Surgical Drainage Devices Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

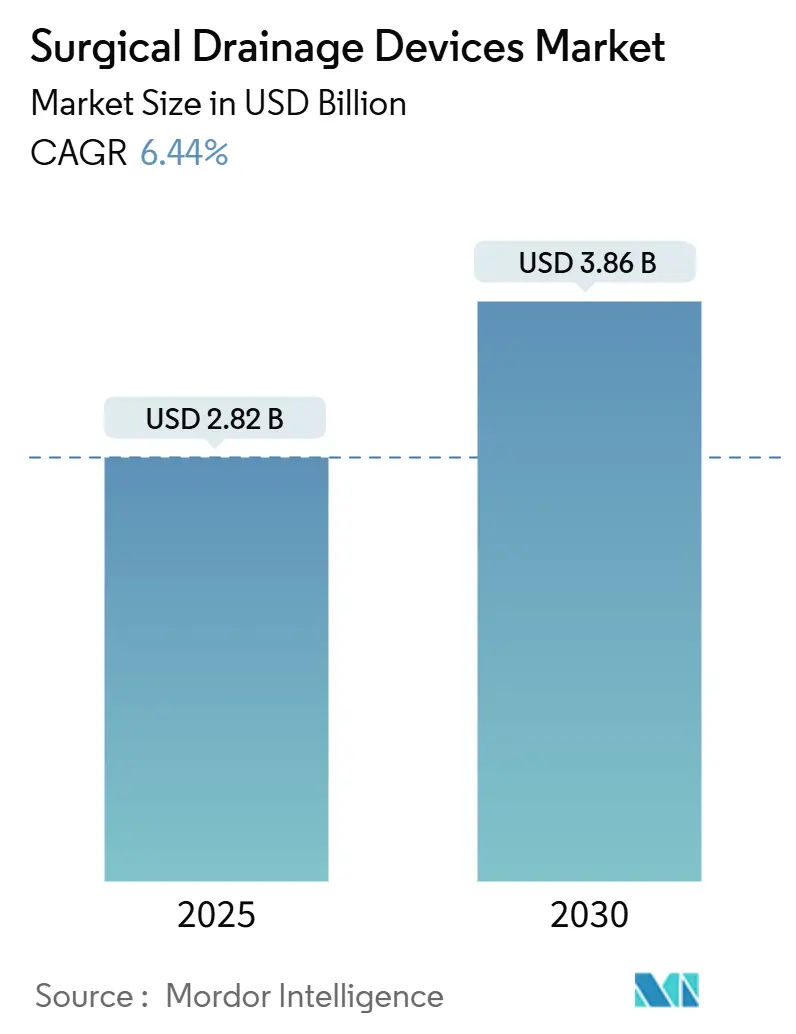

| Market Size (2025) | USD 2.82 Billion |

| Market Size (2030) | USD 3.86 Billion |

| Growth Rate (2025 - 2030) | 6.44% CAGR |

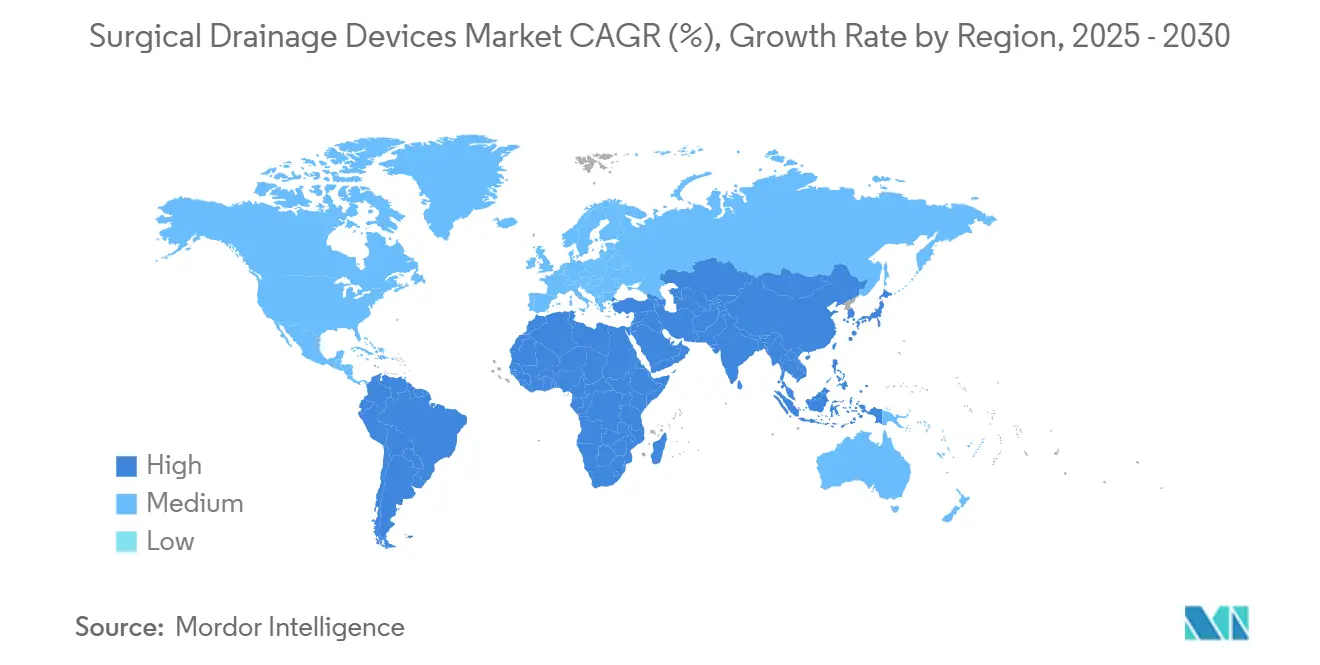

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Surgical Drainage Devices Market Analysis by Mordor Intelligence

The Surgical Drainage Devices Market size is estimated at USD 2.82 billion in 2025, and is expected to reach USD 3.86 billion by 2030, at a CAGR of 6.44% during the forecast period (2025-2030).

Growing case complexity, rapid digital adoption, and patient‐centric care protocols are shaping demand patterns. Hospitals invest in drainage systems that link seamlessly with electronic health records, while ambulatory sites seek devices that support same-day discharge. Advanced infection-control requirements push manufacturers toward antimicrobial materials and closed-system designs. Simultaneously, Asia-Pacific procedure volumes surge as governments channel capital toward new surgical centers, attracting global suppliers and stimulating local production.

Key Report Takeaways

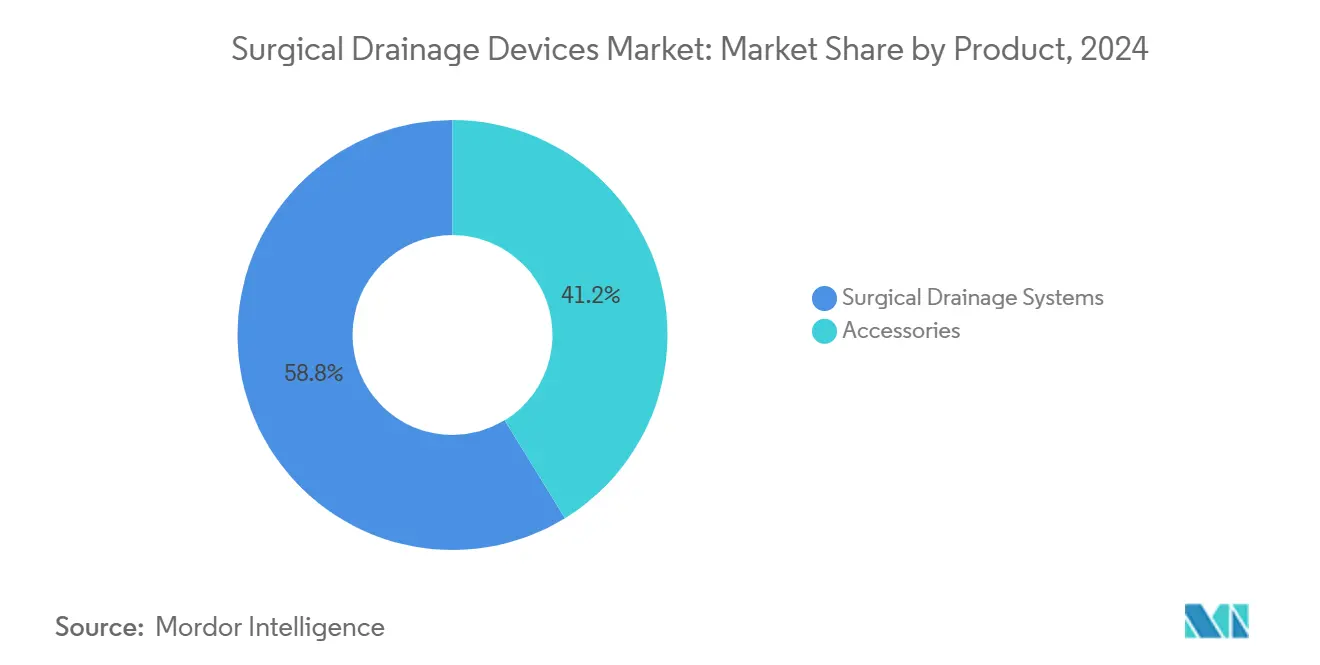

- By product, surgical drainage systems led with 58.76% revenue share in 2024; accessories are forecast to post a 9.24% CAGR through 2030.

- By type, active drains held 59.45% of surgical drains market share in 2024, while passive drains lag yet remain cost-efficient.

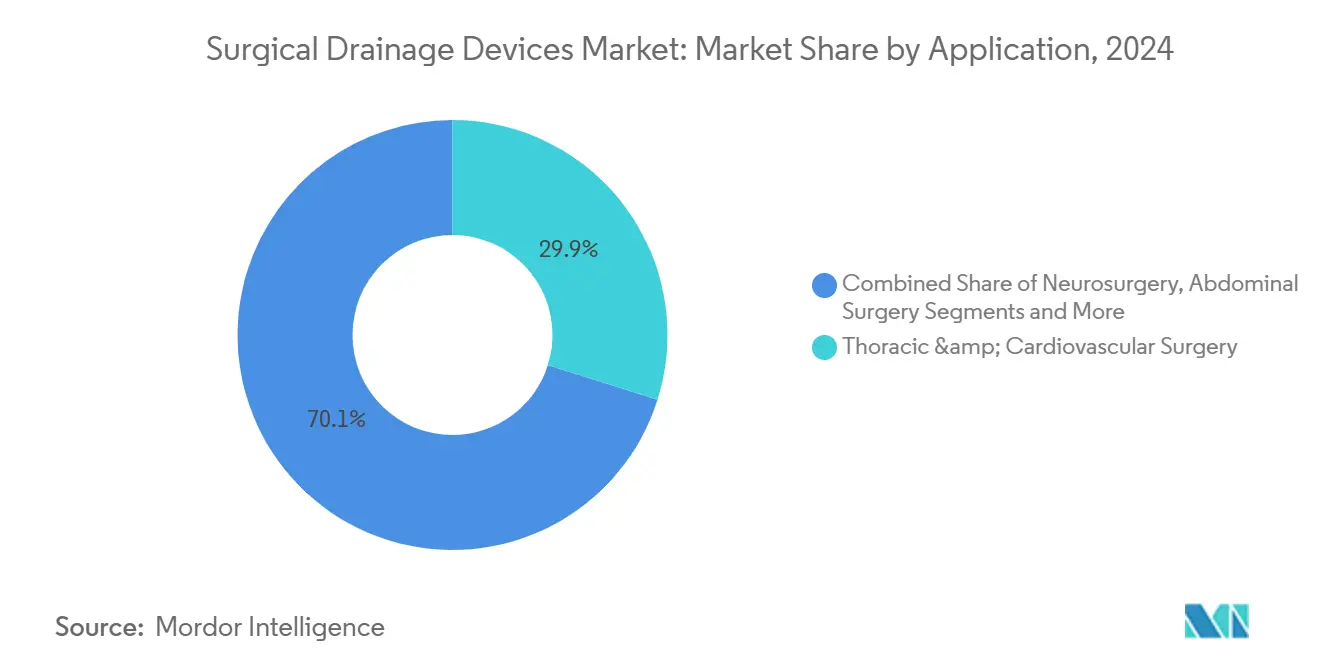

- By application, thoracic and cardiovascular surgery commanded 29.87% share of the surgical drains market size in 2024; orthopedics is projected to grow at 7.56% CAGR to 2030.

- By end user, hospitals accounted for 71.71% of the surgical drainage market size in 2024; ambulatory surgical centers record the highest CAGR at 6.89% through 2030.

- By geography, North America captured 36.71% revenue in 2024, with Asia-Pacific advancing at an 8.19% CAGR through 2030.

Global Surgical Drainage Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing volume of complex surgeries | +1.2% | Global, concentrated in North America & Asia-Pacific | Medium term (2-4 years) |

| Rapid adoption of digital / smart drainage systems | +0.9% | North America & EU leading, Asia-Pacific following | Short term (≤ 2 years) |

| Higher infection-control standards in ambulatory settings | +0.7% | Global, strongest in developed markets | Long term (≥ 4 years) |

| Shift toward day-care surgery & ERAS protocols | +0.8% | North America & EU core, expanding to Asia-Pacific | Medium term (2-4 years) |

| Value-based procurement in high-income markets | +0.5% | North America & Western Europe | Long term (≥ 4 years) |

| Local production incentives in select countries | +0.4% | Asia-Pacific core, selective Middle East & Africa markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Volume of Complex Surgeries

Higher case complexity boosts demand for devices that manage multifaceted fluid dynamics. Medicare reported 3.3 million beneficiaries in U.S. ambulatory centers during 2022, underscoring procedure growth that elevates drainage requirements.[1]Medicare Payment Advisory Commission, “Ambulatory Surgical Center Services: Status Report,” medpac.gov Enhanced recovery pathways still rely on drains for cardiovascular, orthopedic, and neurosurgical interventions that involve sizable fluid shifts. Aging populations ensure continued growth in joint replacements, and minimally invasive approaches require slimline drains that accommodate small incisions. These forces sustain premium system sales within the surgical drainage market.

Rapid Adoption of Digital / Smart Drainage Systems

Real-time fluid analytics shorten hospital stays and cut manual checks. Clinical evaluations of digital chest drains confirmed faster tube removal and reduced length of stay.[2]Kazuto Sugai, Tomohiro Yazawa, “Thoracic Drainage Management Strategies in Postoperative Lung Surgery: A Narrative Review,” shc.amegroups.org IoT–enabled devices transmit output metrics to nursing dashboards, easing workloads and enhancing early-warning capability. Hospitals justify upfront costs through downstream efficiency gains. In parallel, ambulatory centers deploy compact smart units that support home recovery and remote oversight.

Higher Infection-Control Standards in Ambulatory Settings

Closed, silicone-based systems with antimicrobial additives address strict surgical site surveillance rules outlined in the 2024 CDC outpatient manual.[3]Centers for Disease Control and Prevention, “2024 NHSN Outpatient Procedure Component Manual,” cdc.govAmbulatory centers, accountable for post-discharge infection tracking, favor drains that limit exposure while patients recuperate offsite. Manufacturers incorporate barrier filters and secure luer locks to mitigate contamination.

Shift Toward Day-Care Surgery & ERAS Protocols

Randomized trials showed ERAS cut total knee arthroplasty stays from 8.17 days to 5.92 days.[4]Di Han, Peng Wang, “Enhanced Recovery After Surgery Improves Outcomes in Elderly Patients Undergoing Short-Level Lumbar Fusion Surgery,” eurjmedres.biomedcentral.com Devices must permit mobility without compromising drainage, prompting lightweight designs and discreet reservoirs. Home-friendly formats, including wearable reservoirs, align with outpatient expansion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adverse events & litigation over retained drains | -0.8% | Global, highest impact in litigious markets | Short term (≤ 2 years) |

| Accelerating pivot to minimally invasive & drain-less techniques | -1.1% | North America & EU leading, global adoption | Medium term (2-4 years) |

| Supply-chain shortages in medical-grade silicone | -0.6% | Global, acute in supply-dependent regions | Short term (≤ 2 years) |

| Hospitals delaying capital expenditure amid reimbursement pressure | -0.9% | North America & EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Adverse Events & Litigation Over Retained Drains

Retained fragments can trigger gait disturbances and long-term disability, as documented after total hip arthroplasty. Institutions facing liability tighten protocols, eliminating drains where evidence shows negligible benefit. This caution directly moderates device volumes, especially in high-litigation regions.

Accelerating Pivot to Minimally-Invasive & Drain-Less Techniques

Meta-analyses reveal peritoneal drainage after laparoscopic appendectomy raises infection risk without improving outcomes. Growing surgeon confidence in drain-free repairs shrinks demand, notably in general and colorectal surgery. Training curricula reinforce these protocols, further curbing market penetration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Systems Drive Innovation Leadership

Surgical drainage systems generated 58.76% of revenue in 2024 and are forecast to outpace accessories with a 9.24% CAGR. Demand centers on connected platforms that log output, pressure, and alarm data inside the hospital information backbone. Such performance underpins premium pricing in the surgical drainage market. Accessories, while steady, feel commoditization as integrated kits bundle tubing, connectors, and dressings.

Replacement frequency sustains accessory revenue, yet growth trails system upgrades. Novel silicone fixation dressings improve comfort and reduce re-taping, hinting at incremental gains. System makers blur category lines by embedding securement features within primary devices, consolidating procurement and simplifying inventory.

By Type: Active Drains Maintain Technology Edge

Active units held 59.45% share in 2024 and should grow 8.23% annually through 2030. Precision suction and flow regulation fit critical thoracic and cardiac cases that demand tight pressure control. The Interi System, for instance, lowered seroma rates from 22.9% to 4.1% in breast reconstruction. Passive drains thrive in price-sensitive settings; however, their limited monitoring restricts adoption in high-acuity wards.

Emerging reimbursement models reward outcome tracking, reinforcing the appeal of active drains that document performance metrics. Passive silicone variants remain indispensable for low-resource environments, helping preserve surgical access where budgets constrain upgrades.

By Application: Orthopedics Emerges as Growth Engine

The orthopedic segment is poised for a 7.56% CAGR, driven by aging populations and standardized joint replacement protocols. Surgeons balance mobility goals with fluid management, favoring slim drains that sit flush against limb contours. Total joint reimbursement challenges have not dented procedure counts, sustaining volume in the surgical drainage market.

Thoracic and cardiovascular surgery preserved the largest 29.87% slice of 2024 revenue. Complex chest operations necessitate high-capacity devices capable of managing blood, serous fluid, and air simultaneously. Neurosurgical and abdominal cases remain niche but technologically intensive, relying on ultrafine catheters for cerebrospinal or peritoneal drainage.

By End User: ASCs Drive Market Transformation

Hospitals commanded 71.71% of 2024 spending but face budget scrutiny that slows upgrades. Integration with existing electronic systems is paramount, prompting multi-year purchasing cycles. Conversely, ambulatory surgical centers posted a 6.89% CAGR forecast, reflecting patient preference for outpatient options and payer incentives for lower-cost sites.

ASC workflows require lightweight reservoirs and quick-release connectors that patients or home nurses can manage confidently. Manufacturers respond with ease-of-use kits and virtual training modules, aligning product functionality with the ambulatory care continuum and expanding reach of the surgical drainage market.

Geography Analysis

North America retained 36.71% of global revenue in 2024 owing to high procedure counts and early digital uptake. Medicare outlays of USD 6.1 billion for ambulatory surgeries in 2022 attest to robust demand for advanced postoperative care devices. Hospitals emphasize outcome documentation, incentivizing connected drains that feed data to quality dashboards. Supply disruptions highlight vendors able to guarantee on-time delivery.

Europe delivers stable gains anchored in aging demographics and stringent infection prevention rules. ERAS adoption reshapes purchasing by valuing devices that enable early mobilization. National health systems in Western Europe weigh total cost of ownership heavily, rewarding suppliers who quantify reductions in length of stay and complication rates.

The Asia-Pacific is a growth hotspot for the surgical drainage market, with an 8.19% CAGR forecast. Governments are funneling capital into new surgical suites and encouraging domestic production through tax incentives. While China’s tender rules favor local brands, quality gaps in advanced smart systems leave space for collaborations with multinational firms. Medical tourism hubs such as Thailand and India also fuel device imports, particularly for complex cardiovascular and oncology procedures.

Competitive Landscape

The market is moderately fragmented, with established brands reinforcing portfolios through sensor integration and biocompatible polymers. Johnson & Johnson MedTech recorded a 6.4% sales lift in 2025 as new drainage and wound care launches penetrated orthopedic and breast reconstruction procedures. Teleflex earmarked USD 430 million of a USD 2.29 billion medtech budget for surgical tools, illustrating the capital intensity needed to remain competitive.

Players differentiate through outcome evidence and supply reliability. Antimicrobial coatings, pressure-regulated pumps, and cloud dashboards comprise the innovation frontier. Regulatory scrutiny of adverse events drives firms to develop tamper-proof connectors and robust tracking software.

Local producers in Asia ride government incentives yet still license sensor modules from Western partners. Meanwhile, multinational suppliers establish regional plants to sidestep tariffs and accelerate delivery. These dynamics foster incremental consolidation as companies seek scale to fund R&D and withstand pricing pressure inside the surgical drainage market.

Surgical Drainage Devices Industry Leaders

B. Braun Melsungen AG

Cardinal Health

Cook Group

Johnson and Johnson Services LLC

ConvaTec

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: PolyPid announced positive Phase 3 results for D-PLEX100 in preventing surgical site infections in abdominal colorectal surgery.

- June 2024: B. Braun Interventional Systems launched ACCEL All-Purpose and Biliary Drainage Catheters with TrueGlide Hydrophilic Coating.

Global Surgical Drainage Devices Market Report Scope

The surgical drainage systems are widely used to drain out air and accumulated fluids, especially blood and pus, which facilitates wound healing. These drainage systems have also become common for healing wounds and reducing the occurrence of infection in abdominal procedures and orthopedic surgeries, notably in joint replacements. The Surgical Drainage Market is segmented By Product (Accessories and Surgical Drainage Systems), By Type (Active Drains and Passive Drains) By Application (Thoracic and Cardiovascular Surgery, Neurosurgery, Abdominal surgery, Orthopedics, and Others) By End User (Hospitals, and Ambulatory Surgical Centers (ASCS) & Clinics) and Geography (North America, Europe, Asia-Pacific, Middle East, and Africa and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD) for the above segments.

| Surgical Drainage Systems | Open Surgical Drainage Systems |

| Closed Surgical Drainage Systems | |

| Accessories |

| Active Drains |

| Passive Drains |

| Thoracic & Cardiovascular Surgery |

| Neurosurgery |

| Abdominal Surgery |

| Orthopedics |

| Others |

| Hospitals |

| Ambulatory Surgical Centers & Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Surgical Drainage Systems | Open Surgical Drainage Systems |

| Closed Surgical Drainage Systems | ||

| Accessories | ||

| By Type | Active Drains | |

| Passive Drains | ||

| By Application | Thoracic & Cardiovascular Surgery | |

| Neurosurgery | ||

| Abdominal Surgery | ||

| Orthopedics | ||

| Others | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers & Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the surgical drainage market?

The market is valued at USD 2.82 billion in 2025 and is projected to reach USD 3.86 billion by 2030.

Which segment is growing fastest within the surgical drainage market?

Orthopedic applications show the highest growth, forecasting a 7.56% CAGR through 2030.

How are digital drainage systems impacting hospitals?

Connected devices shorten hospital stays and reduce nursing rounds by delivering real-time fluid data to electronic records.

Why are ambulatory surgical centers important for future demand?

ASCs support same-day discharge, driving need for portable, patient-friendly drains and fueling a 6.89% CAGR for the segment.

Which region offers the strongest growth opportunity?

Asia-Pacific leads with an 8.19% CAGR, backed by infrastructure investment and supportive local production policies.

Page last updated on: