market because regulation is now actively supporting that change. CMS added 573 codes to the ASC Covered Procedures List in its 2026 final rule, including cardiac ablation, lumbar spinal fusion, and musculoskeletal procedures that had been more tightly limited before, and it projected total ASC Medicare payments of USD 9.2 billion in 2026. The surgical procedures market is therefore seeing a realignment in the site of care, not just a rebound in postponed cases. Higher-acuity specialties are increasingly part of this shift, which makes outpatient growth more meaningful for revenue and capacity than older low-complexity migration trends. This change also creates a gap between well-served urban markets and underserved lower-density areas, where the outpatient network is still less developed.

Expansion of Minimally Invasive and Robotic-Assisted Surgical Procedures

The surgical procedures market is being reshaped by robotic and minimally invasive techniques because these formats support shorter stays, faster recovery, and broader outpatient suitability. Intuitive Surgical reported nearly 3.15 million worldwide da Vinci and Ion procedures in 2025, up 18% from 2024, and its first quarter 2026 results showed procedure growth of 16% year over year with an installed base of over 13,900 systems. A 2025 study published in ACOS Open found that hospitals introducing robotic-assisted surgery in common general surgery operations increased their minimally invasive surgery rate from 60.5% to 65.8%, while non-adopter hospitals rose only from 56.1% to 57.0%.[2]Rates of Minimally Invasive Surgery After Introduction of Robotic-Assisted Surgery for Common General Surgery Operations That result shows robotics can lift broader minimally invasive use inside a hospital rather than remain a narrow premium tool. Germany also expanded the outpatient reimbursement pathway for these procedures, as the Hybrid-DRG 2026 framework and the OPS 2026 catalog widened the list of ambulatory procedure codes to include more laparoscopic and arthroscopic interventions. As these systems spread, the surgical procedures market is gaining more capacity in procedure categories that fit shorter and more standardized care paths.

Aging Population Increasing Procedure Backlog and Re-treatment Rates

An aging population is adding both more volume and more complexity to the surgical procedures market because older patients now receive a wider range of procedures than earlier practice patterns allowed. Orthopedic procedures are central to this shift, with hip and knee replacement, fracture repair, and revision surgery all rising as older age groups live longer with mobility-related disease burdens. The surgical procedures market is also seeing more re-treatment because implant failures, periprosthetic fractures, and revision procedures add new demand on top of primary surgeries. Geriatric patients are the fastest-growing patient group, which confirms that age-related demand is growing faster than the overall volume of surgical procedures. A 2025 review in Perioperative Medicine found that comprehensive geriatric assessment influenced orthopedic treatment decisions in 25.3% of reviewed cases, which shows that pre-operative readiness is now a major throughput issue in older populations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Workforce Shortages in Anesthesia, OR Nursing, and Surgical Support | -0.9% | North America, Europe, and APAC emerging markets | Long term (≥ 4 years) |

| Operating Room Capacity Constraints and Scheduling Inefficiencies | -0.7% | Global, most acute in NHS England, Canada, and rural United States markets | Medium term (2-4 years) |

| Procedure Deferral from Prior Authorization and Benefit Design Friction | -0.5% | Primarily North America, especially the United States commercial payer market | Medium term (2-4 years) |

| Coding Variability Reducing Cross-Hospital Comparability of Volume Data | -0.2% | Global, most significant in multi-payer systems | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Workforce Shortages in Anesthesia, OR Nursing, and Surgical Support

Workforce shortages remain a clear restraint on the volume of surgical procedures because procedure demand does not automatically convert into completed cases when staffing is thin. Anesthesia coverage is especially important because it directly controls how many operating rooms can run at full schedule on a given day. The surgical procedures market also faces pressure from perioperative nursing shortages, which affect case preparation, turnover time, and post-operative monitoring. These shortages do more than slow growth because they also push facilities to favor shorter and higher-margin procedures over longer elective cases. That shift can alter observed procedure mix even when the underlying demand remains strong. The result is that the surgical procedures market continues to expand, but available labor still limits how much demand can be served on schedule.

Operating Room Capacity Constraints and Scheduling Inefficiencies

Operating room capacity is another restraint on the surgical procedures market because physical room time, setup time, and scheduling discipline still limit daily throughput. NHS England reported in April 2026 that incomplete referral-to-treatment pathways declined 2.3% from April 2025, which shows progress but also confirms that backlog clearance is still gradual.[4]Statistical Press Notice NHS referral to treatment (RTT) waiting times data April 2026 OECD data published in 2025 showed that 52% of patients across 10 surveyed countries waited 1 month or longer to see a specialist, with Canada and the United Kingdom facing some of the longest delays. The surgical procedures market is therefore constrained by process quality as much as by demand strength. Poor block utilization can leave prime operating room time underused, even while elective waitlists remain long. Robotic adoption can also slow throughput during early rollout because setup and scheduling become more complex before the efficiency gains are fully realized.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Procedure Type: General Surgery Holds the Broadest Base While Orthopedics Expands the Fastest

General surgery procedures accounted for 26.51% of the Surgical procedures market size in 2025, which made them the largest procedure category in the surgical procedures market. This position reflects the wide spread of laparoscopic cholecystectomy, appendectomy, hernia repair, and bariatric procedures across age groups and care settings. General surgery benefits from strong suitability for minimally invasive techniques, which supports volume across both hospitals and ambulatory centers. That breadth makes it the most stable anchor within the surgical procedures market when other specialties move more sharply with reimbursement or technology cycles.

Cardiovascular procedures also remain highly consequential because coronary artery disease continues to generate a large flow of interventional cases. Neurosurgery and ophthalmic procedures form smaller but durable pools that are sustained by spinal disorders, cataracts, and glaucoma in aging populations. Gynecological, obstetric, and ENT procedures keep a recurring volume base because their demand is tied to continuing clinical needs rather than long-cycle chronic disease accumulation. Orthopedic procedures are the fastest-growing category at a 7.36% CAGR through 2031, which reflects the combined effect of aging, obesity-related joint degeneration, and wider acceptance of technology-supported arthroplasty in the surgical procedures market.

By Surgical Setting: Hospitals Stay Dominant While ASCs Continue to Gain Ground

Hospitals held 67.73% of the surgical setting share in 2025, which kept them at the center of the surgical procedures market because they still manage the most complex and acute procedures. Their role remains secure in trauma, multi-specialty surgery, intensive post-operative care, and emergency intervention where outpatient facilities cannot match the same level of support. Hospitals also continue to handle cases that require longer monitoring or greater clinical coordination across specialties. This means the surgical procedures market is not shifting away from hospitals entirely, but is redistributing eligible procedures across a wider care network.

Clinics remain the smallest formal setting because they mainly perform minor ophthalmic, dermatologic, and gastroenterologic procedures where local rules allow limited intervention capacity. Ambulatory surgical centers are the fastest-growing setting at a 7.53% CAGR through 2031, which shows that the surgical procedures market is steadily moving more routine and selected higher-acuity cases into outpatient channels. CMS supported this trend in the 2026 final payment rule by expanding the ASC Covered Procedures List and beginning the phased elimination of the Inpatient-Only list for selected musculoskeletal procedures. That policy change matters because it improves the economic case for outpatient care in orthopedic and cardiac categories, which are more valuable growth areas than low-complexity procedures. As this pattern continues, the surgical procedures market is likely to see stronger competition around ownership of outpatient capacity and referral pathways.

By Surgical Technique: Open Surgery Leads Today While Robotic-Assisted Techniques Set the Growth Pace

Open procedures retained 53.19% share in 2025, which kept them as the largest technique category in the surgical procedures market. This reflects the large number of cases in health systems where laparoscopic infrastructure is still limited, especially for complex cancer surgery, trauma, revision arthroplasty, and selected cardiovascular procedures. Open surgery also remains clinically necessary in cases where anatomy, urgency, or disease extent limits the value of a less invasive option. Even so, the share of open procedures is under steady pressure as minimally invasive alternatives expand across more indications in the surgical procedures market.

Laparoscopic surgery occupies the broad middle ground because it is already well established, clinically accepted, and still growing in many emerging settings. Image-guided procedures are also becoming more important because fluoroscopy, CT, MRI, and ultrasound are helping surgeons navigate complex interventions with greater precision across orthopedics, neurosurgery, and interventional cardiology. Robotic-assisted procedures are projected to grow at a 12.16% CAGR through 2031, which makes them the fastest-growing technique in the surgical procedures market. Intuitive Surgical also reported that procedure growth stayed strong in early 2026, while hospitals adopting robotic-assisted surgery showed a much faster rise in minimally invasive rates than non-adopters. That combination suggests that robotics is increasingly influencing institutional care models, not just isolated case selection.

By Patient Segment: Adults Provide the Largest Base While Geriatric Patients Add the Fastest Growth

Adult patients accounted for 61.28% of the surgical procedures market in 2025, which made them the core demand base for the surgical procedures market. This group covers the broadest spread of procedures, including general surgery, reproductive health, orthopedic repair, and cancer-related operations. Adults also benefit from wider insurance coverage and lower average comorbidity burden per case than older age groups, which helps maintain strong throughput in both inpatient and outpatient settings. Pediatric patients remain the smallest segment because they require dedicated facilities, pediatric-specific devices, and specialized anesthesia protocols that limit scale advantages.

Geriatric patients are projected to grow at a 7.45% CAGR through 2031, which makes them the fastest-expanding patient group in the surgical procedures market. This growth reflects stronger clinical acceptance of surgery for hip fractures, cataracts, spinal stenosis, and cardiac valve disease in older adults. A 2025 study on total knee arthroplasty in patients aged 70 years and older found patient-reported outcomes comparable to younger cohorts, which supports the broader willingness to operate on older patients when functional benefit is expected.[5]How Old is Too Old? Outcomes of Primary Total Knee Arthroplasty in Patients 70 Years or Older Older patients also generate more downstream demand because revision surgery, implant management, and repeat treatment often follow the initial intervention. That dynamic means the surgical procedures market gains not only more cases from aging, but also a denser and more resource-intensive pattern of care.

Geography Analysis

North America held 41.38% of the global surgical procedures market share in 2025, which made it the largest regional contributor to the surgical procedures market. The region benefits from a mature hospital system, a large commercial payer base, and the deepest installed base of robotic surgical systems. The United States continues to shape the regional outlook because reimbursement reform is widening the procedure set that can move into ambulatory settings. Prior authorization still acts as a capacity drag, and an AAOS-linked 2025 study found that total hip arthroplasty patients waited 38.7 days with prior authorization compared with 4 days without it. A 2026 study in The Spine Journal also found that prior authorization requirements created an average 14-day delay in more than 67% of elective spine surgery cases.

Europe remains a structurally important region for the surgical procedures market because Germany, the United Kingdom, France, Italy, and Spain form its core volume base. Germany also expanded its outpatient pathway through Hybrid-DRG 2026 and OPS 2026, which added more ambulatory eligibility for laparoscopic and arthroscopic procedures. In the United Kingdom, NHS England reported in April 2026 that incomplete pathways declined 2.3% from the prior year, which shows backlog improvement but not full normalization.

Asia-Pacific is the fastest-growing region in the surgical procedures market at a 7.87% CAGR through 2031. China and India are central to this growth because chronic disease loads are rising while hospital infrastructure continues to deepen. Japan also remains important in advanced surgery adoption, and Osaka Police Hospital performed the country’s first da Vinci 5 surgery in July 2025 with a target of more than 1,000 robotic procedures annually from that facility.

Competitive Landscape

The Surgical Procedures Market features strong competition among large integrated hospital systems, academic medical centers, and ambulatory surgery operators. These providers differentiate themselves through specialty expertise, surgical volumes, geographic reach, care coordination capabilities, and investments in advanced surgical technologies. HCA Healthcare operates one of the largest surgical care networks globally, delivering high volumes of general, orthopedic, cardiovascular, neurosurgical, bariatric, and robotic-assisted procedures across its hospitals and ambulatory surgery centers. Its broad care delivery infrastructure enables it to serve diverse patient populations while supporting standardized clinical protocols, surgeon recruitment, and investments in operating room efficiency.

SCA Health and Surgery Partners have strengthened their competitive positions by expanding outpatient surgical services and specializing in orthopedic, ophthalmic, gastrointestinal, pain management, and minimally invasive surgeries. Their growth reflects the continued shift toward ambulatory surgical care, as payers, providers, and patients increasingly favor lower-cost settings, shorter recovery times, and improved procedural convenience for eligible cases. These operators compete by building partnerships with physicians, expanding ambulatory surgery center footprints, improving scheduling and throughput, and adopting technologies that support safe and efficient outpatient procedures.

Among academic and tertiary referral centers, Mayo Clinic and Cleveland Clinic remain global leaders in cardiovascular surgery, organ transplantation, neurosurgery, oncology surgery, and complex minimally invasive procedures. Continuous investments in robotic surgery, AI-enabled surgical planning, precision medicine, clinical research, and multidisciplinary care models support their leadership positions. In the Asia-Pacific region, Apollo Hospitals Enterprise has emerged as a major provider of cardiac surgery, oncology surgery, orthopedic procedures, transplant surgery, and robotic-assisted interventions. In Europe, Helios Hospital Group has strengthened its position through its extensive hospital network, offering comprehensive general surgery, trauma surgery, vascular surgery, spine surgery, and specialized cancer surgeries. Collectively, these providers compete by expanding specialty surgical programs, enhancing digital operating room capabilities, improving patient outcomes, and scaling advanced surgical technologies across hospital and outpatient settings.

Surgical Procedures Industry Leaders

Cleveland Cinic

Mayo Clinic

Johns Hopkins Hospital

Singapore General Hospital

Helios Hospital Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Surrey Memorial Hospital completed its first robotic-assisted surgery using the da Vinci Xi system, marking the start of a regional robotics program that will expand access to minimally invasive thoracic and ENT procedures.

- June 2025: UC Davis Health opened the 48X Complex, a USD 589 million, 268,000-square-foot outpatient surgery center with 14 operating rooms and 59 recovery bays, underscoring the growth of large same-day surgery campuses.

- June 2025: Ascension agreed to acquire AmSurg, adding more than 250 ASCs across 34 states, which materially expands outpatient surgical capacity and supports the shift from inpatient to outpatient care.

- February 2025: Tenet Healthcare continued to scale USPI, targeting about USD 250 million of annual ambulatory M&A and planning 10 to 12 new de novo centers, reinforcing the ongoing migration of surgical volume into freestanding outpatient settings.

Global Surgical Procedures Market Report Scope

The surgical procedures market represents the global revenue generated from surgical procedures performed across hospitals, ambulatory surgical centers, specialty clinics, and other healthcare settings. It reflects the economic value of surgical care delivery, including professional fees, facility charges, anesthesia services, operating room utilization, post-procedure recovery services, and other procedure-related healthcare services.

The surgical procedures market is segmented by procedure type, surgical setting, surgical technique, patient segment, and geography. By procedure type, it is further divided into general surgery procedures, orthopedic procedures, cardiovascular procedures, neurosurgery procedures, gynecological and obstetric procedures, ophthalmic procedures, and others. By surgical setting, it is segmented into hospitals, ambulatory surgical centers, clinics, and others. By surgical technique, the market is segmented into open procedures, minimally invasive laparoscopic procedures, robotic-assisted procedures, and image-guided procedures. By patient segment, the market is segmented into adult patients, pediatric patients, and geriatric patients. The geography segment is further divided into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market size and forecasts in value (USD) for the above segments.

| Orthopedic Procedures |

| Cardiovascular Procedures |

| Neurosurgery Procedures |

| Gynecological and Obstetric Procedures |

| Ophthalmic Procedures |

| Others (ENT and Urology Procedures, among others |

| Hospitals |

| Ambulatory Surgical Centers |

| Clinics |

| Others (Academic & Research Institutes and Specialty Surgical Centers, among others) |

| Open Procedures |

| Minimally Invasive Laparoscopic Procedures |

| Robotic-Assisted Procedures |

| Image-Guided Procedures |

| Adult Patients |

| Pediatric Patients |

| Geriatric Patients |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| General Surgery Procedures | Orthopedic Procedures | |

| Cardiovascular Procedures | ||

| Neurosurgery Procedures | ||

| Gynecological and Obstetric Procedures | ||

| Ophthalmic Procedures | ||

| Others (ENT and Urology Procedures, among others | ||

| By Surgical Setting | Hospitals | |

| Ambulatory Surgical Centers | ||

| Clinics | ||

| Others (Academic & Research Institutes and Specialty Surgical Centers, among others) | ||

| By Surgical Technique | Open Procedures | |

| Minimally Invasive Laparoscopic Procedures | ||

| Robotic-Assisted Procedures | ||

| Image-Guided Procedures | ||

| By Patient Segment | Adult Patients | |

| Pediatric Patients | ||

| Geriatric Patients | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of surgical procedures volume by 2031?

The Surgical Procedures Market is forecast to reach USD 898.76 billion by 2031, up from USD 647.61 billion in 2026, with a 6.75% CAGR over 2026 to 2031.

Which procedure category leads current volume?

General surgery led with a 26.51% share in 2025 because it spans many high-incidence procedures across different care settings and age groups.

Which surgical technique is growing the fastest?

Robotic-assisted procedures are expected to grow at a 12.16% CAGR through 2031, making them the fastest-growing technique segment.

Why are ambulatory surgical centers gaining importance?

ASCs are growing because reimbursement policy is shifting more procedures into outpatient care, and CMS expanded the eligible ASC procedure list for 2026.

Which patient group is changing demand the most?

Geriatric patients are projected to grow at a 7.45% CAGR through 2031 because older adults are receiving more orthopedic, cardiac, ophthalmic, and revision procedures.

Which region offers the strongest growth outlook?

Asia-Pacific is expected to grow the fastest at a 7.87% CAGR through 2031, supported by rising chronic disease burden and ongoing hospital infrastructure expansion.

Page last updated on: